The federal government announced the Canada Groceries and Essentials Benefit (CGEB) on January 26, 2026. The benefit is an expansion of the existing GST/HST Credit aimed at easing affordability pressures for low- and modest-income Canadians, amid persistently high costs for food and essentials.

The measure has two parts. First, it provides a one-time top-up, equivalent to 50 per cent of a household’s 2025/26 GST/HST Credit entitlement, to be paid in spring 2026. Second, it increases the base benefit by 25 per cent for five years starting in July 2026, indexed to inflation. Government projections estimate that the CGEB would provide $3.1 billion in additional payments through the one-time top-up, and $8.6 billion over five years through the base-benefit increase. The Parliamentary Budget Officer (PBO) estimates that the measure will cost $12.4 billion over the fiscal years 2025/26 to 2030/31. This is a substantial fiscal commitment; design choices are therefore essential to ensure maximum impact per dollar.

Overall, it will reach more than 12 million recipients. This is an important step toward targeted affordability relief, delivered through an existing tax-based program. The CGEB was announced alongside complementary broader measures to tackle food insecurity and strengthen food supply chains in Canada, including support for food banks.

Instead of creating a new program, the CGEB builds on the existing GST/HST Credit, an established transfer delivered through the tax system. This approach supports rapid delivery and broad reach, but its distributional impact depends substantially on the GST/HST Credit’s design features. In earlier Institute for Research on Public Policy (IRPP) analysis for the Affordability Action Council (AAC), we recommended restructuring and expanding the GST/HST Credit into a permanent Groceries and Essentials Benefit to better target support to lower-income households.

In this commentary, we answer questions Canadians might be asking about the CGEB: what it is, who is eligible, how much recipients will receive, why the benefit is needed, and how benefit design choices will affect the impact and effectiveness of the program.

The GST/HST Credit is a tax-free quarterly transfer designed to offset sales taxes paid by low- and modest-income households. The Canada Revenue Agency automatically determines eligibility and credit amounts based on the previous year’s tax return, so households do not need to apply beyond filing a return.

For the 2025/26 benefit year (based on 2024 income, paid out from July 2025 to June 2026), maximum annual amounts are $533 for a single adult and $698 for a couple, in addition to $184 for each child under the age of 19. Benefits are income-tested and begin to phase out at an adjusted family net income (AFNI) of about $42,500. AFNI is the income measure the Canada Revenue Agency uses for income-tested benefits; it is based on family net income from the tax return, so deductions such as child care expenses can affect eligibility.

