Parental Benefits in Canada: Which Way Forward?

Jennifer Robson

Because of their long job tenure, and sector-specific skills that often are not easily transferable to other jobs, some older workers in Canada who suddenly find themselves laid off face con- siderable obstacles to re-employment. They may resort to early retirement as a second choice, rather than accept a lower-paying job. But such hastened retirement will further slow labour force growth, which is already beginning to wane due to population aging, thus reducing eco- nomic growth and putting additional stress on public and private pension plans.

Ross Finnie and David Gray investigate the sources of income and the labour market choices of long-tenured older workers in the five years following layoff, and find that a surprisingly large number choose to or are forced to retire due to poor re-employment prospects. Among those aged 45 to 59 (who are not eligible for Canada Pension Plan benefits), about one-quarter have “retired” within five years, in the sense that they rely on pensions as their primary source of income. This proportion rises to nearly 70 percent in the 60 to 64 age group.

Older laid-off workers (aged 45 to 64) who manage to find new jobs lose about 40 percent of their earnings relative to what they earned in their previous jobs, significantly more than do those aged under 45. Those under 45 are much more likely to find re-employment at or above their previous earnings, and those who initially experience earnings losses typically see their earnings grow steadily thereafter. Older workers, in contrast, rarely succeed in matching their previous earnings upon re-employment, nor do their earnings grow appreciably in subsequent years.

Given the poor track record of existing adjustment policies for assisting older laid-off workers, such as training and short-term income maintenance, the authors argue that wage insurance could be an effective option. Such a program would subsidize a proportion of the wage losses suffered by an older unemployed worker for a fixed period upon re-employment. To be effec- tive, it should be coupled with intensive job search assistance that encourages workers to look further afield than their previous industry and occupation. If implemented properly, wage insurance would enable many older workers, who might otherwise leave the labour force, to earn acceptable wages and gain new occupational and industry experience, thus partly offset- ting the negative effect of population aging on Canada’s prospects for long-term economic growth.

Owing to the aging of Canada’s population, older workers will comprise an increasing fraction of the labour force in coming years. In a similar vein, an increasing share of workers displaced through layoffs, as well as an increasing share of workers who change industry, will be over 50 years old. Riddell (2009), the authors of the “Expert Panel on Older Workers” (Human Resources and Skills Development Canada 2008), Neill and Schirle (2008) and numerous other authors point out that older laid-off workers face adjustment costs that are much higher than those their younger counterparts face in the form of long-term unemployment and wage losses. One contributing factor appears to be older workers’ accumulation of firm-specific, industry-specific or occupation-specific skills. For reasons that are not totally understood, more general skills that could be applied at other jobs appear to deteriorate as the length of job tenure increases. Other obstacles to re-employment include labour-market rigidities, possible age-related job discrimination, and the shorter remaining career, which may discourage retraining or relocation.

Younger laid-off workers normally search for a new job that is comparable (and perhaps even superior) to their prior job. In contrast, older workers’ choices involve some form of labour-force withdrawal, including early retirement (with a public and/or private pension), permanent disability status (indemnified) or partial retirement. There is widespread agreement that alleviating the adjustment costs that older workers face resulting from displacement is a desirable policy objective. Not only would it promote social welfare by easing the hardship facing a select group of workers, but it would also increase labour-market efficiency, permitting workers to adapt to economic shocks as well as to long-term trends without experiencing persistently high unemployment.

A public policy response may be warranted if an excessive number of older laid-off workers is being either forced or induced to retire – presumably because of insufficient prospects for satisfactory employment. This response could be in the form of policies such as wage insurance, enhanced job-search assistance and employment counselling, mobility assistance, and fiscal inducements to working past the normal retirement age (for example, through relaxation of Canada Pension Plan restrictions).

Encouraging older laid-off workers to remain in the labour force takes on added importance in the context of demographic trends. The aging of Canada’s population means that growth in the labour force will slow in the coming years; the magnitude of the slowdown will depend in no small part on the degree to which workers close to retirement age decide to withdraw from the labour force or to continue working. If large wage losses upon re-employment make reemployment options for older laid-off workers financially unattractive compared to retirement, labour-force growth will slow even more than anticipated, putting a further dent in the long-term growth prospects for the Canadian economy.

Another consequence of widespread early retirement among older workers is increased financial pressure on public and private pensions, an issue of growing concern in Canada. Although indepth analysis of pensions is beyond the scope of this study, it is clear that policies to increase the take-home pay of older workers to keep them in the labour force will help strengthen the long-term sustainability of retirement-income systems.1 Such policies may even cost less than the additional pension payments required to finance involuntary early retirement.

Our goal in this study is to document and analyze the postlayoff profiles of displaced workers aged 45 to 64 and discuss the policy implications of our findings. We begin by reviewing the literature on the subject and follow this with a description of our methodology. In the main section of the study we investigate empirically (1) the layoff rates of two cohorts of men and women, (2) their sources of income and what this tells us about their labour-market participation, and (3) the changes in their earnings. To our knowledge, with only a few exceptions, almost none of the research literature on labour-market outcomes of displaced workers looks beyond one or two years after layoff. We seek to fill this void by measuring and analyzing the entry of older laid-off workers into three broad groups: those receiving some form of social insurance, those retiring early and those finding new jobs (at potentially lower earnings).

We also present four policy options for dealing with the issue of older displaced workers: encouragement of early retirement, provision of passive Employment Insurance (EI) benefits (income support and job-search resources), provision of active EI benefits (proactive measures to improve employability) and establishment of wage insurance.

The empirical analysis consists of following cohorts of workers who were laid off in a given year and tracking the numbers of individuals who are observed in a given group in a subsequent year. As this generates a great amount of empirical detail, an important challenge is to distill relevant patterns over a five-year postdisplacement interval. After allowing the data to shape our typology of postdisplacement profiles, we also search for particular patterns such as the outcome of early retirement, the means of financing retirement (whether by public or private pension benefits) and withdrawal from the labour market without any income. Our results are adapted from Finnie and Gray (2009), which contains much more detailed findings.

To measure the magnitude and the distribution of wage losses that are suffered by older laid-off workers, we update the analyses contained in Morissette, Zhang and Frenette (2007) and in Chen and Morissette (2010). For our analysis we draw primarily on Statistics Canada’s Longitudinal Administrative Database (LAD), which consists of a panel of annual tax-based data. One important advantage of this file is that it contains detailed and accurate information on the sources of income and the amounts that are drawn from these sources, including income from social insurance programs and nonlabour income such as self-employment and investment income.2

Any analysis within this policy domain should set out the rationales for government intervention to assist laid-off workers who have trouble finding a new job. Does long-term employment such as this represent a case of market failure? Riddell (2009) eloquently summarizes the case for labour-force-adjustment policies, evoking both equity and economic efficiency concerns. In today’s labour market, shocks to employment can stem from any number of sources, such as rapid advances in information technology, shifting modes and organization of production (for example, outsourcing and “off-shoring”), fluctuating prices for natural resources, volatility in the exchange rate of the Canadian dollar, uneven regional rates of GDP growth, increasing competitive pressure in product markets and high inflows of immigrants. Having a labour market that can respond flexibly to such shocks brings efficiency advantages, but the benefits are diffused widely across society while the costs are imposed on a concentrated minority who lose their jobs as part of the broader economic adjustment.

This distribution of the resultant costs and benefits can justify compensation to the job losers in a form that can be broadly construed as social insurance. There is virtually unanimous agreement that the private insurance market fails to provide coverage for the contingency of earnings losses from such risks. In the absence of either social protection or privately based programs to mitigate earnings losses, politicians and the affected populations tend to favour policies that perpetuate the status quo configuration of jobs and wage structures. A large segment of the Canadian labour force perceives that it has a low degree of job security (Brochu and Zhou 2009) and might appeal to the government for policy measures that expressly inhibit adjustment, such as operating subsidies to declining industries, unemployment insurance programs that function as quasi-permanent income-maintenance programs and bailouts of firms threatened with bankruptcy. The threat of policies that entrench economic inefficiencies, the uneven distribution of adjustment costs, the need for social insurance and the private market’s failure to provide it form the essence of the case for public intervention.

Riddell (2009) notes that the research literature on displaced workers is less developed in Canada than in the United States. This discrepancy can be attributed to the lack of a Canadian counterpart to the specially designed biennial Displaced Worker Survey in the United States. The authoritative (but somewhat dated) study on worker displacement in Canada is by Abe et al. (2002), although earlier studies exist, such as Gray and Grenier (1995) and Kuhn and Sweetman (1998, 1999), which are based partially on the Canadian Survey of Displaced Workers, carried out in 1986.

