Canadian Policy Prescriptions for Dutch Disease

Robin Boadway, Serge Coulombe and Jean-François Tremblay

Canada’s tax system, if properly designed, could play a significant role in making the country’s economy more competitive and vibrant, and thereby contribute to Canada’s emergence as a “Northern Tiger.” This paper addresses the broad architecture of tax policy and offers concrete recommendations for policy action. Drawing on a large body of public finance and tax economics research, the proposals in this paper build on recent tax developments at both the federal and provincial levels.

Designs for an improved Canadian tax system should keep several goals in mind. They should create a competitive advantage for Canada within an increasingly integrated North American economy. They should minimize impediments to specialization, investment and trade, and reduce the effects of the border with the United States. They should create unique attractions to invest and to conduct business on the Canadian side of the border. And they should serve to nurture and retain skilled and talented workers in this country.

If the mix and structure of taxes are efficiently designed, the level of taxes in Canada will not hinder competitiveness. How much of national output to devote to public versus private consumption can then be decided without impeding economic performance. Yet considerations of business investment, skilled workers and trade flows do constrain the design of Canadian taxes relative to those in the US and elsewhere.

One way to promote efficiency and growth is to move toward taxes based on consumption, rather than on income. The priority should be to reduce taxes on personal savings, capital income and business investment without forgoing too much revenue or creating windfall gains for wealth holders. Consumption could be taxed through labour income and reformed tax bases for business. Moreover, a consumption base could be applied to direct personal and business taxes, and indirect sales taxes could be converted into more direct forms to reduce trade frictions.

For personal taxes, the highest priority is to shift further toward a consumption base, preferably by allowing tax-prepaid savings accounts alongside existing tax-deferred accounts and by removing the dollar ceiling on contributions to these. Other pressing needs for personal taxation reform include broadening the base, widening tax brackets (especially at the top) and implementing modest cuts in tax rates for the middle-income brackets of federal tax and the upper-income brackets of some provinces’ taxes.

With respect to payroll taxes, employment insurance (EI) premiums should be set at rates that finance actual program costs, and employers’ premiums should reflect each firm’s EI costs. A federal general payroll tax could be instituted to raise the revenues to finance other tax cuts and reforms; part of the financing of the Canada Pension Plan could also be shifted to such a payroll tax.

Either the federal or provincial sales tax should be converted into a more direct form (such as a business transfer tax) in order to reduce border costs. Alternatively, the goods and services tax (GST) should be simplified and reformed, and provincial sales taxes modified to reduce the burden on business inputs or harmonized with the GST. Excise taxes on gasoline offer an economically and environmentally attractive way to obtain more revenues in order to lessen the reliance on other, more distorting tax bases.

The most vital improvement in Canada’s tax design would be to reduce the burden of business taxes on investment. At the federal level, this should be achieved by eliminating capital taxes, making further small cuts in statutory corporate income tax rates and sharply accelerating depreciation provisions (and possibly shifting to a cash flow base). At the provincial level, the remaining corporate capital taxes should be phased out and corporate income tax rates reduced; alternatively, corporate and other taxes could be replaced with a business transfer tax.

Improved tax design would strengthen the economy, raise Canadians’ real, long-run living standards and increase the country’s policy autonomy. Given the vision and political will to create a world-beating tax system, Canada could become a uniquely attractive place for economic activity – a Northern Tiger.

At this stage, we think the emphasis in public debate on taxation needs to shift from tax reduction to tax reform. Our most serious competitive problem as a country no longer flows predominantly from the overall size of our tax burden, but from what we tax most heavily…What Canada must consider now is a fundamental shift of its tax structure from an income to a consumption base. (d’Aquino and Stewart-Patterson 2001, 307)

Recent federal and provincial budgets are remarkable for how well they have heeded the prescriptions of tax economists in academia, business and think tanks. Rarely have Canadian governments responded so faithfully to formal analysis of the need for a competitive tax system. Most analysts would say, however, that these moves are only the first instalment of needed tax policy changes. Even the finance minister, just days after the 2003 federal budget, announced that further personal tax cuts were a high priority.1 So how can future tax changes in Canada contribute to a more competitive and vibrant economy? What is the tax policy agenda for making Canada a “Northern Tiger”?

Economists assessing the tax requisites for a more productive and faster-growing Canadian economy increasingly favour greater reliance on consumption rather than on income bases.2 Some suggest that this goal be pursued via greater reliance on indirect forms of consumption taxation such as the goods and services tax (GST) or sales taxes.3 There have also been complaints, emanating more from business than from academic quarters, that Canada’s overall tax burden remains too high relative to that of its main trading partner, the United States.4 Yet, despite their frequent reference to the need to be “competitive” with the US economy, these analyses have not considered all the crucial dimensions of tax policy for Canada as an open economy with a dominant trading partner.

To become more competitive, Canada must pursue taxation and related public policies that will minimize impediments to specialization, investment and trade. Tax policies should complement other policies in pursuing further economic integration with the US in ways that reduce the effect of the border between the two countries.5 The parallel challenge is to create a competitive advantage for Canada within an increasingly integrated North American economy. Reducing border frictions is important, but so is creating unique attractions to situate and conduct business on the Canadian side and for skilled and talented people to work here. Tax policies can play a central role in this broader policy strategy, but the goal must not be simply to create a lower tax environment. More critical is to fashion a tax system that can efficiently generate the revenues to support the public services and infrastructure that will attract high-value-added business and workers and that will increase living standards for all Canadians.

This paper addresses the broad architecture of tax policy and offers concrete recommendations for future tax policy initiatives as part of a strategy to make the Canadian economy more competitive.6 I begin by reviewing recent tax policy achievements of the federal and provincial governments and assessing whether Canada’s overall level of taxation is an impediment to a competitive economy. I then examine the comparative tax mixes of Canada and the US and how far Canada needs to go to compete with US tax levels. Next, I examine the key economic issues in the design of tax policies: determining the best base for taxation, how best to implement the desired tax base and whether to rely more on direct or indirect taxes. Then, I apply the analysis to the major types of taxes (personal, payroll, sales and excise and business taxes) at both the federal and provincial levels, and I suggest directions for reform for each of the main tax areas. I conclude with thoughts on the tax strategy that Canada should pursue to become a Northern Tiger.

The tax cuts and reforms that Canadian governments have undertaken since 1998 should be seen in the context of the string of tax hikes that had taken place over the previous dozen years. At the federal level, these hikes included:

The provinces undertook many parallel tax hikes over this period, and several instituted new corporate capital taxes (including Alberta’s introduction of a financial institutions capital tax in 1990).

Most of these tax increases were driven purely by the revenue needs required to address uncontrolled deficits and, as a result, often neglected concerns for economic efficiency and long-run growth. Political considerations caused many of the tax hikes to be targeted disproportionately at higher-earning individual taxpayers and at business and corporate taxpayers — though even moderate earners were not entirely spared. When fiscal room began to emerge in the late 1990s, the first tax cuts focused on low-and moderate-income individuals and on relief for special groups such as the disabled, students and poor families with children.7 In recent years, more fiscal room has opened up, and tax policy has begun to pay proper attention to the neglected criteria — economic efficiency and long-run growth. These objectives remain paramount in designing a tax system for Canada as a nascent Northern Tiger.

The 2003 federal budget continued important tax policy thrusts introduced in federal and provincial government budgets since the late 1990s.8 Essentially, these policies have reduced tax burdens on capital and capital income and placed greater reliance on labour income, consumption bases and user fees. Ottawa has pursued these changes through both personal and corporate direct taxes and by moving the revenue mix from direct taxes toward indirect and payroll taxes. (As this paper shows later, taxing labour income is one way to implement a consumption tax.) These changes are consistent with the prescriptions of formal public finance analysis for making the tax system more economically efficient and growth oriented.

The fall 2000 budget update is often cited as the centrepiece of federal tax cuts. That document, however, represents just one step in a tax strategy that began in 1998, for personal taxes, with the elimination of the general and high-income surtaxes, followed by cuts in the rates for all incomes, the expansion of rate brackets and the restoration of full indexation. In 2000, the personal “income” tax was further shifted toward a consumption base by two cuts in the capital gains inclusion rate and, in 2003, by increased limits for contributions to tax-deferred savings plans (RRSPs and RPPs). The personal tax will move further toward a labour income base if the 2003 budget’s plans to consider tax-prepaid savings plans result in policy action.

