Redesigning Canadian Trade Policies for New Global’s Realities

Overview of the Research Findings

Stephen Tapp, Ari Van Assche and Robert Wolfe

Erik van der Marel is a senior economist at the European Centre for International Political Economy (ECIPE) in Belgium, where his research focuses on services trade policy. Prior to his appointment at ECIPE, he lectured at the London School of Economics and he was a research fellow at the Groupe d’Économie Mondiale (GEM) institute in Paris at Sciences-Po. He has been a consultant at the European Commission, the OECD and APEC, and he was a visiting researcher the World Bank. He received his Ph.D. in international economics from Sciences-Po Paris. He also holds an MSc in economics from the Erasmus University in Rotterdam and an MA in European politics from the College of Europe in Bruges.

Redesigning Canadian Trade Policies for New Global Realities, edited by Stephen Tapp, Ari Van Assche and Robert Wolfe, is the sixth volume of The Art of the State. Thirty leading academics, government researchers, practitioners and stakeholders, from Canada and abroad, analyze how changes in global commerce, technology, and economic and geopolitical power are affecting Canada and its policy.

The rules governing international trade in services increasingly are being negotiated through large regional trade agreements. Services feature prominently in Canada’s recently concluded Comprehensive Economic and Trade Agreement (CETA) with the 28 members of the European Union and in the 12-country Trans-Pacific Partnership (TPP). Canada is also currently involved in the 50-country Trade in Services Agreement (TiSA). (See the appendix to this chapter for a list of the countries involved in CETA, the TPP and TiSA.) Services are important for Canada’s trade for several reasons:

Despite the growing importance of services in its trade, however, Canada appears to be “undertrading,” relative to economic fundamentals, with certain key trade partners. After examining the likely effect of CETA, the TPP and TiSA on Canada’s services trade over the medium term, I conclude that the largest untapped potential for growth is with the United States, followed by several members of the European Union. In terms of trade negotiations to pursue these gains, Canada might benefit from the TPP — most notably with the United States, though likely not as much as was hoped for. Naturally, CETA could improve Canada’s services trade with the European Union, even though several sensitive sectors were essentially kept off the negotiating table. Finally, TiSA could expand market access to a broader set of countries, although the ultimate level of ambition in this deal remains to be tested.

At the same time, I argue that Canada does not need to negotiate trade agreements in order to develop a more competitive services sector. Canada has plenty of opportunities to remove domestic restrictions unilaterally or to lock-in existing trade preferences, particularly in services sectors that are important inputs to the rest of the economy but where barriers to foreign entry remain high, such as in transportation, finance and telecommunications. These actions would provide broader economic benefits to Canada’s economy over the long run even if outstanding trade agreements are not implemented in a timely fashion.

As a share of GDP, Canada’s exports of services rose from 3.0 percent in 1981 to a peak of 5.4 percent in 2004 before falling somewhat to 5.0 percent in 2015.1 Canada has a well-diversified export basket of services, with the most active areas being business services — a key component of Canada’s comparative advantage is in accounting, financial services, engineering, architecture, telecom and computer services — followed by travel and transportation.

Canada’s most important trading partner for services is the United States, the destination of more than half of its services exports. France, Canada’s second-largest services trade partner, in contrast, accounts for only 3.4 percent of services exports. Similarly, more than half of Canada’s services imports are from the United States, followed by the United Kingdom with 4.5 percent. Other notable trading partners for Canada’s services are China, Hong Kong, Japan, Mexico and Australia, all of which, except China, are involved in ongoing trade negotiations with Canada.