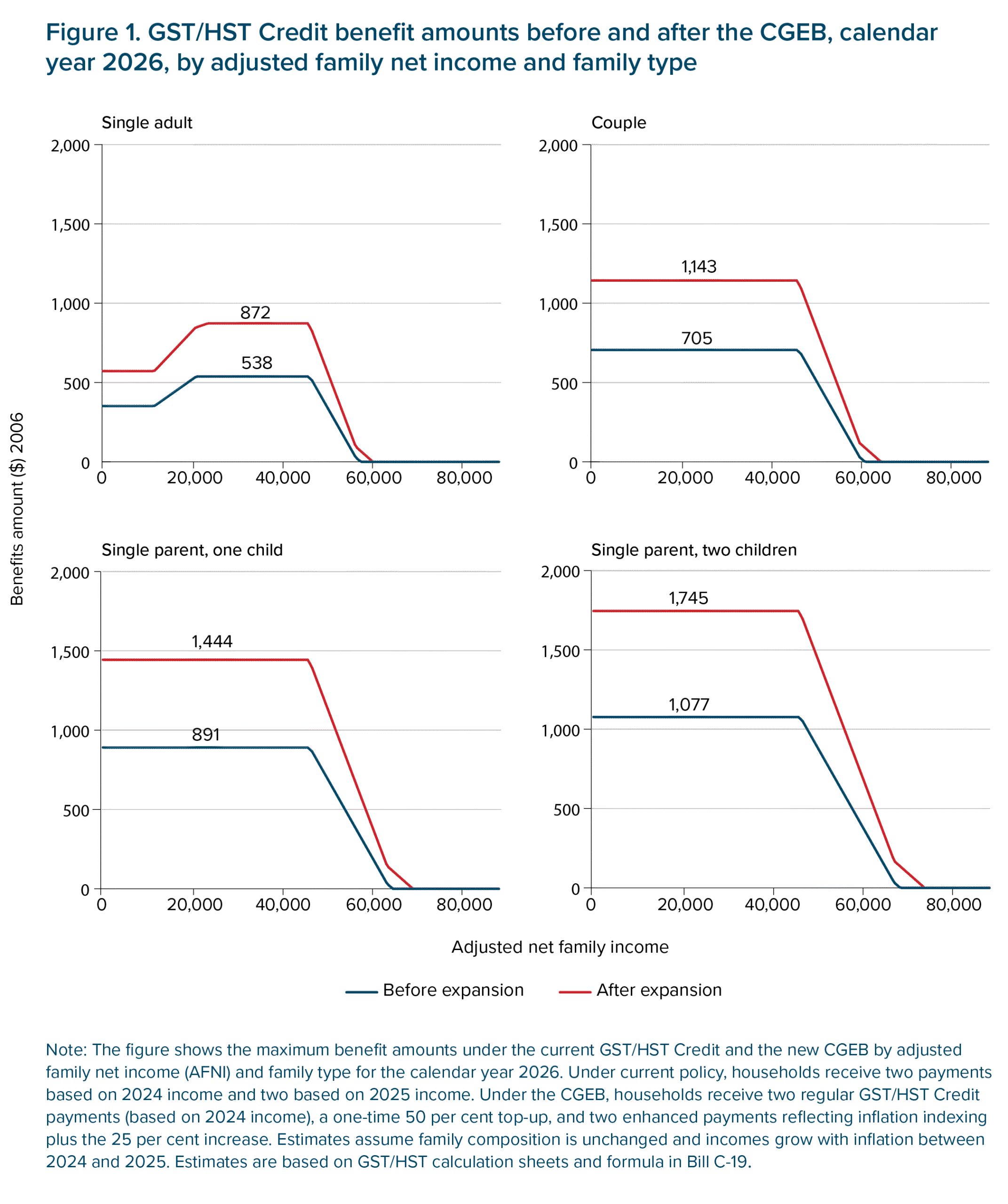

Figure 1 shows the current GST/HST Credit (pre-CGEB, blue line) for the calendar year 2026, by AFNI for four family types: a single adult, a single parent with one child, a couple, and a couple with two children. The GST/HST Credit benefit year runs from July to June. To better document the impact of the CGEB, we visualize the GST/HST Credit over the calendar year rather than the benefit year. For simplification, this assumes that people’s income only increases by inflation (two per cent) from 2024 to 2025.

A key design feature is that the benefit schedule for single adults differs from that of other family types. For single adults, the benefit phases in: for those with zero income up to about $11,500, the maximum benefit is $352 per year. The benefit then increases with the AFNI until it reaches its overall maximum at $538 per year, after which it flattens. It eventually phases out, reaching zero at an AFNI of roughly $46,500. For family types other than single adults, there is no phase-in component: the benefit is flat before phasing out. As a result, single adults with very low incomes receive less support than single adults with low-to-modest incomes. This design feature has important implications for distributional outcomes. For couples, couples with children, and single parents, there is no phase-in: households with zero or very low income receive the maximum benefit from the outset.

The Canada Groceries and Essentials Benefit builds on the GST/HST Credit framework rather than replacing it. The announced changes include:

Overall, a maximum-eligible single adult could receive close to $950 with the one-time top-up plus benefit for the 2026/27 year. In subsequent years, the maximum annual support for a single adult would stabilize at about $700.

