Parental Benefits in Canada: Which Way Forward?

Jennifer Robson

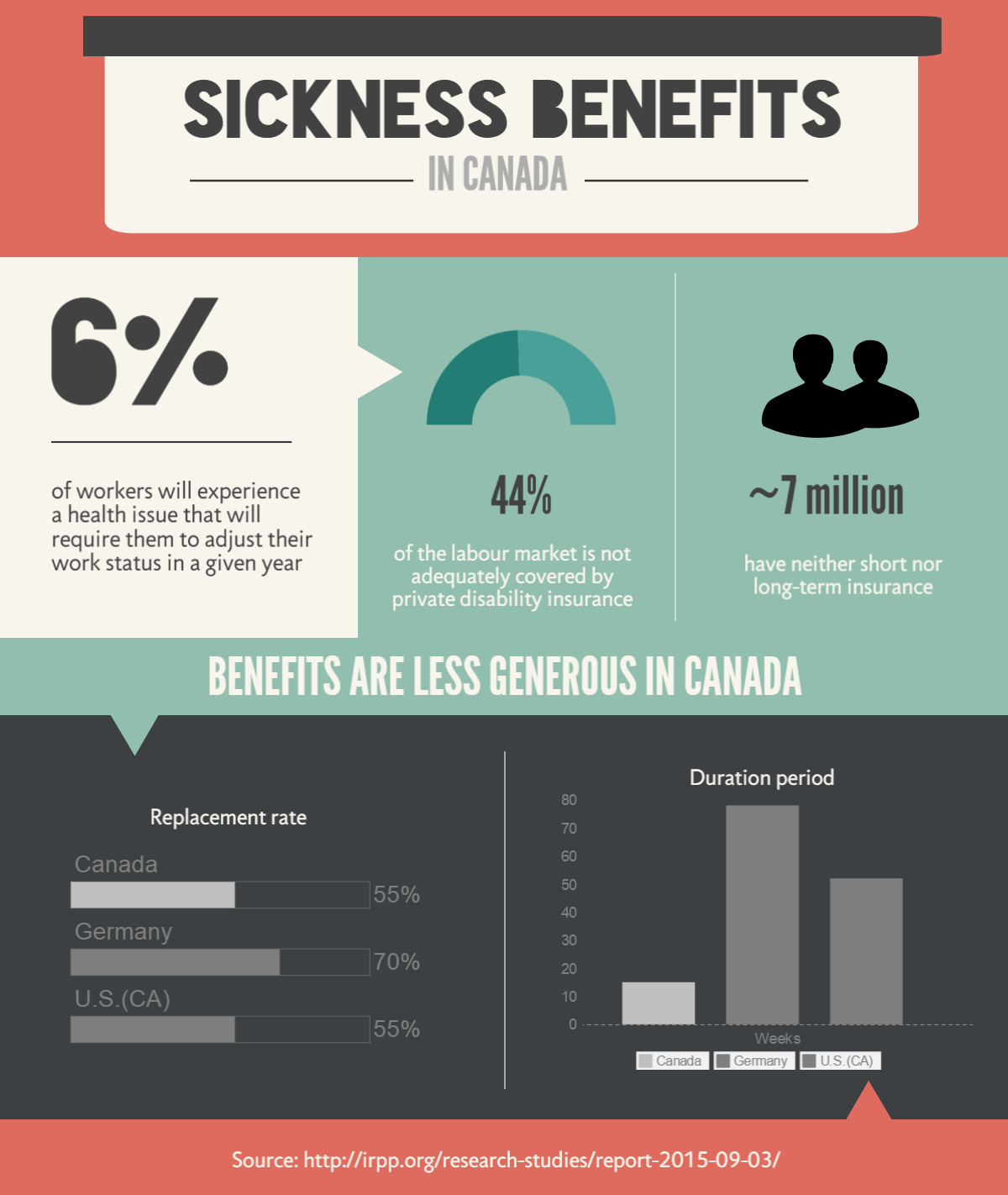

In a given year, six percent of Canadian workers will experience a personal health issue that will require them to adjust their work status. This can include being away from work for an extended period of time, changing from full- to part-time work, or leaving the labour market entirely.

Interrupting work is costly for everyone. In 2010, Canadian governments and insurance carriers provided $29 billion in direct income support to individuals dealing with a personal illness or disability. The loss of productivity to employers, the demand for care and the decline in consumption among households when employment earnings cannot fully be replaced are also significant dimensions of a health episode.

As our workforce ages and episodic and chronic health conditions become more prevalent, it is important that Canada have a robust and integrated system to support workers and employers when someone becomes sick. In June 2015, the IRPP convened a special round table with experts, stakeholders and practitioners to discuss these issues. Building on the round table discussion, Tyler Meredith and Colin Chia examine how Canada is doing, and the policy options governments should consider to strengthen the system.

Although Canada’s current income and employment support system meets the need of a large number workers, the authors note that too many are still being left behind. They identify a number of overlapping problems, including:

Addressing these problems, the authors argue, cannot be resolved by any one level of government in isolation. What is first required is a genuine process of engagement that brings together governments, employers and insurance carriers to revisit definitions of eligibility, and establish an integrated and comprehensive approach to address the needs of the same person. The authors also propose a series of short- and longer-term actions that each actor should consider.

How is Canada doing in supporting the employment and income needs of workers and families when they experience a major health issue? As Canada’s workforce ages and policy-makers strive towards a more inclusive labour market it is important to consider how employers and public policy support individuals through different periods of life involving challenges related to health and care. To address these issues the Institute for Research on Public Policy convened a roundtable in Ottawa on June 17, 2015, with representatives from government, academia, business, labour and health.2 That discussion and this paper focus attention on issues at two levels:

This work has made clear the need for a comprehensive re-examination of how Canadians are able to balance work and income during periods of receiving or giving care. Indeed, the time is right for such an examination. The recent enhancement of the Compassionate Care Benefit (CCB) as announced in the 2015 federal budget opens an important discussion about how care needs are accommodated in labour law and income support systems. This should be a starting point for governments and stakeholders to look at the holistic needs of families, including both those who are sick and those who deliver care, and under what circumstances additional support may be needed.

To that end, this paper provides context and analysis to help guide future research and policy analysis in this area. It briefly reviews the state of knowledge in Canada, summarizes key points of discussion during the roundtable3 and puts forward initial recommendations for governments and stakeholders.

The focus of the roundtable and, thus, this paper, is on what happens to individuals who are employed and subsequently become sick as a result of a health condition acquired outside of the workplace. Individuals whose illness or injury arises due to a health event within the workplace (and are covered as part of workers’ compensation / occupational health and safety programs), or who have an illness or disability but do not have prior work experience, are not discussed in the context of this project. While there are important points of overlap at both research and policy levels with the needs and challenges of these two groups, this project focuses on the broadly defined risk of illness or disability that all working Canadians face.

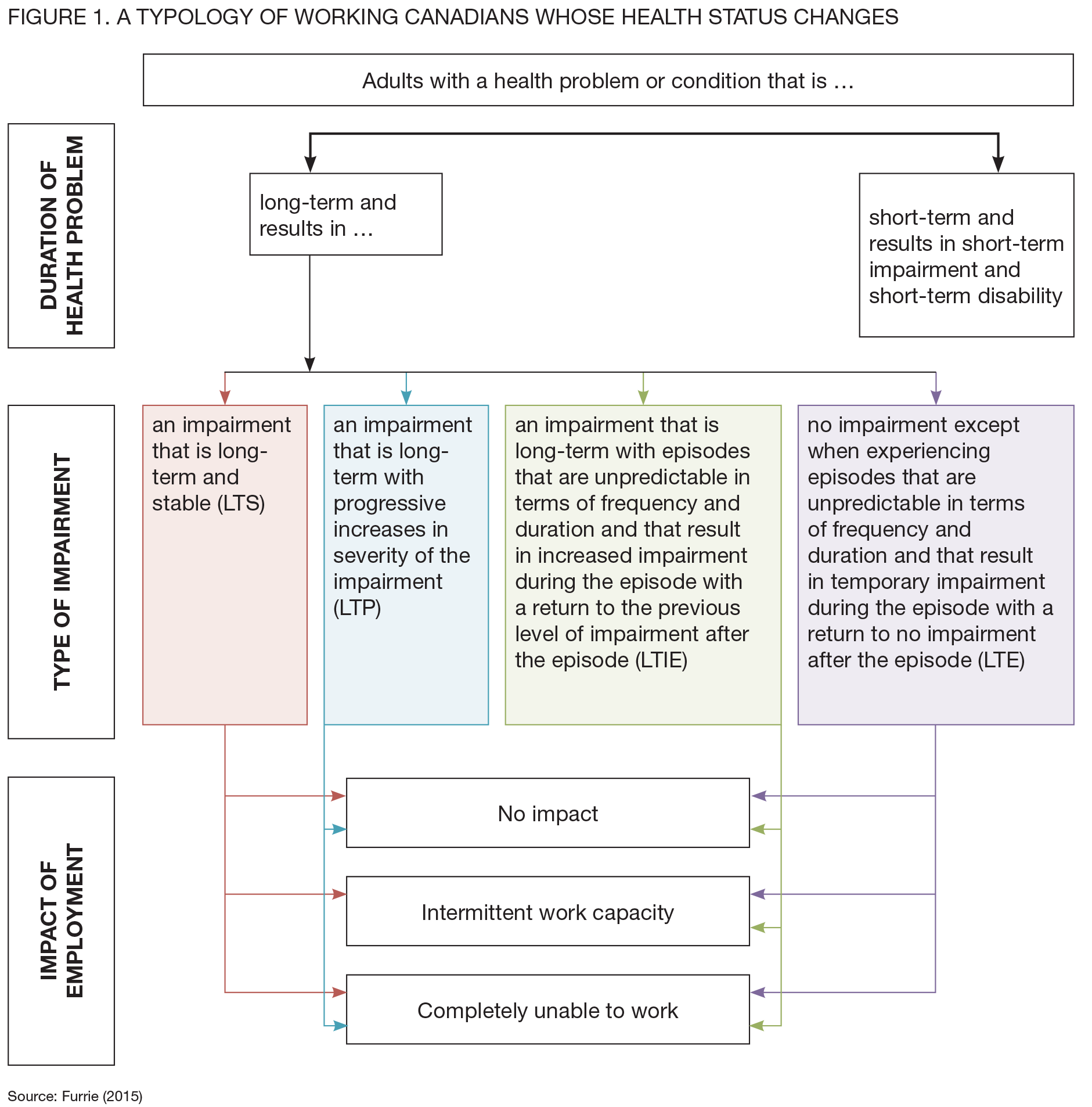

How a health condition presents itself in the context of work can take on many different forms, and operate across several different dimensions of time and severity. Most Canadians who fall sick will experience a condition that lasts only a very short period of time and simply require a leave of absence in order to get well. In other cases, the illness or disability may be episodic or progressive, and require either recurring or permanent accommodation.