The other major strand of federal tax policy has been to reduce the tax burden on corporate income and capital and to provide more uniform treatment across industries. Central to this change was the phased reduction of the federal basic corporate income tax rate for nonmanufacturing sectors to 21 percent, the same rate as for manufacturing firms. As a result of the 2003 budget, this corporate tax rate cut will be gradually extended to the resources sector over the next several years, the small business deduction for corporate tax will be raised over time from the current $200,000 to $300,000, following initiatives at the provincial level, and the federal capital tax on nonfinancial corporations will be phased out over several years, again following the actions of some provinces. These tax changes serve to reinforce the overall move away from capital income taxation.

Further reinforcing the shift of the overall base of the tax system toward labour income was the federal government’s decision to trim employment insurance (EI) premium rates so slowly as to generate ongoing large surpluses relative to program costs. These revenues have provided the fiscal means for larger personal and corporate rate cuts. Sharp phased hikes in premium rates for the Canada Pension Plan (CPP) from 1998 to 2003 have also increased the revenue shift toward labour income bases. Additional revenues to support the overall tax strategy have come from such policies as the 2001 budget’s hike in tobacco taxes and its imposition of the Air Travellers Security Charge (a user fee, which was reduced in the 2003 budget). Over the same period, moreover, the rate and coverage of the GST have remained unchanged, thus raising the relative revenue share of indirect consumption taxes.

Provincial tax changes since the late 1990s have pursued the same general goals as federal tax policies. Like the federal government, the provinces are shifting their overall revenue mix away from capital and capital income and toward labour income; in fact, they have led in important respects. Alberta is reducing its general corporate income tax rates, eventually to 8 percent. Ontario under the Progressive Conservatives was on a similar course, but its new Liberal government is backtracking — raising the corporate tax rate from 12.5 percent in 2003 to 14 percent in 2004 (instead of the 11 percent the previous government had planned). British Columbia has pledged to keep its general corporate rate competitive with that of the other major provinces, and has begun reductions accordingly. Quebec, whose corporate tax rate of 9.3 percent is the lowest of any province, has initiated sharp cuts in its generous tax expenditures for business.9 Several provinces have also reduced their corporate tax rates for small businesses. All provinces from Ontario westward already have small business deductions for corporate tax of at least $300,000 (the target now for federal policy); in the 2003 Ontario budget, the Eves Conservatives set a new target of $400,000, which the new government will also pursue.

Some provinces have eliminated their corporate capital taxes — Alberta abolished its tax on financial corporations in 2001 and British Columbia removed its general corporate capital tax in 2002. The 2003 Ontario budget pledged to eliminate, concurrently with similar action by Ottawa, the province’s nonfinancial corporate capital tax, but the new Liberal government has withdrawn that commitment. Quebec announced a multiyear plan to halve rates on both of its corporate capital taxes, but its new Liberal government is facing fiscal stringencies that have caused it to delay these cuts.

The four provinces with employer payroll taxes (including Ontario and Quebec) have left them intact, so that this source is generating a rising share of total provincial tax revenues. Some provinces have also shifted their revenues toward greater reliance on sales taxes and targeted them more directly at consumption. For example, British Columbia followed its large personal tax cuts in 2001 with a hike in its sales tax rate in 2002, and it reduced the taxation of business inputs. Saskatchewan paired its personal tax rate cuts with a major expansion in the coverage of its sales tax, but it included additional business inputs as well as many consumer items. The provinces have also increased their revenues from fees and user charges — hikes in medicare premiums by both Alberta and British Columbia are examples.

In 2001 the federal government allowed the provinces to shift from a “tax-on-tax” system to a “tax-on-income” system for their personal taxes.10 Most provinces responded by reducing their tax rates and flattening their rate structures. Most notably, Alberta moved to a flat rate of 10 percent above a much higher taxable income threshold. Saskatchewan and British Columbia have significantly lowered their top marginal rates of personal tax and partially flattened their rate schedules. Ontario has cut personal taxes sharply at low and middle incomes but continues to impose a steep surtax that keeps marginal rates on upper incomes high. The Conservative government had promised to reduce the number of taxpayers subject to surtax and had even referred to its ultimate abolition, but the new Liberal government has said it will not proceed with these items. Quebec has reduced personal tax rates but increased their progressive tilt. The province’s new Liberal government entered office committed to a further reduction of personal taxes by 27 percent, or $5 billion annually, over the next five years and to having personal tax rates competitive with those in Ontario within ten years (Parti Libéral du Québec 2003). As with corporate taxes, however, Quebec’s fiscal strains are delaying the start of these cuts as well, and Ontario’s change of government may make the goal itself less ambitious.

Since the provinces, apart from Quebec, use the federal definition of taxable income, they have also implicitly adopted the federal shift of the personal tax base toward consumption and labour income. In fact, Ontario was planning to reduce the capital gains inclusion rate for provincial tax purposes to 50 percent in 2000, and was negotiating with Ottawa over whether this would be permitted within the tax collection agreement, but this was pre-empted by the federal change. In 2000, Quebec also mirrored in its provincial income tax rules the federal reduction of capital gains inclusion rates.

To become a Northern Tiger, Canada requires a tax system that enhances its economy’s competitiveness, especially vis-à-vis that of the US. To determine the kind of tax system that will achieve this end, however, several questions must be addressed. First, does Canada’s overall level of taxes pose a handicap to the economy’s competitiveness? Second, how does Canada’s tax mix compare with that of the US? (I examine the comparative structures of each type of tax later in the paper.) And third, does it make sense for Canada to compete with the generally lower tax rates found in the US?

Some business and academic analysts have asserted that Canada’s higher overall tax burden relative to that of the US represents a competitive disadvantage. In assessing this claim, it is important to distinguish between the effects of taxation on real standards of living and on international competitiveness. Moreover, it is essential to include in real living standards both private consumption (after-tax and after-transfer real incomes) and public consumption (the value placed on publicly supplied goods and services). If Canada’s relatively higher tax burden is borne fully by households in the form of lower net incomes, then that burden affects neither businesses’ costs of production nor their competitive position internationally.11 Whether this scenario reduces or raises real living standards hinges on whether Canadians value the incremental increase in publicly supplied goods and services at less than or more than their loss of real disposable income.

If part of the higher tax burden is borne by businesses, it still will not reduce their international competitive position so long as there are additional public services or facilities (such as highways, medicare or better courts) that reduce their production costs or raise their productivity. Higher taxes could impair Canada’s trade competitiveness only if those taxes were borne in part by businesses and did not carry offsetting business benefits. Examples include pork-barrel regional spending, servicing public debt incurred for noncapital purposes or redistributive programs. Under this scenario, production costs would rise for Canadian producers, making them less competitive with US and other foreign producers, at least initially.

A tax-induced increase in Canadian production costs is not, however, the end of the story. The resulting decline in the current account balance would cause the Canadian dollar to depreciate, thus restoring the competitive position of Canadian businesses.12 According to standard trade theory, a country’s ability to gain from specialization and trade hinges on its comparative advantage in producing some products, not on its absolute productivity or lower production costs vis-à-vis those of its trading partners. Raising taxes in Canada above those in the US, even for “wasteful” purposes, should not harm exports. True, it would reduce Canadians’ real living standards (through lower net incomes, higher import prices and other means), but it would not affect the economy’s international competitiveness.

Although being an open economy per se should not affect Canada’s choice of tax level, integrated Canadian-US markets for capital and skilled labour and the high potential mobility of these factors of production will influence Canada’s optimal tax design. Canadian tax bases, structures and rates must be tailored to maximize the growth of investment, jobs, productivity and real wages. Particular care must be taken with respect to the taxation of capital income and the personal income of higher-skilled labour in Canada and to the efficiency costs of the total revenue system. As I show later, this point has important implications for the design of business taxes and for the progressivity of personal taxes.

The bottom line to this analysis is that Canada’s choice of tax level can be purely a matter of domestic priorities — whether the value of public services outweighs the cost of the associated taxes — not a matter of trade competitiveness.13 If part of Canada’s public spending is misdirected or wasteful, it should be curtailed and taxes reduced solely because of the harm this does to real living standards (private plus public consumption). Still, the chosen level of spending should be financed at the lowest efficiency cost. Thus, Canada should formulate its tax design to be more efficient than that of the US. In so doing, Canada can pursue the goal of a stronger and more competitive economy even if it chooses to devote more of its national output to public consumption through higher taxes than does the US.

