Redesigning Canadian Trade Policies for New Global’s Realities

Overview of the Research Findings

Stephen Tapp, Ari Van Assche and Robert Wolfe

In the 2016 budget, the newly elected federal government announced its goal to build Canada into a centre of global innovation. Over the next few years, the government intends to develop a bold, new innovation agenda to help achieve this objective. This report contributes to the policy discussion by identifying key elements that should be part of the government’s approach.

The departure point is a review of the 2011 Jenkins Report (Innovation Canada: A Call to Action, Review of Federal Support to Research and Development – Expert Panel Report), which recommended various ways to streamline and improve federal research and development (R&D) policies, with an emphasis on accelerating the growth of dynamic small and medium-sized enterprises.

Most Jenkins Report recommendations have been at least partially implemented — and they may be helping at the margin — but this report argues that our current policy approach is failing to stimulate widespread innovation-driven business strategies in Canada. This is because we have been dealing primarily with the symptoms rather than the causes of Canada’s underachievement. Weak business R&D is best understood as the outcome of our current “low-innovation equilibrium.” Paradoxically, this outcome has often been aided by the very microeconomic policies that have been purported to nurture Canadian business development, including those related to taxation, competition, trade and investment. The lack of serious, sustained competitive pressures in many key sectors of the Canadian economy has made it rational for businesses to underinvest in a range of riskier innovation activities, including R&D.

After having largely exhausted 40 years of gains derived from labour market growth, Canada-US economic integration and resource rents, maintaining the status quo is no longer viable. The increasingly competitive global marketplace — with the potential for a “fourth industrial revolution” — may soon overwhelm Canada’s comfortable equilibrium at a time when innovation-driven productivity improvements are the best, sustainable source of future growth.

In these circumstances, the government’s desire to underpin Canada’s future economic performance with a renewed innovation agenda is undoubtedly the right policy inclination. But to be successful, this agenda must go beyond the traditional focus on R&D. It requires a smart combination of microeconomic carrots and sticks to create a more comprehensive, pro-innovation business climate in Canada. Key elements of this approach would include the following:

Andrei Sulzenko is a public policy consultant, specializing in microeconomic, innovation, and trade and investment issues. He is an executive fellow at the School of Public Policy, University of Calgary, where he is leading a research program on transportation infrastructure. He worked for the federal government from 1972 to 2004, and as senior assistant deputy minister of policy at Industry Canada from 1996 to 2004 he led the federal government’s science and technology and innovation policy development. He was also a fellow and adjunct professor at the School of Policy Studies, Queen’s University.

The author would like to thank the IRPP for research support and input in drafting this report, provided by David Deault-Picard and Stephen Tapp, and to acknowledge helpful comments from the following reviewers: Peter Nicholson, Bev Dahlby and Rob Dunlop. The views in this report are those of the author, who is responsible for any errors or omissions.

The IRPP would like to thank the Business Council of Canada, whose financial support helped cover some of the costs of this project.

Canada’s innovation performance has been studied and debated for decades. An early milestone in this process was a comprehensive review of research and development (R&D) by the Senate Special Committee on Science Policy, which concluded the following:

Since 1916…the main objective of Canadian science policy has been to promote technological innovation in industry…Almost every decade since the 1920s has witnessed renewed attempts by successive Canadian governments to achieve it, but on the whole they have all failed.1

Periodic reviews by the federal government and outside advisory bodies, such as the Organisation for Economic Co-operation and Development (OECD) and Council of Canadian Academies, continued throughout the 1990s and 2000s as poor business innovation persisted, notwithstanding generous R&D tax credits and a growing array of direct incentives.

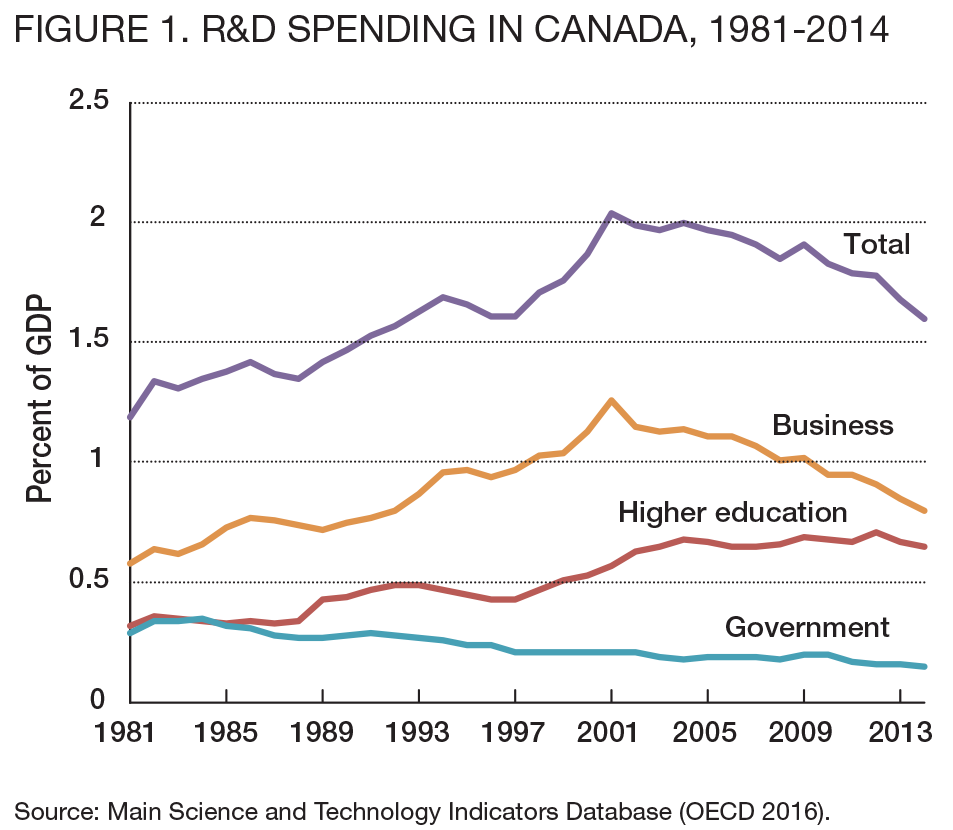

When the previous government decided in 2010 to initiate a new inquiry, total R&D spending in Canada as a share of GDP was in decline after having peaked in 2001, as the high-tech bubble began to burst. The retrenchment of total R&D spending was mostly due to falling business R&D spending, which has been an important long-standing proxy for innovation performance (figure 1).

The Independent Panel on Federal Support to Research and Development (Expert Panel) was chaired by Tom Jenkins, executive chairman of Open Text Corporation, and supported by a group of eminent business and academic members.2

The Expert Panel submitted its report in the fall of 2011.3 During the almost five years since the Jenkins Report there have been four Conservative government budgets and one Liberal government budget.

In Budget 2016, the new Liberal government undertook to develop an “Innovation Agenda.” As the Finance Minister underlined in a press conference: “Our objective of growing the economy is fundamental to us, and our innovation agenda is critical to that…We’re setting ourselves up for a long-term innovation strategy.4

It is timely, therefore, not only to assess the impact of the Jenkins Report on innovation policy over the last five years, but also to offer policy advice for the proposed innovation agenda. In doing so, this report is divided into three main parts:

The Jenkins Report contains a 104-page main text with a 14-page executive summary. Many readers likely stopped at the executive summary and focused on the six recommendations. A close reading of the report, however, demonstrates a unifying theme to the challenge of Canada’s poor innovation performance, an approach that was constrained somewhat by the relatively narrow mandate the Expert Panel received.

The mandate asked for “advice in respect of the effectiveness of federal programs to support business and commercially oriented R&D, the appropriateness of the current mix and design of these programs, as well as possible gaps in the current suite of programs and what might be done to fill them.”5 It also stipulated that the recommendations not result in an increase or decrease in overall funding for R&D initiatives.

Accordingly, the Expert Panel mainly focused on the mix between direct and indirect R&D program support. It did so, however, in the context of a broader view of innovation than R&D performance.

The Expert Panel’s analysis built on work by the OECD and the 2009 report by the Council of Canadian Academies, Innovation and Business Strategy: Why Canada Falls Short, to define innovation broadly as “the implementation of a new or significantly improved product or process, a new marketing method, or a new organizational method in business practices, workplace organization or external relations.”6 In other words, innovation was not just about R&D. It could be initiated anywhere in the value chain, often starting with customer demand.

Further, the Expert Panel recognized that most innovation takes place through adaptation of significant innovations originating elsewhere, but often requiring “substantial creativity to redesign business processes, organization, training and marketing to take advantage of the adopted innovation.”7

A final key observation underlying the Expert Panel’s approach was that government’s focus should be “to strategically target efforts to support the growth of innovative firms into larger enterprises…thereby allowing…the country’s business sector to achieve the scale required to become an innovation leader on the world stage.”8

These perspectives underlay the Expert Panel’s approach toward its mandate and help explain its recommendations.