The typology described in figure 1 is an important starting point for this discussion. Often policies and programs targeted at income or employment support focus narrowly on “disability”, assuming a health condition that is either continuous or progresses linearly through time (Furrie 2010). The Disability Tax Credit, for example, requires that eligible individuals face “marked restrictions” in daily living or work activities at least 90 percent of the time.

Given limitations in data and inconsistencies in definitions between health and social surveys, it is difficult to know exactly how many working Canadians transition into or out of each of the health states described in figure 1. While we are still missing a comprehensive snapshot of the population, various points of data suggest that a broad cross-section of Canadians go through one or more of these events over the course of life. Looking just at the population with episodic conditions, for example, Furrie estimates that at least 1.2 million working-age Canadians in 2012 reported one or more of the twenty conditions within this category (Appendix C). This group represented slightly more than half of the 2.3 million working-age Canadians living with a disability (Statistics Canada 2013).

Each year, about six percent of the Canadian workforce adjust their work status for some length of time in order to deal with a health condition. This can include either formally leaving a job, being absent from work for an extended period of time or taking part-time work in order to accommodate a reduced work schedule (figure 2). About 10 percent of people leaving their jobs in 2014, approximately 123,000 people, did so because of personal illness or disability, and 95,000 of these left the labour force entirely.4 This illustrates the extent to which illness can result in an extended and sometimes permanent separation from work.

Even as rates of labour market adjustment have stabilized in recent years, after growing rapidly between the late 1990s and mid 2000s, expenditures on sickness and disability income benefits have continued to grow above the rate of inflation. Between 2005 and 2010, spending by both public and private sources grew by 23 percent, to a total of approximately $29 billion a year (Stapleton 2013). While this figure includes a portion of expenditures beyond the scope of this paper (workers compensation, veterans benefits and some portion of provincial social assistance payments to those with no prior work experience) its magnitude and continued growth reinforce the need for effective accommodation. Helping individuals dealing with a sickness or a disability find, retain and return to work as soon as possible is important for everyone.

These data points, however, only tell us about aggregate spending. They do not give us any indication about the level of income replacement these benefits actually provide during a period of sickness or disability. How large is the decline in consumption possibilities within households? As discussed later on in the paper, there is some evidence this decline in earnings can indeed be dramatic and is not effectively compensated by the current system.

In economic terms, it is also important to note that absences from and changes in work capacity represent lost productivity for employers. Quantifying the economic cost of all the potential adjustments in work status related to one’s health is a challenging task due to differences in what is measured in and how leaves are classified between studies. As with overall expenditures related to income benefits, the indirect costs to employers are also significant. Looking only at the absenteeism component shown in figure 2, a very rough calculation would suggest a cost to employers of $13.7 billion in 2012, comprising either foregone productivity or replacement labour.5

Projected changes in demography and population health suggest these costs will continue to rise in the future. While active disability management, health promotion and wellness programs can improve prevention somewhat, sickness and disability incidence are still likely to increase naturally as the workforce ages and as certain chronic and episodic conditions become more prevalent and/or more severe across generations (Poschmann and Chatur 2013; PHAC 2014). For example, recent estimates from a four-year study co-managed by the Neurological Health Charities Canada and the Public Health Agency of Canada (Mapping Connections) suggest that the annual economic cost associated with the seven major neurological health conditions will rise from $7.3 to $8.2 billion per year over the next two decades (Bray, et al. 2014). While this rate of growth is slower than what is expected for real GDP over the period, the forecast rise in nominal costs is still significant. Much of this cost pressure will play out in the workplace.

It is important to emphasize that the figures quoted from the Conference Board as well as the Mapping Connections study include the replacement time of both those who are sick as well as those who are giving care, many of whom will also be drawn from the workforce. Just like those who are sick, job protection, flexible work arrangements and income replacement while on leave are critical for helping caregivers balance their work and care responsibilities. In practice, many employers have begun to provide various accommodations to address the rising pressure of care-giving responsibilities among workers (ESDC 2015b). As has been noted by the recent federal Employers Panel for Caregivers, the business case for doing this is potentially strong: taking proactive steps to plan for and address these needs can help to reduce lost productivity and even increase employee loyalty.

At a personal and a household level the impact of a health shock can be significant. Although the research base is still relatively small and disease-specific, a number of recent studies illustrate the profound and long-lasting effects that a health condition has on an individual’s long-term income and employment prospects. In the context of families, where decisions about job search, care-giving, and labour market attachment are often made jointly between spouses, these studies also point to the important ripple effects at a household level.

