Redesigning Canadian Trade Policies for New Global’s Realities

Overview of the Research Findings

Stephen Tapp, Ari Van Assche and Robert Wolfe

International trade and investment are central to economic prosperity. But new global realities, including rising antitrade sentiment, are challenging long-held policy approaches in these areas. With the global trading system at a critical juncture, now is the time to examine new trade realities and explore appropriate responses. In this volume, the culmination of a comprehensive interdisciplinary research initiative, the Institute for Research on Public Policy has brought together groundbreaking contributions from more than thirty experts in eight different countries. Together, they analyze how longer-term changes and emerging trends in international commerce, technology and economic power are affecting Canada, and what these changes mean for public policy.

The authors take an in-depth, firm-level look at Canada’s trade, and assess its integration in global value chains. They provide a rigorous analytical framework, supported by new empirical evidence, that will help readers better understand the global economy. Among the topics they examine are the new business models driving the more fragmented and global nature of production; the technological developments that are allowing new traders to expand their reach; and the shift in economic activity toward emerging markets that is dispersing power and raising new challenges for trade negotiations. The editors’ conclusion distills the research findings into a forward-looking policy agenda for more inclusive trade.

Given the profound transformations taking place in the international trade environment, this volume is essential reading for all those interested in the high-stakes debate over globalization and the best way forward for Canada.

Canada’s trade policy is at a risky crossroads. The prosperity and growth of Canada’s small, open economy depend on international trade and investment, but new global realities require a reassessment of long-standing policy goals and approaches in these critical areas. Canada benefits from an intricate network of international trade and investment rules, but efforts to adapt these rules to accommodate new players, new products and services and new production and ownership models are stymied. Since this research project began, we have observed a dramatic rise in apparent antitrade sentiment on both sides of the Atlantic. Indeed, many citizens in advanced economies think trade is not working for them. A new US president seems set on fundamentally changing US trade policy — putting “America first” while withdrawing from the Trans-Pacific Partnership (TPP) and renegotiating the North American Free Trade Agreement (NAFTA). Without question, the ripple effects of a US retreat from a rules-based trading system would bring considerable risk for Canada.

With this volume, our aim is to provide new empirical evidence and an analytic framework to better understand what new global trade realities mean for Canada and how the suite of Canada’s trade-related policies could be updated to deliver more broadly shared economic prosperity. This concluding chapter takes stock of the main results presented in the volume and policy insights from this multiyear research program of the Institute for Research on Public Policy (IRPP). Our research reveals a complex global trading system, in which productivity, innovation and growth at home depend on both imports and exports. Instead of producing goods and services within the borders of a single country, businesses collaborate in global supply chains and use foreign affiliates to serve foreign consumers directly in their markets. Small firms and big firms face different trading opportunities and constraints, and use different channels to internationalize. Emerging markets, such as China and India, are fast becoming important players in international trade and investment. This has led to a shift in global economic power, which is one reason multilateral trade negotiations have stalled. Yet, global output and trade growth have slowed noticeably since the financial crisis of 2008-09, and diminished growth prospects have led to economic anxiety, in Canada as in other developed countries.

In this new context, Canada needs a renewed approach to its global commerce policies. To preview our main recommendations, we think that a key objective should be to develop inclusive policies that help more Canadians share in the benefits of globalization and technological progress. Indeed, we view an inclusive agenda as vital to maintain the Canadian public’s support for trade and trade agreements. To this overarching framework of inclusive trade we add three main policy pillars: first, facilitate the reallocation of Canada’s resources to their best uses to promote economic prosperity; second, improve international connectivity to help Canadian firms and workers engage better with foreign partners in global value chains; and third, work with other countries to build a strong multilateral foundation for the global trade and investment system. These high-level policy recommendations are summarized in the appendix and described more fully in what follows.

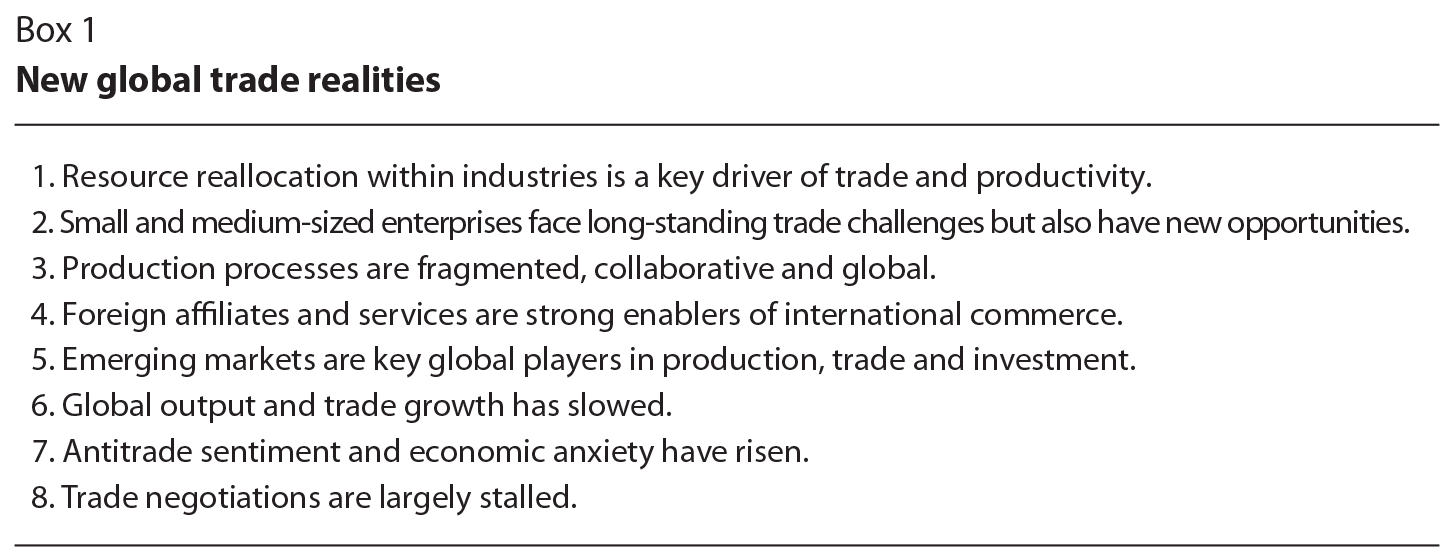

Drawing on the findings in this volume, in this section we distill the changes underway in the international trading system into eight “new global trade realities” that policy-makers should take into account in defining Canada’s trade priorities (see box 1). Let us examine each of these challenges in turn.

The analytic framework of this volume begins in part 1 with a review by Beverly Lapham of twenty-first-century trade models that focus on firms — a natural evolution of traditional country- and industry-level approaches. This literature emphasizes variations in firms’ characteristics, such as size and productivity, and their different responses to changes in the trading environment. A more open environment, for example, offers opportunities abroad and enhances competitive pressures at home. Although economists have long understood that trade can raise a country’s productivity and that trade adjustments create winners and losers, recent research shows how these effects differ across firms. In adjusting to trade liberalization, more productive firms grow and expand their market share at the expense of less productive firms, which contract or leave the market.

Contemporary theory has refined our understanding of this adjustment by identifying a new channel through which trade can raise domestic productivity — namely, by reallocating resources not only among industries, as emphasized by traditional theories of comparative advantage, but also among firms in a given industry. This new mechanism has been particularly relevant for the Canadian economy as it adjusted to new trade agreements. The best estimates suggest that, after the Canada-US Free Trade Agreement reduced tariffs on both sides of the border, most of the impressive productivity gains realized by Canadian manufacturing industries came from shifting production between manufacturing firms, rather than from “within-firm” growth (Melitz and Trefler 2012).

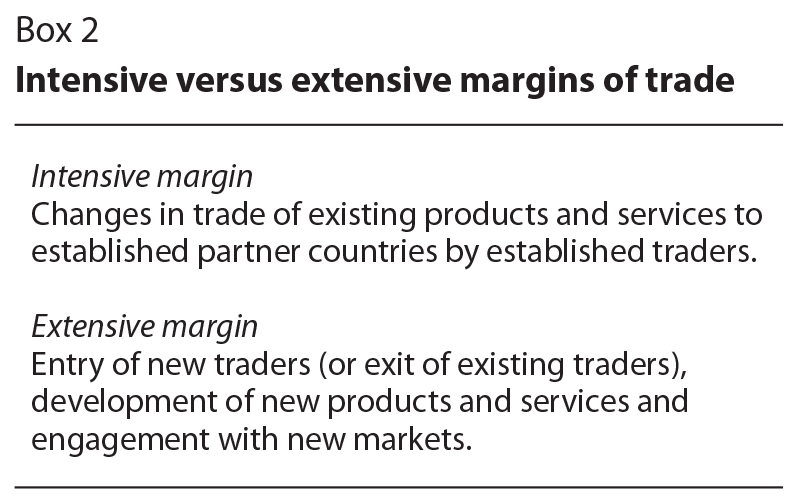

A related insight from this literature is the important distinction between old and new trade; in academic jargon, this distinction is between the intensive margin and the extensive margin (see box 2). This new insight calls for viewing trade negotiations in a different way. People often think that the greatest benefit of a trade agreement is its provision of better foreign market access and reduced trade costs, allowing existing exporters to sell more of their products in the trade partner’s market. Recent research has found, however, that most of the gains in production and exports actually come from new trade that did not take place before the trade agreement was implemented. For instance, a remarkable 90 percent of the increased value of Canadian exports to Chile after the Canada-Chile trade agreement came into effect was due to products not previously exported there (Foreign Affairs and International Trade Canada 2013). In practice, then, the strongest effect of trade agreements is the creation of new market opportunities that encourage the creation of new companies or that entice existing domestic firms to enter the new market. This response often entails the development of new products, using new production processes and new partners and suppliers. Trade negotiators and government trade support programs, therefore, should try to identify the needs of firms that might be prevented from expanding abroad by existing trade barriers (Cernat 2014). This is a difficult task, but adopting a firm-level approach could provide a more nuanced perspective of potential winners and losers, and hence a better assessment of the overall gains, from any trade policy changes (Ciuriak et al. 2015).

The firm-level approach also helps to explain why large firms dominate international trade. Firms, regardless of their size, incur fixed costs in order to trade, such as the time and money they need to spend to learn about new market opportunities, consumers and suppliers; to understand foreign regulations and adapt products to them; or to learn about and apply for government trade support programs. These costs may be hard to predict in advance and cannot be easily recovered once incurred. Other costs include those incurred navigating cumbersome customs procedures, establishing transport and communications infrastructure and obtaining trade finance. The nature of these costs gives bigger companies an inherent advantage in international trade because their larger scale of production reduces their per-unit trade costs. Conversely, small and medium-sized enterprises (SMEs) tend to be less competitive internationally because they have higher per-unit trade costs, and thus their trade is disproportionately restrained, particularly for lower-value transactions. Indeed, recent research suggests that a firm must operate above a certain productivity threshold to become a successful exporter.

John Baldwin and Beiling Yan, in their first chapter, and Sui Sui and Stephen Tapp, in their chapter, offer empirical support for the view that SMEs face a harsher trade reality. SMEs are generally less likely to export, reach far fewer countries when they do and have much lower average export revenues than do large firms. On the plus side, technology and policy changes that reduce fixed trade costs could help SMEs disproportionately to expand their trade. For instance, enhanced international connectivity and improved trust in online financial transactions already have allowed many SMEs to become global traders. As Usman Ahmed and Hanne Melin discuss in their chapter, technology-enabled SMEs, selling through online platforms such as eBay, are much more likely to export and to reach more foreign markets than even traditional, large multinationals, although their sales, of course, are generally much smaller.