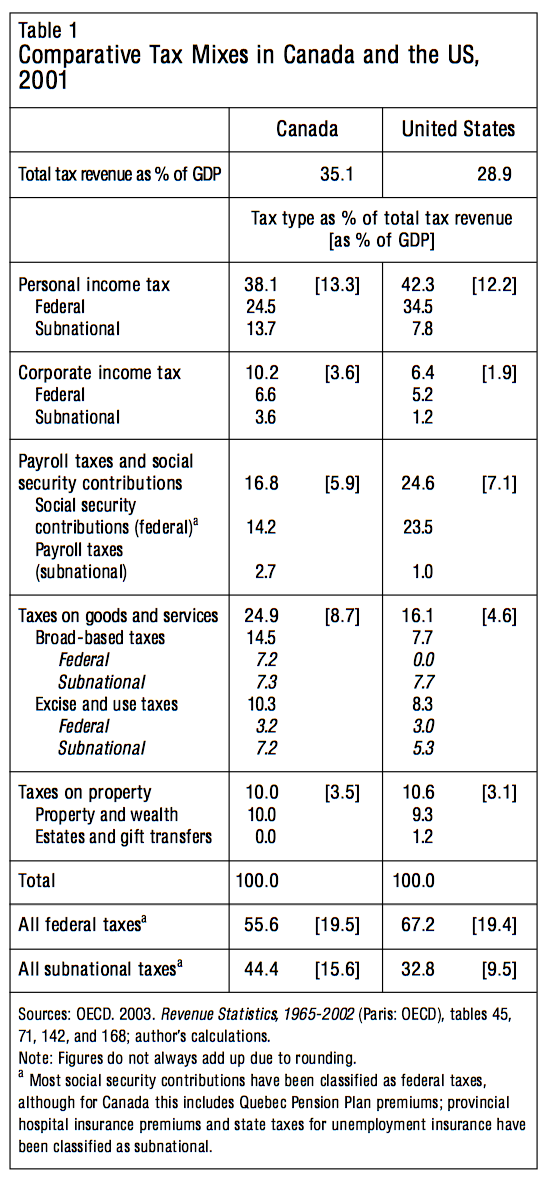

What is the relative overall level of taxes in Canada and the United States, and what are the comparative mixes of taxes in the two countries? Relative to its gross domestic product (GDP), Canada’s total tax burden was about 6 percentage points higher than that of the US in 2001, down from more than 9 percentage points in 1990 (see table 1).14 Significantly, these figures do not include “nontax revenues” of governments — items such as fines, user charges, most licence fees and royalty payments to government for the right to extract natural resources.15 Such royalties are more important in Canada, particularly in the resource-oriented western and Atlantic provinces, than they are in the US, and are an economically efficient way for Canadian governments to obtain revenues that allow them to reduce their need to apply distorting taxes.

More economically important is the mix of taxes the two countries use to finance government (table 1). In some basic respects, the two countries have quite similar tax mixes. Both rely heavily on personal taxes. As well, in both countries personal plus corporate income tax revenues jointly account for about half of total revenues, and property taxes account for about 10 percent of tax revenues. The most notable divergence is that Canada uses taxes on goods and services much more heavily than does the US, which, in turn, uses payroll taxes for social security much more heavily than does Canada. However, adding payroll taxes and goods and services taxes (both of which are ways to move toward taxing consumption) reveals that in 2001 each country collected about 40 percent of its revenues from these taxes jointly.

At a more detailed level, some differences between the two countries’ tax systems are noteworthy. At the federal level, personal taxes in Canada are significantly smaller than they are in the US (even as a percent of GDP). This is, however, offset by the personal taxes that Canadian provinces impose, which are much higher than those levied by US states and cities. Unlike in Canada, in the US cities and counties commonly impose sales taxes on top of state sales taxes, and some US cities also have a personal income tax. At the federal level, corporate income taxes were roughly comparable in the two countries in 2001, but at the subnational level they were about three times as large in Canada as in the US.

The US has no broad-based federal tax on goods and services like Canada’s GST. At the subnational level, both countries apply sales-type taxes (whether on value added or retail sales) to roughly the same degree. But because Canada also has a federal sales tax, its total relative reliance on broad-based taxation of goods and services is nearly twice that of the US. At the federal level, both countries apply comparable excise and use taxes, but at the subnational level, Canadian governments apply such taxes more heavily than do US governments. Comparative use of taxes on goods and services is of particular interest with respect to the issue of reducing border costs, as this might entail loosened border controls on the movement of commodities.

The US relies much more heavily on payroll taxes for social security than does Canada. However, US states have little counterpart to the general payroll taxes that four Canadian provinces apply, nominally to finance health care and education but in practice to supplement general revenues. These employer payroll taxes are an important source of revenues for Ontario, Quebec, Manitoba and Newfoundland and Labrador.

Finally, the two countries rely to a similar degree on taxes on real property and wealth. Canada has no counterpart to US governments’ use of estate, gift and inheritance taxes, but such taxes generate relatively little revenue and are scheduled to be reduced in future years.16 The bottom panel of table 1 shows that taxes for both countries are levied primarily at the federal level but that the federal share of total taxes is significantly larger in the US than in Canada, reflecting the provinces’ relatively larger spending responsibilities.

As explained above, Canada’s overall tax level need not be a competitive concern so long as both the mix and structure of taxes are efficient, but there are further reasons not to pursue blindly US tax levels. These reasons include the unsustainability of US tax levels, differing visions of society’s objectives and the economic returns to smartly focused public expenditures. A key reason is that US fiscal policy is on an unsustainable path that will require either sharp future tax rate hikes or severe spending cuts — either of which will be economically and socially costly.

According to the latest estimates by the US Congressional Budget Office (CBO), US federal deficits are projected to total US$1.9 trillion for 2005–14 (United States 2004, xii). Some independent experts, however, have asserted that the CBO figures seriously underestimate the real fiscal challenge, projecting total deficits on the order of US$4.4–US$9 trillion (Gale and Orszag 2004). They attribute this fiscal deterioration to declining revenues as a result of economic slowdown and the 2001 and 2003 tax cuts. They conclude that the US is on an “unsustainable fiscal path” once the longer-term implications of an aging population are factored in. The US fiscal problem will be further compounded by recent legislation to expand the scope of Medicare coverage to include prescription drugs. Even the normally staid Financial Times opined editorially about US federal policy: “On the management of fiscal policy, the lunatics are now in charge of the asylum…Watching the world’s economic superpower slowly destroy perhaps the world’s most enviable fiscal position is something to behold.”17

It would hardly be prudent for Canada to cut its tax rates to imitate US tax rates that, in the long run, are unsustainable and some of which are already slated to rise. US federal revenue in 2004 will be smaller as a share of GDP than at any time since the 1950s. US legislation specifies that many of the key tax cuts enacted in 2001 and 2003 will “sunset” in various years from 2005 through 2011, and it has been estimated that making the tax cuts permanent would reduce revenues by about US$2 trillion over the next decade (Gale and Orszag 2004). Moreover, state and local governments are also confronting fiscal difficulties.18 Addressing budget problems in the US will evidently require both spending reductions and revenue increases. While Canada faces similar long-run fiscal pressures, it is on a much better fiscal footing. Canada’s federal budget is currently in surplus and projected to remain so for the coming decades. Although the provinces are projected to run deficits over this period, mostly as a result of rising health care costs, fiscal surpluses are expected for all Canadian governments combined (Conference Board of Canada 2003).

Given the greater fiscal stresses in the US, the burden of servicing public debt will become greater there than in Canada. In 2001 all levels of Canadian government paid 5.6 percent of GDP in interest charges against 3.2 percent for US governments.19 This 2.4 percent differential accounts for two-fifths of the 6 percent of GDP differential in the tax burdens of the two countries in 2001. As the US federal government continues to rack up massive deficits, adding to cumulative debt, while the Canadian government maintains at least modest surpluses, this differential in interest costs will diminish and then reverse. Eventually, Canada will be able to reduce its tax burden to that of the US as a percentage of GDP without sacrificing the size of its program spending relative to the economy. Alternatively, Canadians may wish to take part of the dividends from declining debt-service charges in the form of more public benefits and services.