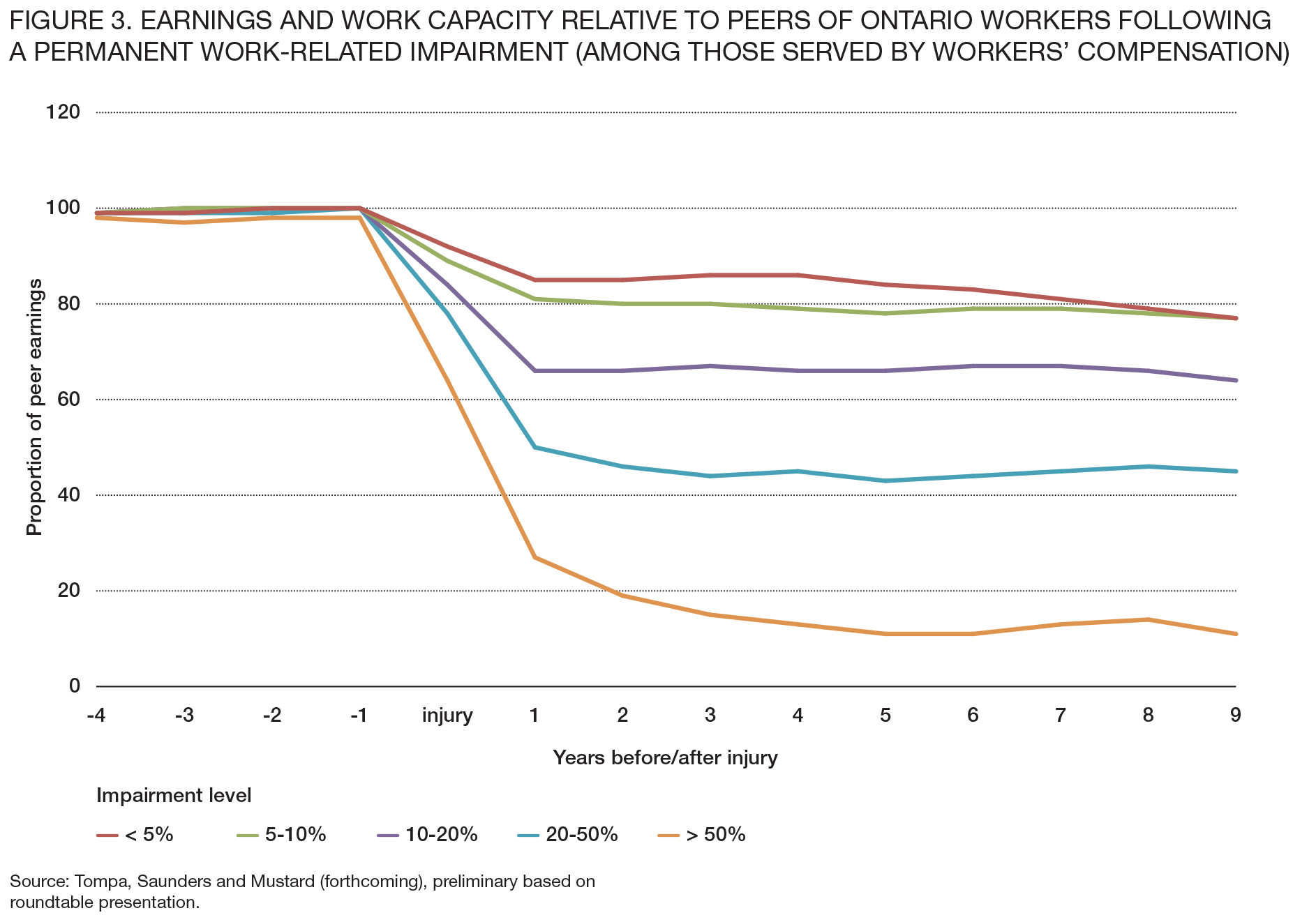

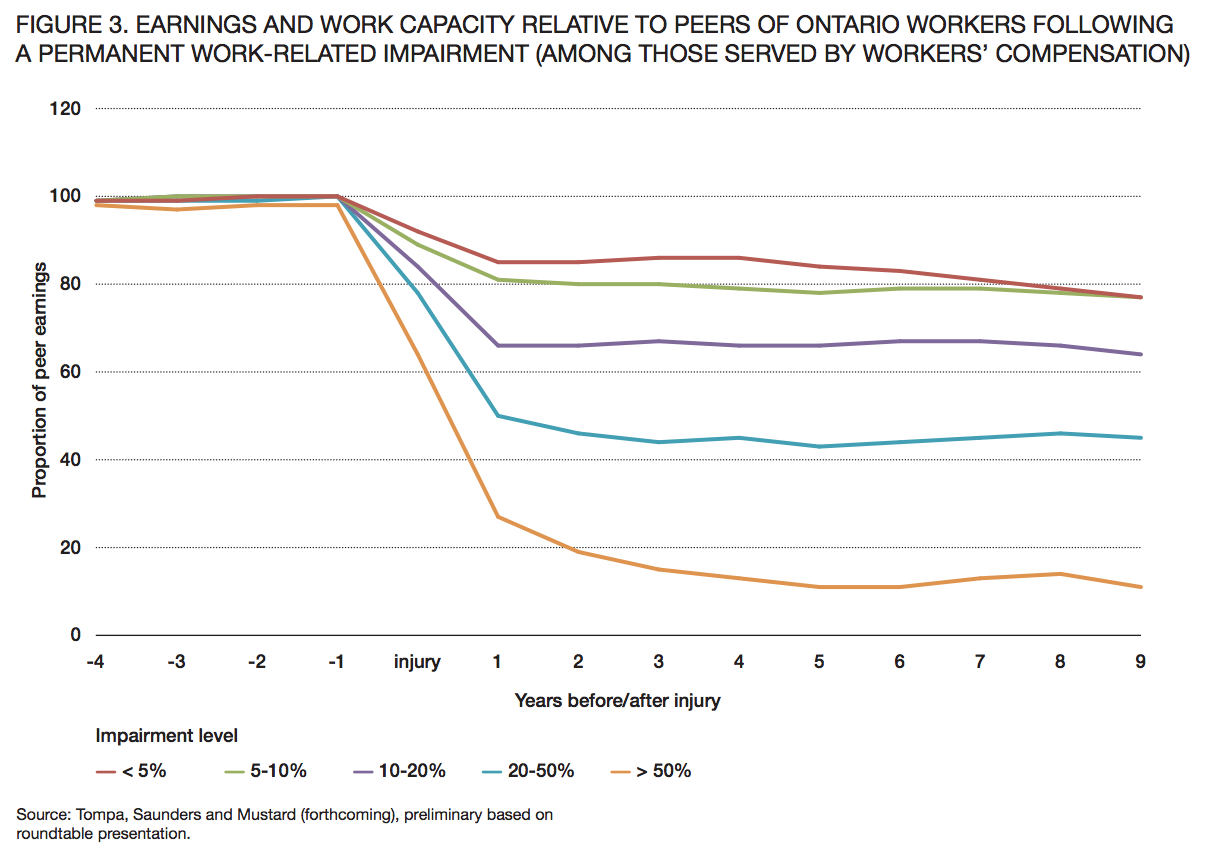

In a forthcoming paper from researchers at the Institute for Work and Health, Tompa, Saunders and Mustard examine how employment earnings change in the years following a major illness or injury. While their sample is restricted to Ontario workers who suffered a workplace-related illness or injury that was considered permanent, the findings are nonetheless instructive about the potential earnings disruption caused by a major health event. Indeed, the authors show that regardless of condition the drop in earnings relative to the individual’s injury is disproportionate and extensive (figure 3). Among workers whose impairment was assessed as being between 0 and 5 percent of total bodily impairment (e.g. relatively minor impairment), earnings post-injury ranged between 77 and 85 percent of the average of matched uninjured workers who had the same earnings during the four years pre-injury. Earnings losses were even more significant among those with more severe impairments.

A significant question to be resolved is whether these findings are unique to the occupational health and safety system, and whether in the presence of such health conditions employers and workers behave differently than would be the case for illnesses or injuries acquired outside of work. To the extent this phenomenon is comparable to the more general context of illness and disability, this research highlights potentially serious concerns about equity, the way in which return to work is supported and facilitated, and how workers are compensated for lost income.

A 2014 study by Jeon focusing on survivors of cancer finds that in the short-term, people with cancer suffer moderate losses of income (12 percent lower one year after diagnosis) and employment (3 percent lower in the first year) but these effects narrow over time, particularly if the person is able to continue working. In the long-run, the study notes, “cancer is more likely to affect survivors’ work status than their earnings” (Jeon 2014). How generalizable this is to other illnesses is not clear.

On the question of how households cope with a change in health status by one or more earners, Gallipoli and Turner (2011) find persistent effects of disability onset on labour force participation. For example, men (both married and single) who acquire a disability never return to their previous level of work hours, but the drop is greater for those who are single (and therefore lack spousal support).6 This may suggest that marriage and household formation provide an important shock absorber to the loss of income. The study does not address the effects of income and employment supports, however.

Given the significant findings of these three research studies, many participants in the roundtable reiterated the need for more extensive and better coordinated research between both stakeholders and government. A detailed description of the research priorities identified by the roundtable is presented at the end of the paper.

This section describes the current landscape of employment protection, income replacement and employment support programs available today to workers when or if they become sick or need to care for someone who is.

Sick leave job protection varies considerably within Canada (table 1). With the exception of Prince Edward Island, employers are generally not required to compensate employees during absences related to personal illness or sickness. In terms of the length of time protected by labour law, most jurisdictions which offer protection do so for a period of less than 10 days. Only employees in federally regulated industries or working in Quebec, Saskatchewan and the Yukon are able to take a leave potentially longer than 10 days a year (under certain conditions and coverage restrictions). Alberta, British Columbia and Nunavut have no employment standard related to personal sick leave.

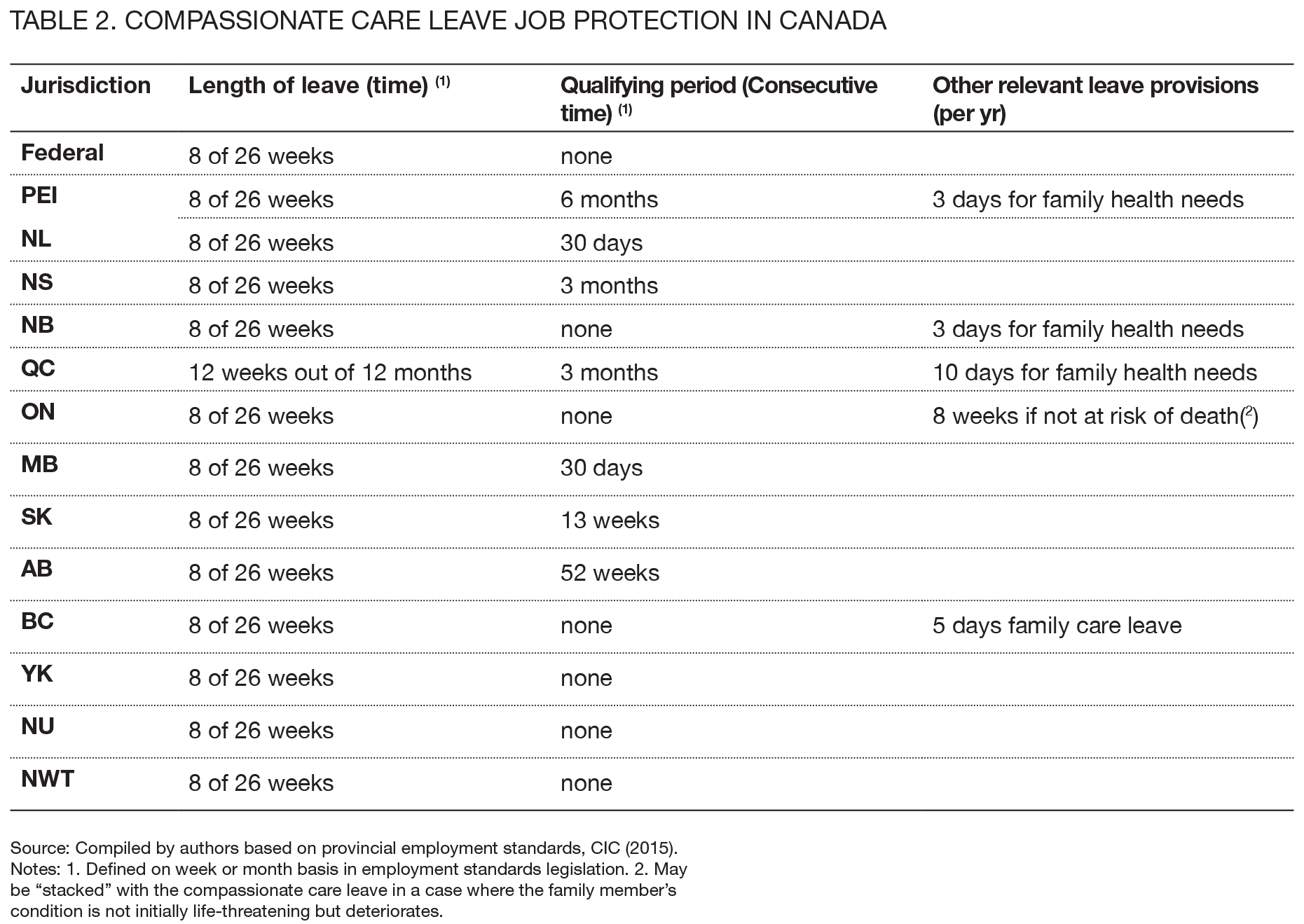

Access to compassionate care leave is more standardized. Compassionate care leave allows workers to be absent from work in order to care for a close family member who is critically ill. Although there is some variation with how broadly this is interpreted,7 most jurisdictions have converged on a period of 8 weeks (table 2) if a doctor certifies that a close family member is at significant risk of dying within 26 weeks. This generally mirrors the design of the CCB (which currently lasts for 6 weeks, after a 2 week unpaid waiting period is satisfied), although provinces and territories have yet to amend their employment standards to reflect the upcoming enhancement to the program (the 2015 federal budget proposed to increase the period of benefit duration from 6 to 26 weeks beginning in January 2016). The leave can generally be renewed if the family member continues to be in critical condition after the 26 weeks.

In addition to the minimum expectations set by labour law, approximately 60 percent of Canadian employers offer formal arrangements for paid and unpaid leave from work during the period of an illness or disability (Conference Board 2013b). Among private-sector employers coverage ranges between 50 and 55 percent depending on the type of leave policy (Conference Board 2013b).

How long absences from work last is hard to estimate because of differences between survey data.

Prior research using the Survey of Labour and Income Dynamics estimated that in 2003, workers who were absent from work due to a personal illness or disability for two weeks or more over the course of the year, were away on average 10 weeks (Marshall 2006). Were this representative of the total working-age population today, this would suggest most absences are handled as part of short-term disability (typically defined as lasting up to a period ranging between 17 and 26 weeks).

Even if they are entitled to take time off to care for themselves or their family, without income support workers will suffer a large reduction in their earnings or may not be able to make full use of the leave available to them. Marshall (2006) notes that access to private disability insurance is one of the most important, job-related predictors of whether a leave will be taken. Non-coverage or delayed entry into short-term disability support is thus a key impediment to taking timely and necessary leave for care.