The first recommendation was to consolidate virtually all business innovation programs across the federal government — some 60 in number — into one new organization to facilitate a whole-of-government approach.

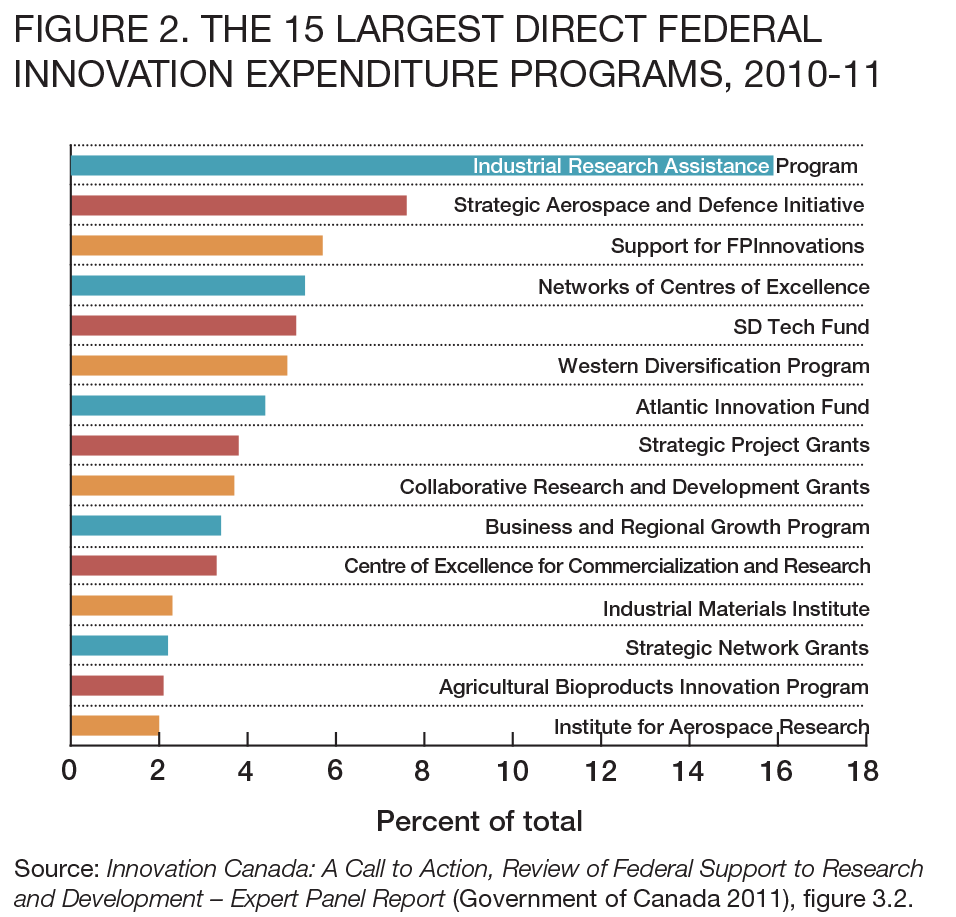

The proposed Industrial Research and Innovation Council (IRIC) would be an arm’s-length funding and delivery agency that would, over time, rationalize support into a smaller number of larger, more flexible programs, anchored by the National Research Council’s (NRC’s) Industrial Research and Assistance Program (IRAP). IRAP is the largest federal business R&D direct support program, amounting to over 15 percent of total direct support and focused on technical support to SMEs. Figure 2 shows the 15 largest programs at the time the Jenkins Report was written.

IRIC would also be responsible for several Expert Panel — recommended sub-initiatives — providing a national “concierge” service to provide companies with high-quality timely advice on access to business innovation assistance; developing a business innovation talent strategy focused on improving access to highly qualified personnel; and building capacity to assess program effectiveness and guide future resource allocation.

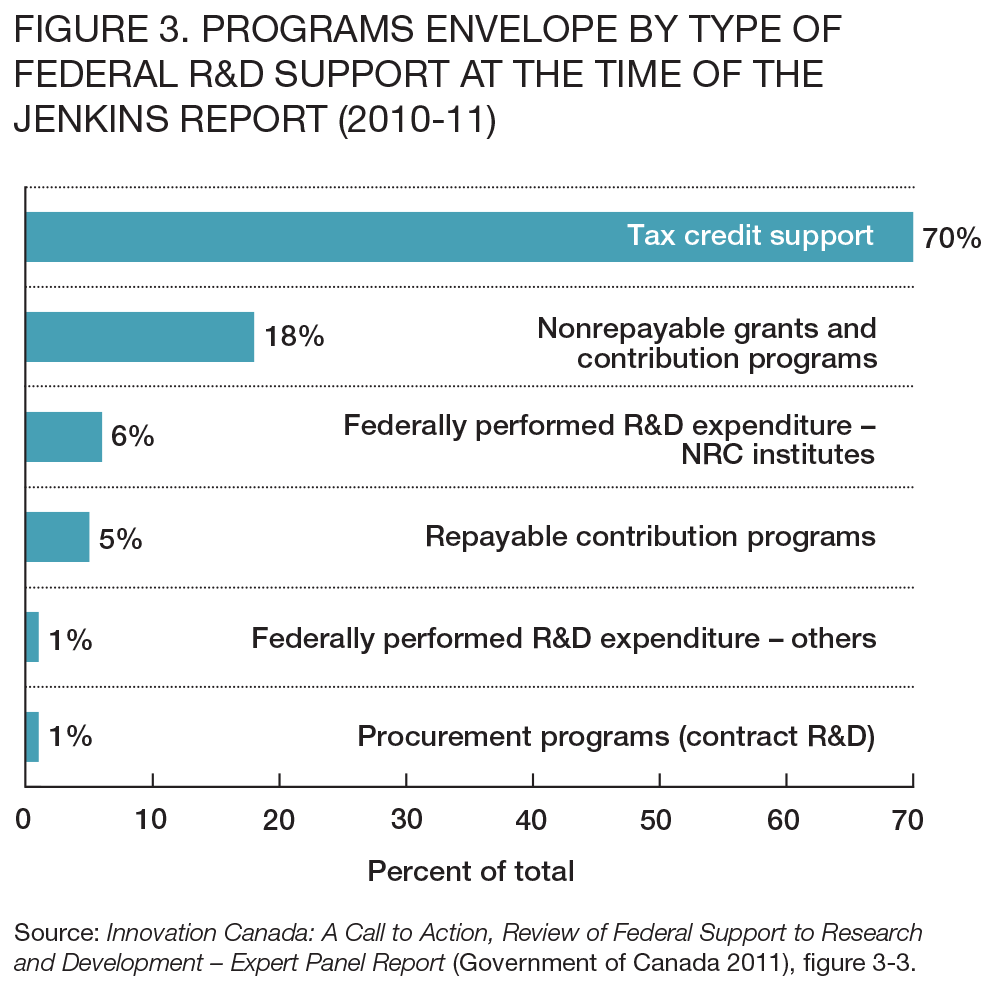

The second recommendation was to rebalance the relative weights of direct support to indirect support through the Scientific Research and Experimental Development (SR&ED) tax credit. The latter constituted 70 percent of total R&D support ($3.5 billion annually at the time, see figure 3), a considerably higher percentage than provided by our OECD counterparts, especially when additional provincial government tax credits are taken into account.

The Expert Panel proposed decreased support through the SR&ED tax credit for small and medium-size enterprises (SMEs) and the savings to be directed to complementary initiatives in other recommendations. This proposal was based on the view that “federal support for innovation may be over-weighted toward subsidizing the cost of business R&D rather than other important aspects of innovation.”9 The resulting savings would be used to focus more sharply and directly on the Panel’s strategic objective of growing innovative firms, the “gazelles,” into larger enterprises.

The specific recommendation was to simplify the SR&ED program by basing the tax credit for SMEs only on labour-related costs and no longer on overhead expenses, materials, capital equipment expenses, contracts and payments to third parties. In addition to saving money for redeployment to direct support, the proposal would reduce SME compliance and administration costs. The Expert Panel thought that switching to a labour-cost base for large firms also merited careful study and consultation, given the greater importance of material inputs and capital equipment.

Its third recommendation, which cited analysis by the OECD of the dearth of demand-side measures compared to the heavy reliance on supply-side programs, was that business innovation become one of the core objectives of government procurement, alongside the traditional value-for-money criterion. The Expert Panel felt strongly that this shift, along with supporting programs to create opportunity for leading-edge goods, services and technologies from Canadian suppliers, would help translate that home-grown start into global success.