Yet another reason for Canada not to pursue US tax levels blindly is that Canadians and Americans often have a different vision for their societies. Many Canadians place greater weight on tolerance, diversity, equality, safe and vital city centres and civil society — all of which require supportive public services and infrastructure (see, for example, Adams 2003; Jedwab 2002, 2003). Hence, Canadians may choose higher tax burdens than do Americans — that is, less private consumption but more public consumption. Recent research on what determines success in the hightechnology and other knowledge-based sectors has focused on the role of vital urban environments in attracting talented workers; they care more about tolerance, diversity, “coolness” and cultural amenities than about tax burdens per se (Florida 2002a, 2002b). Therefore, higher tax burdens can have a significant economic payoff if the revenues are effectively channelled to creating those vital and attractive cities.

Cross-national evidence confirms the disconnect between overall tax levels and the competitiveness of an economy.20 In its latest survey of global competitiveness, the World Economic Forum (2003) ranked Finland, Sweden and Denmark first, third and fourth, respectively; the United States placed second. Yet the three Nordic countries have tax burdens that are 10 to 14 percentage points of GDP higher than Canada’s and are the three highest of all the 30 countries that are members of the Organisation for Economic Co-operation and Development (OECD). Their tax mixes put heavier weight on consumption-type taxes (value-added and payroll taxes) than those in Canada or the US; their personal taxes also apply relatively low flat rates to capital income alongside steep progressive rates on labour income. The lesson is not that high tax burdens per se create economic strength but, rather, that high tax burdens, if properly structured, need not be a hindrance to competitiveness.

Canada placed just sixteenth in the 2003 global competitiveness rankings, down several spots from the previous year. To account for its downgrade of Canada, the World Economic Forum cites issues such as distortive subsidies, favouritism in governmental decisions, bureaucratic red tape and foreign ownership restrictions. The remedies for these problems, however, are to be found in improved governance and regulation, not in tax policy. On the positive side, the competitiveness survey cites Canada’s budgetary surplus, sound banking system, generous paid maternity leaves, Internet access in schools and industry-university research collaboration. Most of these positive factors need to be supported by adequate fiscal resources, which makes the role of a well-structured, efficient tax system even more important.

The analysis of specific tax policies for Canada requires an understanding of some basic taxation principles. Most of the ensuing discussion draws on the research findings of economic theory and public finance and will be familiar to tax economists and tax policy specialists.21 Other readers will likely benefit from a review of this material, but those in a hurry to move on to the examination of specific tax policies in the next section — and those impatient with economic analysis — should be aware of at least the following key findings:

Transiting readers should also be aware of the wide divergence of efficiency costs related to different types of taxes. Economists use a concept called the “marginal efficiency cost” (MEC) to measure the extra loss of valued output per extra dollar of revenue generated by raising the rate on a given tax base. For example, an MEC of zero would indicate that a tax has no efficiency cost — it extracts the extra dollar of revenue without any economic distortions. An MEC of 0.10 would mean that 10 cents of real valued economic activity is destroyed in the process of raising the extra dollar. One study of the Canadian economy found the following MEC values for alternative taxes: 0.17 for a sales tax or a consumption base, 0.27 for a tax on payroll or labour income, 0.56 for a tax on personal income (labour plus capital income) and 1.55 for a tax on corporate income or capital income.22 Hence, taxing capital income is much more economically costly than taxing consumption or labour income.

By shifting its tax bases from capital income (at both the individual and corporate levels) toward consumption and/or labour income, a government can reduce the economic costs of raising any given amount of revenues. Using the MEC values cited above, one can illustrate the potential economic gains from a more efficient mix and structure of taxes in Canada. For example, assume that $50 billion of revenues (out of the total of more than $400 billion per year) is shifted from less efficient bases (such as capital income) to more efficient bases (such as consumption or labour income).23 The ongoing gain in the level of real consumable output would be in the range of $20 billion to $65 billion per year — a pure gain apart from any associated costs of implementation.24 Moreover, if simpler forms of tax were put in place in the process, further potential saving of administrative and compliance costs would be possible.

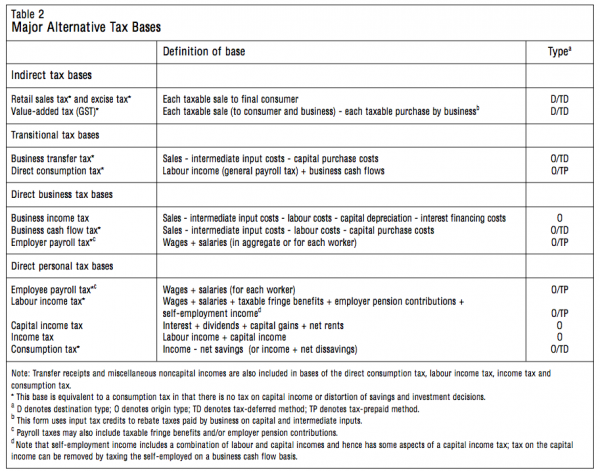

It is useful at this point to preview the alternative tax bases and their definitions; this discussion covers all the major taxes on flows of economic resources and ignores taxes on stocks of wealth (such as property taxes and corporate capital taxes). Table 2 groups the tax bases into three categories: indirect, direct and transitional. An indirect tax is one applied to the sale or purchase of goods and services and is applied on each transaction. Indirect taxes cannot be adjusted to reflect the taxpayer’s situation or tax-paying ability; they tend to be regressive, at least from an annual perspective on tax burdens. In contrast, direct taxes are imposed on businesses or individuals and can be adjusted to reflect their specific situation (through exemptions, deductions or credits) and their tax-paying ability (through progressive rate schedules). Some direct taxes, such as corporate income or payroll taxes, are nevertheless applied at flat rates.

The principal types of indirect tax include two single-stage forms: the retail sales tax, imposed only at the point of final sale to consumers, and the excise tax, typically imposed at the wholesale or distributor level. There is also a multistage form, the value-added tax, imposed at each stage of production and distribution of products but only on the value added at that stage. Canada’s GST applies the commonly used credit-invoice method of value-added taxation. There are two other ways to implement a value-added tax that are economically equivalent yet applied to the financial accounts of business (the business transfer tax) or to those accounts plus payments to labour (the direct consumption tax). These forms might be labelled “transitional” tax bases in that they are not imposed on the sale or purchase of goods and services per se but, like indirect taxes, they cannot reflect the circumstances or tax-paying ability of the consumer.

For direct taxes on business, the key distinction is whether to use an income base or a cash flow base. As can be seen in table 2, the difference between the two bases relates to the tax treatment of capital inputs by the firm. An income base reflects capital costs through an allowance for depreciation (“capital cost allowance” in Canadian tax jargon) over the life of the capital plus a deduction for interest costs in financing capital purchases. In contrast, a cash flow base allows an immediate deduction of the full capital purchase price (often called “expensing”) but no deduction for financing costs. Because of the time value of money to a firm, the expensing rather than depreciation of new capital makes a cash flow base more favourable to firms than an income base. The cash flow base has both operational and economic advantages. It avoids the complexity, inaccuracies and bookkeeping burdens of accounting for depreciation on diverse types of capital. And it avoids the economic distortion to firms’ investment decisions, as expensing fully shields the cost of capital (reflecting a normal return to capital) from tax.

Payroll taxes are direct forms of tax that can be applied to employers, employees or both. Most payroll taxes are imposed to finance specific social insurance programs, but they can also be imposed to collect general revenues. To the extent that a close link exists between the tax paid by (or on behalf of) the individual worker and his or her future benefit entitlements, a payroll tax can eliminate even the modest efficiency cost noted earlier for taxes on payroll or labour income. Payroll taxes are usually applied at flat rates but sometimes have annual exemptions and/or ceilings on the taxable earnings per worker. In most circumstances, the burden of a payroll tax falls fully or mostly on the worker regardless of whether the tax is nominally paid by the employer or by the employee. Although payroll taxes typically are applied to wages and salaries, the base can also include fringe benefits and employer pension contributions. In some cases, a parallel tax is applied to self-employment earnings to avoid a tax bias against employees.

Many jurisdictions prefer to make heavy use of direct personal taxes because their rates and provisions can be tailored to achieve both vertical and horizontal equity. The key distinction for direct taxes is whether their base is income or consumption. A tax on income applies to the full accruing returns to capital as well as to labour income and miscellaneous receipts (such as transfer payments). A tax on consumption — implemented through either a “tax-deferred” method that exempts savings or a “tax-prepaid” method that taxes labour income and exempts capital income — does not distort individuals’ choices about when in their lifetimes to consume. It also does not distort savings or investment decisions and does not insert a “tax wedge” between the gross and net rates of return on investment or savings (see Bradford 1988). Hence, any tax on capital income, such as that on an income base that includes both labour income and capital income, departs from consumption tax criteria.