Both the one-time top-up and the five-year 25 per cent increase change the benefit schedule across income levels and family types over the 2026 calendar year, compared to the pre-CGEB GST/HST Credit (see figure 1). For the CGEB, payments will remain quarterly, automatic and income-tested.

The rebranding of the credit explicitly links these measures to grocery and essential-goods affordability and signals a more focused policy emphasis on cost-of-living pressures.

Rising prices of groceries and other essentials have put sustained pressure on household budgets. Between 2019 and 2025, overall consumer prices have risen by approximately 21 per cent, but the price of food purchased from stores and shelter costs have risen much faster, by nearly 31 and 30 per cent respectively. Food price inflation also picked up again in 2025; by December 2025, prices for food purchased from stores were 5 per cent higher than a year earlier, the highest rate since late 2023.

The CGEB forms part of a broader set of recent affordability measures, including the middle-class tax cut and the cancellation of the federal consumer carbon tax. The CGEB provides additional support through an income-tested cash transfer targeted to lower-income households.

Evidence shows income growth has been uneven. In Q3 2025, the lowest-income households (bottom 20 per cent) were the only group that did not increase average disposable income (-0.5 per cent year over year). Wage gains were offset by declines in self-employment income and net investment income, including lower returns on interest-bearing deposits.

The disproportionate increases in the costs of non-discretionary items have especially squeezed lower-income households, whose budgets are already stretched thin. When prices rise, there is often little room to adjust fixed costs like rent and utilities, so households are more likely to cut back on groceries instead (see figure 2).

Figure 3 shows what this means in budget terms. By Q3 2025, very low-income households (the lowest 20 per cent of the income distribution) spent about 115 per cent of their disposable income (before government transfers) on shelter, food purchased from stores and transportation. Low-income households (the second-lowest 20 per cent of earners) spent about 67 per cent.

The consequences are evident in rising material deprivation: in 2024, over 10 million people in Canada, including 2.5 million children, lived in households struggling to afford sufficient food. In 2025, food banks recorded over two million visits in a single month, one-third from children. Notably, employment is the primary income source for nearly 20 per cent of food bank users, up from 12 per cent in 2019, underscoring the extent to which affordability pressures extend beyond those without work. Single-person households also account for about 42 per cent of food bank users, making them the most common household type accessing food banks.

