Canadian Policy Prescriptions for Dutch Disease

Robin Boadway, Serge Coulombe and Jean-François Tremblay

Since legislation to establish a national securities regulator was tabled in May 2010, there has been a debate around the constitutionality of the legislation, and the Supreme Court is expected to render a decision on the question sometime in 2011. But independent of the constitutional issue, an equally important question is the one Pierre Lortie takes up in this study: Would such a change be sound public policy?

Lortie begins by assessing how Canada’s decentralized securities regulation system has performed according to several measures (including adoption of best practices, cost of regulation, investor protection and business cost of equity), and he concludes that it compares favourably with those of other countries.

The author attributes this performance to a high degree of coordination among provincial regulatory authorities. The national reporting systems and harmonized standards cover many aspects of securities markets. Furthermore, dealers can register and companies can clear prospectuses with the regulator in their home province or territory and have it apply in all other jurisdictions, except Ontario. The fact that Ontario is not part of this so-called “passport” system is an inefficiency that the author recognizes, and he urges Ontario to join.

An important asset of the current system in the author’s view is that it can cater to regional economic differences, which are considerable in Canada. A national regulator would have neither the ability nor the incentive to cultivate the smaller regional exchanges across the country (such as the TSX venture exchange in Calgary) that cater to clienteles with unique needs. The vibrancy of these exchanges is particularly important in Canada, since other sources of corporate finance (such as venture capital markets and private equity) are scarce compared to those in other countries.

Lortie’s conclusion is unequivocal: Notwithstanding legitimate critiques of certain details in the functioning of the current system, Canada has by any measurable criterion a regime that is recognized as one of the best in the world. He finds no evidence whatsoever to support the notion that a national securities regulator would better serve Canada’s needs and interests.

In his commentary, Thomas Hockin, who chaired the 2009 expert panel that recommended a national securities regulator, has a decidedly different perspective. He questions the ability of the current system, however coordinated and harmonized, to react quickly enough to developments in global markets that would have national repercussions in Canada. In addition, he argues that a national regulator would improve investor protection by ensuring better enforcement. As well, it would be organized in such a way as to retain flexibility vis-à-vis regional differences.

On May 26, 2010, the federal government released a proposed Canadian Securities Act and, concurrently, asked the Supreme Court of Canada for its opinion regarding the legislative authority of Parliament to adopt such an Act. The federal proposal is all-encompassing: it would give the federal government control over the securities regulation domain through a comprehensive statutory and regulatory regime administered by a single national regulator. The federal initiative thus constitutes a direct challenge to an area that has long been acknowledged to be within the exclusive jurisdiction of the provinces by virtue of article 92.13 of the Constitution Act, 1867.1 Indeed, two provincial courts of appeal – that of Alberta on March 8, 2011, and that of Quebec on March 31, 2011 – have rendered their decision that the federal proposal, as it stands, is unconstitutional. The Supreme Court of Canada heard interested parties in April 2011, and its decision in the matter of the reference is eagerly awaited. Little noted in the public debate, however, is the federal government’s contention that both Parliament and the provinces have constitutional authority to adopt comprehensive securities legislation and that, in conceding authority to Parliament to do so, the Supreme Court would not be restricting or reducing the constitutional jurisdiction of the provinces.

Issues of two different orders arise from the federal government’s initiative. The first lies in the constitutional realm, which, however, is not the subject of this study. The second pertains to the merits of the federal initiative per se. Is the transition to a single national securities regulator under the jurisdiction of Ottawa sound policy and worth pursuing? Is the transfer of jurisdiction likely to improve materially or, rather, undermine the efficacy of securities regulation in Canada? What are the costs and risks associated with such a fundamental change in the Canadian securities regulatory architecture embodied in the proposed Act? After all, it would be of dubious value to pit the federal government against a majority of provinces in a constitutional battle over this matter unless it could be demonstrated that the performance of the current securities regulatory regime is significantly inferior to what is observed in other countries and that a centralization of the regulatory apparatus is necessary to correct its shortcomings.

The competing economic arguments in this debate can be summarized as follows. Proponents of a single regulatory system posit that centralization is the best approach to securities regulation in Canada since, at the core, uniformity is viewed as necessary to achieve efficiency, and divergence is per se undesirable: “Only a single federal regulator administering a single federal body of law has the power to ensure that market rules are applied consistently across the country” and to “establish a uniformly high standard of investor protection across the country” (Attorney General of Ontario 2010, 21). The current regulatory structure, described in more detail later in this study, is provincially legislated and managed, with each of the 13 provinces and territories having its own securities commission or equivalent authority and accompanying legislation. Thus, preserving the national scope of Canada’s securities markets requires cooperation and coordination among many different jurisdictions, a characteristic that is depicted as a fatal shortcoming that would render the system slow to adapt and respond in a timely manner to important market developments. It is also asserted that “[securities] enforcement could be strengthened across Canada under unity of command” (Crawford 2010). In essence, the argument is that the dynamics inherent in a federal system should be suppressed in the securities field because they are inimical to Canada’s best economic interests. Proponents of a single regulatory system also argue that a national regulator is essential because securities markets are increasingly global in reach and the interdependencies that result call for securities regulation at the international level. This, they argue, necessitates a single Canadian perspective and unified representation in world forums where securities matters are addressed.

Proponents of the current regime, in contrast, insist that, given the heterogeneity of Canadian securities markets – characterized by diversity among regional industries, types and sizes of issuers and local capital market infrastructures – the current regulatory architecture is, in fact, a strength. In short, they reject the proposition that centralization of the regulatory regime is a desirable goal. They argue that under such a national regulatory regime the concentrated structure of a securities industry dominated by six major chartered banks and closely intertwined with the regulatory and economic policy instruments of the federal government would increase significantly the influence of these banks on the formulation of securities policies and regulation to suit their own interests – a risk compounded by the highly concentrated geographic location of major decision-makers in the Canadian financial industry.2 Moreover, high concentration levels would put a premium on uniformity, whereas the varying profile of issuers across Canada requires different regulatory priorities, the flexibility to assess the differential impact of regulatory initiatives, and the ability to adapt regulations accordingly.

In essence, the case for the current securities regulatory architecture rests on two major arguments. First, the close collaboration among the Canadian Securities Administrators produces the most effective response to Canada’s diverse economic needs; it has delivered a regime of securities regulation that is considered one of the world’s best, characterized by a high degree of harmonization in securities legislation and regulations across the country, save where differences fairly reflect local circumstances. Second, the current regime is more efficient from a dynamic perspective because each securities commission is accountable within its region and, therefore, has incentives to pay more attention to the needs and characteristics of its regional economy than to the preferences of the securities industry.

The globalization of capital markets and the urgent need to mitigate the corrosive effects of the phenomenon – as evidenced by the 2008-09 financial crisis – through appropriate regulation are not in dispute. Proponents of the current regulatory architecture are not swayed, however, by the unrestrained use of the recent crisis as a justification for the centralization of securities regulation in Canada. For them, the crisis, which originated in the United States, was mainly the result of inappropriate economic and monetary policies, a failure of prudential regulation and lack of foresight in mitigating and containing systemic risk, a host of issues that lie outside the purview of securities law.

Supporters of a single regulator like to point to a series of royal commissions and high-level task forces that, since 1935, have recommended the establishment of a federal securities commission with comprehensive regulatory powers. They conveniently fail to mention, however, that the Macdonald Commission, which had the explicit mandate to study and propose measures to improve the performance of Canada’s economic union, did not embrace such an enlargement of federal jurisdiction in its 1985 report. Provincial regulation of the stock markets constitutes a particularly interesting example. In principle, there seems to be a strong argument for federal regulation. In practice, we have achieved much the same result with provincial jurisdiction (Report of the Royal Commission on the Economic Union and Development Prospects for Canada 1985, vol. 3, 167). They also fail to explain why no federal government has implemented any such recommendation.