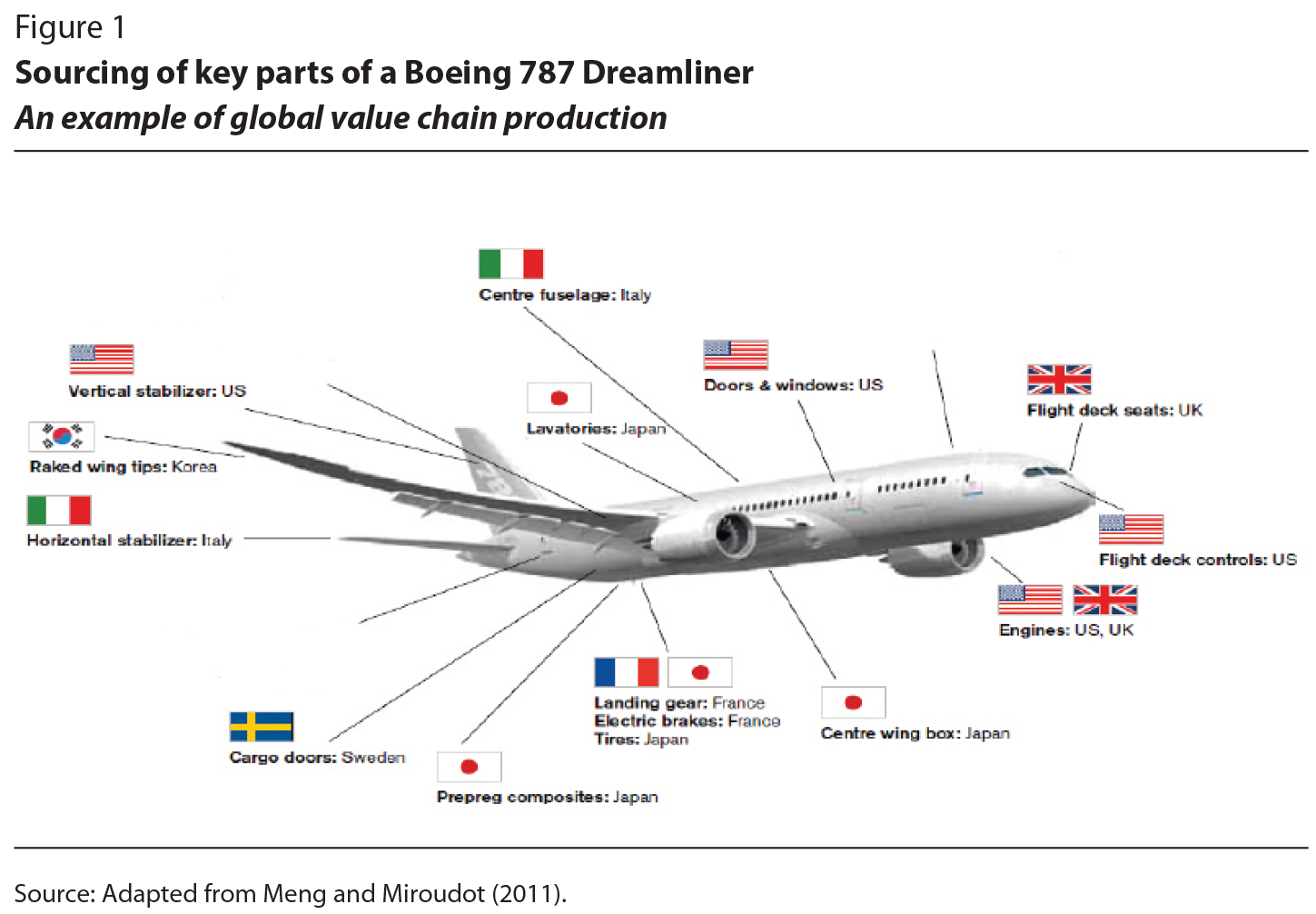

Part 2 of the volume describes how world trade and production are structured around global value chains (GVCs). Few factories make whole products themselves anymore; instead, production has fragmented and become more global. The bits and pieces of a car assembled in, say, Oakville, Ontario, come from various countries and cross borders multiple times in subassemblies. These GVCs feature prominently in manufacturing industries such as motor vehicles, electronics, pharmaceuticals, textiles and apparel — figure 1 provides an illustrative example from the airline industry — and in services. The rapid expansion of GVCs in recent decades is due mainly to technological advances that have lowered the costs of communicating, coordinating and trading over long distances. But GVCs have also expanded because of trade policies that have reduced tariffs and trade frictions both at international borders and “behind the borders.”

As Ari Van Assche discusses in his chapter, global business strategies have both driven these changes and evolved with them. Traditionally, firms viewed international markets as a way to expand their sales. Now, companies with a “supply chain mindset” split their production processes into separate tasks and perform them in the most efficient locations, often in several different countries. These firms are interested not only in the final destinations for their products or services but also in the journey of production along the way. Besides market access, they use international expansion to lower production costs, access foreign technology, collaborate with international production partners and diversify their exposure to supply chain shocks. What was once mainly a linear production process within a country is now inherently more circular and networked, as firms in GVCs contend with the complexities of moving goods, people and information across borders in multistage production systems. Central to the GVC revolution is technology that allows firms and regions to specialize in finer segments of an industry or in specific tasks, rather than participating more broadly in an entire industry or production process.

To understand the global trading system as it is evolving, trade policy analysis needs to make the difficult shift from looking at country- or industry–level activity to examining individual firms and the specific tasks they perform. Consider Montreal, home to the IRPP and often loosely described as being specialized in the aerospace industry. Area plants, however, do not manufacture complete, locally sourced aircraft; instead, it is more accurate to say that Montreal specializes in certain high-value-added activities within the aerospace industry — for instance, through multinational companies such as Bombardier and CAE that perform aircraft design and engineering.

Most international trade now involves exchanging not finished goods but intermediate inputs, which are used to produce a country’s exports. Products “exported by Canada” are not necessarily “made in Canada.” As Koen De Backer and Sébastien Miroudot note in their chapter, in 2011 (the last year for which data are available), only three-quarters of Canada’s gross export value was domestic; foreign value added accounted for the remaining quarter. Similarly, a significant portion of Canada’s exports is ultimately consumed in countries other than those to which it was initially sent. For instance, many Canadian companies export inputs to partners in the United States, which in turn use them to make goods for export to the rest of the world (showing the importance to Canada of follow-on commercial relationships between the United States and that country’s trade partners — the so-called partners of our partner).

Improved data support this more nuanced view of production and trade. Traditional gross, customs-based trade statistics — by simply recording the total value of goods that cross international borders and attributing their full value to the source country — can give a misleading picture of international commerce. These data should be complemented by more sophisticated value-added trade statistics that estimate each country’s incremental value added from domestic sources at various stages of production.

Trade-enabling foreign affiliates and services

Firms are increasingly collaborating with foreign production partners, sometimes through an arm’s-length trade relationship (recorded as export/import transactions) and sometimes through foreign direct investment, by which an affiliate is established abroad to reach foreign consumers directly (recorded as foreign affiliate sales). Indeed, international trade and foreign investment are so intimately linked that they are often two sides of the same coin.

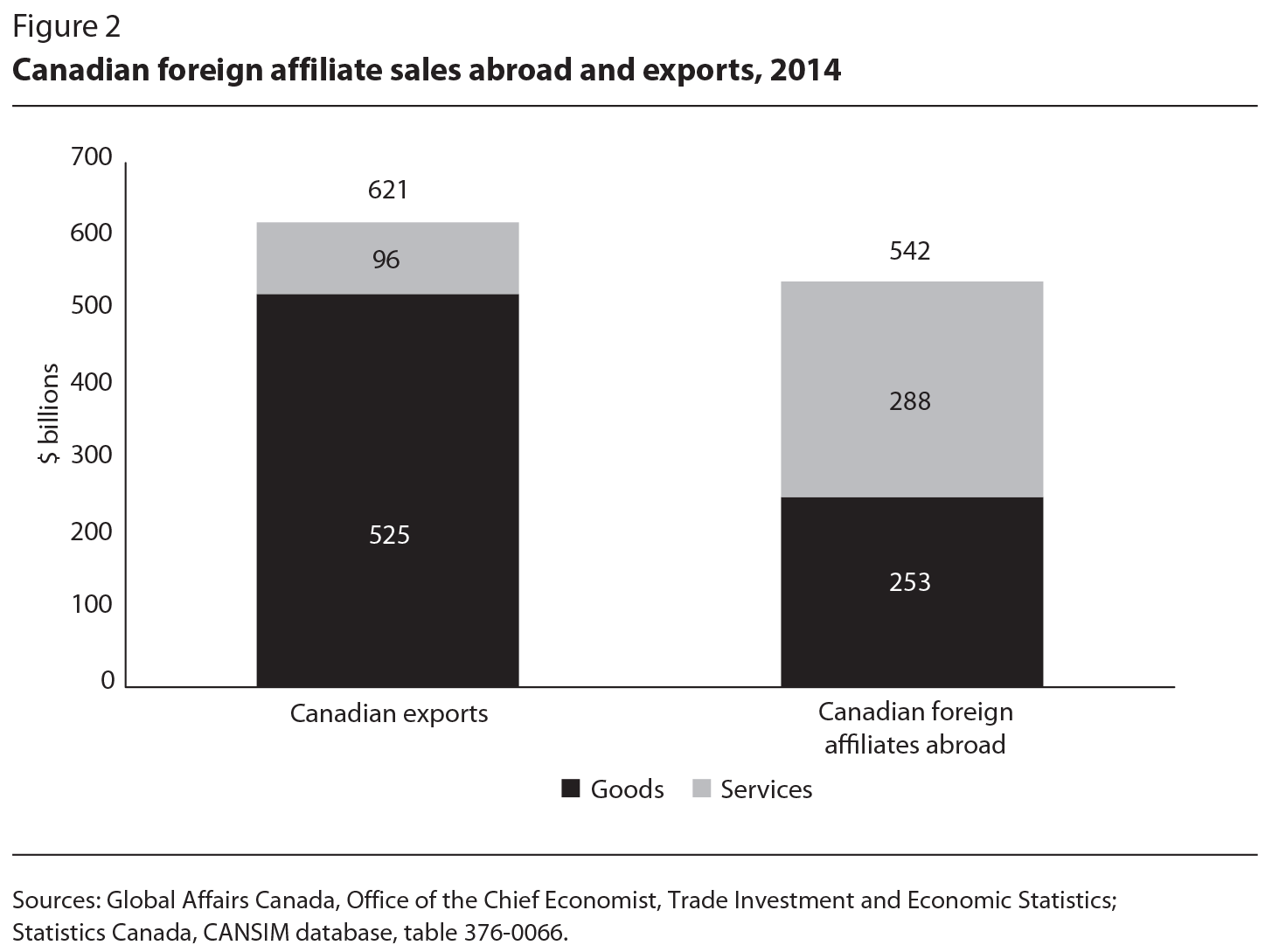

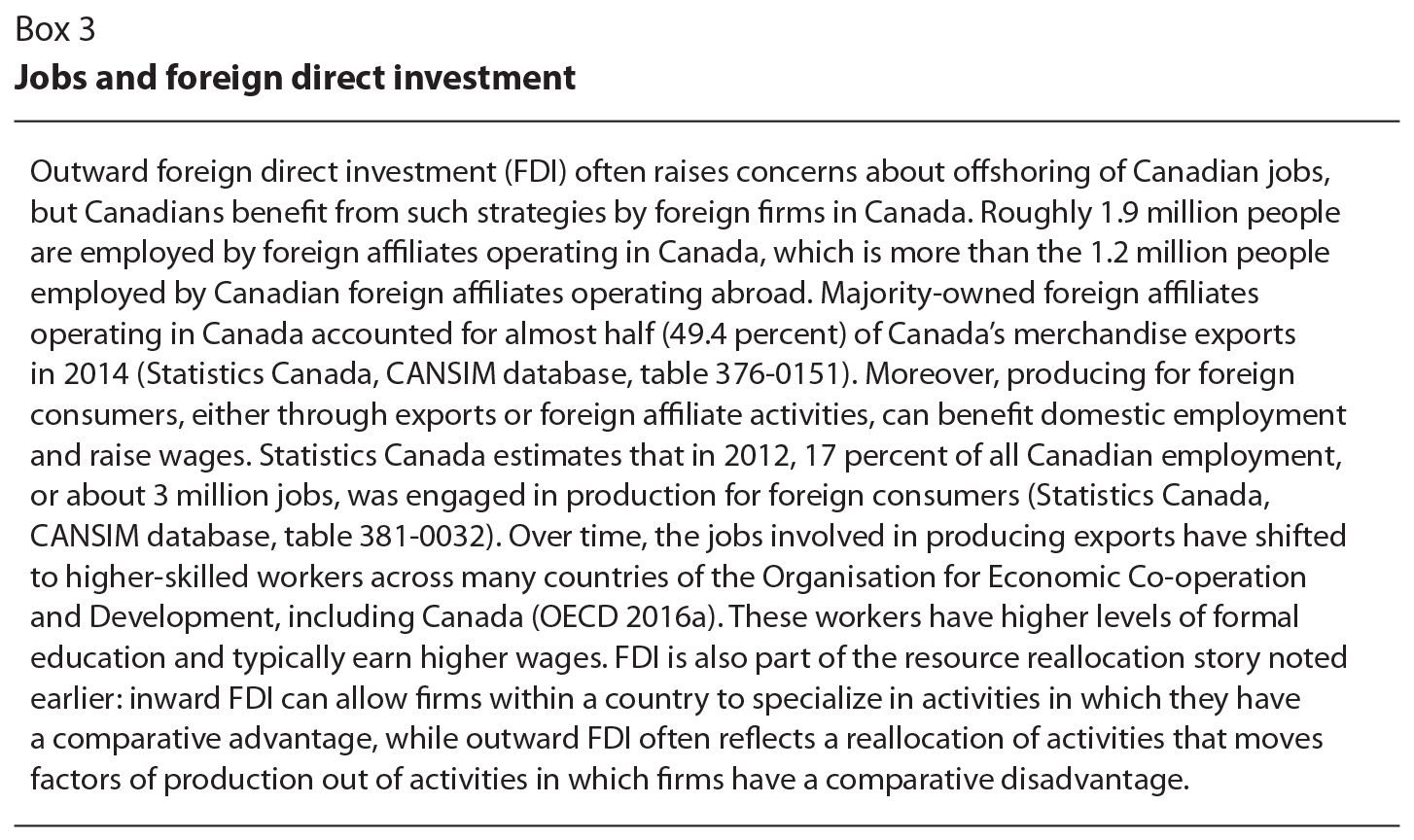

In the Canadian context, the overall significance and rapid growth of foreign affiliate operations is underappreciated in policy discussions, as Daniel Koldyk, Lewis Quinn and Todd Evans discuss in their chapter. In 2014, Canadian foreign affiliates operating abroad collectively generated sales that were almost as large as total Canadian exports (figure 2). These sales were concentrated in the services sectors, where having a physical presence is advantageous for consumer relations, as in the case of professional services, for example. Indeed, foreign affiliate operations and services have been the biggest growth areas in Canadian global commerce activities over the past decade, as Canadian companies increasingly reach foreign customers through on-the-ground affiliates rather than through exports (figure 3; see also Coiteux et al. 2014). These foreign affiliates are helping Canadian firms overcome market access barriers, capture consumption growth in emerging markets, tap into fast-growing South-South trade networks and increase production efficiency. (See box 3 for employment and wage considerations of this growth in foreign affiliates.) Canadian businesses thus are far more engaged with overseas markets and less dependent on the United States than the traditional export data would suggest. Value-added trade data emphasize the rising importance of services in the rapidly growing sales of Canada’s foreign affiliates. Indeed, as Sébastien Miroudot discusses, services — often performed domestically and embedded in goods that cross international borders — contribute about 45 percent of the total value added in Canadian exports, almost three times as much as traditionally reported.