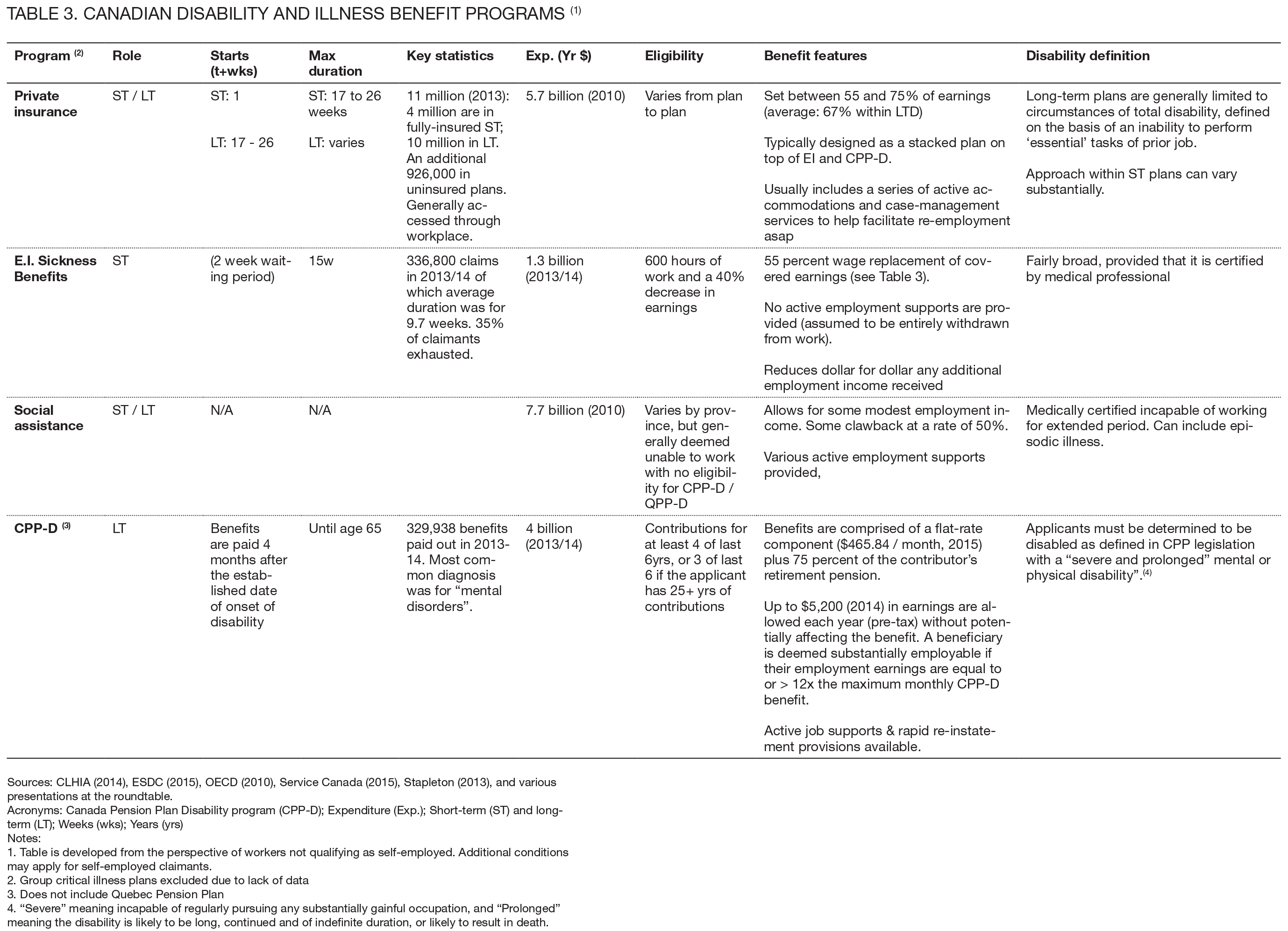

Canada’s sickness and disability insurance system comprises a number of different, integrated tranches, including a mix of both public and private income support. For the purposes of this discussion we focus exclusively on the role played by direct insurance and income support programs, including private disability insurance coverage, Employment Insurance (EI), social assistance programs and long-term disability (LTD) pensions provided through the Canada and Quebec Pension Plans (CPP-D/QPP-D). Table 3 provides a brief overview of each of the major component programs. Table 4 compares Canada’s main short-term disability insurance program — EI sickness benefits — with similar programs in other OECD countries.

Compared to other jurisdictions in the world, Canada’s system of sick leave and disability insurance is characterized by a heavier reliance on private coverage, combined with a smaller and less generous public component of mandatory wage insurance (table 4).8 Indeed, in 2010 private insurance carriers paid out greater benefits ($5.7 billion) to workers on short or long-term disability than Canada’s two primary public disability insurance programs combined ($5.5 billion) (Stapleton 2013).

How a worker transitions between public and private systems, and among the short- and long-term disability components within each, will depend on such factors as: whether an individual has private insurance coverage, the length of withdrawal from work, the severity of impairment, and the level of earnings loss and incapacity to work. Though Canada does not formally mandate private insurance coverage, disability benefits provided within EI are meant to cover short-term insurance as a last resort where employers or individuals do not have their own coverage through a private carrier. In this context, employers who provide disability insurance as part of a group benefits package are assumed to be the first payer and often operate their benefits as part of a stacked unit with public programs. Both the level of income replacement provided and the extent of ancillary services to help facilitate return to work are less generous and less extensive in Canada’s public programs than what is provided in the private market.

The transition process that occurs when or if someone exhausts short-term benefits will depend on whether they have private insurance or not, and whether their impairment is significant enough to qualify for a particular benefit program. Unless the impairment is severe enough to automatically qualify for CPP-D or QPP-D, a worker without LTD coverage would be forced to apply for general welfare or to draw down on their own personal savings. The same is also true for individuals who are solely covered by an LTD program whose benefit period does not automatically start after the exhaustion of EI benefits. These gaps in “medium-term” disability insurance present a major challenge for individuals, including those who have some form of private insurance (Prince 2008; Stapleton 2013).

Given these constraints it is not surprising that Canada’s public system of short-term disability insurance compares far less favourably to many of our international peers, including certain state-level programs in the United States. Limited to 15 weeks and 55 percent wage replacement, the provisions available within EI are particularly modest relative to similar programs elsewhere in the world. Converted to a standard measure of full-time equivalent weeks, Canada’s entitlement of 8.25 weeks is the smallest among the jurisdictions sampled in table 4.

Clearly it is important to have private insurance. If Canadians want a meaningful level of income replacement when sick, benefits that last more than 15 weeks and access to a broad suite of accommodations to help transition back to work, they will need a combination of both short and long-term disability insurance from a private carrier.

In 2013, a total of 11 million Canadians had access to at least one private disability insurance product, of which 10 million were members of LTD plans and 4 million were part of some form of a short-term plan (CLHIA 2014). While precise figures are hard to come by, these high-level estimates imply that of Canada’s approximately 17.7 million workers aged 15 to 64 that year:

At 10 million, LTD membership is equal to approximately 56 percent of workers aged 15 and over, almost exactly the same as in 2001 (Prince 2008). Based on data presented during the roundtable it is estimated that approximately 67 percent of full-time workers are enrolled in some form of private disability insurance, compared to just 23 percent of part-time workers. Coverage rates are highest among large employers and in workplaces and industries with a significant union presence. Sectors such as hospitality, entertainment and accommodations, which are dominated by low-wage employment or temporary and part-time work, have particularly low rates of coverage.

To encourage take-up of private disability insurance, a portion of EI premiums are rebated to employers offering plans with comparable or better benefits than those offered by the EI sickness program.9 Although the number of incorporated businesses participating in the rebate program is relatively low, participation in disability insurance programs is heavily weighted toward large employers. As of 2006, the latest year for which data is available, employers participating in the premium reduction program accounted for 41 percent of all employees in Canada. Approximately two-thirds of all members of short- or long-term disability insurance in Canada are covered by a plan receiving the premium rebate (ESDC 2013).10 More research is needed to understand how employers make decisions about the provision of group benefits. In the limited information available, cost is often the most cited reason for not offering group disability insurance (ESDC 2013).

The extent to which participants in the premium reduction initiative are representative of all disability plans in the country is not known. It is at least interesting to note that 90 percent of employers participating in the premium reduction program offer both short- and long-term coverage, and the vast majority of short-term plans offer sufficient coverage to bridge between 15 and 52 weeks (ESDC 2013).

How episodic, chronic and non-physical impairments are accommodated within each program is a rather complex issue. Like private disability insurance, both CPP-D and provincial social assistance systems have been noted to use definitions of impairment that are either highly conditional on prolonged or indefinite withdrawal from work, or which reflect a significant restriction of work capacity (Prince 2008). Where insurance payouts are triggered by being unable to resume the previous job, CPP-D requires claimants to be unable to be employed in “any substantially gainful occupation.” While these are not explicit exclusions, it can make formal medical certification a challenge. Despite these potential barriers, it is noteworthy that mental illness is the most common disorder among CPP-D claimants (see table 3).

Notably, British Columbia’s social assistance system has explicitly included episodic illnesses and mental health disorders in the eligibility for benefits. Persons with such diagnoses can qualify for one of two income support streams: Persons with Disabilities, which is meant to support those with different levels of severity in activity limitation; or Persons with Persistent Multiple Barriers, which is based on medical impediments to employability.

Not only do workers experience a drop in income while on leave, but like any absence from the labour market there are often future consequences in the form of reduced earnings and employment prospects, and slower progression in seniority (Galarneau and Radulescu 2009). Stigma, stress and difficulties obtaining workplace accommodations can compound these challenges.

While leave is formally protected in many provinces, how a worker transitions back into employment following a period of illness will be affected by a number of factors including how income benefits are designed to incorporate and support employment while a worker is on claim and, in turn, the kind of practices that take place in the workplace. For persons with episodic or chronic illnesses whose work capacity may be intermittent, qualitative research has noted three factors as being key for successful employment (Fowler 2011):

The provision of employment supports within private insurance programs is often quite extensive given the direct incentive that both employers and insurance carriers have in achieving a successful return to work. By comparison, the practice in public programs such as EI and CPP-D or QPP-D is much more haphazard. While on claim, individuals receiving EI sickness benefits receive no formal employment supports and are not permitted to earn any additional wages without being subject to a full claw-back of benefits.