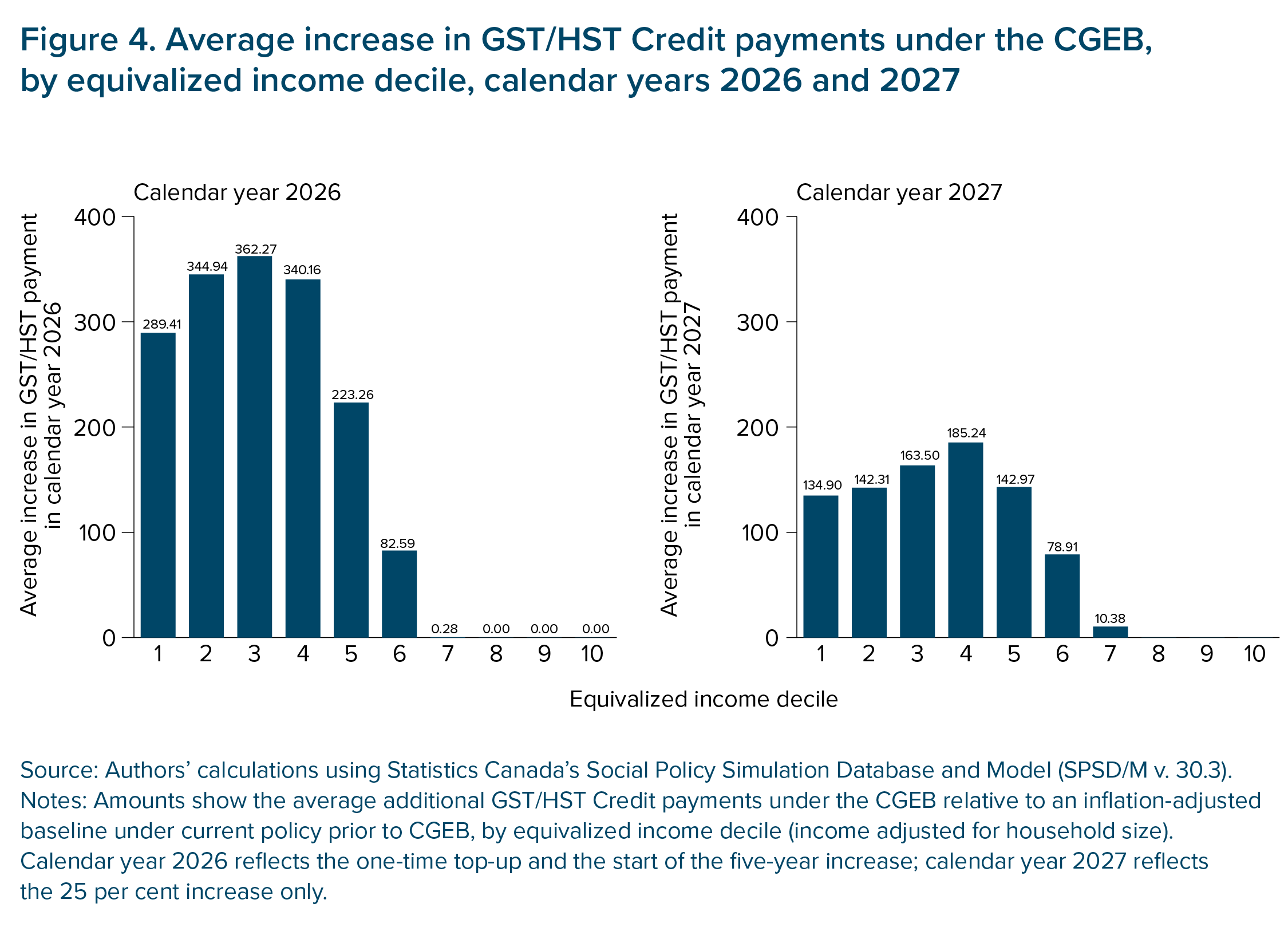

The CGEB is expected to reach about 12 million recipients, but the average benefit increase is modest relative to the scale of recent affordability pressures. Our simulations using Statistics Canada’s Social Policy Simulation Database and Model (SPSD/M v. 30.3) show that households that receive a GST/HST Credit payment under current rules (prior to the CGEB) would receive, on average, about $307 more in calendar year 2026, and $152 more in 2027, than they would have received under an inflation-adjusted baseline.

Gains vary across the income distribution and by family type. Measured by equivalized income decile (which groups households into 10 equal-sized income groups after adjusting for household size), average benefits peak in the third decile at an additional support of about $363 in 2026 (figure 4). In 2027, once the one-time top-up has expired, average gains peak slightly higher in the distribution, in the fourth decile at an additional support of about $185.

This pattern reflects the underlying benefit design, in particular the phase-in structure for single adults, which concentrates the largest gains among single adults in the second and third deciles, rather than those with the very lowest incomes (in the bottom 10 per cent of the income distribution) (figure 5). Figure 5 also shows that couples with children in the two lowest income deciles receive the largest additional benefits, on average.

These distributional effects translate into a measurable, but limited, reduction in poverty. Under the Market Basket Measure (MBM), our simulations estimate that the CGEB would reduce the poverty rate by 0.39 percentage points in 2026 (from 8.86 per cent to 8.47 per cent) — a 4.4 per cent relative reduction. The largest effects are concentrated in the fourth income decile where more households are near the poverty threshold.

These results highlight how the design of income-tested benefits in determining who benefits most, and not just their overall generosity, requires our attention and reflection. This point was emphasized in our prior IRPP analysis.