Underlying these developments are dramatic shifts in sectoral employment as jobs migrate from making goods to performing services, a trend underway across the developed world. For every net job lost in Canada’s goods sector since 2001, roughly 30 have been created in the services sector (Poloz 2016). The real value of output in goods-producing sectors is still growing, but fewer workers are needed to produce the growing value of output because of sustained productivity growth in that sector.

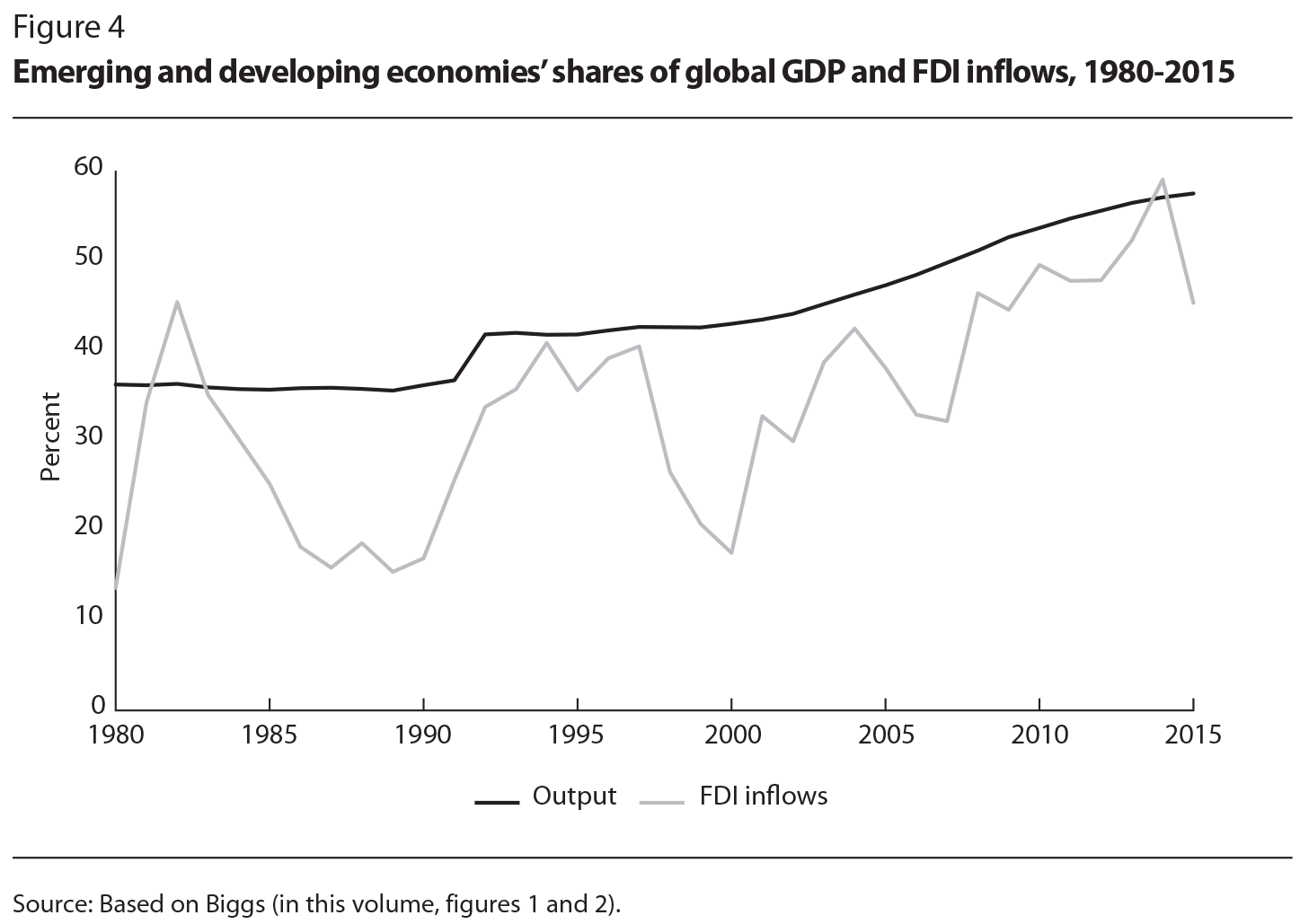

Another new global reality is the dramatic shift in the location of production, trade and investment flows. Developing and emerging markets are fast becoming big players. Their share of world output now exceeds that of the advanced economies, and they have become drivers of global growth and major recipients — and sources — of foreign direct investment (FDI), as Margaret Biggs explains in her chapter (see figure z4). The rapid and sustained income growth that emerging economies such as China and India have enjoyed in recent decades is a monumental accomplishment, bringing hundreds of millions of people out of extreme poverty. At the same time, the associated increase in demand for commodities has also helped propel a sustained rise in global commodity prices, which has benefited Canada. The growing economic clout of emerging markets is shifting and dispersing global power, and in the process challenging the representation, policy focus and relevance of post-Second World War economic institutions, which have struggled to involve these countries and reflect their priorities. The task of integrating developing economies into the global trade and investment system is no longer a secondary issue but one that is vitally important to improving economic and social outcomes in all countries.

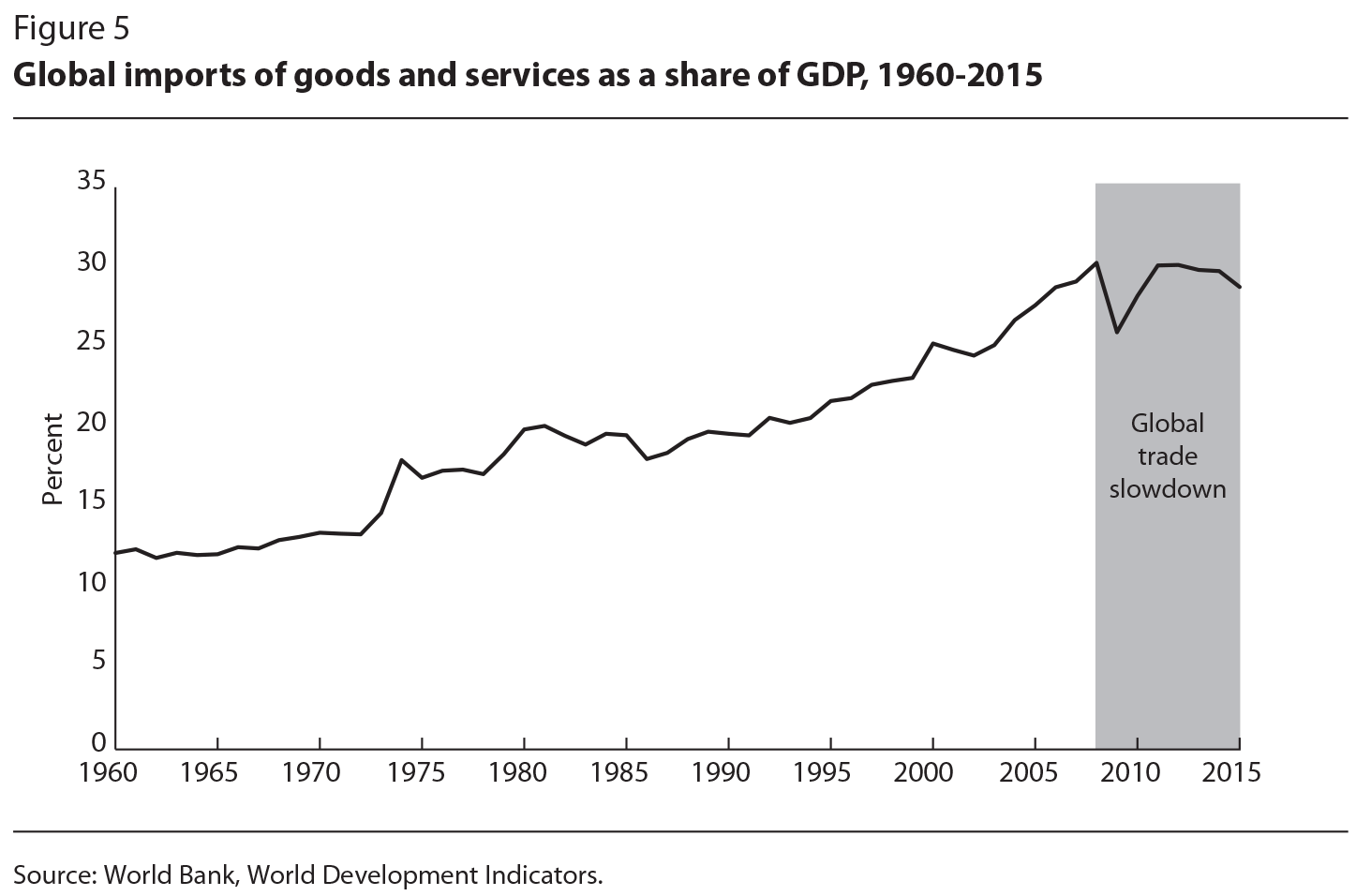

Across the developed world, trend output growth has slowed. The slowdown reflects several complex, interrelated and often-disputed factors, but the consensus view emphasizes two key elements: (1) population aging, which is slowing the growth of the labour force as the baby boom generation retires; and (2) weaker productivity growth (IMF 2015). Global trade, too, is now growing at less than half the pace it registered over the previous three decades. As figure 5 shows, after successive decades when global trade steadily rose as a share of gross domestic product (GDP), the ratio actually fell during the slow recovery after the global financial crisis of 2008-09, in what has been called the “global trade slowdown” (see Haugh et al. 2016; Hoekman 2015; IMF 2016).

The trade slowdown reflects both cyclical and structural factors. On the cyclical side, the global economy has operated consistently below its longer-term productive capacity in recent years. In addition, weak business capital investment (which is generally more trade intensive than other economic activities) and a weak European economy (which is more trade dependent than the economies of other regions of the world) also have restrained global trade. Another factor that has played a smaller role is the slowdown in trade liberalization, where trade policies have become more protectionist in many G20 countries, particularly after 2012 (WTO 2016). Canada, for example, has reduced many tariffs in recent years, but has also increased its use of antidumping and countervailing duty measures (WTO 2015). A more structural factor is the maturing of GVCs, which, after expanding rapidly between 1990 and 2007, have slowed noticeably since. One significant contributor to slower supply chain trade growth is the increasing substitution by Chinese manufacturing firms of domestic inputs for foreign ones. Looking ahead, as the composition of trade -continues to shift from manufacturing to services, trade growth might once again exceed output growth, especially if trade costs affecting services are reduced (Hoekman 2015). The dual trends of slowing output and slowing trade, however, make it important to find ways to improve economic performance.

Economic anxiety is running high across the developed world. People are worried about a wide variety of issues: the increased offshoring of production and competition from low-wage countries; potential job losses from automation; increasingly precarious work; immigration; and the lack of progress for the “middle class,” with deteriorating intergenerational economic progress and income gains captured too narrowly by those at the top. Nationalism is on the rise, as seen in the United Kingdom’s Brexit vote and the election of Donald Trump in the United States, both of which were attributed to antitrade and anti-immigrant sentiments.

Trade agreements — particular lightning rods for criticism — are often characterized as allowing multinational corporations to set the rules of global commerce in their favour, in ways that limit national sovereignty over policy–making through negotiations that are not transparent to the public. But are trade agreements the right target? In our view, trade agreements per se merit only a small part of the blame for much broader economic disruptions, particularly in the United States, where policies have largely failed to help citizens adjust to various economic changes, not just those attributable to trade deals. The more general forces of globalization, technological change and automation appear to be much more responsible for the challenges facing middle-class workers in developed economies (DeLong 2017).

