Families in the Eyes of the Law

Contemporary Challenges and the Grip of the Past

Robert Leckey

Does the way Canada taxes families need changing? Is the current system fair and efficient? What are the options for reform? This study provides answers to these complex questions through a comprehensive analysis of the main issues surrounding taxation and the family. Authors Carole Vincent, research director at IRPP, and Frances Woolley, associate professor of economics at Carleton University, look at the parameters and structure of tax provisions that affect Canadian families and the implicit policy choices involved, and propose options for reform. They argue that, while Canada’s tax system does many things right, significant improvements could be made to ensure more efficient and equitable treatment of all families with children. In their view, the immediate priority for change is the reinstatement of a universal child benefit.

To support their conclusions, Vincent and Woolley provide an in-depth evaluation of three major aspects of the taxation of families: (1) the treatment of the costs of childcare incurred by all parents, regardless of their choice of arrangements; (2) the recognition of the responsibilities for raising children; and (3) the issue of family- versus individual income-based taxation.

Regarding the treatment of childcare costs, Vincent and Woolley argue in favour of maintaining the Child Care Expense Deduction (CCED). Deductibility creates a tax system that is neutral with respect to home-provided and purchased childcare and does not discriminate between single- and dual-earner couples. The authors argue that since parent-provided childcare is not taxed, the income earned to replace parent-provided care with other care also should not be taxed. This is precisely what the CCED does. Moreover, they show that those who claim the CCED is unfair considerably overstate the actual tax benefits this provision gives to parents who choose purchased childcare arrangements.

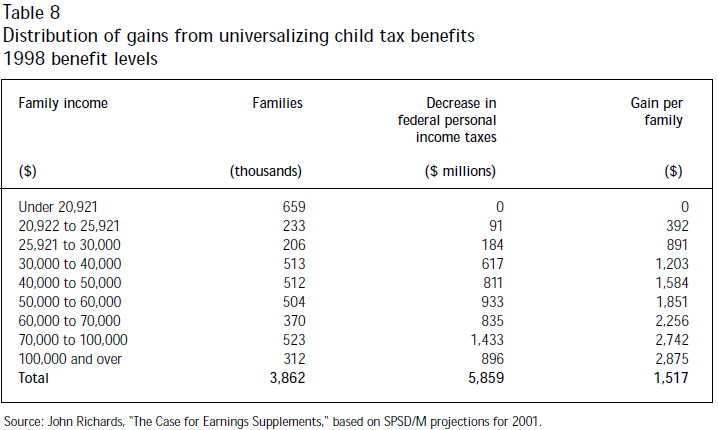

The Canada Child Tax Benefit (CCTB) is the single most important tax programme directed at families with children. However, it is meant to be the main instrument to fight child poverty and is phased out for higher-income families. Its introduction in 1993 was accompanied by the elimination of family allowances, the refundable child tax credit and the non-refundable dependant credit. While Vincent and Woolley recognize that the current CCTB does deliver a reasonable level of transfers to low-income parents, they argue that it has created significant inequities between families with children and those without children. The authors recommend converting the CCTB into a universal benefit, as this is the only policy option that fixes the two most important problems with Canada’s tax treatment of families. First, it restores fairness since it guarantees to all parents some recognition of the responsibilities and costs of raising children, acknowledging that a family with children requires more resources than one without to achieve the same standard of living. Second, it reduces the high effective marginal tax rates faced by low-income families with children that result from benefits being clawed back as income increases. Moving to universal child benefits could lower effective tax rates by as much as 25 percentage points for those families with incomes between $25,000 and $30,000.

Finally, the authors review the arguments put forward by critics of Canada’s current tax treatment of the family who compare single-earner and dual-earner families with the same total income and argue that the greater tax paid by single-earner families is unfair. In this area, the authors show that the issues involved are not that simple. They assess income splitting provisions and family- versus individual-income-based taxation systems. They argue in favour of the current individually-based system since a family-based system that failed to take into account elements such as the value of the goods and services provided by stay-at-home parents would actually give rise to further inequities across families.

Our tax system’s effect on the Canadian family has provoked considerable debate over the past few years, giving rise to numerous policy options presently under consideration. Some argue our tax system favours dual-earner families and works to the detriment of families in which one parent chooses to stay at home to take care of the children. These proponents also often claim that parent-provided care is superior to other types of care and advocate policies that subsidize stay-at-home parents. Others maintain that universal, subsidized childcare generates greater social and economic benefits. In order to improve fairness, some recommend reinstating a tax exemption for children. And still others make a case for a universal child benefit, stressing that a family assistance policy should be based on society’s recognition of the collective benefits accrued from raising children.

Critics of Canada’s current tax treatment of the family often compare single and dual-earner families with the same total income and argue that the greater tax paid by single-earner families is unfair. The problem with this comparison is that it ignores the value of the goods and services that are provided by the parent who stays at home. A family in which one parent earns $30,000 and the other does not work outside the home enjoys a higher discretionary income than a family in which both parents earn $15,000 each, working full-time outside the home.

Similarly, the growing number who are lobbying to extend the Child Care Expense Deduction (CCED) to families that do not incur childcare expenses fail to recognize that this deduction is designed to account for the direct costs associated with earning income. Deductibility provides neutrality between home-provided and purchased childcare. What’s more, the tax benefits related to the CCED are often overstated in this debate — the average childcare expense claim is less than $2,000 per child, a fraction of the “$7,000 in tax-free income” often cited by those who argue the CCED is unfair.

By explaining how the language of equity and efficiency is used in economics, this Choices paper attempts to unravel the following puzzle: How is it that proponents of different policy options, who all appeal to some notion of fairness and efficiency, arrive at very different conclusions? Authors Carole Vincent, research director at IRPP, and Frances Woolley, associate professor of economics at Carleton University, survey a wide range of recent research on household economics and provide a coherent analytical and empirical study of the main issues surrounding taxation and the family. They offer a comprehensive analysis of the overall tax treatment of families in Canada, the implicit policy choices involved and the options for reform.

They argue that Canada’s tax system does many things right but fails to provide adequate recognition of the responsibilities of caring for children. Recent initiatives aimed at fighting child poverty have created inequities between families and have compromised economic efficiency.

The authors advocate converting the Canada Child Tax Benefit into a universal benefit. This is the only option that would fix both problems with Canada’s current system. It would restore fairness between families by providing benefits to all Canadian children and reduce the high effective marginal tax rates facing families with children that arise from clawing back child benefits as income increases. Based on both principles of equity and economic efficiency, they find this is the best policy option.

Families with children have faced increasingly intense financial pressure since the early 1980s. The average real and relative earnings of young adults, who head most families with young children, have declined;1 men of all ages have seen their employment rates fall; and single-parenting rates have increased.2 These factors combine to create economically vulnerable kids: children under 14 have a higher incidence of low incomes, after taxes and transfers, than any other age group,3 according to a study conducted by Statistics Canada and Human Resources Development.

Canada’s policy response to the struggles of young families has been to eliminate universal measures such as family allowances and child tax relief, redirecting these fiscal resources toward low-income families. The variety of programmes we now have provides some families with adequate, even generous benefits. But other families, particularly those with older children, those who do not use formal childcare, and those with above average earnings, are taxed as if they had no care giving responsibilities at all. The disparities in benefits across family types have created a general sense of unfairness and inequity among various groups. The time has come to take a comprehensive look at the overall structure of the tax and transfer provisions that affect Canadian families, the implicit policy choices it reflects and the options for reform. This study summarizes a wide range of recent research on household economics in order to provide a coherent economic analysis of the main issues surrounding taxation and the family.

Since the fundamental unit of taxation in Canada is the individual, why have a policy debate on the tax treatment of families? Several reasons: First, because children are not considered distinct entities for tax purposes, the tax treatment of families reveals how society views the cost of raising children and how this cost is shared across members of society as a whole. Second, household production within the family is a significant contribution to Canada’s economic well being; while household production is recognized as valuable, its appropriate tax treatment should be well understood. Third, families, to some extent, share their resources. Therefore, some view family income as a better measure of ability to pay taxes, in which case the family could be considered a more appropriate tax unit than the individual.

Our assessment relies on in-depth evaluations of three major aspects of household economics and the taxation of families:

We will show that Canada’s tax treatment of families does many things right. But, it could also do some things better, since it fails to provide adequate recognition for the responsibilities of caring for children faced by all families. The immediate priority for change is the reinstatement of a universal child benefit programme. Universal benefits would create a tax system that would treat families with and without children more fairly and would reduce the inefficiency costs associated with the high marginal tax rates facing families with children.

No universal recognition for children currently exists in the Canadian tax and transfer system. This has not always been the case. In 1945, the Canadian government introduced family allowances, payable to all eligible parents regardless of their income or assets; a tax exemption with respect to dependent children was introduced two years later; and in 1972 we saw a new deduction for childcare expenses. At that time, all working women but not all men could claim the deduction.

Over the years, the evolution of the tax treatment of family allowances reflects a policy of targeting benefits toward lower-income families. In 1974, family allowances became taxable, thus creating a selective benefit. While a large part of the allowance remained in the hands of the lowerincome families who did not earn sufficient income to pay taxes or earned just enough to be taxed at the lowest marginal tax rate, families in higher income tax brackets received a benefit that was progressively reduced as income rose.