Indeed, the Panel saw such merit in the potential of procurement as a demand-pull instrument — particularly to stimulate the growth of SMEs — that it produced a supplementary Special Report on Procurement, which was submitted soon after the main report.

The fourth recommendation sought to address Canada’s challenge of having suboptimal scale of public-private research activities. In the Panel’s recommendation to help develop globally competitive companies, it saw the NRC, with its already established base of 17 research institutes, as needing to transform the business-oriented institutes into a “constellation of large-scale, sectoral collaborative R&D centres involving business, the university sector and the provinces.”10

This recommendation, in conjunction with the first recommendation involving the transfer of its flagship IRAP to the proposed IRIC, as well as the transfer of basic and public policy research to universities and federal departments, would essentially repurpose the NRC into a series of independent, non-profit Frauenhofer-type corporations.11 These proposals would constitute the most radical change to the NRC since its creation a hundred years ago, in 1916.

The fifth recommendation was designed to address the risk-capital gap for innovation-focused businesses from start-up through to maturity, when public financial market access is not available. The Panel was of the view that “subscale size limits the ability of Canadian fund managers to follow firms through to maturity as the size of successive funding rounds increases,”12 adversely affecting financing opportunities for innovative firms. Accordingly, it recommended that the federal government facilitate access to an increased supply of risk capital in both start-up and late-stage financing through its Crown corporation, the Business Development Bank of Canada (BDC).

This recommendation, like number four, recognized that Canada’s small scale — particularly relative to that in the United States — created in effect a venture capital “infant industry” that merited further public support in order to enhance growth prospects for small, innovative firms, especially technology companies.

The sixth recommendation, like the first and fourth, focused on mandate or “machinery of government” issues, proposing that innovation policy responsibility be consolidated internally and policy advice externally on a whole-of-government basis, thereby facilitating a national dialogue on innovation involving provincial and business leaders.

In summary, the Jenkins Report made three broad mandate recommendations and three specific program recommendations.

The mandate recommendations were consistent with the prevailing view, certainly outside government, that greater discipline in roles and responsibilities, and a sharper, consolidated focus on priorities would allow for the more efficient allocation of scarce resources.

The program recommendations essentially sought to transfer resources from the SR&ED tax credit to direct R&D and other program support that could more effectively target high-growth SMEs. However, the Expert Panel did not analyze the plethora of R&D support programs and suggest their rationalization. Rather, it focused on augmented funding for two existing SME-support mechanisms – through IRAP and the BDC – and, in addition, a new SME-oriented initiative designed to promote innovation through government procurement.

It is fair to say that the Jenkins Report has had a significant impact on policy. The 2012 budget announced that, “the Government is committed to a new approach to supporting innovation that focuses resources on private sector needs.”13 By this it meant that incremental resources were being increasingly directed to helping business innovation, compared to the previous decade’s heavy investment in university-based research needs.

Consistent with the Report’s recommendations, substantial investments were made in early-stage risk capital and large-scale venture capital funds led by the private sector; support for companies under IRAP was doubled; additional funds were provided to the NRC for business-led, industry-relevant research; relatively smaller amounts were allocated for industrial R&D internships, business-led networks of centres of excellence and a procurement-related initiative, currently called the Build in Canada Innovation Program; and the SR&ED tax incentive program was to be streamlined and improved.14 In fact, the changes to the SR&ED program went beyond the Expert Panel’s recommendations by reducing the regular tax credit to 15 percent, from 20, (by 2014) and by removing for all claimants expenditures on capital equipment and on the profit component of contract spending. In total, these changes amounted to a $1.3 billion cut to the SR&ED program.

Budget 2013 followed with the same themes. Highlights included providing the NRC with funds to support the strategic focus of growing innovative businesses; providing the Canada Revenue Agency with funds earmarked for the improvement of predictability and enforcement of the SR&ED tax incentive program; funding to allow “incubator” and “accelerator” organizations to expand services to entrepreneurs and for the BDC to invest in firms graduating from business accelerators; and providing additional funding to federal granting councils in support of research partnerships with industry.

By the time Budgets 2014 and 2015 came around, much of the response to the Jenkins Report was completed. Aside from increased funding in 2015 for the NRC’s industry-partnered R&D activities, by then the government had adopted more of a sectoral focus, such as increased funding for the Automotive Innovation Fund and new aerospace supplier initiatives.

In 2014, the federal government released an update of its 2007 science and technology (S&T) and innovation strategy. In this update, it highlighted the impact of the Jenkins Report on innovation policy:

Informed by the recommendations of the Panel, Canada’s Economic Action Plans 2012 and 2013 were built around a new approach to promoting business innovation – one that emphasizes business-led initiatives and focuses on fostering the growth of innovative firms…Our government implemented policy changes to provide a more comprehensive and coordinated suite of business innovation support programs focused on industry needs. We also removed obstacles and barriers to innovation, and addressed gaps in the current program and policy mix.15

The elements of the Jenkins Report that were not adopted by the federal government were the “machinery” recommendations — namely, to establish a new Industrial Research and Innovation Council that would consolidate R&D programs, including the NRC’s IRAP; and to transform the existing Science, Technology and Innovation Advisory Council into an external advisory committee to provide whole-of-government advice. This is not surprising since there have been very few machinery-of-government changes at the federal level for more than 25 years, and as a sole prerogative of the prime minister, external advice on machinery has generally not been followed.

One such recommendation has, however, been partially implemented — the proposed transformation of the NRC’s institutes into business-oriented, large-scale collaborative research centres and the transfer of public policy–related research to other federal agencies. In this regard, the government announced in May 2013 that the NRC would consolidate its disparate operations into a dozen business units, focusing on five core areas of research: health, manufacturing, community infrastructure, security, and natural resources and the environment.16 It is difficult to determine, on the basis of publicly available information, whether these changes are designed to emulate the model of the well-known Frauenhofer operations in Germany involving cost-shared research for industry clients.17