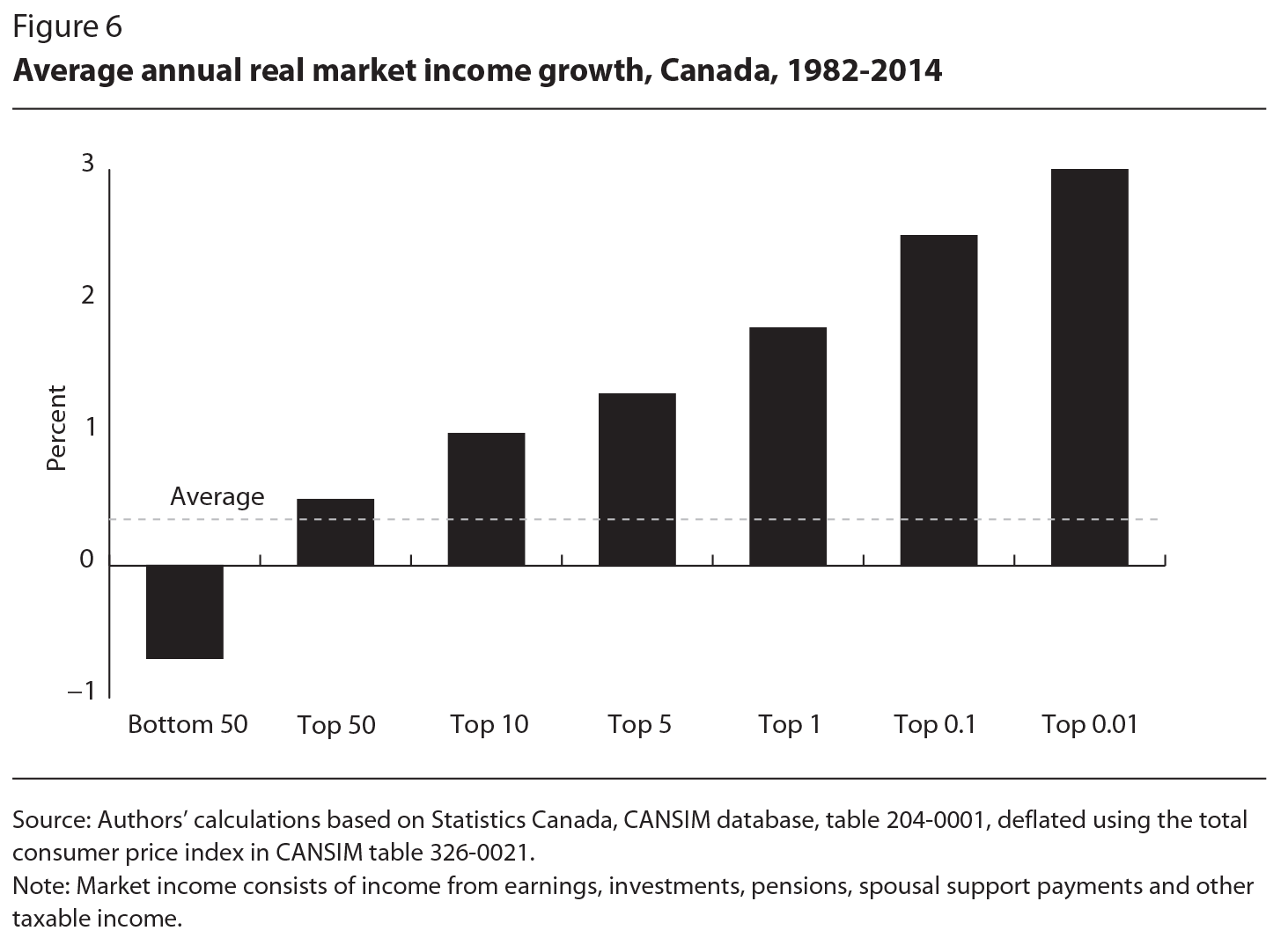

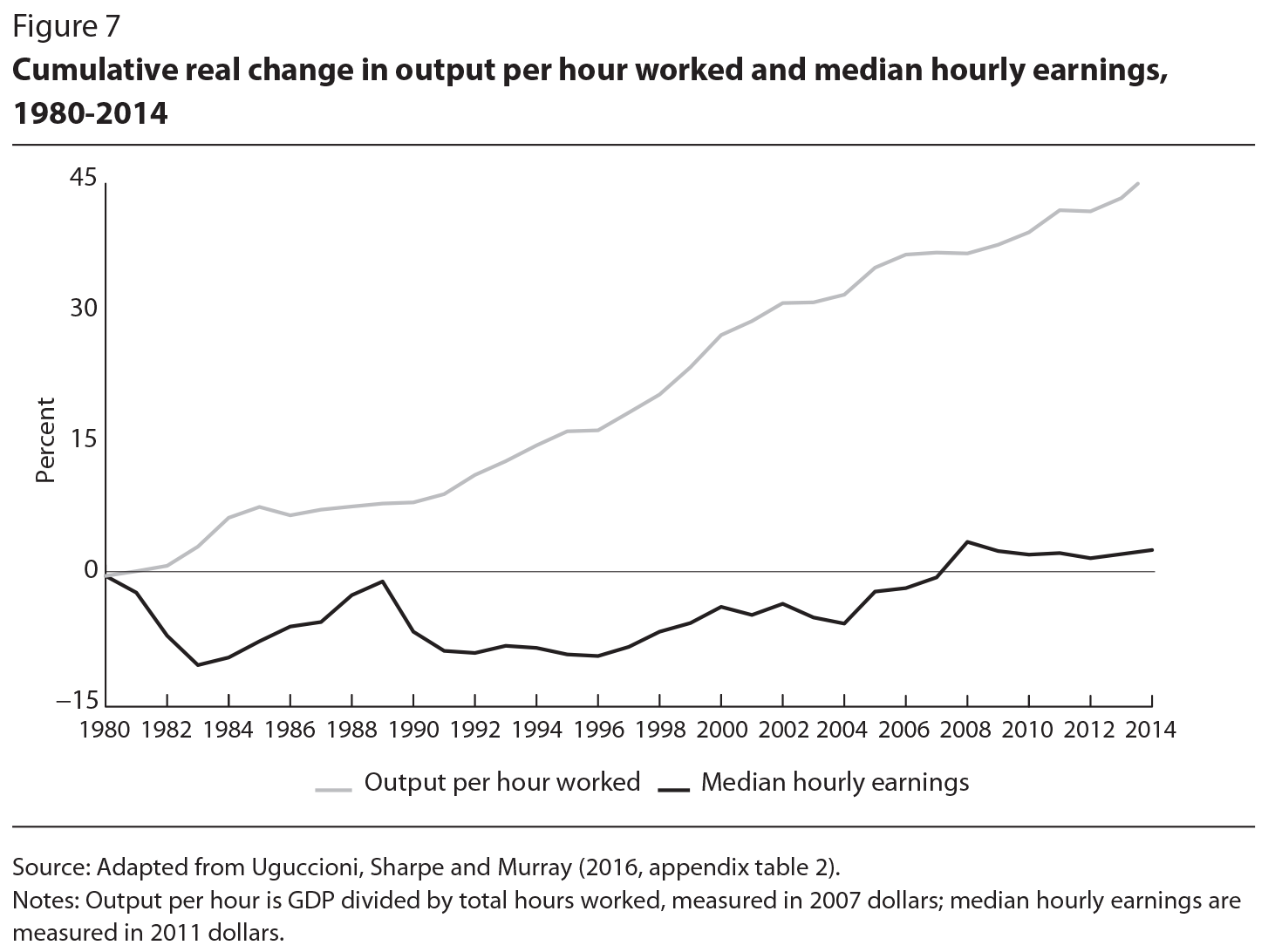

Regardless of the precise causes, income gains over the past three decades have been largely concentrated at the top end of the distribution in many advanced economies, particularly the English-speaking ones (OECD 2015). Canada experienced a significant increase in income inequality — primarily during the 1980s and 1990s — that featured dramatic gains by those at the top end, reflecting not only the increased demand for highly skilled workers in an increasingly knowledge-based and global economy but also the increased ability of these workers to capture economic rents (figure 6; and Green, Riddell and St-Hilaire 2016). A related concern is that aggregate productivity gains — perhaps the major promise of increased trade and trade-enhancing policies — have not been reflected to any meaningful degree in workers’ median earnings, which runs counter to what economic models often assume (figure 7). Despite strong evidence of aggregate gains from trade for the economy as a whole, there is not a large body of evidence on how the gains from trade have been shared across the income distribution in Canada.

The net distributional effects of any gains depend on many factors, including individuals’ consumption patterns and employment circumstances. Evidence on the spending side for many countries, including Canada, shows that trade tends to favour poorer consumers because they spend relatively more on tradable goods and hence benefit more from trade-related increases in purchasing power. In other words, tariffs and trade restrictions hurt poor consumers more (see Cardwell, Lawley and Xiang 2015; Fajgelbaum and Khandelwal 2016). On the other hand, Canada’s manufacturing sector appears to have experienced not only large productivity gains following the implementation of the Canada-US Free Trade Agreement but also sizable job losses (Trefler 2004). Similarly, in the United States, increased trade with China appears to have led to job losses in the manufacturing sector, as well as to depressed incomes and lower labour force participation in local labour markets most exposed to Chinese import competition (Autor, Dorn and Hanson 2013, 2016). Thus, on the earnings side of the ledger, the income and employment prospects of middle- and lower-skilled workers in developed countries — specifically those in routine manufacturing production and assembly jobs — are more vulnerable to increased trade. Criticisms of trade and trade agreements can be exaggerated in political discourse, but they and the larger concerns they encapsulate cannot and should not be ignored.

Our final new global reality, the slowing pace of trade negotiations and the deteriorating prospects for trade liberalization, relates to factors discussed above. Over the past decade, momentum stalled in multilateral trade negotiations at the World Trade Organization (WTO) with limited but important exceptions, such as the Trade Facilitation Agreement. The Doha Development Agenda that finally launched in 2001 was designed in the 1990s, before many of the new realities fully manifested themselves. The trading system now must adapt to seismic changes in what is traded and by whom, but the WTO is stuck, as are most other multilateral negotiations, in a world without global leadership.

The proliferation of bilateral, mega-regional and plurilateral negotiations in recent years is both a reaction to and a cause of the WTO’s slow progress, as Robert Wolfe discusses in his chapter. Such negotiations allow smaller groups of like-minded partners to experiment with agreements that vary the topics, participants, negotiation methods and legal relation of the results to the WTO. Several ambitious preferential negotiations have gone well beyond reducing tariffs to address a variety of behind-the-border issues. Partly, this new trade policy agenda reflects the fact that tariffs in advanced economies are generally already low in most sectors. Coupled with increasing GVCs, what really restricts international flows of goods, services, knowledge and professionals is issues such as regulatory differences among countries — with respect to, for example, health and safety rules, professional licensing and certification of conformity with product standards, as Bernard Hoekman explains.

China’s emergence as the world’s largest trader is a main driver of shifting global power. In his chapter, Wolfe characterizes the global trade context before the recent US presidential election as a “G-Zero world,” in which no group of countries — including the G7, which is too small and does not include China, and the G20, which is too amorphous — was willing or able to lead on global trade policy. The stated preference of the new US administration for a bilateral approach may further undermine multilateral negotiations, since the United States remains the indispensable participant. At the same time, however, a radical US pivot on trade also might galvanize other countries into playing a stronger role in defining new rules — not least in regulatory domains, where the need to satisfy business demands to remove inefficient regulatory differences, and citizens’ demands to address health and environmental concerns, will not diminish.

Canadian firms generally have not fared well in these new global trade realities, with troubling implications for Canada’s economic growth and productivity and for the job prospects of Canadians.