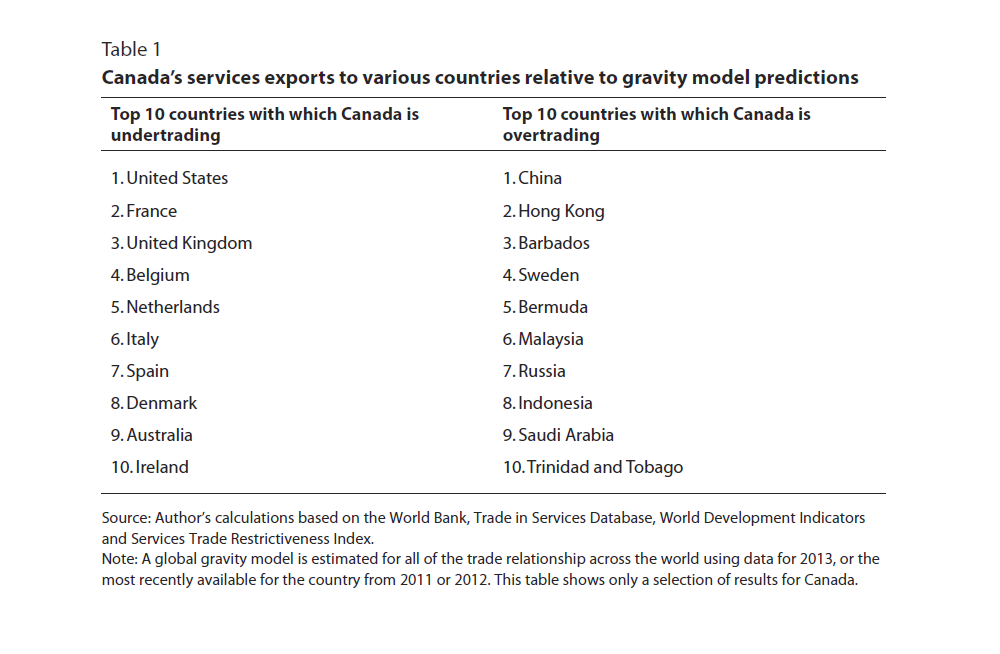

The extent to which Canada stands to gain from trade agreements with various trading partners varies considerably. One way to shed light on the upside of Canada’s services trade potential is through gravity analysis. This approach shows how much a country’s exports differ from a gravity model’s predictions based on factors such as distance, the size of the country’s GDP and endowments such as the quality of the labour force, information and communications technology infrastructure and the regulatory environment, all of which also affect trade costs.2 If Canada exports more services to a given country than the gravity model predicts, it is said to be “overtrading” with this partner; conversely, Canada is “undertrading” when actual values are below the model’s predictions (see table 1) which reports results for the top 10 countries with which Canada is estimated to be under- and over-trading based on the structural factors described above). These results provide useful, if noisy, signals suggesting that Canada could improve its services trade more with particular countries, especially if it implements more supportive services trade policies.

Using such gravity analysis, an important finding — consistent with that of Anderson, Milot and Yotov (2014) — is that, even though the United States is by far Canada’s top services export market, Canada is significantly undertrading with that country, as well as with several EU members, including France, the United Kingdom, Belgium, the Netherlands, Italy, Spain, Denmark and Ireland. On the other hand, Canada is overtrading with China and Hong Kong, as well as with certain tax havens such as Barbados and Bermuda — likely related to financial services flows.