Abe et al. (2002) is based on a few waves of Statistics Canada’s Canadian Out-of-Employment Panel (COEP) survey from the mid-1990s. Because the COEP file is based on a representative sample of job losers, it does not reflect the entire labour force. The survey limits its time horizon to 14-15 months after layoff. These authors estimate re-employment hazards of jobless workers as well as wage losses (or gains) for those who are re-employed. They find the median duration of joblessness to be 5-6 months for men and 7-9 months for women. Younger and older workers, and workers with longer tenure in the former job, fare worse in re-employment chances than others. On average, laid-off workers below age 45 do not experience major wage losses, and some laid-off workers actually gain. When all other factors are held constant, age and union membership before layoff correlate with wage loss. Wage losses also increase with length of tenure in the former job. Displaced workers sometimes expect layoffs to be temporary, but they are often mistaken on that point.

The study by Morissette, Zhang and Frenette (2007) is among the most recent and best-known studies dealing with displaced workers in Canada. Using Statistics Canada’s Longitudinal Workers File (LWF), these authors focus on the earnings losses of displaced workers rather than the duration of unemployment. They follow 10 cohorts of workers between 1988 and 1997, over a window that starts three years before the layoff and ends five years later. This is one of the few studies whose data enable us to know the situation of these laid-off workers (in this case, those displaced through mass layoffs) and to compare their earnings outcomes to those of a control group composed of workers who have not been laid off. The authors interpret the earnings of this group as an indicator of counterfactual earnings for the laid-off workers (that is, what they would have earned had they not been laid off).

Morissette, Zhang and Frenette (2007) find that high-seniority male workers – defined as those with more than five years at the firm – who are displaced as a result of either mass layoffs or permanent plant closures suffer losses in earnings that are both substantial (between 18 and 25 percent of their predisplacement earnings) and persistent, and they are thus likely to experience a permanent drop in income. For their female counterparts, the corresponding estimates vary between 24 and 35 percent. Earnings also tend to taper off a bit before layoff. The authors break down these losses in earnings according to two age groups: 35-49 years (the “prime age”) and 25-34 years. (They include no workers over 49 years of age at the time of layoff in their analysis of wage losses.) Among male workers with high seniority, prime-aged workers lose less in earnings than their younger counterparts, but this pattern is not found among women. (In this study we provide updated estimates of the distribution of wage losses of displaced workers using the same approach.)

Morissette, Zhang and Frenette use a methodology developed by Jacobson, LaLonde and Sullivan (1993). That US study was one of the first that measured wage losses appropriately, investigating wage outcomes of displaced workers over a time horizon spanning periods long before and long after layoff. Perhaps more importantly, the authors included in their analysis a comparison group of workers who had not been laid off to permit a comparison of their earnings outcomes with those of displaced workers with five or more years of tenure on the job. Their principal findings are that displaced workers actually experience relative wage losses before their final layoff and afterwards make only a partial recovery.

Another recent Canadian study is by Neill and Schirle (2008), who estimate earnings losses of displaced workers between the ages of 50 and 69 using longitudinal data drawn from the Survey of Labour Income Dynamics (SLID) for the period 1993-2005. Their methodology is similar to that of Jacobson, LaLonde, and Sullivan (1993) and has the advantage of observing individuals’ characteristics, their earnings, the timing and incidence of layoff, and reasons for layoff for up to six years. Neill and Schirle (2008) include a rich set of control variables. Their estimates suggest that male workers of all ages suffer substantial and persistent losses in earnings after layoff, which is consistent with the existing literature as well as with the results that we report in this study.3 A key finding is the important role of length of time in the previous job in determining an older worker’s losses in earnings. Men with more than 10 years of service in their predisplacement job suffer losses in earnings exceeding $22,000 (in constant 1996 dollars) in the first year following layoff. Interestingly, these authors claim that the high losses that are statistically associated with age are more closely tied to tenure in the job. They also find that the impact of educational attainment on losses in earnings is not as strong as is typically thought.

The objective of Chen and Morissette (2010), which is based on the LWF, is to discern longterm trends over the period 1979-2004 in postdisplacement labour-market outcomes for workers aged 50-54 years at the time of layoff. Since the labour force evolved considerably over that period, the authors posit that there may have been some improvement in these workers’ reintegration and their ability to adjust, holding aggregate labour-market conditions constant. They detect no upward trend in the postdisplacement re-employment rates of male displaced workers in either the manufacturing sector or the nonmanufacturing sector, although reemployment rates for displaced women generally increased over time. They uncover substantial evidence that median and average earnings losses of males displaced from manufacturing over the period 2000-04 were higher than those of comparable cohorts laid off in the 1980s, most of which they attribute to fewer hours worked as opposed to lower wages. Finally, they find that median and average earnings losses of females displaced from nonmanufacturing jobs fell over time.

A number of studies, most notably Picot, Lin, and Pyper (1998) and Morissette (2004), deal with the incidence of layoffs in Canada in recent decades. Picot, Lin, and Pyper (1998) provide an overview of permanent layoffs in Canada between 1978 and 1993. They are interested in cyclical variations, potential time trends, and the association between layoffs and attributes of firms such as industry-level growth and firm size. They find that the probability that a worker was laid off during the 1990s recession was no higher than during the 1980s recession, with the exception of older workers. The permanent layoff rate was lower in the early 1990s than in the early 1980s, after the factors of sex, age, province, firm size and industry are controlled for. These authors conclude that permanent layoffs have limited sensitivity to the business cycle, as the permanent layoff rate remains fairly high during recovery periods. Rather, permanent layoffs tend to be associated with idiosyncratic events occurring at the level of individual companies; most occur in small and medium-size firms. Fluctuations in the aggregate permanent layoff rate can be attributed primarily to the evolving composition of firms within an industry or within the entire labour force, as opposed to global trends in the layoff rate.

The study by Picot, Lin, and Pyper (1998) is updated by Morissette (2004), who examines the evolution of permanent layoffs over the period 1983-99 for various demographic groups using the LWF database. Morissette’s principal finding is that there is little evidence to show that permanent layoff rates rose substantially between the 1980s and the 1990s. Permanent layoff rates rose from 1989 to 1999 in large firms in the private sector but were stable for small firms having fewer than 20 employees. Temporary layoff rates did rise by at least half a percentage point for men older than 35 years, as well as for women aged 35-44 years and 55-64 years. Morissette (2004) suggests that displaced workers’ chances of finding a new job in the late 1990s fell markedly compared to their chances in earlier periods. He bases this conjecture on a measured decline in hiring rates rather than any tracking of displaced workers following layoff.

Riddell (2009) looks at consequences of layoffs on social welfare that go beyond the two economic outcomes that are typically measured – duration of joblessness and losses in earnings and wages. He cites three studies. Sullivan and von Wachter (2009) determine on the basis of US data that experiencing a layoff causes a nontrivial decrease in life expectancy. Workers with larger losses in earnings tend to suffer greater increases in mortality. There are also adverse intergenerational effects. Using Canadian data, Coelli (2005) finds that the teenaged children of the affected worker are less likely to pursue post-secondary education. Oreopoulos, Page, and Huff-Stevens (2008) report that when children whose parents were previously laid off enter the labour force as adults, their earnings are approximately 9 percent lower than the control group. This next generation also has a higher likelihood of receiving both EI benefits and social assistance.

The findings from this literature can be summarized as follows. In nonrecessionary periods, the median duration of joblessness for displaced workers is approximately five to six months for men and seven to nine months for women. Previous length of job tenure tends to be an important factor in loss of earnings, especially for unionized workers; some of the earnings losses that appear to be due to age might actually be confounded with the effect of job tenure. Long-tenured workers tend to experience high and persistent earnings losses that owe more to re-employment at wages substantially below their prelayoff levels than to unemployment. Prelayoff earnings tend to taper off before the point of permanent layoff.

The empirical approach and methodology that we employ for this study are borrowed from Finnie and Irvine (2006). That study identifies individuals who have exhausted their EI benefits in a given year and examines their sources of income in subsequent years. In this study, we adapt that methodology by identifying prime-age and older workers with strong labour-force attachment who have suffered a layoff in a given year and by examining their income sources in subsequent years.

To construct our sample, we need to define in operational terms what is meant by “prime-age and older workers with strong labour-force attachment.” Following the literature on labourmarket dynamics of displaced workers, we restrict our sample to individuals aged 45-64 who meet our specific criteria for strong labour-force attachment.