Claimants receiving CPP-D are entitled to volunteer as well as receive earnings up to $5,200 per year without affecting their benefit. While still relatively low, this earnings disregard has been found to have a positive effect on both the income and workforce attachment prospects of claimants without increasing uptake of CPP-D more generally (Campolieti and Riddell 2012). Furthermore, CPP-D and some provincial social assistance programs also provide automatic reinstatement for two years after someone resumes work. Such provisions allow claimants to gradually re-enter the labour market for a trial period (usually limited to several months) during which time recipients can restart benefits without re-applying, if they find they cannot sustain workforce involvement.

Over the last decade various provincial social assistance systems have moved in the direction of relaxing claw-back rules and earnings exemptions in order to increase the financial incentive toward work. Ontario, for example, now exempts 50 percent of earnings over $200 each month from the calculation of eligible Ontario Disability Support Program entitlements (Ontario 2015). B.C. provides an earnings exemption ranging from $9,600 for singles up to $19,200 for couples where both adults have a disability designation (British Columbia 2015). The flexibility of such parameters is obviously beneficial for people with periodic absences from work. The restrictiveness of EI sickness benefits with regard to employment can have a significant impact on personal and household experience (see Appendix D).

In addition to supports provided by a private insurance carrier or a public benefit program, employers also have an important role to play in helping accommodate workers. Often these accommodations, which can include such things as flexible work hours or assistive devices, are relatively inexpensive to implement. What is required is effective awareness of potential needs, understanding of the types of job accommodations that might be beneficial, and a commitment to practice.

Given their significant HR capacity and ongoing workforce needs some large employers are already well advanced in thinking about and addressing these issues. The roundtable heard from practitioners who spoke about how organizations such as Walmart and Royal Bank have successfully implemented initiatives to coordinate the provision of accommodations for employees when an illness or disability arises. In these and other case-studies, an emerging body of research has demonstrated the long-term benefits such programs can bring to an employer, in particular to turnover and related costs.11

Overall, however, such examples remain the exception among Canadian employers. A recent survey of employers by the Conference Board estimates that only 18 percent of organizations have structured stay-at-work programs to help employees preserve employment while off on leave, while only 41 percent have formal return-to-work programs in place (2013).

For persons with disabilities who do not qualify for CPP-D or EI, a range of employment support measures are also available under the Labour Market Agreement for Persons with Disabilities (LMAPD). Through the LMAPDs, the Government of Canada transfers funding to provinces and territories to help deliver programs which enhance the employability of and increase employment opportunities for persons with disabilities.

In addition, the federal Opportunities Fund for Persons with Disabilities (OF) supports a wide range of programs and services, including skills training, job placements and wage subsidies to encourage employers to hire persons with disabilities. Employers are also able to apply for financial assistance with implementing workplace accommodations. Accommodations have often focused on investments in physical adaptations and technology.

Through the CCB, EI provides up to six weeks of income support to individuals who require time away from work to temporarily provide care or support to a family member who has a serious medical condition with a significant risk of death within 26 weeks. Thanks to a recent enhancement, beginning in January 2016 claimants will be able to receive the benefit for up to 26 weeks over the period of a year.

Eligibility for the CCB, like EI sickness benefits, requires workers to have accumulated 600 hours of employment over the prior year. However, unlike EI sickness benefits, claimants receiving the CCB are able to maintain their claim as they gradually return to work. Under the current EI Working While on Claim pilot project, EI claimants receiving CCB are able to keep 50 cents of their benefits for every dollar they earn, up to 90 percent of the weekly insurable earnings used to calculate the EI benefit amount. If they earn more than this amount, additional earnings will be deducted dollar for dollar from their EI benefits to ensure that the combined earnings and EI benefits are not more than the amount of earnings used to calculate the benefit amount.

As part of the recent enhancement to the CCB, the federal government has also made corresponding amendments to the Canada Labour Code so that employees in federally-regulated industries are able to protect their employment for up to 28 weeks, including the full period while on claim (Canada 2015). Provinces and territories have still to update their respective labour codes to reflect this change.

A key message from the roundtable is that Canada’s support system is in need of fundamental renewal. This section briefly details the range of problems with the existing system, setting out key context and considerations as to how policy-makers and stakeholders should approach these issues.

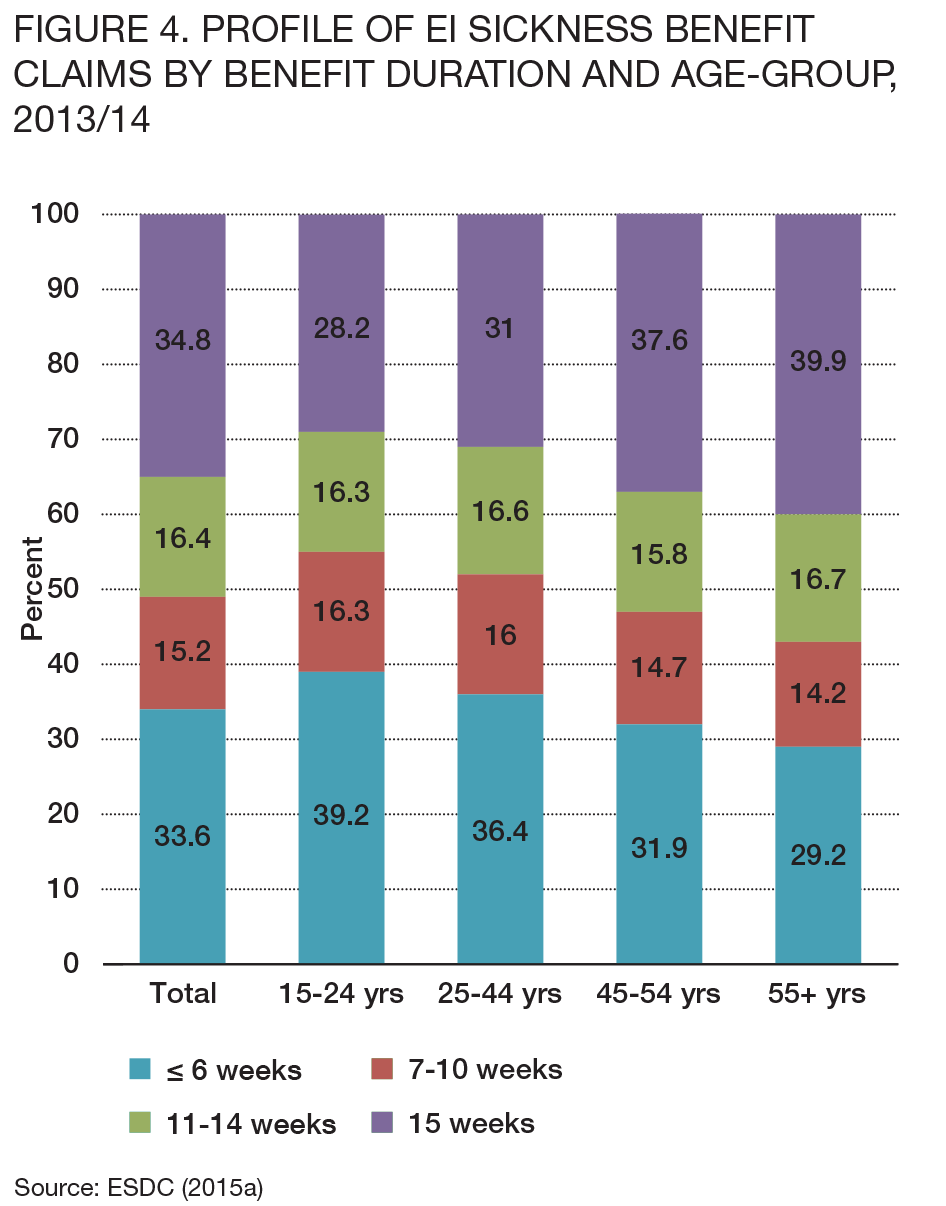

In 2013-14, approximately 337,000 Canadians received sickness benefits through EI, and slightly more than a third of these claimants fully exhausted their benefits after 15 weeks. It is not known how many Canadians exhaust short-term disability without automatically qualifying for LTD, either from CPP-D or QPP-D, or through their own private insurance. Needless to say, given both the number of EI claimants who exhaust benefits and what is known about the gaps in time and coverage between short and long-term disability plans in the private market, the combined number of people who fall through the cracks is likely non-trivial.

It is also important to note that, within EI, benefit exhaustion rates have increased over time. Although there is no publicly available data which examines benefit exhaustion rates by the nature of illness or disability, those who face long-term, recurrent and or severe illnesses, such as cancer, would obviously be at heightened risk of benefit exhaustion. A 2007 study of EI clients who exhausted sickness benefits found that nearly three-quarters did not return to work within six months, or ever (ESDC 2015). Consistent with the profile of disability and illness, those who use sickness benefits, and those who exhaust them, are most often older adults (figure 4).

Exhaustion of benefits is not itself a problem if there are effective and seamless bridges between benefit programs. This is not the case today. Not only is this system exceedingly difficult to navigate but for the large portion of the labour market not covered by either a private LTD program or one which begins in tandem with the exhaustion of EI benefits, the decline in living standards can be significant if the worker needs to remain on extended leave and is not immediately eligible to begin CPP-D. The absence of a common definition of eligibility with respect to “disability” was cited by many participants in the roundtable as a major source of this problem.

For example, a worker who is dealing with an extended period of recovery from an illness for six to eight months would not likely fit the definition of the prolonged or severe impairment as required by CPP-D, especially if at the end of their EI claim treatment has been successfully concluded but additional recuperation remains necessary.12 If the worker does not have private LTD insurance, and requires additional leave beyond what is provided for through EI, they are left with essentially two choices: 1) seek accommodations through their employer; or 2) temporarily access provincial social assistance, and likely accept a significantly reduced benefit. Such difficult choices arise regularly for working Canadians (see examples in Appendix D). Ironically, were the worker laid off by their employer they would be entitled to EI for an additional, and potentially longer, period of time.13

The fact that private insurance coverage has remained relatively stable since 2001 was seen by participants in the roundtable as both a success and a challenge. As some noted, the fact that coverage did not decline during this period despite slow economic growth, eroding labour cost competitiveness within Canada, and two major recessions, is an indication of the resilience and importance that employers attach to group benefits such as disability insurance. This, however, only speaks to the population of firms already offering private insurance.

