Canadian Policy Prescriptions for Dutch Disease

Robin Boadway, Serge Coulombe and Jean-François Tremblay

Analyses of the impacts of population aging in Canada have typically emphasized the costs of aging while neglecting some important, positive impacts. This omission of likely positive factors leads to overly pessimistic scenarios about the economic and fiscal consequences of aging in Canada, even though some data indicate that population aging can have economic benefits as well as costs.

In particular, the oft-predicted shortfall in net domestic savings due to a drawing-down of assets by retired individuals and increased government spending on programs serving the elderly does not take into account the fact that the uses of savings will also decline with reduced needs to finance physical capital. This means that there will be no net shortage of savings, and that capital returns (interest rates) will fall relative to wages instead of rising, as is usually anticipated. When compounded over the next fifty years, a span embracing an unprecedented pace of population aging in Canada – and in many of the countries accounting for the lion’s share of world income, including China – this rise in wages will have dramatic impacts.

In particular, the relative attractiveness of wages will provide a strong incentive for younger individuals to accumulate human capital through education or training, and for future older workers to remain in the labour force longer than current older workers do. The wages of skilled workers belonging to a given age group (cohort) do indeed rise when the relative cohort size diminishes. There is also evidence that workers are more inclined to join the labour force when labour is in high demand, and that more educated cohorts remain longer in the labour force. This suggests that in future years workers will tend to retire at an older age than they do now.

As a result of these factors, it is even possible that the overall economic impact of aging in Canada will be positive. Although it would not be prudent to base policy on such a best possible outcome, it can be concluded at the very least that apocalyptic scenarios are exaggerated.

Another reason to view population aging with equanimity, at least in Canada, is that governments’ revenues will be bolstered by taxable withdrawals from Registered Retirement Savings Plans (RRSPs) and other tax-deferred private pension programs, precisely when upward pressure public expenditures related to old age – particularly on health care and public pensions – are expected to be most acute. Currently, the net cost of the tax exemption related to these programs constitutes a net “tax expenditure” for governments – but, as demonstrated by new simulations, the net tax expenditure will drop considerably in the years to come, and even turn into a sizeable source of net revenues beyond the year 2030.

The role of net tax expenditures associated with private pension programs has been too often neglected in the literature. This has resulted in an overly somber assessment of both the future ability of Canadian governments to handle aging-related spending pressures, and the intergenerational equity problem implicit in the need to finance the baby boomers’ old age out of the earnings of a less numerous younger generation.

The challenges associated with aging in Canada will require greater flexibility in the face of changing spending priorities, encouraging human capital acquisition in younger generations and removing barriers to labour force participation among individuals nearing retirement. They also require defusing the expected regional imbalances in the country between aging-related needs and fiscal resources. If we can deal with these issues, there is no need to dread the impact of the aging of our population on Canadians’ standards of living or on public finances.

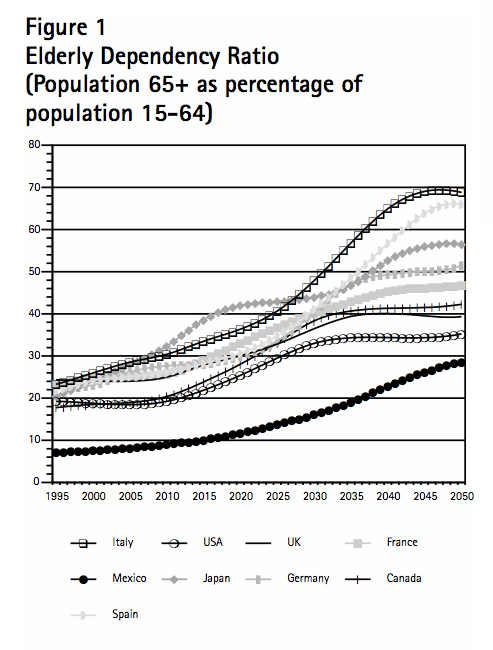

Many parts of the world, especially industrialized countries, will experience a rapid increase in the proportion of elderly in their populations early in this century. The cause of this demographic shock will primarily be the baby boom generation (those born between 1946 and 1966) heading for retirement, although increased longevity and persistent low birth rates are also contributing factors. Consequently, the elderly dependency ratio, defined as the number of individuals aged 65 and over divided by those aged between 15-64, is expected to rise dramatically. According to the United Nations’ medium variant population projections, in the coming decades the proportion of elderly people in Organization for Economic Cooperation and Development (OECD) countries will more than double (from 11.3 in 1990 to 24.5 percent in 2050).1 Low birth rates have already affected total world population trends: the population growth rate has decreased from 1.5 percent in the early 1980s to the current rate of 1.25 percent and is projected to fall steadily to 0.5 percent by 2050.2

Many studies are predicting difficult if not apocalyptic times as a result of these striking demographic transitions. For instance, in a 1994 report the World Bank speculated that because extended families and other traditional means of supporting the old were weakening, and at the same time public pensions were unsustainable and difficult to reform in many countries, a “looming” age crisis was threatening not only the old but also their children and grandchildren.3 In 1998, the OECD said that urgent reforms were needed to discourage early retirement and to slow, even to stop the increase in the amount of time spent in retirement.4 According to the OECD, if such reforms are not adopted, there will be serious fiscal problems and economic growth will suffer. The Group of Ten (G-10) states that demographic developments in the G-10 countries will significantly widen budget deficits and have adverse effects on material living standards unless action is taken to encourage national saving, the supply of labour, and an efficient allocation of savings, both within and across borders.5 Bichot claims that pension benefits are threatened in France,6 and Peterson,7 a former US Secretary of Commerce, asserts that the aging crisis threatens to bankrupt the world’s wealthiest nations, deter the gains of liberal democracies and fuel intergenerational conflict. Ferguson and Kotlikoff concur, and predict that the European Monetary Union will disintegrate in the medium term as the single currency becomes incompatible with the fiscal strains that accompany aging populations in the most of the euro zone countries.8 With respect to Canada, Gee cites apocalyptic scenarios described in a series of newspaper reports,9 and the popularity of David Foot’s book, Boom, Bust, and Echo10 is a good indication of the extent to which the importance of our demographic fate is deeply rooted in common beliefs.

I will offer a more optimistic view of these important demographic changes. I believe that there are numerous market and institutional feedback mechanisms in modern economies that would offset many of the pessimistic scenarios predicted. One key factor is human capital. Population aging implies an increase in the scarcity of labour relative to physical capital, and one of its effects will be to increase future wages relative to capital return. This will create greater incentives for investment in human capital, whose importance as an engine of growth is increasingly being recognized as industrialized countries shift away from resource-based and toward knowledge-based economies. This trend and the consequent implications for human capital are likely to accelerate with the globalization of markets and technological change. In Canada, this offsetting beneficial effect on wages will be accompanied by a favourable institutional factor, as a sizeable stock of taxable wealth is amassed in the form of contributions to tax-deferred retirement savings plans. These programs lowered Canadian government revenues by 2.3 percent of GDP in 1998, but they are likely to become a new source of government revenue at the most critical point in Canada’s population aging process. These two factors combined will not only smooth the demographic transition toward a much older population, but will arguably offer opportunities for a better standard of living to young and future generations.

Before clarifying the differences between the pessimistic and optimistic scenarios, I will briefly describe in the next section the most salient demographic trends in key regions of the world, including Canada. Then, taking into consideration these demographic trends, I will review the arguments of the apocalyptic school and report on its most important implications. In a subsequent section, I will respond to the predictions of an abyss associated with population aging and present arguments that counter the pessimistic scenario. More specifically, I will discuss human capital formation, labour force participation, educational attainment and productivity trends in the context of an aging population in more optimistic terms and dispute the predicted negative effect of this aging process on economic growth. After showing that an aging population needs not give rise to weak or negative economic growth, I will then investigate the fiscal effects of aging for Canada. In particular, I will describe and report the results of a new model that projects the tax expenditures associated with the existing tax-deferred retirement savings plans in Canada. This institutional factor, added to the non-negative effect on economic growth, should be sufficient to dispose of the idea that a pessimistic scenario is inevitable, at least for Canada. A concluding section follows.