To identify the individuals who meet these criteria, we examine labour-market activity for each of seven annual cohorts and retain only those workers who have what we term a “clean” employment record for four consecutive years, defined as follows:

The subsample of older workers with “clean” four-year employment records is obviously much smaller than the entire LAD, which contains information on more than four million individuals for each year. Once we apply our criteria with regard to filing status, age, self-employment status and labour-force attachment, only about 7 to 9 percent (depending on the year) of the sample remains (approximately 315,000 individuals in 1996, rising to 428,000 in 2002). We base our empirical analysis on this subsample.

After we have formed the cohorts of individuals with “clean” four-year employment records, the next step is to determine whether or not the subject experienced a layoff in the following year. Our flag for the event of a layoff is the collection of regular EI benefits in that year. Thus, in order for an individual to be identified as laid off in our sample, the jobless spell following layoff had to last for at least three weeks (owing to the two-week waiting period required to qualify for EI benefits).

As our data set contains no information on the employer, we cannot distinguish between a temporary layoff and a permanent one. An individual who is temporarily laid off but expects to be recalled has a strong incentive to file a claim for EI/UI benefits and, given our sampling criteria, is likely to qualify for them. Thus, workers expecting a recall and receiving EI benefits will enter our sample irrespective of whether these expectations are warranted or not.

The first set of results that we report pertains to the sources of income that laid-off workers draw upon in the years following a job separation. For each cohort, which is identified by the year of separation, we compile the number of individuals receiving a given income source for each of the five subsequent years.4 We separate the sample into two age groups – those between 45 and 59 years, and those between 60 and 64 years – in order to better account for differences in retirement patterns.

These subjects have many potential sources of income during any given year, and many (if not most) individuals have multiple sources of income. We elaborate a typology of income configurations that are prevalent and have labour-market significance and policy relevance. The central thrust is the following: What is the principal source of income for the worker after layoff? We are particularly interested in discovering how many subjects rely primarily on the labour market as opposed to retirement income. The principal source of income is defined as that which accounts for 50 percent or more of the subject’s total income.

For each type of income, we calculate the proportion of all laid-off workers in our sample who received it as their primary income source. For any subject-year observation for which there are only one or two sources of income, there must by definition be a principal source. For individuals with more than two sources of income, we define two additional “aggregates” of primary income sources that cover a large number of individuals and are of interest to policy-makers:

The second set of empirical results that we report measures changes in the employment earnings of laid-off workers in the years following layoff. The sample of laid-off workers is the same as the one from which the first set of results is derived. The losses in earnings are calculated relative to earnings in the last full year for which we observe prelayoff earnings. We note that this calculation will understate the losses in earnings as measured by the counterfactual (that is, what the workers would have earned in a given year had they not been laid off). The most important explanatory variable is age, which we divide into the following categories: 3539 years, 40-44 years, 45-49 years, 50-54 years, 55-59 years and 60-64 years.5

Unlike most research in the literature, we include in our estimates workers nearing retirement age. In many studies, workers over 54 years of age are dropped from the sample in the interest of excluding outcomes related to retirement.6 Nonetheless, it is of great interest to policy-makers to assess the earnings losses of laid-off workers who are approaching an age where retirement becomes an option. If their earnings losses are significantly larger than those of younger age groups, policies to increase these workers’ take-home earnings (whether in the form of employment subsidies or wage insurance) might encourage them to remain in the labour force – albeit receiving lower wages – rather than opting for early retirement.

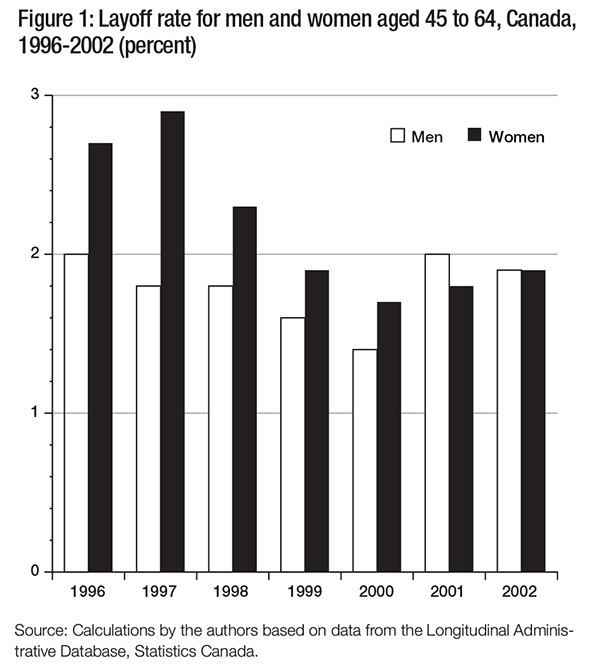

In figure 1, we show the layoff rate over time by sex. The rate for women is slightly higher than it is for men. In 2002 (the latest year in which layoffs are observed), 1.9 percent of workers of both sexes with a high degree of labour-force attachment lost their jobs. Patterns for men and women contrast sharply in prior years. For men, the layoff rate declined from 1996 to 2000 in the context of strong economic growth and then returned to the 1996 level following the slowdown in economic growth in 2001. The layoff rate for women was significantly higher than that for men in 1996 but declined sharply through the rest of that decade and stayed relatively constant from 1999 to 2002. We acknowledge that the sample period is rather short and is dominated by the strong macroeconomic expansion that dominated the late 1990s.

These calculated values are much lower than the estimates of the permanent layoff rate that have been presented elsewhere in the Canadian literature, such as in Morissette (2004). This large discrepancy can be attributed to several factors. First, Morissette’s sample includes only workers between the ages of 15 and 34, who experience higher layoff rates than do older workers. Second, his figures are based on data in which almost all layoffs, quits and dismissals that occur are reported. Other esearch has indicated that well over half of all laid-off workers do not file an EI claim and collect benefits within a two-month window.7 Morissette’s sample of workers at risk for layoff is much more broadly based than ours. While we consider only those we deem to exhibit a high degree of attachment to the labour force, his sample includes many workers who are at the periphery of the labour force, exhibiting some form of nonstandard employment or low labour-force attachment, and who are thus more susceptible to being laid off.

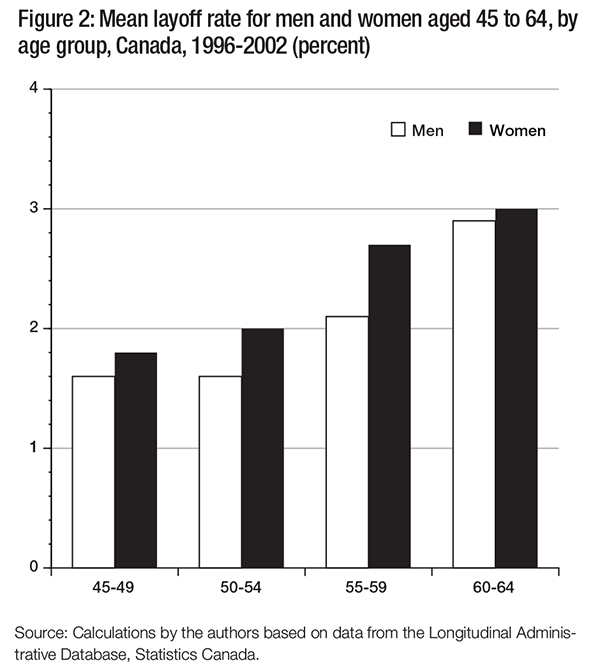

In figure 2, we show the average layoff rate by age group over the entire sample period. There is a strong pattern of rising layoff rates for older workers. The rate for men aged 60-64 is almost double that for those aged 45-49 (2.9 percent compared to 1.6 percent); for women, the rate rises to 3.0 percent for those in the 60-64 cohort. This runs somewhat counter to the notion that workers with longer tenure (and hence likely to be older) are more likely to avoid layoff when their firm downsizes.

Data constraints do not allow us to examine recent trends in the layoff rate for older workers with strong labour-force attachment. However, Statistics Canada’s Labour Force Survey provides more current information on the duration of unemployment by age group, which is pertinent for laid-off older workers. Between 2000 and 2010, the unemployment rate for all workers 45 years and older was slightly lower than that for their younger counterparts. Nevertheless, the proportion of all unemployed older workers who had been unemployed for more than a year was much higher than that of the younger group. In mid-2010, almost 14 percent of all unemployed workers aged 45 and over had been unemployed for more than a year, almost double the rate for those aged 25-44. This provides complementary evidence that laid-off older workers have a much more difficult time finding employment than their younger counterparts, particularly during recessions – even though long-term unemployment increases for both groups during recessions.