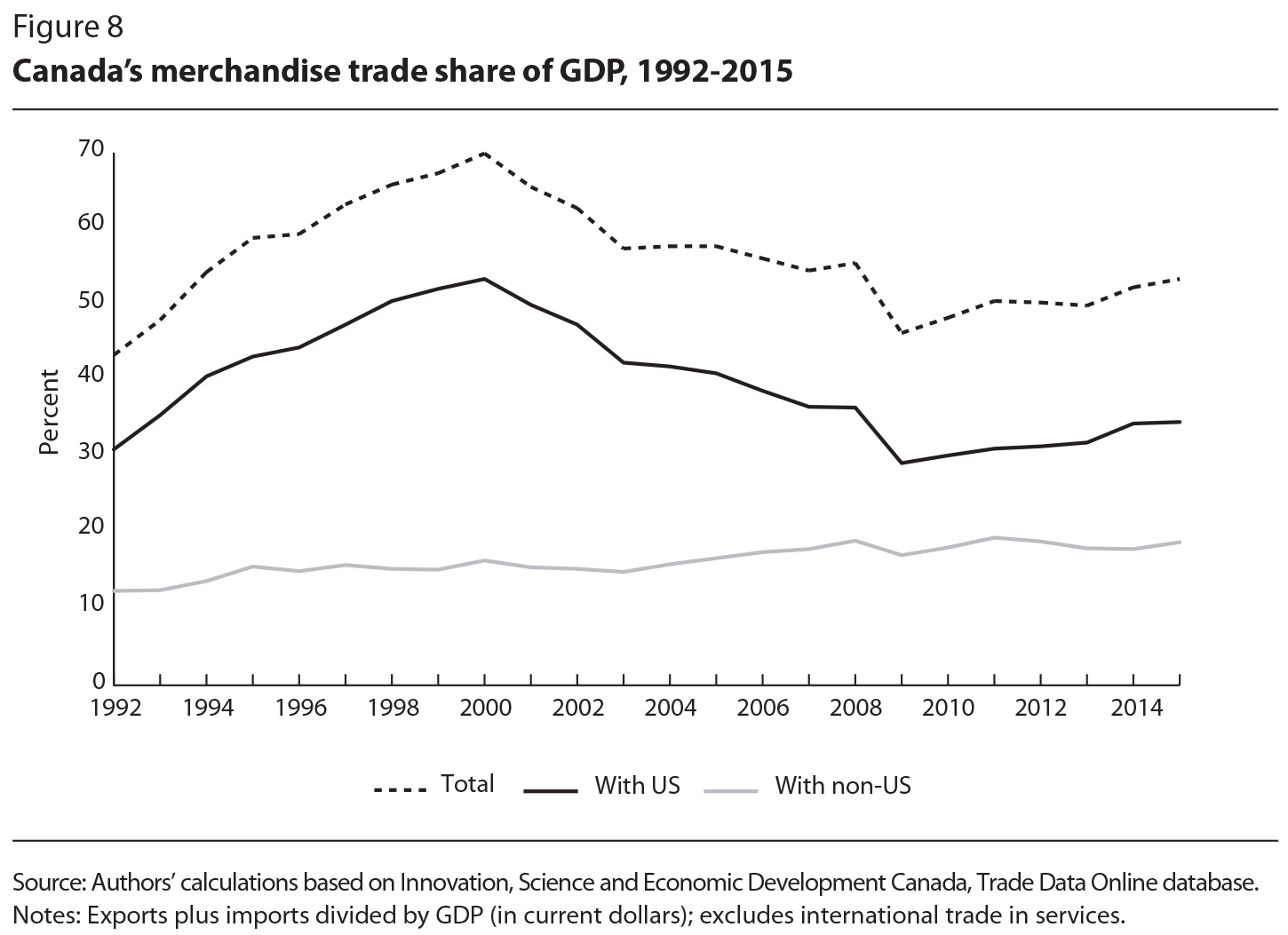

Consider the evolution of merchandise trade as a share of Canada’s economy in recent decades. Here, the dynamics of trade with the United States have largely driven the results (figure 8). Three distinct periods are evident. First, there was a period of rapid growth in the 1990s following the Canada-US Free Trade Agreement and subsequently NAFTA, combined with a depreciating Canadian dollar and a strongly growing US economy. These gains for Canada were almost completely unwound during the second period, 2000 to 2007, which featured the US dot-com bust, a thickening of the Canada-US border due to tighter US security measures after the 9/11 terrorist attacks (Brown 2015) and an appreciating Canadian dollar due to rising global commodity prices (Issa, Lafrance and Murray 2008). The third period began in 2008 with a global recession that caused a trade collapse, followed by an unusually slow recovery.

Several contributors to this volume support the view that the overall trade performance of Canadian business, particularly in the US market, has generally been lacklustre since the strong gains of the 1990s, despite some modest but sustained improvements in other countries.1 Until recently, however, this poor performance was partly offset — at least for total nominal export revenues — by a global commodities boom that significantly increased export prices and demand for Canada’s resources. This fundamentally weak performance is visible across many indicators, not only according to traditional trade metrics but also in terms of GVC trade and inward FDI. As Jim Stanford finds in his chapter, between 2001 and 2015, the average annual real growth of Canada’s goods and services exports was a mere one-fifth of the average pace of that of the Organisation for Economic Co-operation and Development (OECD) as a whole, with Canada ranking 33rd of 34 OECD countries. Around this same period, among a slightly larger group of 39 advanced and emerging market countries, Canada’s GVC participation ranking fell from 24th in 1995 to 35th in 2011 — a result that, as De Backer and Miroudot explain, is not merely due to changes in the industrial composition of Canada’s exports associated with global commodity price movements.2 Canada also has not fared well in attracting new “greenfield” FDI compared with its main competitors (Moloney and Octaviani 2016).

This poor trade and investment performance is widely lamented but cannot be reduced to a simple, single explanation, as many factors have played a role. In the most charitable interpretation, Canada’s swift descent down global rankings reflects a natural catch-up phase that features remarkable success stories as some countries have rapidly integrated into GVCs in Asia (China, South Korea, India, Vietnam) and Europe (Ireland, Poland). Even among peer countries, however, Canada’s poor performance stands out. Some analysts (for example, de Munnik, Jacob and Sze 2012) rightly attribute a sizable part of this underperformance to Canada’s limited market diversification and weak productivity growth. Its international links are most developed with slower-growing advanced economies such as the United States and the European Union; despite recent gains, Canada’s engagement with faster-growing developing and emerging markets is the weakest of any G7 country’s, as Biggs notes in her chapter.

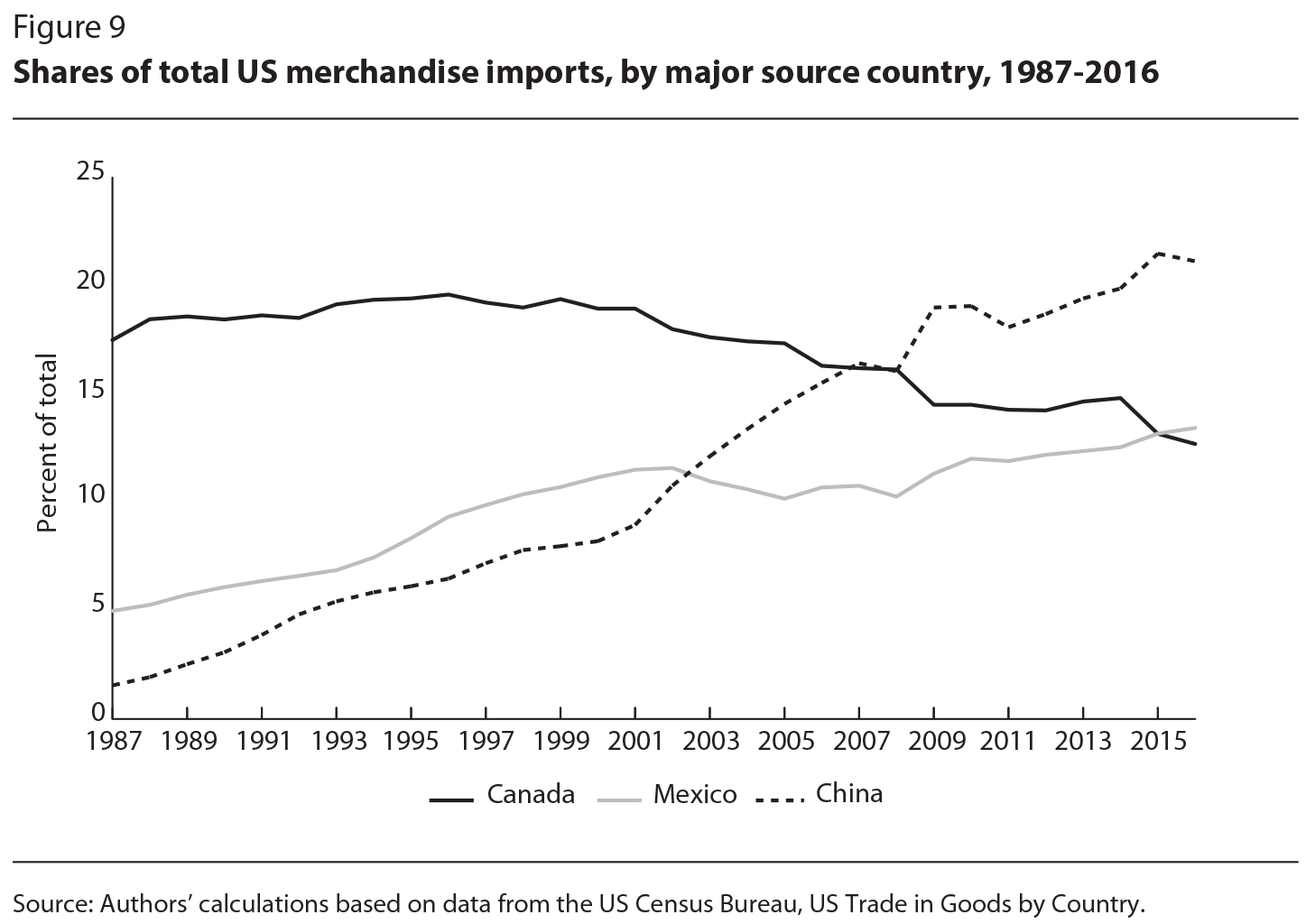

Even beyond this problematic trade orientation, however, Canada faces acute challenges in the market of the United States, by far its largest international trade and investment partner. As John Manley and Brian Kingston highlight, China and Mexico have gained significant US market share at Canada’s expense as its preferential market access has eroded over time (figure 9). Some commentators emphasize the effect of the global commodities supercycle of 2002 to 2014, which led to a strong appreciation of Canada’s currency and hampered its export competitiveness. We are not convinced, however, that the exchange rate was the primary reason for Canada’s weak overall export performance — except perhaps in a limited number of narrow manufacturing industries (Shakeri, Gray and Leonard 2012). Furthermore, even if the exchange rate did play a significant role overall, we would advocate against futile policy efforts to lower the value of the Canadian dollar artificially to try to make Canadian exports more price competitive in international markets.

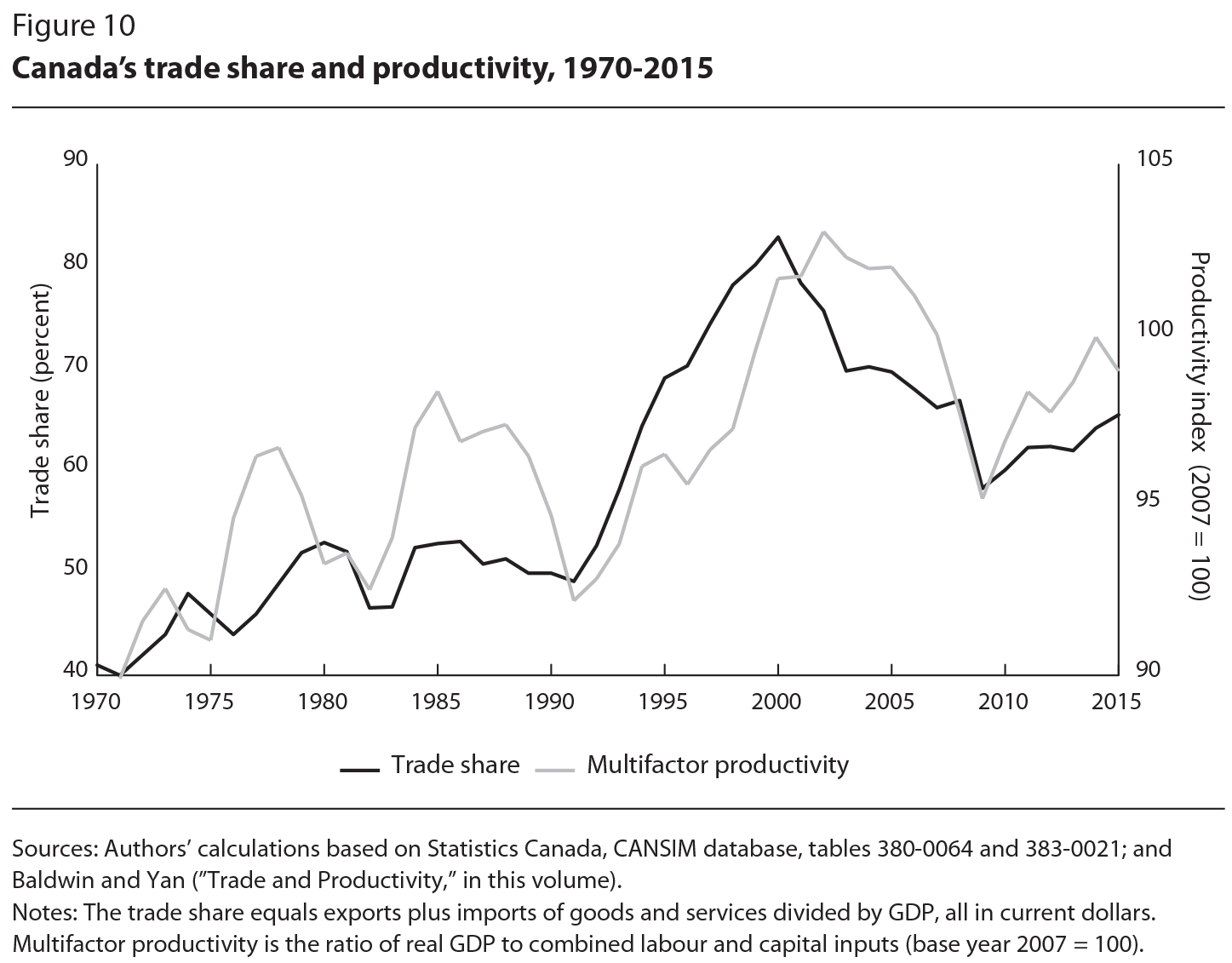

The implications of the poor international performance of Canadian firms are troubling because of compelling empirical and theoretical evidence that international trade and foreign investment can enhance productivity, innovation and growth — particularly for small, open economies such as Canada’s. To begin, as Baldwin and Yan explain in the first of their two chapters, evidence suggests that the trade share of the economy and overall business sector productivity have tracked each other closely over recent decades, which means that the downward trend in the share of trade in the twenty-first century might well be problematic for Canada’s productivity (figure 10).