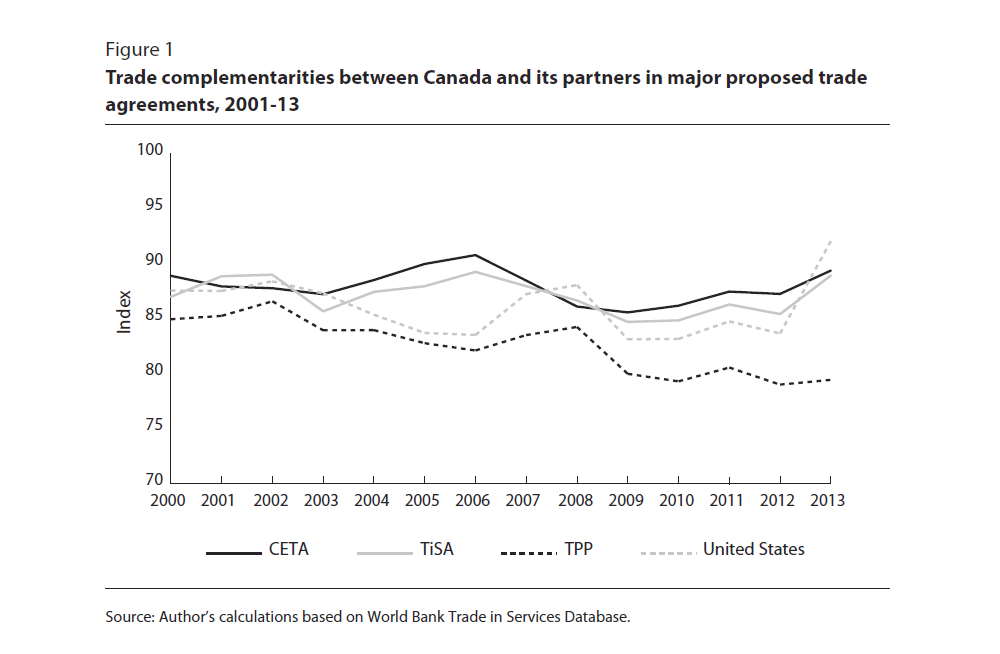

Another approach to gaining some insight into Canada’s services trade prospects is through a services trade complementarity index, which tries to capture the “goodness of fit” between Canada’s services exports and its trading partners’ services imports. This approach assumes that each trading partner will benefit more from exporting in its areas of comparative advantage and from importing in its areas of comparative disadvantage (for further details, see Cadot, Carrère and Strauss-Kahn 2011). A higher score indicates that the country is better-suited as Canada’s services trading partner, while a lower score indicates less potential to expand Canada’s exports to these countries.3 As figure 1 shows, Canada’s complementarity scores are high for all three trade agreements recently concluded or still in negotiations (generally in the 80s out of 100), which indicates that the country groupings in these trade deals are a reasonably good fit for Canada. A smaller point to note is that, although the good match between Canada and its CETA and TiSA partners has been relatively stable over the past decade, the services trade complementarities between Canada and its TPP partners — the United States aside — have declined slightly over this period.