The basis for our typology analysis is the likelihood of receiving income from a particular source in a given year following job loss. The 12 possible sources of income are grouped into four categories: labour and investment income, social insurance income, retirement income and a residual category that includes all other potential sources of income. The residual category includes very few individuals; in most years, it accounts for less than 1 percent of all laidoff workers. A subject is assigned a primary income source if that individual obtained more than 50 percent of his or her income from that source. The categories are constructed to be mutually exclusive and exhaustive, and thus their shares sum to 100 percent.

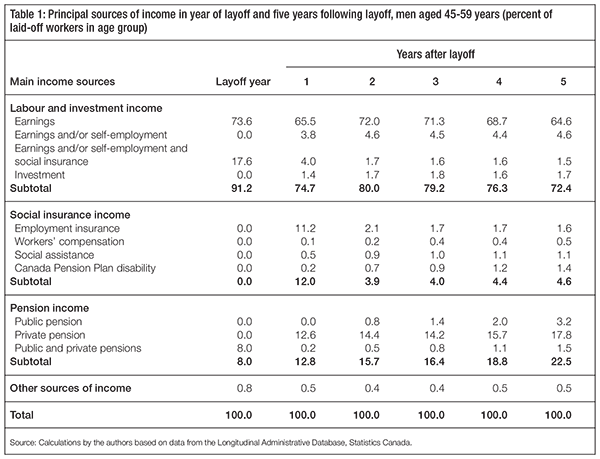

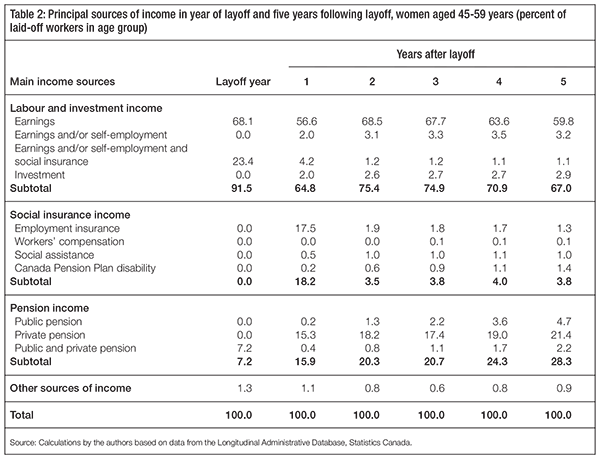

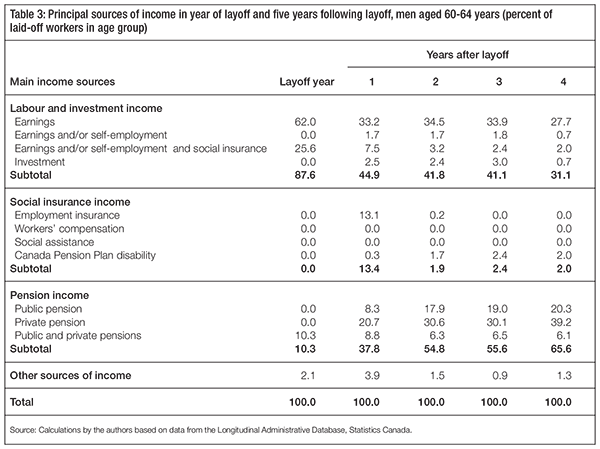

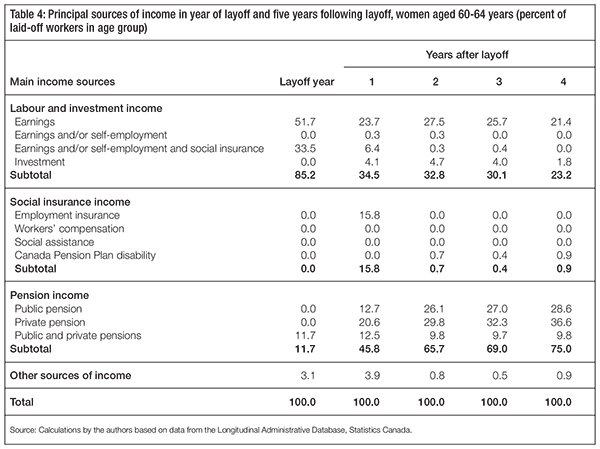

The results of the analysis are presented in tables 1 through 4, separated according to age group (45-59 years and 60-64 years) and sex.8 The columns show the distribution of primary income sources for the postlayoff years. The discussion that follows emphasizes comparisons between reliance on earnings and reliance on pensions, which are almost entirely private for workers below 60 years of age.9 We also discuss briefly the option of self-employment (which is not trivial) and reliance on disability insurance.

Focusing our attention first on the group aged 45-59 (tables 1 and 2), we see that in the five years following layoff, the large majority earned most of their income from the labour market. This should not be surprising, since all of the subjects were highly attached to the labour market before being laid off and they are much younger than the statutory retirement age. In the first year after layoff, 65.5 percent of males relied on labour-force earnings for their primary source of income, a share that increases in year 2 as some workers make the transition from receiving EI benefits to finding employment. By year 5, however, the share of workers relying on the labour market as their primary source of income falls below the previous minimum, reached in year 1. The corresponding shares for women are slightly lower but show the same general pattern. Income from self-employment is small, although not inconsequential: the share of workers having self-employment earnings as a primary source of income rises from 3.8 percent to 4.6 percent among men and from 2.0 percent to 3.2 percent among women.

Turning to the early-retirement option for these “younger” older workers, 12.6 percent of the men relied on private pensions in the year following layoff. As might be expected, these proportions trend upward with time, so that five years after layoff, almost 18 percent of displaced workers have “retired” in the sense that they rely on pensions as their primary source of income. Although we cannot observe these workers’ preferences between labour and leisure, it seems doubtful that such a large minority of workers aged 45-59 would willingly choose pensions as their primary source of income. Although these workers may have access to substantial savings or to a private pension (attached to a high-paying prelayoff job), it seems more likely that they faced poor opportunities on the labour market. We shall return later to loss of earnings.

Leaving the labour force in the wake of a layoff is much more prevalent in the 60-64 age group (tables 3 and 4). Only 33.2 percent of laid-off men count labour-market earnings as their primary source of income in the year immediately following job loss, a number that falls to 27.7 percent four years after layoff. Interestingly, 13.1 percent of these “older” older men (and 15.8 percent of women) apply for and receive EI benefits in the year immediately following layoff, suggesting that many do attempt to find re-employment for a limited time before deciding whether to retire or not.

Not surprisingly, the proportion of men aged 60-64 who rely on some form of pension income after layoff is far higher than that of their counterparts aged 45-59: 37.8 percent, 54.8 percent, 55.6 percent and 65.6 percent in years 1 through 4, respectively. In the case of “older” older women, the share rises from 45.8 percent to 75.0 percent. Note that for laid-off workers aged 60-64, in particular, the incidence of reliance on pension income rises over time for strictly mechanical reasons, as workers age and thus begin to qualify for public retirement benefits.

Turning now to social insurance income, although a significant minority of workers does file at least one EI claim after the initial layoff, in any given year less than 2 percent of both age groups becomes dependent on EI as the primary source of income. Virtually none of the subjects who are older than 59 years do so. This finding is also true for other social insurance income. Hardly any of the subjects we studied meet our criterion of dependence in regard to social assistance, workers’ compensation or CPP disability benefits.

These findings regarding the CPP disability regime contrast sharply with trends in the United States. Black, Kermit, and Sanders (2002) and Autor and Duggan (2006) demonstrate that US disability regimes have evolved from their original function of insuring workers against loss of earnings attributable to a disabling medical event to providing long-term income support for the unemployable. (Both studies label this function “non-employability insurance.”) On the basis of their own research and related studies, the studies conclude that labour-market shocks causing layoffs and reduced opportunities for workers with low skill levels have encouraged a growing and unduly high fraction of displaced workers to withdraw from the labour force and seek disability benefits. We find no such phenomenon in Canada, perhaps because the eligibility conditions for the Canadian program are extremely stringent. The workers in our sample are far more likely to be dependent on early retirement financed by either public pension schemes (up to 20 percent of men aged 60-64 and up to 28 percent of women aged 60-64) or private pension schemes (up to 39 percent of men aged 60-64 and up to 37 percent of women aged 60-64). A further 6.1 percent to 12.5 percent of the group derives more than half of its postlayoff income from a combination of public and private pension benefits.