Population aging is a worldwide phenomenon, although it is most pronounced in industrialized countries. In both developing and developed countries the proportion of elderly in the total population is projected to double between 1995-2050 (from 5.6 to 11.2 percent for the former and 11.2 to 21 percent for the latter). However, the difference between the proportion of seniors in the developing and developed countries will widen.11 Similar observations can be made about the elderly dependency ratio. For OECD countries, the average ratio is expected to rise from 17.1 percent in 1990 to 42.1 percent in 2050. For the same time horizon, this ratio is expected to rise from 14.8 to 28.5 percent in Argentina, from 7.1 to 28.9 percent in Brazil, from 8.4 to 31.0 percent in China, from 7.3 to 23.2 in India and from 6.4 to 24.6 in Indonesia.

Among OECD countries, the population aging process started earlier in Japan than in Europe, and earlier in Europe than in Canada and the United States. It is projected that the scale and timing of population aging will continue to differ across countries in the coming decades. As shown in Figure 1, which reports the elderly dependency ratios for OECD countries, population aging will be more rapid and more extensive in countries such as Italy, Spain, Germany and Japan. The ratio for Mexico is lower for the entire period but that country’s eventual aging process is predicted to be faster than that in a number of other OECD countries.

In Canada, the population of seniors is projected to increase at an unprecedented pace, from 3.7 million in 1997 to 10.8 million in 2046, which is equivalent to half of the projected growth in the total population (from 30 million to 44.4 million). The largest part of this increase will take place in the period 2011-2031 as the baby boomers move into the 65 and over age group.

The median age of the population is expected to increase from 36 years today to almost 45 years by 2041. Growth in the working-age population (traditionally defined as the 15-64 age group) will be considerably slower than in previous decades, and a larger proportion of the working-age population will be in “older” age groups. The weight of the 45-64 age group in the working-age population is projected to increase from 32 percent in 1997 to 42 percent by 2021, mostly at the expense of the 25-44 age group. The age composition of the working-age population is then expected to stabilize after 2021. As a result of increased life expectancy, “old” seniors (those aged 75-84) will represent nine percent of the total population in 2046, up from four percent today. “Very old” seniors (those aged 85 and over), the fastest growing segment of the population, will represent five percent of all individuals in 2046, up from one percent today.

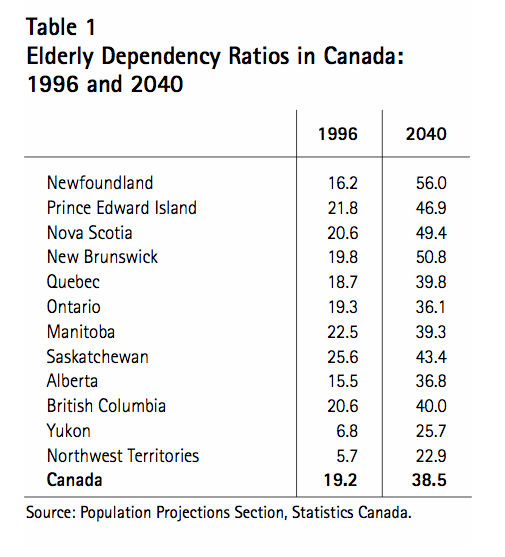

Population aging will not be uniform across Canada. Assuming that interprovincial migration flows will follow the average pattern observed during the 1976-1996 period, population aging will be more extensive in the poorest provinces (Table 1). For instance, between 1996 and 2040 the elderly dependency ratio is projected to rise from 16.2 to 56.0 percent in Newfoundland, whereas in Alberta it will rise from 15.5 to “only” 36.8 percent.

No factor seems able to reverse these trends. There is no evidence of any significant increase in the birth rate or of a favourable change in the age composition of immigration flows. In Canada, life expectancy is expected to continue to increase over the next several decades, with an additional gain of four years for women (to 86 years) and six years for men (to 82 years). And Billings, Lawlis and Roth show that it would take a huge increase in the gross immigration quota — 500,000 per year rather than the current level of around 200,000 — to make a significant dent of three percentage points in the projected share of seniors in the total population.12 Denton and Spencer report similar results.13 Such an increase is improbable, especially as competition between aging societies for immigrants may well become stiffer.

Demographic changes would not be such an important economic issue if individual behaviour was not changing with age and government programs were not sensitive to the age of the population. There is considerable evidence that many individual economic decisions, such as consumption, saving, labour market participation, portfolio diversification and the kinds of goods and services purchased change with age. Typically, people born in industrialized countries have the following life-cycle pattern: In their youth, they borrow in the capital market, invest in human capital by devoting a good portion of their time to education, and work a little; in their middle age, they work a lot, acquire land (with all that is built on it) and save physical and financial capital in order to finance future consumption; in their old age, people have a strong preference for leisure, receive an implicit revenue from the rent of the land, decrease their physical and financial assets, and consume health-care services. Even if we were all born clones of one another, this life-cycle pattern suggests that the size of different age cohorts (i.e., those born in the same year) matters for a large number of economic issues. For instance, government expenditures and transfer programs such as education, health care, and public pensions are sensitive to the demographic structure of the population: a young population stimulates public education needs, whereas an old one puts pressure on public pensions and health care. In addition, cohort sizes influence the size and quality of the active population and the market price of assets, goods and services and factors of production.

When a change in the composition of the population is as significant as the current aging process is in many countries, it may indeed trigger significant macroeconomic effects and pose important fiscal policy challenges. Individual life-cycle behaviour is the microeconomic basis for the potential macroeconomic impact of population aging on the fiscal burden, aggregate consumption and national savings, output and economic growth, and welfare across generations. But while population aging might have sizeable macroeconomic effects, the direction of these effects is debatable.

The direction predicted by the pessimistic macroeconomic scenario works like this: Population aging means those of working age have to support a growing proportion of inactive people, so a decline in public and private savings must be expected. This trend is exacerbated by the fact that people in industrialized countries are living longer and healthier lives, and they are also retiring earlier. Consequently, the length of time spent in retirement is growing. Since the demographic change will be sizable, major adjustments on the fiscal side (higher taxes and/or debt) are inevitable. These fiscal adjustments in turn will create a shortfall in the economy-wide savings rate relative to the investment rate, which will require larger net foreign borrowing and wider trade and current account deficits. All this will lead to a significant slowdown in economic growth and a decline in living standards for the current young generation and future generations. Intergenerational inequity will be considerable as the young and future generations will have to bear the economic burden of providing for aging baby boomers and at the same time provide for themselves when they retire.14 Let us look at these arguments in greater detail.

The OECD estimates that barring increases in participation rates and immigration levels, labour force growth could come to a halt in a few years in many industrialized countries,15 as soon as in 2002 in Japan, according to another study.16 Moreover, a gradual return by older men to the higher labour force participation rates of 1970 would not even come close to reversing the current trend. If this happened, according to the OECD study, the average annual labour-force growth rate in 1995-2020 would still decline significantly, but at a somewhat slower pace: 0.9 percent instead of 0.4 percent, compared with 2.4 percent in 1970-95.

In addition to the labour force being smaller in number, its median age will also increase. According to the pessimistic view, an older workforce may suffer from a depreciation of its skills and may well be harder to retrain when the economy goes through rapid structural change. The rate of industrial innovation and creation may also decline as older workers become less prepared to take risks and thus are less entrepreneurial.

Over time, population aging is expected to lead to a lower private savings rate as individuals begin to consume their accumulated wealth when they reach retirement. A study of seven major industrial countries by Heller concludes that aging will lead to a significant decline in private savings rates after 2000.17 As population aging will affect most industrialized countries, which account for a vast share of global GDP, the pessimistic view emphasizes that the swelling tide of retirees could lead to a dramatic reduction in the world supply of savings and thus significantly increase world interest rates.