The new Liberal government’s approach

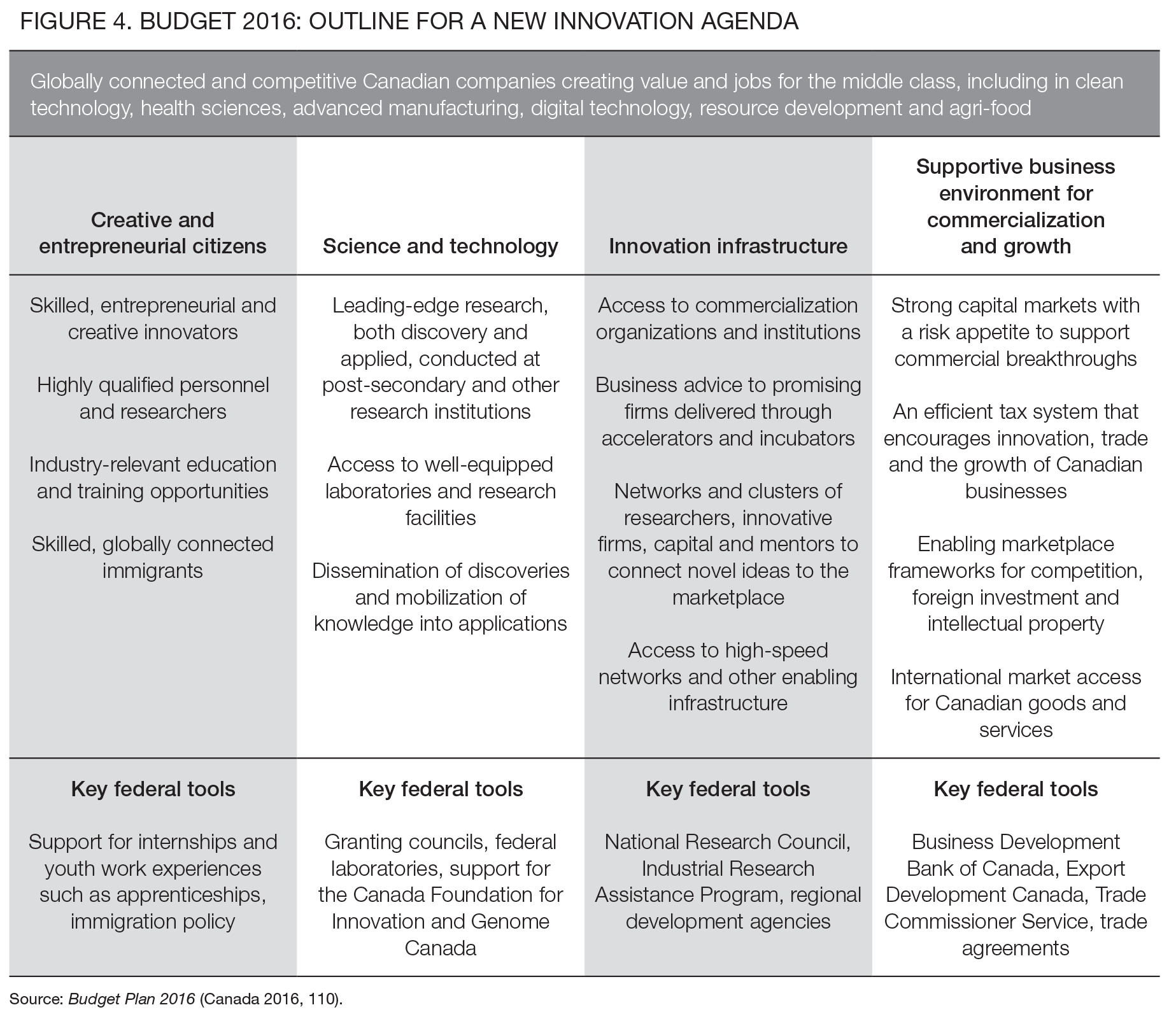

The new Liberal government quickly signalled the importance it placed on innovation by changing the name of Industry Canada to Innovation, Science and Economic Development Canada. Shortly thereafter, Budget 2016 announced the “Innovation Agenda” as a cornerstone of a long-term growth strategy for Canada (figure 4). The budget plan made the following undertakings:

In many respects this “plan to make a plan” is a prudent approach to a complex set of issues, especially after only a short period in office. As a result, it offers little insight into the key elements of an Innovation Agenda.

The budget did, however, announce significant investments in “strengthening science and research,” notably,

Specifically, with respect to business innovation, the budget took some “interim actions to support innovative and growth-oriented businesses in reaching their potential and to help firms put innovation at the core of their business strategy.”19 These included the following:

In terms of antecedents to these last two initiatives, the concept of innovation networks/clusters has deep roots in the business literature;20 and governments have made various attempts over the years at promoting them. Although not specifically advocated in the Jenkins Report, its philosophical thrust is consistent with promoting networks/clusters, as it saw the scaling up of high-growth firms as a key driver for improved innovation performance.

Similarly, the initiative of providing coordinated services to firms is consistent with the Jenkins Report’s recommendations for concierge services through a consolidated, whole-of-government approach.

These specific budget initiatives demonstrate some level of continuity in innovation policy thinking, while the broader plan to develop an innovation agenda suggests there is scope for new directions.

While there have been several changes in innovation policy since 2012 — changes that are generally consistent with the Jenkins Report’s recommendations — it is still too early to judge whether these changes are making a positive difference. In general, any impacts (positive or negative) will only gradually show up in the statistics and, even then, it is a heroic exercise to demonstrate causality. Furthermore, in terms of keeping governments accountable, in the past the auditor general has tried and failed to measure value for money for innovation expenditures.21 Another challenge in assessing the impact of various innovation policy initiatives is that whichever political party forms the government of the day will naturally place its policies in the best possible light. In addition, there is only a tiny academic community in this country that studies innovation policy and scant media attention is paid to these issues (except for a few business columnists, and even then, such complex issues do not make for scintillating copy). In short, we really don’t have great knowledge of what works and doesn’t in innovation policy, specific to Canada.

This section, therefore, comes at the issues indirectly — that is, I do not attempt to assess the impact of Canada’s innovation policy, but instead ask a more fundamental, prior question: Is our policy mix actually addressing the reasons for long-standing poor innovation performance? My thesis is that it is not and, specifically, that there is currently too much emphasis on R&D support relative to other policy initiatives.

To explain this thesis, I will take readers back to some basic questions: How is innovation measured? Why has Canada’s performance been poor? And why does this poor performance matter? On the basis of this analysis, I will outline emerging market-driven catalysts for innovation and the way our traditional innovation model needs to be redefined.

Studies undertaken over many years by research groups in Canada and abroad reveal that Canada’s innovation performance has been lamentably poor.

One prominent organization is the Conference Board of Canada (CBOC). It periodically produces a document that measures Canada’s performance on the economy, innovation, environment, education and skills, health and society against OECD peer countries’ performance. In this report card, innovation has consistently been Canada’s lowest grade — most recently receiving a “C,”22 with performance assessed on 10 indicators.23 The CBOC ranked Canada 9th among 16 peer countries. Among the recent developments, the CBOC notes:

Note that virtually all the indicators are essentially inputs to the innovation process — such as R&D and patents — not really measures of outcomes. The same observation applies to reports by the federal government. In its 2014 update of a 2007 strategy document, it reinforces this input-centric approach to assessing innovation performance, recognizing that “while measuring innovation is difficult, R&D spending is one way to gauge a country’s commitment to it.”24 As a result, much of the analysis and consequent policy debate on innovation has focused on improving input performance, especially R&D.

A more instructive way of measuring innovation performance is to come at it from the other end, by disaggregating productivity statistics. Productivity consists of three interrelated elements: the quality of labour; capital intensity; and a residual known as multifactor productivity (MFP). MFP is a proxy for innovation. It is essentially about how well businesses combine labour and capital with know-how.

In a 2013 study, the Council of Canadian Academies came to the following conclusion on the importance of MFP as a metric:

MFP is a key statistic because it is a measure of outcome, as well as of innovation in the broad sense and not just its technological aspects. Virtually all other commonly reported indicators of Canadian business innovation (e.g., R&D; patenting; investment in machinery and equipment, especially in ICT) point in the same direction as the MFP statistics. But these other indicators are more limited since they are either inputs to, or intermediate stages of, the innovation process, and, with the notable exception of ICT, are relevant principally to certain sectors like manufacturing and its related knowledge-based services.25

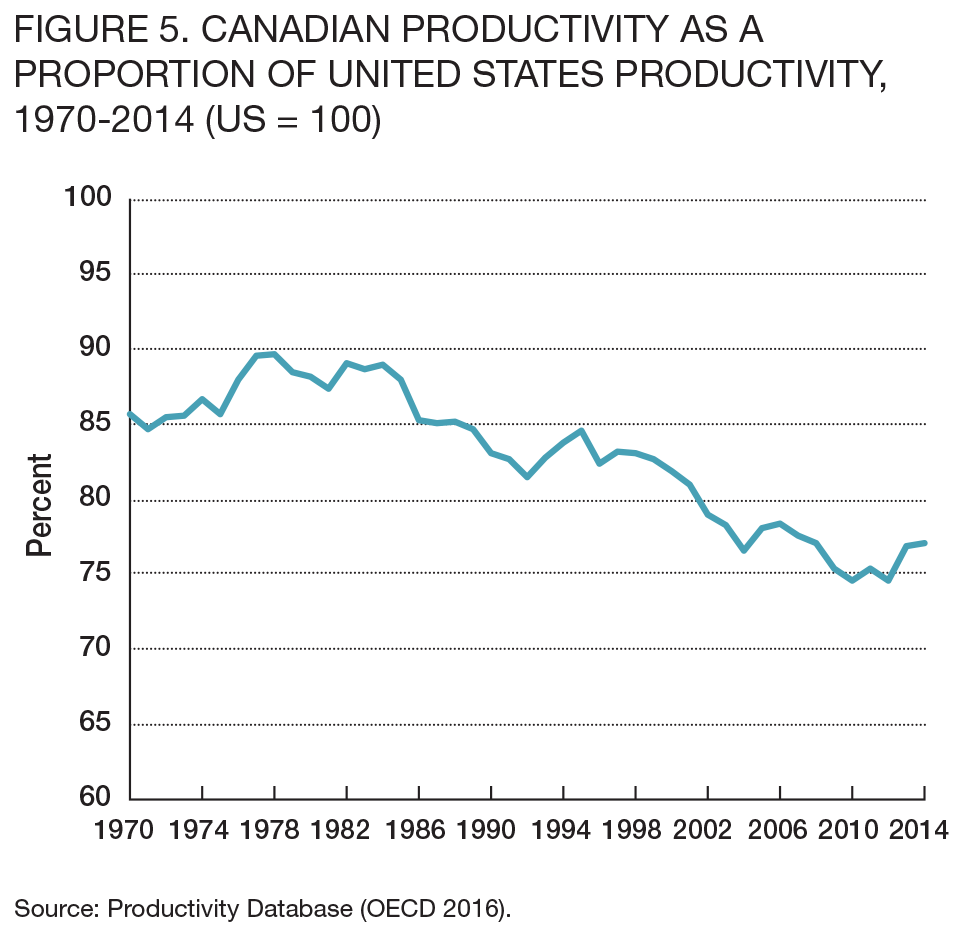

The challenge with MFP is its measurement, in terms of both methodology and data. On the basis of the officially reported statistics, Canada’s MFP performance record is dismal, especially compared with that in the United States. While our overall productivity gap was as close as 10 percent in the 1970s and 1980s, it has grown to about 25 percent more recently (figure 5),26 and virtually all of that deterioration is attributable to MFP. Over a 30-year period until 2011, the quality of labour and capital intensity increased at about the same rate in Canada as in the United States, but MFP grew by only about a fifth of the rate in the United States.27 That is why the Expert Panel, citing earlier work by the Council of Canadian Academies, concluded in its Report that “Canada’s subpar productivity growth is largely attributable to relatively weak business innovation.”28

Recent research on MFP comes to less dramatic conclusions than those derived from official data, suggesting that between 1961 and 2011 MFP growth averaged 1.03 percent compared with the Statistics Canada estimate of 0.28 percent.29 Beyond that headline, however, much of the difference is accounted for in the 1961-1973 business cycle; in more recent business cycles, MFP growth has been poor: 1.12 percent per year from 1981 to 1989; 1.02 percent from 1989 to 2000; -0.04 percent from 2000 to 2008; and -0.02 percent from 2008 to 2011. Over comparable periods, therefore, the results are similar.