The refundable child tax credit, introduced in 1979, provided additional assistance for lowto middle-income families in meeting the costs of raising children. The amount of the credit was based on a rudimentary form of family income. It provided a benefit payable to families with income under a given threshold. The amount of the credit was clawed back as income exceeded that threshold.

Until 1988, family allowances paid in respect of a child were required to be included in the income of the person who claimed a personal exemption for the child. As a rule of thumb, it was always beneficial for the higher-income spouse to report the family allowance and claim the exemption as long as the exemption exceeded the allowance. However, when the child tax exemption was converted into a credit as part of the tax reform of 1988, this simple rule of thumb no longer applied in all cases. For those taxpayers facing a higher tax rate than the 17 percent rate of credit, the tax payable on family allowances exceeded the tax relief provided by the child credit.

The 1989 federal budget introduced a provision to ensure the recovery of family allowances (and old-age security benefits) from higherincome taxpayers. Repayments of family allowances were calculated on the income tax return of the higher-income spouse although it was almost invariably paid to the mother. This provision contributed to the erosion of public support for the programme, since men — the higher income earner in the majority of households4 — strongly resented paying back family allowances they never personally received.

In 1993, the federal government enacted a major reform of child benefits under which the Child Tax Benefit replaced three separate federal benefit programmes for children: family allowances, the non-refundable dependant credit with respect to children under 18, and the refundable child tax credit. It provided a basic amount and included a working-income supplement for low-income working families.

The Child Tax Benefit has subsequently been enriched and, with extensive federal-provincial co-operation under the National Child Benefit Initiatives, was crafted into a new programme in 1998. This new benefit comprises a base benefit, the Canada Child Tax Benefit and a National Child Benefit Supplement available to all low income families regardless of their source of income. Provincial initiatives, through various programmes, also support lowand modest income families.

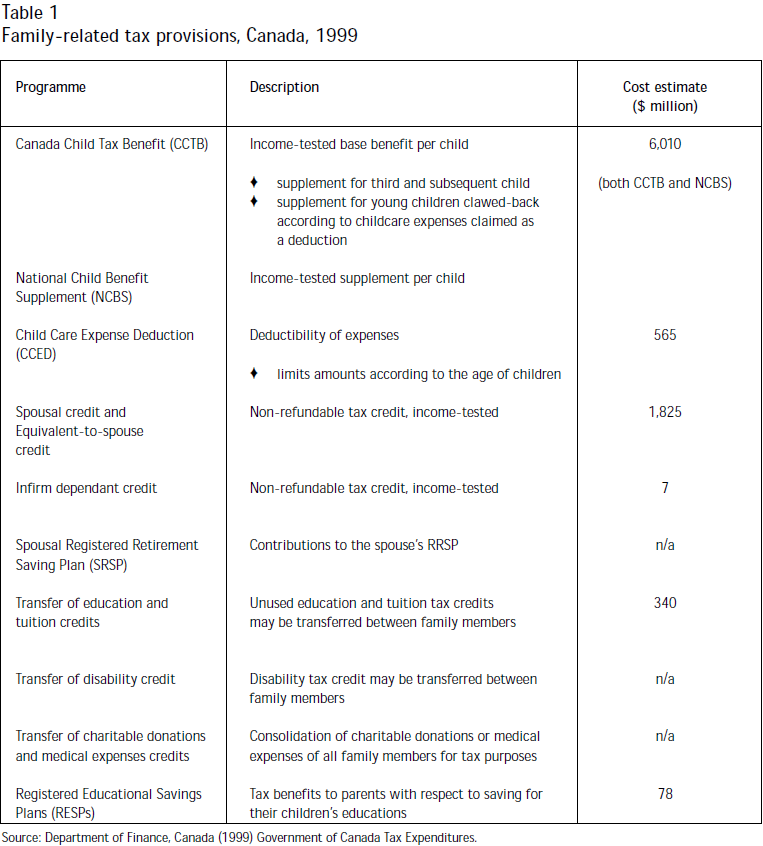

Successive compromises have therefore created a number of programmes with different though overlapping constituencies. Table 1 provides a summary of these programmes and their estimated cost for 1999. The Canada Child Tax Benefit (CCTB) annually provided a basic credit of $1,020 per child plus $75 for the third and each subsequent child. It also included a supplement of $213 for each additional child under the age of seven, and this supplement is reduced by 25 percent of all childcare expenses claimed as a deduction. Because this basic amount is income-tested, the benefit was gradually reduced when family income exceeded $25,921. For families with one or two children, benefits were eliminated when family net income reached $66,721 per year. The National Child Benefit Supplement provided up to $785 for one-child families and additional amounts for second and subsequent children. This supplement was clawed back when family income exceeded $20,921 and the schedule of benefits was such that only families with income below $27,750 qualified for some amount of supplement. Therefore, the constituency for the CCTB is lowand modest-income families with children.

The Child Care Expense Deduction (CCED) allows families to deduct up to $7,000 per year in childcare expenses for each child under seven and $4,000 per child for children between seven and sixteen years old. While the benefit is theoretically available to all families without an at-home parent, its value is greatest to people in the upperincome brackets who face higher marginal tax rates. For someone facing a combined federalprovincial marginal tax rate of 45 percent and claiming $7,000 in childcare expenses, the CCED would reduce taxes owing by $3,150. Thus, the primary constituency for the CCED is dual-earner and single-working-parent families, particularly those with young children.

The Spousal Credit is a non-refundable credit that reduces taxes owing by the amount of the credit ($6,055) multiplied by the first bracket tax rate of 17 percent. At a basic 25 percent combined federal-provincial credit rate (assuming provincial taxes are equal to 50 percent of federal taxes), the spousal amount would reduce taxes owing by $1,345. This credit is reduced by 17 percent of the amount by which the spouse’s income exceeds $606. Therefore, the credit is zero with respect to a dependent spouse with more than $6,661 in net income. The spousal amount provides assistance to two-parent families with a stay-at-home spouse, as well as to families where one adult is not in the labour force for any other reason. The EquivalenttoSpouse Credit is calculated like the spousal amount and can be claimed by single parents on behalf of their first child under age 18. The Infirm Dependant Credit can be claimed for dependent relatives over 17 years of age who are physically or mentally infirm.

Another form of tax support for families comes from a number of measures that reduce the tax burden of families through income-splitting provisions. One individual’s Registered Retirement Saving Plan (RRSP) contributions may be made to the spouse’s RRSP, allowing couples to transfer retirement income from the higherto lower-earning spouse, thereby reducing total tax liabilities at the time funds are withdrawn from the plan. The unused portion of some non-refundable tax credits — disability, age and pension, and tuition and education credits — is transferable to the individual’s spouse or parent, thereby recognizing income sharing between spouses and between parents and children. In addition, the consolidation of all charitable donations or medical expenses onto one partner’s tax return reduces a family’s total tax liabilities. Finally, the Registered Educational Savings Plan (RESPs) provides some tax benefits to parents who save for their children’s educations.

In terms of foregone federal tax revenue, the Canada Child Tax Benefit is the most important programme. It cost $6 billion in 1999, as reported in the Department of Finance’s report on tax expenditures. The spousal (and equivalent-tospouse) amount is the second most significant, at $1.8 billion, while the much-debated childcare expenses deduction costs the federal government an estimated $565 million. The moderate cost associated with the childcare expense provision is explained by two factors: First, only a fraction of parents use formal childcare arrangements that provide the receipts required for claiming the tax relief. Second, most parents spend less on child care than the maximum amount for deduction.