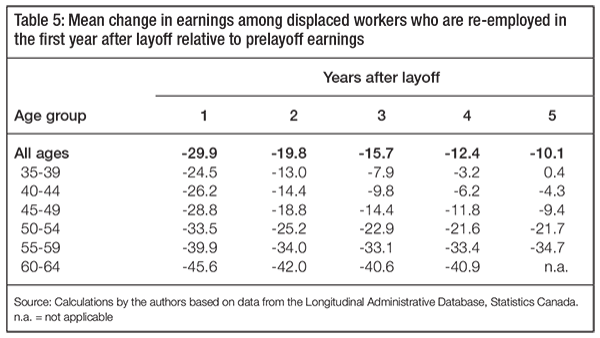

Table 5 reports the values for the mean relative wage losses (in reference to the level of earnings in the year before layoff) experienced by displaced workers. The earnings losses are calculated for both sexes pooled together and reported for each of the five years after layoff. In order to ensure accurate comparisons, the postlayoff wage gaps are calculated for workers who had some labour-market activity during subsequent years, measured as having earnings in excess of $1,000 (constant 2005 dollars). This implies that any worker without earnings for that year, whether that worker was unable to find employment or had withdrawn from the labour force, is not counted.

For all age groups taken together, the mean earnings loss amounts to 29.9 percent of prelayoff earnings in the first year following displacement. However, the loss decreases steadily to just 10.1 percent five years after layoff owing to increases in wages or in hours worked, or a combination of both.

There are sharp differences across age groups along two important dimensions. First, in the year immediately following layoff, the wage losses increase steadily by age. The smallest loss, 24.5 percent, is suffered by the group aged 35-39, while the group aged 60-64 suffers a loss of 45.6 percent. This is consistent with the conjecture that the work experience of older laid-off workers is not easily transferable to potential job vacancies and that long tenure in the previous job may be a liability, limiting the ability of these workers to command high wages. It also may indicate that older workers are more likely to work part-time.

The second striking finding is the evolution of postlayoff earnings over time by age group. At one extreme are individuals aged 35-39. In addition to having the smallest average wage losses immediately following layoff, they see their incomes grow rapidly in subsequent years until they are actually earning slightly more in inflation-adjusted terms than they were before being laid off. The wage losses for those aged 40-44 narrow to a negligible 4.3 percent five years after layoff. This pattern is ubiquitous in the Canadian and US literature on displaced workers: by virtue of their tenure and/or their age, older workers suffer very high losses in earnings in relative (as well as absolute) terms. Since we do not observe a worker’s length of tenure with a firm before layoff, the age variable in all of our analysis is picking up the combined effects of age and job tenure.

It should be noted that because our estimates of losses in earnings pertain only to those laidoff workers who are able and willing to find a job, they are based on a selected sample. They do not capture the counterfactual earnings of those who withdraw from the labour market. As a result, the losses in earnings that we observe may not be indicative of the losses for the entire population of older laid-off workers. The direction of this potential bias is not clear a priori, however. On the one hand, it is possible that those with the least attractive labourmarket opportunities will withdraw shortly after being laid off. This selection effect associated with low potential earnings will cause us to underestimate the losses in earnings. On the other hand, one can imagine an income effect in the case of well-pensioned workers that could work in the opposite direction, if these are workers who forgo high potential wages. To our knowledge, the only study that attempts to assess the direction and magnitude of the bias is Schirle (2007), which suggests that the degree of bias is not high, and that therefore researchers may be able to ignore the selection issue in calculating wage losses.

In summary, the losses in earnings experienced by our sample of older displaced workers are large and persist for years after layoff. Our estimates of the losses in earnings are significantly larger than those reported in the analyses of displaced workers in the United States by, for example, Farber (2004) and O’Leary and Eberts (2007), and somewhat larger than those found for Canada in Morissette, Zhang, and Frenette (2007). Farber’s well-known analysis of displaced workers contains estimates of weekly losses in earnings for those moving from one full-time job to another and finds that the mean wage loss for all ages is in the range of 12.2 percent (during the interval 1989-91) to 5.4 percent (during the interval 1987-89). Unlike our analysis, his sample is not restricted to workers with long tenure in their prelayoff jobs or with established work histories. This may help explain the discrepancy between our results, to the extent that older workers with stable employment histories may have more difficulty in transferring their skills to other occupations than the labour force as a whole. Also, the fact that his sample is limited to displaced workers who find fulltime re-employment (rather than both fulland part-time, as in our analysis) likely plays a role.

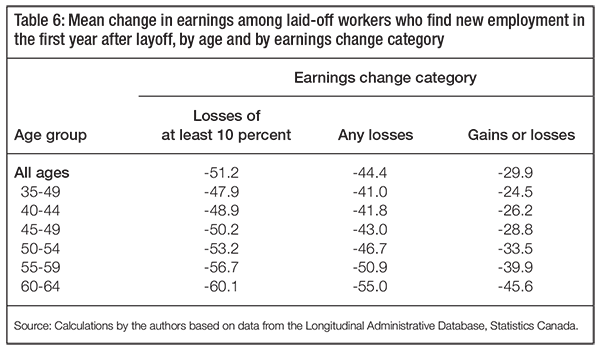

For the purposes of evaluating the typical loss in earnings among the set of workers that might be targeted by a wage-insurance program, we have further divided our sample of laid-off workers into two subgroups: those who experienced any earnings loss at all, and those who experienced a loss exceeding 10 percent of their prelayoff annual earnings (assuming that such a group would be targeted by a wage-insurance scheme). We are deliberately excluding reemployed workers who realized a gain in earnings, as they certainly would not benefit from a wage-insurance program. These calculations are designed to give some indication of the magnitude of losses in earnings that might be partially covered by wage insurance. Table 6 presents the mean losses in earnings for both groups for the first year following layoff.10 Next to these figures it sets out the mean change in earnings for all workers in our sample for the first year after layoff (taken from table 5), revealing that those who lose earnings experience large declines that are somewhat masked by the averages reported in table 5. The average losses that emerge when we exclude those reporting small losses (of under 10 percent) tend to be about 5 to 8 percentage points higher than the corresponding figures for all losers. The average wage losses for those exceeding 10 percent are almost twice as high in percentage terms for the younger workers (nearly 50 percent, compared to about 25 percent for all re-employed younger workers), while the corresponding difference among older workers is only about 40 percent. This implies that laid-off younger workers are more likely to experience wage gains upon re-employment.

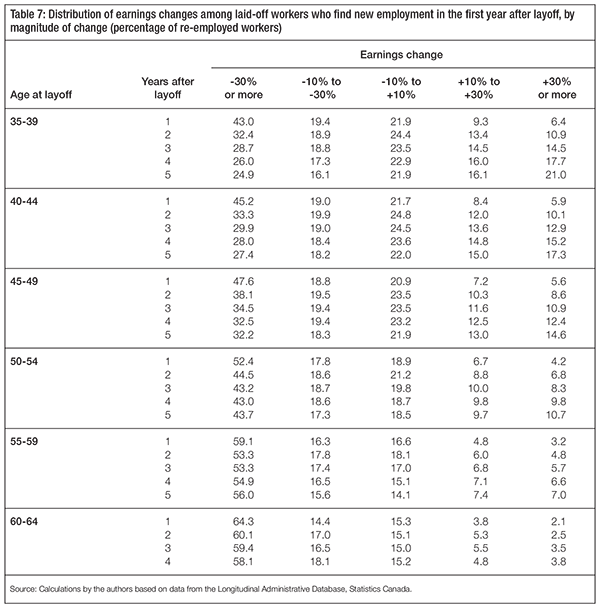

These results give only the means for the distribution of the losses in earnings, which yields no information on their dispersion. In the next part of our analysis, we provide more information on the distribution of the losses by showing the discrete distribution of wage losses and/or gains in percentage terms. In this analytical perspective, the shares will sum to 100 percent. This work is modelled after table 3.15 in Abe et al. (2002), which displays the densities for the distribution according to the following bands of earnings changes: +30 percent or more, +10 to +30 percent, -10 to +10 percent, -10 to -30 percent (which is considered to be a substantial loss in earnings) and -30 percent or more (which is considered to be a severe loss in earnings).

The results from this exercise are presented in table 7, which reports the proportions for the entire sample. The proportions are cross-tabulated only according to age category, and the values are listed for years 1 through 5 after layoff. For all the age groups, the proportion of workers suffering a severe fall in earnings (greater than 30 percent) declines with the elapsed time since layoff, although the decline is marginal for the older age groups. For example, among the 55-59 age group, 59.1 percent suffered a severe wage loss relative to prelayoff earnings in the first year after layoff, and four years later (in year 5), 56.0 percent still found themselves in this predicament. For the categories of 30 percent loss to 10 percent loss (substantial earnings losses) and 10 percent loss to 10 percent gain (fairly flat earnings), however, there are no such patterns. For the younger groups, in particular, the proportion eventually earning more than they did before layoff rises with the number of years elapsed since layoff. Three years after layoff and thereafter, 20 to 30 percent of workers below age 49 do realize earnings gains. For younger workers aged 35-39, the proportion with moderate-to-large gains is almost as large as the proportion with significant losses. In sharp contrast, even after five years, almost 60 percent of workers 55 and older still suffer severe earnings losses.