The CBOC and others have puzzled for some time over the question why Canada’s performance has been poor.30 For example, a recent CBOC report on innovation makes the following observation:

Many explanations for poor innovation performance have been proposed over the years by academics, industry groups, think-tanks, and government bodies. But these studies have been limited by a lack of sufficient data and information. Consequently, more conclusions have been reached based on beliefs and opinions than on actual evidence.31

Certainly the answer does not lie in a lack of R&D incentives or because of high corporate taxes, or an otherwise unfavourable business climate. On these indicators, Canada has among the best records of OECD countries.

Much of the answer may actually be quite simple. As the Council of Canadian Academies has recently concluded, “Canadian firms have been as innovative as they have needed to be.”32 By this they meant that Canadian business has been able to prosper over a sustained period of time without having to develop riskier innovation-based strategies.

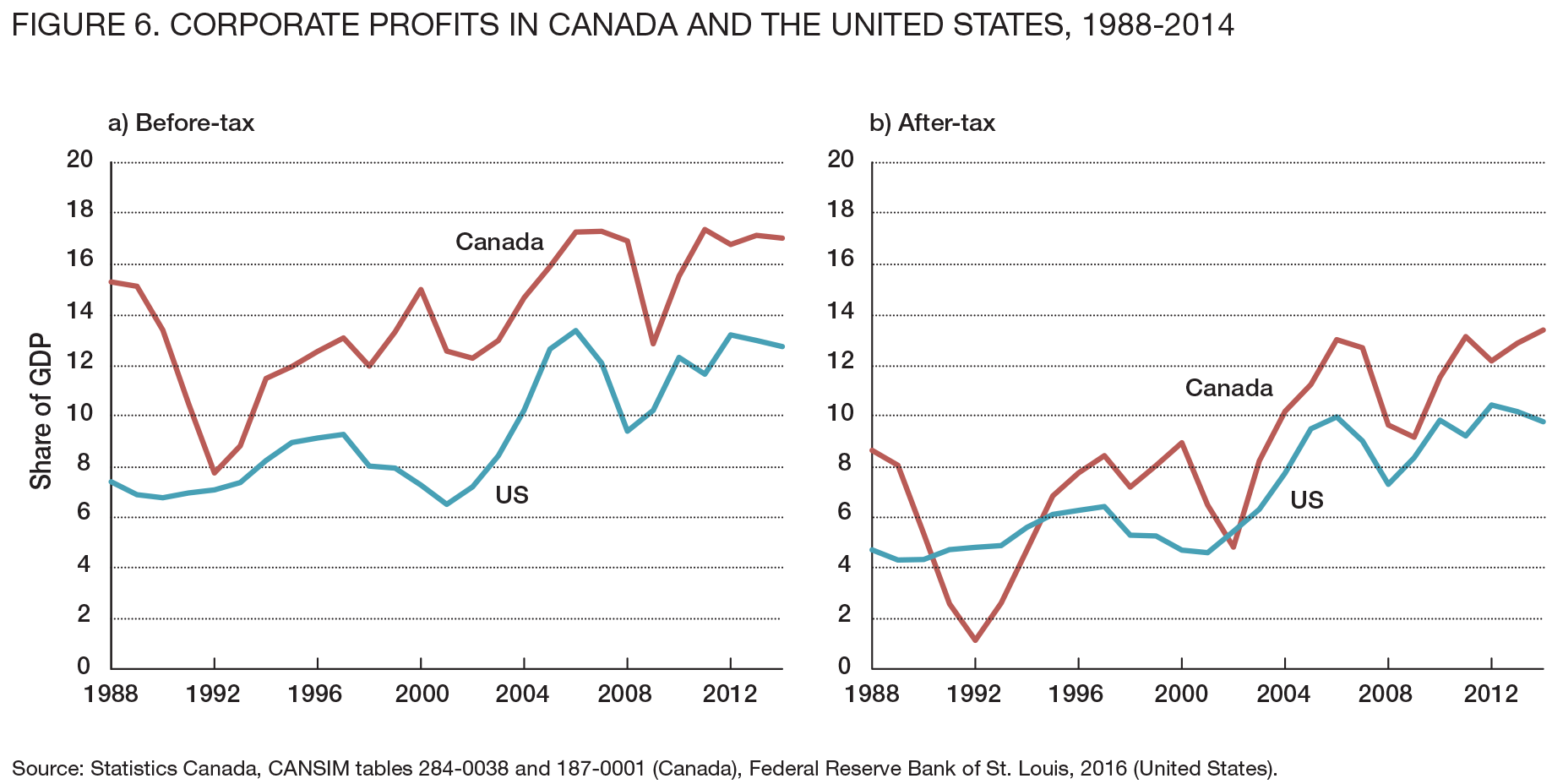

The evidence for this lies in an earlier study on business innovation by the Council. It found that a key measure of business success, aggregate corporate profit as a share of GDP, has generally been higher in Canada than in the United States.33 More recent data confirm that this situation has endured (figure 6). Before taxes, corporate profits as a share of GDP were higher in Canada than in the United States every year from 1988 to 2014, with an average annual difference of 4.5 percentage points (13.9 percent in Canada versus 9.4 percent in the United States).

Importantly, even after taking corporate taxation into account, these general findings appear to hold. The main exception to this basic pattern for after-tax corporate profits is found in the early 1990s recession, which was much deeper and longer in Canada than in the United States. Regarding the tax rates, combined federal and provincial tax rates in Canada were about 26.5 percent in 2015, roughly in the middle of the pack among OECD countries, while the United States remained a clear outlier at 40 percent.34 It should be noted, however, that measuring effective tax rates is complicated by the ability of transnational corporations to minimize their overall tax burden.

It is ironic that Canada’s push for corporate tax competitiveness — by lowering tax rates and, in effect, raising after-tax rates of returns — may have had the unintended -consequence of decreasing the pressure on Canadian business to adopt innovative strategies. However, the inconvenient truth goes beyond taxation. Compared with other jurisdictions, particularly the United States, Canadian businesses have had less competitive pressure to stimulate innovative responses in many sectors of activity. For example, we have key enabling sectors that are also a cost input for other businesses, which continue to enjoy oligopoly status, such as telecommunications, financial services and transportation. Public policy measures also continue to enhance the profitability of other significant sectors, such as agriculture, or to sustain “pay to play” sectors, such as aerospace and automotive.

It goes beyond the scope of this report to debate how these legacy policies should be reconsidered in the interests of spurring innovation. However, the report of the 2008 Competition Policy Review Panel, of which Tom Jenkins was a member, made a number of recommendations on competition and foreign investment policy that still have not been addressed.35

Trade is another important policy area that has an impact on innovation performance. In theory, trade liberalization will spur innovation through increased competitive pressure.36 Indeed, Baldwin and Yan (2015) find evidence of a link between trade intensity and aggregate business sector productivity in Canada (figure 7), and they demonstrate that trade and trade-enhancing policies have improved the productivity performance of the manufacturing sector.37

Despite long-standing multilateral agreements under the World Trade Organization (WTO) and the as-yet unrealized potential of new regional and bilateral agreements — such as the Comprehensive Economic and Trade Agreement with the European Union and the Trans- Pacific Partnership — Canada’s main economic relationship remains with the United States.

The North American Free Trade Agreement (NAFTA) has created an integrated North American economy dominated by US firms, with Canada as primarily an upstream, more commoditized supplier that largely acquires rather than creates innovation. Many firms in this relatively comfortable and stable environment have settled into what the Council of Canadian Academies call “a low innovation equilibrium” in which ambition beyond the US market is not deemed necessary.