Much like pensions and other ancillary benefits, there are significant gaps at both an industry and firm level in the accessibility of disability insurance. As insurance participation is heavily influenced by the size of an employer, and whether a job is offered on a full-time and permanent basis, there is a risk that existing gaps will worsen as the labour market continues to undergo significant structural shifts in labour demand. Since the 2008-09 recession, for example, the rate of employment growth among SMEs has significantly outstripped large employers.14 Combined with the greater prevalence of non-standard work compared to decades past there are important questions to be asked as to whether the provision and accessibility of disability insurance should be guaranteed on a more universal basis. If governments believe that private insurance is optimal then there must be an effective strategy to address existing gaps in the labour market.

One of the virtues of private insurance is that it often provides more generous income support and higher quality supports for assistance with return to work than is available within either EI or other public programs. However, for those in the labour market who are left to rely on public programs alone, it stands to question why this two-track reality exists and whether it makes sense.

One might argue that by providing inferior benefits to what is generally available within the private market, there is a strong incentive for workers and employers to purchase supplemental insurance. While this is understandable from a theoretical perspective, the stagnancy of private coverage remains.

As mentioned earlier, those who qualify for EI sickness benefits are assumed to be fully withdrawn from work during the course of their benefit claim and, as such, are not allowed to top-up their benefits with any partial employment earnings (without being subject to claw-back). In contrast to recipients of regular unemployment benefits, an employer is not able to access work-sharing benefits, wage subsidies or accommodation grants to help a claimant of EI sickness benefits find or retain work. Once a claimant becomes eligible for CPP-D they are entitled to, among other things, a nominal earnings exemption and can access a number of programs to help find work.

This arrangement among public programs, effectively limits employment supports to the farthest point in a worker’s claim journey (CPP-D), a point of time when their impairment is likely most severe and the odds of moving back into employment are lowest.15 Not only is this approach inconsistent with the incentive among private insurers to help return an individual to work as soon as is practical, but it may also make it more difficult for workers to obtain and retain employment with the help of flexible work arrangements. There was broad agreement among many participants in the roundtable that this approach does not make sense from either an actuarial or equity perspective. Providing active employment supports for both employers and workers earlier on in the course of an illness may help improve the well-being of workers as they recover from an illness, enhance earnings capacity, raise long-term employment retention, and, as a result, potentially reduce the need for future claims.

Participants expressed the desire to see the federal government move toward greater parity in the extent of employment supports which are provided between EI and CPP-D, and in particular to adopt a more active approach to employment within both.

As the preceding discussion has made clear, there exists a high degree of incoherence in how each component program is designed to serve the same person. While this reflects a broader problem across social and labour market policy in Canada, the point remains salient: of the various public and private programs which support individuals in need of income or employment support during an illness or disability, each tends to be oriented towards its own outcomes rather than the client’s holistic well-being, or the overall system.

Consider the example of someone living in Ontario: when they receive EI sickness benefits, any employment earnings received while on claim are deducted dollar for dollar. If, following the exhaustion of EI benefits they subsequently qualify for the Ontario Disability Support Program the individual would be permitted to continue working (at least partially) while receiving assistance; if they qualify for CPP-D, their benefit may be reduced or terminated if they earn more than $5,200 per year. Considering that over the course of a claim journey individuals may end up being served by multiple programs, the inconsistent and, in some respects, radically different approaches taken with respect to the treatment of work make if exceedingly difficult for an individual to navigate.

During the course of the roundtable participants heard several powerful examples of how the lack of an integrated approach to benefit eligibility, case management and employment can result in delays accessing benefits and even hardship. In some cases one program can terminate benefits without clear direction or assistance of where to go to next.

As a combined system these programs are deeply fragmented and lack coordination. The recent enhancement of the CCB provides an excellent illustration of this. While the enhancement of benefit duration from 6 to 26 weeks is a welcome development, one of the unintended consequences of this change is that, within the context of EI, those who provide care may now receive greater benefit support than those who receive care (limited to 15 weeks). This points to a major problem of inconsistency across the system as a whole in terms of both the definitions used to determine eligibility (in particular how disability is interpreted and applied), and the length of time and triggers that are used to set the duration of benefits. Some programs, for example, allow benefit stacking, while others count payments from other programs as income and claw-back benefits.

Participants were adamant that as part of changes in any one program there must be a broader commitment to revisit the overall design of sickness and disability support programs in Canada. The goal of such a review should be a more consistent set of definitions and transition mechanisms between federal, provincial and privately delivered benefit programs. As was articulated by numerous experts and stakeholders, the system, with its multiple moving parts and distinct income sources, too often results in substantially different outcomes for individuals suffering the same impairment.16

As a symptom of the challenges of coordination and coherence across the system, many participants also expressed concern about how intermittent work is valued on the part of various income support programs.

While it is important to note that governments at all levels have undertaken a variety of incremental reforms over the last several decades to encourage greater labour market attachment when someone is receiving income support, important barriers still remain, particularly at the federal level. A prominent example, as already noted, includes the treatment of employment income within the EI sickness program, where earnings are clawed-back at a marginal effective rate of 100 percent (i.e. dollar for dollar). Though CPP-D does provide an earnings disregard and a rapid-reinstatement process not available within EI, many participants noted that the treatment of earnings above the earnings disregard threshold of $5,200 can be unclear and in some cases still create perverse disincentives to employment.

A clearer and more consistent approach to the treatment of work-related earnings, both as it relates to benefit eligibility and claw-back rules, is needed across all programs. This should be regarded as a system-level issue and resolved in collaboration between federal and provincial officials.

While employer awareness around issues of disability and illness has risen in recent years thanks to educational efforts on the part of both government and stakeholders, it remains low, particularly among SMEs who likely also do not have extensive in-house HR capabilities.

The experience of many organizations involved in vocational rehabilitation is that employers generally want to accommodate and retain workers with disabilities, but lack the required knowledge and resources to do this well. One participant in the roundtable noted that in their experience 55 percent of employers who receive awareness briefings or training go on to employ persons with a disability. Replicating and bringing these resources to scale is integral to any comprehensive strategy in this area.

No one actor can address each of the issues outlined above. These are collective problems which require coordinated action, supported by a common vision of how to serve the integrated, household-level needs of both caregivers and care-receivers at the time an illness occurs.

This project is a starting point toward that vision. As part of the roundtable, participants collaborated on defining a potential roadmap with concrete actions that could potentially be undertaken by governments, the private sector and stakeholders, looking at both the short and long-term horizons.

Perhaps the first and the most important step toward this vision is to revisit the concept of disability and the way it conditions how governments deliver benefits and how employers assess work capacity. As many participants underlined during the roundtable, much as an illness or disability may change the potential level and pace at which work can be undertaken, for most, an impairment does not alter the underlying skill-set or the desire to work. That workers can experience a drop in earnings disproportionate to their impairment (see figure 3) underscores the critical importance of affecting how employers and governments view the relationship between work and health.

Building on this, participants identified a series of principles that could form the starting point for a broad process of inter-governmental and cross-sectoral engagement for defining a new, integrated framework for supporting individuals dealing with sickness or disability. These principles are agnostic to questions of who and how program delivery is arranged.

Underpinning this vision are two key axes: that employees are well supported so they can be healthy and remain working; and, as a consequence, that employers benefit from a workforce that effectively utilizes the talents, productivity and “diverse-abilities” of every worker.

Based on these principles, we put forward a series of possible policy directions for consideration by stakeholders and policy-makers. Given the deliberative process of review and reform called for above, we recognize that some of these directions will be easier to implement than others, and that in some cases additional research is required before a particular course of action can be undertaken. We have therefore grouped these into what constitute elements of a longer-term transformation across the system, versus specific actions that could be taken in the short- and medium-term.

Arguably the most important areas for reform over the long-term involve: 1) improving the coordination of basic definitions and program parameters across the disability support system, and 2) enhancing the breadth and quality of disability insurance coverage within the labour market.

Achieving a better coordinated and more integrated system of benefits will, as already mentioned, require an extensive engagement on the part of government, the private sector and stakeholders in order to arrive at some consensus on how eligibility definitions and the sequencing of benefits can be made more consistent and robust. Over the last several decades there have been several attempts on the part of various provincial and federal governments to initiate a similar kind of coordination process. While these have brought about some needed reforms, clearly we are left with a system that operates in piecemeal and even, at times, at cross-purposes. Surmounting these same challenges will require a process that begins not from the perspective of who should do and fund what, but rather how better outcomes can be achieved for individuals and families. For this to succeed the federal government must be a champion. Given the sheer magnitude of both CPP-D and EI sickness benefits within the broader income support system for persons with disabilities it would be impossible for this vision to be achieved in the absence of federal leadership.

It is critical that this engagement process include not just ministries responsible for the delivery of social assistance and employment support benefits, but also provincial and territorial ministries of labour, as well as insurance regulators and other relevant parties.

The second major problem that must be addressed over the long-term is to improve disability insurance coverage so that all workers have access to an adequate standard of income replacement, reasonable benefit duration in order to cover both short and long-term insurance needs, and active labour market supports to help facilitate or maintain employment. Here, governments have a number of options, which could include either enhancing EI sickness benefits so they are more directly on par with what is offered in the private market or, at the other end of the spectrum, adopting a formal insurance mandate that could even potentially remove the need for the EI sickness program. Under the latter option, federal and provincial governments would establish a series of common conditions and minimum benefit parameters that insurance providers would be required to meet. In either case, we recognize Canada begins from a framework in which private insurance is considered to be the primary benefit unit for most workers. Any enhancements in both coverage and quality should seek opportunities to enhance benefits within this framework.

In thinking about how to increase private disability coverage it is noteworthy that Canada already provides a direct financial incentive — the EI Premium Reduction Program — to employers who offer disability insurance benefits which are equal to or better than what is offered by EI. While the program has received broad take up among employers who already offer group disability benefits, it is not clear what direct impact it has had on expanding insurance coverage across the labour market . Indeed, one participant during the roundtable cited an anecdotal example of an employer interested in exploring options for an insurance product that would carve out the portion of sickness benefits provided by EI. Under this model, short-term insurance coverage would begin only after EI benefits are fully exhausted, thereby making the public program the first payer. While there are no specific examples where this is known to have been implemented, it illustrates the critical need for the federal government to carefully examine the effectiveness of different mechanisms for expanding private coverage while ensuring consistency in benefit design.