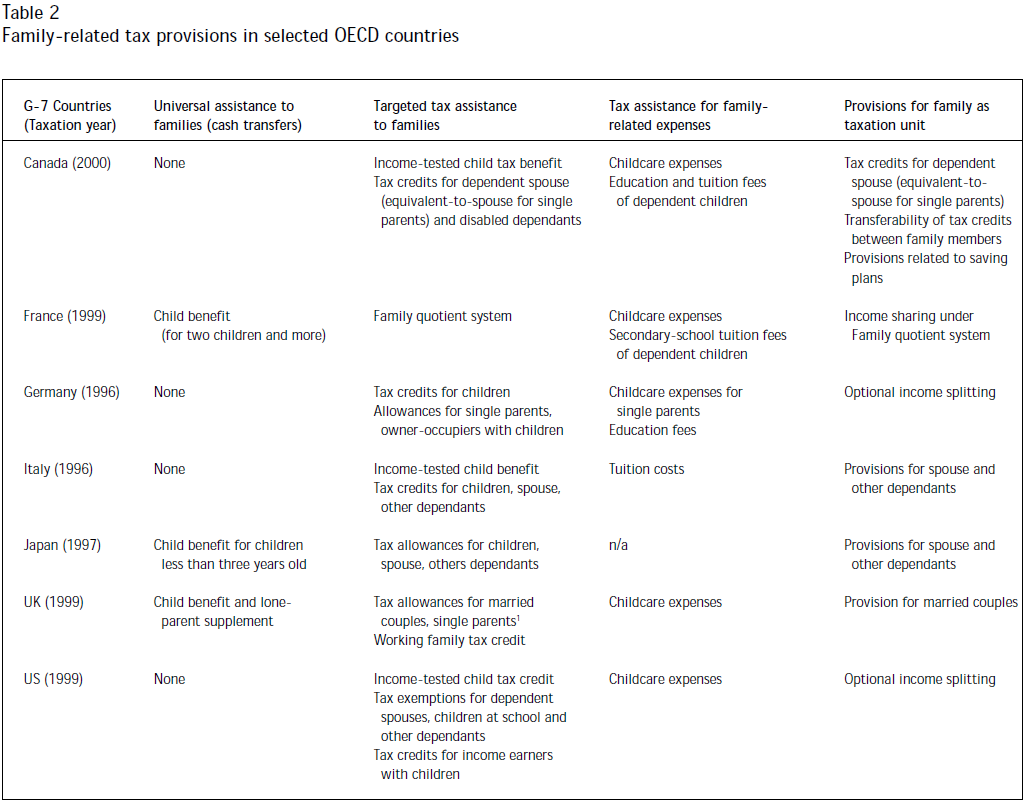

Table 2 summarizes family-related provisions of the tax and transfer systems for the G-7 countries and other selected OECD countries. Universal transfers to families with dependent children, or demogrants, are cash transfers paid directly to the parents independently of their level of income. Among all G-7 countries, only France, Japan and the United Kingdom have universal assistance with respect to children, although France has some restrictions that depend on the number of children and Japan has some that depend on the age of the child. Belgium, Ireland and Sweden also offer universal child benefits, while there is no such provision in Australia. Among all 29 OECD countries, only five other countries have universal child benefits: Denmark, Finland, Luxembourg, Norway and the Netherlands.

Provisions in the form of tax assistance to families with dependants include tax allowances, also called tax exemptions, and income-tested nonrefundable as well as refundable tax credits. The level of benefit provided through these provisions depends on factors such as income level and other characteristics but are unrelated in amount to any specific expenses incurred by the taxpayer. The tax system of each country in Table 2 includes provisions for targeted assistance to families, with the exception of Sweden.

All G-7 countries except Japan, for which such information was not available, allow for deductions from income (or tax credits) that are related to expenses incurred with respect to children, such as childcare costs or education fees. Belgium also allows expenses-related deductions for childcare costs, but Australia, Ireland and Sweden do not allow for such deductions.

Finally, there are a number of provisions in the income tax systems of most countries that take into account an individual’s involvement in a spousal or caring relationship. These provisions include some forms of income sharing, income splitting or even joint taxation. In subsequent sections of this paper, we review these various tax provisions in more detail.

A wide range of policy options are presently under consideration, from re-evaluating the CCED to providing some universal recognition for the costs of raising children. While proponents of various policy options all appeal to some notion of equity or fairness — and use strikingly similar language to determine the appropriate treatment of families — it is interesting to note that they nevertheless come to very different conclusions. A starting point to unravelling this puzzle is understanding how the language of equity is used in economics.

Equity has been taken to mean two things: horizontal equity and vertical equity. Horizontal equity refers to the principle where people with equal “ability to pay” taxes should have equal tax liabilities. No one disputes that the Canadian tax system should be horizontally equitable. The focus of debate is on the interpretation of this principle. Does horizontal equity mean the tax system should be neutral with regard to household type, implying that persons earning the same amount of income should pay the same tax regardless of whether they live alone or whether they share their income with others or benefit from the economies of sharing household goods?

Vertical equity is the principle according to which people with greater ability to pay should have greater tax liabilities. Vertical equity underlies the progressive nature of Canada’s income tax system, where the proportion of income that goes to paying taxes increases with the level of income. The difficulty with implementing vertical equity is that no guidance is given as to how much more tax should be paid by those with a greater ability to pay.

The proponents of various policy options also rely heavily on arguments of economic efficiency when they suggest changes to the tax treatment of families. A tax system is efficient when it minimizes distortions in people’s behaviour: their decisions to marry or have children, their labour supply, saving and investment decisions, and even their choices in child care can be influenced by tax considerations. These decisions are affected by changes in marginal tax rates that determine how much additional employment income or return on savings is taken away from the taxpayer through taxation: the higher the tax rate, the greater the efficiency cost. This can create a tradeoff between efficiency goals and equity goals. The higher tax rates needed to finance redistributive programmes result in greater distortions in people’s decisions.

In the personal income tax system, the component levied on wage income distorts the choice between work and leisure, altering labour choices in a variety of ways. It may influence the decision to participate in gainful employment, it may change the number of hours offered and may affect the work effort of employed workers. Taxes may also have some impact on more qualitative aspects of labour decisions, such as the willingness to accept more responsibility, training and occupational choice, formal educational incentives and the like. Taxes on capital income gained by individuals distort their choice between current and future consumption, affecting their saving and investment decisions.

The sensitivity to changes in taxes, prices or wages varies considerably from one individual to another. For instance, the impact of changes in after-tax rates of return on savings may depend on factors such as the type of savings involved. For individuals whose main savings vehicles are public pension plans (e.g., Canadian Pension Plan) or employer-provided pension plans, the responsiveness to changes in rates of return may be relatively low. These types of savings are compulsory savings for retirement which are by definition less responsive than discretionary types of savings such as stock options or RRSPs. For the economy as a whole, aggregate savings will depend on the age and income profile of the population, since age and income affect individual savings patterns.

Many factors affect the labour supply response to changes in tax rates. The primary earner in a family (often a man) usually shows less response to changes in after-tax wages, possibly because he may feel the responsibility to maintain a certain standard of living. The secondary earner (often a woman) has greater flexibility and is usually more responsive to changes in taxation, especially where children are involved.5 Also, there may be institutional constraints in the form of fixed hours of work, and these constraints do not apply uniformly to all workers. Highly skilled workers of both sexes are more likely to be salaried and thus have fewer opportunities for varying working hours, while lower-skilled workers, especially part-timers, have greater flexibility with their working hours.

Therefore, one expects wide variations in the sensitivity to taxes by age, sex, occupation, family status and income. This means tax reform proposals’ effects on efficiency do not depend on the overall changes in marginal tax rates. They depend on the changes in marginal tax rates faced by different groups, the behaviour responsiveness of each group and the relative importance of each group in the population. This distinction is particularly relevant when analyzing the efficiency effects of policy proposals on the taxation of families because they generally involve specific changes in marginal tax rates for critical groups of individuals such as women with children or low-income workers with children.

While the concepts of equity and efficiency, as described above, are commonly used in tax policy debates, public finance specialists are more often turning to broader concepts of fairness and economic efficiency. For instance, policy changes may affect economic efficiency through their impact on administrative costs, compliance costs and opportunities for tax evasion or tax avoidance. The administrative cost of enforcing and collecting taxes is an expenditure that, if financed through higher taxes, will increase economic distortions. Similarly, compliance costs on the part of businesses and individuals reduce welfare by raising the cost of goods and services produced and by wasting a portion of the time dedicated to leisure. Taxes also affect efficiency to the extent that they provide incentives for individuals to relieve themselves from their fiscal burden through legal (tax avoidance) or illegal (tax evasion) means. If due to these activities government revenue loss is recovered through other taxes, the result is higher overall tax rates and increased economic distortions. Tax avoidance and evasion also raise issues of equity since the opportunities to resort to such measures are not equal for all taxpayers. Therefore, they can alter the pattern of the distribution of the tax burden by income class, family type or the type of engagement in productive activities.

When evaluating the performance of a government policy, other principles can come into play. For instance, the adequacy of a policy can be evaluated in terms of the outcomes it achieves. One possible outcome measure is poverty reduction, which has been a primary goal of recent tax reforms, especially those surrounding child benefits. A second valuable outcome that greatly concerns a growing number of analysts is the reduction of income inequality, and the degree to which government policy can reduce income inequality between men and women, types of workers and families, and across generations.

In recent tax policy debates, some have turned to notions of equity that focus on “process,” or how the tax system operates, rather than what outcomes it achieves.6 Opposition to a particular government tax policy may reflect taxpayers’ perceptions that the policy was introduced against the expressed will of the majority of the population. In such a case, there may be suspicions of abuse of political power. A recent example of concern over the legitimacy of certain tax policies is Beverley Smith’s communication to the United Nations Commission on the Status of Women alleging that a large group of women in Canada face discrimination through the income tax system. Specifically, her communication alleged that women who stay at home to care for children are discriminated against because the Canadian income tax system does not allow employed parents to pay a salary to their stay-at-home partner.7

Other groups are beginning to articulate principles for non-discriminatory taxation. The Women’s Working Group of the Ontario Fair Tax Commission made a start by arguing that a key goal of the tax system should be the “recognition of women’s autonomy.” According to this group, provisions in the tax system should “treat women as individuals, distinct from their familial relationships and, in particular, from their male partners.” 8 Unanimous agreement on taxation policy is not likely to happen. However, respect for individual rights is a growing issue in tax policy.

Some policy analysts, such as Kenneth Boessenkool,9 distinguish between the goal of tax policy, which is “how to design an equitable and efficient system of raising the required revenues for governments”, and the goal of social policy, which he defines as “providing income transfers to less-well-off citizens.” The tax policy v. social policy distinction is one we reject. We believe the evaluation of any tax proposal should be based on a comprehensive analysis of family policy. A tax system that is, or is perceived to be, onerous, unfair or overly complex, or tends to increase inequalities of income and opportunity cannot be counted on to support the efficient functioning of that system.