Arguably, this ambition is further cushioned by the current low value of the Canadian dollar, which allows profit maintenance or enhancement for Canadian firms. As shown above, however, the opposite situation of a Canadian dollar hovering around parity during the 2010-2014 period does not appear to have had a negative impact on profitability.

Overall, it is difficult to isolate the impact of the exchange rate from other factors that affect corporate decision-making. As a general observation, however, the more integrated that supply chains in the two economies become and, with that, the more that intermediate goods and services flow in both directions, the less direct impact the prevailing exchange rate has. By way of example, a historical rule of thumb in the automotive sector is that components and subassemblies cross the border about seven times before final assembly into a vehicle.

If one accepts that Canadian business has, over an extended period of time, been only as innovative as it needs to be, does this matter? After all, a preference for low-risk, comparatively high-return investment is a completely rational response to our competitive situation.

The problem is that the “good old days” of relatively easy growth are over, while complacency remains. Why this is the case is somewhat complicated, but the logic of the argument is as follows:

In conclusion, then, improved innovation is the only sustainable source for Canada’s future economic growth.

The most efficient incentives for businesses to shift to innovation-based strategies are market-driven. If in the past Canadian businesses were only as innovative as they needed to be, in the future they will need to respond to new competitive pressures.

The Council of Canadian Academies noted in a 1972 quote from the CEO of Northern Electric:

It is uncertain whether any incentive plan to stimulate the growth of domestic technology and innovation, or to make corporations expand aggressively into foreign markets, can achieve significant success when it is applied to companies in which the drive to do these things has not already been forced to emerge because of exposure to a real stimulus from the economic environment. What we seem to need in Canada are “small catastrophes.”40

The Canadian oil industry offers a good recent example of the counterintuitive positive impact of a small catastrophe. Reinforcing pressures from the crash in the price of crude oil, higher cost production requirements for nonconventional sources in the oil sands and widespread public concerns about negative environmental impacts have spurred Canadian companies not only to cut costs but also to reposition their output in the marketplace with serious efforts to reduce emissions — what is known as de-carbonization.41 A former oil sands executive provides the following summary:

When you are the producer of the lowest-cost oil (such as Saudi Arabia), you don’t have the burning platform to innovate that you do if you’re at the high end of that curve…We have much greater urgency and much greater importance of innovating our way into the future. That innovation will lead to benefits in technology development and expertise. Carbon competitiveness is an important dimension of future success.42

The academic business literature is replete with similar cases of the cause and effect between competitive pressure and innovation. Indeed, going back more than 40 years, Michael Porter of the Harvard Business School outlined in his seminal treatise the dynamics of competition on innovative performance.

A nation’s competitiveness depends on the capacity of its industry to innovate and upgrade. Companies gain advantage against the world’s best competitors because of pressure and challenge. They benefit from having strong domestic rivals, aggressive home-based suppliers, and demanding local customers.43

Now, a new wave of business thinking suggests that the accelerating speed of technological change is creating a Darwinian world of winners and losers. A recent monograph by Klaus Schwab, Founder and Executive Chairman of the World Economic Forum, outlines the likely impact of a “fourth industrial revolution.”44

In this typology, the first, second and third industrial revolutions were, respectively, agrarian, manufacturing and information and communication technologies (ICT). The ICT revolution is still playing out as these technologies embrace increasingly sophisticated robotics, big data and advanced analytics, the Internet of Things and artificial intelligence. The fourth revolution takes off from the third but is wider in scope with breakthroughs in areas ranging from gene sequencing to nanotechnology.

As Schwab summarizes it, “It is the fusion of these technologies and their interaction across the physical, digital and biological domains that make the fourth industrial revolution fundamentally different from previous revolutions.”45

Although still speculative as to speed and direction, these changes will have a profound impact on the basis for future competition among advanced economies. It will clearly be innovation-driven, in an increasingly flexible, sophisticated and inter-disciplinary, but often disruptive, way.

How well will Canadian business respond to the challenge? At one level, business will be forced to move quickly and effectively from its relatively low innovation starting point, or face steeply declining prospects in previously stable markets like financial services, as well as in new, high-growth markets like artificial intelligence. Furthermore, governments will be less able to insulate industry from competition that involves relatively less traditional trade in goods and relatively more trade in services (services that can be delivered digitally or via foreign affiliates that can provide a local presence in faraway places).

At another level, a focus on maintaining current shares in the mature market segments of commodities and cost-competitive manufactured products is not only a recipe for low growth, but also a potentially risky strategy as emerging economies compete increasingly in that space — for example, witness the massive gains that China has enjoyed since it joined the WTO in 2001, particularly in the US market, or Mexico’s growing market share in the automotive sector.

Although Canada’s innovation challenge has long been recognized, with public policy focused on the proxy of weak business investment in R&D, there has been a relative lack of serious analysis about what has really been going on or a truly ambitious government response to these issues. The most important analytical contributions have probably been a series of studies by the Council of Canadian Academies, a number of which are cited in this report.

The public debate has nevertheless remained largely ill-informed, aided and abetted by the politically palatable convenience of equating improved innovation performance with increased R&D spending rather than a more complex interplay of difficult public policy issues.

Furthermore, it has been in many stakeholders’ interests to portray the challenge in these terms. This has been the case for academic researchers, to the point that Canada stands at the top of OECD countries in terms of public support for university-based research as a percentage of GDP. It has also been the mantra of the private sector, whether it is for generous R&D tax credits or for sector-specific R&D programs that help level the playing field with competitor jurisdictions.

As a result, successive governments, while bemoaning our poor innovation performance, have continued to look to the same purported solutions to the challenge — namely, more or better R&D support. Indeed, that view underlay the mandate given to the Jenkins Expert Panel.

Before we move on, it is important to distinguish between public support for basic research, usually at the university level, and industry support for more applied R&D. The former has been demonstrated to have important “public good” benefits, including the critical training of highly qualified personnel. The latter benefits mainly recipient firms, but the translation into innovative outcomes is much more difficult to demonstrate.

Furthermore, the argument for favouring more and better business R&D support is too simple. It is based on a linear model of innovation — basic research leads to invention (often patentable), which in turn moves on to development and engineering, and then to product commercialization. The linear model was more applicable in the past when large corporate R&D facilities fed a pipeline of products, though it still has some application today in a few sectors such as pharmaceuticals and aerospace, in which huge upfront costs are incurred before any financial return is realized.

Most businesses in a modern economy do not operate on that kind of scale, with the attendant multi-year risks. In many sectors, speed and agility, supported by ICTs, are the keys to success, with innovation often starting on the demand side — identifying market opportunities and creatively developing business strategies, sometimes disruptive, to take advantage of those opportunities. This is the “skate to where the puck is going” approach.

R&D, as traditionally conceived is not necessarily a key feature of this approach. Indeed, the Council of Canadian Academies estimates, on the basis of work carried out by the OECD, that “roughly 80 percent of most modern economies involves firms that perform little or no R&D, yet many of them innovate in terms of business models, processes, marketing, and organization.”46

The Expert Panel recognized this paradigm shift, implicitly agreeing with the Council of Canadian Academies’ assessment that “Canada’s low business R&D spending is a symptom rather than a cause of weak business innovation.”47 It tried to stretch its supply-push, R&D-focused mandate to a demand-pull orientation, such as government as first buyer of innovative products, and to a more supportive approach to the financial ecosystem. These were helpful suggestions, but in today’s $2-trillion Canadian economy, hardly of enough consequence to move the innovation needle.

This raises the question: What is an appropriate public policy approach to invigorate Canada’s innovation performance?

Invigorating Canada’s innovation performance is a daunting, complex challenge that will not succumb to easy solutions. At the heart of it is the question regarding the right combination of public policy carrots and sticks that will induce business to adopt innovation-based strategies.

Governments have traditionally been comfortable with the carrot approach — namely, providing incentives, but they have not been as enthusiastic about using the stick approach.

This section will argue that innovation policy should try to find the right balance between these approaches:

If Klaus Schwab and other theorists of the tsunami wave of innovation-driven change prove to be even partially right, the future international marketplace will be not only fiercely competitive but also more driven by quality than by price. This is both a threat and an opportunity for advanced economies like Canada’s.

The first rule for governments in this environment should be to “do no harm.” By this I mean do not create barriers that will try to insulate domestic firms from international competition, whether they be non-tariff measures or subsidies.

The second rule should be to review systematically the restrictions on competition still in place. At a federal level, these include general and sector-specific legislative and regulatory frameworks that protect Canadian firms from foreign competition. The Wilson Report made a number of recommendations in this regard some years ago, but many were not embraced by the previous government.48

A true innovation focus would reverse the onus on governments to explain why it is in the public interest to keep various anti-competitive instruments in place. This is by no means a deregulatory screed. Indeed, as outlined below, “smart regulation” can be an important stimulus for innovation. Rather, the reverse onus would force governments to justify maintaining discriminatory measures against foreign competitors — or, in the case of provinces and territories, against each other, as is now largely sanctioned under the Agreement on Internal Trade.