All federal commissions or task forces that have recommended a single federal securities regulator have done so in the context of the conditions that prevailed at the time, contending that the existing regulatory apparatus was not capable of fostering the development of a market infrastructure that ranks with the best worldwide. But subsequent developments typically have proved them wrong. For example, in supporting a draft securities act in 1979, the Department of Consumer and Corporate Affairs stated that federal government involvement in securities matters was necessary because it would be impractical for the provinces to establish a book-entry national clearing system.3 Today, the Canadian Depository for Securities Limited is just that.

There is no denying that the globalization of capital markets – particularly non-regulated over-the-counter derivatives and interbank markets – requires coordinated regulatory measures. To a very large extent, however, the key instruments of policy necessary for this task are already under the control of the federal government. Hence, the focus should be on resolving these issues, which, when all is said and done, the proposed Securities Act does not address. The public debate on the Canadian securities regulatory regime is, at its core, between competing views about the “best” structure. In a nutshell, the central questions are whether a single regulator is optimal in the Canadian context, and whether such a federal agency would be functionally superior to the current decentralized architecture.

This study is structured as follows. In the first part, I review the empirical evidence concerning the functional performance of the Canadian securities regulatory regime on the continuum from regulatory inputs to market outcomes. In the second part, I address one of the major reasons many provinces are opposed to the federal initiative by examining the respective merits of a centralized securities regulator and the current multijurisdictional architecture with respect to regional economic growth. In the third part, I address concerns pertaining to the capacity of the current regulatory regime to cope with issues related to the globalization of capital markets and the systemic risk this phenomenon entails. In concluding remarks, I draw together the key findings.

Securities regulation is primarily concerned with issues of business conduct. The main purpose of securities regulations is nicely captured by the following provision of the Ontario Securities Act: to “provide protection to investors from unfair, improper or fraudulent practices; and to foster fair and efficient capital markets and confidence in capital markets.” A similar provision is found in modern securities legislation around the world. The International Organization of Securities Commissions (IOSCO) Objectives and Principles of Securities Regulations provide a comprehensive framework for capital markets regulation and the characteristics of a sound regulatory regime. The IOSCO Principles delineate the essential qualities and powers of a capital markets regulator; the elements of proper oversight of issuers; collective investments, intermediaries and markets; and the components of an effective enforcement regime. A large consensus prevails in this regard, which explains the regulatory convergence, harmonization and mutual recognition observed internationally among jurisdictions. The reduction of systemic risk was added as a core objective in 1999, reflecting the fact that securities commissions generally exercise prudential oversight aimed at ensuring the financial integrity of securities firms and market infrastructure organizations. To a very large extent, however, this is no longer the case for provincial securities regulators in Canada since this task is already performed by federal government regulators with respect to the parts of the Canadian securities industry that may present a systemic risk for the country.

Regulation is not an end in itself. The purpose of securities regulation is to improve market outcomes – the measures of economic activity that relate to the efficient and effective functioning of securities markets. It is on this basis that the performance of a regulatory regime should be assessed, not solely on regulatory inputs and the pursuit of similarity in regulatory requirements and supervisory structures and approaches. To be sure, the causal relationship between regulatory inputs and market outcomes is often blurred, calling attention to intermediate indicators such as compliance activities, issuer and securities industry behaviour, transaction costs and investor confidence. In several instances, the structure and performance of the industry are the dominant determinants of market outcomes. It is noteworthy that considerations pertaining to the highly concentrated structure and behaviour of the Canadian financial industry are generally absent from the public debate, whereas these features are major determinants of the dynamics of primary and secondary capital markets. In a nutshell, the efficiency and competitiveness of capital markets and financial centres depend on a complex mix of private and public factors that need to be analytically untangled if public policy is to be based on a sound footing.

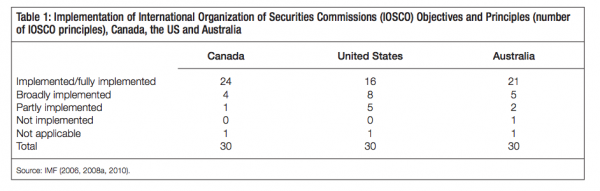

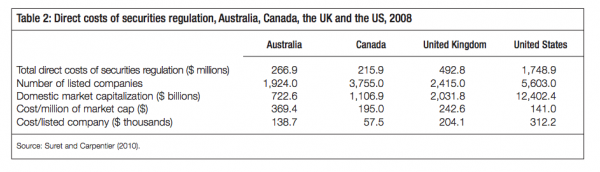

A recent assessment by the International Monetary Fund (IMF) confirms that securities regulation in Canada conforms to the IOSCO Principles and Objectives (IMF 2008a,b). Table 1, which compares the aggregate ratings from the IMF assessments of Canada (2008), the United States (2010) and Australia (2006), shows that the major Canadian securities commissions have been diligent in implementing best practices.4 Thus, the suggestion of the Wise Persons’ Committee (2003, 34) that “if Canada were to [centralize] its securities regulatory structure, it could have the same level of regulation at materially less cost, or much better regulation at the same cost,” has no basis in fact. Rather, the comparative data shown in table 2 do not support the contention that the total direct cost of Canada’s securities regulatory apparatus is larger than that of common law jurisdictions with a centralized regulator. As a percentage of total capitalization, the total direct cost of Canada’s securities regulatory apparatus is significantly lower than that of Australia or the United Kingdom. Indeed, when compared on the basis of the number of listed issuers, the cost of the Canadian securities regulatory apparatus is by far the lowest among common law jurisdictions.

Lower direct costs should not be interpreted, however, to mean that Canadians are being short-changed. In a study commissioned by the Task Force to Modernize Securities Legislation in Canada, Jackson (2006) concludes, “In terms of budgets and staffing levels, the Canadian regulatory system is comparable to the overall regulatory system in the United States.” At least from the point of view of direct regulatory inputs, proponents of a single securities regulator have yet to make their case. For the Canadian Securities Administrators, a constant concern is to reduce compliance costs for participants while preserving the quality and effectiveness of the regulatory regime. The Wise Persons’ Committee singled out three examples of inefficient regulatory divergence as evidence of unnecessary compliance costs, pertaining to substantive registration requirements, the procedure and conditions for private placement exemptions and the rules restricting the resale of securities initially sold under a prospectus exemption; all three matters have since been substantially harmonized across Canada.5

In practice, it is the de facto functioning of the regulatory regime that matters to participants, not the de jure aspects. The Canadian regulatory regime is highly harmonized and characterized by

The passport system ensures that public companies are subject to only one set of harmonized continuous disclosure requirements. Despite its preference for a centralized regulator, the Crawford Panel on a Single Canadian Securities Regulator (2006) confirmed that the benefits accruing from implementation of the principal regulator system, which preceded the full implementation of the passport system, were significant and recognized by industry participants.

On the critical dimension of market fairness, comparisons by the Organisation for Economic Co-operation and Development (OECD), the IMF and the Milken Institute consistently rank Canada among the best with respect to the quality of its securities regulations and investor protection. Additionally, a substantial body of independent, peer-reviewed empirical studies (summarized in Lortie 2010) confirms that the fairness and efficiency of Canadian capital markets rank with the best worldwide. The uniform regulatory framework that governs takeover bids and going private transactions firmly establishes as its cornerstone that all shareholders must be treated fairly. The mandatory coattail provision, which requires that, in such events, all shareholders be treated equally, is a significant contributor to these favourable results.

