Parental Benefits in Canada: Which Way Forward?

Jennifer Robson

While Canada’s education and training system does a fairly good job in producing highly educated workers, often it does not provide sufficient support to meet the learning needs of adults who may be working but require a “second chance.”

In this study authors Torben Drewes and Tyler Meredith find that although investments in education undertaken earlier in life generally provide a higher payoff, returns to education and training appear to remain positive up to age 40. This suggests a considerable portion of Canada’s labour force might benefit from improved access to learning later in life, including the 1 in 7 working-age adults who report having insufficient qualifications for their current job, and the 1 in 5 who lack basic literacy and numeracy skills.

Why, then, do more adults who might benefit from learning not undertake it? An important reason, note the authors, is the difficulty of balancing responsibilities for care and work, and the consequently high opportunity costs of time. In addition, behavioural science suggests some adults, particularly those with low skills, appear to be more risk-averse in the presence of an unknown outcome, a potentially high barrier when one considers the time and money involved.

Instead, those most willing to take this leap are often the higher-skilled. In 2011, Canada’s highest-skilled adults were five times as likely to participate in job-related learning than the lowest-skilled. This differential is among the highest in the OECD.

While financial barriers are not a major constraint, they can matter. As a result of age-based grants, expectations for spousal contributions, and the treatment of household assets, many of the programs in Canada’s student financial assistance system are heavily skewed toward younger learners. The authors present the examples of two fictional Ontario families with similar income and asset profiles to show how the proportion of financial need covered by the aid package can vary between young and mature students by a factor of two or more.

Perhaps most critically, the authors say the market for adult learning through apprenticeships is broken. Completion rates are low, the need for essential literacy and numeracy training is high, and the capacity of employers to train is limited. As the skilled trades are among the largest source of learning for older adults, this is an area of particular concern.

Addressing these challenges will take more than just modest adjustments to existing policies. Drewes and Meredith call for an ambitious pan-Canadian adult education and training strategy centred around three key reforms: 1) Improving labour market information and research to better understand the unique needs of adults, including the development of a permanent adult education and training survey; 2) Developing a comprehensive, income-contingent loans system targeting older adults; and 3) Overhauling provincial apprenticeship systems to make the learning process and the capacity of training institutions more similar to those in the post-secondary education system.

Investment in human capital has always been essential to Canada’s economic prosperity, but education and training will be especially important in the coming years. Over the next decade, Canada will be subject to a combination of demographic forces: population aging and slower labour force growth. As Halliwell has noted, increased immigration flows will do little to offset these significant forces (2013). We must therefore improve labour productivity simply to sustain our current standards of living.

Canada’s labour force is already highly skilled — among the member countries of the Organisation for Economic Co-operation and Development (OECD), Canada has the highest proportion of workers who have completed some form of post-secondary education (PSE) (college or university) (OECD 2013a). Nevertheless, there could be large numbers of people who would benefit from learning later in life. This could include workers who did not enrol in PSE programs earlier in life, were unable to complete them or did not choose the right form of education for success in the labour market. Workers who fit into any of these three categories still have the potential to make a meaningful contribution to overall productivity growth if they can move up the skills ladder by acquiring new credentials or education. In this context, there have been calls for Canada to formalize the availability of long-term training supports for working-age adults. Such efforts range from the adoption of a formal second-chance system for those lacking foundational skills (OECD 2013a), to efforts by the federal government to expand access to workplace training (for example, the Canada Job Grant program), to, more recently, a proposal floated by the Leader of the federal Liberal Party to offer adults access to their own version of the Registered Education Savings Plan (RESP) (Wells 2014).

Though each of these ideas targets a different issue, all are concerned with how workers develop skills over the course of the many decades following graduation. For its own part, the OECD has been especially vocal in insisting that continuous reinvestment in skills development is essential for productivity and for adapting to the shift to a knowledge-based economy (OECD 2004). While Canada’s labour market has demonstrated a high degree of job stability in recent decades (Morissette, Lu and Qiu 2013), rising demand for cognitive skills has increased the skill content of work (Plesca and Summerfield 2014). In theory, this suggests the importance of offering training to two groups: the involuntarily unemployed who need to change jobs midcareer, and the low-skilled who want to move up in the labour market.

As greater policy attention shifts toward supporting education and training for older adults, a critical question that policy-makers must ask is whether such investments will be productive. Over the last several decades, there has been an extensive and exhaustive examination of the outcomes of formal schooling among youth, one that pays close attention to how individual choices are made and the complex statistical issues involved in measuring the causal effects of schooling. With some exceptions (see, for example, Carneiro and Heckman 2003), the economics of adult learning have not been critically examined with the same level of analytical or empirical care. There is, for example, a presumption that adult learning will raise the skill level of adults with too little education; it is taken as an article of faith that such human capital investment will have a positive rate of return. However, in such cases we must question whether the second chance will be stymied by the same factors that prevented success the first time around.

To fill these important knowledge gaps, we review what is known (and still unknown) about formal adult learning in Canada with an emphasis on establishing the need and appropriate role for public policy. In particular, we seek to identify the population of adult learners who might benefit from additional education or training and to determine how large these benefits might be and how the payoff changes with age. What unique barriers and challenges do adult learners face? And how should public policy-makers think about the balance between work, life and the financing constraints facing adults who are still working? To support this analysis, we begin with a brief review of the theory of human capital, discussing how the benefits of learning should be understood and analyzed within this framework.

It is important that we define adult education and training. Our focus here is on formal learning that occurs after the age at which most Canadians have entered the workforce — approximately 25.1 We refer to investments leading to certified skills acquired either through education (that is, skills acquired outside the workplace) or training (courses or formal training delivered in the workplace). This includes learning that occurs in the formal PSE sector, as well as apprenticeship (which involves on-the-job learning) and employer-sponsored training. In keeping with the scope of this paper, we focus primarily on PSE and apprenticeship training, as these generally lead to formal certification.

Why and to what end should adults pursue education and training later in life? How might we think about the different effects that educational investments would have for learners over different stages of the life course? To provide a useful framework for analyzing these questions, we start with a brief examination of what economic theory tells us about adult education and training.

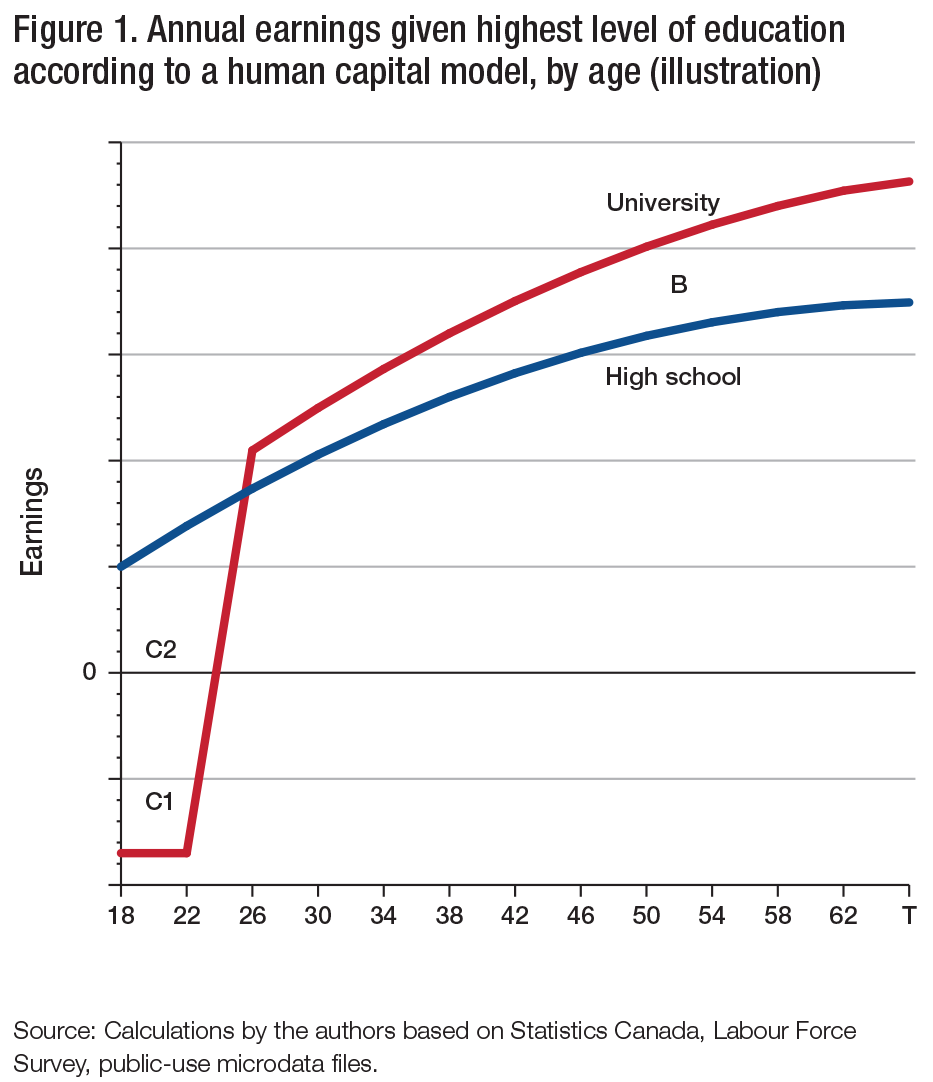

Arguably the most significant and pervasive economic theory of education is Becker’s human capital model (1964). Consider an individual leaving high school at age 18 who must choose between undertaking a four-year post-secondary degree or directly entering the labour market. Figure 1 plots the hypothetical annual earnings profiles associated with each choice. The human capital model envisions the individual comparing the benefits of that four-year investment (the increased earnings in area B) against the costs, which include both out-of-pocket educational expenses such as tuition and books (area C1) and the earnings forgone as a result of not working during those four years (area C2). Because the benefits accrue for many years after the costs have been incurred, the comparison must be made in the same way that investments in physical capital are considered, using either present values or internal rates of return. This is very different from simply comparing differences in earnings (often referred to as the “earnings premium”) across education and occupation pathways.

Although simple, this model provides multiple insights. For example, using Canadian data on earnings, tuition costs and expected length of working life, the human capital model shows that, despite significant differences in lifetime earnings,2 the internal rates of return are quite similar between college and university,3 reflecting differences in years to completion and direct and indirect costs between these two PSE pathways.

In the context of adult learning, the model reveals an important relationship between age and outcomes. All things being equal, the earlier an investment in education is made, the better. Rates of return on an investment in education will be sensitive to a number of factors, including the opportunity cost of employment later in life and the number of years one has to recoup the investment. This is not to say that upgrading skills later in life won’t generate positive returns; it simply means that the rate of return on such investments will likely change over the course of a person’s life. How this plays out is a critical question, and one that this paper seeks to address.

In evaluating the returns to education, we must take into consideration that costs and benefits will appear in a number of forms, and they will be spread in several directions across society.

The economic importance of education is obvious at both a micro and a macro level (Krueger and Lindahl 2001). A large body of evidence shows that human capital is a key determinant of the income and productivity generated by individual workers and, in aggregate, a country’s economic growth (Krueger and Lindahl 2001; Coulombe, Tremblay and Marchand 2004; Murray and Shillington 2011). A much smaller literature also shows that compared to lower-skilled workers, workers with higher levels of education enjoy greater occupational mobility; have a lower risk of unemployment and job displacement; exhibit higher levels of civic participation and a reduced dependency on social assistance and welfare; and have better health outcomes (DeClou 2014).4

How the returns to education and training are distributed between individuals, employers and society is an important consideration for public policy. If most benefits from higher learning are privately held, then policy should seek to allocate the costs of education to the individual student, and vice versa. It is often argued that employers will only invest in the learning and educational development of workers to the extent that the learning is job-specific and gains in productivity can be retained within the firm. If learning is too general in nature, then -employees are entirely free to take human capital with them elsewhere in the labour market and firms will not have an incentive to invest. When we consider the role of employers in apprenticeship training — arguably a form of general learning that happens to take place in the workplace — we see that this theory has significant implications.

Though there are few studies that examine the size of both public and private returns specific to adult education and training, the literature on younger learners suggests that private and social returns are of approximately equal magnitude (Riddell 2004; Riddell and Song 2009). For reasons demonstrated later in this paper, we believe that this finding likely also applies to adults.