Taxes can also be characterized by whether they are origin type or destination type, a distinction that is important for the freer movement of goods and services across borders at minimum cost to business and consumers. A destination-type tax is one applied in or by the jurisdiction where the ultimate consumer resides; for exports, this requires that the tax not be applied in the producing jurisdiction, but for imports, the tax must be collected at the border or in a manner closely related to each shipment. An origin-type tax is applied in the jurisdiction where the good or service is produced or where the productive factors are located and paid; this obviates the need for border controls or the taxing of the movement of goods and services. Only the retail sales tax, excise tax and value-added tax are destination type. All other transitional and direct taxes (both business and personal) are origin type.

There is growing consensus among tax economists that shifting tax bases away from income, particularly capital income, and toward consumption and labour income would yield significant benefits. It would improve the lifetime horizontally equitable treatment of households with different savings preferences — that is, individuals with the same lifetime labour earnings would pay the same total discounted taxes despite differing choices about when to consume. Shifting tax bases toward consumption and labour income would also improve incentives for savings, and to the extent that savings did increase, it would promote long-run growth of both the economy and living standards. Even if aggregate savings were not affected, such a shift would improve the efficiency of resource allocation over time, thereby raising real living standards.25 Total savings would be allocated to different types of capital formation (such as business investment versus housing) on a more neutral basis. Additional benefits would arise from simpler record keeping and tax reporting and potentially from reduced opportunities for tax avoidance and evasion using complex investment schemes.

In shifting tax bases, several possible problems would need to be considered in designing the new taxes. For example, without proper formulation, the vertical equity of the tax system could be unduly compromised. Total revenues might also be reduced unless they were offset elsewhere in the tax system. In particular, revenues might be lost in the form of windfall gains to holders of “old” capital at the time the transition took place without any concomitant incentives for incremental savings. Since the largest holders of capital have high incomes, this issue also relates to the preservation of vertical equity. In addition, it would be important in shifting tax bases to avoid creating new kinds of opportunities for tax avoidance and undue burdens on households and businesses. And any such reform would also have to be coordinated with the tax systems of other countries, principally the US.

There are two ways to implement a consumption-based personal tax. One way is the “tax-deferred” or “registered-assets” method, which permits a deduction from the taxpayer’s income of savings in the form of contributions to trusteed plans. In effect, this method provides for the deferral of tax on both the principal amount saved and the accruing investment returns to such savings; when the funds are withdrawn for consumption, they become taxable. RPPs and RRSPs embody the tax-deferred method within the direct personal tax. If all limits were removed from contributions to tax-deferred plans, the scheme would become a “personal consumption tax,” which could retain tax rate progressivity of any desired degree. Indirect sales taxes on consumption also embody the tax-deferred method, as no sales tax is paid on earnings until they are spent, but they tend to be regressive in practice.

The second way to implement a consumption-based tax is through the “tax-prepaid” method, sometimes called a “labour income” or “wage” tax. Rather than working with the “uses” of income (consumption versus savings) as in the tax-deferred method, the tax-prepaid method considers the “sources” of income. Labour income is taxable but capital income is exempted from tax; the capital income simply reflects the return to savings. A tax-prepaid personal consumption tax would be a progressive tax on labour and other noncapital incomes. A partial move in this direction would require the establishment of tax-prepaid savings plans with limits on the contribution amounts. The tax-prepayment principle is already manifested in the tax-free treatment of gains on owner-occupied housing, the preferential tax inclusion rate on other capital gains and the tax treatment of some insurance products.

A simple numerical example can be used to illustrate the equivalence of the tax-deferred and tax-prepaid methods. Assume that the marginal tax rate is the same in two periods, t, and that all savings yield a rate of return equal to the rate used to discount future values, r. Person A earns an extra dollar, which he immediately spends, with the result that it is taxed as part of current consumption and incurs tax of t. Person B similarly earns an extra dollar, but she saves it for consumption in the next period. There is no consumption tax due in the first period, but the dollar grows to 1 + r in the second period, when it is spent, incurring tax of t(1 + r). However, discounting that tax back to its value in the first period yields a present value of t(1 + r)/(1 + r) = t, the same as the tax that person A paid. Alternatively, if the tax is applied to labour income rather than consumption, both individuals would pay the same tax of t in the first period, again independent of when they chose to spend the earnings.

Both the tax-deferred and tax-prepaid methods are economically equivalent under particular conditions. That is, they yield the same present value for a person’s lifetime stream of consumption irrespective of choices made about when to save and consume, so the tax does not distort either consumer or investment choices. The net rate of return to an individual saver is then equal to the gross rate of return on the tangible real investment, which promotes the economy’s allocative efficiency and growth potential. However, if there are departures from either of the stated conditions — that the rate of return on all assets equals the rate used for discounting future values, and that the individual’s marginal tax rate is identical when saving and consuming — then the two methods are no longer equivalent, with possible consequences for equity and efficiency (see Kesselman and Poschmann 2001).

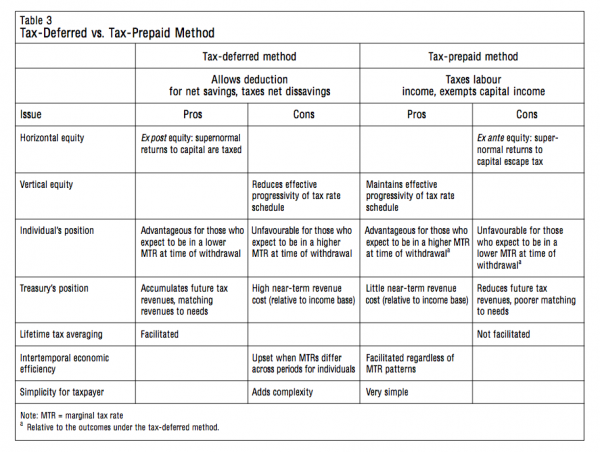

When rates of return or marginal tax rates depart from these assumptions, the tax-deferred and tax-prepaid methods will have different effects, as shown in table 3. If some assets have rates of return that differ from that used to discount future consumption, the two methods give rise to differing concepts of horizontal equity — the equal taxation of people with the same level of economic resources. The tax-deferred method displays ex post equity in that assets yielding above-average returns are taxed on their supernormal returns (a consumption-based tax exempts the normal return to capital). With the tax-prepaid method, there is ex ante equity, which means that taxpayers are treated equally only in the sense that they do not know beforehand which assets will prove to yield high rates of return. The supernormal returns that accrue to some assets will escape tax under the tax-prepaid method.26

Table 3 also shows, under “individual’s position,” which method is advantageous or unfavourable depending on the divergence of marginal tax rates (MTRs) between the points of saving and consumption. With the tax-deferred method, there is a gain to the individual whose MTR declines between saving and the withdrawal of funds for consumption. Conversely, tax deferral penalizes those whose MTRs rise between the time they save and the time they consume. In contrast, under the tax-prepaid method, changes in MTRs have no impact on the net returns to saving for later consumption, making this method more advantageous than tax deferral for those with rising MTRs and unfavourable for those with declining MTRs. These differing attributes also mean that the two methods can be combined usefully within a personal tax. Tax deferral allows individuals to undertake lifetime averaging of their tax burden in a system with progressive annual tax rates; tax prepayment affords “intertemporal” economic efficiency in choices about when to save and when to spend.

Additional attributes of the two tax methods are summarized in table 3. In terms of vertical equity, tax deferral reduces the effective rate progressivity of the personal tax because savings are deductible at the individual’s MTR. Tax prepayment, in contrast, does not allow for the deduction of amounts saved, and hence treats savers in different tax brackets in a more uniform manner, thus preserving greater effective progressivity of annual tax burdens. Another way of viewing this difference is that tax deferral offers a form of lifetime averaging of taxes. It is also much simpler for taxpayers to comply with tax prepayment than with tax deferral, since only the latter method requires complex calculations and forecasts about future income for the individual to decide when to make tax claims or when to withdraw funds.

From the treasury’s position, the tax-deferred method entails large current revenue costs because of the tax deductibility of savings. These costs may grow for an extended period as the middle-aged population increases, but eventually they will reverse as individuals retire and withdraw their tax-sheltered savings. The deferral of tax means that additional revenues will be generated in the future, which, in Canada’s case, could be helpful for financing public pension and health care needs when the large population of baby boomers retires (see Mérette 2002). In contrast, the tax-prepaid method entails revenue costs that are small at the outset but grow over time and are not reversed when savers retire and spend their savings. Hence, tax prepayment may aggravate future revenue problems when the baby boomers retire, unless budgetary surpluses are generated in advance.