Moreover, the Canadian securities regulatory regime and capital markets enjoy considerable recognition and respect worldwide. At the institutional level, Canada has always exerted a great deal of influence within IOSCO. The Quebec Autorité des marchés financiers (AMF) and the Ontario Securities Commission (OSC) have voting status and, since IOSCO’s founding, have been members of both its executive committee and its technical committee.7 The Alberta and British Columbia securities commissions are associate members. Even though Canada’s capital markets represent only about 3 percent of the global capital markets, only Canada, China and the United States have two IOSCO memberships. Moreover, several Canadian securities commissions participate actively in the North American Securities Administrators Association and the Council of Securities Regulators of the Americas. In addition, Canada is the only country to have a mutual recognition and harmonization agreement – the Canada/US Multijurisdictional Disclosure System (MJDS) – with the SEC. The MJDS is “a unique system only available between Canada and the US. The SEC in the US and each of the provincial securities commissions have agreed to recognize the other’s prospectus review system and automatically accept prospectuses cleared by the other without further review” (IIAC 2010, 46). The MJDS has stood the test of time and remained in force for close to 20 years – surely a measure of the SEC’s high regard for the consistent quality of securities regulation in Canada.

With respect to investor confidence, it stretches credibility to lament that the Canadian securities regulatory regime is, in the words of federal Finance Minister Jim Flaherty, “a national embarrassment” at the international level (Singleton 2011) and, at the same time, to boast that foreign investors and issuers are increasingly active participants in Canada’s capital markets. In testimony before the Select Committee of the Legislative Assembly of Ontario on the proposed merger of the Toronto Stock Exchange (TSX) and the London Stock Exchange (LSE), it was reported that, over the past five years, issuers listed on the TSX and TSX Venture Exchange (TSX [V]) accounted for 80 percent of the mining equity financing across the globe. In addition, in their attempts to merge with or acquire the TMX Group, both the LSE and the Maple Group referred to the TMX Group’s global leadership in the resources sector and its expertise with respect to small and medium enterprises (SMEs) and public venture capital financing for early-stage growth companies. These votes of confidence belie any suggestion that Canadian equity markets are not well regulated or are uncompetitive on a global basis.

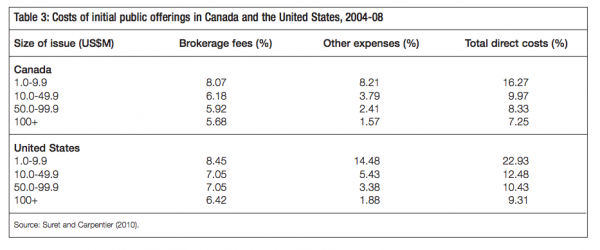

The cost of securities regulation governing the issuance of stock in public markets is embedded in the direct costs borne by the issuer.8 A comparison of the cost of initial public offerings (IPOs) in Canada and the United States shows conclusively that the Canadian securities regulatory regime does not impose on Canadian issuers, including junior issuers, a burden that is higher than that in the United States. The results presented in table 3 for the 2004-08 period are in line with those of previous studies of IPO costs in Canada and the United States over the 1997-99 period (see, for example, Kooli and Suret 2003). If anything, the cost of IPOs in Canada as a proportion of the size of the issue decreased over the 1997-2008 period. In short, contrary to prevailing views, the Canadian multijurisdictional regime places a lighter cost burden on issuers than that imposed in the US market.

With respect to enforcement, it is essential to note that Canadian securities commissions are not criminal enforcement agencies; rather, their main recourses are administrative, civil and penal sanctions, and it is on these dimensions that the performance of the current regime must be assessed. Responsibility for the investigation and prosecution of criminal activity in capital markets rests with the police and attorneys general. Parliament has exclusive jurisdiction to bring securities crimes under the ambit of the Criminal Code. The federal government already has responsibility for the enforcement of the Criminal Code provisions concerning securities fraud and the prosecution of serious offences, since the Attorney General of Canada has concurrent jurisdiction to prosecute fraud-related cases, including insider trading offences.

Critics of the Canadian regime often use raw comparisons of the number of enforcement actions in Canada and the United States in the public debate. Indeed, the US/Canadian ratio of public enforcement actions is about double the ratio for domestic market capitalization. The validity of the conclusion drawn from these top-line comparisons, however, rests on two implicit assumptions. The first is that the incidence of securities violations and criminal offences must be the same in both countries, yet wide differences in crime trends across other segments of the two countries’ societies cast serious doubts that this assumption is reasonable. Moreover, the high level of concentration of the securities industry in Canada enhances the level of compliance across the country and accordingly reduces the incidence of violations compared to what occurs in a fragmented and highly dispersed structure.

The second assumption is that regulators in the two countries have the same propensity to rely on ex post sanctioning and litigation rather than on ex ante supervision, but an analysis of the lessons drawn from many developed markets other than the United States suggests otherwise. For instance, a comprehensive study of the regulation of related-party transactions in 72 countries (Djankov et al. 2006) demonstrates that common law countries typically emphasize ex ante measures such as extensive disclosure and the approval of related-party transactions by disinterested shareholders. The United States, however, is unique in placing greater emphasis on ex post litigation and enforcement mechanisms. These findings, which reinforce those of earlier studies of securities law, show that regulatory requirements concerning private contracting, transparency and full public disclosure of information coupled with private enforcement mechanisms are significantly more effective than public enforcement in promoting efficient capital markets (La Porta, Lopez-de-Silanes and Shleifer 2006). It does not follow that public enforcement does not have a role to play, but it is ill-advised to overstate its importance and beneficial impact on market outcomes.

Interestingly, detailed comparisons of the records of public enforcement actions in Canada and the United States during the 2002-04 period are instructive in that they actually lead in a direction opposite to that advocated by the federal government. In the United States, the superiority of state agencies in taking public enforcement actions (40.8 percent of public enforcement actions versus 17.6 percent for the SEC) is clearly established (Jackson 2006). Indeed, the jurisdiction of state securities commissions to investigate and bring enforcement actions with respect to fraud, deceit or unlawful conduct in connection with securities transactions was explicitly preserved under the National Securities Markets Improvement Act of 1996, while the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 confirmed the jurisdiction of the states under the NSMIA and expanded the investor protection and enforcement roles of state securities regulators.

Clearly, proximity and knowledge on the part of individual players render enforcement more effective. The important role given to self-regulatory organizations (SROs) in the supervisory and enforcement machinery in Canada and the United States is based on that premise. The comparative data concerning enforcement by SROs show, first, that the ratio of enforcement actions taken by Canadian SROs and their US counterparts is no different than the proportion of enforcement actions taken by Canadian securities commissions relative to those taken by US federal and state agencies; and, second, that the proportion of monetary sanctions imposed by SROs relative to those imposed by government agencies is 31 percent in the United States and 12 percent in Canada. These results provide ample reasons to refute the contention that the architecture of the Canadian securities regulatory regime explains the difference in the incidence of enforcement actions in the two countries.

Few enforcement issues have more political resonance than illegal corporate insider trading. The number of high-profile criminal indictments for illegal insider trading in the United States compared to the rather subdued record in Canada has prompted many to insinuate that insider trading is a scourge in Canadian capital markets (Insider Trading Task Force 2001). The empirical evidence again tells a different story. A study of 420 takeover announcements of publicly listed Canadian firms from 1985 to 2002 (King and Padalko 2005) demonstrates conclusively that the magnitude and timing of pre-bid runups for Canadian and US takeovers are very similar and that the price-volume dynamics in the case of Canadian takeovers are more consistent with the predictions of the marketanticipation hypothesis than with that of illegal insider trading. As the study notes, “While we cannot dismiss the possibility of illegal insider trading in any takeover in our sample, the evidence suggests that this problem is not widespread for this type of corporate event” (3).