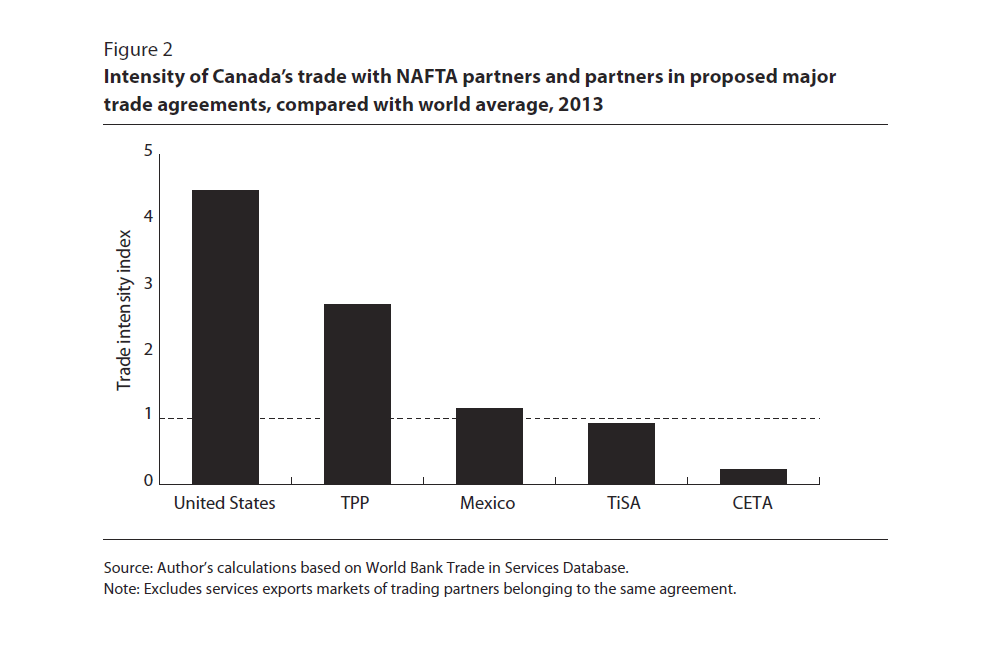

A third perspective on Canada’s services trade can be gained by estimating how its relative “services presence” differs with the countries in each trade agreement. For this purpose, figure 2 displays a trade intensity index that indicates if the value of trade between the partners is greater or smaller than expected based on their importance in world trade. Here, the index is measured by the share of Canada’s services exports to each of these agreements’ trading partners, divided by share of the world’s overall services exports to each of these agreements’ collective markets. A value of more than 1 indicates that Canada’s bilateral trade flows with these countries are larger than the world average and, thus, that Canada already has a higher-than-average services presence in these markets prior to the implementation of these agreements. In these results, the United States and Mexico are reported separately from the rest of the TPP partners in order to assess the potential incremental benefits of free trade with the others as an add on to the North American Free Trade Agreement. By this measure, Canada is already trading relatively intensely with its partners in the TPP overall. On the other hand, Canada exports slightly fewer services to TiSA countries, and far less to the European Union, than the world average.4

In sum, there is potential for Canada to expand its services exports to the United States and to several EU countries. However, although Canada is already quite active in the US market, it is much less so in the European Union, as seen in its low services trade intensity with its CETA partners relative to the global average. At the same time, Canada has quite a high trade complementarity with both the United States and the European Union. Finally, trade negotiations might open up the markets of some countries — including Israel and South Korea — that are not in either CETA or the TPP, but are negotiating TiSA. Indeed, in 2015, Canada implemented a new trade deal with South Korea and modernized its existing agreement with Israel.

Since Canada is undertrading with EU countries with respect to services exports, it makes sense to tackle, through the CETA negotiations, regulatory trade and market access policies in those countries that are hampering Canada’s exports in areas where it has a comparative advantage. For example, Estonia has high restrictions in engineering and legal services, while Poland has nationality requirements in accounting and auditing, architecture and engineering. Ideally, CETA would address these and other issues that inhibit increasing trade and investment flows. As with any trade negotiation, however, CETA accords special treatment to “sensitive” sectors such as air transport, government and cultural services, telecoms and finance, leaving unchanged restrictions on many services in which Canada is quite productive.5

Imports matter, too, which is why Canada’s services trade performance could be increased if it were to open up its own services markets by abolishing unnecessary regulations that raise costs in Canada and by reducing market access regulations for foreign services providers operating in Canada. Such moves not only would benefit sectors of the economy in which services are an important input; they would also reduce the significant adverse influence of regulatory measures at the border and behind-the-border on the productivity of the services sector itself (van der Marel 2012). Indeed, inputs such as transportation, finance and telecommunications are essential drivers of aggregate economy-wide productivity (Arnold et al. 2010; Arnold, Javorcik and Mattoo 2011). Better productivity in these sectors, in turn, could help Canada discover new export markets beyond those identified above as having high potential for its services trade.