In the following sections of this paper, we will adopt this comprehensive view when evaluating provisions in the current Canadian income tax system and when proposing an agenda for change. Our assessment starts with a single, simple provision: the deduction for childcare expenses. This provision could be considered the least disputed, to the extent that very few people would like to see it disappear altogether. Yet it still raises many controversial issues.

The main tax provision for child care is the Child Care Expense Deduction (CCED), which allows individuals with earned income to claim up to $7,000 in childcare expenses for each child under seven years of age and up to $4,000 for each child under age 16. In most cases, claims for the CCED are restricted to the lower-income spouse. The value of the deduction depends upon the claimant’s marginal tax rate. For example, at a 25 percent combined federal-provincial marginal tax rate, $1,000 in childcare expenses reduces taxes owing by $250, while the same $1,000 reduces taxes owing by $450 when the marginal tax rate is 45 percent.

The CCED has been greatly expanded and extended since its 1972 introduction. Only in 1983 was the deduction restricted to the lower-income spouse. At that time, the maximum amount one could claim was $2,000 per child. In the 1988 budget, the deduction was increased to $4,000. In the 1992 budget, it was increased to $5,000 for children under age seven and to $3,000 for children between seven and fourteen. In 1996, the age limit for eligible children was raised to 16, ostensibly to help “single parents whose jobs require them to be away from home at night.”10 And in 1998, the deduction was again increased, to $7,000 for children under seven and to $4,000 for children between seven and sixteen. The cumulative effect due to the CCED changes has been a decrease in federal tax revenue, reaching $565 million in 1999.

Canada’s tax treatment of childcare expenses is relatively generous compared with that of other countries. As Table 2 shows, Australia, Ireland, Italy and Sweden provide no tax deductions or no credits for childcare expenses. The United States (US) provides a system of tax relief similar to that existing in Canada, but it targets tax benefits toward lower-income households. The US allows a tax credit for childcare expenses at a rate of 30 percent (i.e., expenses of US $1,000 reduce tax liabilities by 30 percent of $1,000, or $300) for families earning under US $10,000. The credit rate is gradually reduced to 20 percent as family income rises to US $28,000 and higher. The maximum amount for the credit is US $2,400 per child for the first two children, which at the maximum rate of credit of 30 percent yields a tax credit of US $720, or about $1,100 in Canadian dollars. This is substantially less generous than the potential tax savings under the Canadian CCED.11

Canada’s tax treatment of child care has both critics and supporters from across the political spectrum. In early 1999, the Reform Party advocated reducing the value of the CCED for higher earning individuals by converting the deduction into a credit.12 Yet the CCED was also criticized by the Women and Taxation Working Group of the NDP-sponsored Ontario Fair Tax Commission. In their 1992 report, they argue

“. . . tax-delivered assistance should be redesigned to make it more equitable. Specifically, the current limited deduction for childcare expenses should be converted to a refundable credit and increased to more realistically reflect the costs of child care. A minimum credit should be available for parents with no receipts.”13

Does Canada’s tax treatment of child care need changing? How does the current system fare in terms of equity and efficiency criteria? What is the best direction for change? One way to evaluate the adequacy of this tax provision is to look at its distributional impact.

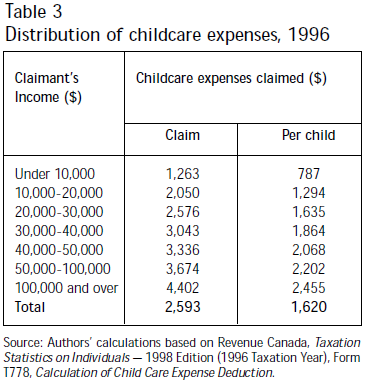

Table 3 shows the distribution of childcare expenses claimed in Canada in 1996 by claimant’s income class, both per claim and per child.14 On average, parents claim $2,593 in childcare expenses. The average amount per child is $1,620. Higher-income earners claim more, on average, than do lower-income earners on a per claim or per child basis. This reflects the greater number of hours worked by high-income earners and the more expensive childcare choices they make. Typically, a parent earning $20,000 to $30,000 and claiming childcare expenses has only $2,576 in allowable expenses. This is several thousand dollars less than the maximum childcare deductions allowed.

The figures given in Table 3 demonstrate that some analysts considerably overstate the potential benefits related to the tax provision for childcare expenses. For example, Boessenkool15 reports dual-earner families enjoying $14,000 in tax-free income solely due to the CCED provision, assuming this dual-earner family of two children claims the maximum amount of $7,000 per child under age seven. In reality, Table 3 shows the average childcare expense claim is only $1,620 per child, or $3,240 for a two-child family, a fraction of the number assumed by Boessenkool.

Similarly, the Reform Party assertion that the tax system discriminates against single-income families since “[a] dual-income family making $30,000 would pay less than half the income tax owed by a single-income family making the same amount”16 was based on the same misleading assumption that dual-income families claim the maximum amount of allowable childcare expenses.

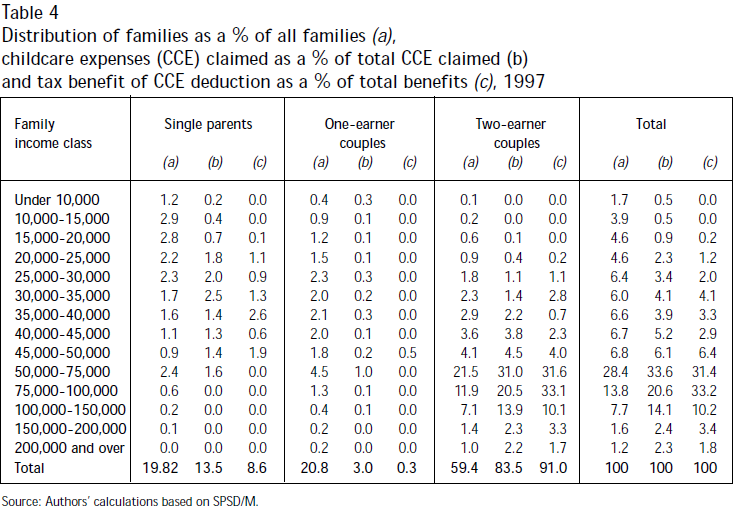

Table 4 shows the amount of expenses claimed by family, per family type and income category, as a percentage of the total claims, and the associated distribution of the tax benefit, i.e., the amount that federal taxes are reduced by the CCED.17 It also shows the distribution of families as a percentage of all families. Dual-income families make more use of the CCED: they represent almost 60 percent of all families with children but claim 91 percent of all childcare expenses. About 40 percent of childcare expenses are claimed by families with incomes above $75,000 a year, representing 24.3 percent of all families, while over 70 percent of childcare expenses are claimed by families with incomes above $50,000, representing 52.7 percent of all families. The progressivity of the income tax system further skews the distribution of the tax benefit of the CCED toward higher-income earners: families with incomes over $75,000 receive 48.6 percent of the tax benefits, although they represent only 24.3 percent of all families. The share of tax benefits received by higher-income earners is likely to increase due to the 1998 budget’s enrichment of the CCED.

The figures in Table 4 are not surprising. An average dual-income family earns about $60,000 a year, so the clustering of benefits in the $50,000 to $75,000 income range simply reflects the large number of families in this income group. In fact, families in this income range represent 28.4 percent of all families and they receive 31.4 percent of the tax benefits. Moreover, unless the claimant is in the middle or higher tax bracket, it is actually disadvantageous to use receipted child care and claim the CCED rather than simply paying a caregiver in cash, because the caregiver will be required to pay Canada Pension Plan or Quebec Pension plan (CPP/QPP) and Employment Insurance (EI) premiums and may also lose transfer income such as the Goods and Services Tax (GST) credits. It is not surprising, therefore, that an estimated less than one third of families with childcare expenses actually make a claim under the CCED.18

From the viewpoint of horizontal equity, a person with a gross income of $60,000 and income earning costs of $10,000 should pay the same taxes as a person with a gross income of $50,000 and no income-earning costs. The strongest equity argument in favour of the current deduction is that childcare expenses represent costs incurred to earn employment income. Because childcare expenses reduce a parent’s ability to pay taxes, horizontal equity provides a justification for tax recognition of childcare expenses.

This argument in favour of childcare expense deductibility can be put another way, based on efficiency principles: childcare expense deductibility creates a tax system that is neutral between home-provided and purchased child care and therefore does not discriminate between oneearner and dual-earner couples. Neither pays tax on the cost of childcare. If parent-provided childcare is untaxed, but income earned to replace parentprovided childcare with other care is taxed, the tax system will create strong incentives for parents to care for their children at home, distorting individuals’ behaviour. This neutrality rule is well explained by McCaffery:19 “Since the self-provided services of childcare are not taxed, the working wife should not have to pay tax on the dollars she earns simply to replace those services. Put another way, the cost of childcare — whether performed by a natural parent or a paid third party — should not be taxable. That’s a “neutral” rule.”20

It is important to recognize that the beneficial effects of the tax deductibility of childcare costs may extend beyond its immediate gains accruing to parents with young children. This provision, like other tax provisions, causes changes in prices that shift the incidence of benefits to other groups of individuals. For instance, the CCED provides a strong incentive for parents to use formal, regulated child care rather than paying caregivers in cash, at a level possibly below the minimum wage, and not providing employees with social benefits, such as CPP/QPP benefits or workers’ compensation coverage. Therefore, a fraction of the tax savings from the CCED may be passed on to childcare workers in the form of higher wages and better working conditions.