When devising measures to eradicate the occurrence of illegal insider trading, account must be taken of the fact that the typical insider transacts only modest amounts of shares – on average, fewer than 10,000. An analysis of detailed trading data in the period preceding important announcements on several exchanges leads Michael Aitken to conclude: “Of some surprise is the generally low level of activity…The numbers ranged on average across markets from 1.7/100ths of 1 percent to 4.4/100ths of 1 percent” (2010, 8; see also Market Regulation Services 2004). It would also appear that illegal trading by corporate insiders takes place early in the process, not immediately before the announcement. The impact of such trading is therefore generally inconsequential to the market and hence very difficult for exchanges or regulators to detect.

It has also been demonstrated that efforts to manipulate a security’s closing price at the end of a trading session induce volatility and raise the cost of executing larger trades through a widening of market spreads. The incidence of such manipulative trading behaviour can be estimated by the mean frequency of daily exchange stock-price-ramping alerts. The results of a rigorous study show that the “mean alert incidence” per thousand listed securities was 0.88 for the TSX compared with 1.01, 1.28 and 1.04 for the Australian Stock Exchange, the LSE and the New York Stock Exchange, respectively (Aitken, Harris and Ji 2010). Here again, market design measures, the prohibition of certain trading practices and real-time surveillance (ex ante) are significantly more effective in preventing trade-based manipulation than ex post enforcement penalties.

Relative to gross domestic product (GDP), the market capitalization of Canadian issuers is greater than that of issuers in most developed economies, a measure indicative of a well-developed and efficient capital market (Hendry and King 2004).

Canadian corporations raise about one-quarter of their financing needs abroad, mostly in the United States. In the 2000s, the share of foreign placement of new Canadian equity securities represented around 20 to 25 percent of total issuance value. In the case of corporate bonds, the portion sold offshore, mostly in the United States, was about 40 percent. These US offerings are, on average, twice the size of Canadian offerings, a clear indication that the factors at play are not of a regulatory nature but, rather, a direct consequence of the size and depth of US corporate and high-yield bond markets. Moreover, according to data from the Bank for International Settlements, foreign loans account for 40 percent of total bank loans to the Canadian nonbank sector (Klyuev 2008). Based on the proportion of foreign financing in each source of funding, Canadian public equity markets are very competitive, at least compared to other sources of corporate financing.

Another indication of the relative health of market outcomes in Canada is the finding that, unlike Canada, the United States is experiencing a secular decline in its population of listed companies. Between 1996 and 2008, the total number of companies listed on a US exchange declined by 38.8 percent, while domestic company listings declined by 43 percent. In Canada, during the same period on the TSX, the total number of listed companies increased by 10.6 percent. These results are a direct consequence of IPO activity in the two countries, which, between 1990 and 2006, increased by 396 percent in Canada and 129 percent in the United States. As a result, the aggregate value of equity raised in Canada through IPOs relative to that raised in the United States grew from 6 percent in the 1990-95 period to 20 percent in the 2001-06 period (Cetorelli and Peristiani 2009).

Other international comparisons indicate that, relative to other jurisdictions, the Canadian securities regulation regime facilitates access to public capital markets by Canadian issuers. According to the IMF, “The current system has responded to the specific characteristics of its capital market, such as allowing for a large presence of small issuers, and the concentration of certain industries in specific provinces” (2008a, 37). On the basis of their listing requirements and international criteria, the TSX is considered a junior market whereas the TSX (V) is a public venture capital market. Overall, about 3,600, or 94 percent, of the companies listed in Canada fall within the SEC’s small or micro capitalization categories (Carpentier and Suret 2009). Notwithstanding their much smaller average and median size, the survival rate of listed SMEs five and ten years following their IPO is superior in Canada to that observed in the United States, a result assisted in part by unique features of Canada’s securities regulatory regime – notably, the ability of nonprofitable listed companies to make follow-on seasonedequity offerings in the private or public markets (Suret and Carpentier 2010).

Ultimately, the net effect of the functional performance of a securities regulatory regime will materialize in one critical economic factor: the cost of equity. As is to be expected, the cost of capital is higher in markets with less effective regulations since shareholders investing in such markets demand a higher risk premium – hence the assertion of proponents of a national securities regulator that the allegedly lower quality of securities regulation penalizes Canadian firms in their financing costs relative to US firms. In fact, however, comparative studies indicate that the cost of equity in Canada is one of the lowest in the world and that Canadian firms are not burdened by a “made-in-Canada” risk premium that increases their cost of equity relative to that in other developed economies and discounts the trading price of their shares. For instance, estimates of the cost of equity in the main common law countries for the 1992-2001 period are as follows: the United States, 10.24 percent; Canada, 10.52 percent; the United Kingdom, 10.64 percent; Australia, 10.72 percent; and New Zealand, 11.14 percent (Hail and Leuz 2006).9 A study published by the Bank of Canada concludes that, when longerterm sovereign bond yields are taken into account, “our tests are unable to conclude definitely that there is a difference between the Canadian and U.S. cost of equity” (Zorn 2007, 33). Other studies find that there is no material difference between the cost of equity in the United States and in Canada except in the finance and resources sectors, where Canada enjoys a net advantage of approximately 100 basis points (Claus and Thomas 2001; He and Kryzanowski 2007). The results of these comparative studies of the cost of equity are consistent with the higher propensity of Canadian firms to access public equity markets.

Critics of the Canadian securities regulatory regime assert that the requirements of multiple regulators have led some issuers of securities to limit their public offerings in some provinces. Indeed, several Canadian and foreign issuers have avoided the Quebec market because of the actual or perceived burden of having to publish their prospectuses and other disclosure material in French – an examination of the number of public financings by prospectus in Canada reveals that in 2009-10 only about 48 percent of issuers filed their prospectus with the AMF during that period. The June 2011 announcement by IAMGOLD Corporation is a case in point.10 Notwithstanding serious concerns about this unhealthy state of affairs, the fact remains that requirements concerning the language of disclosure documents, which relate, in part, to concerns about investor protection, would not change under a single federal regulatory regime, as federal government authorities have stated unambiguously. The solution to that problem accordingly lies elsewhere.

The strongly held view prevailing in several provinces that the takeover of the securities regulation domain by the federal government would have, over time, a deleterious effect on regional economies is not a hollow concern. Periodic consultations with the Council of Ministers likely would not be enough to ensure that regional concerns are addressed; the proposed Securities Act specifies only that a meeting “must be held at least once per year.” The proposal to establish regional offices might be comforting for the employees concerned but, from a decision-making point of view, it is not reasonable to expect regional offices to carry the same clout as headquarters. The main impetus for the federal initiative is to assume control of securities regulation and to establish uniformity across the country; this cannot be achieved through regional offices that have management and policy-making autonomy. An abundant literature on the behaviour of organizations, supported by experience, teaches that it is an imprudent wager to overlook the logic of institutions and industry structures. This is an area where the federal proposal really falls short since, by its very nature, a national regulator cannot entertain a regime of exceptions to accommodate local and regional differences and promote the economic development initiatives that are inherent to Canada’s multijurisdictional architecture. Rather, such a regime is likely to prejudice and stymie growth and job creation in many regions and sectors without any commensurate benefits at the national level.