Robust firm-level analysis in this volume and elsewhere supports this country-level relationship. Increased trade and trade-enhancing policies — such as tariff reductions or other actions that lower the costs of conducting business across international borders — generally have been good for the overall productivity of the Canadian economy. The rationales for enhanced trade are described throughout the volume; ultimately, however, they reflect the fact that trade promotes allocative efficiency and helps to transfer technology and know-how, which drives innovation, investment, research and development (R&D) and training (again see the first of the two chapters by Baldwin and Yan). The productivity gains from trade come from interprovincial as well as from international trade, and from importing as well as from exporting. Trade liberalization increases competition in the domestic market, inducing firms to become more efficient. Access to larger markets raises productivity by allowing firms to specialize their production, exploit economies of scale and increase their capacity use. Imports provide cheaper or better inputs to production, while offering consumers more choices and lower prices. Between 2000 and 2007, two-thirds of Canada’s effective multifactor productivity gains came from intermediate inputs produced abroad — primarily in the United States — and imported to support production by Canadian firms.

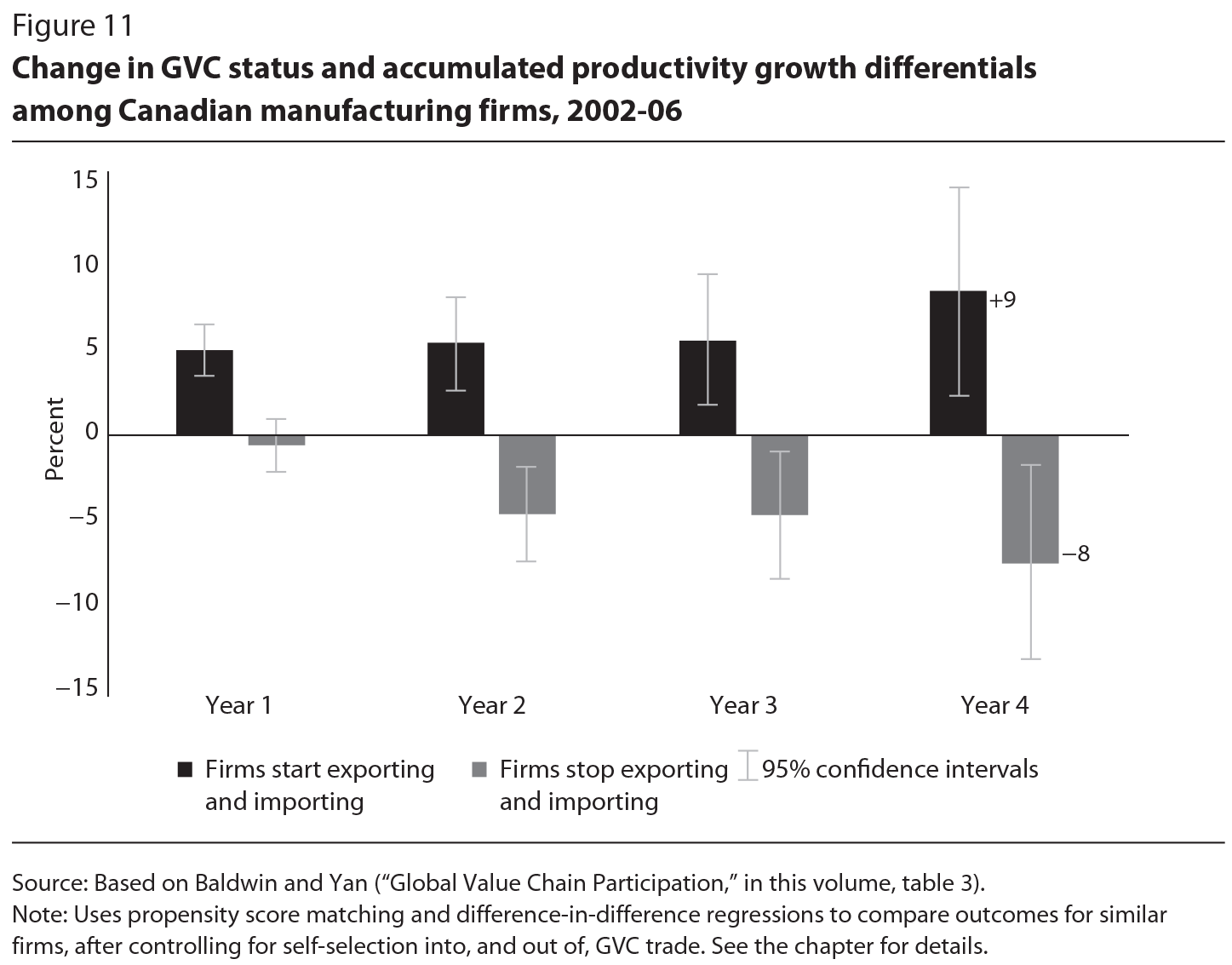

Not only do “better” firms — those that are larger, more productive and pay higher wages — become traders, as Lapham explains in her chapter; the act of trading itself improves firm-level performance. As Baldwin and Yan relate in the second of their chapters, Canadian manufacturing firms that become two-way traders — that is, they both import intermediates and export — are significantly more productive than firms with similar characteristics that only export, only import or do neither. Similarly, firms that stop two-way trading perform worse than firms that continue (figure 11). As well, as Van Assche notes, countries that have integrated more quickly into GVCs have enjoyed faster growth in real output, per capita output and employment. Unfortunately, Canadian firms have lagged behind in GVC trade as well: if GVC trade had simply maintained its share of the Canadian economy between 1995 and 2009, rather than falling by 1.5 percentage points, Canada’s real GDP per capita growth would have been nearly 0.2 of a percentage point higher per year, other things being equal.

Taken together, our research paints a pessimistic picture of Canadian firms that generally are not faring well in the context of twenty-first-century global trade realities. We nevertheless see some reason for hope. On the one hand, this disappointing performance likely reflects a variety of structural factors working against Canada that are not easily reversed, including a heavy reliance on links with slower-growing advanced economies — particularly as Canada’s share of the vital US market has fallen relative to that of emerging, lower-cost competitors. More generally, Canada’s performance within the broader nexus of trade, investment, productivity and -innovation — so central to a country’s overall economy — has also been weak across the board in recent decades. Given the strong interdependence of these variables, this outcome is not likely a coincidence. On the other hand, the engagement of Canadian firms with the major emerging markets that are now driving global economic growth is steadily increasing, even if this trend is less obvious in the traditional trade data and links with these markets remain underdeveloped. Ultimately, the evidence clearly shows that trade contributes to Canada’s growth and productivity, including through GVCs. Our reason for optimism, then, is the scope for great benefit to the economy — particularly in the context of slow output growth — if Canada can improve its currently depressed trade and investment performance.

New global realities involve many risks for Canadian trade strategy, but also opportunities. The broad-based weakness in Canada’s international economic performance over the past 15 years suggests that a concerted, comprehensive and long-term approach will be needed to improve the situation. Yet Canada faces short-term pressure to react to the uncertain trade policy orientation of its largest trading partner.

To help Canadian policy-makers keep their focus on the key long-term strategic objectives, even as they attempt to manage the risks in the short term, we present a set of recommendations, arranged in four pillars, for future trade policy (see the appendix). We stress at the outset that trade policy is not a goal in itself; rather, international engagement is an effective way to improve economic performance — in terms of productivity, innovation, investment, higher-paying jobs and income growth — as well as to advance broader goals such as a clean environment and a reduction in global poverty. In other words, crafting a trade policy agenda is about much more than deciding what trade rules to negotiate, where and with whom; it starts by considering Canadians’ broader economic and social objectives.

Each of our four pillars comes with associated policy tools and recommendations. The first pillar is an overarching one: to ensure that more Canadians share in the benefits of globalization and technological progress. If Canadians believe that the benefits are too narrowly concentrated at the top, then efforts to use more open trade to promote economic prosperity will face resistance.

The second pillar relates to resource reallocation, the key mechanism through which the growth of new trade will be unlocked and productivity improved (as the firm-level research in part 1 of this volume reveals). Here policies are needed to facilitate the reallocation of production to put capital and labour to their best uses, and to do so flexibly and quickly in response to changing circumstances in the global economy.

The third pillar is to enable international connectivity so as to enhance the ability of Canadian firms and workers to engage with foreign partners and markets (a clear message that arises from the global value chains research in part 2 of this volume). Now, more than ever, the productivity of Canadian firms and workers reflects not only their own actions but also their connections, networks and ability to collaborate with the strongest partners, regardless of where they are located.

The fourth and final pillar is to build a stronger multilateral foundation for a robust, rules-based global trade and investment system. A multilateral approach should be the default longer-term inclination, given the global nature of production, trade and investment evidenced throughout this volume. Working with other countries — including by deepening links to fast-rising emerging markets and thereby further diversifying Canada’s trade and investment — will be key to achieving this objective.

This anxiety towards the economy and trade — the worry that our kids won’t have access to the same jobs and opportunities that we have — can be addressed only if we ensure that trade is inclusive, and that everyone benefits.

— Prime Minister Justin Trudeau, 2017

Economic policy recommendations are often meant primarily to pursue economic efficiency, leaving as an afterthought how gains will be shared and losers compensated (Corak 2016). And even though improved productivity is necessary to ensure that economic progress can be broadly shared in principle, it has not been sufficient in practice (recall figure 8). Failure to make trade more inclusive may be the biggest risk for Canadian trade strategy. Indeed, demonstrating progress on inclusive trade will be vital to maintaining a permissive consensus in Canada for trade and trade agreements, which is needed if the federal government is to continue to pursue policies to increase international economic integration (Advisory Council on Economic Growth 2017).

Canada is not immune to the broader concerns that recently have manifested themselves as populist and protectionist politics and policies in the United States and Europe. Such concerns are less pronounced in Canada, but the potential for social tension increases in the current context of a slow-growing economy. Moreover, although income inequality in Canada has remained elevated since the start of the twenty-first century, the fact that it has not become more pronounced is likely due more to good luck than to good policy. Rapid growth in emerging markets helped fuel a global resource boom that significantly raised commodity prices and, in turn, demand for middle- and lower-skilled workers in Canada. The associated income gains by these workers helped to compensate for the diminished redistributive power of the tax-and-transfer system after the mid-1990s due to program cuts to employment insurance and social assistance. With the global resource boom now over, inequality in Canada could once again resume its previous upward trend (Green, Riddell and St-Hilaire 2016).

We see inclusive trade policy as one part of promoting an “inclusive growth” strategy, because inclusion, adjustment and transition cannot easily be separated into “trade-related” and “other” components. This view is in line with the idea of “predistribution,” which seeks to increase equality of opportunity — in contrast to “redistribution,” which uses the tax-and-transfer system to address inequalities after they have occurred (Hacker 2017). The OECD inclusive growth framework also identifies “health and education outcomes, social connections, personal security, work-life balance, environmental quality of life and subjective well-being as important non-income aspects of well-being” (OECD 2014, 7).

For trade to have broadly based benefits, it must be underpinned by strong social and labour market foundations. Such an agenda needs to foster shared prosperity within advanced countries, but must also include developing countries, as Biggs explains in her chapter (see also González 2016). The rest of this section discusses some issues that are specific to the trade aspects of an inclusive agenda: expanding trading opportunities to reach and benefit broader groups that previously have not been the focus of trade policy, enhancing public engagement and promoting sustainable development.

We see a focus on SMEs as part of an inclusive agenda. The returns from the increased global integration of SMEs are likely, on average, to be smaller than for larger-scale multinational enterprises,3 but because these gains are more widely dispersed, they can contribute to greater public support for trade. We noted earlier that, because of inherent differences related to firm size and trade costs, SMEs generally have had a tougher time clearing barriers to become direct international traders. Individual firms are also likely to underinvest in obtaining information on foreign trade and investment opportunities, since they fear that subsequent firms might “free ride” on their investment. Thus, the nature of such information as a public good gives governments a clear role as information providers to correct a market failure, as Sui and Tapp discuss in their chapter. Governments should pay particular policy attention to SMEs and first-time traders, which may have a harder time finding this information, but which may be more receptive to making the necessary production or organizational changes needed to succeed in foreign markets. At the same time, one should not have unrealistic expectations about what might be accomplished. In emerging markets, in particular, Canadian SMEs should understand that the potential rewards are generally higher, but so too are the risks.