We find that in any given year of our sample period, approximately 2 percent of our sample of older workers with strong attachment to the labour force experience a layoff, with the rate being higher for those aged 55-64 than those aged 45-54.

During the first five postlayoff years, over two-thirds of the group of laid-off workers aged 45-59 continue to depend on the labour market as their primary source of income. What is somewhat surprising about this number is that it is not larger. Virtually none of them is eligible for receipt of CPP retirement benefits, yet despite that fact, more than one-quarter of the members of this age group derive more than half their postlayoff income from pensions five years after layoff and have thus largely withdrawn from the labour force. The proportion of those aged 60-64 depending primarily on pension income five years after layoff rises to 66 percent.

A significant minority of laid-off workers relies on unemployment benefits as their primary source of income in the first year of layoff, but this proportion drops below 2 percent in subsequent years. Similarly, very few draw on other types of social insurance benefits, such as CPP disability, social assistance and workers’ compensation. This finding contrasts with the situation in the United States, where many older workers are turning to the social security disability regime as a form of “nonemployability insurance.”

For those who do find re-employment, the mean loss in earnings is 29.9 percent during the first year after layoff; this loss declines gradually to 10.1 percent by the fifth year after layoff. First-year mean losses increase steadily with age, rising to almost 50 percent for those aged 60-64. In addition, these initial re-employment wage losses do not narrow appreciably over time for older workers. A significant minority of laid-off workers fail to find suitable new employment and appear to withdraw from the labour force prematurely or become long-term unemployed. For the cohort that was laid off in 2002, 22.7 percent of all age groups combined had little or no earnings in the subsequent year. For all cohorts, the corresponding average figure is 26 percent (29 percent among women and 23 percent among men). This proportion increases significantly with age.

A significant number of these highly attached workers who experience a permanent layoff suffer severe and persistent earnings losses. The most common outcomes for laid-off workers between 45 and 59 years of age, who have not yet reached retirement age, are a return to the labour market, albeit at much lower earnings, and reliance on private pension benefits, in that order. Together, these outcomes account for about 80 percent of all individuals. Among the older workers (aged 60-64 years), reliance on some form of pension income (public and/or private) accounts for about 60 percent of individuals.

The literature on laid-off workers agrees that older workers tend to suffer unduly high adjustment costs. We now enumerate four policy options to address the question of whether older displaced workers should retire early (by choice or by force) or continue to work:

The option of subsidized early retirement, which in the past has been used extensively in certain European countries such as France, would be very popular among its targeted beneficiaries. This scheme was the essence of The Atlantic Groundfish Strategy (TAGS), implemented in response to the collapse of the cod fisheries in Atlantic Canada in the early 1990s.

Trying to apply such a program across the economy, however, would be fiscally crippling. Currently, more than 50,000 Canadians aged 45 and over have been out of work for more than a year. Providing them with a subsistence income would cost $500 million annually, and replacing even a modest percentage of prelayoff income would cause costs to balloon into the billions of dollars.

But, more importantly, financial incentives to keep older Canadians out of the work force are completely at odds with current and future labour-force dynamics and needs. A huge wave of baby boomers has begun to retire and will continue to drain out of the labour force over the next two decades. This will substantially reduce the proportion of individuals of normal working age in the total population and will slow the growth of the labour force. At the same time, the average retirement age decreased significantly through the 1990s and into the early 2000s (although it has risen marginally in recent years), and life expectancy continues to increase. Barnett (2007) and Denton and Spencer (2010) forecast that unless the labour-force participation rates of older Canadians can be increased, the growth potential of the economy is likely to decrease substantially. There is virtually unanimous agreement that a higher rate of labour-market activity among older Canadians is both desirable and feasible, and that encouraging these workers to leave the labour force would be a mistake.

Part I of the EI regime provides primarily passive income support and job-search resources, as opposed to taking active measures to improve the employability of laid-off workers. There is widespread (but not unanimous) agreement that, in its current form, part I fails to address the needs of older laid-off workers and falls short in both efficiency and equity. Gray (2006) argues that, until quite recently, almost all of the policy changes that have been implemented since the major reform of 1996 were expressly targeted to raise the generosity of benefits for seasonal workers. The September 2009 issue of Policy Options (on employment insurance) contains some pertinent quotations. Leonard asserts that most recent changes to the EI regime have “simply encouraged more seasonal employment and long-term dependence on EI” (2009, 14). Courchene and Allan criticize “the practice of allowing short-term labour force attachment to trigger long-term…benefits” in some regions of the country (2009, 22). MacKinnon adds that “workers who have paid into the EI system for many years often discover when they are unemployed that the level and duration of the benefits are insufficient to sustain them until they find a new job” (2009, 32). Riddell (2009), looking at laid-off workers with long tenure in their former job, finds that the targeting of the benefits is not commensurate at all with the workers’ losses in earnings. A common theme running through all of these writings is that EI part I is structured to benefit seasonal workers facing temporary layoff more than full-time workers facing permanent layoff.

Recent changes to the EI regime documented in the “Monitoring and Assessment Report 2009: Employment Insurance” (Human Resources and Skills Development Canada 2010) target a broader clientele than seasonal workers with sporadic work patterns. The Harper government’s Economic Action Plan made all individuals with an active claim for regular EI benefits between March 1, 2009, and September 11, 2010, automatically eligible for five additional weeks of regular benefits. This measure was originally implemented as a pilot project in 2004 (renewed in 2006) restricted to claimants in high-unemployment regions.11 Its extension through the Economic Action Plan was clearly intended to address recession-induced unemployment as opposed to recurrent seasonal unemployment. The Economic Action Plan also included the Extended Employment Insurance Training Initiative, which lengthens the regular EI benefits entitlement period for claimants undertaking training that qualifies under the program, and the Severance Investment Training Initiative, which allows workers who have spent all or part of their employer-provided severance payments on job-retraining ventures to collect all of the regular EI benefits to which they are normally entitled.12 “Long-tenured workers” can receive regular benefits for up to two years in conjunction with job retraining.13 This can include up to 12 weeks of benefits following completion of the job training.

The Targeted Initiative for Older Workers, which dates to 2006 (before the recession), is in the same spirit. With this two-year, $70-million envelope, Human Resources and Skills Development Canada shared with the provinces on a 70-30 basis the costs of interventions for skills assessment, counselling, skill upgrading and work experience for new jobs, intended for “older workers in vulnerable communities in sectors such as forestry, fishing, mining, and textiles.”The program was designed for permanently laid-off workers, particularly those situated in thin labour markets.

This new direction in the targeting of EI resources follows the recommendation made in the document “Expert Panel on Older Workers” (Human Resources and Skills Development Canada 2008), as Beach (2009) points out. The adjustment of the maximum benefit entitlement period to the length of the period of prior contributions constitutes a very significant departure from the previous structure of eligibility and entitlement, modifying it in the direction of a central insurance principle and away from pure income maintenance. Continued movement in this direction will provide needed additional benefits to laid-off workers and may help some of them find jobs and avoid unwanted early retirement.

Human Resources and Skills Development Canada has boosted funding by $1.5 billion for the EI part II regime, which consists of active measures to improve employability, known as Employment Benefit and Support Measures. The federal government delivers these programs in collaboration with the provinces by means of Labour Market Development Agreements. Job training and education are by far the most important tools they use.

Research on the efficacy of these measures indicates that they yield mixed results with laid-off workers. In a recent paper, Frenette, Upward and Wright (2010) investigate the long-term impact on earnings of post-secondary schooling (as opposed to government-sponsored retraining) following job loss. (This study employs a quasi-experimental approach and is based on Canadian data.) The authors find evidence of large gains in earnings associated with participation in post-secondary education among workers aged 25-34, but virtually none among workers aged 35-44.

Human Resources and Skills Development Canada conducted rigorous scientific evaluations for all provinces and territories between 1999 and 2002.14These reports look at three postintervention outcomes: annual hours of employment, annual earnings and number of weeks per year in receipt of EI benefits. Each of these outcomes is measured and analyzed for four types of interventions, which are evaluated separately for a sample of active EI claimants and a sample of former EI claimants. The results show that active claimants who participated in the skills-development intervention (which focuses on obtaining credentials) increased their earnings in 7 of the 12 provinces and territories studied.15 In proportional terms, the gains in earnings are large by international standards – about 10 to 20 percentage points higher than the estimated counterfactual earnings of the control group. The impact on employment activity (estimated to average 211 weeks annually) tended to be positive but subject to a high degree of variability. Active EI claimants tended to fare better than former claimants. Overall, these interventions appear to have a limited effect.