In 2009, the Canadian economy ranked 13th in the world, as measured by its GDP. In that same year, Toronto was 12th in the City of London Global Financial Centres report (City of London 2010). No doubt this rating reflects the fact that Toronto is home to 5 of Canada’s largest domestic banks, 55 foreign bank subsidiaries and branches and 6 of Canada’s top insurers. All these great financial institutions are under federal regulatory authority. The TSX, under provincial regulation, is the eighth-largest stock exchange in the world by market capitalization. Thirteenth, 12th and 8th – these three rankings show clearly that Canada has not paid a price for its decentralized network of securities regulators, despite the important national and global dimensions of capital markets.

Stock, commodity and derivative exchanges and their clearing organizations are key market infrastructure institutions around which high-value service industries coalesce. Their vitality and dynamism have a direct effect on the real sector of the economy. The recent debate engendered in Toronto in the wake of the proposed merger of the LSE Group and the TMX Group provided a vivid illustration of its importance, real or perceived. It is indisputable that measures that undermine the competitiveness of an exchange or clearing organization have broad regional economic implications; this phenomenon can be observed in Quebec since the withdrawal of stock trading activities at the Montreal Exchange in 2000. The converse is also true, and Toronto is a case in point.

It is no coincidence that the first provinces to oppose the federal government’s initiative were Alberta (home to the TSX [V] and the Natural Gas Exchange), Manitoba (home to ICE Futures Canada) and Quebec (home to the Montreal Exchange). The survival of these exchanges occured not simply because of their specialization but because each of these provinces had the regulatory authority to ensure that each exchange had a governance regime that promoted its development and shielded it from myopic corporate behaviour. Battle-scarred by the negotiations to protect the economic interests of their provinces, notably Alberta and Quebec, they have no reason to believe that, in similar circumstances, a national regulator would have gone to the mat to secure equivalent results.

To avoid duplication and streamline the regulatory supervision of exchanges and clearing houses, the Canadian Securities Administrators have developed a coordinated approach that takes the form of a “lead regulator.” Thus, the regulator for the TSX is the Ontario Securities Commission (OSC); for the Montreal Exchange and the Canadian Derivatives Clearing Corporation (CDCC), it is the AMF; for ICE Futures Canada, it is the Manitoba Securities Commission (MSC); and for the Natural Gas Exchange, it is the Alberta Securities Commission (ASC). The ASC and the British Columbia Securities Commission (BCSC) assume these responsibilities for the TSX (V).

This arrangement has powerful implications for regional economic growth since each “lead regulator” has a vested interest in the long-term success of the exchange and clearing organizations under its umbrella. This provides the impetus for developing the special expertise particular to the markets under the lead regulator’s supervision, gaining intimate familiarity with all the processes and rules, becoming knowledgeable about the participants in its segment of the industry, both in Canada and abroad, and nurturing the competency to recognize and anticipate competitive threats. And make no mistake, those threats differ greatly between markets. For instance, the intricacies of regulating alternative trading systems to ensure the fair and orderly execution of all trades and high-frequency algorithmic trading are, in their technical aspects, issues that are mainly confined to the TSX, albeit with implications for specific Montreal Exchange derivatives and TSX (V) markets. For the ASC and the BCSC, issues pertaining to the regulation of venture issuers have more salience, whereas the MSC focuses mainly on the exigencies of agricultural commodities markets.

In the face of this demonstrated diversity of expertise and strong incentives to foster the development of local market infrastructures and capital markets, proponents of a centralized system have not shown how a national regulator would deliver the same focused attention, expertise and responsiveness to competitive threats with the direct accountability for results as is the case with the current regime. The inherent inability of a centralized regulator to promote diversified financial infrastructures is well understood in the United States, where the SEC is considered the “protector” of New York and the Commodity Futures Trading Commission (CFTC) the “protector” of Chicago. Despite many reports recommending the merger of the SEC and the CFTC, Dodd-Frank not only did not follow this course of action but, on the contrary, it enlarged the CFTC’s mandate.

As another case in point, the European experience should serve as a lesson for Canadian decision-makers. The European Commission observed that second-tier markets for SMEs did not succeed as expected, in large part because the senior management of the senior exchanges that owned the junior exchanges and their regulators focused their efforts on the main market, which accounts for most of their revenues and prestige, and did not commit the attention needed to promote their development (Bannock 1994). To date, the TSX has not smothered the TSX (V). This is in large part because the activities and market behaviour of the latter remain under the watchful eye of the Alberta and British Columbia securities commissions. In this regard, it is noteworthy that, while the economies of these two western provinces account for 29 percent of Canada’s GDP, in the first five months of 2011 they generated 78 percent of Canadian corporate listings on the TSX (V) and 64 percent of Canadian corporate listings on the TSX and the TSX (V) combined.

The structure of the Canadian securities regulatory system also promotes the global reach of Canadian exchanges. This is the case not only for the TSX but for all other Canadian exchanges. For instance, ICE Futures Canada, the country’s only agricultural commodities exchange, benefits from a broad international participation. It has received regulatory approvals to offer its services in jurisdictions throughout the world, including in the allimportant US, UK and French markets. Each of these regulatory approvals has been based on the foreign regulator’s being satisfied that the MSC is providing competent oversight and regulation of ICE Futures and its designated clearing house ICE Clear. The same can be said of the Montreal Exchange, where, depending on market conditions for Canadian debt and currency, between 40 and 60 percent of the volume of its financial futures markets is generated from abroad; it also must be noted that the Montreal Exchange is the only Canadian exchange to operate a US exchange – the Boston Options Exchange.

Another major economic cost associated with the centralization of the securities regulatory apparatus is most likely to be the gradual elimination of the conditions conducive to the functioning of a Canadian public venture market with its concomitant effect on the ability of fastgrowing Canadian SMEs and junior national resources companies to obtain financing. The promise that a national regulatory agency would adopt proportionate regulation is not easily reconciled with the strong drive underlying the federal government’s initiative to ensure uniformity of regulations and enforcement across the country. This issue cannot be casually dismissed because it goes to the heart of the policy conundrum of establishing the balance between the conditions of access to public (and exempt) markets by small issuers and the goal of protecting public investors.11

Following the seminal work of David Birch (1981) we have gained a much better understanding of the dynamics of economic growth. We know that high-growth companies create a disproportionate number of net new jobs even though they account for only a small percentage – around 5 to 7 percent – of firms. In Canada, the high-growth firms that had a continued existence between 1985 and 1999 accounted for 56 percent of the net jobs created during that period but were only 6 percent of the total number of firms. In the United States during the 2002-06 period, high-growth companies represented 6.5 percent of total firms but accounted for 84 percent of net job creation. Only 2.5 percent of these firms were less than four years old (Acs, Parsons and Tracy 2008), which belies the conventional idea that start-ups and technology firms are the engine of economic growth. These results are congruent with the fact that, during that period in the United States, the median age of firms at the time they went public was about four years and the fact that they mirror the distribution of firms across all industrial classifications. Similar results are observed in Canada, except that junior natural resources firms are overrepresented, a consequence of the fact that other sources of external capital are virtually nonexistent for such firms.

High-growth firms generally do not generate sufficient capital internally to fund current operations, let alone fuel rapid growth. There is substantial evidence that financing obstacles are more growth constraining for SMEs and prevent firms from reaching their optimal size. The traditional sources of external equity required by high-growth firms are venture capital, private equity and public markets. In Canada, however, venture capital and private equity firms do not constitute a buoyant industry; thus, the mix of funding sources for SMEs in Canada is singularly different than in other developed economies. During the 1989-2006 period, 802 companies graduated to the TSX from the TSX (V) whereas venture-capital-backed IPOs accounted for only 122 new TSX listings. During the 1991-2008 period, Canadian venture capital firms exited through an IPO in about 5 percent of the cases compared with more than 39 percent in the United States.