The old linear, supply-push model of innovation is now largely defunct. The innovative impulse can come from anywhere in a business operation. Intuitively, the shortest route to business innovation is from a perceptive reading of the market.

Government policy has a significant impact on product markets and, therefore, on innovation. Regulatory frameworks, whether they be related to drug patent policy, carbon-reduction mechanisms or fuel-economy standards, set the rules of the game. If these frameworks are well designed, regulation can have two huge benefits: first, to promote the broad public interest; second, to stimulate innovative responses from industry.

There is nothing new in this, but smart regulation has generally not been explicitly tied to innovation. By way of example, following on the heels of a federal innovation strategy document published in 2002,49 the government appointed a blue-ribbon External Advisory Committee on Smart Regulation. The Committee’s report50 made numerous recommendations on the need for regulatory process streamlining, but did not even implicitly suggest that regulatory policy should promote innovation as one of its objectives.

A similar approach to promote innovation as a policy objective in demand-side instruments was also prominent in the Jenkins Report, which recommended that it become an explicit objective in government procurement policy. To this day, the federal government maintains only a very modest program designed to encourage Canadian firms to come up with innovative proposals that respond to government needs.

In a sense, these outcomes are not surprising given the entrenched culture among government regulators and purchasers of a narrow interpretation of the public interest, with no compensating political direction to build in positive, pro-innovation considerations. Little wonder then that the OECD came to the following observation in its review of business innovation policies: “Responses from OECD member countries to the OECD Science, Technology and Industry Outlook 2010 questionnaire indicate that demand-side innovation policy is still considered a low priority compared to -supply-side policy approaches.”51

For most observers, R&D is synonymous with innovation. As a result, most discussions of innovation policy start and end with R&D incentives.

There is clearly a case for the public support of R&D because of the positive social and economic externalities. Whether R&D programs are well designed and achieve stated objectives is another matter, but that should be subject to regular periodic audit and evaluation. In that regard, the Jenkins Report’s recommendation to free up expenditures on the broadly based SR&ED tax credit and redeploy those resources to support ambitious, high-growth companies more directly would arguably provide better bang for the buck in terms of influencing corporate behaviour at the margin. That hypothesis would, of course, need to be tested empirically. The only publicly available evaluation of the SR&ED tax credit goes back almost 20 years; it found then that the program generated $1.38 in incremental R&D spending per dollar of forgone tax revenue.52 An update of this work plus similar evaluations of direct support programs, like IRAP, would be required to make a comparison.53

I would argue, however, that instead of spending a great deal more time and effort in debating the niceties of R&D programming, attention should be placed on other key supply-side drivers of innovation. Two of these drivers — highly skilled people and risk capital — suffer from a type of market failure to the extent that supply is inefficiently low, thereby effectively capping new opportunities in Canada. Importantly, as well, the two can come together to form a powerful innovation dynamic — clusters of innovation-driven, high-growth companies.

Although Canada has one of the highest rates of post-secondary graduation in the OECD, we are only middle of the pack in terms of actual employable skills — average in literacy, below average in numeracy and above average in using technology to solve problems.54 It is not surprising, therefore, that according to a recent Conference Board survey, over 70 percent of employer respondents observed gaps in candidates’ and recent hires’ critical thinking and problem-solving skills, and nearly half said that they see insufficient oral communication and literacy skills.55

Further, fewer-than-optimal proportions of students enrolled in universities and colleges choose courses of study that are in high demand by employers, particularly science, technology, engineering and mathematics (STEM) disciplines — representing approximately 25 percent of graduates.56 Proficiency in STEM disciplines and a greater level of STEM-literacy among graduates in other fields are critically important for an ICT-led transformation of business models in most industry sectors.57

At its root, the problem lies with the education system itself, which has not yet come to grips with the urgent need to educate for the competencies required for participation in the innovation-driven economy.

Indeed, there seems to be a lack of recognition on the part of provincial and territorial governments that there is, in fact, a problem. For example, the Council of Ministers of Education (CMEC, on which the federal government is not invited even as an observer) reacted positively rather than negatively to the above-cited OECD findings, claiming that “Canadians are increasingly embracing information and communications technologies and are well positioned for the society and economy of the 21st century.”58

Unlike virtually every other advanced-economy federation, it is problematic for Canada’s federal government to engage on this issue other than as a supplier of funding. In this regard, the 2015 federal budget provided “a one-time investment of $65 million to business and industry associations to allow them to work with willing PSEs to better align curricula with the needs of employers.”59 Furthermore, the 2016 budget announced a four-year $73-million Post-Secondary Industry Partnership and Cooperative Placement Initiative. The purpose of the initiative is to support partnerships between employers and willing post-secondary institutions to better align what is taught with the needs of employers [including] new co-op placements and work-integrated learning opportunities for young Canadians, with a focus on high demand fields, such as science, technology, engineering, mathematics and business.60

Perhaps in developing proposals to use this kind of funding, Canadian business groups can press for needed improvements not only with willing PSE institutions, but also more directly with provincial and territorial education ministries. The Business Council of Canada’s recently launched Canadian Business/Higher Education Roundtable — made up of CEOs and post-secondary presidents — offers the promise of a more coordinated approach to work-integrated learning.

The situation constitutes a public sector failure requiring urgent remediation because supply from the PSE system in Canada either is not adequately meeting existing business demand or is responsible for capping investments in future growth.

Some would argue that, on the contrary, this is more a problem of lack of business demand. A key indicator of such low demand in Canada is the finding that labour composition (the effect of skills upgrading through experience and education) contributed only 0.2 percent of the meagre 1 percent annual average increase in productivity since 2000, while capital intensity contributed 0.08 percent.61

However, the centrality of a highly skilled workforce to success in the third (or fourth) industrial revolutions stands the usual demand and supply calculus on its head. With talented people still being the least mobile of the factors of production, it follows that capital and technology will be attracted to locations where a critical mass of talent resides. To put a point on it, studies over the years on investment attractiveness have consistently placed quality of the workforce as the number one factor.

By any international measure Canadians are highly entrepreneurial, and our business climate for start-ups is favourable. The long-standing lament in Canada relates more to the paucity of start-ups that grow to “large-value creators.” Indeed, SMEs in Canada tend to be much smaller on average than their US counterparts, with the attendant managerial and financial challenges.

On the financial side, there is the perennial challenge of funding for relatively high-risk, high-return business strategies. The market failure in this case relates to the risk-averse culture of the financial sector, compounded by a small base of angel capital investors and an immature venture capital sector that has arguably been Balkanized by public policy. Even though venture capital investment in Canada hit a 10-year high in 2015, ours is still an “infant industry” compared with that of the United States, which invests two and half to three times more money per capita in venture capital.62

This market failure lies behind the Jenkins Report’s fifth recommendation and the subsequent further branching out of the BDC into various special funds in collaboration with private sector investors. Tom Jenkins put it in his testimony to the Senate Standing Committee on Banking, Trade and Commerce as follows:

We felt that the direct investor…should be the private sector, should be the banks, the pension funds, the other financial firms and, indeed, foreign firms that would like to come and invest in Canada. Our charge to the BDC was to facilitate that through the matching that you had mentioned before and the Israeli model. In the Israeli model they do not lead; they simply de-risk.63

At the margin, I would argue that further initiatives in this area would likely have greater long-term economic payoff than equivalent expenditures on R&D support.

The critical talent and financing inputs to innovation-driven business strategies do not work in isolation. They meld into an innovation ecosystem based on competitive and complementary interactions among numerous actors, usually in a relatively confined economic space. An often-cited role model is Silicon Valley. The Toronto-Kitchener-Waterloo corridor is the closest Canadian equivalent, but on a much smaller scale.

There is a substantial body of literature on the innovation-led growth of urban areas populated with what Richard Florida describes as “the creative class,”64 building on earlier academic work by Michael Porter and others on the factors leading to the formation of innovation-driven clusters.65 The thesis underlying this work is that a locational concentration of talented people, often anchored by PSE institutions, will create agglomeration economies for small, high-growth companies, with a positive feedback loop for new investment flows.

Over the years, governments have tried to help create clusters. For example, one of the stated aims of establishing the NRC’s various institutes across Canada was to nurture the development of technology-based clusters, such as nanotechnology in Alberta. Typical of the Canadian way, though, equity considerations often trumped excellence as governments responded to pressures to promote cluster development across the country. We are now learning that enduring clusters tend to evolve organically, aided often by fortuitous accidents of history, rather than through prescriptive public intervention. The lesson for governments is to get behind a cluster and push once it has formed.