As the baby boom generation enters retirement age and the proportion of the elderly increases, the pessimistic scenario spotlights the upward pressure on government spending, stemming from increased demand for health-care services and higher public pension benefits. Already in 1988 the OECD made the following gloomy prediction: “Under existing regulations the evolution of public pension schemes is likely to put a heavy and increasing burden on the working population in coming decades. Such a financial strain may put intergenerational solidarity at risk.”18

Disney argues that most public pension programs in OECD countries are in crisis, as their unfunded status — the fact that current pension payments are financed by current contributions usually levied as payroll taxes — will lead to unacceptable payroll taxes along the demographic shift.19 Robson estimates that the implicit healthcare services liability associated with the pressure of an aging population amounts to more than 50 percent of GDP in Canada, which is almost as large as the current public debt.20

The decreasing proportion of the population that is of working age is also expected to lead to an erosion of the overall tax base (e.g., the personal income and payroll tax bases). This in turn will put upward pressure on government deficits and the debt-to-GDP ratio. Thus, in the absence of additional cuts in government spending or an anticipatory reduction in the debt-to-GDP ratio, the tax burden will have to rise substantially to finance the resulting increase in government spending.

Under the pessimistic scenario, major fiscal adjustments will in turn lead to imbalances between national savings and investments. The resulting large swings in trade and current account balances could exacerbate friction among nations concerning trade and foreign investment policies and even strain monetary policies and exchange-rate regimes, as evoked by Ferguson and Kotlikoff.

The pessimistic view holds that reduced labour force growth, increased world interest rates, and a shrinking tax base forcing governments to raise distorting taxes and/or the public debt will result in slower real potential output growth

Thus, the simulation model of Auerbach et al., in which human capital is not a factor, predicts a gradual and persistent decrease in the national savings rate and the real after-tax wage for Germany, Japan, United States and Sweden between 1990 and 2050.21 Hviding and Mérette, extending the Auerbach et al. analysis to seven OECD countries, find that real per capita GDP would be between 10 and 30 percent lower in 2050 relative to a scenario with no aging.22 The projections resulting from this exercise show Canada’s GDP declining by 20 percent over 50 years, which represents an average annual decrease in real per capita GDP growth of 0.4 percentage points. Denton and Spencer state that in the coming decades, with total population increasing faster than the working population, there will be a decrease in the growth of living standards (that is, GDP per capita) unless there are substantial improvements in productivity per worker.23

I will now turn to a series of points that show the pessimistic view to be, for the most part, an exaggeration. This section contrasts the pessimistic view with a more benign outlook that emphasizes the likely beneficial effect of population aging on human capital investment and the expected positive long-run effects of demographic change on participation rates.

Probably the most important factor determining the implications of population aging on economic growth will be human capital. It is the contention of this paper that population aging will enhance the role of human capital as an engine of economic growth because it creates strong incentives for young and future generations to invest in human capital formation. That investment, in turn, could more than compensate for the decrease in the proportion of the population of working age and the decrease in national savings. This implies that, in policy terms, the importance of the issue of human capital, already highlighted in the aftermath of the information technology revolution, will be reinforced. If the investments in human capital materialize, population aging may stimulate economic growth in the context of a knowledge-based economy and increase the living standards of young and future generations. The mechanisms leading to this result are worth exploring in some detail.

For the majority of economists, the most important determinants of aggregate economic growth are the level of technological progress and the stock of physical and human capital. Invention and innovation are then considered a source of economic (GDP) growth as both imply technological progress that improves the joint productivity of physical and human capital; that is, they lead to an increase in total factor productivity. The other source of GDP growth is the accumulation of factors of production, that is, the increase in the stock (quantity) of physical and human capital. While, as mentioned above, it has been argued that population aging inhibits creation and innovation, it is worth noting that historically, useful technological change has often coincided with changes in resource scarcity. For instance, as predicted by Rosenberg in the context of a potential shortage of natural resources (oil) in the 1970s, a series of innovations improved fuel efficiency in machinery and equipment in the aftermath of higher energy costs, thereby lessening the destructive impact of this change on world economies.24 In other historical periods it has transpired that market economies are able to display adaptive mechanisms to respond to shifting patterns of resource scarcity. Hence we may expect some labour saving technological changes in the future to accompany the aging of the population.

In addition, I expect that such technological changes will be accompanied by an increase in the rate of accumulation of human capital, relative to that of physical capital. This will stem from a rise in wages relative to interest rates (which in the medium term are determined by the return to physical capital), a phenomenon which I explore below.

Human capital can be distinguished from physical capital in two important ways. First, human capital, unlike physical capital, is a non-market good, which implies that the benefit of investing in human capital is restricted to the stream of future net revenue from labour supply. Second, it is embodied in people with finite lifetimes. These two dimensions imply important life-cycle patterns for portfolio decisions. As the returns are the discounted sum of future wage revenues, it is rational for individuals to invest in human capital (e.g. education or training) when young. Since the title to physical capital assets can be sold, it is rational to prefer these assets in preparation for old-aged retirement. Consequently, it is not surprising to observe that investors in human capital are generally young, whereas investors in physical capital are middle-aged.

Both types of capital can be accumulated in the economy without bounds, and thus may be part of the engine of economic growth if they are transferable to succeeding generations. The transfer of physical capital from living to succeeding generations takes place through the market. That of human capital, a non-market and embodied good, is institutional. Indeed, as basic education is compulsory in most countries, we can consider an individual’s own human capital investments as equivalent to studying at the post-secondary level. Therefore the basic educational system preserves a portion of human capital accumulated by living generations for the benefit of new cohorts and permits human capital to grow without bounds, as is the case for physical capital.

The transmission process is based on the fact that, although each person has only a finite number of years that can be spent acquiring human capital, any good this person produces that can be replicated (what economists call “nonrival goods,” e.g. a mathematical theorem, a patent, a blueprint, new ideas, new ways of working) or that can be shared with others (teaching, supervision), lives on after the person dies. The basic educational system is the principal institution under which new knowledge is passed on to young cohorts. Once adult, members of young cohorts have received, as a form of in-kind inheritance, an amount of human capital stock that can be increased if they pursue post-secondary studies. Their contributions to changing the world will later be passed on to succeeding cohorts. Naturally, a change in the quality of the basic educational institutions would alter the process of transmitting human capital and thus affect economic growth.

In the context of aging populations, the economic mechanism stimulating human capital investments could be described as follows. Although aging will put downward pressure on private savings, slower labour force growth will reduce the need for physical capital investment. If the drop in investment is larger than the decline in savings, then, in contrast to the pessimistic macro-economic scenario, interest rates would decline.

Is this likely to happen? I believe so. Cutler et al. have demonstrated that, as the investment rate drops, the optimal savings rate actually declines as the population ages.25 Furthermore, numerous simulation results using overlapping generations models in the framework of a closed economy show a drop in investment that is larger than the decline in savings, thus leading to a decline in interest rates.26 This issue may not be settled yet, since the disparate processes of aging in the different parts of the world and the globalization of financial markets suggest that regional considerations may alter the results obtained by closed economy models. Indeed, Turner et al. have pioneered a global model to investigate this issue, and they obtain a lower and not a higher wage-interest rate ratio.27 However, this model does not properly capture the evolving age composition of the population. In an international model with correctly specified life-cycle behaviours (overlapping generations model), the Ingenue Team obtained projections for the wage-interest rate ratio that are similar to those generated by closed economy frameworks.28

Moreover, the argument sometimes advanced that the wage/interest ratio would fall because of the much slower population aging process in many developing countries disregards the important fact that the countries where aging is most pronounced comprise a very large share of world GDP (China can be included in this category). We can thus reasonably expect that with a relative scarcity of the labour force, population aging will put upward pressures on the wage-interest-rate ratio, i.e make the acquisition of human capital more attractive than that of physical capital.