One reason given to explain the difference is that the valuation of companies that issue IPOs is higher in the United States than in Canada. The president of the Business Development Bank of Canada (BDC), one of Canada’s largest venture capital institutions, suggested at a recent event of the Institute of Corporate Directors that the proportion of failures in a Canadian portfolio of private equity and venture investments is the same as in the United States, and the difference lies in the fact that we do not have many “home runs.” Indeed, the valuation of venture-capital-backed IPOs appears to be 48 to 66 percent lower in Canada than in the United States (Carpentier, Cumming and Suret 2010a).12 Another explanation put forward is that the lower pricing of IPOs in Canada reflects the price exacted by the market for Canada’s more lenient regulatory requirements. Recent empirical studies have demonstrated that the spread between IPO pricing in Canada and in the United States is due to differences in liquidity prevailing in the markets in the two countries, but when comparisons are made between IPOs where the expectations of liquidity are similar, the difference in IPO valuations is not significant. The argument that the current regulations penalize Canadian companies that issue an IPO thus does not stand up to scrutiny (Carpentier, Cumming and Suret 2011).

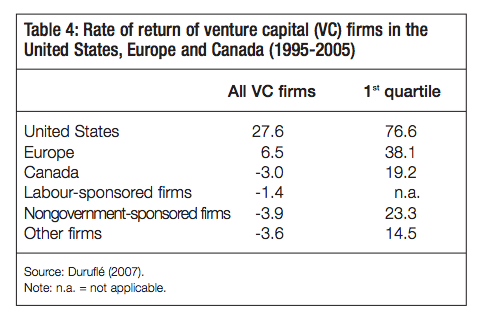

Since the 1980s, the Labour-Sponsored Venture Capital Corporation (LSVCC) program and the BDC’s venture activities have been the federal government’s main tools to support venture capital activity. The tax-subsidized LSVCC program has been costly, accounting for more than half of all venture capital under management but delivering dismal rates of return. There are strong indications that the program has crowded out private venture capital (Cumming 2007). Consequently, and contrary to the situation in the United States (see table 4), the venture capital industry in Canada has not delivered returns sufficiently attractive to entice institutional investors to allocate significant capital to this segment. No doubt reflecting this performance, the total amount of capital raised by venture capital firms has been in steady decline since 2006. Moreover, banks, venture capital and private equity firms generally shun natural resources exploration and junior mining, oil and gas companies.

Canada is unique in having developed a vibrant public venture market. International comparisons indicate that, relative to other jurisdictions, the Canadian securities regulation regime facilitates access to public capital markets by Canadian issuers. A very large proportion of the TSX and TSX (V) issuers are SMEs; 82 percent of the listed companies have a market capitalization of less than $250 million. Overall, about 3,600, or 94 percent, of the companies listed in Canada fall within the SEC’s small or micro capitalization categories (Carpentier and Suret 2009).13 The TSX (V) has become the most effective avenue for the financing of small firms, particularly high-growth firms, in all sectors of activity. Interestingly, the evidence shows that listing on the TSX (V) greatly facilitates subsequent financing in the private (exempt) market, including junior firms in the natural resources sector. Eighty-two percent of new equity raised by TSX (V)-listed companies was generated through private placements.

The proclivity of a national regulator to tilt the current balance between ease of access and investor protection through the adoption of more stringent regulations would be encouraged by four powerful forces. First, at the policy level, it would need to counter a widely held view in the academic and regulatory communities that non-onerous listing requirements and regulation with respect to the conditions of access to public markets are detrimental to investors. Many studies conclude that lenient listing requirements inexorably lead to the emergence of a “lemon market,” in which only companies of poor quality list, increasing the incidence of market manipulation and hurting investors by yielding poor returns on a systematic basis (see, for example, Black 2001; Klausner and Litvak 2001).14 These results raise insistent questions about the appropriateness of current listing regulations. In a public debate, the TSX (V) is at a disadvantage since all failures of listed issuers are public whereas those of the venture and private equity industry remain confidential. From an economic growth perspective, the appropriate approach is not to deny the empirical data but to ensure that the TSX (V) results are compared fairly with those stemming from other modes of SME financing, including firms unable to raise sufficient equity capital.

Second, comparisons with other developed countries provide a facile excuse for a national regulator to tighten the regulatory requirements governing access to public and exempt markets. Listing requirements on the TSX (V) and the rules that govern IPOs, seasoned equity offerings and private placements are currently significantly more permissive in Canada than is the case abroad. During the 1986-2006 period, 3,857 companies listed on the TSX (V); average gross proceeds at listing were $2.05 million (median = $0.65 million), 49.3 percent had no revenues and 80.1 percent had negative earnings. True to form, a recent confidential report on the Canadian venture industry by an international consulting firm commissioned by a federal agency states, without nuance, that “relatively low listing requirements in the TSX (V) are counterproductive.”

In the United States, the SEC Penny Stock Rule requires newly listed firms to have a positive net income, a market value of US$50 million and a minimum bid price of US$4 per share. Thus, the average market capitalization of TSX (V) companies is about 10 percent of the minimum size set by the SEC.15 In Europe, listing requirements on junior markets generally call for minimum IPO gross proceeds of about $8 million. On the London Alternative Investment Market, average IPO gross proceeds amount to $15 million. On the First North market (Scandinavia), the mean market capitalization is $15 million, and on the New Zealand Alternative Exchange it is $12.5 million. In Canada securities regulations preclude investors who acquire securities distributed under prospectus exemptions from selling these securities for a period of four months, while in the United States the mandated holding period is two years for nonregistered securities. Clearly, the duration of the mandatory holding period will influence the size of the discount investors will require at issuance to compensate for the additional risks created by the resale restriction.

Third, the Canadian government attitude vis-à-vis public venture capital can be characterized as one of benign neglect. For instance, the federal Scientific Research and Experimental Development (SR&ED) program provides Canadian-controlled private corporations a refundable investment tax credit at an enhanced rate of 35 percent on the first $3 million of annual qualified research and development expenditures, refundable at 100 percent; the credit rate is 20 percent for such expenditures exceeding $3 million and it is refundable at 40 percent. Public technology companies that otherwise would meet the eligibility criteria for SR&ED cash refunds are thus disqualified; the applicable credit rate is reduced to 20 percent and is nonrefundable. This policy discriminates against some 745 technology companies, many of them high-growth companies, that have been listed on the TSX (V) since 1986.

Fourth, the structure of the financial industry has potent effects on entrepreneurial equity financing. Following the enactment of the Gramm-Leach-Bliley Act in 1999, which ended the separation between commercial and investment banking in the United States, commercial banks acquired most of the investment banks specialized in the financing of small companies. Concurrently with that structural change in the investment industry, the number of IPOs and listings on the AMEX and NASDAQ exchanges began its steep decline. In Canada, although the number of listings on the TSX continued to increase, the average annual rate of new listings slowed considerably from 47 per annum in the 1991-97 period to 13.6 per annum between 1997 and 2008; about 31 percent of 1997-2008 new listings are graduates from the TSX (V). In Quebec, a recent study aimed at identifying the main reasons behind the dearth of going public transactions and the fact that, in 2010, only 5 percent of new Canadian corporate listings on the TSX and TSX (V) were Quebec-based companies concludes that the structure of the financial ecosystem, particularly the dominance of bank-owned securities firms, is one of the main culprits (FMC-Avocats/PWC 2011).