However governments approach the coverage problem, there is also a need to ensure that the duration of benefits in both public and private programs eliminate any potential gaps in the hand-off between short- and long-term insurance. The simplest way to address this would be to expand the basic short-term benefit period from 15 to 26 weeks, a change which would also be consistent with the newly-enhanced CCB provisions. While such an enhancement would provide a more resilient and coherent income support system, we do recognize the potentially significant fiscal implications this may impose, both in terms of potentially encouraging a longer claim and any potential substitution of privately insured beneficiaries into the public system.

To mitigate some of these concerns, the federal government may wish to consider implementing this enhancement as part of a distinct tranche of benefits, in between the current basic EI sickness provision and CPP-D. Under such an arrangement, beneficiaries who exhaust the first set of short-term benefits (e.g. EI) would be streamed to a follow-up medical certification to determine the extent and severity of an ongoing illness and, if necessary, to place them on this new supplemental benefit program. Combined with appropriate support services, this check-in point could be used as the basis for developing a return-to-work plan for beneficiaries and help clarify future transitions over the course of their claim journey. The government will need to consider various regulatory options to ensure that substitution is minimized.

Federal, provincial and territorial governments should look to this enhancement as an opportunity to have a broader conversation about the length of time that sick leave should be protected under employment law. To the extent the federal government can replicate the success of the CCB in leveraging a series of coordinated changes to provincial and territorial employment standards this conversation should be pursued.

Other changes to enhance the flexibility of benefit design must also be explored. For the federal government this could involve the potential introduction of an earnings disregard within the EI sickness program (or access to Working While on Claim), and an expanded earnings disregard, clearer earnings claw-back rules and greater return to work accommodations within CPP-D. Ultimately, this must be part of a coordinated effort with provincial and territorial governments to arrive at an integrated and consistent approach. In the next section we present more modest changes that can be implemented in the short-term to similarly encourage successful re-employment.

Reorienting employment and income support policy will be a long process. In the short term, there are important and achievable things that can be done which would improve the current system. Let us briefly comment on two such actions.

Consistent with the long-term objectives of a more flexible and active approach toward employment, the federal government should begin to introduce a series of support services into the EI sickness program in order to help facilitate return to work. While it may not be possible to replicate the full range of supports available within private insurance programs, a revised program should ideally incorporate the following elements. Many of these supports exist elsewhere within EI and would simply involve opening them up to claimants of sickness benefits, including:

In addition, the federal government should also consider establishing a center of expertise to help disseminate information to employers on their respective duties, potential best-practices and available resources to draw on when a worker experiences a health shock and may require a leave from or accommodation to their work.17 This could potentially build on the newly created network, Canadian Business SenseAbility, an employer network supported by ESDC to help promote the hiring of persons with disabilities.

Based on the issues and literature presented in this paper it is evident there are many areas in which we simply do not know enough. These must be resolved if the policy directions and long-term vision we have described are to be implemented effectively. From the roundtable and subsequent research carried out in preparing this paper we see the following items as research priorities for both stakeholders and policy-makers. All should be actioned as soon as possible.

As Canada enters a period in which demographic change will increase the cost and prevalence of absenteeism due to illness, it is important that workers and employers are properly insured to deal with these risks. While Canada’s current system of income and employment support does help many Canadians dealing with illness access the help they require, too many are still left behind.

Though a majority of Canadian workers are adequately covered by private disability insurance, a large portion of the labour market has no coverage and must therefore rely on a host of different public programs which, in some cases, may provide inadequate support and are often characterized by poor coordination and a relatively passive approach toward employment support. These reflect problems of design, coordination and inadequate flexibility, such that where one works and the nature of one’s impairment can dictate how effectively income and employment needs will be supported during the period of illness. This situation is neither fair nor an effective approach if we are to support all Canadian workers in realizing their potential.

Income and Employment Needs of Persons

Dealing with Illness: Roundtable

Wednesday June 17, 2015

8:30 a.m. – 4:00 p.m.

Rideau Club

99 Bank Street, 15th Floor, Ottawa

8:00 – 8:30 a.m.

Continental breakfast – buffet

8:30 – 8:45 a.m.

Welcome and introduction

8:45 – 9:30 a.m.

Session 1 – Framing the issues

Opening presentation

Tyler Meredith (Institute for Research on Public Policy)

Reactions, comments

Annette Ryan (Employment and Social Development Canada)

Neil Pierce (MS Society)

9:30 – 10:45 a.m.

Session 2 – Insurance and income support

Presenters

Paula Allen (Morneau Shepell)

Kathryn Gregory (Sun Life Financial)

John Stapleton (Open Policy Ontario)

Discussant

Emile Tompa (Institute for Work and Health)

10:45 – 11:00 a.m.

Break

11:00 a.m. – 12:00 p.m.

Session 3 – Employment support: Leaving and returning to work

Presenters

Adele Furrie (Adele Furrie Consulting Inc.)

Maureen Haan (Canadian Council on Rehabilitation and Work)

12:00 – 12:30 p.m.

Session 4 – Lived experience

Sharing the perspectives of families and stakeholders

12:30 – 1:15 p.m.

Lunch – buffet

1:15 – 2:30 p.m.

Session 5 – Assessing the policy options

Discussants

Herb Emery (School of Public Policy, University of Calgary)

Nora Spinks (Vanier Institute of the Family)

Peter Hicks (Consultant)

2:30 – 3:30 p.m.

Session 6 – Developing a roadmap

Facilitated roundtable discussion

3:30 – 4:00 p.m.

Concluding remarks

| Owen Adams | Canadian Medical Association |

| Paula Allen | Morneau Shepell |

| Sara Bergen | Mental Health Commission of Canada |

| Andrew Brown | Employment and Social Development Canada, Government of Canada |

| Gillian Campbell | Canada Pension Plan Disability Program, Government of Canada |

| Warren Comeau | Rehabilitation Alternatives Limited |

| Marcelle Crouse | Ministry of Labour, Government of Ontario |

| Laurie Down | Canadian Life and Health Insurance Association |

| Herb Emery | School of Public Policy, University of Calgary |

| Patricia Emery | Social Sciences and Humanities Research Council of Canada |

| Adele Furrie | Adele Furrie Consulting |

| Rebecca Gewurtz | School of Rehabilitation Science, McMaster University |

| Joyce Gordon | Neurological Health Charities Canada, and Parkinson Society Canada |

| Kathryn Gregory | Sun Life Financial |

| Maureen Haan | Canadian Council on Rehabilitation and Work |

| Peter Hicks | Consultant |

| Sung-Hee Jeon | Statistics Canada |

| Elizabeth Kwan | Canadian Labour Congress |

| William MacMinn | Finance Canada, Government of Canada |

| Tyler Meredith | Institute for Research on Public Policy |

| Nancy Milroy-Swainson | Employment and Social Development Canada, Government of Canada |

| Denise Page | Canadian Cancer Society |

| Neil Pierce | MS Society of Canada |

| Wendy Porch | Canadian Working Group of HIV and Rehabilitation |

| Annette Ryan | Employment and Social Development Canada, Government of Canada |

| Susan Scotti | Canadian Council of Chief Executives |

| Nora Spinks | Vanier Institute of the Family |

| John Stapleton | Open Policy Ontario |

| Nicole Stewart | Conference Board of Canada |

| Catherine Suridjan | Canadian Caregiver Coalition |

| Emile Tompa | Institute for Work & Health |

| Sherri Torjman | Caledon Institute of Social Policy |

| Sarah Van Diepen | Privy Council Office, Government of Canada |

Based on Episodic Disabilities Network (2015).

Employment insurance system is heavily flawed (Windsor Star)

I’m writing in regards to a disturbing situation involving the practices of employment insurance. I have a long-term illness which is a series of pockets of remission followed by relapses.

This deters me from working continually at times, even though I still trudge along and sometimes take on other part-time jobs to supplement my income. By society’s standards, working against the odds to avoid being dependent on anyone or any system.

I went off work mid-May due to an “attack” as well as a back injury. I have not yet received a dime from EI, although I have provided all the necessary items.

It has recently been brought to my attention that the part-time job I had had for about six months, ending last October, was the reason for the delay. I quit because with my illness became too m–ch and was affecting my health, all the while working at my primary place of employment.

I do not think my “summer part-time position” should have any bearing on my claim now but oh, does it ever.

The government doesn’t want people on assistance but here I am working, sometimes two jobs, but when I get sick I can’t readily collect unemployment sick benefits. This system is heavily flawed and honestly, I wonder why I bother.

Good hard-working people overcome adversities only to get slapped in the face. I could easily go on disability but why should I?

Why should I take a lesser income?

MICHELLE BALDWIN, Windsor

(Baldwin 2013)

* * *

Interview with a family caregiver

“If you really need it financially, and you just have to get up and leave work, I mean…how are you going to survive getting through [the waiting period] without money?”

–family caregiver, interview from Evaluating Canada’s Compassionate Care Benefit from the Perspective of Family Caregivers,

(Williams et al. 2010)

Baldwin, W. (2013). “Employment Insurance System is Heavily Flawed: Letter to the Editor . The Windsor Star. July 4, 2013.

Bray, G.M., D. Strachan, M. Tomlinson, A. Bienek and C. Pelletier (2014). Mapping Connections: An Understanding of Neurological Conditions in Canada. Ottawa: Public Health Agency of Canada.

British Columbia Ministry of Social Development and Social Innovation (2015). “Earnings Exemptions.” Date modified: March 19, 2015. https://www.eia.gov.bc.ca/factsheets/2006/Earnings_Exemption.htm

Campolieti, M. and C. Riddell (2012). “Disability Policy and the Labour Market: Evidence from a Natural Experiment in Canada, 1998-2006.” Journal of Public Economics, 96(3-4): 303-16.

Canada (2015). Bill C-59, Economic Action Plan 2015 Act, No. 1. Part 3: Various Measures, Division 4 – Compassionate Care Leave and Benefits. Ottawa: Department of Finance Canada.

CIC (2015). “Labour Standards in Canada”. Date modified: 12 May, 2015. https://www.cic.gc.ca/english/work/labour-standards.asp. Date accessed: June 3, 2015. Ottawa: Citizenship and Immigration Canada.

CLHIA (2014). Facts and Figures: Life and Health Insurance in Ontario. Toronto: Canadian Life and Health Insurance Association. Date modified: March 19, 2015. https://clhia.uberflip.com/i/396037-life-and-health-insurance-in-ontario-2014-edition

Conference Board (2013a). Missing in Action: Absenteeism Trends in Canadian Organizations. Ottawa: Conference Board of Canada.

Conference Board (2013b). Disability Management: Opportunities for Employer Action. Ottawa: Conference Board of Canada.