The above discussion does not imply that rates of return on capital will fall precipitously, which would be the case if the economies with aging population were closed to trade and capital flows. Indeed, the fact that world populations are aging at different paces may give rise to new opportunities for profitable exchanges between regions, a situation of mutually beneficial gains from intertemporal trade, through international financial transactions and capital mobility. The population aging effects on current account balances can be considerable; Higgins estimates that they have exceeded six percent of GDP over the past three decades for a number of countries, and are likely to be substantially larger over the coming decades given the upcoming demographic changes.29 Kenc and Sayan show for the case of Turkey (versus other European countries) how a more rapidly aging region can benefit from higher return to capital in foreign countries.30 Yang confirms Kenc and Sayan’s analysis for the case of Mexico, as a more rapid aging process (versus the United States) has a positive impact on its current account balance.31 Taylor and Williamson document how the massive capital flows from Britain (or the Old World) to the New World (Canada, Argentina and Australia) in the late 19th century was driven by high dependency rates (which depressed private savings) in the New World.32 The projected differences in population aging processes may well permit the repetition of this phenomenon in this century, though not with the same participants nor the same capital-flow directions. This will cushion, but not stop, the decline in the relative return to physical capital in countries where aging is more pronounced.

Population aging will thus encourage human capital formation as the expected decrease in the real return on physical capital (and consequently interest rates) and the expected increase in future real wages encourage young and future cohorts to decrease their investment in physical capital and increase their investment in human capital. Life-cycle patterns of time allocation will thus be affected, as individuals increase their investment in human capital when they are young to supply both more and higher quality labour during middle age than they would otherwise. This, in turn, will raise the productivity of labour and contribute to higher economic growth and living standards in the long run. Stronger productivity growth, as well as increased labour force participation, which I discuss below, would significantly offset the adverse impact of population aging on potential output growth. This would also mitigate the pressure on government finances associated with population aging, as the tax base will increase.

Simulation models have been used to estimate the potential favourable effect of human capital investment. In Fougère and Mérette’s 1999 study, the new investment in human capital that accompanies population aging actually increases economic growth between 0.1 and 0.6 percentage points for the seven OECD countries investigated, compared with the no aging case.33 The same authors have also developed a more detailed model calibrated with a rich set of Canadian data that incorporates institutional features of government programs.34 In their baseline scenario, the human capital formation arising from population aging increases at a steady rate between 1995-2050, resulting in a stock of human capital that is 17 percent higher in 2050 compared with the no aging case.35 This increase in human capital formation does not stem merely from a greater number of post-secondary students, but also from increased effort and intensity on the students’ parts. These features contribute to an average annual rate of economic growth that is higher by 0.8 percentage points, compared to a scenario without aging.

The work of Sadahiro and Shimasawa fairly supports these simulation outcomes. The noteworthy result they obtain for Japan with their computable overlapping generations model is that the growth rate of human capital completely offsets the negative population growth rate, with the implication that the economic growth rate does not decline with population aging.36 This result is based on a reasonable — but as yet untested — assumption in their model that the correlation between the growth rates of the labour supply and of human capital is negative.

A key idea behind the results just discussed is that, as labour force growth slows, wages will rise. It is therefore worth asking whether there is existing evidence that members of a smaller cohort obtain relatively higher pay throughout their working lives. And if so, whether this evidence tells us something about the probability that young and future generations will take the opportunity offered by population aging to invest further in human capital. To respond to these two questions, a review of empirical studies on the subject is warranted.

Intuitively, if age groups are perfectly substitutable in the labour market, the only impact of a change in the size of one labour market cohort would be on the total labour supply, and hence on average earnings. In the polar opposite case, when different age groups are not substitutable in production, a change in a cohort’s size affects the earnings of that cohort only. One way to investigate this imperfect substitution possibility is to study the impact of the entry of the baby boom generation onto the labour market at the end of the 1960s and the beginning of the 1970s. This is a difficult exercise, as the relative wages between cohorts are influenced by the general state of aggregate demand for labour in the economy, as well as the rising participation rates of women during that period. Still, economists have used sophisticated econometric tools in an effort to untangle the different effects.37 The main conclusion of these studies is that cohort size variables have no effect on the earnings of those with low education, thus implying that all such workers are perfect substitutes, or that the excess supply of such workers feeds into the unemployment rate. For groups with post-secondary education, cohort size is significant. There is strong evidence that larger than average cohorts faced depressed initial and subsequent pay earnings. With population aging this means that the smaller upcoming cohort will benefit from higher wage income — i.e. will enjoy greater returns on investment in human capital.

Another way of looking at this question is through the effect of retirements on the real wages of skilled (highly educated) workers, relative to unskilled workers within the same cohort. One possibility is that the retirement rate of the baby boomers will be proportionally greater for the unskilled workers and hence would reduce the ratio of the relative wages of skilled to unskilled workers. In such a case young individuals would rather invest less in human capital as the opportunity cost of foregone earnings is too high and the marginal returns to investment in education decrease. However, I expect instead that demand factors such as the information technology revolution, combined with the globalization of markets for goods through North-South free-trade agreements and other economic integration initiatives (such as the euro zone), will likely generate a more significant shortage of skilled labour.

An important caveat is that even if we accept that population aging offers greater opportunities for investment in human capital, we cannot be certain that these investments will occur. For instance, young individuals and future generations may not anticipate that the smaller size of their cohort will positively affect their future earnings, so they will expect future wage incomes that are equal to the current wage incomes of older workers. In this case, young and future cohorts will underestimate the return to human capital, and the proportion of young and future cohorts seeking post-secondary education will not increase. There may thus be a role for government to ensure that young and future cohorts have complete information before they choose between post-secondary education and the job market. Fortunately for Canada, the behaviour of the young seems to reflect some foresight, since they tend to stay in school significantly longer than their counterparts of 40 years ago and are more likely to pursue some post-secondary education.38 Also, Sunter and Bowlby find that the drop in the labour force participation rate of young people age 15 to 24 between 1989 and 1997 is explained mostly by the rise in full-time school attendance.39

The effect of demographic change on labour force participation rates is underpinned by a range of both demand-side and supply-side factors, and as such is difficult to gauge. Nevertheless, a number of factors that may accompany population aging have the potential to offset some of the negative labour force impacts outlined by the pessimists. These factors are improved job market opportunities, a better-educated labour force and the likelihood of steady rather than declining performance by older workers.

First, it is recognized in the literature that when there is a downturn in the economy, the probability of obtaining work is reduced. As a result, workers are discouraged in their search for jobs, and labour force participation declines. Conversely, the aging process will increase the relative scarcity of labour, and the probability of finding work will increase in the coming years. This will decrease the cost of job searches in the labour market and should stimulate labour force participation.

Second, educational attainment is presently higher among younger cohorts, which implies that the older workers of the future will be better educated than older workers are now.40 As educated workers tend to work over a longer horizon, the participation rate will increase and the current trend toward increased time spent in retirement may be reversed.

Using an econometric model that employs data on specific age-sex cohorts, Paquet, Sargent and James investigated the past and future behaviour of the employment rate in Canada for all ages.41 Their results show that improvement in the economy will increase employment rates in most groups, especially the young, until around 2005. Participation rates of older men could also increase if housing prices and interest rates decline, a scenario consistent with that predicted by models with correctly specified life-cycle behavior. Past 2005, the employment rate will stay relatively constant for men but rise for women, as women are expected to work longer at an older age than the current working generation. It must be noted that the economic analysis by Paquet et al. does not include an education variable. Since the education level of the Canadian population has increased significantly since 1970, and since better-educated people tend to retire later, it is highly probable that employment rates will be even higher when these better-educated cohorts approach the traditional retirement age.

Third, on the productivity front, there is no evidence that the performance of older workers is generally and systematically lower than that of their younger counterparts. Warr cites numerous studies that show that there is no significant difference between the job performances of older and younger workers.42 Also, Statistics Canada’s International Adult Literacy Survey points to only a modest decline in literacy skills between ages 40 and 65, after controlling for demographic, education and economic variables.43

One worry, however, is that some institutional features of the income security system may have perverse incentives on older individuals’ labour force participation. For instance, Baker, Gruber and Mulligan report that in Canada the public income security system provides increasingly strong disincentives to work after age 60.44 That system alone could explain 34 to 40 percent of early retirements among men and 34 to 44 percent of such retirements among women. These numbers are about twice those observed in the United States by Coile and Gruber.45 Clearly, reforms that reduce these disincentives would reinforce the positive impact I just described of population aging on labour force participation.