In a survey on adult education and training, Ferrer and Riddell make the following observation: “In summary, government sponsored training has a mixed record, raising earnings of some groups (adult women and displaced workers), but having little impact on earnings of others (disadvantaged adult men and youths). Even when they are positive, the impacts on earnings are modest…training does, however, have a better track record in improving the transition to employment” (2008, 7). They conjecture that the best results are obtained when classroom training has a strong work-experience component linked to local employers. The benefits of training appear to vary among the participants and according to the local labour market and other characteristics that might be difficult to observe prospectively.

Since the evaluative literature on job-retraining programs in the United States is more developed than in Canada and serves as a model for most studies carried out in other countries, it deserves a mention here. Heckman, LaLonde, and Smith (1999) surveyed the first wave of evaluative studies. This early wave of research found that government-sponsored training programs had disappointing results, and that large investments would be needed to plug the gap between former and current earnings of laid-off workers. More recently, Jacobson, LaLonde, and Sullivan (2002, 2005a) examined the impact of community college attendance as opposed to government training programs on labour-market outcomes for laid-off workers. On the basis of administrative data from Washington State, they determined that the equivalent of one year of community college attendance is associated with an increase of 7 percent in annual earnings for older men and 10 percent for older women. Training programs for laid-off workers have, in general, a better track record than those for the disadvantaged. Nonetheless, in a related survey, Jacobson, LaLonde, and Sullivan determined that “for workers late in their careers and with still substantial marketable skills, it [retraining] is unlikely to be the optimal form of assistance” (2005b, 62).

Evaluations in the United States have tended to show that job-training programs do boost future earnings somewhat, but the improvement is not nearly large enough to compensate for the losses typically suffered by an older displaced worker. The missing ingredient, according to Eberts, is closer linkages with employers through sectoral initiatives that can render training more relevant. In an oft-cited piece, he discusses “what works and what doesn’t work in helping workers find jobs” and he examines “some cutting edge practices” (2005, 75). He provides a qualitative treatment of the job-search process and briefly surveys the array of interventions that have been deployed in the United States. He emphasizes publicly provided job-search assistance services that should be provided (and taken up) soon after the layoff occurs. The steps involved in a successful re-employment are “recognition, assessment, search, and if necessary, retraining – [but] successful execution of these steps requires coordination of services and a strong network of information and support” (2005, 83; emphasis added). These job-search-assistance measures are a component of Canada’s Labour Market Development Agreements, they are not fiscally costly and they could have unexploited potential in improving re-employment prospects for older workers.

One innovative policy measure suggested by the authors of the “Expert Panel on Older Workers” (Human Resources and Skills Development Canada 2008) is wage insurance, but its track record in North America is limited. Wage insurance is a policy proposal whereby longterm earnings losses following layoff are partially cushioned by a temporary wage subsidy in the new job. In essence, it fills a portion of the gap between old earnings and new. It aims at encouraging laid-off workers to accept jobs in other industries and/or at lower wages than those to which they are accustomed, in the hope that the experience in the new job will allow wage increases over time to at least partially compensate for the loss of the subsidy when it expires. Another Canadian proponent is Leonard, who states: “Because labour force benefits of training appear to be essentially nil for older workers, it is time for policy makers to think seriously about pilot projects: some sort of wage loss insurance program targeted at older displaced workers, which would partially offset the earnings losses suffered upon re-employment and (we hope) increase the labour force attachment of those older displaced workers who regard early retirement as a second-best option” (2010, 10).

There is a small literature on this in the United States, where it is largely an untried option. Parsons (2000) sets out a conceptual model of the labour market in which the wage-insurance scheme is to operate. The labour market has a dichotomous structure; one segment has high-paying jobs, and the other has jobs that do not pay well but are relatively easy to obtain. Job search is a costly activity and takes place in an uncertain environment. From both an empirical and a theoretical perspective, those in the secondary labour market have little need for wage insurance. What he finds to be the most appealing feature of wage insurance is that it targets assistance to a group of laid-off workers whom he views as both needy and underserved by the UI regimes that exist in the United States: those who experience large losses over extended time periods.

LaLonde (2007) is an enthusiastic proponent of wage insurance. He believes that relative to the conventional UI system, it provides very strong incentives for job search. Furthermore, he views it as superior to a one-time re-employment bonus, because in the latter case, the recipients receive no further bonus once they have landed the first postlayoff job.16 In addition, the size of the bonus payment has no relationship to the loss of earnings stemming from the layoff. However, the net additional income from a better-paying job is lower under a wage-insurance scheme and therefore the wage-insurance scheme weakens the incentive to search for higher-paying jobs. This disadvantage is not found with either the re-employment bonus or the absence of any intervention. LaLonde recommends a long benefit entitlement period for wage insurance – perhaps two years or longer – which he bases on the fact (confirmed by our results) that affected workers can suffer wage losses for many years. He points out that the only members of the working poor who would claim wage-insurance benefits are those who had been laid off from a job that paid higher wages. This factor mitigates the cost of the program. In theory, the wage-insurance program would be quasi-universal and many workers would qualify, but in practice, the benefit levels would be low for this particular group of workers.

Like the work of LaLonde, the study by Kling (2006) reads something like a manifesto. His discussion of wage insurance is coupled with what he calls a “temporary earnings replacement account” (TERA). Together, his reform proposals are tantamount to a complete restructuring of UI in the United States and EI in Canada, which, as he says, would be an end to UI as we know it (31). The core principle is that in the event of temporary layoff, smaller, short-term needs can be met through private savings and borrowing, thus allowing for more public funds to be earmarked for workers facing long-term wage losses following re-employment. The current system focuses solely on short-term cash transfers. The minority of layoff victims who face long-term losses in earnings would benefit greatly from a wage-insurance scheme.

Although she is a proponent of wage insurance, Kletzer (2004) suggests that there might be some incentive for workers receiving wage insurance to accept work too quickly, which would lead to suboptimal matching of workers and jobs. She notes that inherent in the program is a trade-off between the efficiency objective and the indemnification one: the greater the incentive for reemployment, the less generous the program. Kling (2006), however, argues that wage insurance will make the discouraged-worker syndrome less common, and that, in most cases, workers will not be induced to accept unappealing jobs quickly; he believes that neither conventional UI nor wage insurance has much influence on the characteristics of future jobs. He expects wage insurance to provoke a significant increase in intensity in the search for employment, tantamount to an increase in the supply of labour. All other factors held constant, he believes, an increase in aggregate employment would result, and hence a slight increase in revenues from EI contributions and shorter durations of unemployment. Economic theory also predicts that there would be a decrease in wage levels in the aggregate, but that empirically the effect would probably be very small. Kling rules out the possibility that jobs that are subsidized by wage insurance (which is indeed the case) would cause a displacement effect such that other jobs would be eliminated.

Finally, Kling mentions a possible misuse, or abuse, of a wage-insurance scheme. Given a certain level of weekly or monthly earnings, the firm and particularly the worker have an incentive to report that the worker is working long hours at a low wage rather than short hours at a high wage.17 This potential gaming of a wage-insurance program should be addressed by imposing fines on firms in violation. Furthermore, unless the firm places all of its workers (not just those who participate in the wage-insurance scheme) within a lower-than-standard pay grade in such an arrangement, an enormous and visible inequity will emerge, which would damage labour relations and hurt the firm’s image. The desire to avoid overt wage discrimination also explains why a low-wage employer would not be able to capture the entire subsidy embedded in wage insurance by paying the workers who participate in the program commensurately lower wages.

Jones (2009) is the most recent Canadian study that treats wage insurance. In his view, its primary advantage is related to equity. As mentioned earlier, the labour market of the advanced, postindustrial economy is extremely dynamic and is constantly adjusting to changes in trade patterns, the technology of production, the organization of firms, the instability of banking systems and other shocks. Although these forces result in major gains in productivity and hence living standards in the aggregate, the costs of adjustment are borne by a minority of the labour force, and they can be very steep. In order for the gains to be shared among those who have lost the most, it is desirable on equity grounds to compensate these workers. Such a policy also facilitates future adjustment by attenuating lobbying aimed at antiliberalization measures.