The reporting incentives created by the CCED also mean that estimates of the tax revenue foregone due to this provision may overstate the measure’s true revenue cost. Although it is hard to estimate the increase in tax evasion that would accompany an elimination of the deduction, it is likely that more caregivers would be paid in cash and the income not declared for tax purposes.

It is true that some expenses claimed as “child care” may be primarily entertainment, educational or housekeeping expenses. For example, summer camps for older children provide entertainment and education as well as child care, and nannies may perform light housekeeping in addition to childcare duties. However, myriad provisions in the tax system are open to similar forms of abuse, from home office expenses to charity golf tournaments. The possibility of abuse argues for more closely monitoring childcare expenses rather than eliminating the provision. A simple mechanism of limits on the deduction amount — as done under the current system — helps avoid major abuses by containing the deduction to “reasonable” expenses.

Underlying the efficiency arguments for childcare expense deductions is the view that purchased child care is no better and no worse for children than care provided at home. Not everyone agrees. Some groups tend to argue that parent-provided care is superior to other care. Consequently, they argue for policies that subsidize stay-at-home parents. The Canadian Family Tax Coalition, for example, argues that the CCED should be converted into a refundable child tax credit for all children. 21 The result would be a non-neutral tax system that creates incentives for parents to provide in-home childcare.

The Sub-Committee on Tax Equity for Canadian Families also recommended that “[t]he government should consider reviewing the Child Care Expense Deduction in order to ensure that it is meeting its policy objectives in a way that is most efficient and effective for Canadian families with children.”22 One of the options under review will certainly be converting the CCED into a credit.

The major impact of converting the CCED into a credit is that it would be a progressive policy reform, thus enhancing vertical equity. But would it help the average Canadian family, considering over half of childcare expenses are claimed by individuals with income under $30,000 who would be unaffected by changing the CCED into a credit? Parents in the bottom income tax bracket would suffer no losses, assuming the credit rate would be equal to the first bracket tax rate of 17 percent and that any related change to their level of “net family income” for the purpose of calculating CCTBs would not affect their eligible child benefit payments. 23 Parents in the top income tax bracket, on the other hand, would lose because the value of the credit would be lower than the value of the deduction. The revenue savings from such a measure would most likely be too small to provide a foundation for fundamental reform, and any immediate savings would most likely be offset by a reduced incentive to use formal, receipted childcare arrangements.

Moreover, the conversion of the deduction into a credit would generate horizontal inequity among those individuals facing a marginal tax rate higher than the rate of the credit. To reiterate the argument presented above, consider the example of two people, one incurring childcare costs equal to $10,000 to earn an income of $60,000, the other earning an income of $50,000 without having to incur such costs. Assuming the marginal tax rate faced by these two people is 50 percent, and the rate for conversion of the CCED into a tax credit is 17 percent, there is horizontal inequity since the person with the childcare costs pays $3,300 more in taxes than the other person, although the two have the same income net of childcare costs and thus, presumably, the same ability to pay taxes.

Efficiency arguments for the CCED rest on the efficiency of choices between work, domestic production and leisure. Although the CCED lowers the barrier to labour market participation imposed by childcare expenses, this provision is, unfortunately, of little value to low-income earners and other “marginal workers.” Yet, in order to facilitate labour market reinsertion or attachment, society has a strong interest in reducing the costs these marginal workers face when entering the labour market. This is especially relevant for parents with lower levels of education and few professional qualifications, who would otherwise have to turn to social assistance to meet their needs and those of their children. Therefore, provinces are increasingly using childcare subsidies as a way of promoting labour market attachment.

There is a substantial body of evidence that shows the cost of child care has a significant effect on women’s labour force participation. Cleveland, Gunderson and Hyatt,24 for example, found that a 10 percent increase in the cost of child care reduces the mother’s probability of employment by 3.9 percent, while a 10 percent increase in the mother’s wage increases the probability of employment by 8.1 percent and the probability of purchasing market child care by 2 percent. US studies have found similar or greater effects of childcare costs on labour supply: a 10 percent increase in the cost of child care reduces the probability of employment by between 2 and 13.6 percent, with white single mothers feeling the greatest impact.25

In 1997, Quebec introduced a policy of highly subsidized daycare, justified in terms of its educational and socialization value. In its March 2000 Speech from the Throne, the government of British Columbia stated that it intends to introduce a universal childcare programme, somewhat along the lines of the Quebec scheme, although no details have yet been provided. The Quebec government chose to provide child care at a rate of $5 per day for all children aged two to four years regardless of their parents’ income (and eventually extend this programme to younger children). This new government measure was accompanied by reduced and more selective monetary assistance to families. Family allowances are now targeted at low-income families and replace several provisions that had previously been offered to all families. Baril, Lefebvre and Merrigan26 estimated that, compared with the pre-reform situation, 72 percent of families would receive less financial assistance from the provincial government the year after the reform. A portion of this reduction in direct financial assistance is being used to finance subsidized childcare services and the extension of educational services. However, according to Baril, Lefebvre and Merrigan, the new services offered are not likely to compensate for the financial losses experienced by parents.

Little information is currently available about the programme’s longer-term impacts on labour force participation, child development or the family financial situation, for examples. As time goes on however, the $5 per day programme will provide an interesting “natural experiment,” enabling researchers to determine the effect of childcare provision on parents’ labour force participation, family incomes and child outcomes. But, while natural experiments are wonderful opportunities for social science researchers, there is reason to be cautious about this experiment’s overall impact on children, parents and Quebec’s society and economy.

Moreover, no strong evidence currently exists that shows universal, subsidized child care generates greater social and economic benefits than other possible government programmes aimed at the development of young children. Until recently, the type of longitudinal data necessary to determine the long-term impact of child care on children’s development was unavailable.27 The National Longitudinal Survey of Children and Youth will address these data gaps. But the survey has not been underway long enough to permit an evaluation of childcare options.

The question of the appropriate treatment of the costs of raising children is, and will remain, a crucial issue for Canadian families. Although the CCED has its problems and critics, the provision is too small to provide a foundation for fundamental reform. What’s more, it preserves horizontal equity in the tax system.

The costs of childcare services — either formal or informal — are only one aspect of child-rearing expenses and responsibilities. The next section looks at broader issues: the appropriate recognition for the responsibilities of caring for children in our tax system and the adequacy of child related programmes in delivering a reasonable level of transfers to families with children.