The benefits of more open trade cannot be inclusive if large groups of people continue to face barriers to full participation in the economy. An inclusive trade agenda should acknowledge the striking disparities between men’s and women’s participation in trade as a result of the unique obstacles that women entrepreneurs face, as Arancha González discusses. Because men and women traditionally have had different roles in the economy and society and different access to and control over resources, the effects of trade policies are not gender neutral. As part of broader efforts to increase the scope and rigour of gender-based analysis, the federal government could regularly examine the effects of trade and trade agreements on the advancement of women’s economic empowerment, including supporting such efforts in the WTO’s Trade Policy Review Mechanism.

The pursuit of an inclusive trade agenda should also encompass ensuring public confidence in the process of reaching new agreements. As noted, concerns about trade are more muted in Canada than elsewhere, which may suggest that Canadians are generally comfortable with their country’s approach to trade negotiations. Indeed, as Robert Wolfe explains, concerns about the degree to which trade negotiations are open and transparent do not appear to be the main cause of current antitrade sentiment in other countries, nor is it clear that the degree of such transparency in negotiations makes much difference to the success or failure of negotiations. Nevertheless, we support a recent Senate committee report that makes several sensible recommendations to increase public involvement and parliamentary oversight of Canada’s trade agreements and to establish standards to measure the success of an agreement after its implementation (Senate 2017).

Firm-level data analysis has improved our understanding of the mechanisms through which trade can affect firms differently. Improved research access to anonymized data that match workers to their employers could similarly improve our understanding of the ways in which international trade and investment — and their related policies — affect Canadian workers at different parts of the wage and income distributions (see Lapham, in this volume). Such “matched employee-employer” datasets and related distributional evidence of trade effects are relatively sparse for Canada, but are growing for other countries, including the United States. Making progress in this area should be a clear priority to support the design of better-informed and more inclusive trade policy.

The UN’s Sustainable Development Goals (SDGs) offer a new way of looking at trade issues, which cannot be isolated from other economic, social and environmental factors needed for inclusive growth and sustainable development, as Scott Vaughan explains in his contribution. The universality of the SDGs could help break down the “us-versus-them” mentality that often gets in the way of mutual understanding and progress at the WTO. The SDGs provide a shared framework within which developed and developing countries can identify areas of common interest, such as responsible investment, skills development, assisting SMEs, environmental standards and green growth (see Biggs, in this volume). Canadians and people in other countries need to see how inclusive trade serves their interests and values.

A forward-looking trade policy agenda should reflect the importance of reallocating economic resources to more productive sectors, firms and activities if trade is to promote growth. Canadian policy-makers could take several steps to develop a trade policy mix to help facilitate that reallocation.

With fragmented and globalized production, governments need to create an environment in which Canadian firms can focus on activities — such as R&D, product design, marketing, logistics and after-sales services — that add the most value in supply chains, rather than necessarily performing assembly and manufacturing activities domestically. We acknowledge there are big challenges: for instance, from 2007 to 2013, the number of R&D jobs in Canada fell by 21 percent (Richards, Lonmo and Gellatly 2017). Nevertheless, getting the basic framework policies right is more important than ever. Governments could help by maintaining a stable macroeconomic environment, competitive tax rates and supportive behind-the-border policies on education and immigration to develop and attract skilled workers and entrepreneurs.

Services trade liberalization should also be considered. As we noted earlier, a country’s export and manufacturing competitiveness depends on the efficiency of its domestic services sectors, as well as on its ability to import services easily (Nordås and Rouzet 2015). Yet, as Erik van der Marel explains, despite the growing importance of services, Canada is “undertrading,” relative to economic fundamentals, with key trade partners, such as the United States and several European countries. Restrictions on foreign entry into Canada’s services sectors limit competition in the domestic marketplace and are a part of Canada’s outward export competitiveness problem. Cross-country evidence shows that reducing FDI restrictions on services trade improves competitiveness across the domestic economy (Beverelli, Fiorini and Hoekman 2017). Better access for Canadian services providers to US and European markets would also be beneficial, but the Canadian public might well resist the reciprocal access that likely would be entailed, for instance, to increase temporary foreign workers in Canada.

Overall, Canada ranks near the middle of the pack of OECD countries in the restrictiveness of its services trade policies, but it maintains high restrictions on foreign entry in several “networked” sectors, as Miroudot shows. These sectors, such as -transportation and telecommunications, are key inputs into the rest of the economy and thus have broader spillovers. Not surprisingly, Canada also lags behind in OECD comparisons of overall FDI restrictiveness — in large part because of restrictions on foreign entry into its services sectors. Recent research estimates that reducing Canada’s overall FDI restrictiveness to the OECD average would raise labour productivity in Canada by 0.8 percent, increase employment by over 130,000 jobs and increase average annual earnings per worker by almost $650 (Hejazi and Trefler 2016). We therefore recommend that the federal government take steps to promote competition in the domestic market by relaxing foreign entry requirements in, for example, backbone services sectors such as telecommunications and banking.

The regulatory framework for goods is also a determinant of participation in GVCs. Typically, regulations are developed independently by officials with little incentive or ability to take into account the cross-border economic effects of their decisions. The result is a plethora of minor differences across jurisdictions in regulations that have similar policy objectives but impose redundant or inconsistent requirements. These differences raise the cost of doing business and hinder global trade, and they have now become a top concern for companies involved in GVCs. Estimates suggest that much larger gains could be achieved from better regulatory cooperation than from further tariff cuts (World Economic Forum 2013).

Significant net benefits — including productive efficiencies and increased consumer purchasing power — are associated with having an open trade and investment environment that is integrated with the global economy. The catch is that realizing these net gains necessarily causes some economic disruptions, and some workers will lose out. Given the importance of the new (or “extensive” margin) trade spurred by trade liberalization, it may be difficult to predict which specific producers and workers will win and lose from a particular trade policy decision. This more nuanced understanding of trade adjustment puts a premium on the domestic mobility of factors of production. Taking advantage of changing economic circumstances to achieve better economic performance requires an approach that is flexible and adaptable — one that allows economic resources to follow incentives to be used to their highest potential. Promoting a highly skilled and flexible labour force is a crucial part of making trade inclusive, and that requires a high-quality education system and lifelong opportunities for workers to acquire new skills in order to adapt.

Some countries offer trade adjustment assistance (TAA) programs for workers negatively affected by trade and import competition. These programs can include providing affected workers temporary income replacement and subsidies for retraining or relocation. Lysenko and Schwartz (2015), examining the use and effectiveness of these programs across a range of countries, conclude, however, that Canada does not need a new, stand-alone TAA program. Such programs have not been particularly effective in encouraging economic adjustment — though they have played a compensatory role — and determining program eligibility is arbitrary in practice since it requires difficult judgments about which jobs or firms are negatively affected by a specific deal. Lysenko and Schwartz argue instead for a more comprehensive policy approach to enhance the skills and adaptability of Canada’s labour force. The ultimate goal should be to help workers adjust to important longer-run structural changes in the labour market — whether caused by specific trade agreements, technological change or other factors — so that they can move from jobs in declining firms to jobs in faster-growing firms.

In today’s interdependent and competitive global economy, governments that recognize the vital importance of international connectedness and adopt policies to facilitate the seamless provision of inputs, ideas, data, investment and labour across international borders will best position their firms and citizens to realize the benefits from new business models and growth opportunities.

Being connected with the global economy is fundamental to allow firms of any size to participate in GVCs. Governments thus should foster an environment in which companies and individuals can connect rapidly and reliably with foreign partners by “greasing the wheels” on both the export and import sides. In GVCs, when firms import in order to export, tariffs and other barriers to intermediate inputs are effectively a “tax on exports” that raises production costs and inhibits international competitiveness. Fast and efficient customs procedures are essential to the smooth operations of supply chains where factors of production cross borders multiple times along the way.

Empirical evidence shows that the quality of the transportation infrastructure, communications networks and regulatory environment all positively affect the ability of firms to integrate into GVCs. As Jacques Roy explains, many of Canada’s key trading partners have invested heavily in major hubs to connect various transportation modes efficiently. Canadian governments at all levels thus should work in concert to increase investment in trade-related infrastructure: road and rail capacity, border crossings, bridges, airports, ports, pipelines and communications networks, including broadband Internet facilities to help expedite cross-border exchanges (see Canada 2016).

Developing international connectivity also requires policy-makers to acknowledge that SMEs face different trade and investment barriers than do large firms. In this volume, chapters by Ahmed and Melin, Joy Nott and Sui and Tapp identify concrete ways to encourage trade by Canadian SMEs by enhancing their ability to connect with the world. Their recommendations include reviewing and reducing red tape at the border to make customs procedures as transparent

and predictable as possible; designing trade programs with SMEs’ needs in mind and promoting them better; waiving duties on low-valued shipments; and, more generally, lowering the costs for Canadian firms wishing to enter emerging markets, such as through trade and investment agreements that include specific chapters and provisions related to SMEs’ participation and post-agreement monitoring frameworks to track progress toward specified targets.

Much of what we have recommended so far the Canadian government can do on its own, but a successful trade strategy also includes working with other countries. In this regard, the multilateral trading system should be the foundation, because it provides the overall framework for Canada’s trade with the world, including within North America, and is especially important for integrating Canadian firms in GVCs.

The first goal for a small, open economy such as Canada’s should be to maintain and improve the WTO — its trade agreement with 163 other countries. Maintaining a functional WTO is essential: all significant traders are members, and its rules cover goods, services and intellectual property, as well as other topics, such as subsidies, for which no alternative negotiating forum exists. The WTO’s main principles and strengths — inclusiveness, nondiscrimination, reciprocity, transparency, and neutral and effective dispute settlement — have served Canada and the rest of the world well. This system, however, is under threat, most obviously from recent signs of a radical pivot in the United States toward the -pursuit of more protectionist policies to be pursued in bilateral negotiations. True, the WTO’s progress has been painfully slow since the beginning of the -century, leaving its members struggling to update its agenda. Although the WTO’s negotiating function remains sclerotic for now, its underlying institutional apparatus is healthy, and the effectiveness of many aspects of preferential trade agreements ultimately depends on the WTO’s robust transparency and accountability mechanisms, as Wolfe discusses.

In devising a new trade strategy for Canada, policy-makers need to consider both existing trade patterns and potential trading opportunities (i.e., extensive margin trade), but detailed forecasts of the shape of the world economy in 10 or 20 years are bound to be unreliable. The WTO is therefore Canada’s best hedge against unavoidable uncertainty — part of a future-proof trade strategy that allows Canada to take advantage of growth wherever it occurs. The WTO will wither, however, if duelling bilateral and regional trade deals come to define the universe of trade agreements.

Canada thus should work with like-minded partners to foster an eventual return to a more inclusive, cohesive and multilateral global trading system. Indeed, the current absence of multilateral leadership is an opportunity for Canada to do more than just keep the lights on at the WTO; rather, it could convene small groups to chart the future course of the trading system — including by using its analytical resources to craft informal policy papers on new issues to focus discussion — a traditional role for Canadian leadership that is needed now more than ever. Canada should also remain active in plurilateral talks — such as those developing the Trade in Services Agreement and the Environmental Goods Agreement — that eventually could strengthen the multilateral system, while being open to experiments with plurilateral approaches to other issues, such as digital trade, international regulatory and standards-setting cooperation and state-owned enterprises. The same arguments apply to the international investment regime, where the fundamental rationale is to protect and promote investments by adhering to and enforcing international standards on nondiscriminatory treatment of foreign investment. Canada and other countries have a strong systemic interest, which extends beyond any single agreement, in continuing to support a well-functioning architecture of international investment agreements backed up by effective, publicly supported dispute settlement rules, as Newcombe concludes. Efforts by Canada and the European Union to multi-lateralize the new investor-state dispute settlement provisions of the Comprehensive Economic and Trade Agreement (CETA) are a positive step on what likely will be a long road ahead on this contentious topic.

A predominant, perennial objective for Canadian trade policy is to maintain access to the (North) American market and to US-centred supply chains that is as good as or better than that of any other country. At the time of writing, the new Trump administration’s stated trade agenda had already sent shock waves across the global trading system. The details of any new US approach, however, were obscure, the new administration’s trade team was not yet in place, the President had not provided the legally required notice to Congress on his aim to renegotiate NAFTA, and it was unclear what he meant when he said during a press conference with Prime Minister Trudeau in February 2017 that NAFTA, at least with respect to Canada, needed only “tweaking.” Our comments are therefore necessarily speculative.