The CGEB reflects a central conclusion and suggestion of prior IRPP analysis and research conducted for the Affordability Action Council: targeted cash transfers delivered through the tax system can provide rapid, low-administrative-burden support to households facing elevated costs of groceries and other essentials.

Like the IRPP/AAC proposal, the announced measure builds on the GST/HST Credit platform, leveraging its key strengths: automatic delivery through the tax system, income-testing, and broad reach among low- and modest-income households.

The announcement also explicitly links the credit to groceries and day-to-day essentials, mirroring the renaming and reframing recommended in IRPP/AAC work. This aligns with the underlying diagnosis of that analysis: the baseline GST/HST Credit provides modest support relative to the recent rise in non-discretionary costs, particularly food and shelter, which have risen faster than the overall consumer price index in recent years. It is worth noting though that the government’s framing places more emphasis on grocery affordability and food-price pressures relative to headline inflation, while the IRPP/AAC recommendation benchmarked support against a broader essentials basket (food, shelter and transportation).

The announced benefit is best understood as an incremental time-limited expansion of the existing credit: a one-time top-up equal to 50 per cent of the annual 2025/26 GST/HST Credit value and a 25 per cent increase for five years starting July 2026, for a total of $11.7 billion in additional support over six years.

By contrast, the IRPP/AAC envisioned a more substantial and permanent redesign: a permanent Groceries and Essentials Benefit with a higher maximum base ($1,800 per adult and $600 per child annually), monthly delivery, and stronger concentration of benefits among very low-income working-age households.

A key design lever enabling this concentration was tighter targeting through an earlier phase-out. The IRPP/AAC proposal lowered the net-income threshold at which the benefit begins to phase out to $24,824 for single adults, compared with $42,335 under the current GST/HST Credit. Lowering the phase-out threshold concentrates additional support at the bottom of the income distribution while still providing modest increases to households above that level.

Prior IRPP/AAC analysis recommended monthly payments to improve income smoothing and help households manage recurring expenses. The announced CGEB retains quarterly payments, paid in July, October, January and April.

The IRPP/AAC proposal would have excluded seniors from the expanded benefit amounts, reflecting evidence that food insecurity and poverty rates are lower among seniors and that seniors already receive targeted supports via Old Age Security and the Guaranteed Income Supplement.

In contrast, the CGEB is framed as a uniform enhancement to the existing GST/HST Credit and includes seniors in the expanded benefit amounts. Illustrative examples show a single senior receiving the same enhanced support as a single working-age adult.

A further point of divergence is the shape of the benefit schedule for single adults. As discussed, the existing GST/HST Credit includes a phase-in for unattached singles, under which those with very low incomes receive smaller benefits than those with modest low incomes.

The IRPP/AAC proposal explicitly sought to address this design feature by raising the benefit level for single adults with income below roughly $11,000, eliminating the phase-in and bringing the maximum benefit amount in line with the maximum benefit amount for single adults with modest-low income. This benefit schedule would bring the treatment of single adults in line with that of other family types.

The CGEB increases benefit values but does not alter the underlying structure — meaning the existing phase-in/phase-out pattern for singles will remain, delivering a lower benefit amount to single adults in the lowest income deciles.