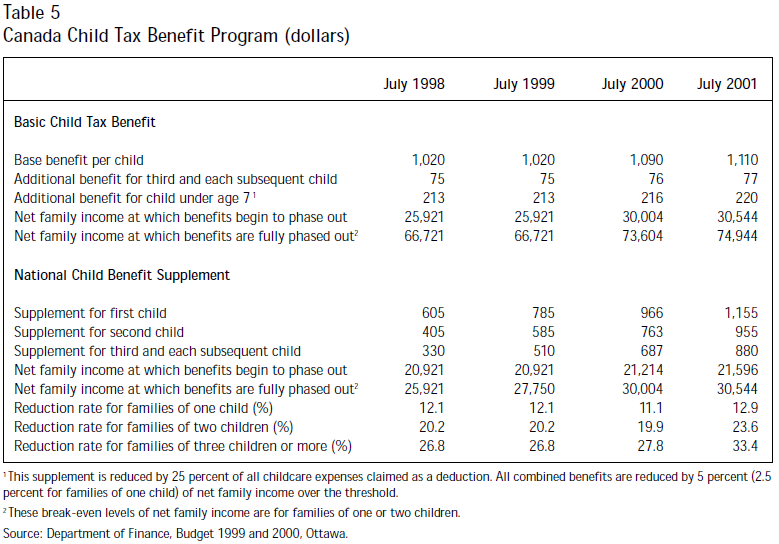

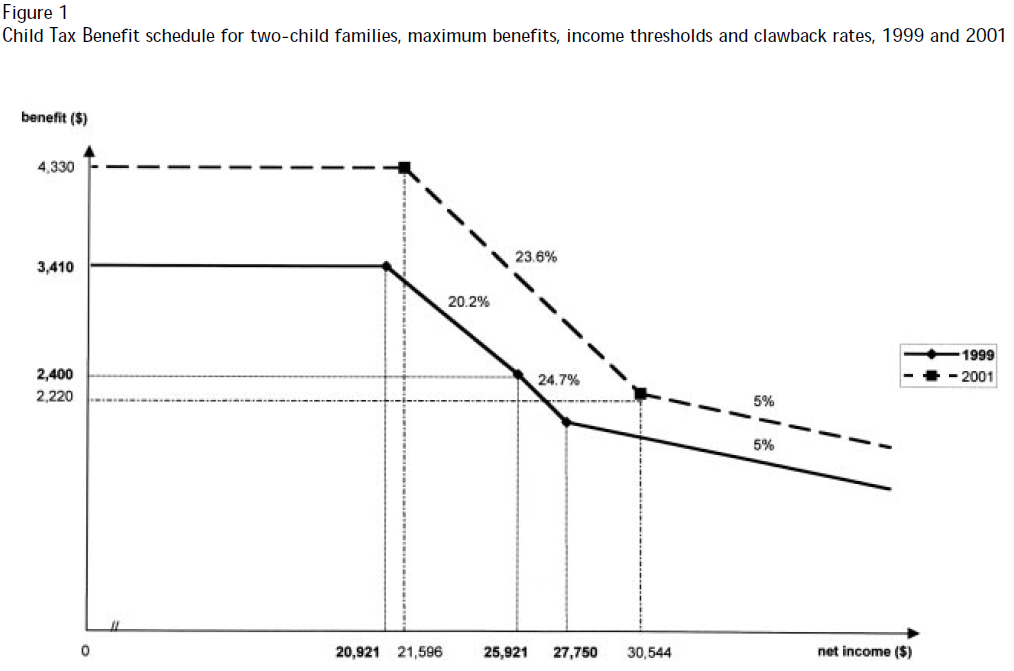

The major programme for Canadian children is the Child Tax Benefit. The Canada Child Tax Benefit (CCTB) is a joint federal-provincial initiative designed to help children in lowand moderateincome families. In July 1999, the base benefit was worth $1,020 per child per year, with additional benefits for third and subsequent children and for children under age seven. For a two-child family, benefits were reduced by five cents for each dollar earned above $25,921 (by 2.5 cents for one-child families) and phased out entirely at a family net income of $66,721. The National Child Benefit (NCB) supplement provided up to $785 for onechild families and additional amounts of up to $585 for a second child and up to $510 for each subsequent child. The supplement was reduced by 12.1 percent of family income over $20,921 for a one-child family, by 20.2 percent for two-child families and 26.8 percent for families with three or more children. The schedule of benefits was such that only families with income below $27,750 qualified for some amount of NCB supplement.

As of July 2000, all of these benefits were enriched, as shown in Table 5. In the February 2000 federal budget, the government announced that the CCTB and thresholds of family income for maximum benefits would be fully indexed to the cost of living, starting January 2000. The base benefit increased by $70 per child. When combined with increases announced in the 1999 budget that also took effect in July 2000, this brings the maximum benefit to $2,056 for the first child (excluding the additional benefit for children under the age of 7) and to $1,853 for the second child of families with net income below $21,214. Benefits are fully phased out at a family net income of $73,604. In July 2001, the NCB supplement for lower-income families will further increase by $200 per child. The schedule of benefits will be such that only families with income below $30,544 will qualify for some amount of NCB supplement in 2001.

The CCTB has two major goals. The first is “to help children in low-income families get off to a good start in life.”28 It is explicitly targeted at lowand moderate-income families. The second goal is to improve work incentives and help low-income families breach the “welfare wall.” The NCB supplement is a “portable” benefit in the sense that parents retain their NCB supplements when they move off welfare into a paying job. To make sure working is relatively more attractive than social assistance, the NCB supplement is offset by a reduction in social assistance payments (except in Quebec and New Brunswick). The provinces reinvest the savings from reduced social assistance payments in programmes for children and families at risk. By moving support for children out of social assistance programmes and into the income tax system, the NCB encourages parents to move into the work force where they have better long-term financial prospects.

Do child benefits help children in lowerincome families? From the mid 1980s to the mid 1990s, low-income families in Canada have seen a steady decline in earnings and employment — the poor have become poorer in terms of their market incomes. However, the decline in earnings has been offset by increases in government transfer payments, keeping total family income constant.29 Therefore, Canada has, in part through increased reliance on government transfers, managed to avoid the increases in after-tax income inequality experienced by other developed countries, particularly the US.30

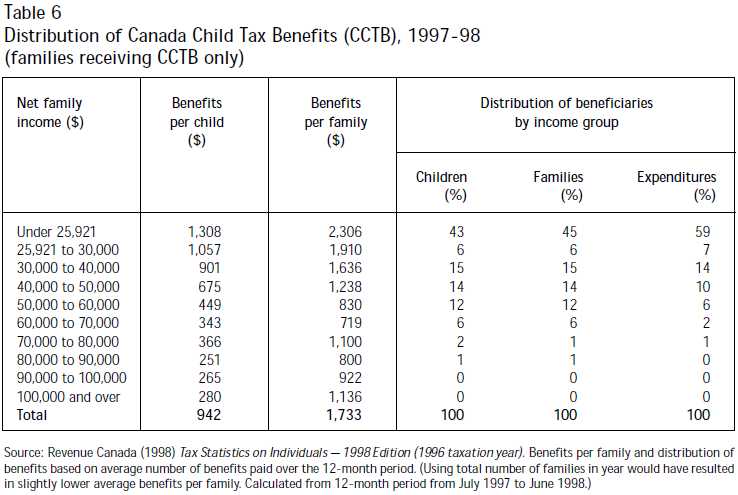

Child tax benefits are part of Canada’s relatively successful record. Table 6 shows estimates of the average amount of CCTB received on a per child and per family basis (conditional upon CCTB receipt), based on Revenue Canada’s Taxation Statistics, and the distribution of benefits across net family income groups.31 As expected, most childbenefit expenditures go to low-income families. Forty-three percent of children receiving benefits are in families with net family incomes under $25,921, as are 45 percent of families receiving benefits. Almost 60 percent of CCTB expenditures go to helping these low-income families. Average benefit levels decrease with income until family incomes reach the $60,000 to $70,000 level. Above that level, only families with three or more children receive benefits. For these higher-income families, changes in family size offset the effect of benefit tax backs, so that average benefits per child are relatively stable.

The figures presented in Table 6 reflect the benefit reduction rates that apply to middleincome families embodied in the structure of the CCTB programme. Some caution should be exercised in interpreting these numbers. First, the “net family income” figures and the “benefits” figures do not refer to the same time period. Net family income is for the 1996 taxation year, while benefits are for July 1997 to June 1998. If a family member has moved into or out of employment, income and benefits will not be so neatly aligned. Second, the figures in Table 6 exclude those families that do not file income tax returns or do not register for child tax benefits. Third, “net family income” excludes some sources of family income, such as child support, and therefore does not provide a complete measure of families’ economic resources.

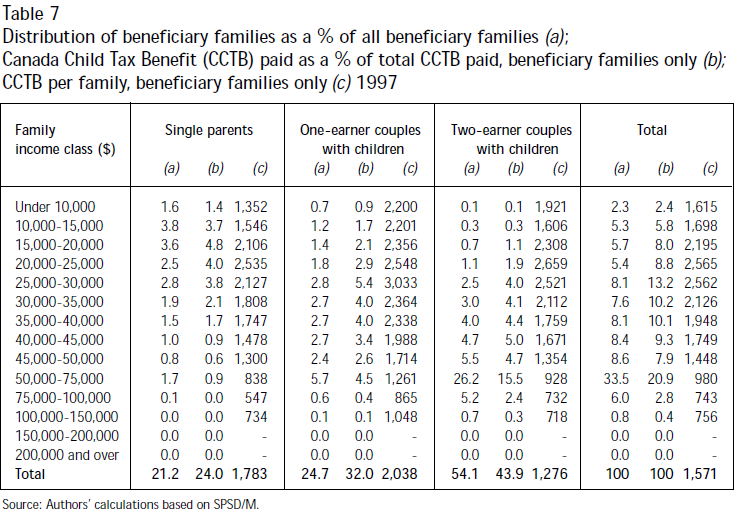

Table 7 shows the distribution of the CCTB, in 1997, by family income class and family type, based on the SPSD/M database.32 It also shows the distribution of CCTB beneficiary families by income class and family type as a percentage of all beneficiary families. On average, beneficiary families receive $1,571 with respect to the CCTB. Lowerincome families, on a per family basis, receive more on average than do higher-income families. Families with income between $20,000 and $25,000 receive average annual benefits of up to $2,565, while families with incomes over $75,000 receive average annual benefits just below $800.

The figures given in Table 7 demonstrate that single parents and single-earner couples with children have, on average, lower incomes and therefore are more likely to receive child benefits. According to our estimates, 32 percent of CCTBs are received by single-earner couples and they represent 24.7 percent of all beneficiary families (and 20.8 percent of all families as reported in Table 4 above). Single-parent families account for 21.2 percent of CCTB beneficiary families and they receive 24 percent of benefits. The Department of Finance projects that for the year 2000 over 75 percent of all CCTBs will go to single-earner families, including single-parent families.33

The CCTB is relatively successful in achieving its first goal, helping children in low-income families. What about the second goal of breaking down the “welfare wall” by reducing disincentives for parents to enter the labour force? Although the number of families with children that are on social assistance has fallen since 1995, to less than 550,000 from 650,000 according to the National Child Benefit Progress Report, there is some question about whether the Canada Child Tax Benefit does in fact improve the work incentives of families with children.