Jones asserts that the behavioural responses stemming from wage insurance will be minor and the efficiency gains will be unimportant. As suggested earlier, the efficiency effect might cut both ways. On the one hand, wage insurance might induce certain participants to accept work for which they are overqualified, even though continuing their job search would be warranted and more efficient. On the other hand, wage insurance almost certainly reduces the wage that workers are willing to accept, leading to faster re-employment, all other factors held constant. Jones also points out that the size of the targeted group – high-seniority laid-off workers – is quite small relative to the size of the labour force; he estimates that perhaps 10 percent of all laid-off workers meet that criterion.18 One should not expect the program to save money, but it would not be fiscally burdensome because eligibility would be limited to workers with long tenure. His overall assessment is that there is an appealing case for a limited wage-insurance program because of the substantial earnings losses of laid-off workers with long tenure, the apparent inability of other policy levers to tackle the problem and the promise of wage insurance to improve the lot of this group.

Although a large-scale wage-insurance program has never been implemented in Canada, a pilot program was undertaken as part of the Earnings Supplement Project (ESP) between 1995 and 1998. This project consisted of two randomized social experiments sponsored by Human Resources Development Canada and conducted by the Social Research and Demonstration Corporation. The ESP provided a financial incentive designed to promote rapid re-employment among laid-off workers. Like wage insurance, it provided a top-up benefit to earnings received by workers who were re-employed at wages that were lower than the prelayoff level. Bloom et al. (2001) describe the program and subject it to scientific evaluation.

The terms of the earnings supplement were fairly generous. Eligible workers had to be permanently displaced from their former jobs. Any worker who expected a recall, either with or without a specific date, was excluded from the sample that was used for the evaluative study. Before becoming eligible for the program, all workers were entitled to at least 38 weeks of regular EI benefits. In order to qualify for the wage supplement, they were required to find a new full-time job within 26 weeks of entering the program. The replacement ratio of benefits to the loss in earnings was 75 percent (up to a maximum of $250 per week) and was paid for a period of up to two years. As a result, total income from earnings supplemented with the wage-insurance payment was potentially far higher than standard EI benefits, in principle providing a strong incentive for re-employment.

The experiment took place in the late 1990s, a time of strong economic growth and robust labour markets. The sample of 5,912 permanently displaced workers (before the point of randomized selection) cannot be considered as representative of the Canadian labour force, as the workers were drawn from only five cities. By research design, however, the observable characteristics of the treatment group were similar to those of the control group. Most of them had a fairly high level of tenure with their previous employer: 86 percent had been working at the same firm for more than one year.

The results of the ESP experiment in terms of take-up rates were disappointing. Among all of those who were offered the earnings supplement, only 20 percent found a lower-paying job in the required 26 weeks and received benefits. Those in this minority did benefit heavily; however, they received benefits for an average of 64 weeks, and their re-employment income (including the income supplement) averaged 88 percent of their earnings before layoff.

The main reason for not receiving wage-insurance benefits was not finding a suitable job within the required time period: 58 percent of the treatment group was not able (or willing) to do so. A relatively small group of workers (13 percent) found a new job at equal or better wages than their previous job and thus had no need for wage insurance. A relatively small number in the treatment group returned to work with the former employer (and were thus disqualified) or enrolled in an education or training program. The data measuring the workers’ job-search activities indicate that the ESP supplement offer had almost no effect.19

The only evidence that is available regarding the low take-up rate is qualitative. Bloom et al. conducted a follow-up survey that found that many subjects were able and willing to remain jobless and continue their job search until an appropriate offer arrived. Very few workers considered participating in the ESP during the early stages of their job search, but take-up rates did rise toward the end of the “window of opportunity.” According to Bloom et al., “These findings further reinforce the conclusion that the main barrier to supplement use was an inability to quickly find suitable [full-time] work” (2001, 514). They assess the overall efficacy of the ESP as follows: “It appears that this approach can help cushion the shock experienced by some displaced workers, as they try to make a transition from their past to their future, but it is not likely to change this future” (2001, 522).

Babcock, Congdon and Katz (2010) appeal to behavioural economics to provide new arguments in favour of developing a wage-insurance program, which may shed light on why the ESP did not live up to expectations. In essence, they argue that psychology plays an important role in economic decision-making, and in some cases leads to poor choices. In the case of displaced workers, they suggest that those searching for a new job face psychological barriers to re-employment that are likely to prolong the jobless spell. In particular, they posit that many displaced workers have excessively high expectations of the wages that they can command in the market, are averse to large pay cuts and are prone to procrastination when it comes to searching for a job. These effects may reduce the intensity of their job search and make them unwilling to accept realistic wage offers or jobs that are different from their former jobs. The authors conclude that wage insurance that covers a large portion of the re-employment wage gap could offset many of the psychological obstacles faced by laidoff, long-tenured workers, and that “By manipulating the realized values of wages…and making job offers more attractive, it averts to some degree the impacts of biased wage expectations and mitigates the effects of loss aversion. In the longer run, it may smooth the painful but sometimes necessary process of psychological adjustment to lower-wage employment” (6). They also note that, to be effective, wage insurance should cover a large portion of the re-employment wage gap.

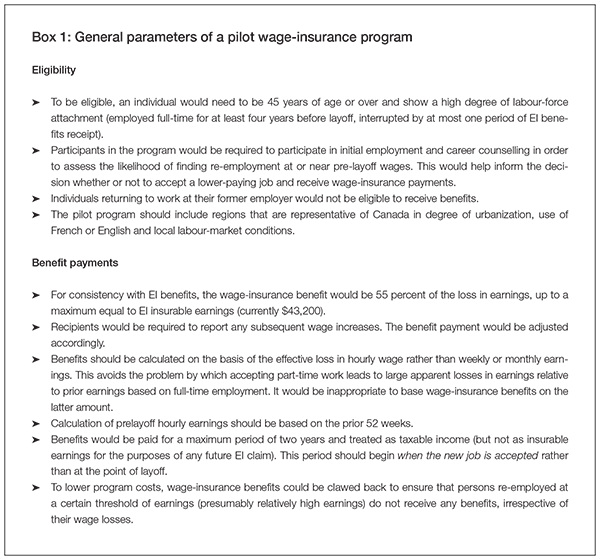

What lessons can be learned from the ESP? Our main conclusion is that changes in the program’s design could significantly improve its effectiveness. It would appear that the most important challenge facing its successful implementation is to encourage participation at relatively early stages of the job search. Unless this obstacle is surmounted, take-up is likely to be postponed until a late stage of the job search, which undermines the efficacy of wage insurance. It is probably a hard task to convince many permanently laid-off workers – especially those with high seniority, at whom the intervention is targeted – that their salvation lies in accepting a job with significantly lower pay (and perhaps lower prestige) than the one they recently lost. It does not seem reasonable to expect them to reduce their wage expectations and aspirations significantly until they have been unsuccessful in their job search for perhaps many months. To alleviate this hindrance, we suggest that several modifications (detailed in box 1) be considered for a redesigned pilot project. First, the requirement for entry that a full-time job be obtained should be loosened to include part-time jobs, which should encourage a quicker return to the labour force and eventually lead workers to find a full-time job. In this instance, the wage-insurance benefits would be prorated according to the length of the work week. Second, eligible workers should be required to avail themselves of the job-search assistance provisions that are already part of the EI part II regime. We note that this was not a stipulation of the ESP intervention. Reinforced employment counselling could potentially clarify workers’ wage and employment expectations and help develop more fruitful job-search activities, so that perhaps the new job would not involve a large pay cut. Third, the length of the eligibility period for finding the new job should be extended beyond 26 weeks from the point of layoff.

Population aging means an increase in the number of workers who lose their jobs (as a result of either structural shifts in the labour market or cyclical economic conditions) at or near potential retirement age. Because older laid-off workers often have more difficulty than their younger counterparts in finding suitable employment at prelayoff wage levels, they may be tempted (or forced) to retire early, a trend that could both curtail future economic growth and add to existing fiscal pressures on public and private retirement-income systems.

Careful analysis of the income sources of older laid-off workers in this study shows that a surprisingly high proportion depend on some form of retirement income rather than seeking reemployment. About one-quarter of those laid off aged 45-59 (who in principle are not yet eligible to receive CPP benefits) effectively withdraw from the labour force within five years. Among those aged 60-64, the proportion rises to 66 percent for men and 75 percent for women.

Older laid-off workers who do succeed in finding new jobs suffer substantial losses in earnings relative to prelayoff earnings, on the order of 35 to 40 percent. These losses remain persistent, in sharp contrast to the experience of these workers’ younger counterparts.

Given the particular labour-market difficulties faced by older laid-off workers, as well as the fact that their numbers will grow in coming years, it is imperative for policy-makers to devise adjustment policies that best serve their interests and the interests of the economy as a whole. Encouraging involuntary early retirement via taxpayer-funded payments to older displaced workers would address the problem of income loss among those not yet eligible for public or private pensions, but it would be very costly both in terms of dollars and the adverse effect on overall economic growth. For this reason, it is neither a viable nor an appropriate option.