On a final note, it is important to appreciate the way in which higher education and the benefits it produces are leaned on as policy tools. Where higher learning produces a positive return on investment, it is possible that access to PSE will worsen income inequality within society to the extent that it accentuates earnings gaps between individuals, reinforces parental education patterns or creates new demands for technological change that leave lower-skilled workers behind (Foley and Green 2015). For those who do go on to obtain these credentials, such education may, however, act as an important gateway to social mobility. These two very different outcomes for social policy need to be carefully weighed by policy-makers as they think about and design incentives for human capital development.

It is often said that Canada lacks a “culture of lifelong learning” (Goodale 2015). This viewpoint holds that Canada’s education and training system places far too much weight on the development of skills in the early stages of life without adequate investment to help workers replenish their skills and develop new ones once they begin working (CCL 2010, 2011).

Were this statement true, Canada would rank relatively low internationally in terms of providing access to learning for its working-age population, and we would observe fairly limited growth in educational attainment once workers reached the age (approximately 25) at which most careers begin. However, neither is the case.

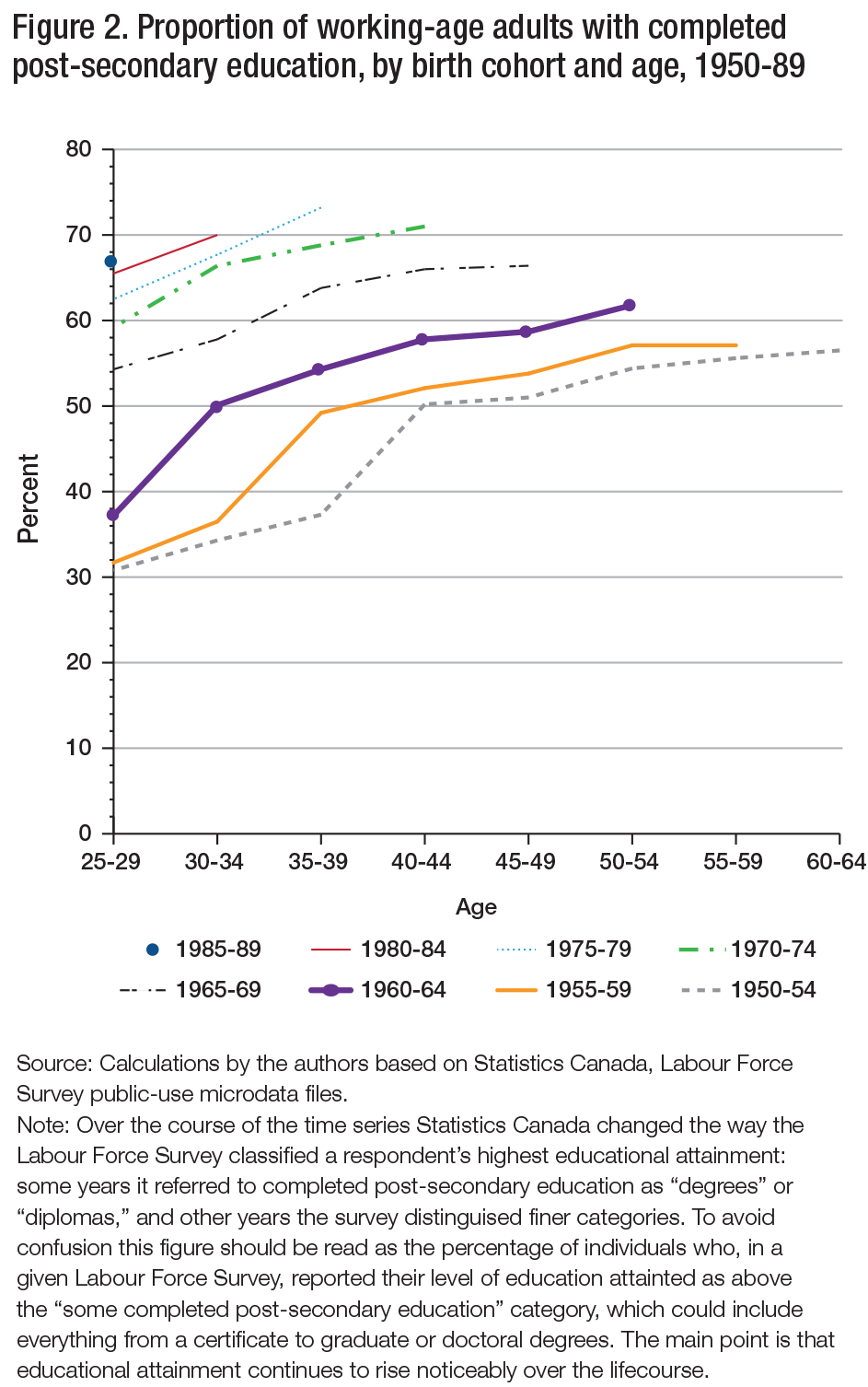

The significant rise in educational attainment that Canada has experienced in recent decades has occurred across all age groups and birth cohorts, a fact that underscores the importance and the impact of education and training among adults (figure 2).

To put this in perspective, PSE attainment among baby boomers born between 1950 and 1960 rose by more than 25 percentage points over the course of their working lives, from age 25 on.

As shown in figure 2, much of the increase in educational attainment among these cohorts occurred during the 1980s and 1990s, a period that was also marked by a substantial increase in female labour force participation and major changes in technology and industry. Adult education and training likely played a crucial role in facilitating broader labour market adjustment. The change in the age profile of PSE attainment has been flatter in subsequent cohorts, although this is likely because incoming youth are increasingly more highly educated.

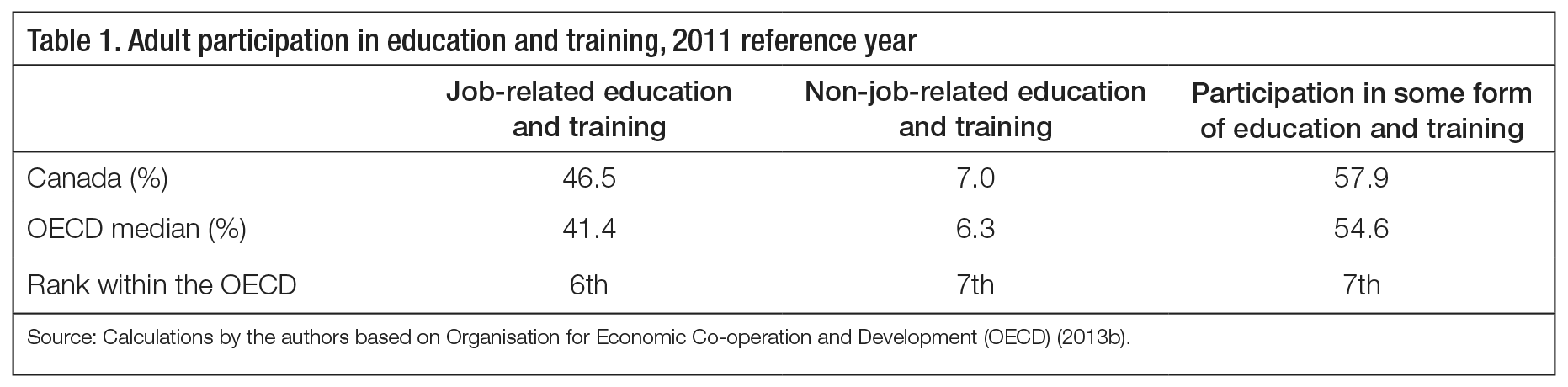

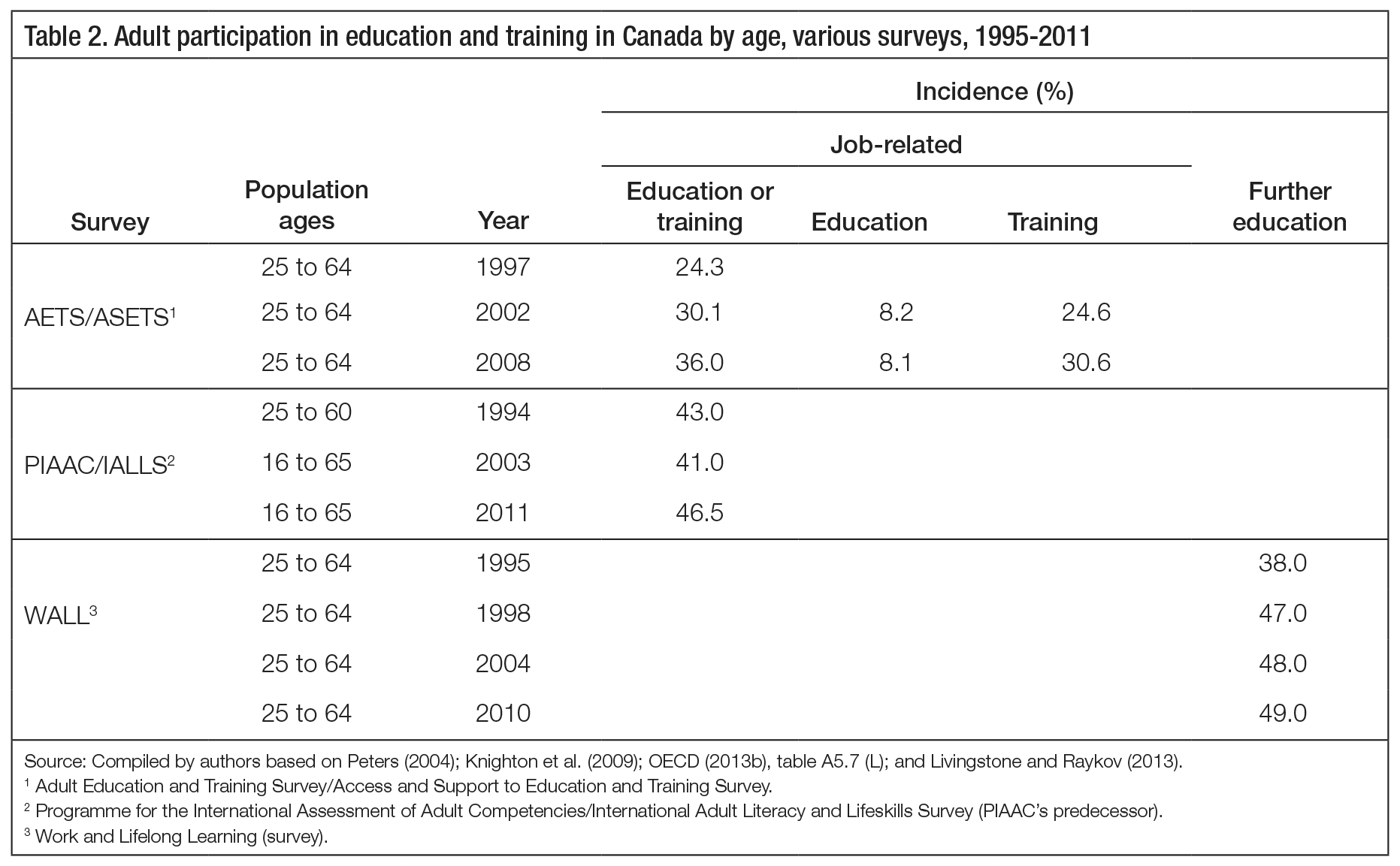

Similar to the gains in credential attainment, participation in ongoing learning activities, both within and outside the workplace, has been robust. While Canada is slightly below the OECD average in providing noncredential training within the workplace (Munro 2014), data from the 2011 Programme for the International Assessment of Adult Competencies (PIAAC) suggest that we rank approximately seventh among OECD member countries in terms of our proportion of working-age adults who participate in all forms of education and training, and sixth in terms of our proportion of working-age adults who specifically pursue learning that is job-related (table 1). The latter learning includes all forms of skill development that participants identify as being motivated by reasons related to current or future employment. Job-related learning can occur either in the classroom or in the workplace, and it can be sponsored by an employer, government or the individual learner.

While Canadian and international surveys vary in how they define and track learning activities, there is a fairly consistent upward trend over time across all measures of participation in education and training (table 2). In a given year, 40 percent or more of Canada’s working-age population is engaged in some form of education or training.

Most of this learning is short-duration training of about 50 hours per year, per worker (Knighton et al. 2009), and it is conducted outside of traditional PSE institutions. Though workers are less likely to undertake a formal credential program as they move from the early stages of their careers to the midpoint, their participation in job-specific training remains relatively high for most of their working lives. In a way, this is to be expected, given the significant differences in cost and time commitment between on-the-job training and more substantive investments in human capital, such as a degree or certificate program offered by a college or university.