The conclusion is unmistakable: large national investment bankers and institutional investors are averse to small IPOs and investment in small public companies, in part, because SMEs are not capitalized enough to allow them to justify investments of meaningful size. Their segmentation of the market responds to economic considerations that are rational from their corporate point of view. It does not follow, however, that their corporate interests are necessarily aligned with Canada’s and the provinces’ economic growth needs and objectives. Hence, the concern is well grounded that the influence that large Canadian banks and institutional investors would exert on a national regulator would erode, consciously or inadvertently, the conditions of success of a public venture market. Moreover, it does not follow that, under these circumstances, investors would be better off. In the United States, the odds of failure of a firm taken public by a top-tier investment bank are about twice those of a firm underwritten by a smaller specialized investment banker (Peristriani 2003).

Proponents of public venture financing give significantly more weight to economic growth, which shows strong regional variation in Canada. For instance, 48.1 percent of the new listed issuers on Canadian exchanges between 1986 and 2006 belonged to the natural resources sector, a segment of the economy where bank or debt financing for and institutional investments in junior companies are virtually nonexistent. Proponents can point to the fact that the value-weighted average rate of return of new listings on the TSX (V) amounted to 15.7 percent over the 1995-2005 period, outperforming the TSX’s 10.7 percent.16 For the 2001-06 period, the annual return of the TSX (V) S&P Index was 23.5 percent, compared with 13.1 percent for the TSX S&P Index. The graduation rate of TSX (V) issuers to the TSX for the 1986-2006 period was 7.67 percent, a proportion that corresponds to that of high-growth firms. Indeed, their value-weighted cumulative abnormal returns over the three years before graduation were 75.56 percent, and rates of return thereafter were in line with the market (except for issuers with no revenues) (Carpentier and Suret 2010). It must also be noted that 31.5 percent of the new TSX listings of Canadian companies during the 2007-10 period graduated from the TSX (V), that 20 percent of companies in the TSX/S&P Index started as TSX (V)-listed companies and that the TSX (V) is for all practical purposes the only avenue for the junior natural resources sector. In September 2010, mining and oil and gas companies listed on the TSX (V) represented 4 percent of the average market capitalization value of TSX-listed companies in the same sector. Yet between January 2008 and September 2010, these TSX (V) firms accounted for 29 percent of the total equity capital raised by natural resources companies.

It is true that the average stock market performance of TSX (V) issuers conceals a high skewness: many investors incur losses and approximately one-third of issuers fail, wiping out the total equity investment. It has been shown that the average long-term returns of investments in the stock of companies that have listed on the TSX (V) through the reverse merger option are negative and are worse than for IPO-listed firms and that the multiple obtained through a reverse merger is half that achieved by IPO issuers (Carpentier, Cumming and Suret 2010b). Securities regulatory policy involves a trade-off between the stringency of regulation and investor protection. For instance, many issuers accept the lower multiple associated with a reverse merger as a trade-off for the rapidity and certainty of the financing. Considering the volatility of markets, this is not an irrational choice. In the Canadian system, it is one provincial government’s prerogative to choose a balance that differs from that in another province in order to achieve broader objectives. In light of the manifest success of the Canadian public venture market in allowing a large number of SMEs to reach their high-growth potential, it is a legitimate and rational choice for a province to favour high skewness exposure over lower mean-variance portfolio yields.

The current Canadian securities regulatory regime allows the venture market to be segmented from the major market – and the TSX (V) unambiguously is. Consequently, the spillover effects in terms of reputation and other qualitative considerations are minimal. Tasked with a national mandate, this segmentation of markets would be inherently difficult to sustain or justify for a national regulator since, under its narrow mandate, investor protection considerations would always trump regional economic growth considerations. This is precisely why a national securities commission, in the long term, would not likely support the development of both a seasoned and a venture stock market.

Ostensibly, one of the main arguments consistently put forward in support of the federal initiative is the growing international interdependencies of capital markets and the regulatory implications that ensue, particularly with respect to systemic risk.

The globalization and interdependencies of capital markets are indisputable developments with serious consequences for all economies. With respect to securities regulation, which is primarily concerned with business conduct and investor protection, as opposed to prudential and systemic risk issues, it is not realistic to expect countries to shed their legal traditions, which evolved naturally from the norms, traditions and institutions that have shaped their individual societies, in favour of internationally uniform rules and regulations. The differences observed between civil and common law jurisdictions are a case in point. These legal and institutional frameworks and regulatory, supervisory and enforcement mechanisms and practices, therefore, are unlikely to converge – IOSCO, after all, issues guidelines, not binding rules. This implies that the focus of the global approach toward securities regulation must be centred on the ends to be achieved – the performance of the regulatory regime – rather than on the approaches and means used to attain them. Mutual recognition of regulatory regimes – recognition that a given regulatory regime delivers the results that are sought under the IOSCO Objectives and Principles – thus becomes the most efficient approach to enhance and promote high-quality securities regulation internationally.

The stance various jurisdictions have adopted following the demutualization of exchanges illustrates the point. Traditionally, stock, commodity and derivative exchanges exercised extensive regulatory powers over members and participants. The demutualization of exchanges, which changed their not-for-profit status to that of for-profit corporate organizations, raised serious questions about the conflicts, real or potential, arising between their regulatory role and their new profit mandate. Governments worldwide have sought to ensure greater independence of market and industry regulation from market operation despite the significant advantages and benefits of self-regulation. A review of the approaches taken by governments reveals fundamental differences in approach that can be categorized into three groups:

The absence of consensus regarding which of these three regulatory approaches better fulfills the objectives of securities regulation is to be expected. The solution, of course, is to anchor mutual recognition on the basis of shared principles and objectives and the comparability of market outcomes, not on the equivalency of regulatory inputs and uniformity in laws, regulation and approaches to implementation and enforcement.

The IOSCO’s assessment methodology is unambiguous with respect to the relevance of the structure of the regulator for functional performance: “There is often no single correct approach to a regulatory issue. Legislation and regulatory structures vary between jurisdictions and reflect local market conditions and historical development. The particular manner in which a jurisdiction implements the objectives and principles described in this document must have regard to the entire domestic context, including the relevant legal and commercial framework” (IOSCO 2003a, 3). The results of the evaluation of the functional performance of regulators in implementing IOSCO’s Objectives and Principles reveal no clear correlation between the architecture of the regulatory apparatus and the delivery of quality securities regulation. Adoption of a federal Securities Act would not alter this reality.17

The 2008-09 financial crisis gave renewed salience to the regulation of systemic risk. This is an area where the federal government has clear responsibilities and, it needs to be emphasized, already possesses the tools to do its job. These have stood the test of time, particularly in periods of substantial turmoil and stress in financial markets.

The Office of the Superintendent of Financial Institutions (OSFI) has the prudential regulatory responsibility to oversee and regulate the securities-related activities of Canadian banks “in a system where all banks, and all of their subsidiaries (including investment banking), are under the scrutiny of a single regulator” (Price 2010, 1).18 This, of course, is perfectly in line with the powers and duties assigned to the superintendent under the OSFI Act. The federal government’s contention that the proposed Securities Act is “squarely aimed at dealing with systemic risk,” in view of provisions permitting compelling the production of documents from “market participants” (section 109) and the sharing of information in Canada and abroad (section 224[1]), does not break new ground. These powers are already available to OSFI, and, to the extent it was deemed important to extend its ambit to certain unregulated organizations such as hedge funds and “dark pools,” the simple extension of the definition of financial institutions in the OSFI Act to include such “market participants” would accomplish that objective.