In Canada, several services sectors — including transportation services and retail — enjoy high levels of protection from international competition. Most restrictions in these services are on foreign entry and investment. For instance, screening approvals for telecoms, cargo and passenger air transport and the distribution sector require that the foreign services provider demonstrate a positive net economic benefit when investments exceed certain thresholds. Domestic investors, in contrast, face no such tests. Under CETA, the screening procedure would remain, but the threshold would increase for EU members (from $354 million to $1.5 billion, excluding state-owned enterprises), and at least 25 percent of the board members of Canadian enterprises would have to be Canadian residents or citizens. Restrictions would also remain on the maximum equity share a foreign company can have in the telecoms sector (one-fifth) and on the maximum share of foreign ownership (one-third). Yet, if Canada wants to be truly competitive in services in global markets, it needs to negotiate away policy barriers in partner countries and abolish its own domestic restrictions. Although Canada and the European Union could still push for greater concessions in TiSA, it remains to be seen what that forum can deliver beyond simply locking in previous reforms (see Marchetti and Roy 2014).

Although abolishing regulatory barriers under CETA, the TPP or TiSA should help to lower the trade costs that Canadian firms and consumers face, having a services trade agreement in place does not guarantee to reduce such costs significantly (Miroudot and Shepherd 2014). Accordingly, Canada should seek other ways to lower its trade costs. For one, since regulatory policies within Canada itself affect the competitive environment for its exporters (Sáez et al. 2015; Nordås and Rouzet 2015), reducing restrictions on services trade — which are nondiscriminatory and impact both imports and exports — would improve Canada’s export performance. Such a move could also improve other domestic policies. For instance, with more liberal services markets, Canada would face pressure to increase both its level of human capital (including entrepreneurial ability) and the quality of infrastructure for services, such as telecommunication networks, that facilitate the delivery of services across borders, and to maintain a strong rule of law to ensure foreign confidence in using Canadian services that are contract-sensitive.

Admittedly, these “enabling” factors of services trade are broad and cannot be easily adjusted in the short run, but they nonetheless could promote services trade in the long run. They are also related to a country’s comparative advantage. For instance, Canada has a comparative advantage in business services, which are often complex and require a longer start-up time before workers are fully trained in their jobs. These services are even more sensitive to some of Canada’s domestic economic and structural endowments. Business services not only require strong human capital, but also sound domestic institutions that can enforce contracts between buyers and suppliers. These services often need to be tailored to the needs of individual consumers, and since services are intangible, tailored characteristics are harder to define in contracts. Other important enabling factors that a government can implement are an attractive business environment, improved trade-related infrastructure for services such as logistics services — which, in turn, could help global supply chains function more smoothly — and a better domestic governance framework that regulates services markets.