Not immediately visible within these figures is the significant contribution that Canada’s apprenticeship system makes to the human capital development of adults. Despite the fact that much of the public discourse promotes apprenticeship as an alternative educational pathway for youth, apprenticeship training has long been a source of second-chance learning for older workers (O’Grady 2007). In 2012, the average learner entering an apprenticeship program was 28 years old (table 3). This age profile has remained relatively stable over the last two decades, even as the number of people entering apprenticeship programs each year has more than tripled.5 Since most apprenticeship programs require a minimum of four years to complete, the average age of all registered apprentices currently training in Canada is likely close to 30, or in the early 30s.

As a source of learning, Canada’s apprenticeship system represents an order of magnitude roughly equivalent to the college sector. In 2012, a total of 444,672 workers were registered as ongoing apprentices; this compares to the 527,433 students who were enrolled in colleges during the 2011-12 academic year.6

One conclusion we can draw from this high-level portrait it is that Canada does not suffer from a gross undersupply of education and training opportunities for adult learners. In the aggregate, Canadians engage in a fair amount of learning activity over their working lives — far more than our policy discourse would suggest.

While this may put to rest the notion that Canada is at a particular disadvantage in relation to its global competitors, the question now turns to adult learning itself. Is there enough of it to meet the demand? Does it actually raise productivity and incomes in the same way learning undertaken earlier in life can? Does it effectively promote the social policy objectives of equity and equality of opportunity?

The incessant focus by policy-makers on the quantity of learning that takes place has, for both young and older learners, obscured a number of more systemic challenges lying below the surface of Canada’s education and training system. For working-age adults, these challenges are even more pronounced, given that many must balance the competing pressures of learning, work and family. Here, we briefly review the source and extent of these challenges.

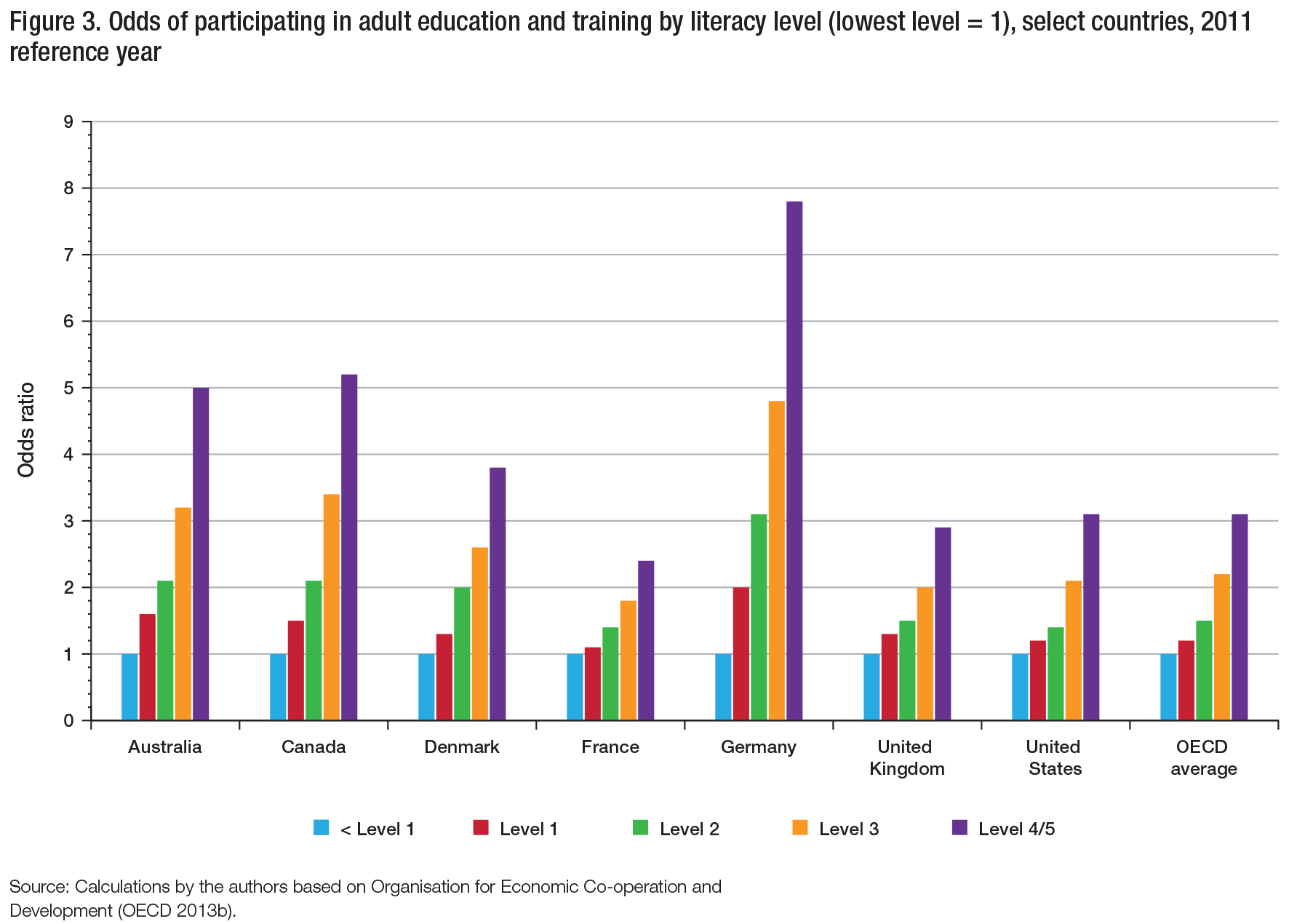

The basic and inescapable fact about adult education and training is that it is most often demanded by and afforded to those who already possess high levels of human capital (Halliwell 2013; -Desjardins 2011). Though this applies in almost every country, Canada exhibits some of the highest differentials in the OECD between the participation in learning of the lowest-skilled and highest-skilled workers (figure 3). In 2011, Canadians who had a level 4 or 5 literacy score (the highest scores) in the PIAAC were five times more likely (an odds ratio of 5) to participate in learning activities than those who scored below level 1 (the lowest score) (see box above for an explanation of odds ratios).

Unfortunately, the inequality in training participation observed in figure 3 is not new. Looking at working-age adults between 2002 and 2007, Drewes found that participation in adult education and training was highly correlated with an individual’s prior education level (2010). In general, college and university graduates are far more likely to engage in further education and training in their adult working lives than those who did not complete PSE or high school. To quote an earlier, but equally relevant finding from Gower: “Adult education does not seem to be the chosen means for reducing economic inequality. People who go back to school are largely already in favourable economic circumstances” (1997).

While these results serve as a cautionary note about how access to learning should be designed, the fact that a more equal distribution of educational participation has not occurred is itself a compelling case for policy reform. If we are to rely on learning as a pathway to successful economic adjustment and to a second chance later in life, then we must offer access to learning to those who need it most.

To the extent that Canada has thought about second-chance learning, most researchers and policy-makers have focused attention on the small population of individuals who do not complete high school (Finnie, Laporte and Sweetman 2010). While a high-school certificate is vital to future employment and income prospects, one has to question whether this credential is still a useful proxy for the basic floor of skills that workers are expected to possess in the labour market today. Increasing demand for labour in middle- and high-skilled jobs would suggest that this is at best a limited indicator of the type of training and education one may need later in life.

The point here is not to debate what the optimal level and mix of credentials should be within society, but rather to illustrate that skills upgrading is likely to be generated from a number of directions. This upgrading can be motivated by a desire to obtain prerequisites for career progression, change occupations in order to pursue better employment or achieve higher income, or retrain due to unemployment or a shift in technology.

It is impossible to quantify precisely all of the circumstances that might lead an individual to want or need skills upgrading. That being said, there are three indicators that can help us to illustrate the scope of a more formalized second-chance system. These indicators are related to separate and potentially overlapping issues in the labour market, and each affects labour productivity to a different degree.

The first and most obvious group that could benefit from a second-chance system is people with low or inadequate skills. It is ironic to note that although Canada boasts one of the highest rates of attained PSE, a substantial portion of working-age adults scores near the bottom on international assessments of literacy, numeracy and information-processing skills. For example, approximately 17 percent of Canadian adults rate at or below level 1 literacy, while 22 percent rate at or below level 1 numeracy (both are measured on a scale of 5) (Hango 2014).7 This compares to the OECD average of 16 and 19 percent, respectively (OECD 2013b).

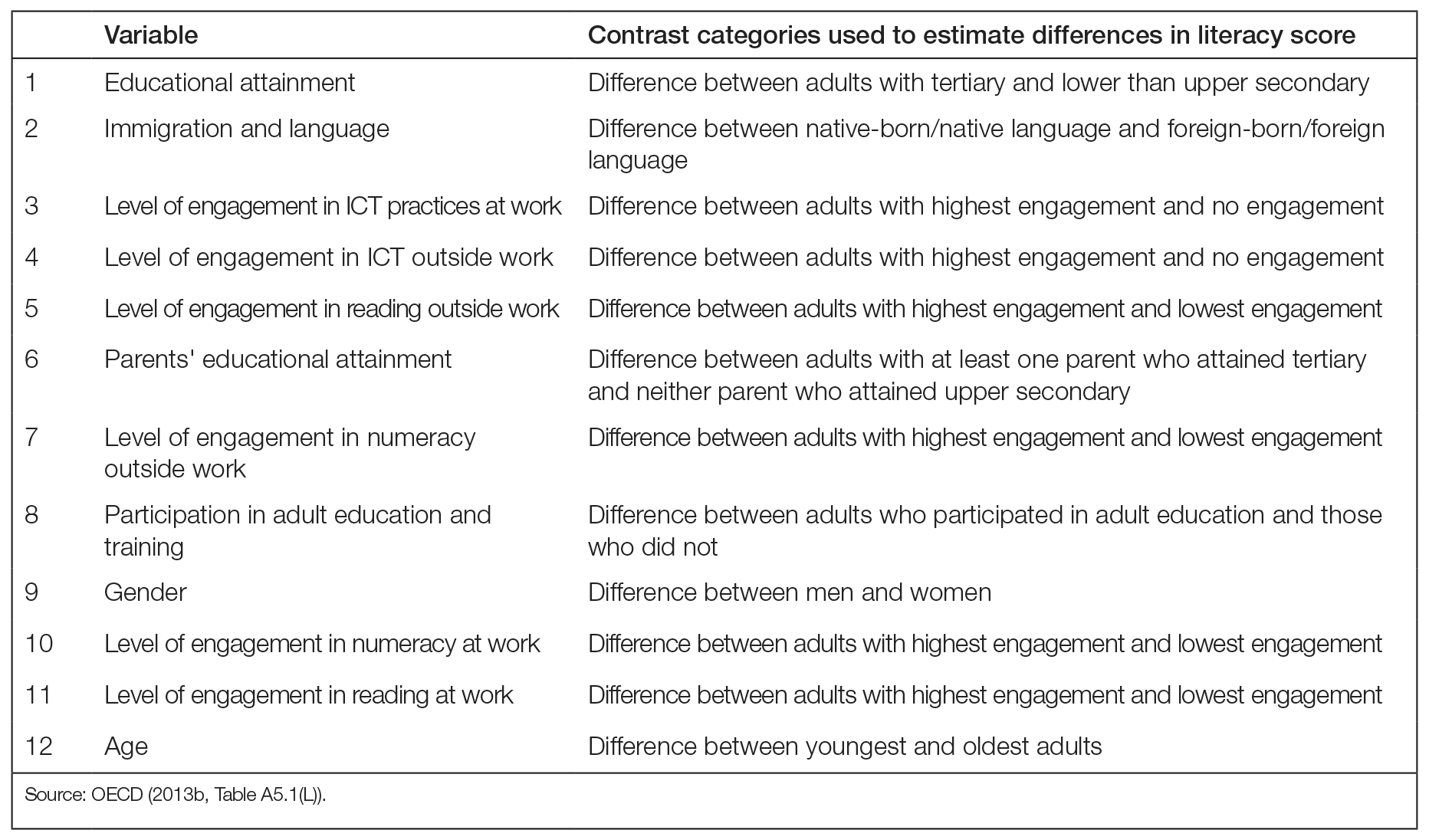

Though essential skills such as literacy and numeracy are inherently different from the technical skills embedded in formal credentials, analysis by the OECD suggests that the formal education system can play a significant role in helping to close these skills gaps (figure 4). Of 12 variables tested by the OECD, educational attainment had by the far the most direct and positive relationship with the literacy performance of Canadian adults. This analysis implies that a Canadian adult who has completed a PSE credential would, on average, score 36 points higher on literacy tests than someone who has not completed high school. The fact that educational attainment provides a much stronger explanation for differences in literacy than participation in adult education and training reinforces the point that existing training opportunities are inequitably distributed within the labour market.