The operating arm of the Canadian Depository for Securities Limited (CDS) – namely, CDS Clearing and Depository Services Inc. (CDS Clearing) – is a systemically important part of the Canadian financial infrastructure. Hence, in 2003, the CDS clearing and settlement system was brought under the regulatory authority of the Bank of Canada in accordance with the Payment Clearing and Settlement Act, even though the activities and conduct of CDS and CDS Clearing remain regulated by securities commissions. At the same time, the Canadian Derivatives Clearing Corporation (CDCC) systems have not been brought under the oversight of the Bank of Canada in accordance with the Payment Clearing and Settlement Act, suggesting that the CDCC was not considered large enough to present systemic risk for Canada. It is well noted that the exchange-traded derivatives markets were not significantly disrupted during the 2008-09 financial crisis, in large part because of the markets’ transparency and the central counterparty mechanism that characterizes their clearing houses.19 In December 2009, the CDCC was selected by the Investment Industry Association of Canada to become the central counterparty for the Canadian repo market, a critical infrastructure for Canadian-dollar core funding markets. The Bank of Canada has indicated its intent to designate it under the Payment Clearing and Settlement Act when the service comes into force.

Looking forward, it is urgent to correct deficiencies in the market infrastructure institutions for over-the-counter derivatives markets that were exposed by the financial crisis and to ensure their resilience to future shocks. The main axes of reform include product, legal and process standardization, increased transparency, including the establishment of trade repositories, and the design, establishment and monitoring of central counterparty clearing organizations.

At the end of 2009, the six largest Canadian banks held almost 97 percent of the approximately $12.4 trillion of over-the-counter derivatives held by all Canadian financial institutions. In terms of prudential regulation, these institutions are already regulated by a federal agency, OSFI. Eighty percent of these derivatives contracts are booked in a foreign jurisdiction on at least one side of the transaction. Given the global nature of the over-the-counter derivatives market, the viability of a stand-alone Canadian central counterparty clearing organization presents challenges. Moreover, since the most important asset classes are derivatives linked to interest rates and currencies, it follows that central banks effectively will become the guardians with respect to the means employed to contain systemic risk and the backstops of last resort in the event the financial integrity of such a central counterparty clearing organization is threatened.

An interagency working group has been established to develop policy options for Canada, to coordinate policy developments with industry and, in due course, to spearhead the adoption of legislation and regulations and the implementation of policies. The group is composed of representatives of the federal Department of Finance, OSFI, the OSC, the AMF and the ASC, and is chaired by the Bank of Canada, as it should be. This composition also ensures that Canada’s objectives and concerns will be well represented at IOSCO since both the AMF and the OSC have standing and, even though Canada represents less than 2 percent of global overthe-counter derivative markets, they exert significant leadership in IOSCO’s key decision-making bodies. And all this is being accomplished without creating any constitutional heartburn. Canadian federalism will not prevent Canada from meeting its G20 commitments concerning these matters.

A substantial body of empirical evidence supports the proposition that the performance of the current Canadian securities regulatory regime compares favourably in terms of regulatory inputs, intermediate indicators and, most important, market outcomes against the results achieved by other developed countries. The high degree of legislative and regulatory harmonization that prevails across Canada, the establishment of truly national reporting systems and the acceptance of mutual recognition as an organizational principle are remarkable achievements. Notwithstanding critiques of certain details in the functioning of the system, the fact remains that the federal government’s absence from the field of securities regulation has not led to a “race to the bottom” with regard to quality and effectiveness. On the contrary, Canada has by any measurable criterion a regime recognized as one of the best worldwide. There exists no evidence whatsoever to support the notion that a national securities regulator would better serve Canada’s needs and interests.

While the IOSCO Objectives and Principles are explicit with respect to the functional attributes of a securities regulatory regime and an extensive body of empirical studies exists pertaining to the many dimensions of functional performance, no such formal guidance is professed with regard to structural matters. Indeed, IOSCO states that “there need not be a single regulator. In many jurisdictions, the desirable attributes of the regulator set out in the Principles are in fact the shared responsibility of two or more government or quasi-government agencies with governmental powers” (IOSCO 2003b, 9). It is therefore up to us.

From an economic and business point of view, available data clearly show that the current securities regulatory architecture serves Canada very well. It is respected internationally, costs are low, compliance is high and it is highly responsive to regional economic conditions and needs. Given the magnitude of the changes in the proposed Securities Act, the burden is on its proponents to make the case for how moving to a single federal regulator would benefit Canadians. In my opinion, they simply have not done so.

A mature understanding of the principle of subsidiarity – one of the main features of federalism – would have the federal government focus on matters of major and significant importance for the Canadian economy that cannot be performed effectively by the provinces. This is clearly not the case for securities regulation.

Some commentators suggest that the Canadian asset-backed commercial paper (ABCP) crisis provides a rationale for a federal securities regulator. With hindsight, it is easy to lecture on what securities regulators might have done differently to help prevent the debacle, but this would fail to recognize that, in line with applicable securities regulation in other major jurisdictions, issuers of commercial paper are exempted from the obligation to issue a prospectus when their issues are rated investment grade by a credit-rating agency.20 It needs to be noted that retail investors were made whole early in the unfolding crisis. John Chant concludes that “this case offers no evidence one way or the other with respect to the organization of regulation” (2009, 40). Stephen Choi of the New York University Law School draws a similar conclusion: “Importantly, the ABCP crisis does not provide support for the argument that Canada should move toward a national securities regulator. The regulatory structure for exempt offerings underlying the ABCP market prior to the financial crisis was similar to the regulatory structure within the United States securities regime. Similar with the provinces, the SEC provides for private placement exemptions from public offering registration requirements for securities sold through exempt transactions to primarily sophisticated investors” (2010, 94). The final word on this matter belongs to Purdy Crawford, the architect of the ABCP restructuring, who stated that, even if a federal agency had been in place, the same exemptions would have governed the issuance of commercial paper.21

Valid comparisons about the performance of the Canadian securities regulatory regime cannot be those made against an idealized, error-free system; the appropriate standards are the actual performance, over time, of regimes in jurisdictions with well-developed capital markets. Lofty vision statements do not a high-performance organization make. Nor should claims of the impotence of the current securities regulatory regime to address specific matters of national import be accepted at face value. The history of developments in Canadian securities markets has taught us otherwise.

The central thesis that appears to motivate the federal government is that high formal and public enforcement intensity is essential to ensure the quality of capital markets.22 The evidence does not give any credence to this approach. It fails to recognize the effectiveness of ex ante disclosure measures over ex post enforcement actions and the importance of instilling a culture of compliance through the effective use of the whole arsenal of regulatory tools. The experience of many countries provides insightful lessons of what works in securities regulation. It is definitely not what is argued by the federal government. Moreover, the denigration of Canada’s capital markets is unwarranted and surprising given their superior performance relative to those of other countries: the OECD’s assessment of the quality of securities market regulation assigned Canada the 2nd rank in terms of investor protection; the United States ranked 3rd, the United Kingdom ranked 4th and Australia ranked 12th.

Whatever the Supreme Court of Canada decision in the matter of the proposed Securities Act, the financial industry should fear, and would do well to prepare for, the unintended consequences of the federal initiative. In any case, if the Supreme Court were to rule against the federal government, one hopes that Ontario would join the passport system. The reason it gives to justify its position – that the passport system does not eliminate multiple fees – is not material enough to justify the fragmentation and added costs for issuers caused by the province’s abstention.

The biggest risk, however, is that the impetus that has driven the Canadian Securities Administrators to pursue further harmonization and coordination will wither away. Although it remains a non-dit, there is little doubt that the fear the federal government could step in constitutes an incentive to address with a national perspective the needs of the Canadian capital markets. What will happen once this perceived threat is eliminated? I submit that the actions of the financial industry to encourage Ontario to join the passport system and the decision of the Ontario government in this regard would have considerable influence on the future course of events.