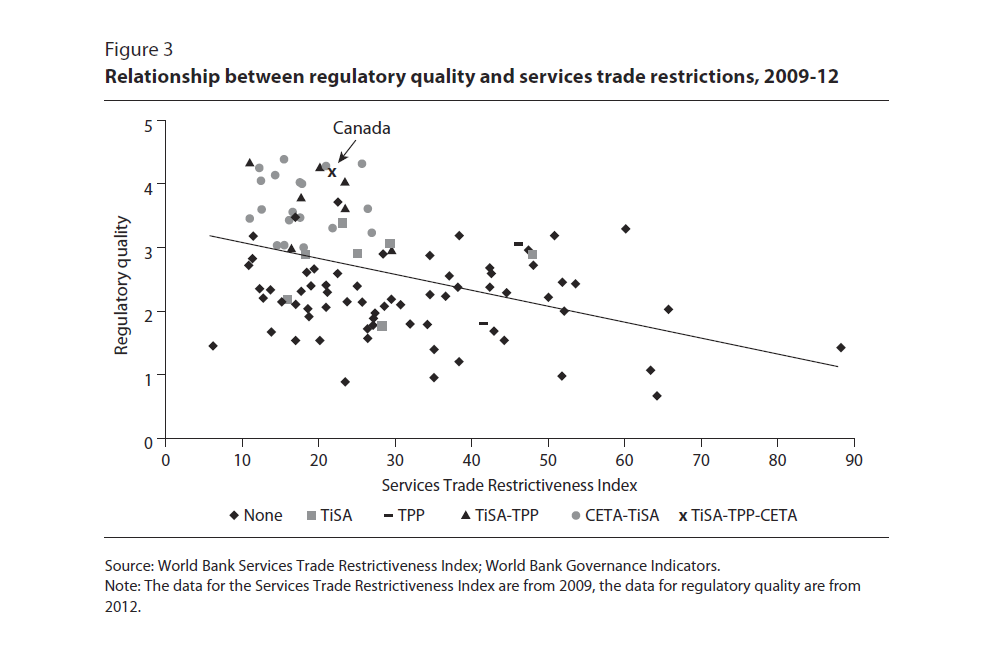

Undoubtedly, it is essential that the regulatory framework for services markets work well, most obviously because services are regulation-intensive. This requires strong, independent regulators who reduce trade restrictions and implement complementary policies — including competition policy — for open market development after trade liberalization takes place (van der Marel 2016). As figure 3 shows, on average, countries with better overall regulatory quality (countries higher up the vertical axis) also tend to have lower levels of services trade restrictions (countries farther to the left on the horizontal axis).

From a global perspective, Canada is relatively well placed, as it exhibits a lower–than-average level on the Services Trade Restrictiveness Index compiled by the World Bank (which differs from that of the OECD) and governs its markets in a highly competitive manner by comparison. Canada’s trading partners in CETA, TiSA and the TPP vary widely in their levels of both regulatory services restrictions and regulatory quality. Most CETA countries have only minor restrictions in place, while their regulatory governance structures are, on the whole, relatively good, making the European Union an attractive services trade partner for Canada. Services are nonetheless an important component of the proposed agreement, which deals with competition policy (Chapter 17) and state enterprises and national monopolies (Chapter 18) in its support of the tradability of services. Again, however, various services sectors are excluded, including audio-visual services (in the European Union), cultural services (in Canada) and financial services and air transport services (on both sides). Notably, in air transport services, Canada would retain not only its high restrictions on foreign entry, but also its many barriers that inhibit competition. These services are essential to Canada’s overall trade competiveness, and ideally should be addressed in the TiSA negotiations, though this might be unlikely.

CETA, the TPP and TiSA have not actually been implemented yet, so their benefits have yet to be realized. Nonetheless, these expected benefits can be described as follows: Canadian services firms would have greater access to the markets of agreement signatories, leading to greater economic benefits. In return, Canada would face greater competition at home from services suppliers based in the trading partner countries, leading to lower prices and more choice for consumers. Since some disruptions and skill adjustments likely would occur, the Canadian government should help smooth this adjustment process by implementing effective skills reallocation policies, given that services are particularly labour intensive. Canada could also do much beyond trade agreements to improve the overall competitiveness of its services sector by increasing skills and information and communications technology infrastructure, and by creating a more efficient logistics structure.

Even with the implementation of these agreements, Canada has to be aware of the potential effects of other proposed deals, notably the Transatlantic Trade and Investment Agreement (TTIP), currently under negotiation between the European Union and the United States, Canada’s biggest partner in the North American Free Trade Agreement (NAFTA) and the market for the bulk of Canada’s services exports. Even though the likely outcome of the TTIP agreement is not yet known — at the time of writing, expectations are not high (see Francois, Hoekman and Nelson 2015) — the possibility of preference erosion away from NAFTA is a concern. Canadian firms, which already encounter tough competition in the US market (Messerlin 2015), would face still tougher competition there from EU companies if a meaningful TTIP agreement on services were put in place. That said, the services dimension of NAFTA is relatively deep, which should buffer Canadian firms against some of the effects of a deeper TTIP agreement. Similarly, a relatively deep CETA would give Canadian firms an “insurance policy” against tougher competition in the EU market in the event of subsequent agreements between the European Union and other countries.

