Canadian Policy Prescriptions for Dutch Disease

Robin Boadway, Serge Coulombe and Jean-François Tremblay

Canada’s productivity growth record has been mediocre by international standards, which does not bode well for our future standard of living. Many explanations have been advanced over the years for Canada’s lagging productivity performance. A recurring theme is that Canada’s disappointing record is due in part to a lack of innovation in the business sector of the economy. Despite the implementation of many remedial federal programs, neither our productivity growth nor our commercial innovation record appears to have improved appreciably relative to those of other advanced countries. This paper addresses the question of whether policies intended to encourage commercial innovation have been misdirected or misapplied and, if so, whether there are lessons for future policy design.

The author begins with a survey of informed opinion regarding the nature and severity of Canada’s productivity growth problem. Productivity growth rates can vary for many reasons and the role played by innovation is difficult to measure, as is innovation itself. Moreover, the effect of weak productivity growth on national income may be offset by improvements in Canada’s terms of trade with the rest of the world. Given these caveats, the evidence suggests that Canadian productivity growth has been relatively slow by international standards, and that this is attributable in part to a relatively slow rate of organizational, technological and commercial innovation. Some of this may be a result of the underlying characteristics of the Canadian economy, but some is also due to the public policy environment.

Of particular importance for public policy is the market environment in which potential innovators operate. Marketplace factors bear directly on market opportunities and rewards, the drivers of commercial innovation. These factors include effective access to markets both in Canada and internationally; market rivalry; market integrity (e.g., certainty about rules regarding regulation, proprietary rights and restrictions on collaboration). Taxation, in particular, requires more attention, and this goes beyond specific tax measures such as the scientific research and experimental development (SR&ED) tax credit. While it is generally acknowledged that commercial innovation must be market driven, public policy has tended to focus more on encouraging the supply of scientific knowledge.

The author goes on to examine the evidence on the effects of public policies to support commercial innovation, including the support of financing institutions, the support of linking institutions, tax policies supporting SR&ED and direct subsidization of research and development.

On financing innovation, analysts have long debated whether there are “gaps” on the supply side of capital markets or a lack of investment opportunities. The consensus seems to be that the venture capital market needs more “experienced” money, rather than simply more money – past government tax incentives for venture capital investors have attracted new money, but much of it has not proven to be experienced or smart. Some suggest there is a role for government-backed venture capital organizations that can mimic the best practices of private-sector investment banks, but others question the need for a government institution that simply duplicates the work of private-sector counterparts.

A major focus of public policy in Canada has been to facilitate and encourage links among government laboratories, university researchers and the business sector. While this focus has been successful, some analysts caution that the main economic contribution of universities should be education, rather than commercial innovations.

Canada’s SR&ED tax credit is relatively generous by international standards, but in spite of this, business sector R&D intensity remains low by the standards of other industrialized countries. In addition, other business taxes may offset the effect of the credit. Two useful suggestions for reform are broadening the eligibility for refundable credits and reducing the discrepancy between the respective credit rates available to small Canadian-controlled private corporations and larger firms.

Many federal grant programs purporting to support innovation, such as the Economic Development Program, have been unequivocal failures, largely because they pursued a multiplicity of policy objectives, some of which were not consistent with innovation or productivity growth. Other programs, such as the Industrial Research Assistance Program, have a better track record, but they must recognize that their objective is to improve use of resources (including human resources), rather than to simply provide employment.

The author concludes that the commercial innovation problem is essentially one of opportunities and rewards for entrepreneurship. If governments are truly concerned about the innovation gap and serious about reducing it, they must depart from the “science-push” approach to innovation of the past 40 years and face the politically difficult tasks of reducing taxes on work, savings, investment and risk taking, and easing marketand competition-restricting regulation.

Canada’s productivity growth record has been mediocre by international standards, which does not bode well for our future standard of living. Many explanations have been advanced and, indeed, many factors have been in play over the years. A recurring theme is that Canada’s disappointing record is due in part to a lack of innovation in the business sector of the economy. For more than 40 years, this theme has been the subject of debate and a virtually endless series of remedial policies, and the focus of numerous federal and provincial government programs. Ministries, departments, councils, committees and panels have come and gone. Yet neither Canada’s record on productivity growth nor that on commercial innovation appears to have improved appreciably relative to the experience of other advanced countries. Indeed, they may have become worse.