Recent work in Canada on the issue changes both the nomenclature and the approach. The focus is now on using publicly and privately sponsored business accelerators and incubators across Canada as the locus of attention for venture and angel capital investors. According to the Centre for Digital Entrepreneurship and Economic Performance, there are 146 such organizations across Canada that create the backbone of a “high-functioning innovation ecosystem…that acts to help transform ideas into substantive businesses, and entrepreneurs and technical engineers into company founders and executives.”66

This approach holds some promise in strengthening what the Council of Canadian Academies calls the “connective tissue”67 that facilitates the creative interplay among actors in the innovation ecosystem. As noted above, Budget 2016 is making a substantial investment, starting next fiscal year, to this end. The challenge in developing the initiative will be to use public funds to reinforce rather than distort market-driven trends.

A sustainable, long-term growth strategy for Canada rests on continuous, innovation–driven productivity improvements. Unfortunately, Canadian business as a whole is not currently positioned to take up the challenge. Until now, it has provided shareholder value without having to invest in higher-risk, innovation-based strategies. Indeed, this conservative approach has been rational.

The question is whether that business culture can transform itself quickly enough to compete in the rapidly changing international environment, as previewed by informed musings about an advancing fourth industrial revolution.

In my opinion, there is some reason for optimism. The market will do most of the heavy lifting in forcing increasing adaptation to innovation-driven business strategies. For example, the creative resiliency of Canada’s oil patch reminds us why we have clichés such as necessity being the mother of invention.

Government policy plays an important supportive role; the challenge will be to get the right combination of carrots and sticks that will facilitate rather than hinder innovation-driven strategies. To do so, innovation policy must be considered in much broader terms than has traditionally been the case. Indeed, program spending on R&D and related issues has in aggregate only a marginal impact compared to regulatory, trade and tax policies that underpin the broader microeconomic policy landscape.

Further, even within program spending, R&D is not the holy grail for most modern businesses. Rather, innovation is driven primarily by business opportunities in private and public markets. There are some things that matter more to businesses than R&D (which can be bought). First is access to highly skilled people, an area where public policy is faltering. Second is access to risk capital, where private markets are underperforming. Both need remedial action.

In my view, the way to address Canada’s innovation conundrum is not to focus narrowly on our chronic underinvestment in business R&D. The appropriate policy prescriptions should be multi-faceted and based on a coherent set of microeconomic instruments designed for long-term, innovation-driven growth.

Looking back to the Jenkins Report of five years ago; despite its narrow mandate, it may still prove to have an enduring legacy in helping point the way forward to invigorating Canada’s innovation performance.

Montreal – To improve Canada’s lamentably poor innovation performance we must move beyond our traditional focus on research and development (R&D) and take steps to reinforce competition rather than hinder it, says a new report from the Institute for Research on Public Policy.

“As the global market place becomes increasingly competitive, Canada’s innovation performance is clearly lagging behind — this despite generous R&D tax credits,” says author Andrei Sulzenko, a former senior assistant deputy minister of policy at Industry Canada.

His report, released in the wake of the government’s commitment to make Canada an innovation powerhouse, assesses the policy impact of the 2011 Jenkins Report on innovation, and recommends a way forward for the new Liberal government.

Sulzenko argues that despite recent steps in the right direction, Canada’s policy approach has been too timid and is failing to stimulate widespread innovation-driven business strategies. The reason is, he says, we have been dealing with the symptoms (i.e., Canada’s weak R&D performance), rather than tackling the root of the problem. “The lack of serious, sustained competitive pressures in key sectors of the Canadian economy has made it rational for businesses to underinvest in a range of riskier innovation activities, including R&D,” he says.

According to Sulzenko, Canada’s new innovation agenda will require a smart combination of microeconomic carrots and sticks to create a more comprehensive, pro-innovation business climate. Key elements of this approach should include:

It will be crucial to seize the opportunity to get the policy approach right, because innovation-driven productivity improvements are the best sustainable source of future growth for Canada.

Canada’s Innovation Conundrum: Five Years after the Jenkins Report by Andrei Sulzenko can be downloaded from the IRPP’s website (irpp.org).

Media are welcome to attend a working lunch with the author and commentators Hon. John Manley (president and CEO, Business Council of Canada), Ilse Treurnicht (CEO, MaRS Discovery District), and Iain Klugman (CEO, Communitech).

What: Canada’s Innovation Conundrum: Five Years After the Jenkins Report

When: June 13, 2016, 11:45 a.m. – 2:00 p.m. Panel discussion will begin at 12:30 p.m.

Where: Rideau Club, 99 Bank St, Ottawa

-30-

The Institute for Research on Public Policy is an independent, national, bilingual, not-for-profit organization based in Montreal. To receive updates from the IRPP, please subscribe to our e-mail list.

Media Contact: Shirley Cardenas tel. 514-594-6877 scardenas@nullirpp.org

In its inaugural budget, the federal Liberal government vowed to develop a bold, new innovation agenda as the centrepiece of its strategy to bolster long-term economic growth. This was the right call, not only because it plays well—who would disagree with Canada becoming “a centre of global innovation?”—but also because innovation-driven productivity growth is unequivocally essential for our future prosperity.

My recent paper on the subject, published by the Institute for Research on Public Policy (IRPP), explains why this is so. Quite simply, Canada can no longer rely heavily on previous sources of growth—like a trade boost after signing onto NAFTA or a commodity-price boom—that have masked its innovation problem.

That leaves us with improving productivity—working smarter. Productivity figures can be disaggregated into three components: workforce quality; capital deepening; and what economists call multi-factor productivity, essentially the know-how in combining labour and capital, i.e. innovation. Compared to the U.S., Canada has done relatively well in recent years on the first two elements, but dismally on the last. In fact, innovation-driven productivity improvement has made virtually no contribution to Canada’s growth since 2000.

How can Canada turn this around? For many years the mantra has been to increase business research and development (R&D). However, despite generous tax credits and a myriad of direct funding programs, business R&D as a share of GDP has fallen since peaking in 2000. There is no reason to believe that more of the same will get us from here to there.

The answer to a turnaround lies in a better understanding of what motivates business decisions. The Council of Canadian Academies concluded in a 2013 study, that “Canadian firms have been as innovative as they have needed to be,” doing business in “a low-innovation equilibrium.” A lack of competitive pressure in many key sectors of the Canadian economy has provided the basis for this seemingly rational response.

Business profits as a share of GDP have been higher in Canada than the United States over the last three decades—suggesting that many Canadian companies have until now done relatively well without innovating.

Today, the key questions are: Will Canadian businesses respond to the urgent need to focus on innovation-based strategies? And what can public policy do to facilitate the transition?

Building on the 2011 Jenkins Report on innovation, my paper makes three broad recommendations.

First, systematically review trade, investment and regulatory policies that have served to inhibit competition in Canada and reinforce the low-innovation equilibrium. For example, ownership restrictions in key sectors like telecommunications and airlines inhibit competition in those sectors and increase the cost of doing business in Canada.

Second, emphasize demand-side instruments such as smart regulation and government procurement that can be designed to incentivize innovative responses, while protecting the broader public interest. For example, going beyond the current token effort at stimulating business innovation through creative government procurement contracting, like the U.S. and other countries, would allow Canadian companies to develop new products and processes for global markets.

Third, rebalance supply-side instruments by de-emphasizing business R&D support relative to other key elements, such as enhancing workplace skills, de-risking growth financing, and reinforcing innovation ecosystems involving sectoral and regional clusters. Building on pilot initiatives in each of these areas into full-blown programs would help high-growth firms scale-up more rapidly and increase the probability of remaining based in Canada.

By following this approach we would broaden innovation policy from a longstanding, almost singular, focus on R&D to a more challenging, but more rewarding, multi-faceted micro-economic agenda. It’s more challenging because various interests would resist changes to the status quo, but it will be more rewarding because that will be what it takes to make Canada a centre of global innovation.

Andrei Sulzenko is a former senior assistant deputy minister of policy at Industry Canada. He is the author of Canada’s Innovation Conundrum: Five Years after the Jenkins Report, published by the Institute for Research on Public Policy (irpp.org).

The federal government has announced an ambitious goal of turning Canada into a centre of global innovation. Over the next year or so, it will develop a bold new innovation agenda to help achieve this objective. What should be the crucial elements of this agenda? And how much can changing government policies actually boost Canada’s innovation performance, which has been lamentably poor relative to those of peer countries? The IRPP hosted a working lunch with the author of an IRPP report on this topic, Andrei Sulzenko (former senior assistant deputy minister, Industry Canada), and commentators Hon. John Manley (president and CEO, Business Council of Canada); Ilse Treurnicht (CEO, MaRS Discovery District); and Iain Klugman (CEO, Communitech). The moderator of the event was president and CEO of the IRPP, Graham Fox.