Approximately 15 percent of Canadian adults report being underqualified for their current job (OECD 2013b, figure 4.25b). Here, again, Canada is somewhat above the OECD average (13 percent). The extent to which this group (people who lack technical certification) overlaps with people who score lowest in terms of literacy and numeracy skills, is unknown. Though members of the first group are probably somewhat more highly educated than members of the second, they are likely at greater risk of job loss or having limited employment prospects as technology and skill demand continue to change.

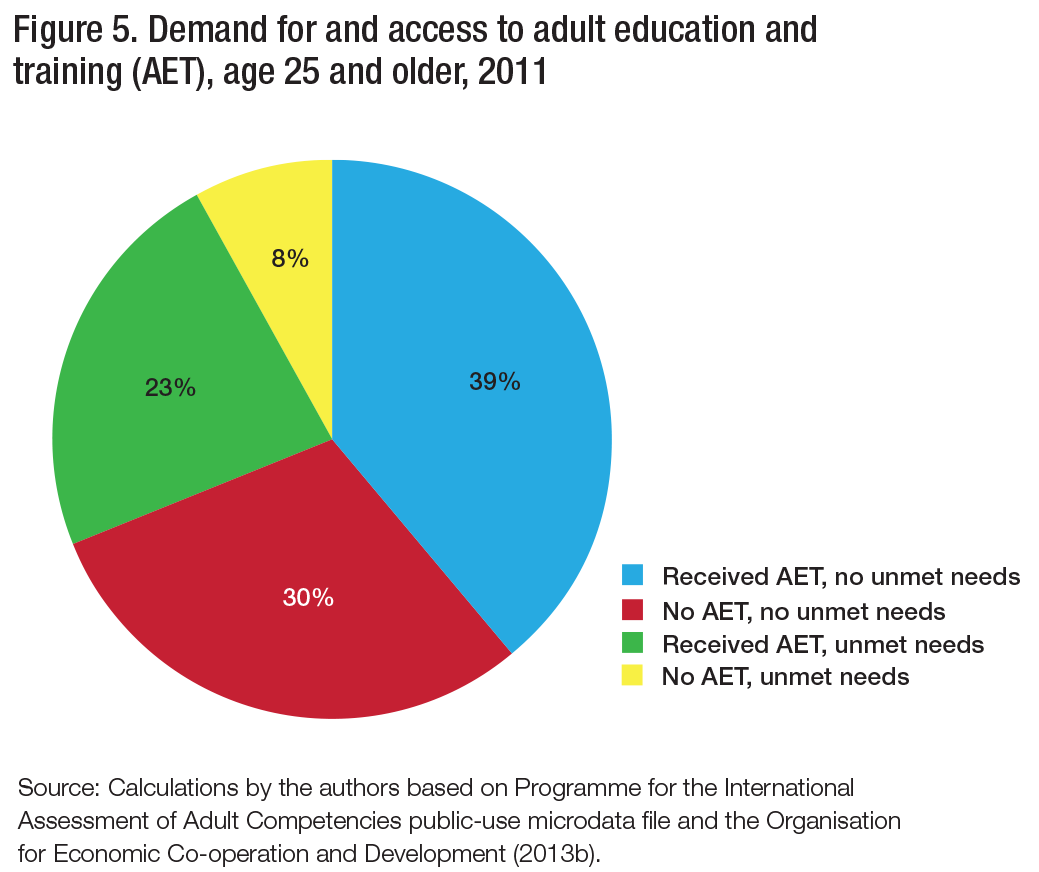

It is interesting to note that in contrast to these two measures of presumed need, a much larger portion of workers, approximately 31 percent of those age 25 and older, reported a need for learning that was not fulfilled in 2011 (figure 5). This is up from 26 percent in 2003 (Peters 2004). Consistent with the stylized fact that learning begets learning, approximately 40 percent of -respondents with a university degree reported an unmet need, compared with 21 percent of those who had completed high school or less.

The 31 percent of learners who did not receive training can be categorized into two sets: those who desired more training and received at least some (23 percent of all adults); and those who wanted to learn but did not participate in any learning activity (8 percent of all adults). Though the second set represents only one-third of those who reported an unmet need, past research suggests that they are most often individuals who have not completed PSE (OECD 2013b, table A.7a).

Taken together, these three data points suggest that there remains an important need for additional learning, primarily among those who lack essential skills and those who do not receive any training at all — groups that are, to a certain extent, one and the same. Though precise estimates are difficult to come by, the data lead us to believe that at least one in five working-age adults could benefit from skills upgrading of some kind. Given the current landscape of adult learning, it is likely that this group would benefit more from learning within the formal education sector than from training in the workplace.

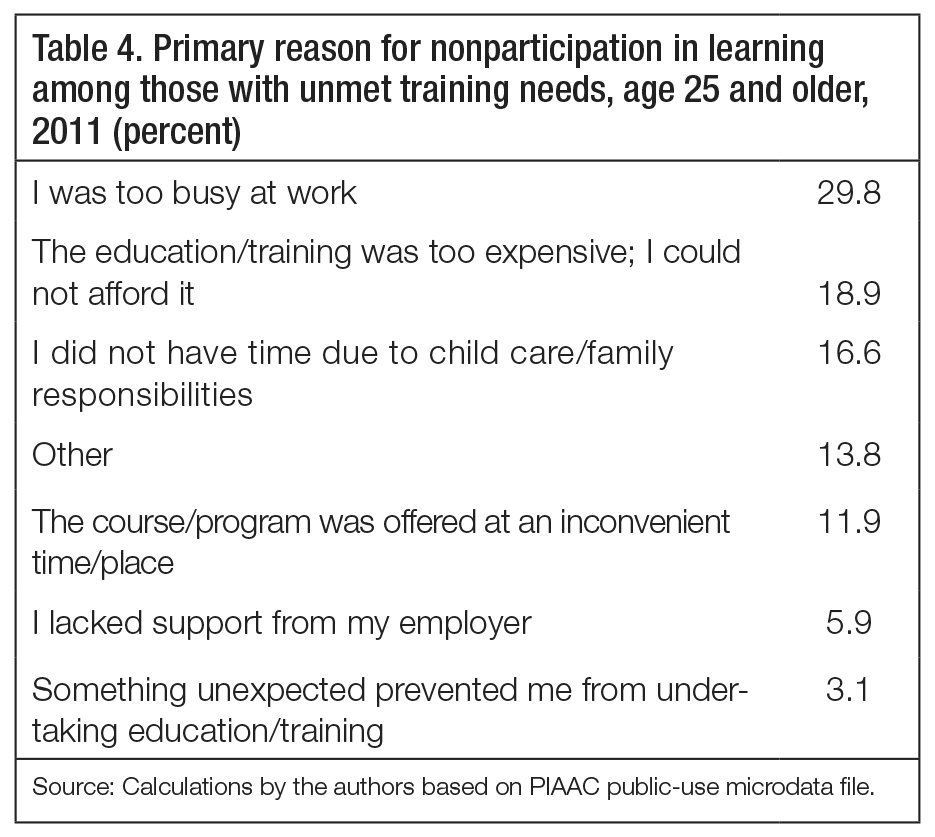

In order to create public policy that will increase opportunities for skills upgrading, we must first understand what, if any, barriers prevent adults from undertaking more learning. Consistent with the findings of a number of previous studies (Peters 2004; Knighton et al. 2009), those who reported an unmet training need in 2011 were predominantly discouraged from undertaking additional learning due to competing pressures of work and family life (table 4). The inability to arrange learning opportunities with the support of their employer or to find the time to undertake learning during the workweek was cited by a combined 36 percent of respondents. A further 17 percent of respondents noted the lack of time due to responsibilities at home as the primary reason they did not embark on learning. Just under one in five said the learning they desired was too expensive for them.

Because of differences among various surveys, it is not possible to directly assess how barriers to participation have changed over time. However, a large body of research has shown that what holds working-age adults back from undertaking additional learning is primarily a function of the opportunity cost of time. This underscores an important distinction between the life context of adult learners and that of youths, who at 17 or 18 generally have not yet formed families or started careers.

The difficulties that some workers presumed they would encounter in attempting to balance learning and working are an important consideration for policy. There is some evidence to suggest that older adult learners who stay with the same employer while obtaining certification achieve a higher earnings premium postlearning compared to those who switch occupations (Zhang and Palameta 2006). The ability to arrange education and work jointly is therefore essential.

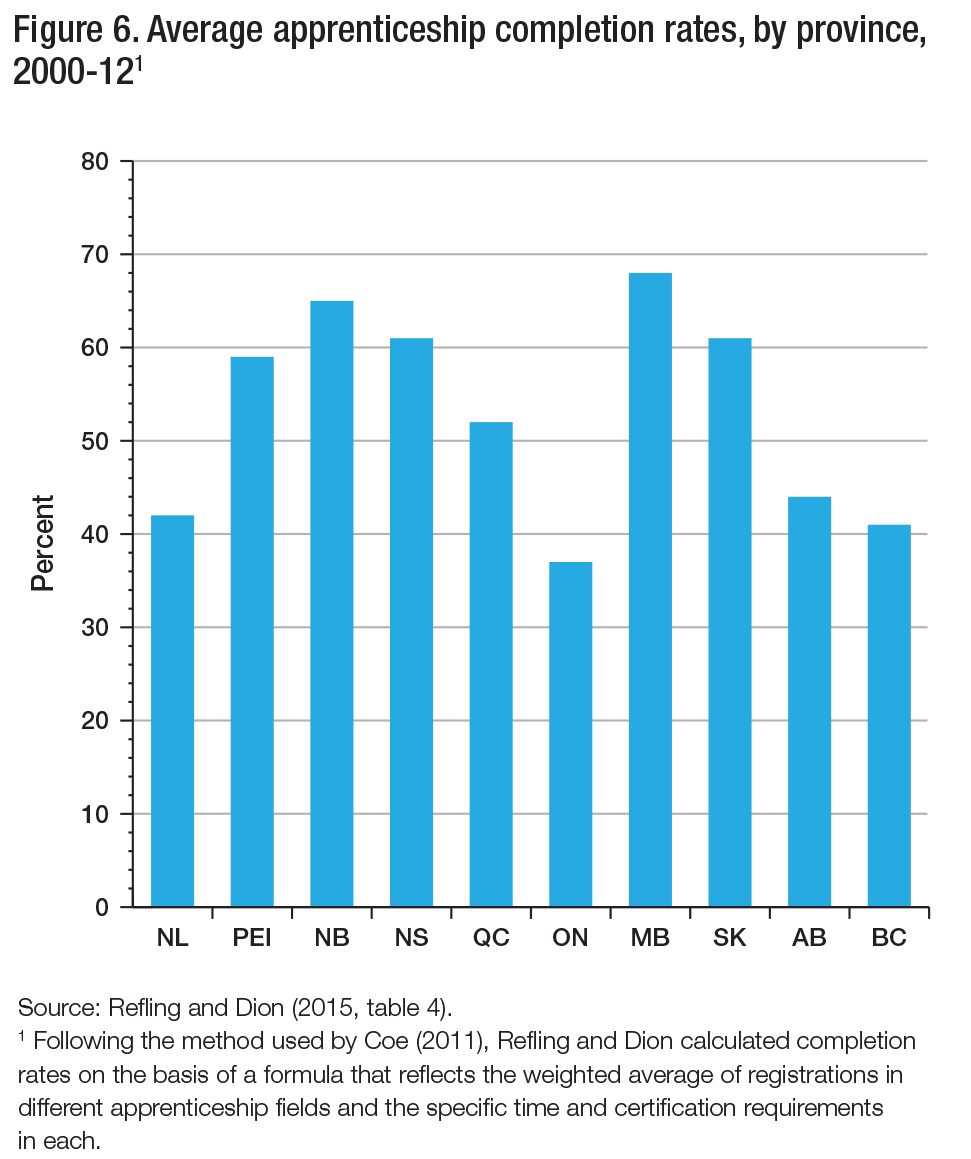

Perhaps one of the greatest and least discussed challenges facing Canada’s adult education and training system today is the basic dysfunction within one of its largest source components for learning — apprenticeship. Though the skilled trades have the potential to offer highly rewarding employment, training programs in most provinces are failing to ensure that apprentices are able to complete their training in a timely and efficient manner (figure 6).