In the near term, one way for Canada to avoid preference erosion as a consequence of a deep TTIP agreement is to rely on “ratchet mechanisms” that would emulate whatever policies the European Union and the United States subsequenly agree to. Gains could also be realized by establishing effective regulatory councils — of which the Regulatory Cooperation Forum created under CETA is a good example. In the long term, preference erosion could be reduced by pushing for the TTIP to be an open agreement, which would allow other countries to join later if they so desired. Canada and Mexico would be natural candidates to join such an open agreement, given the tightly integrated North American market. Finally, looking ahead at the remainder of the TiSA negotiations, Canada could push for additional market access beyond just locking in the status quo, which would be beneficial for all of the agreement’s signatories.

Comprehensive Economic and Trade Agreement (CETA)

Trans-Pacific Partnership (TPP)

Trade in Services Agreement (TiSA)

Anderson, J.E., C. Milot, and Y.V. Yotov. 2014. “How Much Does Geography Deflect Services Trade: Canadian Answers.” International Economic Review 55 (3): 791-818.

Arnold, J., B. Javorcik, M. Lipscomb, and A. Mattoo. 2010. “Services Reform and Manufacturing Performance: Evidence from India.” CEPR Discussion Paper 8011. London: Centre for Economic Policy Research.

Arnold, J., B. Javorcik, and A. Mattoo. 2011. “Does Services Liberalization Benefit Manufacturing Firms? Evidence from the Czech Republic.” Journal of International Economics 85 (1): 136-46.

Cadot, O., C. Carrère, and V. Strauss-Kahn. 2011. “Trade Diversification: Drivers and Impacts.” In Trade and Employment: From Myths to Facts, edited by M. Jansen, R. Peters, and J.M. Salazar-Xirinachs. Geneva: International Labour Organization.

Francois, J., B. Hoekman, and D. Nelson. 2015. “TTIP, Regulatory Diversion and Third Countries.” In Catalyst? TTIP’s Impact on the Rest, edited by M.S. Akman, S. Evenett, and P. Low. London: CEPR Press.

Head, K., and T. Mayer. 2014. “Gravity Equations: Workhorse, Toolkit, and Cookbook.” In Handbook of International Economics, vol. 4, edited by G. Gopinath, E. Helpman, and K. Rogoff. Kidlington, UK: Elsevier.

Marchetti, J.A., and M. Roy. 2014. “The TISA Initiative: An Overview of Market Access Issues.” Journal of World Trade 48 (4): 683-728.

Messerlin, P. 2015. The Transatlantic Trade and Investment Partnership: The Services Dimension. Paper 6 in the CEPS-CTR project “TTIP in the Balance” and CEPS Special Report 106. Brussels: Centre for European Policy Studies.

Miroudot, S., and B. Shepherd. 2014. “The Paradox of ‘Preferences’: Regional Trade Agreements and Trade Costs in Services.” World Economy 37 (12): 1751-72.

Nordås, H., and D. Rouzet. 2015. “The Impact of Services Trade Restrictiveness on Trade Flows: First Estimates.” OECD Trade Policy Paper 178. Paris: OECD Publishing. Accessed June 26, 2016. https://dx.doi.org/10.1787/5js6ds9b6kjb-en.

Palladini, J. 2015. Spotlight on Services in Canada’s Global Commerce. Ottawa: Conference Board of Canada.

Sáez, S., D. Taglioni, E. van der Marel, C. Hollweg, and V. Zavacka. 2015. Valuing Services in Trade: A Toolkit for Competitiveness Diagnostics. Washington, DC: World Bank.

Tinbergen, J. 1962. Shaping the World Economy: Suggestions for an International Economic Policy. New York: Twentieth Century Fund.

van der Marel, E. 2012. “Trade in Services and TFP: The Role of Regulation.” World Economy, 35 (11): 1387-1429.

van der Marel, E. 2016. “Ricardo Does Services: Service Sector Regulation and Comparative Advantage in Goods.” In Research Handbook on Trade in Services, edited by P. Sauvé and M. Roy.