To summarize, slower labour force growth rate is a widely recognized consequence of population aging, but there are offsetting factors such as higher investment in human capital and rising participation rates. As a result, growth in the effective labour force may not drop much with population aging. Fougère and Mérette show for the case of Canada, that when this mechanism and the tax smoothing effects of private pension plans (to be discussed in details below) are fully at work, an aging population actually raises the welfare of young and future cohorts by up to five percent for individuals born in 1995 and almost 7.5 percent for those born in 2010, although those born before 1965 suffer a welfare loss.46 When these mechanisms work at only half of their probable strength, welfare improves only for cohorts that are born after 1985 (two and four percent increases for those born in 1995 and in 2010, respectively), whereas the welfare losses for previous cohorts oscillate between 0.5 and 2.5 percent. Finally, the welfare impact is negative for all cohorts if neither new investments in human capital nor tax smoothing effects from private pension plans occur.47

To these two mechanisms can be added the probability of technological progress in response to the emerging resource scarcity (labour), already mentioned, and the possibility of a further small but positive increase of the labour force that could be obtained by increasing the annual flow of immigrants. Thus, we can reasonably conclude that aging populations will not weaken economic growth to the extent forecast by the pessimistic predictions — and could indeed usher in gains for younger generations of Canadians.

I now turn to an examination of the extent to which an aging population presents a fiscal problem for governments overall in Canada.

The Canadian case is an unusual one given the existence of generous tax-deferred savings plans. I address the issue of fiscal balance under the assumption that an aging population will not result in weak or negative economic growth, consistent with the conclusion of the preceding section of the paper — although my main conclusion would hold under more pessimistic growth scenarios. I address the issue by reviewing government expenditure programs that are the most sensitive to population aging.

Pressures on public health expenditures are inevitable; health-care costs rise steeply during old age. On average, the per capita public spending on health for those aged 65 and over is almost five times greater than for the rest of the population.48 Moreover, the very old, who require more frequent medical and long-term care, are expected to be the fastest-growing age group in the population and will thus increase the pressure on health care. King and Jackson estimate that those aged 85 and over absorb 9 times the per capita health-care dollars devoted to those aged under 40.49

The health of elderly Canadians has improved significantly over the past generation, thanks to the expansion of the retirement income system and universal medicare. However, relative to the rest of the population, seniors are more likely to suffer from chronic conditions, be limited in their daily activities, and have illnesses that are serious enough to require hospitalization.Whereas for seniors, the risks of some major heart disease and strokes have declined, the risks of chronic diseases are growing. The effect of this shift on health expenditures is not clear. Moreover, seniors are great consumers of drugs, another important driver of health-care costs. Indeed, it is estimated that about 40 percent of prescription drug expenditures are for those aged 65 and over, which is more than three times their share of the population. This proportion will be difficult to contain, at least for some types of health problems. For example, Bland reports that the remission rate for psychiatric disorders is low in the over-50 age group, and that future retirees will have higher rates of depression than preceding generations.50 But the most intensive strain on health-care expenditures may come from the very old, who are more vulnerable to severe disabilities and require more health care and social support. In 1996, 84 percent of seniors living in institutions were aged 75 years or older. Seniors aged 75 and over use three times more home care services (housework, meal preparation and personal care) than those aged 65 to 74. With the breakdown of the traditional nuclear family, it is unrealistic to hope that the expected increase in the demand for home care services will be supplied in great proportion by informal channels.

It is believed that the risks of being subjected to many types of health problems, including those occurring later in life, are linked to economic, social, environmental, cultural and gender-related factors. Seniors with low incomes are significantly more likely to experience adverse health conditions than are those with high incomes. Not surprisingly, Canadians in the highest income brackets live longer than those in the lowest brackets. These facts are true for both men and women, although more so for men. Almost 70 percent of men from rich neighbourhoods live to the age of 75, compared with about 50 percent in the poorest neighbourhoods.51 Among the very old of both sexes, those who are alone are much more likely to find themselves in institutions compared with those who still live with a spouse or companion.52

Containing health-care costs may require a profound review of health-care services. For example, Bland argues that the best way to control psychiatric costs would be to encourage independence and mobility in the elderly. This would require a major change in psychiatric practices, toward working more closely with the people they serve and with primary care givers. Carrière argues that the biggest challenge for the Canadian health-care system will be to find the will and the capacity to reallocate financial resources to home care services.53

In summary, the key drivers of public health-care costs related to aging are the health of future cohorts of seniors, their economic and social status and their family situations; trends in medical technologies and medications; the provision of long-term care; the extent to which families and relatives provide informal care; and the proportion of health expenditures that is privately funded. With so many unpredictable factors, projecting health-care costs is a highly uncertain venture in comparison, for example, with public pension spending. Still, there have been some tentative attempts to project costs for health-care services.

The Office of the Auditor General of Canada predicts that health-care costs will rise from 6.6 percent of GDP in 1996 to 9.4 percent in 2031, conditional on an increase in real annual per capita health-care costs of one percent.54 Under the comparable assumption that health-care costs will be driven by increases in real wage rates, simulations using the Fougère and Mérette general equilibrium model show health-care costs rising to around nine percent of GDP by 2050, with most of the increases taking place by 2030. However, if costs increase at the rate observed over the last two decades, public health-care expenditures will rise to 13 percent of GDP. Robson also calculates that health-care spending as a share of GDP will rise significantly in Canada, that is, from six percent in 2000 to 10 percent in 2040. He notes, moreover, that the rise will be very unequal across the provinces, with the highest ratio in Newfoundland, at 20 percent, and ratios below the Canadian average for Ontario, Saskatchewan and Alberta.

The extent to which health-care expenditures may rise relative to the GDP is a challenge for all concerned. Hopefully, as suggested by the OECD, trends toward better health among the senior population will offset part of the pressures on overall health care and long-term care expenditures as a proportion of GDP.55 But what is worrisome is the fact that in Canada, as elsewhere, population aging has accounted for very little of the increase in health-care costs over the past three decades. As shown by Barer et al., per capita rates of health-care use by the elderly have increased significantly, but so far this has been driven by changes in patterns of health-care practices, not by changes in the number and age of the elderly in the population.56 The bottom line is that, as Bohn suggests, given that the cost of health care rises steeply with age, a significant increase in demand for health-care services is inevitable.57 Therefore, increasing health-care expenditures will just be a politically and socially desirable response to an aging population. The issue of the efficiency associated with this increase in healthcare expenditures is one on which more research is needed and whose outcome may depend on the collective willingness to make the necessary adjustments in the health-care system to meet the challenge of the changing population structure.

No doubt the rapidly growing ranks of older people will put upward pressure on government spending on pensions: Canada/Quebec pension plan (CPP/QPP) benefits, as well as Old Age Security (OAS), Guaranteed Income Supplement (GIS) and Spousal Allowance (SPA), in relation to GDP. This will begin in 2006, when the oldest of the baby boomers become eligible for early retirement CPP/QPP benefits, and accelerate in 2011, when this cohort reaches 65 years of age. In its 1998 report, the Office of the Auditor General predicted that population aging will push total pension spending from 5.4 percent of GDP in 1996 to about 8.4 percent in 2031, with two-thirds of that increase taking place in CPP/QPP benefits. Less optimistically, Fougère and Mérette report an increase of 2.3 percent of GDP for OAS+GIS+SPA alone, whereas King and Jackson report an increase of almost 1.5 percent just for the OAS program. Fortunately, to strengthen the financial viability of the CPP/QPP, public authorities have opted to increase the funding of the plans by raising contribution rates more rapidly than previously planned. In the long term, greater funding of the CPP/QPP allows for contribution rates around 10 percent rather than the 15 percent with no funding. Disney reports that because of that CPP/QPP reform, Canada is one of two countries out of 23 that can claim to expect negative net financial liabilities by 2030.58 In other words, from now until 2030 the CPP/QPP is on strong footing, as the present value of currently legislated contribution revenues is greater than the projected pension benefits.