It is true that parents receiving social assistance have improved work incentives, in that they can retain child benefits when they re-enter the job market. However, the effective marginal tax rate faced by low-income families can match or exceed that faced by high-income earners. A number of studies have documented the effect of tax transfer programmes on effective marginal tax rates. When the child tax benefit was first introduced in 1993, Woolley, Vermaeten and Madill34 concluded that the working income supplement, ostensibly designed to reinforce the incentives for lowincome parents to participate in the workforce, lowered marginal tax rates for only 22 percent of the target group but raised marginal tax rates for a much greater number, 36 percent of the target group. Since that time, the supplement has been enriched and the rate at which it is taxed back increased correspondingly.

The changes to child tax benefits effective in July 1999 extended the range over which the NCB supplement was taxed back. Families with incomes between $25,921 and $27,750 saw their tax back rate increase to 12.34 percent from 2.5 percent for a one-child family or to 24.5 percent from five percent for a two-child family.35 Macnaughton, Matthew and Pittman36 simulated the net marginal tax rates faced in 1999 by Canadians with no children and those with one, two or three children. The difference in the net marginal tax rates between those with and those without children is substantial, especially for those with incomes below $30,000. Over a wide range of incomes, individuals with three children face net marginal tax rates eight percentage points higher than those with no children. These marginal tax rates do not include the benefits lost when social assistance payments are reduced as earnings increase. Adding these would create even higher net marginal tax rates at lower income levels.

The changes recently announced in the 2000 budget further enriched both the base benefit and the supplement. This means that as of July 2001, the tax back rates of the NCB supplement will increase again, reaching their highest levels since the introduction of the programme, as shown in Figure 1. The supplement for low-income families with children will provide up to $1,155 for the first child, up to $955 for the second and up to $880 for each subsequent child. These enriched amounts are the result of a $200 per child increase, including the ongoing indexation of the entire supplement, effective January 2000. Since the schedule of benefits is such that only families with income below $30,544 qualify for some amount of NCB supplement, this implies the supplement is reduced by 12.9 percent of family income over $21,596 for one-child families, 23.6 percent for two-child families and as much as 33.4 percent for families with three or more children.

The CCTB programme has moved, not removed, the “welfare wall.” The high effective marginal tax rates faced by those on social assistance have been shifted to those in the $20,000 to $30,000 range. Whether work incentives for families with children have, on balance, improved or worsened is an empirical question. The answer depends on the changes in marginal tax rates faced by different groups, the number of people in each income group, their demographic and economic characteristics and behaviour responsiveness to changes in tax rates, and the interaction of child benefits with other aspects of the tax system. At this point, there is no clear evidence that the CCTB does in fact encourage more parents to enter the labour force.

In assessing the adequacy of the CCTB, the principle of horizontal equity should also come into play. In particular, does the CCTB respect the notion that individuals with similar abilities to pay taxes should face similar tax liabilities?

To address this issue, it is useful to refer to the concept of the “equivalence scale,” adjusted for family size. One widely used set of equivalence scales is the one implicit in the Statistics Canada Low Income Cut Off (LICO). Statistics Canada estimates that a family of four living in a major metropolitan area needs 1.5 times the income of a couple without children at home to achieve the same standard of living. This means a family of four with an income of $70,000 has an income equivalent to a childless couple earning $46,700, an equivalent income of $23,300 less than that of a couple without children also earning $70,000 per year.

Despite the huge difference in the equivalent incomes of those with and without children at home, there may be no difference in the tax liabilities of those couples even when accounting for child tax benefits. Because those benefits are taxed back as income increases, a substantial portion of families with children receive no child benefits whatsoever. By July 2000, the Canada Child Tax Benefit programme will provide benefits to about 3.4 million of families or 83 percent of all families in Canada. Put another way, almost 20 percent of Canadian families with children receive no CCTB whatsoever. If the purpose of child benefits is to provide recognition of children, regardless of their parents’ labour market skills and choices, the Canada Child Tax Benefit is clearly inadequate.

The current system of child tax benefits has helped poor children by taking money away from better-off families with children. Redistribution based on vertical equity considerations has completely replaced those of horizontal equity. Jonathan Kesselman37 argues that “[the] Child Benefit scheme in effect finances much of its gains for lower-income families by increasing taxes only on upper-income units with children.” Similarly, Baril, Lefebvre and Merrigan38 argue that by increasing the funds devoted to the CCTB in 1998, the federal government has chosen to give back to certain families — those with incomes between $10,000 and $25,000 — the sums of money it has taken away from all families with children during the 1980s. There is an emerging consensus that redistributing money among families with children is an unsatisfactory strategy and real changes need to be made.

The reinstatement of exemptions for dependent children is a proposal with many supporters. The C.D. Howe Institute has advocated exemptions be made available to all taxpayers with dependent children, as did the Reform Party.39

The major advantage of such an exemption is that it would provide benefits to those middleand upper-income families that do not incur childcare expenses and receive little or no recognition of their caregiving responsibilities. As its advocates claim, it “introduce(s) a measure of horizontal equity between couples with and without children, ending the tax system’s current treatment of children as consumer expenditures.”40

What are the potential efficiency gains from such a proposal? Exemptions, like deductions, provide higher benefits to higher-income earners. As a person moves into a higher tax bracket, the value of the exemption increases. This increase offsets the increase in taxes payable, thus reducing marginal tax rates and leading to potential efficiency gains. However, a child exemption will do little to address the high marginal tax rates faced by families with incomes between $20,000 and $30,000 unless it is part of a package that includes changes in the clawback rates of the CCTB.

The potential efficiency gains arising from reduced marginal tax rates for those claiming a child exemption have to be weighed against those arising, for instance, from a reduction in the clawback rates of the CCTB. Even though the value of the CCTB is assessed on the basis of family income, the child benefits are in most cases paid to the mother. Therefore, any change to the structure of the CCTB programme is more likely to affect women’s behaviour. In contrast, because the value of an exemption increases with income, it is advantageous for the higher-income parent — most often a man — to claim any exemption.41 Econometric evidence suggests that men and women differ significantly in how they respond to economic incentives such as marginal tax rates, in terms of labour supply, tax evasion or other decisions. The behavioural responsiveness to changes in tax rates depends on other characteristics such as the level of income, family status, level of education or type of occupation.

Men appear to be more responsive to high taxes than are women when it relates to tax evasion.42 However, as far as labour supply decisions are concerned, empirical evidence suggests that men, particularly those that are the sole financial supporters of their families, are not greatly affected by changes in their after-tax wage rate.43 A reduction in those men’s marginal tax rates would, therefore, be unlikely to produce major gains in economic efficiency in that respect. To the extent that exemptions would do little to change the trade-offs facing individuals who would readily exchange work (in terms of pay or prospects) for other activities such as working at home, their efficiency benefits appear limited.

An exemption for dependent children — like any other exemption — can be justified on the grounds that an individual’s ability to pay taxes does not start at the first dollar of income earned; rather, it starts after attaining a minimum level of income necessary for fulfilling basic needs or sustenance. This level of income depends on sociodemographic characteristics such as the presence of children. Therefore, it can be argued that an exemption that takes into account the basic needs for the care of dependent children improves horizontal equity by equally taxing all people with the same level of “gross income minus needs.” However, exemptions alone are an imperfect tool for the establishment of horizontal equity since they do not account adequately for differences in basic needs at a given income level.

To illustrate this argument, suppose Phillip has an income of $40,000 and “extra needs” of $5,000, needs which are deemed to be the responsibility of the whole society. Suppose Ruth has an income of $40,000 and no “extra needs.” Assume, for the sake of argument, they both face a 25 percent marginal tax rate. Phillip’s disposable income, after taxes and the cost of meeting its “extra needs” is $26,250 ($40,000 income, minus $5,000 needs, minus 25 percent of taxable income $35,000); Ruth’s disposable income is $30,000 ($40,000 income, minus 25 percent of taxable income $40,000). Even with an exemption equal to the cost of meeting Phillip’s “extra needs”, Ruth is still better off than Phillip although she has no “extra needs”. Regardless of income, children increase a family’s basic needs. If provisions for children are regarded as compensation for needs, it is not clear that an exemption is the appropriate mechanism for recognizing the costs associated with dependent children.

Another disadvantage of a child exemption is that it is an impractical way of providing benefits to the caregiving parent. Exemptions, deductions or non-refundable credits all reduce the amount of taxes a person pays. Stay-at-home parents often have very low income, which translates into very low tax liability. Therefore, they may receive no benefit from such tax relief, when benefits paid directly to caregiving parents are in fact more likely to be spent on children, not to mention the fact that such benefits can enhance the economic autonomy of caregivers. Lundberg, Pollak and Wales44 have found that when Britain substituted child benefits paid to mothers for an income tax deduction received by fathers (in most cases), family expenditure patterns changed measurably, with more money being spent on children’s and women’s clothing.

According to a C.D. Howe Institute study, a $2000 exemption for each dependent child would cost the federal government about $3 billion.45 The author estimates that when the introduction of this child exemption is accompanied by a reduction in the CCTB and GST credit clawback rates (from current levels to 7.5 percent), the greatest gains from this proposal would be for families with incomes between $25,000 and $50,000. It is clear that without any change in the CCTB and GST clawback rates, the greatest beneficiaries would be those facing the highest marginal tax rates. There is no intrinsic connection between the reinstatement of a child exemption, on the one hand, and reductions in the CCTB and GST credit clawback rates, on the other. Therefore, one can ask this: Why not simply consider a proposal where reduced marginal tax rates and greater benefits to moderate-income households can be achieved independently of any child exemption proposal?