Another issue arises when there is a shift between the two methods of taxing consumption. Although the two methods are equivalent for individuals who live their entire lives under them, they are not the same if applied to individuals at different stages of their lives. To illustrate this point, suppose the tax-deferred method is applied through an indirect sales tax and the tax-prepaid method through an employee payroll tax. Clearly, a shift from a sales tax to a payroll tax would favour retirees and those late in their working lives, since most of their lifetime labour earnings would escape the payroll tax, but it would be unfavourable to those who were young or early in their working lives. Conversely, a shift from a payroll tax to a sales tax would favour younger workers while penalizing older workers and retirees (who would have already paid payroll tax on most of their earnings and who would pay again, in sales taxes, when they spent their lifetime savings). This point suggests that policy should avoid sharp shifts between the two methods of taxing consumption and that it may be desirable to use a balanced mix of the two.

Both methods of consumption taxation have been recommended in previous tax reform proposals. In the US, the tax-deferred method was endorsed by Senators Sam Nunn and Peter Domenici in their proposed USA (unlimited savings allowance) tax (Boskin 1996); in Canada, it was supported in the Fraser Institute’s 1994 proposals for replacing the GST with a “personal consumption tax” that could retain a progressive tax rate schedule (Walker 1994). The tax-prepaid method was elaborated in the US in the Hall-Rabushka (1985) flat tax plan, promoted by congressman Dick Armey and presidential candidate Steve Forbes. The Hall-Rabushka scheme is a combination of a personal tax that exempts financial capital returns and a business tax based on cash flow (this is the business counterpart to consumption for households). In Canada, the former Reform Party favourably assessed a scheme of this kind but did not endorse it as official policy. A variant of the Hall-Rabushka scheme, Bradford’s “X-tax” (1986) combines progressive personal tax rates and a flat business tax rate imposed at the top rate of personal tax.

Major problems arise with the full implementation of a consumption-based tax. A central problem is how to handle capital or savings that were already accumulated at the time of transition. Under the tax-deferred method, such pre-existing wealth taken from undocumented sources could be contributed to registered savings plans as “new” savings, thus sharply reducing the tax liabilities of high-wealth holders for many years. Under the tax-prepaid method, preexisting wealth could be used to finance personal consumption without incurring any direct taxes. To prevent this revenue loss during the transition, it would be necessary to establish comprehensive accounting of all initial wealth holdings to ensure they were not being used for tax avoidance. The difficulty of achieving such a goal, however, means that substantially higher marginal tax rates would need to be applied to taxable consumption and labour earnings, which would undermine the efficiency gains of the reform. This kind of tax avoidance would also sharply reduce effective tax progressivity because of the high concentration of wealth that is in the form of neither registered savings nor home equity.

One way to control opportunities for avoidance, reduce potential revenue losses and focus the incentives on incremental savings is to implement a consumption-based personal tax only partially, rather than fully. For example, annual contributions to registered savings plans — whether tax deferred or tax prepaid — can be limited as a percentage of current labour earnings. This approach is used in the current Canadian RPP and RRSP schemes, which have both a percentage limit and an annual dollar limit, with liberal provisions for the carry-over of unused contribution amounts. Two other methods of applying the tax-prepaid approach are annual exemptions on given amounts of financial income and partial exclusion of realized capital gains from personal tax.

Partial implementation methods do, however, have some limitations. One is that they restrict the forms of savings that qualify for consumption treatment. With registered plans and an annual financial income exclusion, the holding of marketable financial securities is favoured relative to kinds of savings that do not qualify (for example, tangible assets, real estate and business assets other than those that are publicly traded). In addition, partial exclusion of capital gains is further biased toward equities, especially growth equities, relative to holdings of debt and dividend-paying equities, though the latter is partially mitigated in Canada by the dividend tax credit.27 The tax-prepaid method is equivalent to a zero tax on capital gains — which some analysts (for example, Grubel 2003a) have backed — but it also offers neutral treatment of interest and dividend incomes. Moreover, tax-prepayment with limits on annual contributions avoids some of the most severe problems of eliminating taxes on all capital gains, including large and economically inefficient revenue losses, windfall gains to the wealthy and a sharp reduction in personal tax progressivity.

The business tax counterpart to a consumption base for households is a cash flow base. Economists regard a business cash flow base as economically efficient and neutral for real investment decisions.28 Such a base further simplifies tax accounting by eliminating the need for depreciation accounting, as all capital purchases can be fully expensed (and there are no deductions for financing costs). Indeed, the business component of the Hall-Rabushka plan embodies cash flow taxation. However, because the cash flow base exempts the normal return to capital, it reduces corporate tax revenues and these would need to be replaced elsewhere. A cash flow base also leads to difficult transition problems for firms with high debt loads, since their interest financing costs would no longer be deductible. Most of these difficulties could be avoided by allowing highly accelerated depreciation, or full expensing, only for new capital investment.

The choice of whether to apply a tax directly or indirectly pertains mostly to consumption-based taxes, for which there are both direct and indirect forms, but it raises similar issues in comparing an indirect consumption tax with various forms of direct personal and business taxes. The first consideration is that an indirect tax is of limited use because its operation prevents adjusting rates based on the taxpayer’s ability to pay or on other attributes such as family size or health status. For this reason, an indirect tax is suitable only as a supplementary means of collecting revenues where substantial use is made of direct taxes on households. An indirect tax’s lack of discriminatory power often leads to the use of compensatory provisions such as income-tested refundable tax credits for lower-income households.

Second, it has been argued that diversifying tax collection between direct and indirect methods reduces the potential for tax avoidance and evasion. Spreading taxes over multiple bases and collection points reduces the incentive to cheat on any one tax, it is claimed, and increases the cost of cheating on multiple taxes. Yet this argument is easily overstated, in that a business that cheats on its collection or remittance of GST will consistently misreport its gross revenues and costs on its income tax return. If it did not, an audit for one of the taxes would reveal that the other tax had not been properly reported. Hence, multiplicity of tax bases and collection points does not necessarily improve the tax authorities’ detection powers, but it typically increases their administrative costs and taxpayers’ compliance costs.

Third is an aspect of tax collection and enforcement of particular salience for Canada in choosing between direct and indirect tax formats. As noted above, an indirect tax is applied on a “destination” basis, whereby the tax is levied, paid and collected in the jurisdiction in which the final consumer of the good or service resides. In contrast, a direct tax is applied on the basis of the “origin” of the income used to purchase the good or service, and it is levied by the jurisdiction in which that income is generated and in which the factor owner resides. Hence, an indirect tax requires the means to collect taxes on purchases that individuals make across the border and consume at home — typically through controls on commercial and private purchases of goods shipped or carried across the border.

Canadian tax design must heed the last point in particular if the goal is to increase the country’s competitiveness. Existing border controls to enforce the GST and provincial sales taxes impose large real burdens on businesses, individuals and governments. These burdens include customs officers, brokerage and Canada Post import fees, shippers’ costs of preparing export documentation and higher courier and postage fees for shipments between Canada and the US than for shipments within either country. On top of these tangible costs are the time costs imposed on truckers and individuals queued at the border and on Canadian businesses waiting for the delivery of needed materials, parts and supplies.29 All these items are added to the costs of doing business in Canada, perhaps rivalling the costs of having a separate currency, which have been much-discussed in the dollarization debate.

Any plan to spur Canadian economic growth should thus seek to minimize border costs. Canada might also contemplate an eventual customs union with the US, whereby trade between the two countries is tariff free and both apply common tariff rates to trade with other countries. Such an arrangement would allow Canadian producers to operate in the North American market with as little friction to doing business as US firms experience. Gains to Canadians’ real living standards also might result from reducing the use of Canada-specific distributors for many products.30 However, present sales-type taxes, with total rates averaging about 15 percent for all provinces except Alberta, are roughly double their US counterparts, a tax differential that is a major barrier to relaxing border controls on trade. Hence, Canada should consider reducing total indirect taxes toward the average US level, which would entail changing the form of federal and provincial sales taxes.31

In switching from a destination-type indirect tax to an origin-type direct tax, two notable effects would arise. First, Canadian residents would be taxed on their consumption abroad, to the extent that it was financed out of domestic earnings. Unless the direct tax effectively captured their foreign earnings, Canadians might in part escape taxes here. Second, switching to an origin-type tax would raise domestic production costs; however, as explained earlier in the discussion of tax levels, an automatic adjustment of the exchange rate would offset this effect. With flexible exchange rates, domestic autonomy over tax rates would be preserved even with more relaxed border controls on trade.