The effects of population change on the costs of other government programs, particularly in the area of education, are estimated to be favourable, which will offset part of the population-induced increases in public pensions and health care. Fougère and Mérette estimate that education spending will decline by an equivalent of one percent of GDP in the next 50 years, while the other types of spending (including child tax benefits and employment insurance) will fall only modestly (by 0.3 percent).59 King and Jackson report similar results.60 However, it should be noted that no retrenchment in public education expenditures took place when the ranks of school-age youth (5-24) declined in the late 1970s and early 1980s.

Education and other program spending will likely only partially offset spending pressures from health care and public pensions. However, I will show next that Canada’s fiscal capacity to withstand the upcoming period of demographic change is secured by the implicit revenue provisions in the private tax-deferred pension programs. This would imply, as suggested by Denton and Spencer that the main challenge for public policy in Canada in the face of population aging may not be how to deal with an unavoidable increase in public spending relative to GDP, but how to deal with political and administrative reallocations.61

Here I express the view that the transition toward an aging population will not create a worrisome fiscal strain in Canada. Indeed, despite fiscal pressures on public pensions and health care, and even if our more optimistic growth scenario is not fully realized, Canadian governments will have access to revenues from an offsetting asset that will smooth, in a synchronized way, the fiscal effects of population aging. This offsetting asset, resulting from tax-deferred private pension plans (TDPPPs), will eventually enlarge the tax base and accommodate the rising expenditures in public pensions and in health care.

By private pension plans, I am referring to registered retirement savings plans (RRSPs) and employer-sponsored registered pension plans (RPPs). Employer-sponsored RPPs were introduced soon after Confederation and have expanded rapidly since the 1940s and 1950s. RRSPs were created later, in 1957, to allow non-participants in RPPs to receive the same advantages on savings for future retirement.62 Contributions to RRSPs only became really significant after 1970. These plans were established to stimulate private savings in order to ensure economic growth and financial security for the elderly. The incentive takes the form of a tax exemption on contributions and accrued interest. Canada’s programs are generous relative to comparable ones elsewhere. In 1999, contributions to RRSPs and RPPs were permitted up to a comprehensive limit of 18 percent of earned income for the preceding taxation year, to a maximum of $13,500.

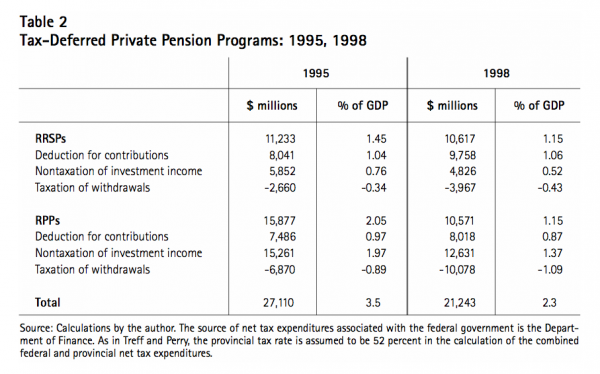

The amount invested in these programs has grown rapidly over the past 25 years. The accumulated contributions and accrued interests, that is the stock of private pension assets, has reached the astonishing size of over 100 percent of GDP. As contributions and accrued interests are tax exempted, these programs have represented a loss of tax revenue to the government. That loss has been only partially compensated for by the full taxation of the principal and interest of investors’ withdrawals. The net cost of the tax exemptions related to these programs constitutes what is called a net tax expenditure (NTEs). Tax expenditures are governmental financial assistance programs that operate through special tax concessions rather than direct government expenditures. For the Department of Finance, a tax concession is considered a tax expenditure if it can be delivered in an equivalent manner through program spending. If not, it is a tax reduction. The tax concession associated with private pension programs is called “net” tax expenditures because some components of the programs (contributions and earned interests) imply a loss of revenue, whereas the other component (withdrawals) is a source of revenue. According to Department of Finance estimates, in 1998 these federal NTEs only amounted to $13.9 billion or 1.5 percent of GDP.63 Under the usual assumption that the impact of tax-deferred private pension plans on provincial government revenues represents 52 percent of the corresponding impact at the federal level, provincial NTEs both RPPs and RRSPs totalled $7.2 billion or 0.8 percent of GDP in 1998.64 In other words, the estimated net revenue loss for Canadian governments associated with TDPPPs amounted to as much as 2.3 percent of GDP in 1998 (see Table 2). The latest year estimated by the official document is 1998. The Department of Finance estimates that NTEs were significantly greater before 1998 and will also return to higher levels after that year; i.e., 1998 tax expenditures were atypically low. The estimate for 1995 is more than $27 billion or 3.5 percent of GDP (Table 2). Note that the significant decline in interest rates is largely responsible for the decline in tax expenditures associated with investment income between 1995-98.

Despite the popularity of the programs and the large amount of money invested, evidence of the expected positive effect on savings is thin. Engen, Gale and Scholz have not found statistical evidence in such programs in the United States,65 nor have Ragan and Veal for Canada.66 It is as if investors were substituting tax-deferred for nontax-deferred forms of savings, rather than raising their saving rates. Still, the deferral of tax payments through these two programs nicely offsets the spending pressure arising from health care and public pensions during a demographic transition toward an aging population.

The offsetting effect (or the smoothing process), occurs because contributions and earned interest of these programs are tax deductible, while withdrawals are fully taxed, the net cost to the government depends on the composition of the population. An aging population means lower growth in tax-deferred contributions and accumulated assets. In contrast, taxable withdrawals will grow more rapidly. Thus the upcoming demographic trend toward an older population means significant reductions in the cost of these programs for the government. The programs may even become a net source of revenue. Nevertheless, if the principle is clear, the magnitude of the effect remains to be demonstrated.

The NTEs associated with private pension programs can be expected to decline for two reasons. First, the system is not yet mature, particularly the RRSP program. As mentioned earlier, investment in the RRSP program really started to become significant in the 1970s. In addition, contribution ceilings were raised a number of times, which stimulated individuals to accumulate more of their savings in RRSPs. The last modification was in 1990. For the coming years the Department of Finance predicts RPP contributions will be stable but RRSP contributions will continue to rise, which confirms the nonmaturity of the program.67 This nonmaturity implies that while contributions have grown substantially in recent years, the mirror effect on withdrawals will only show up in the coming years.

Second, the demographic structure of the population has been pushing up NTEs. The baby boom generation entered the labour force during the 1970s and 1980s, leading to a sharp increase in the proportion of the population that is of working age and to a rise in the number of contributors to private pension plans. The baby boomers are now in their 40s and 50s and more inclined to save the maximum for retirement. However, when they retire and gradually run down their retirement assets, the government will regain the lost revenue. As a result, the net government revenue loss will be attenuated when the program becomes mature and the demographic structure moves toward an older population.

The role of net tax expenditures associated with private pension programs has been too often neglected in debates regarding medium-and long-term fiscal planning. For instance, Robson and Scarth recommend an up-front debt reduction as the long-run fiscal plan for Canadian governments in order to make room for future expenditure pressures arising from population aging.68 However, they do not take into consideration the potential compensating effect of TDPPPs, which implies that both sides of the government’s balance sheet are not fully examined in their evaluation of the long-run fiscal plan.