Episodic Disabilities Network (2015). “Episodic Disabilities Network (EDN) Episodic Conditions List”. Toronto: Episodic Disabilities Network.

ESDC (2013). Summative Evaluation: Employment Insurance Premium Reduction Program, December 2009. Ottawa: Employment and Social Development Canada.

ESDC (2015a). Employment Insurance Monitoring and Assessment Report 2013/14. Ottawa: Employment and Social Development Canada.

ESDC (2015b). When Work and Caregiving Collide: How Employers Can Support Their Employees Who Are Caregivers. Ottawa: Employment and Social Development Canada.

Fowler, H.S. (2011). “Employees’ Perspectives on Intermittent Work Capacity: What Can Qualitative Research Tell Us in Ontario?” Report submitted to Human Resources and Social Development Canada. Ottawa: Social Research and Demonstration Corporation.

Furrie, A. (2015). “Identifying the population.” Presentation to IRPP Roundtable on Income and Employment Needs of Persons Dealing with Illness. June 17, 2015. Ottawa, ON.

Furrie, A. (2010). Towards a better understanding of the dynamics of disability and its impact on employment. Ottawa: Adele Furrie Consulting Inc.

Galarneau, D. and M. Radulescu (2009). “Employment among the disabled.” Perspectives on Labour and Income, May 2009, catalogue no. 75-001-X. Ottawa: Statistics Canada.

Gallipoli, G. and L. Turner (2011). “Household Responses to Individual Shocks: Disability and Labour Supply.” Canadian Labour Market and Skills Researcher Network, Working Paper no. 23.

Jeon, S.H. (2014). “The Effects of Cancer on Employment and Earnings of Cancer Survivors.” Analytical Studies Branch Research Paper Series no. 362. Ottawa: Statistics Canada.

Marshall, K. (2006). “On Sick Leave,” Perspectives on Labour and Income, April 2006, catalogue no. 75-001-XIE. Ottawa: Statistics Canada.

New York State Workers’ Compensation Board (n.d.). A Guide to Disability Benefits: Employee Benefits for Injuries and Illnesses off the Job in New York State. Albany: New York State Workers’ Compensation Board, Disability Benefits Bureau.

Ontario Ministry of Community and Social Services (2015). “ODSP: Information Sheet.” Date modified: February 12, 2015. https://www.mcss.gov.on.ca/en/mcss/programs/social/odsp/info_sheets/ employment_supports.aspx

OECD (2010). Sickness, Disability and Work: Breaking the Barriers, A Synthesis of Findings Across OECD Countries. Paris: Organization for Economic Cooperation and Development.

PHAC (2014). The Chief Public Health Officer’s Report on the State of Public Health in Canada, 2014: Public Health in the Future. Ottawa: Public Health Agency of Canada.

Poschmann, F. and Chatur, O. (2013). “Absent with Leave: The Implications of Demographic Change for Worker Absenteeism.” E-Brief (September 24, 2013). Toronto: C.D. Howe Institute.

Prince, M. (2008). Canadians Need a Medium-Term Sickness/Disability Income Benefit. Ottawa: Caledon Institute for Social Policy.

Schliwen, A., A. Earle, J. Hayes and S.J. Heymann (2011). “The Administration and Financing of Paid Sick Leave.” International Labour Review, 150 (1-2): 43-62.

Service Canada (2015). “Statistics Related to the Old Age Security Program and the Canada Pension Plan.” https://www.servicecanada.gc.ca/eng/services/pensions/statistics/index.shtml. Date accessed : June 2, 2015.

Stapleton, J. and S. Procyk (2010). “A Patchwork Quilt: Income Security for Canadians With Disabilities,” Institute for Work and Health. Issue briefing, November 2010.

————- (2013). The “Welfarization” of Disability Incomes in Ontario: What Are the Factors Causing This Trend? Toronto: Metcalf Foundation.

Statistics Canada (2013). “Disability in Canada Initial Findings from the Canadian Survey on Disability.” Fact Sheet. Catalogue 89-654-X no. 002. Ottawa: Statistics Canada.

Tomlinson, K. (2011). “Cancer patients lose EI during treatment: Lymphoma sufferer hit twice speaks out; thousands affected.” CBC. Date modified: April 19, 2011. https://www.cbc.ca/news/cancer-patients-lose-ei-during-treatment-1.1047165

Tompa, E., R. Sauders, and C. Mustard (forthcoming). “Impairment and work disability of workers’ compensation claimants in Ontario, a cohort study of new claimants from 1998-2006.” Canadian Institutes of Health Research, Operating Grant, 2013-2015.

U.S. Social Security Administration (n.d.). “Social Security Programs Throughout the World.” Accessed June 3, 2015. https://www.ssa.gov/policy/docs/progdesc/ssptw/index.html

Williams, A. et al. (2010). Evaluating Canada’s Compassionate Care Benefit: From Perspective of Family Caregivers. Hamilton: School of Geography and Earth Sciences, McMaster University.

Montreal – Gaps in insurance coverage, poorly coordinated income support programs, and an outdated approach to disability are leaving too many workers behind when they become sick. These problems will intensify as the workforce ages and episodic and chronic health conditions become more prevalent, argues a new report from the IRPP. A new approach is needed.

In any given year, 6 percent of Canadian workers will experience a personal health issue that will require them to adjust their work status. Authors Tyler Meredith and Colin Chia note that, without proper support, employers will face significant lost productivity costs, while workers and their families may see their standard of living fall.

Building on a roundtable discussion with experts convened by the IRPP, the report finds that close to half of the labour market is not adequately covered by private disability insurance. These workers must rely on public programs that are less generous, more rigid and less proactive to support a return to work than some private programs.

“This situation is neither fair nor effective if we are to support all Canadian workers in realizing their potential” say the authors. “It reflects problems of design, coordination and inflexibility, such that where one works and the nature of one’s impairment can dictate how effectively income and employment needs will be supported during illness.”

The report identifies a number of overlapping problems, including:

The authors argue that these problems cannot be resolved by any one level of government alone. What is required is a genuine process of engagement that brings together governments, employers and insurance carriers to revisit definitions of eligibility, and establish an integrated, comprehensive approach to address workers’ needs.

To help inform this process, the authors propose a series of short- and longer-term actions. For example, they urge the federal government to introduce employment support services to help facilitate a return to work through the EI sickness program, and, over the long term, potentially expand the program from 15 to 26 weeks of coverage (under certain conditions). Additionally, they say, the government should establish a centre of expertise to provide information and resources for employers when a worker experiences a health shock. Several knowledge gaps and research priorities are also identified.

Leaving Some Behind: What Happens when Workers Get Sick can be downloaded from the IRPP’s website (irpp.org).

-30-

The IRPP thanks the MS Society of Canada, the Canadian Cancer Society and the Canadian Caregiver Coalition for their financial support in organizing the roundtable discussion.

The Institute for Research on Public Policy is an independent, national, bilingual, not-for-profit organization based in Montreal. To receive updates from the IRPP, please subscribe to our e-mail list.

Media Contact: Shirley Cardenas tel. 514-594-6877 scardenas@nullirpp.org

Child benefits, income splitting, pensions, flexible work arrangements and compassionate care leave—this federal election is putting social policy in the window. But if we are going to have a much-needed conversation about how Canadians are dealing with the various demands of work, care, and aging then we are missing one very big element: what happens to you if you get sick.

By this, I am not referring to the health care system, but rather: what happens to your job, your income and your family’s standard of living if you become ill?

This isn’t a trivial question. In a given year, approximately six per cent of Canadian workers are forced to change their work status due to a personal illness or disability, either taking an extended leave from work, changing the number of hours they work, or leaving the labour market entirely.

Getting sick is a risk we all face. But, what happens to you in such a situation depends very much on where you work and who you work for.

First, there is a huge discrepancy between provinces in terms of the minimum amount of time employers must offer in terms of sick leave (almost uniformly unpaid). This can range from no entitlement in provinces like Alberta, to as much as 26 weeks in Quebec. Many employers accommodate employees with paid or unpaid leaves greater than the minimum required under labour law, but the point is that we have no common baseline.

Second, how much income and employment support you would receive during the period of illness is unclear. Canada’s approach to sickness and disability insurance assumes that all workers should be privately insured, and that private insurance will be the first payer before any public support program. While this is a perfectly acceptable approach, many workers are not adequately insured.

As of 2013, about 44 per cent of workers were not enrolled in a private, long-term disability benefit plan. As with pensions, group benefits and other characteristics of a “good job,” coverage for disability insurance varies significantly between those working full- and part-time, for large and small employers, and in high- and low-wage industries.

Though not without its own problems, private disability insurance often provides a higher level of income replacement and a wider suite of support services than is typically available in public programs. Unbeknownst to many, the sickness benefit offered under Employment Insurance (EI) only provides 55 per cent wage replacement, lasting no more than 15 weeks. Moreover, EI offers no active employment supports to help you or your employer ease your transition back to work; if you work even intermittently, every dollar you earn will be clawed back.

Aggravating this situation are other serious problems, including a significant lack of coordination from one program to the next, and an outdated concept of disability around which parameters of eligibility are set.

Approximately one in three workers who go on EI sickness benefits exhaust their claim after 15 weeks. Assuming their illness isn’t severe or prolonged enough to qualify as a permanent disability (think of someone with a cancer diagnosis) the worker likely won’t be eligible for the Canada Pension Plan Disability benefit. If they don’t have private LTD, three options remain: seek a paid leave from their employer; draw down on personal savings; or apply for general welfare. To these workers, we are saying, in effect: you are sick but not disabled enough.

Failing to properly support workers and employers to navigate the difficult circumstances presented by an illness has long-term consequences. Emerging evidence from the related field of workplace injuries suggests that the drop in earnings and employment experienced by an affected worker is often disproportionate to the level of impairment.

he costs are broader still. In 2010, Canadian governments and insurance carriers spent nearly $30 billion in direct financial assistance to persons and families who got sick. Billions more are forgone in lost productivity, while, at a personal level, many families cope with the pressures of care and work.

In an aging population we can’t afford to ignore these issues. If good social policy is good economic policy then we need to hear from all of the political parties about how they propose to fix Canada’s system of sickness and disability supports.

Tyler Meredith is a research director at the Institute for Research on Public Policy, and co-author of the recently released paper, Leaving Some Behind: What Happens When Workers Get Sick.