If Canada’s largest trading partner wants to talk about bilateral commercial arrangements, the federal government, of course, will engage, while stressing that any changes should improve, not undermine, the complex North American value chains on which jobs in both countries depend. And Canada will have no objection to a renegotiation of NAFTA — in effect, that is what both sides were doing in the TPP negotiations. The results of those (now-abandoned) negotiations will provide a rich menu of starting points when new negotiations begin. Many chapters of the TPP made advances on new issues, such as e-commerce. On the dairy industry, if Canada’s supply management programs are put on the table, the TPP outcome might be as much as the United States could expect, given its own import sensitivities. The TPP text on rules of origin might be a useful counter for Canada if the United States tries to make the NAFTA rules more restrictive. US language is found throughout the texts, notably on intellectual property; many TPP chapters represent the recent high-water mark of US ambition on, for example, labour and the environment — provisions that will be important to secure the votes in Congress of Democrats who might be inclined to support President Trump’s approach to trade agreements.

What would Canada want in any renegotiation of NAFTA beyond what was in the TPP? Both sides might want easier terms for pipeline construction. Canada might want to make it easier for professionals to cross the border to provide services, including in sectors not covered in NAFTA. Canada would want to blunt any new “Buy American” requirements, an old problem that is likely to get much worse if Congress incorporates such provisions in new infrastructure spending. Buy American -provisions already limited the ability of Canadian firms to bid on subfederal contracts that were part of the stimulus package created in response to the 2008-09 financial crisis. In 2010, Canada negotiated a waiver, applicable only to that temporary package, in return for permanently including the provinces in the WTO Government Procurement Agreement. The TPP would not have constrained Buy American provisions, but the Americans now might be willing to talk about a more permanent arrangement on procurement that would apply the higher CETA standard.

New US measures, such as a destination-based cash-flow tax and a “border adjustment tax” that Republicans have proposed in Congress, would pose strategic challenges for Canada. Should Canada negotiate a bilateral exemption or work with others in the WTO to counter such policy? Given the WTO’s strong dispute settlement system, NAFTA’s dispute settlement process is not worth much energy to preserve, especially if President Trump needed to declare victory on some aspect of the negotiation. As well, NAFTA chapter 11, on the settlement of investment disputes, is now a couple of generations behind current agreements; would Canada not counter any US pressure on this provision with the CETA approach? The principal provision in chapter 19 provides an alternative to judicial review by domestic courts of final antidumping and countervailing duty determinations. Cases involving Canada under this provision have been few in number and of declining frequency; how much is the chapter worth to Canada? Chapter 20, governing disputes about the interpretation or application of NAFTA, has rarely been used; why worry about its loss? Moreover, if the United States does indeed decide to ignore the results of WTO disputes — a plausible reading of the President’s 2017 Trade Policy Agenda — it certainly would choose to ignore NAFTA panels (Office of the United States Trade Representative 2017).

Although not part of NAFTA, the Canada-US Regulatory Cooperation Council (RCC) helps to ensure the smooth functioning of North American supply chains, and Canada should make it a priority to maintain the important work of the council. Regulatory cooperation requires building trust and promoting learning through recurrent interactions and information exchanges between regulators and stakeholders. If the RCC proves vulnerable in the current context — although we are encouraged by President Trump and Prime Minister Trudeau’s commitment, in their February 2017 joint statement, to “continue our dialogue on regulatory issues” (Trump and Trudeau 2017) — Canada could propose the creation of new North American supply chain councils. As Hoekman explains, these would be advisory bodies consisting of senior representatives from business, labour, government departments and regulatory agencies. Working around specific supply chains — narrowly defined ones for automobiles, more broadly defined ones for energy, agri-food or information and communications technology trade — their goals would be to identify areas with the most to gain from regulatory cooperation, and to establish performance indicators to monitor the implementation of policy reforms.

Finally, Canada should ensure that its trade relations with Mexico and the broader relationship are not damaged by whatever happens with NAFTA. The two countries had different interests in the original NAFTA negotiations, and Mexico will face different pressures from the Americans in the current context — on immigration even more than on trade — but Canada and Mexico will still need to make common cause on some issues, and they have a shared interest in strengthening North American supply chains.

The Canada-EU trade agreement is a considerable achievement. As we finished this chapter, the European Parliament had approved CETA, which could allow for provisional implementation of the agreement in early 2017. The political obstacles to full ratification in Europe should not prevent smooth implementation on both sides of the Atlantic. The commercial opportunities CETA will enable are important in themselves, as are innovations such as the Canada-EU regulatory cooperation forum, but the political signal that implementation will send is especially important at a time of resurgent economic nationalism in Europe and the United States.

With considerable uncertainty surrounding Brexit, the United Kingdom likely will not be in a position to solidify a new trade relationship with Canada for quite some time. In the long term, Canada should create a framework for commercial relations with the UK that is at least as good as in CETA. But negotiations on a new agreement would be futile until the UK clarifies its arrangements with both the EU and the WTO.

Our preference is multilateral first, not least because Canada already has a trade agreement with all its Asian partners through the WTO and because we are skeptical of the value of preferential agreements outside the WTO, which have significant shortcomings, as both Wolfe and Blanchard note in their chapters. Systemically important traders are omitted from preferential negotiations, often by design; significant aspects of the modern trade policy agenda are not covered; and overlaps and inconsistencies between agreements will ultimately become unmanageable for the many large multinational firms that operate in multiple markets. Although these agreements can improve market access in traditional areas, such as tariffs, and solve particular supply chain problems, institutional deficiencies limit their effectiveness and make it difficult to achieve real gains in areas such as regulatory cooperation.

Nevertheless, we believe that Canada should strengthen its economic linkages in particular with China by launching formal trade negotiations with what is now the world’s largest trader and Canada’s second-largest trading partner. Such bilateral negotiations would help both sides learn about how to integrate China further into the global trading system. American hostility toward China might create difficulties for Canada, but it would also increase the systemic importance of engagement.

The collapse of the TPP after the US withdrawal means that Canada has lost, at least for now, what would have been an important new agreement with several other TPP participants, notably Japan, Mexico and Australia. Canada already has a framework for bilateral talks with Japan and a good sense of that country’s positions on many issues because of the TPP negotiations. But would Japan want to be part of a trade agreement that did not include the United States? How would market access work? Would Canada be trading better access for its exports of beef, pork and natural gas, in return for more Japanese automobile imports into Canada? Some TPP participants, though not Japan, have expressed interest in pursuing the agreement without the United States. Were they to do so, each chapter would have to be assessed to determine if the compromises made to satisfy US interests still make sense — no simple process. For Canada, rules of origin would pose a particular negotiating challenge given the dependence of many Canadian sectors on inputs from the United States.

The situation in Asia might change quickly as countries adjust to a new US orientation. The proposed Regional Comprehensive Economic Partnership (RCEP) is less ambitious than the TPP with respect to new rules, but it offers greater potential for gains in market access. Canada should consider whether participation offers worthwhile opportunities, especially if more of its key trading partners join the negotiations. On the other hand, would China and South Korea, both party to the RCEP negotiations, be interested in joining a revamped TPP? If so, some chapters, such as the one on state-owned enterprises, would need to be substantially rewritten. The participation of those countries, however, might tip the balance toward a re-engagement in the TPP.

Developing countries are the new engines of global growth. Engaging with these markets is thus a source of long-term competitive advantage for Canada. As Biggs argues, however, business-as-usual approaches will not get Canadian investors and firms to the high-growth frontiers of global economic activity. More-inclusive trade could also reduce global poverty and advance sustainable growth, both objectives for Canadian foreign policy in general — indeed, such an agenda is key to the future success of the international trading system, and to Canada’s efforts to play a leadership role in global fora such as the UN Security Council. To that end, Canada should help developing countries improve their trade capacities through the WTO’s Trade Facilitation Agreement, which expedites the movement of goods across international borders by creating norms for customs and logistics. Given the unprecedented levels of investment required to help developing countries grow, the need for development finance has never been greater in a wide variety of areas, such as climate-smart transportation, connectivity, water and sewage, clean energy and energy efficiency. If Canada is to play a leadership role in this process, it needs a development finance institution of global scale and ambition to attract private capital and demonstrate clear development effects.

The new global trade realities described in this chapter highlight several -important shifts in economic activities, thinking and policy focus. Taken together, the research in this volume calls for a trade policy approach that better recognizes the role of firms and the tasks they perform; that gives more weight to value-added trade and services and the activities of foreign affiliates; and that considers the need to reallocate resources within the economy to fuel new trade and growth.

These new realities also highlight the importance of enabling international connectivity and collaboration, particularly in light of recent calls for thicker international borders. Now more than ever, countries cannot become stronger by going it alone. Any jobs “saved” by protectionist policies will come at a high cost in reduced productive efficiency, slower growth and lower living standards. The evidence presented here supports a strong preference for a multilateral first approach because of the integrated and interconnected nature of global commerce. The new US approach to focus on bilateral trade agreements is at odds with these realities, where global commercial activities often involve production platforms and partial owners in multiple countries. Canada’s interests and those of other small, open economies ultimately lie in a transparent, rules-based international trade and investment system, not an ad hoc, deals-based system. At the same time, in this pursuit, the federal government should continue to help Canadian firms engage with the fast-growing emerging markets that are increasingly driving global growth, and help these countries integrate better into the global economy and the governance of the main international institutions.

More generally, trade policy needs to become more “inclusive,” both in Canada and in other countries. By this we mean trade that is more open to all participants in the global economy, including women, SMEs and developing and emerging countries — and, importantly, ensuring that the income gains from increased trade are shared more broadly within countries. An indispensable part of a more inclusive trade policy agenda should be developing stronger social safety nets to support individuals whose jobs are negatively affected by a variety of economic dislocations, by emphasizing skills development and retraining.

We started this chapter by acknowledging that Canada’s trade policy is now at a risky crossroads. The pervasive ongoing uncertainty about global trade relations is a compelling reason to be clear-headed and deliberate in defining Canada’s long-term trade policy priorities. We have outlined some starting points and fundamental priorities that we think should constitute Canada’s policy focus. We hope our policy road map, together with the empirical evidence and theoretical framework articulated in this volume, will stimulate fruitful discussions about how a more comprehensive approach to the design of Canadian trade policy could help achieve more inclusive economic prosperity.

Help ensure that all Canadians can share in the benefits of globalization and technological progress

Promote economic prosperity by putting resources to their best uses

Allow Canadian firms and workers to better engage with foreign partners

Build a more comprehensive, coherent and inclusive rules-based system for global trade and investment

Advisory Council on Economic Growth. 2017. Positioning Canada as a Global Trading Hub. Accessed March 21, 2017. https://www.budget.gc.ca/aceg-ccce/pdf/trade-commerce-eng.pdf

Autor, D., D. Dorn, and G. Hanson. 2013. “The China Syndrome: Local Labor Market Effects of Import Competition in the United States.” American Economic Review 103 (6): 2121-68. Accessed March 21, 2017. https://www.aeaweb.org/atypon.php?doi=10.1257/aer.103.6.2121

_____. 2016. “The China Shock: Learning from Labor Market Adjustment to Large Changes in Trade.” Annual Review of Economics 8: 205-40. Accessed March 21, 2017. https://www.ddorn.net/papers/Autor-Dorn-Hanson-ChinaShock.pdf

Beverelli, C., M. Fiorini, and B. Hoekman. 2017. “Services Trade Policy and Manufacturing Productivity: The Role of Institutions.” Journal of International Economics 104: 166-82. Accessed March 21, 2017. https://www.sciencedirect.com/science/article/pii/S0022199616301441

Brown, M. 2015. How Much Thicker Is the Canada-US Border? The Cost of Crossing the Border by Truck in the Pre- and Post- 9/11 Eras. Economic Analysis Research Paper 99. Ottawa: Statistics Canada. Accessed March 21, 2017. https://www.statcan.gc.ca/access_acces/alternative_alternatif.action?l=eng&loc=/pub/11f 0027m/11f0027m2015099-eng.pdf

Canada. 2016. Pathways: Connecting Canada’s Transportation System to the World. Accessed March 21, 2017. https://www.tc.gc.ca/eng/ctareview2014/CTAR_Vol1_EN.pdf

Cardwell, R., C. Lawley, and D. Xiang. 2015. “Milked and Feathered: The Regressive Welfare Effects of Canada’s Supply Management Regime.” Canadian Public Policy 41 (1): 1-14. Accessed March 21, 2017. https://dx.doi.org/10.3138/cpp.2013-062

Cernat, L. 2014. Towards “Trade Policy Analysis 2.0”: From National Comparative Advantage to Firm-Level Trade Data. Chief Economist Note, issue 4. Brussels: European Commission. Accessed March 21, 2017. https://trade.ec.europa.eu/doclib/docs/2014/november/tradoc_152918.pdf

Ciuriak, D., B. Lapham, R. Wolfe, T. Collins-Williams, and J.M. Curtis. 2015. “Firms in International Trade: Trade Policy Implications of the New New Trade Policy.” Accessed March 21, 2017. Global Policy 6 (2): 130-40. https://onlinelibrary.wiley.com/doi/10.1111/1758-5899.12183/abstract

Coiteux, M., P. Rizzetto, L. Suchanek, and J. Voll. 2014. “Why Do Canadian Firms Invest and Operate Abroad? Implications for Canadian Exports.” Discussion Paper 2014-7. Ottawa: Bank of Canada. Accessed March 21, 2017. https://www.bankofcanada.ca/2014/12/dis cussion-paper-2014-7/