Similarly, Oreopoulos and Vaillancourt execute generational accounting calculations to evaluate the intergenerational equity of the fiscal stance in Canada.69 Generational accountings examine the implications of the government’s long-run budget constraint for current and future generations. The long-run (or intertemporal) budget constraint imposes that present and future government expenditures (including interest payments on the debt) be financed by current and future taxes. Given projections of government expenditure, generational accounting calculates the current and future generations’ shares of the fiscal burden. Oreopoulos and Vaillancourt do not consider the existence of TDPPPs at all in their calculations. The outcome of their analysis is that current and future generations shared the fiscal burden equally as a result of the fiscal consolidation by Canadian governments in the second half of the 1990s. This implies that the inclusion of TDPPPs would result in a fiscal balance in favour of future generations. King and Jackson also do not include TDPPPs in their numerical analysis of the implications of population aging for public finances.70 Robson argues that a “seniors health grant” would be more equitable across generations as it would ensure that baby boomers contribute to the cost of their own health care in advance.71 But again, TDPPPs should be included in any equity balance calculations regarding current and future generations. Murphy and Wolfson are the first to recognize the role of TDPPPs in the fiscal balance.72 Fougère and Mérette were the first to simulate the fiscal balance effect of these programs in a general equilibrium framework, in two papers, “Economic Dynamics of Population Aging” and “Population Aging, Intergenerational Equity, and Growth.”

As their focus was on more general issues related to aging populations, Fougère and Mérette described the role of net tax expenditures in the simplest fashion. The contributions and interest income components were aggregated into one element, and the RPPs and RRSPs integrated into a single program. In the current paper, I build a partial equilibrium but detailed life-cycle model to investigate further the numerical projections of government NTEs associated with population aging. This model has the advantage of separating the two programs and of taking into account the three components associated with each of these programs, that is, deductions for contributions, nontaxation of investment income and taxation of withdrawals. Before discussing the results I obtain with this model, I will first introduce its salient methodological features.

The tax legislation requires full taxation of the principal and returns in tax-deferred private pension plans when either withdrawals or bequests occur.73 Accordingly, a budget constraint on each cohort in the model is imposed to ensure that all sheltered assets are taxed by the time an individual dies. RPP and RRSP contributions are assumed to be mature, meaning that individuals’ contributions increase over time at the growth rate of productivity. On the other hand, withdrawals are not considered to be mature. The full maturity of RPP and RRSP withdrawals is determined in the model by satisfaction of the budget constraint of each cohort. When the programs are fully mature, individuals’ withdrawals and assets also increase over time at the growth rate of productivity. The distribution of contributions and withdrawals across age groups in 1995, our benchmark year, is taken from survey data.74 The level of contributions and withdrawals across age groups for each plan is such that total amounts equal the corresponding estimated tax expenditures of the Department of Finance.75 To compensate for the lack of data on assets across age groups, the 1995 asset distribution is determined by ensuring consistency with the observed distribution of contributions and withdrawals. Withdrawals and assets after 1995 are determined by cohorts’ budget constraints. To ensure that tax expenditures are adjusted smoothly, full maturity of both programs is imposed for cohorts that enter adult life in 2022 or after. Since this is an accounting exercise, tax rates, rates of return, productivity growth per capita and the demographic structure are exogenous. In particular, the assumed growth rate of productivity per capita is one percent annually, which is compatible with, but does not depend on, the optimistic growth scenario developed earlier in the paper.

The long-term projection for real GDP, used here as a scaling variable, the rate of return on tax-deferred pension assets and the demographic trend are taken from the baseline scenario in Fougère and Mérette, meaning that the exogenous variables of this experiment are consistent with a general equilibrium framework built to investigate the economic effects of population aging.76 In “Economic Dynamics of Population Aging,” Fougère and Mérette use a neo-classical model, whereas in “Population Aging, Intergenerational Equity, and Growth,” the model features endogenous growth. It appears more prudent to use the long-term projections of the former paper in this experiment. The population aging simulation in “Economic Dynamics of Population Aging” suggests a real per capita GDP growth rate that is 0.2 percentage points lower than a scenario with no aging, over the period 1995 to 2050. The rate of return declines slowly in the first half of the period, but increases slightly thereafter. Finally, the demographic trend is consistent with the United Nations projection discussed in the introduction. In addition, I assume that the average marginal tax rate for withdrawals is five percent lower than for contributions, a conservative assumption.

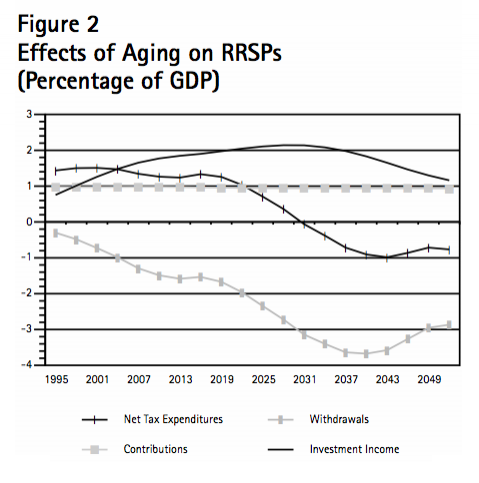

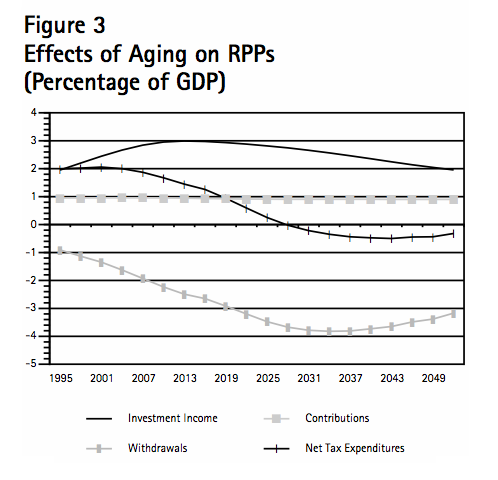

The model is simulated over the period 1995 to 2160. Figures 2 and 3 present the impact of aging on the components of tax expenditures for both RPPs and RRSPs and for the period 1995 to 2052. These figures present the revenue loss from deductions of contributions and tax exemption of accrued interest, as well as the revenue gains from the taxation of withdrawals. As shown, the revenue loss associated with the deduction for contributions remains modest and stable throughout the projection horizon. The impact of aging on contributions is small for two reasons. First, although the proportion of potential contributors (in effect, those between age 17 and 64) declines with population aging, the proportion of large contributors (those between age 41 and 55) grows substantially relative to the total population. Second, individual contributions are assumed to grow over time with productivity. In both programs, the tax expenditure associated with investment income is expected to increase and then decrease. The level will remain relatively high over the period covered. Withdrawal taxation will increase (decline in the figures) very rapidly to reach around close to four percent of GDP after 2030, which contrasts particularly with the behaviour of contributions. The sum of these three components gives the net tax expenditures, which remain positive for both programs but decline rapidly after 2010 for RPPs and after 2020 for RRSPs. Both become negative in the third decade of the this century. Overall the pattern of the three components is similar in the two plans as both faced the same demographic shock. But whereas NTEs for RRSPs decline later, they decline further than do those for RPPs. The differences in the patterns of the two plans are due to the nonmaturity of the RRSP plan.

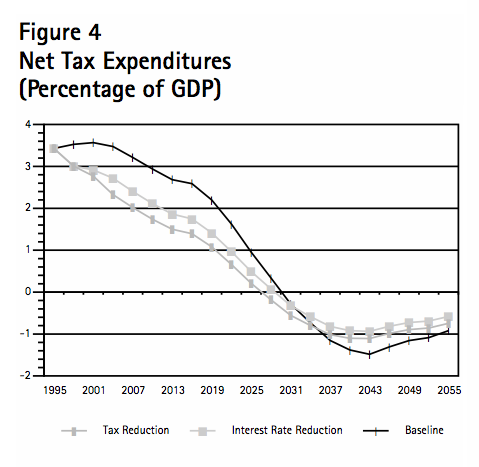

The total net tax of both programs is shown in Figure 4 as the baseline scenario. The figure shows that total net tax expenditures, which amounted to 3.5 percent of GDP in 1995, will become a net tax gain of close to two percent of GDP with population aging in 2040. For governments, this constitutes a total revenue increase of over five percent of GDP. I then assume two alternative scenarios (see Figure 4). I first consider the possibility that the decline in interest rates observed at the end of the 1990s persists over the entire period. In the simulation model, this implies that the interest rate remains lower by almost one-fifth than in the baseline scenario. This drop means a lower investment return on contributions to these plans and hence a lower tax expenditure on the investment income component. Along the transition period, this means that the net tax expenditure declines more rapidly in the short run but less rapidly in the long run. That is, the lowest point for net tax expenditure is higher than in the baseline scenario. Second, I add to the first alternative the personal income tax reductions planned by the federal government from now to 2004, assuming it will remain in place thereafter. In the simulation model, this takes the form of a five percent average marginal income tax reduction starting in 2001 and a 10 percent reduction starting in 2004. The tax reduction scenario strengthens the effects described in the interest rate reduction scenario. It does reduce the absolute value of the net tax expenditure, which means smaller losses for governments in the short run but also smaller benefits in the long run. Still, the simulations of the three different scenarios show that demography is the main factor driving the net tax expenditure associated with TDPPPs. Interest and tax rates will influence the size of the decline of the net tax expenditure but not its dynamic pattern.