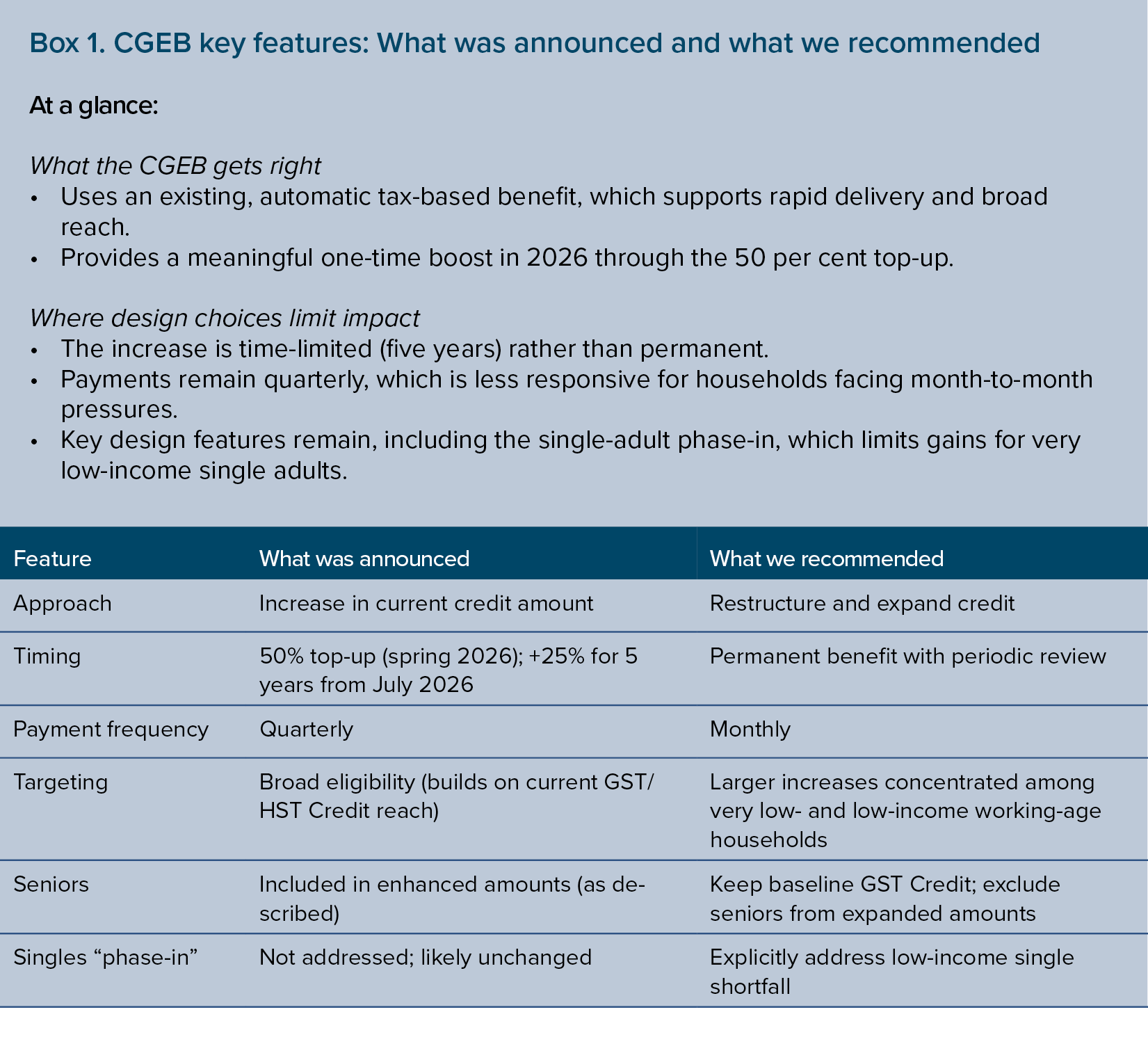

Box 1 highlights what the CGEB does well and where design choices limit impact. We also summarize key differences with our earlier IRPP/AAC analysis.

From an affordability perspective, the key distinction between the announced CGEB and the earlier IRPP/AAC proposal is not whether the benefit provides relief, but how much relief it provides and who receives it.

The CGEB primarily improves affordability for households near the low-income threshold, helping to cushion higher grocery and essentials costs, but leaves those households facing the most severe material constraints with smaller relative gains. By contrast, the IRPP/AAC proposal was designed to prioritize adequacy at the bottom of the income distribution, concentrating support among working-age adults and families for whom rising costs of food and other essentials pose the greatest risk to basic needs.