One might question whether Canada’s direct tax system could bear heavier usage if indirect taxes needed to be reduced to minimize border costs. This approach might appear to run counter to the advice of Bev Dahlby:

We should levy both direct and indirect consumption taxes because they are subject to different forms of tax evasion and avoidance… Therefore, it is preferable to have two systems of consumption taxation, each levied at a moderate rate, rather than have one consumption tax system levied at the full rate. (2003, 100–01)

Dahlby cites two types of cross-border tax evasion: underreporting of foreign earnings for a direct tax, levied on a residence basis; and cross-border shopping with respect to an indirect tax, levied on a destination basis. Relaxed border controls on the movement of goods would make the latter type of evasion easier without changing the ease of the former type. Hence, it would dictate some shift of the tax mix away from indirect and toward direct taxes. Indeed, only a full common market, in which average workers could readily obtain US earnings, would also ease the former type of evasion and thus tilt the balance toward indirect taxes.

The analysis of provincial taxes differs from that of federal taxes in two important respects. First, at the national level, any differential tax burden will be accommodated through an exchange-rate adjustment to restore trade competitiveness; this process occurs regardless of whether the taxes provide good value for households and businesses. In contrast, any province that raises its tax burden without providing fully valued public goods and services for households and businesses will impede the ability of firms in that province to compete both nationally and internationally. There is no adjustment counterpart at the provincial level to the exchange rate for the national economy.32 Consequently, the provinces face more severe market constraints than does the federal government on their ability to overtax relative to the value of public expenditures.

The second factor that differentiates provincial and federal tax policy is the greater mobility of labour within the country than internationally. Such mobility arises across the skills spectrum but is greatest at the highest levels. As a result, a province must not only provide public goods and services that all tax-payers fully value; it must also do so with respect to the taxes high earners pay and the services they enjoy. Otherwise, some of them will leave the province, thus raising the gross pay for those occupations and shifting the burden of more progressive taxes onto employers. Evidence from US states suggests that this mobility process prevents them from pursuing much redistribution through the tax system (Feldstein and Wrobel 1998). Accordingly, the provinces may be more constrained than the federal government in their ability to use tax and spending policies for redistributive purposes.33

Personal taxes are the largest component of the Canadian revenue system at both the federal and provincial levels, making them critical in any tax design. My analysis begins by assessing the Canadian personal tax base and comparing it with the US base. This leads to proposals for both expanding and reforming the base — including, most importantly, further moves toward a consumption base. I then examine personal tax rates in Canada as well as the top tax rates on various types of income, and compare them at both the federal and sub-national levels with those in the US. This provides a basis for assessing the most economically beneficial ways to modify the personal tax rate structure at both the federal and provincial levels.

In its efforts to become a Northern Tiger, Canada should seek to implement the broadest, most efficient base for personal taxes, with due regard for horizontal equity. For both Canada and the US, the personal income tax is by far the largest source of tax revenues at the federal level. Fortunately, Canada enjoys some advantages by not replicating several leakages found in the US tax base. One of these is the deductibility of mortgage interest, which moves the US base away from consumption, favours current spending and biases savings toward investment in home equity at the expense of business investment.34 In the 2000 tax year, itemized deductions for mortgage interest totalled US$300 billion, or about 7 percent of total US adjusted gross income. Another leakage in the US tax base is the federal deductibility of state and local income taxes, real estate taxes and personal property taxes, which in the 2000 tax year shrank the tax base by a further US$295 billion, or another 7 percent.35

A third type of personal tax base erosion in the US arises through the tax-free treatment of interest on state and municipal bonds (“munis”).36 As of late 2002, the total volume of munis outstanding was US$1.76 trillion, of which about 70 percent was held by individuals (either directly or through funds).37 At a tax-equivalent interest rate of 4.5 percent (almost all munis are long term), this treatment removes more than US$55 billion from the tax base of upper-bracket US taxpayers. Tax-free treatment is an inefficient method for making intergovernmental transfers. It also reduces the progressivity of the tax system and encourages excessive spending by governments that have access to cheap financing. For these reasons, Ontario’s issuance of tax-free Opportunity Bonds in 2003 is a troubling Canadian precedent, one that other jurisdictions should eschew.38

Although the deductions and exclusions available in the US lessen effective tax burdens, they do so in a way that is economically inefficient. They necessitate marginal tax rates that are higher than would otherwise be needed to generate the same total tax revenues. These higher MTRs carry larger efficiency costs than necessary by distorting taxpayer choices with respect to work, saving and investment.39 Hence, by avoiding such base-eroding tax deductions, Canada can either raise the same relative revenues as the US with lower MTRs and lesser economic distortion or raise greater revenues than the US with comparable MTRs and economic distortion — either way, a useful competitive advantage.

Canada’s personal tax base is broader than that of the US, but it still has some areas in which efficiency and horizontal equity could be improved.40 The most notable of these areas is the omission of employer-paid health and dental insurance benefits as a taxable fringe benefit for employees. This omission reduces the tax base while causing inefficient overprovision of such coverage relative to taxable compensation. It also penalizes disproportionately workers at lower earnings levels, who have little or no such coverage. Another example is strike pay, which is nontaxable, while the union dues that finance it are tax deductible, an arrangement that is inconsistent and encourages more and longer work disruptions. Moreover, some transfer payments to individuals are nontaxable, which may make sense for income-tested transfers, where taxability would exacerbate work disincentives, but transfers such as workers’ compensation benefits should be taxable just as are employee compensation and unemployment benefits.

To improve efficiency, growth and competitiveness with the US, however, the most critical change that could be made to Canada’s personal tax base is a further shift toward consumption. Currently, high earners in Canada can take advantage of only about one-third of the tax-recognized savings of their US counterparts, which raises their relative tax burdens and distorts their savings behaviour. The 2003 federal budget’s proposed phased hikes in the dollar ceiling for RPP and RRSP contributions from $13,500 to $18,000 over several years is long overdue, but it does not go far enough. Any dollar ceiling on contributions eliminates the efficiency gains for individuals who are constrained by that ceiling; for them, it is like a lump-sum tax reduction with no marginal incentives to save. Moreover, there is no reason to keep high earners from undertaking lifetime savings on the same consumption-tax basis as low and middle earners.

Maintaining the link between contributions and labour earnings is an effective way both to limit consumption treatment to lifecycle savings and to prevent the large revenue loss of a full consumption tax base. The existing 18 percent rate is adequate for those not constrained by the dollar limit, given the ability to carry forward unused contribution amounts — a point confirmed by the fact that very few of those individuals actually contribute their full allowance. However, along with eliminating the dollar ceiling on contributions, it might be sensible to apply a lower rate (such as 15 percent) for allowable contributions on earnings above $100,000 per year. Such a change would reflect the progressivity of the tax rate schedule, the application of the percentage limit to gross earnings and the need for retirement savings to replace only part of net earnings.41

Further moves toward a Canadian personal consumption tax will invoke the choice between tax-deferred and tax-prepaid methods. The 2003 federal budget announced plans to consult on the possible adoption of tax-prepaid savings plans (Canada 2003a, 341–42). In fact, several considerations support the expansion of access to tax-recognized savings along tax-prepaid, rather than tax-deferred, lines (Kesselman and Poschmann 2001). These include lower immediate revenue costs, greater economic efficiency, less sacrifice of vertical equity, and greater benefits for low-income earners whose higher MTRs in retirement make tax-deferred savings unattractive. Yet another virtue of the tax-prepaid approach is that high earners would not be tempted to emigrate to skirt their tax-deferred liabilities on dissaving; at present, after emigrating, such earners can reduce their tax on withdrawals from tax-deferred plans by taking advantage of low nonresident tax-withholding rates. Still another incentive for Canada to move toward treating tax-recognized savings along tax-prepaid lines is that the US administration has proposed converting existing tax-deferred Individual Retirement Accounts to tax-prepaid schemes.42

In addition to instituting new TPSPs that are integrated with existing tax-deferred savings plans, Canada could usefully reinstate annual exemptions on a limited amount of interest and dividend income. Prior to the tax reforms of the late 1980s, individuals could exempt $1,000 of such income each year; an appropriate contemporary figure would be about $2,000 per year. This provision would allow for consumption-type treatment of small amounts of savings without the need for formal registration of plans or record keeping of contributions. An exemption method would not be a suitable substitute for much larger TPSPs, however, since the exemption can be used for pre-existing savings, and access to it cannot be readily linked to labour earnings. A fixed exemption for interest and dividends would also encourage families to accumulate a modest rainy-day fund outside their registered savings to help tide them over emergencies or jobless spells.