The significant gap between the number of individuals who start an apprenticeship and the number who attain certification is alarming. Between 1991 and 2012, new apprenticeship registrations more than tripled, while completions doubled.8 Coe estimates that, consequently, the national completion rate across a subset of trades, accounting for 75 percent of all registrations, fell from 54 to 35 percent between 1991 and 2006 (Coe 2011). Any learning system that graduates less than half of a given year’s cohort should be considered broken.

We should note that completion rates have recovered somewhat since Coe’s analysis was performed, and variation among provinces is quite significant (figure 6); however, Canada’s apprenticeship system is still plagued by a number of endemic problems and inefficiencies, making it difficult for learners to navigate the learning pathway in a timely manner. These problems include an incoherent role for training institutions; a haphazard approach to voluntary versus mandatory certification requirements across trades (Refling and Dion 2015); and a low participation rate on the part of employers, estimated at 19 percent (CAF 2011a). The Canadian Apprenticeship Forum has also noted that many prospective apprentices come to the trades with poor literacy and numeracy skills, which raise obvious barriers to successful and timely certification (CAF 2011b). This only reinforces the need for a more systematic pedagogical approach.

Fixing apprenticeship training is therefore critical to any effort to improve the accessibility and effectiveness of second-chance learning. Doing so will yield important benefits for apprentices of all ages, but especially for the majority — older adults who have fewer working years left to recoup their investment in learning.

Adapting Canada’s adult learning system so that it better responds to the need for second-chance opportunities will require a combination of fixes that permit more focused access for those in need, as well as specific reforms to the ways in which learning is delivered. Before assessing how such reforms can best be put into action, we must answer a broader question: How, and to what extent, will investments in education remain beneficial for individuals and society as workers age? The answer to this is critical to determining precisely what kind of second chance the learning is likely to produce.

As we cautioned at the outset of this paper, the evidence on the earnings and employment effects of adult education and training is relatively thin compared to the evidence on education and training for youth. However, research on the US labour market has shown that the long-term earnings profile following the completion of a college or university program is generally comparable across graduates, regardless of age (see Leigh and Gill 1997; Jacobson, Lalonde and Sullivan 2003).9

While this gives us a general sense of the premium associated with higher learning, it does not tell us anything about how the rate of return to education would change based on such things as the age at which studies are undertaken, and the value employers attach to work experience accumulated prior to going back to school.

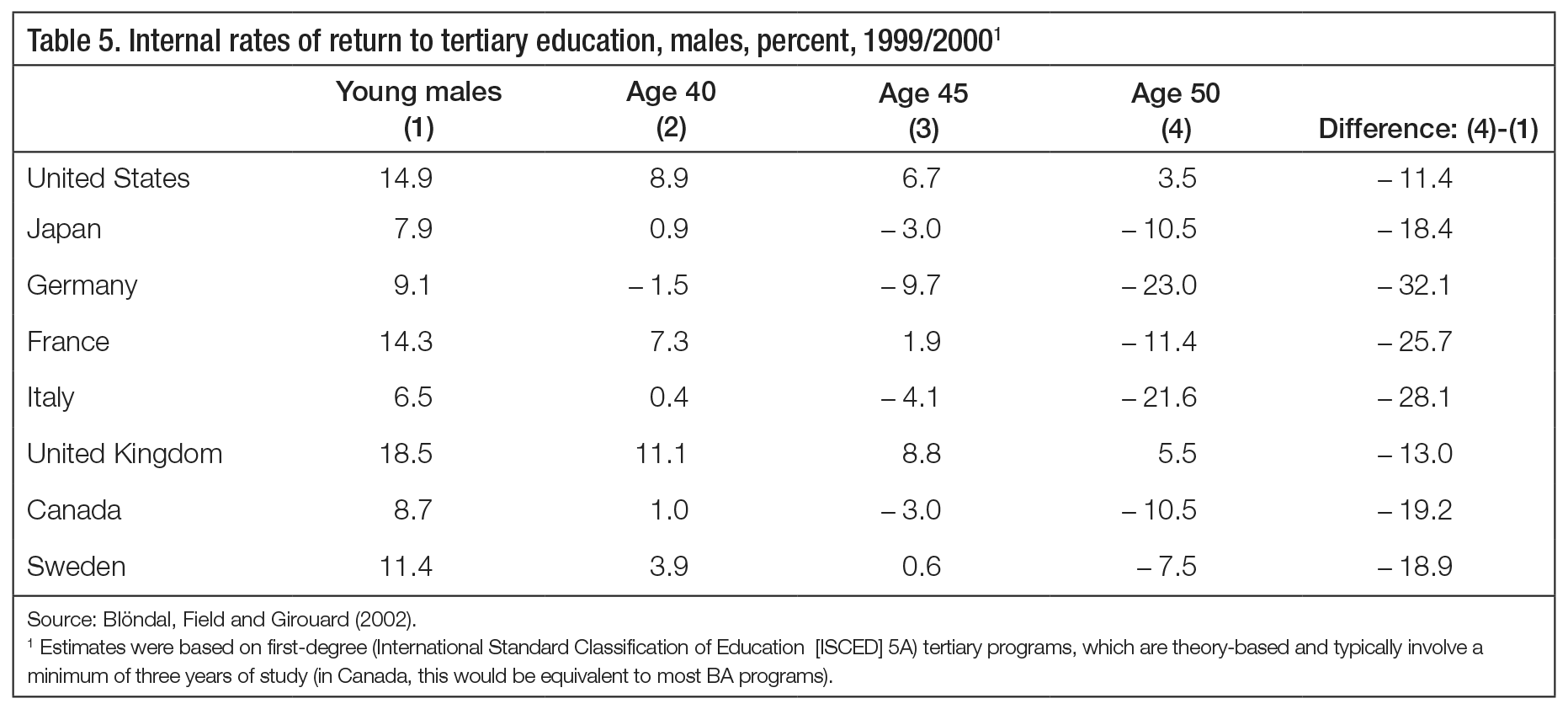

Blöndal, Field and Girouard (2002) provide the most extensive international comparison of estimated rates of return for adults upgrading their education from high-school to PSE level at different ages (table 5). In their analysis, the authors assumed that students had no earnings while studying but did receive modest public support in the form of loans or grants. These estimates took account of the higher opportunity costs, reduced amortization periods and potential restrictions in a country’s student financial assistance program arising due to age or wealth.

Though the return to education varies quite a bit across countries, the general trend is one of positive returns up to some point between the ages of 40 and 45. With the exception of the United Kingdom and the United States, the return is negative in all countries as of age 50.

Without access to the original data, it is not possible for us to definitively explain the differences in results between countries. Higher income inequality in the United Kingdom, shorter–duration learning in Germany, and a general trend toward earlier retirement in France, Italy and Germany (OECD 2013c) all likely play an important role in generating different rates of return from country to country.

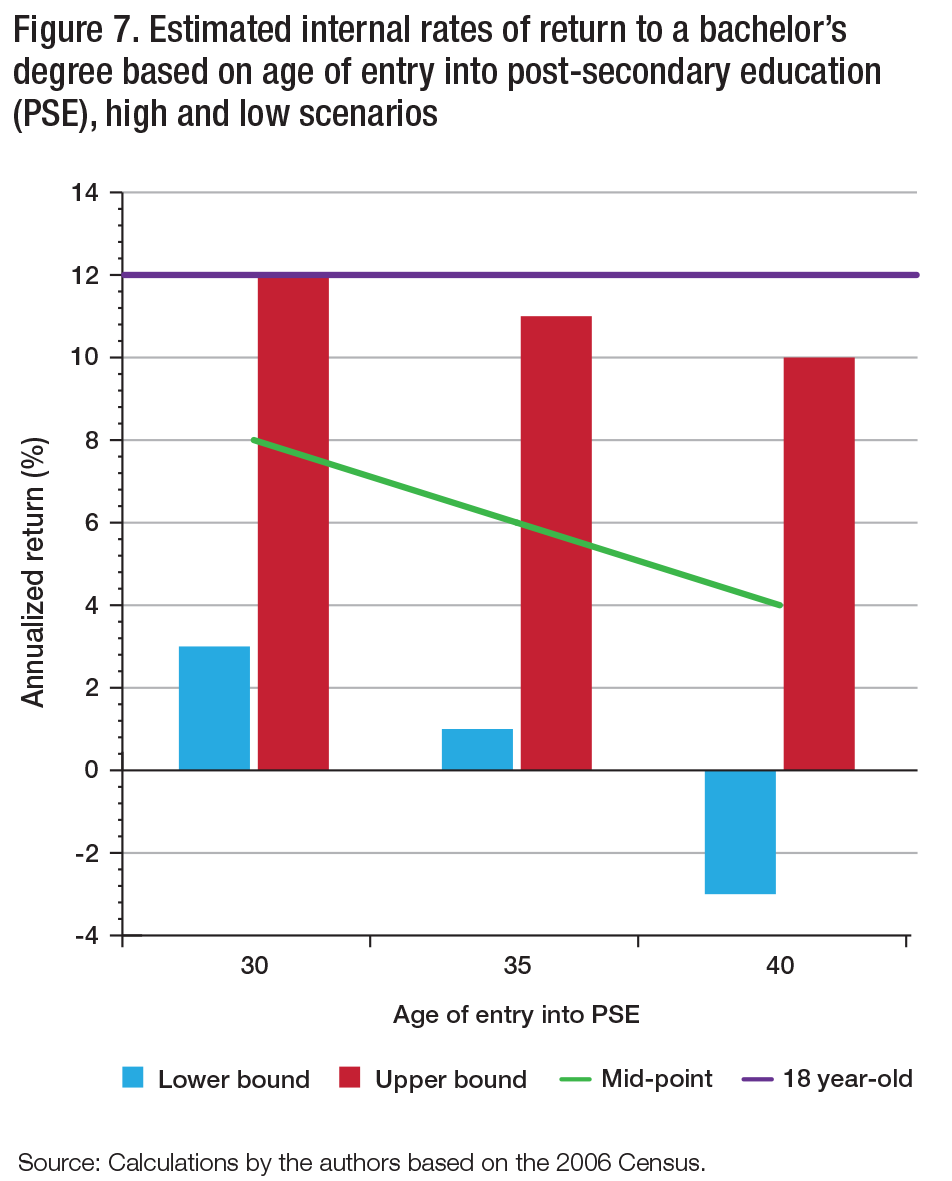

To update Blöndal, Field and Girouard’s assessment (2002) with more recent data for Canada, we performed our own estimate of age-earnings profiles using microdata from the 2006 census. Focusing on Canadian males who worked full-time, we examined the relationship between age and market earnings among those who had completed high school only and those with a bachelor’s degree. From these data we then constructed a best- and a worst-case scenario to estimate the internal rate of return to entering PSE at ages 18, 30, 35 and 40 (figure 7).

In these scenarios, we assume that there are out-of-pocket costs of $6,000 per year and that completion of a BA takes four years, during which no income is earned. Retirement occurs at the current national average. The best-case scenario assumes that older graduates are fully compensated for the work experience they gained prior to returning to school, earning the same amount upon graduation as workers of their age who did not put off PSE. The worst-case scenario assumes that older graduates must start at the beginning of the age-earnings profile, earning the same amount as younger graduates who completed their studies at the same time.

The best-case scenario suggests substantial returns to education well into middle age, although this assumes that mature learners are not penalized for lost time and that they have the same personal attributes associated with earnings (for example, motivation and ability) as those who invested in higher education earlier in life. However, the worst-case scenario discounts completely adult learners’ previous work experience and maturity, as well as any broader skill set they may have acquired through other life experience.

Recent longitudinal evidence from the 1995 cohort of graduates suggests that reality is somewhat closer to the best-case scenario. In their study of different pathways between school and work, Ferrer and Menendez (2009) found that those who delayed entry into PSE and were successful in obtaining work during the intervening period had earnings on average 8 percent higher than those who undertook PSE directly from high school. These estimates adjust for the effects of greater experience among delayed learners and for potential ability bias.