The Sub-Committee on Tax Equity for Canadian Families with Dependent Children has recommended the following:

The government should consider introducing a new refundable tax credit under the Canadian Child Tax Benefit to be available to parents who provide direct parental care. We believe that such a measure would improve the equity of the tax transfer system and provide recognition of the value to society of child rearing.46

There are many possible ways to deliver a credit for direct parental care. For example, the supplement for every child under the age of seven, available in the current CCTB to families that do not incur childcare expenses, indirectly credits parental care, although the amount is meagre (up to $213). The Sub-Committee opted for another approach:

Another possibility to improve horizontal equity is to deliver a non-taxable benefit only to those parents who give up market income and employment opportunities to raise children. In such a case, the benefits would be restricted to parents who forego earned income. A parent could, for example, be eligible for a benefit for each eligible child for every month the parent had no earned income. The amount could be linked to the value of the benefit currently provided by the CCED. Additionally, it could be delivered as part of the CCTB but not be subject to the familyincome test. The Committee believes this would provide some equity for parents who provide direct parental care.47

This approach targets parents without earned income, rather than parents without childcare expenses. This is a poor direction for policy reform for several reasons.

First, it confounds labour market decisions and childcare choices. Many dual-earner couples provide only direct parental care and do not make use of childcare services: nurses who work nights and weekends while their partners care for the children; parents who juggle their schedules so someone is always available to pick up their children after school; or parents who run home daycare centres are just a few examples. One the other hand, some parents without earned income — students, unemployed parents actively looking for work, parents with health problems, or parents who may not report their earnings — do make use of either formal or informal types of childcare services. Yet other parents sacrifice considerable amounts of income, without reducing their earnings entirely to zero, by replacing full-time employment by parttime work to care for their children.

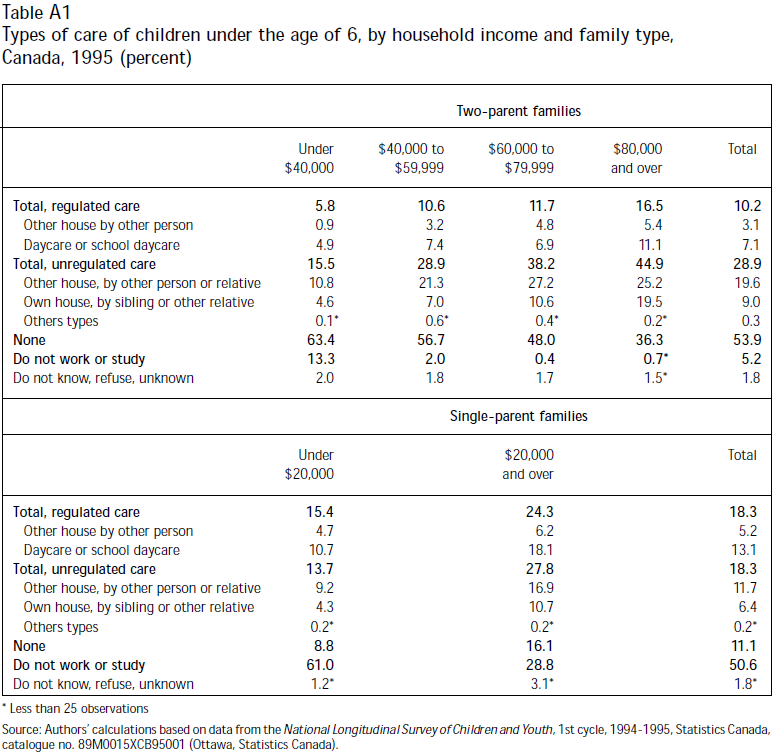

Paying benefits to parents without earned income is thus an indirect and often inaccurate way of targeting those providing direct parental care. Moreover, such measures would do nothing to help families where grandparents or other relatives look after the children. From an examination of data from the National Longitudinal Survey of Children and Youth (NLSCY), Baril, Lefebvre and Merrigan48 conclude that government policies have to show sufficient flexibility to support a variety of childcare arrangements. For instance, their analysis reveals that 25 percent of two-parent, two-earner Quebec families with preschool children did not use any formal (daycare centre, school daycare or other regulated childcare service) or informal type (unregulated childcare services, child care by relatives or other persons) of child care in 1995. Informal childcare arrangements are particularly important among families with young children and low-income families. Based on the same data from the NLSCY, we found that 59.1 percent of two-parent Canadian families with pre-schoolaged children (and 61.7 percent of single mothers) did not use any formal or informal type of child care in 1995. These figures rise to 76.7 percent for two-parents families with annual incomes under $40,000 and 69.8 percent for single mothers with income below $20,000.49

Second, providing benefits only to parents who forego earned income reinforces a traditional division of labour. Supporting parents who provide direct care for their children is a worthy goal of a family policy. However, there is strong empirical evidence showing that women who drop out of the labour force to care for their children face a lifetime of lower earnings and worsened employment prospects.50 Favouring parents who choose to provide direct parental care is no better than favouring families in which both parents work at regular nine-to-five jobs and child care is provided by accredited centres, as is done under the Quebec programmes. Again, policies that are more neutral toward personal choices enhance efficiency and provide more options to parents, allowing a balance of work and family life while promoting flexibility and choice.

Third, it raises the “welfare wall.” Paying benefits to people without earned income raises the attractiveness of welfare relative to work. Lone mothers are more likely to be stay-at-home parents than are married women. In 1998, 69 percent of married women with pre-school-aged children worked outside the home, as compared to 53.9 percent of lone mothers. In the case of mothers with children under the age of three, the difference in participation rates is even greater: 67.2 percent of married women worked outside the home and just 44.4 percent of lone mothers.51 Increasing payments to those lone mothers without earned income would make the transition into the work force all the more difficult. Even for families not on social assistance, a benefit lost when a parent enters the labour market raises that parent’s effective marginal tax rate.

Fourth, families with a stay-at-home parent already enjoy significant tax advantages. As mentioned before, over 75 percent of all CCTB go to one-earner families (including single-parent families) while they account for less than 50 percent of all families; they receive spousal or equivalent to-spouse credits; and the value of their household production is not taxed. We will return in more detail to this latter argument in following sections of this paper.

The final and perhaps most convincing argument against a direct parental care credit is that it would not address the major problems with the current system: a lack of recognition for caregiving responsibilities in middle-income families and high effective marginal tax rates created by targeted benefits.

A compromise proposal would be to provide a refundable tax credit to all families. To achieve the same positive results as a child exemption and avoid increasing effective marginal tax rates, this refundable credit should not be subject to benefits clawback at higher income levels. Such a credit would avoid the major disadvantages of both the child exemption and credits for direct parental care proposals. The cost of the proposal would clearly depend on its exact parameters. To illustrate, the proposal of a non-refundable tax credit of $2,000 per child put forward by Poschmann and Richards52 is estimated to cost $1.7 billion. If this credit were to be made refundable as opposed to non-refundable, the cost estimate of such proposal could increase to about $2.5 billion.53 In comparison, the cost estimate for a $2,000 exemption for each dependent child is in the neighbourhood of $3 billion.54

Although the introduction of a refundable credit available to all Canadian families would considerably improve the tax treatment of children in Canada, it would not address one of the major problems with the current system: it would do nothing to reduce the high effective marginal tax rates faced by families with net incomes between $20,000 and $30,000. For this, one needs to reform the structure of the CCTB programme. The next section discusses the proposal for universalizing child benefits.

None of the proposals discussed so far address the two major problems with the current CCTB: high effective marginal tax rates and inaccurate targeting. A reform that would address these two major problems and still incorporate the advantages of previous proposals would be to universalize the child benefits.

The essence of all universalizing proposals is a change in the structure of the CCTB clawback rates. Many options are possible. The most expensive would be to completely eliminate clawbacks. A less radical option would be to reduce the benefit clawback rates, particularly in the $20,000 to $30,000 family income category. Finally, it would be possible to end the clawback of benefits at a level that guarantees all children access to some minimal level of benefits. These last two options could be achieved in a simple and straightforward fashion by converting either the NCB supplement or the base benefit of the CCTB into a universal benefit.

There are advantages to universalizing child benefits. First, all families would be guaranteed some recognition of the cost of raising children. At the very least, universal benefits would enhance horizontal equity between those who have children and those who do not, acknowledging that a family with children requires more income than one without to achieve the same standard of living. Family equivalence scales could serve as a guiding principle to determine the level of benefits.

Second, universal child benefits could increase economic efficiency. Universalizing the NCB supplement would lower effective marginal tax rates by over 25 percentage points for those facing the highest clawback rates. Approximately 440,000 families with incomes in the $20,000 to $30,000 category would see their effective marginal tax rates reduced by universality, while 2.7 million families with incomes greater than $30,000 would receive a lump-sum gain without any direct effect on marginal tax rates.55 Universalizing the base benefit, as well as the NCB supplement, would reduce marginal tax rates for the 80 percent of all Canadian families that receive the CCTB.