As part of the move toward a consumption tax base, changes to the rules for interest deductibility would be appropriate. Current rules require tracing borrowed funds to specific financial assets to block deductions on homeowner or consumer loans; interest cannot be deducted on loans to finance RRSP contributions; and Finance Canada has proposed barring deductions for interest to finance equities oriented to capital gains rather than to dividends. An attractive way to reform these rules would be to limit the tax-payer’s annual interest deductions to total income from interest, dividends and taxable capital gains. Any excess amount could be carried forward for use in future years. This approach would eliminate the complexities of tracing, prevent economically inefficient tax arbitrage on leveraged equity investments and maintain the consumption tax base’s integrity. The US tax system already uses a similar method.

Reform of Canadian personal taxes relating to matters in the international arena would also bring greater economic benefits. For example, the limits on foreign content in registered savings and pension plans operate to the disadvantage of Canadian workers and savers with no offsetting benefits (see Fried and Wirick 1999) and should be completely eliminated. The withholding taxes on interest and dividends paid to non-

residents impose significant burdens on the Canadian economy (see Mintz 2001b), and they should be removed through bilateral agreement with the US or else unilaterally lifted. Other US tax provisions make it more burdensome for US managers, professionals and technical workers to work in Canada,43 thus reducing the benefits to the Canadian economy from tapping specialized skills. Canada should negotiate with the US to remedy this matter.

Personal income taxes (PITs) represent a somewhat smaller share of total taxes in Canada than in the US and a slightly larger share of GDP (see table 1). Despite this rough aggregate similarity, the composition between federal and subnational usage of the PIT differs sharply in the two countries. In Canada, federal income taxes are lower than in the US, but provincial income taxes are nearly twice as large as their US state and local counterparts.44 In this section, I examine the comparative tax rate structures at the federal level in the two countries, then at the subnational level and finally the top MTRs for combined federal-subnational income taxes.

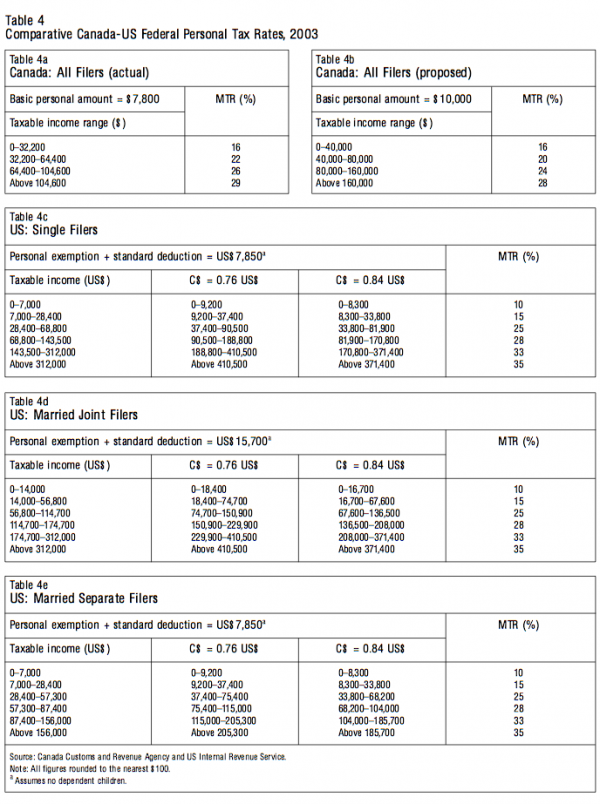

Table 4 presents the federal PIT rate schedules for the two countries in 2003, with the US taxable income brackets converted into Canadian currency using two exchange rates: a recent market rate (US$0.76) and the purchasing power parity (PPP) rate (US$0.84).45 The table includes the major US rate cuts of 2003 and presents schedules for three types of tax filers; Canada has just one rate schedule for all filers. When married couples in the US opt to file separate returns, they face tax rate brackets that are just half the width of those for married joint filers. Hence, for Canadian couples with partners having equal incomes, the US rate schedule for married separate filers (table 4e) offers the most appropriate comparison.

At incomes below $30,000 for single earners and $65,000 for couples, US federal MTRs are distinctly below those in Canada, a disparity that is augmented by larger personal exemptions and deductions in the US. At a taxable income of about $60,000, or $120,000 earned equally by married partners, the Canadian federal MTR of 22 percent compares with an MTR of 25 percent in the US. The top MTR of 29 percent in Canada applies for taxable incomes above $104,600, while the top MTR in the US is 6 percentage points higher at 35 percent and applies for taxable incomes above US$312,000 (or US$156,000 for married separate filers). In Canada, a couple with equal incomes does not incur the top rate until reaching a combined taxable income of $209,000. At a comparable income using PPP in the US, the couple filing jointly would pay an MTR of 33 percent.

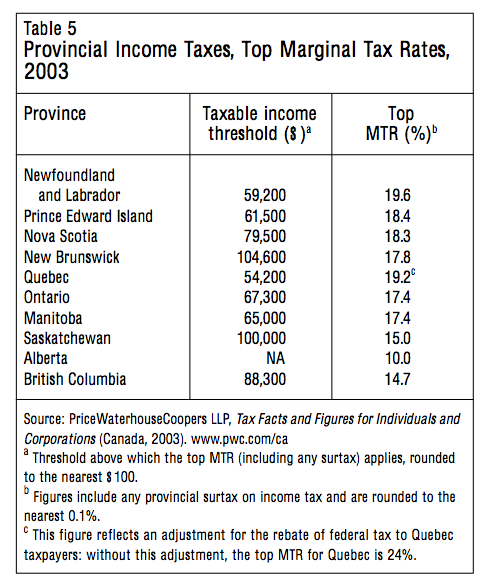

Tables 5 and 6 show the top MTRs for PIT at the Canadian provincial and US state levels, respectively, for 2003. In Canada, the top MTRs range from 10 percent for Alberta (with its flat rate PIT) to the upper teens for several provinces (after adjusting for the rebate of federal tax to Quebec taxpayers). British Columbia and Saskatchewan have top MTRs of 15 percent or just below. In most provinces, these top-rate brackets apply to incomes substantially below the $104,600 threshold for the top federal MTR, although New Brunswick matches the federal threshold and Saskatchewan approaches it. Overall, the rate schedules of the provinces other than Alberta display considerable progressivity of MTRs across incomes (though this is not displayed in table 5).

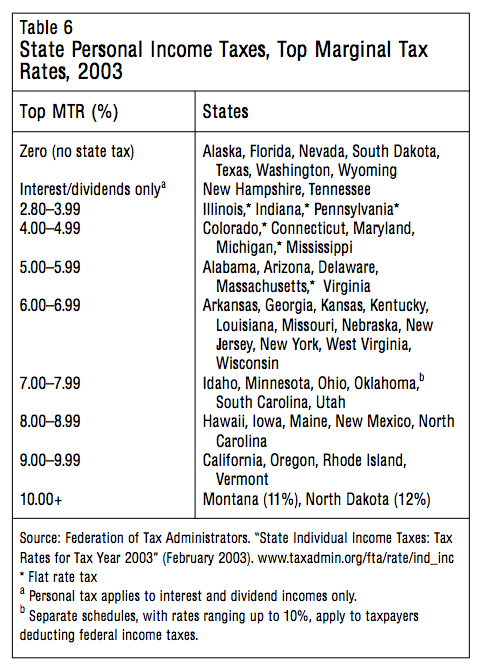

Table 6 classifies the US states by their top MTRs, with seven states having no PIT and another two taxing only interest and dividends. Six states, including most of those with the lowest top MTRs, apply flat rate schedules. For many states with progressive PIT schedules, the top MTR is attained at relatively moderate incomes, such as US$20,000 (or US$40,000 for couples) in New York. This pattern and the fact that several states have either no PIT or a flat rate PIT means that, overall, US state PITs are much less progressive than Canadian provincial PITs; this contrasts with the greater progressivity of the US PIT than the Canadian PIT at the federal level.46 Only two states (Montana and North Dakota) have top MTRs above 10 percent, and their rates are exceeded by those of all Canadian provinces except Alberta.