Implicit in both Blöndal, Field and Girouard’s work (2002) and our own is a critical assumption about whether someone should be expected to give up employment earnings during the period of study. Opportunity costs are the largest component of the cost of higher education for any age group, but especially for older workers who face greater forgone -earnings. -Delivering courses through modules and online platforms such as massive open online courses (MOOCs) and other innovations that permit study without major work interruption would alter the age gradient in favour of adult education. Workers who extend their working lives even modestly to make up for the period they returned to school could also experience higher returns to learning.

The literature on the impact of essential skills and apprenticeship training is even more limited than that examining the effects of acquiring a university degree later in life. Most of the available evidence only looks at the potential earnings premium and does not provide any assessment of how this changes with age. These caveats notwithstanding, the available literature suggests potential benefits large enough to meaningfully improve the earnings and employment prospects of adults well into middle age.

In the case of apprenticeship, for example, Gunderson and Krashinsky (2012) and Boothby and Drewes (2011) found that those who complete apprenticeship training earn as much as 24 to 27 percent more than those with only a high-school education. Though both studies also found substantial variation across trades, including an earnings penalty within certain low-paying personal service professions (such as hairstyling), the estimates are large enough to suggest that opportunities in the apprenticeable trades are generally quite rewarding. Timely completion of an apprenticeship is therefore a key to success for the second-chance adult learner.

In this paper, we have placed particular emphasis on the need to assess the pursuit of education or training later in life as one would a financial investment. Though a higher level of education will usually increase one’s potential to earn more, the question is whether future labour market prospects are sufficient to render the investment viable for whoever finances it — be it the government, the employer or the individual worker.

Given the persistence of positive returns to education well into middle age, one has to ask why the distribution of learning activity in Canada remains so heavily skewed toward younger people and individuals with a higher level of education. The answer goes to the heart of the life and psychological context within which households make major decisions about work, learning and saving. We have already mentioned the importance of nonfinancial factors such as access to child care and time off work. In addition to these, there are several more significant factors that can inhibit educational participation among older and lower-skilled populations:

Consider the example of the Canada Learning Bond (CLB), the objective of which is to support PSE participation among the children of low-income families. The CLB provides an unconditional grant to be credited to the Registered Education Savings Plan (RESP) accounts of low-income families qualifying for the National Child Benefit. Yet, since its inception in 2005, a significant proportion of eligible families have forgone the CLB, either because they didn’t already hold an RESP account or they did not apply for the grant. Though participation has risen in recent years, nearly 70 percent of eligible children still did not receive a CLB payment in 2013 (ESDC 2015). Parents of low-income families face the same challenges in using programs to support their own educational goals as they face on behalf of their children.

In many ways, older adults likely start from a context that is more risk-averse than that of young people, who face few opportunity costs and whose participation may be more influenced by the circumstances of their parents (Finnie, Childs and Wismer 2011). If the goal is to raise participation in education and training among older adults, particularly low-skilled or low-income older adults, then policy-makers must recognize that the issues are much broader than simply how learning is financed, whether it is available within the workplace and whether the information available to prospective learners is sufficient. They need to think about how individuals weigh things like risk and uncertainty in making decisions.

As Canada transitions into a prolonged period of slower labour force growth, the need to improve the way in which skills are produced and used in the labour market becomes paramount. Part of this process will require Canada to do a better job of supporting and unlocking the potential of the large number of low-skilled and underqualified individuals who make up the working-age adult population. Though precise estimates are hard to come by, one in seven working-age adults indicate that they do not have sufficient qualifications for their current job, while another one in five lack basic literacy and numeracy skills. Both figures are above the OECD average.

It is ironic that in a country that boasts such high levels of educational attainment and support for lifelong learning, a relatively large share of the working-age population persistently lacks the basic education and skills that would permit a move up in the labour market. Obviously, not all of these Canadians will want to pursue additional education or training, and not all of those who do will succeed. But if we are to improve our productivity and labour force potential, then we must ensure that there exist meaningful skill ladders for those who have the ability and the desire to move up.

This ideal is not yet a reality due to the way in which Canada’s adult education and training system is designed — that is, there are critical challenges related to access, equity and efficiency. Indeed, today’s system features:

What is needed is a strategy that comprehensively addresses each of these challenges.

Although no government or political party has sought to tackle these issues in an integrated fashion, a number of new policy initiatives have been launched in the last few years — in particular, initiatives to improve people’s access to training opportunities later in life. We will briefly assess and comment on these before examining how a more comprehensive strategy could be developed.

Since the Canada Job Grant (CJG) was first announced by the federal government, in 2013, three approaches have been put forward to improving the accessibility of lifelong learning: training subsidies (the CJG, for example), leave policies and savings policies. Each has its own flaws.

The CJG, which is now being rolled out across the provinces, partially addresses at least one of the challenges identified in this paper — namely, the need to better support the training needs of Canadians while they are still employed. However, because the program focuses heavily on short-duration training supported through employers, the end result is unlikely to offer significant new opportunities for lower-skilled Canadians to upgrade their credentials and certification.12 In fact, as many commentators have pointed out, funding for the CJG comes from the existing envelope of federal transfers for employment supports, meaning that some provinces will offset this new initiative by providing less funding for programs such as essential skills training (Mendelson and Zon 2013).

One alternative, proposed by Mendelson, Green and Luff (2013), is the Canada Skills Grant (CSG). The CSG would build upon the CJG by offering a guaranteed training leave to be financed jointly by employers and workers through employment insurance (EI). Under the CSG, workers would be able to secure their position while taking a leave that would be partly supported through replaced wages in much the same way EI supports leave for new parents and caregivers.

Leave policies are attractive because they recognize that income replacement is a primary barrier to educational participation among working adults. A critical challenge they run into, however, is the interaction with employment protection law and the financing obligations they impose on employers. If the goal is to support the acquisition of general rather than firm-specific skills and, by extension, to enable workers to have greater occupational mobility, then the rationale for investment on the employer’s side is tenuous. While parental or care benefits are intended to preserve employment and labour market attachment during a life event, support for additional education would be intended to provide greater opportunities for workers, including those beyond their current occupation or independent of their employer. Employers would only enter into such a contract with employees if employees could guarantee that any gains from the employers’ investment in their education could be recouped through increased retention and productivity. Employees may not be willing to accept this kind of obligation.

A final proposal comes from the leader of federal Liberal Party, who has proposed to introduce a tax-preferred savings account for training along the lines of the current RESP, which helps parents to save for their children’s PSE.13

A type of individualized training account already exists in Canada: the Lifelong Learning Plan allows individuals to withdraw up to $10,000 per year (to a maximum of $20,000), tax-free, from their Registered Retirement Savings Plan (RRSP). The funds must be used for full-time educational programs and be repaid into the RRSP within 10 years, essentially resulting in interest-free borrowing for the individual. Not surprisingly, this option has not been very popular, owing, some speculate, to the program’s lack of visibility and the fact that it requires participants to have accumulated capital (for retirement purposes) (Banerjee 2010). An adult RESP would differ from the Lifelong Learning Plan in that it would create a separate tranche of savings that would be accessible exclusively to fund training needs. If it were implemented along the same lines as the plan for children, an adult RESP could provide options for matching contributions from government, similar to the Canada Education Savings Grant.

While the RESP operates somewhat differently from the way individualized training accounts do in other countries, the general experience (Schuetze 2005), including two major pilot programs in Canada (Lecki et al. 2010) — Learn$ave and Future to Discover — suggests that results would be mixed.

Conceptually, individualized accounts address an important informational gap by providing users with a clear sense of what benefits are available to fund learning needs; they can also be adapted to create strong incentives to save. In principle, however, it is unclear why savings would be a desirable method of funding education. Since education and income are strongly correlated, it is reasonable to believe that those with higher initial educational attainment are the most likely to take advantage of such a scheme. This is certainly the case with RESPs, which are used in much greater proportions as parental education and income rise (Knighton et al. 2009, chart 4.4). As such, learning accounts may reinforce the frustrating phenomenon of education begetting further education and training. Though there is certainly a role for individual learning accounts for some, a model predicated on savings is unlikely to support the type of adult learning we focus on in this paper.

Stepping back, then, we ask what principles we can use to devise possible reforms. In light of the issues and gaps identified in this paper, we argue that an ideal second-chance system would incorporate the following elements:

Based upon these principles, we propose a new, pan-Canadian strategy for adult education and training centred on three components of reform.

Underlying many elements in this paper is the clear need to improve the quality of labour market information (LMI). While much has been said about the fact that it is difficult for young persons to choose their appropriate level of education and field of study, the same is true of older, working-age adults. Because of the relative paucity of evidence of how returns to education evolve over the life course, the challenge may be even greater for older individuals.

Not only do we require a more comprehensive LMI system for all learners, but we also need to undertake significant additional research if we are to understand how different learning pathways affect the long-term earnings of those who return to school at different stages of their working lives. The evidence reviewed in this paper suggests that, on average, learners can expect a positive return on education up to their mid-40s, but the data on which this is based are relatively limited. In the context of an aging workforce, this represents a significant impediment to effective policy development.

If adult learners are to make the right choices, they must have access to a more robust LMI system (Drummond 2014). To this end, governments must renew educational surveys such as the Access and Support to Education and Training Survey, last completed in 2008; and they must develop a comprehensive system of longitudinal data on graduates. They must then leverage these data to develop informational products that will help Canadians evaluate the actual rate of return to different investments in education based on their age, potential field of study and their preferences for their future working lives. Closing these large gaps in data and evidence must be a top priority for those involved in the next round of labour market development agreements and for the Council of Ministers of Education, Canada.

At the centre of a second-chance system there should be better tools to ensure that Canadians, particularly those who are underqualified or lower-skilled, have the resources to pursue productive investments in education and skills training.

Canada has a highly developed student financial assistance (SFA) architecture consisting of both loans and grants. Though Canada’s SFA has a number of moving parts, the fact that family income is no longer the strongest determinant of who goes on to higher education (Finnie, Childs and Wismer 2011) is a testament to its long-running success in supporting the needs of youth. As a system, it also operates fairly efficiently.

The system is challenged, however, in dealing with the unique needs of adult learners.14 Problems include:

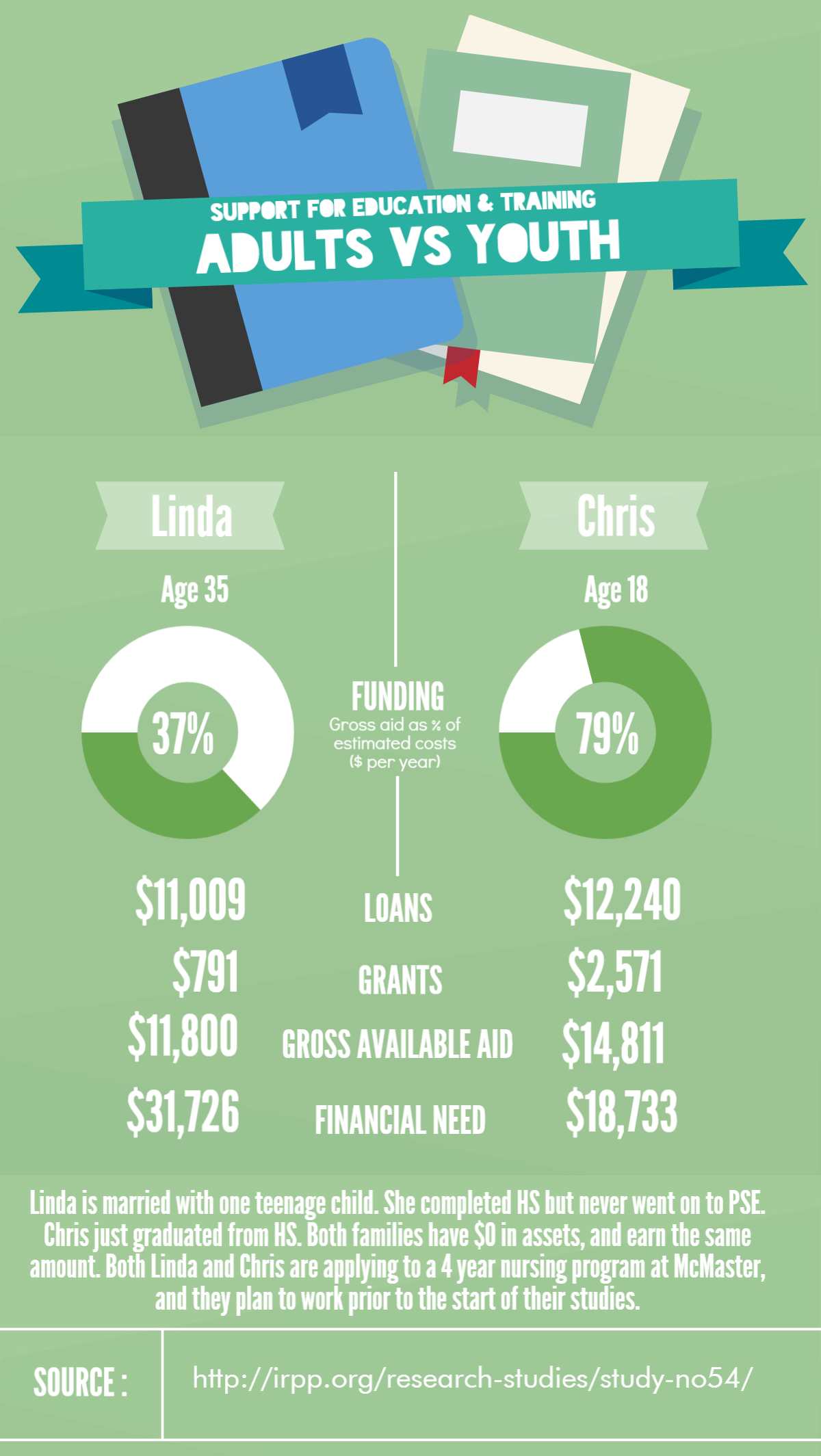

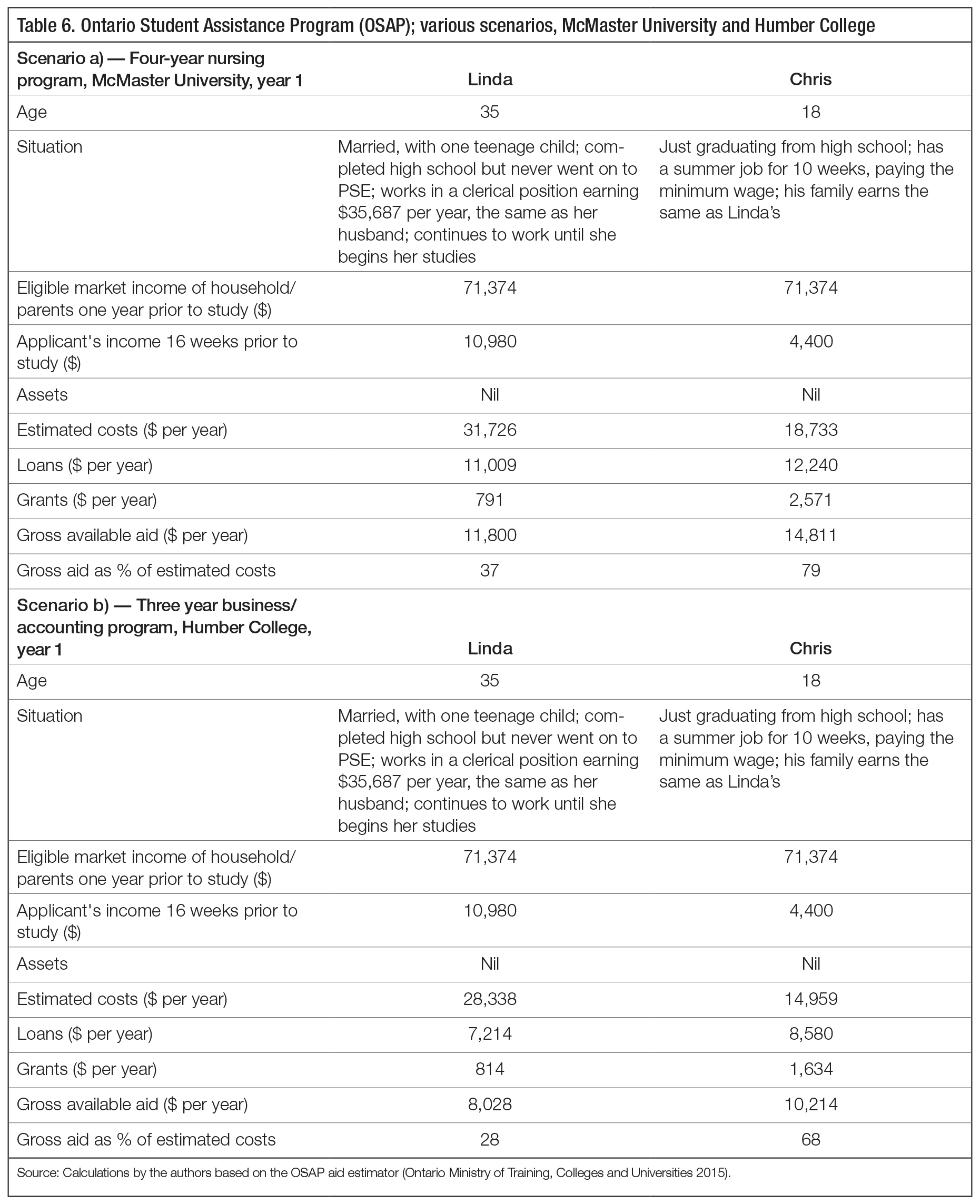

Consider the fictional example of “Linda” and “Chris” (table 6, scenarios a) and b), who live in Ontario and who are applying to the same college and university programs, both for the first time. Although Linda is 35 and Chris is 18, they come from households with a similar income, family structure and asset profile (no assets). The families of both are not particularly well-off — each family earns only 75 percent of the median market income of a working-age, two-parent family with kids.15 Because Ontario’s integrated SFA system does not support older adults in the same ways it supports younger ones, Linda would only be eligible for support covering between 28 and 37 percent of the direct and indirect costs of her learning, depending on which program she chooses. Chris, by contrast, can expect to receive support covering between 68 and 79 percent of his assessed financial need. Although Linda has significantly higher living costs than Chris (her household loses her earnings, while Chris’s still has the income of two parents), she receives less loan support and substantially less grant aid. If either household had even modest assets, total available support could be even lower.16

It is important to note that results will vary from one provincial SFA system to another, but the basic point is the same in most cases: SFAs are primarily designed to meet the needs of youths transitioning directly from high school, while older adults who don’t have a disability are treated as an atypical user group. A one-size-fits-all approach results in inequitable outcomes.

As a first step, provinces should be encouraged to review all existing student grants in order to remove age bias where it exists. With respect to provincial and federal borrowing programs, it is important to recognize that working-age adults are fundamentally different from youths and require a system aligned with their unique needs. Creating a separate borrowing program focused on adults, but administered within existing federal and provincial SFA infrastructure, would be a good starting point for establishing a properly differentiated system.

The system we propose would be known as the Lifelong Learning Loans Program (LLLP), and it would be available to adult learners as of age 25 who have been absent from school for a minimum of five years. Though both parameters are largely arbitrary, we have chosen them in order to properly distinguish between youths who continue through to graduate studies on a relatively uninterrupted basis and those who are seeking to return to education later in life.

There are many ways in which such a system could be designed to better address the needs of adult learners. A particularly appealing approach would be to make such loans available entirely on an income-contingent basis, as do the student loan systems of Australia, the United Kingdom and New Zealand. In such a system, all learners would be automatically eligible for assistance, regardless of assets or income, and their repayment terms would be based on the income they earn upon completion of their studies. The LLLP would thus provide the opportunity to create notional individualized learning accounts and to know in advance what one could borrow.

Because repayment is tied to future labour market outcomes, income-contingent loans (ICLs) remove a substantial amount of the risk and uncertainty related to investments in learning. For adult learners, who are generally more risk-averse and face higher opportunity costs to learning than youth, these improvements would be significant. Moving in this direction would certainly better support the needs of adult learners, but it would also have horizontal implications for how the SFA is designed for youth.

Some, such as Usher (2014), argue that Canada’s SFA already reflects principles of income contingency, thanks to a number of progressive repayment assistance mechanisms.17 While it is true that Canada’s existing SFA system enables borrowers to adjust repayment terms in relation to posteducation income, this view only considers how loans are consolidated. Critical to any ICL system is the principle of universality: regardless of the circumstances of need, income, age or wealth, financing is available on efficient terms. This recognizes that education is a credence good — its impact is not guaranteed, and it is hard to assess ex ante. The disparity between the borrowing experience of adults and that of youth in Canada’s SFA undermines the notion of universality.

By the same token, we should also note that adults in countries employing ICL systems still face significant hurdles in acquiring support for their needs. Much depends on the design of each system. For example, Australia’s ICL system only assists with direct costs of learning deriving from tuition, compulsory fees and textbooks; it provides no support for living expenses or income replacement — aspects that are at least modestly addressed by Canadian borrowing programs.

To respond effectively to the needs of adults, the LLLP would need to incorporate both direct and indirect costs of learning while maintaining near-universal eligibility. Analysis of the Australian system by Chapman, Higgins and Taylor (2009) suggests that these parameters can be incorporated into an ICL design in a fashion that would still produce attractive repayment terms for low- and modest-income populations looking to start training even as late as age 45.

Providing broad access at a higher borrowing limit, particularly one that is high enough to incorporate both direct and indirect costs of learning, raises a number of issues related to cost, moral hazard and adverse selection. Considerable research will need to be undertaken to study these issues in relation to a number of factors, including the threshold of posteducation income that would trigger repayment; the kinds of PSE institutions and learning that would be eligible (for example, there is likely good reason to continue to exclude short-duration training programs at for-profit institutions); admission standards; and the role of private lending, which may or may not continue.

Based on international experience, it is reasonable for us to believe that the proposed LLLP can address many of these issues. On the cost side, an ICL system should not necessarily result in substantially higher debt liability for government. Including repayment assistance, it is estimated that about 15 percent of new debt issued in a given year by Canada’s federal student loan program will never be recovered (excluding interest-rate subsidies) (Office of the Chief Actuary 2012). This is somewhat lower than the “doubtful debt” expense of 17 percent in Australia; a number of reforms have recently been proposed in that country that could potentially reduce the liability rate to only 7 percent of newly issued debt (Norton 2014).

Actual budgetary expenses will reflect a number of factors, including take-up, the composition of borrowers and the potentially larger amounts of borrowing that the system could allow. Each of these involves important design issues that must still be worked out, but we can at least provide some high-level preliminary estimates.

We assume that the system is sufficiently focused on second-chance learners with an average profile similar to that of Linda, and that borrowers are equally split between those applying to college and those who wish to attend university. There are many ways an ICL can be -implemented using either a lifetime borrowing cap or a standard percentage of assumed need (including both living expenses and direct costs). For this exercise, we will assume that the policy goal is to fill 100 percent of assumed need (see “estimated costs” in tables 6a and 6b), although a lower threshold could be used. In this scenario, if default rates maintain the same pattern as in the current Canada Student Loans Program, it would be possible to support approximately 20,000 adults per year at an incremental cost of approximately $435 million in bad debt provisions.18

An investment of this magnitude is approximately equal to the current bad debt provision assumed each year by the Canada Student Loans Program (ESDC 2014), and it is well within the fiscal room available to the federal government over the coming decades. Net costs would also likely be much lower, as an ICL would render most needs-based grants and other tax credit incentives moot, allowing governments to shift the composition of aid heavily in favour of borrowing. We have not explored what savings this might produce, but the gain from simplification is probably substantial. The purpose here is simply conceptual and illustrative. Much research and design thinking is still required.

A final point concerns the kind of training that would be supported by the LLLP. While the focus would be on the acquisition of formal PSE credentials, some users of a second-chance system could also need complementary access to essential skills training in advance or as part of their return to school. Integrating this learning into the credentialing process would be most beneficial to learners, but in all likelihood some would still need to complete additional preparatory training before being admitted to a credential program. In developing the LLLP, provincial and federal governments should examine how these pathways can promote seamless transitions, and they should determine whether essential skills training would be part of the financing package offered to students or funded out of general revenues.

Just as we need to better connect older Canadians with education and training opportunities, so too must we improve the effectiveness of the training system itself. This is especially true in the area of apprenticeship training, where older adults are already disproportionately represented. Apprenticeship training is a medieval model, and we need to rethink it from the ground up. We must examine its foundations and ask how it can more effectively and efficiently produce advanced skills. In the last several years, there has been a growing call among policy-makers for a new Canadian apprenticeship model inspired by the German one (Hardt 2014). In this context, it is vitally important that we appropriately diagnose the problems and think critically about how we might begin to address them.