This distinction in approach to affordability translates into different impacts on poverty. While we estimate the CGEB will reduce the poverty rate by about 4.4 per cent, the IRPP/AAC proposal would have reduced the poverty rate by 6.7 per cent. The CGEB’s effects are concentrated among households close to the MBM threshold, while the IRPP/AAC modelling showed that tighter targeting and higher benefit adequacy could generate larger reductions in poverty and food insecurity. In affordability terms, the CGEB functions as a broad-based measure near the poverty threshold, while the IRPP/AAC proposal focused more support for households facing deeper affordability pressures.

Beyond overall generosity, the design of income-tested benefits plays a central role in determining who benefits most. Holding total program costs constant, alternative targeting parameters can meaningfully shift resources toward households experiencing the greatest affordability pressures.

The structure of the GST/HST Credit illustrates these trade-offs clearly. Because benefits phase out gradually over a relatively wide income range, incremental increases tend to deliver meaningful gains to households near the low-income poverty threshold, while providing smaller relative improvements to those with the lowest incomes. Design features such as the phase-in for single adults further influence how support is distributed across the income spectrum, limiting gains for individuals in deepest poverty.

Alternative targeting choices, including concentrating benefit increases at lower income levels, adjusting phase-out thresholds, or modifying benefit schedules to prioritize adequacy at the bottom, can alter the affordability impact of a program without increasing total expenditures. In this sense, who receives additional support, and at what income levels, can matter as much as how much is spent overall.

Households near the MBM threshold can still face affordability challenges. However, when resources are limited, benefit design can determine whether an expansion primarily stabilizes household finances near the poverty line or delivers deeper relief to households struggling most to meet basic needs.

Even well-designed income supports can fall short of their intended impact if structural barriers limit access or offset gains. Two implementation challenges are particularly relevant for the CGEB: non-take-up due to tax non-filing and interactions with provincial income-tested programs.

First, reliance on the tax system means that individuals who do not file a tax return remain excluded. Non-filing rates among low-income Canadians are estimated at 10 to 12 per cent, with higher rates among working-age individuals, Indigenous peoples, people experiencing homelessness, and those in precarious housing. These are also the groups most likely to experience food insecurity and severe affordability pressures. The planned rollout of automatic tax filing, beginning in 2026, has the potential to substantially improve reach, but its effectiveness will depend on implementation that accounts for barriers related to digital access, financial exclusion and unstable housing.

Second, interactions with provincial and territorial income-tested programs may reduce the net impact of the CGEB for some recipients. In jurisdictions where particular income and social support or housing benefits are clawed back as income rises, federal benefit increases can be partially or fully offset, limiting improvements in affordability. Without co-ordination, these interactions risk blunting the effectiveness of federal efforts to address cost-of-living pressures.

Together, these factors underscore that improving affordability requires consideration of not only benefit design, but also accessibility, delivery and policy interactions across orders of government. Addressing non-filing and minimizing offsetting clawbacks would strengthen the CGEB’s ability both to reach households facing the greatest affordability challenges, and to translate nominal benefit increases into real improvements in living standards.

The Canada Groceries and Essentials Benefit is a step toward addressing persistent affordability pressures through an existing, well-established transfer mechanism. By expanding the GST/HST Credit, the federal government has opted for a policy tool that can be delivered quickly, reaches a large share of lower-income households, and involves relatively low administrative complexity.

At the same time, the analysis in this commentary underscores that the effectiveness of affordability measures depends as much on design as on overall generosity. The CGEB improves affordability primarily for households near the low-income threshold, while offering more limited relief for those facing the most severe material constraints. Comparisons with prior IRPP/AAC work highlight how alternative targeting and benefit structures that concentrate support at the bottom of the income distribution can better address affordability issues for those with the lowest incomes and yield larger reductions in poverty.

Looking ahead, the CGEB should be viewed not as the final policy response to food insecurity, but as a foundation. Adjustments to targeting parameters and attention to take-up barriers such as tax non-filing could significantly strengthen its impact. As governments continue to grapple with elevated costs of food and other essentials, refinement of how support is delivered will be critical to ensuring that affordability measures meaningfully improve living standards for those who need them most.