Note also that if contributions were not increasing at the productivity growth rate because, for example, of the reluctance of the government to raise the current limit on RRSPs, the decline of net tax expenditures would speed up in the short run, but the size of the subsequent trough would also be reduced. Finally, it is worth noting that the difference in terms of GDP between 2000 and 2050 is enough to pay the implicit health-care liability calculated for the same period by Robson.77 Moreover, the increase in the implicit tax base is concentrated on those who will have contributed to the private pension plans. The rise in tax payments will thus be greater for individuals contributing larger amounts into RRSPs. Assuming that the tax revenue paid on the withdrawals made by these large contributors is recycled into healthcare expenditures and public pension benefits, we will witness an implicit redistribution of income from individuals with high incomes to those with lower incomes.

Thanks to the reversal in the tax expenditures of private pension plans, Canadian governments will have the fiscal room to meet the new expenditure requirements in health care and public pensions that go together with population aging. Moreover, keeping the debt-to-GDP ratio constant, governments may even have the room to reduce wage-income tax rates in the medium and long terms, raising the benefits of investing in human capital further as future after-tax wages increase.78 Thus for Canada the incentives to human capital investment and the subsequent positive effect on economic growth could be larger as a result of the positive effect on the fiscal balance arising from tax-deferred savings programs.

The smoothing fiscal role played by TDPPP against potential negative fiscal effects that accompany population aging, such as health care and public pension programs, is probably unique to Canada. The comprehensive limit on tax-assisted savings programs in the Unites States such as individual retirement accounts (IRAs) and 401(k) accounts is more restrictive. Moreover, such programs are uncommon in Europe. Only the United Kingdom and the Netherlands have private pension plans that have permitted the accumulation of a fund whose value is on the order of the Canada’s, but these plans allow tax deductions only on the return to the investment income. In other words, these programs do not offer tax deductions on contributions.79 In exchange, they do not tax withdrawals either.

Qualifying population aging as an impending crisis is overstated. While we cannot ignore the challenge it poses to public expenditures and economic growth, we should not forget that it also generates new opportunities. All modern economies have market and institutional mechanisms that respond to — and help offset — potentially negative trends. In this paper, I have dwelled on two such mechanisms that I expect will significantly mitigate the negative consequences of population aging for per capita income. The first is the likelihood that population aging in the countries that account for the majority of global GDP will result in an increase in wages relative to interest rates – which should promote an accumulation and deepening of human capital in younger cohorts in the years ahead. The second is the likely rise in labour force participation among individuals over the age of 55.

Contrary to pessimistic scenarios, these two factors combined may well result in no decline at all in the effective labour force over the next 50 years, and it is even conceivable that they will result in population aging enhancing rather than detracting from economic growth during that period. In addition, favourable technological change in response to a scarcer labour force overall, and moderate increases in immigration as necessary to sustain labour force growth, provide additional sources of optimism that demographic trends need not spell a declining level of well-being for most generations in the decades ahead.

In addition, from the point of view of its public finances, Canada is probably the best equipped among OECD countries to face population aging. The dynamics of tax-deferred retirement savings plans should substantially reduce the negative pressure of aging on Canadian public savings by encouraging the shifting of taxable income well into the future when tax revenues will be most needed.

Important policy issues with respect to population aging remain. However, this paper has shown they are not in the order of an inevitable growth slowdown or fiscal crisis, as is sometimes predicted. Rather, they concern the economy’s ability to adjust better to the anticipated changes, already identified in the literature, that will occur at a more micro level. Canadian governments will need to acquire the flexibility to reallocate, not only increase, spending in the long run. Young

generations may need encouragement to acquire human capital if they do not have the foresight to make these investments themselves — and in that light a high-quality education system may well be key to successfully dealing with population aging. Certain features of the Canadian system that discourage labour force participation among individuals nearing retirement age may need to be revisited. And the regional tensions that may be caused by populations aging at different speeds and intensities across the country need to be defused well ahead of time. But when all this is considered, the negative impact of aging on growth and public finances need not be severe — and we could even surprise ourselves with a strong performance as our society becomes older.

I would like to sincerely thank Maxime Fougère and Carole Vincent for their encouragement and helpful comments on an earlier draft of this paper. I would also like to express my gratitude to the two referees, J.C. Herbert Emery and William C. Scarth, whose substantial and insightful comments have improved this paper significantly. Warm thanks are also due to Daniel Schwanen and Francesca Worrall for useful editing and revision of the paper. All errors are mine.

Aglietta, Michel, Regis Breton, Jacky Fayolle, Michel Julliard, Cyrille Lacu, Bronka Rzepkowski and Vincent Touzé. “An Applied International Overlapping Generations Model.” Manuscript presented at the SME 2001 Conference, Klagenfurt, Austria, September 2001.

Auerbach, Alan J., Laurence J. Kotlikoff, Robert P. Hagemann and Nicoletti Giuseppe. “The Economic Dynamics of an Ageing Population: The Case of Four OECD Countries.” OECD Economic Review, no. 12 (Spring 1989): 97-130.

Baker, Michael, Jonathan Gruber and Kevin Mulligan. “Income Security Programs and the Retirement Decisions of Older Workers: Evidence From Canada.” Draft prepared for Human Resources Canada and Statistics Canada, 2000.

Barer, M.L., R.G. Evans and C. Hertzman. “Avalanche or Glacier?” Canadian Journal on Aging, Vol. 14, no. 2 (Summer 1995): 193-224.

Beaudry, Paul and David Green. “Cohort Patterns in Canadian Earnings: Assessing the Role of Skill Premia in Inequality Trends.” Working Paper no. 6132, NBER, Cambridge, Massachusetts, 1997.

Berger, M. C. “Changes in Labour Force Composition and Male Earnings: a Production Approach.” Journal of Human Resources, Vol. 17, no. 2 (Spring 1983): 177-196.

———-. “The Effect of Cohort Size on Earnings: A Re-Examination of the Evidence.” Journal of Political Economy, Vol. 93, no. 3 (June 1985): 561-573.

Bichot, Jacques. Retraites en Péril. Paris: Presses de sciences politiques, 1999.

Billings, B., J. Lawlis and W. Roth. “Population Aging: Basis Facts and Extension.” Applied Research Branch, HRDC, Quarterly Macroeconomic and Labour Market Review (Summer 1998): 19-29.

Bland, Roger C. “Psychiatry and the Burden of Mental Illness.” The Canadian Journal of Psychiatry, Vol. 43, no. 8 (October 1998): 801-809.

Bohn, Henning. “Will Social Security and Medicare Remain Viable as the US Population is Ageing?” Carnegie-Rochester Conference Series on Public Policy, Vol. 50, no. 1 (June 1999): 1-53.

Carrière, Yves. “Population Aging and Hospital Days: Will There Be a Problem?” In The Overselling of Population Aging, Apocalyptic Demography, Intergenerational Challenges, and Social Policy, eds. Ellen M. Gee and Gloria M. Gutman. Oxford: Oxford University Press, 2000.

Coile, Courtney and Jonathan Gruber. “Social Security and Retirement”, mimeo, MIT, 1999.