The policy debate over apprenticeships focuses predominantly on the demand for such training — that is, on how we can increase the number of candidates, particularly young Canadians, going into apprenticeable trades. Many financial incentives have been created to encourage apprentices and their employers at each step of the process, from application to completion. The 2014 federal budget continued in this direction by introducing the Canada Apprentice Loan, which provides up to $4,000 in interest-free loans for apprentices during their training (Department of Finance, Canada n.d.); this is in addition to supports that already exist within the EI and tax systems. While each may have its own merits, as a whole these incentives imply that the first-order problem facing apprenticeship training is one of interest and persistence on the part of students. This arguably ignores many of the much more critical failures in policy and market behaviour on the supply side for training. In essence, we cannot expect employers to establish an effective and efficient supply of opportunities for training when that training produces general, portable human capital. Canadian college and university students benefit from a well-developed market in which suppliers (institutions) compete to attract them. Apprentices do not have access to such a well-developed supply side.

Over the last two decades, the number of Canadians starting apprenticeships each year has more than tripled, while completion rates have fallen. How can we regard this as a well-functioning system? Rather than creating additional incentives to increase the number of people taking on apprenticeships or enhancing the income supports they are offered, we ought to be asking fundamental questions about how the system itself is designed. In this paper, we cannot solve the apprenticeship conundrum, but we can raise some of these fundamental questions.

Attaining certification in most apprenticeable trades takes approximately four to five years. Though it varies by trade, about 90 percent of this training period comprises gaining mandatory work experience with an employer (Ontario College of Trades, n.d.). This implies a ratio of 1 to 9 between the time spent satisfying formal and experiential learning requirements. This raises several issues.

First, we must determine whether this is an appropriate balance. In many licensed professions, the allocation between formal and experiential learning is much more even. An accountant or engineer seeking certification in Ontario would be required, for example, to spend three to four years in a related undergraduate program and then acquire an equivalent amount of practical experience with an employer before being granted membership in a regulated body. In other professions, such as teaching and dentistry, the proportion of training allocated to on-the-job learning is even smaller. What this reveals is that, in many licensed professions, the value of hands-on experience in the workplace is at most equal to the value of a degree. If formal learning requirements are an indication of the level of foundational skills one must have in order to practise a particular profession, then we have to question why apprenticeable trades are such an outlier. Why do we place so much more weight on informal skills development in these occupations than we do in others? If anything, this only implies that employers who take on apprentices are less efficient at delivering instruction than are formal learning programs.

Second, we must ensure that adult learners complete apprenticeship programs expeditiously. All provinces make available some kind of process through which an apprentice can obtain credit for prior learning or experience. While these processes vary somewhat across specific trades, in most cases the onus rests on the individual to apply for credit. We believe that training institutions should be more formally and comprehensively engaged in the apprenticeship system; if they become so, then a critical step forward would be to make the prior-learning-assessment process automatic at the time of registration or enrolment.

Finally, there is a fair bit of variation across trades in terms of whether certification is mandatory. Were mandatory certification increased as part of a more comprehensive reorganization of the distribution of learning between in-classroom and on-the-job training, it might be possible to create a more efficient pathway for apprentices toward completion of a recognized credential, such as the Red Seal.

As the Government of Ontario quite explicitly states, “Apprentices are workers, so you will need to find an employer who will train you” (Ontario Ministry of Training, Colleges and Universities 2013). As such, “anything you can do to make yourself more attractive to employers will help” (Ontario College of Trades, n.d.). Many provinces have made resources available to facilitate matches, as they assume that employers see the cost-benefit of sponsoring an apprentice in the same way students or policy-makers do. That may not be true.

Apprenticeship training can produce significant earnings gains in most trades. As such, apprentices should be willing to pay for training just as college or university students pay for their education. When apprenticeship training is equated with paid work, there is no avenue through which this willingness to pay can be expressed, and our current system must be regarded as a market failure.

Why do we assume that individuals certified in an apprenticeable trade are also qualified to teach?

There is nothing in a journeyperson’s training to ensure that he or she has the communication skills, pedagogical capacity or motivation required to effectively transfer knowledge and curriculum to apprentices. Though a similar criticism might be made of the training of PhD candidates — that it does not prepare them to teach at the college or university level — the formal PSE sector does provide pedagogical supports for newly hired young faculty. Placing a large share of the apprenticeship-training burden on employers while offering them no training supports is unfair to both the employers and the students.

All of these questions make evident the need to challenge the premise that apprenticeships should be differentiated from other forms of human capital formation. The requirement that apprenticeship happen, for the most part, within the workplace, through employers, forces organizations that are not in the business of providing general education to do so. This invariably creates problems related to finding a trainer and seeing the apprenticeship through to completion. If training could be more concentrated within Canada’s community and vocational college system, then both young and adult learners would benefit from having access to the same efficient and effective training market as exists in PSE.

To some extent, this is beginning to happen. In some provinces and some trades, certain college programs provide an integrated system that transitions a graduate to a sponsoring workplace, where the apprentice receives equal credit toward their apprenticeship for time spent in school. This closer link between workplaces and training institutions is important, but many such initiatives only deal with the immediate challenges to instruction and apprenticeship search. They do not change the basic requirements and system design, which can constitute significant barriers to employment for apprentices both young and old. Policy-makers need to comprehensively examine the design of apprenticeship systems, including basic expectations related to instruction, certification, completion requirements and the role of employers.

It might be argued that current arrangements that allow apprentices to work and train simultaneously favour adults, especially those with family responsibilities. While this is certainly true in some cases, individuals are no better off if they are unable to break into an occupation because they can’t find an employer match or are unable to complete training quickly. If, as former federal minister of employment Jason Kenney has said, the goal is to achieve a “parity of esteem” between apprenticeship and university- or college-level learning, then this must change (Galloway 2014). We have to change the system as a whole, not just who enters it.

The problem facing Canada’s system of adult education and training is not that older adults aren’t undertaking sufficient learning over their lifetime, but that the opportunities for learning are not fairly distributed. Those who would benefit most from the opportunity to learn — people who didn’t succeed earlier in life — are forgoing this opportunity, for reasons that could be addressed with more creative policy design. For too many Canadians, the pressure to replace earnings, return to work quickly or deal with time constraints imposed by family responsibilities makes it difficult to go back to school, even if the payoff would be significant. Once an adult passes the age by which PSE has commonly been completed, many other opportunity costs intervene. This is why so many Canadians — even those who are unemployed and would particularly benefit from it — fail to return to PSE (Frenette, Upward and Wright 2011).

Canada will increasingly require higher levels of productivity from an older, slower-growing workforce; these barriers to human capital development are thus becoming significant. We cannot solve this problem by taking a passive approach and enhancing existing efforts. While it is always better to ensure that educational success happens earlier in life, we can no longer afford to ignore those who need a second chance. Ironically, in a country with a population as highly educated as Canada’s, an above-average share of the workforce remains underskilled, underqualified or in need of a new career path. It is time for this to change.[:fr]Investment in human capital has always been essential to Canada’s economic prosperity, but education and training will be especially important in the coming years. Over the next decade, Canada will be subject to a combination of demographic forces: population aging and slower labour force growth. As Halliwell has noted, increased immigration flows will do little to offset these significant forces (2013). We must therefore improve labour productivity simply to sustain our current standards of living.

Canada’s labour force is already highly skilled — among the member countries of the Organisation for Economic Co-operation and Development (OECD), Canada has the highest proportion of workers who have completed some form of post-secondary education (PSE) (college or university) (OECD 2013a). Nevertheless, there could be large numbers of people who would benefit from learning later in life. This could include workers who did not enrol in PSE programs earlier in life, were unable to complete them or did not choose the right form of education for success in the labour market. Workers who fit into any of these three categories still have the potential to make a meaningful contribution to overall productivity growth if they can move up the skills ladder by acquiring new credentials or education. In this context, there have been calls for Canada to formalize the availability of long-term training supports for working-age adults. Such efforts range from the adoption of a formal second-chance system for those lacking foundational skills (OECD 2013a), to efforts by the federal government to expand access to workplace training (for example, the Canada Job Grant program), to, more recently, a proposal floated by the Leader of the federal Liberal Party to offer adults access to their own version of the Registered Education Savings Plan (RESP) (Wells 2014).

Though each of these ideas targets a different issue, all are concerned with how workers develop skills over the course of the many decades following graduation. For its own part, the OECD has been especially vocal in insisting that continuous reinvestment in skills development is essential for productivity and for adapting to the shift to a knowledge-based economy (OECD 2004). While Canada’s labour market has demonstrated a high degree of job stability in recent decades (Morissette, Lu and Qiu 2013), rising demand for cognitive skills has increased the skill content of work (Plesca and Summerfield 2014). In theory, this suggests the importance of offering training to two groups: the involuntarily unemployed who need to change jobs midcareer, and the low-skilled who want to move up in the labour market.

As greater policy attention shifts toward supporting education and training for older adults, a critical question that policy-makers must ask is whether such investments will be productive. Over the last several decades, there has been an extensive and exhaustive examination of the outcomes of formal schooling among youth, one that pays close attention to how individual choices are made and the complex statistical issues involved in measuring the causal effects of schooling. With some exceptions (see, for example, Carneiro and Heckman 2003), the economics of adult learning have not been critically examined with the same level of analytical or empirical care. There is, for example, a presumption that adult learning will raise the skill level of adults with too little education; it is taken as an article of faith that such human capital investment will have a positive rate of return. However, in such cases we must question whether the second chance will be stymied by the same factors that prevented success the first time around.

To fill these important knowledge gaps, we review what is known (and still unknown) about formal adult learning in Canada with an emphasis on establishing the need and appropriate role for public policy. In particular, we seek to identify the population of adult learners who might benefit from additional education or training and to determine how large these benefits might be and how the payoff changes with age. What unique barriers and challenges do adult learners face? And how should public policy-makers think about the balance between work, life and the financing constraints facing adults who are still working? To support this analysis, we begin with a brief review of the theory of human capital, discussing how the benefits of learning should be understood and analyzed within this framework.

It is important that we define adult education and training. Our focus here is on formal learning that occurs after the age at which most Canadians have entered the workforce — approximately 25.1 We refer to investments leading to certified skills acquired either through education (that is, skills acquired outside the workplace) or training (courses or formal training delivered in the workplace). This includes learning that occurs in the formal PSE sector, as well as apprenticeship (which involves on-the-job learning) and employer-sponsored training. In keeping with the scope of this paper, we focus primarily on PSE and apprenticeship training, as these generally lead to formal certification.

Why and to what end should adults pursue education and training later in life? How might we think about the different effects that educational investments would have for learners over different stages of the life course? To provide a useful framework for analyzing these questions, we start with a brief examination of what economic theory tells us about adult education and training.

Arguably the most significant and pervasive economic theory of education is Becker’s human capital model (1964). Consider an individual leaving high school at age 18 who must choose between undertaking a four-year post-secondary degree or directly entering the labour market. Figure 1 plots the hypothetical annual earnings profiles associated with each choice. The human capital model envisions the individual comparing the benefits of that four-year investment (the increased earnings in area B) against the costs, which include both out-of-pocket educational expenses such as tuition and books (area C1) and the earnings forgone as a result of not working during those four years (area C2). Because the benefits accrue for many years after the costs have been incurred, the comparison must be made in the same way that investments in physical capital are considered, using either present values or internal rates of return. This is very different from simply comparing differences in earnings (often referred to as the “earnings premium”) across education and occupation pathways.

Although simple, this model provides multiple insights. For example, using Canadian data on earnings, tuition costs and expected length of working life, the human capital model shows that, despite significant differences in lifetime earnings,2 the internal rates of return are quite similar between college and university,3 reflecting differences in years to completion and direct and indirect costs between these two PSE pathways.

In the context of adult learning, the model reveals an important relationship between age and outcomes. All things being equal, the earlier an investment in education is made, the better. Rates of return on an investment in education will be sensitive to a number of factors, including the opportunity cost of employment later in life and the number of years one has to recoup the investment. This is not to say that upgrading skills later in life won’t generate positive returns; it simply means that the rate of return on such investments will likely change over the course of a person’s life. How this plays out is a critical question, and one that this paper seeks to address.

In evaluating the returns to education, we must take into consideration that costs and benefits will appear in a number of forms, and they will be spread in several directions across society.