The apparent lack of incentive for commercial innovation has been intractable from a policy perspective. Although the problem might have been worse were it not for the programs that have been put in place, it is hard to avoid the conclusion that results have fallen well short of expectations. This paper addresses the question of whether federal policy responses have been misdirected or misapplied. Have policy-makers learned anything? If it was misguided before, is policy on the right track now?

The paper takes a historical perspective, since the disenchantment with public policy toward commercial innovation goes back a long way. In a 1970 report, the Senate Special Committee on Science Policy concluded that

[s]ince 1916, too, the main objective of Canadian science policy has been to promote technological innovation by industry…. Almost every decade since the 1920s has witnessed renewed attempts by successive governments to achieve it but, on the whole, they have all failed. What progress has been made in this respect results almost exclusively from the initiative of industry itself. (1970, 111)

If innovation policy has not accomplished much, it is not for want of attention, at least during the past half-century – Canada ranks highly internationally in the study of innovation policy, if not in innovation itself. Contrary to George Bernard Shaw, we can learn something from history, at least in this case. There are some commonalities. Some support programs, either by design or default, have pursued a variety of objectives of which some were antithetical to innovation. Policy might also have had too narrow a focus, placing too much emphasis on reducing the perceived cost of business research and development (R&D) and not enough on making the economic climate more hospitable to entrepreneurship.

The debate over public policy toward commercial innovation runs along deep and familiar lines. There is the big government-small government debate, with proponents of the former advocating high taxes and selective give-backs to encourage specific manifestations of innovative behaviour, while advocates of the latter recommend lower taxes in general. There is the nationalist-internationalist debate, with nationalists focusing on the development of and reliance on domestic institutions and linkages, while internationalists recognize the role that immigration, foreign institutions and linkages and foreign-owned firms play in the innovative process. There is the structuralist-behaviourist debate, with structuralists advocating support of designated (“strategic”) industries and firms (“winners,” “champions” or “anchor tenants”), while behaviourists focus on the impediments to innovation that existing firms and industries face.

The innovation issue runs deeper yet. There is much talk about the need for an innovation culture. At one level this is trivial – amounting to periodic exhortations from politicians, think tanks and business leaders to be more innovative. There is, however, something more fundamental involved. Any important innovation threatens existing interests and entitlements, and threatened interest groups might be able to forestall innovation politically. It is the degree to which the political process insulates itself from the pressures of entrenched interests that is the mark of an innovative society. A political environment in which innovation policy is merely a payoff to one more lobby group (“the science lobby”) is unlikely to generate much in the way of either innovation or productivity growth.

I begin with a discussion of the productivity growth and commercial innovation problems. This is important, because productivity growth rates can vary for many reasons and innovation is difficult to measure. Innovation takes a variety of forms and there is no particular reason for Canada to mirror another country. If it ain’t broke, we don’t need to fix it. Those seeking to have their agenda implemented argue there is a crisis that demands attention. Is there a crisis?

I then discuss characteristics of the Canadian economy that impede innovation. Here I note the importance of distinguishing among factors that are readily amenable to changes in public policy, those that might be amenable over the long term to fundamental policy shifts and those that are immutable.

I then go on to examine policies and policy options with regard to various features of the innovation system. These include linkages and linking institutions, financing, tax incentives and direct government support of business innovation. I offer some concluding observations in the final section.

Discussions of public policy toward innovation often refer to “innovation systems” and “externalities” or “spillovers,” terms I also use in various places in this paper, so it is important to define them.

An innovation system is the totality of knowledgeproducing and knowledge-using organizations and the interactions among them. The national systems approach recognizes that innovation can be the result of learning-by-using and learning-by-doing, as well as various forms of research activities of varying degrees of formality and orientation. This approach emphasizes the importance of linkages among the various sources of learning and also of linking and facilitating institutions. One insight of the innovation systems approach is that sustained innovation is often a consequence of the existence of a geographically concentrated critical mass (cluster) of innovating organizations.

A positive externality is a benefit conferred on others for which the source of the benefit is not compensated. This is often referred to as a positive spillover, although the term is frequently misused. Innovation generates positive externalities to the extent that the innovator is unable to appropriate the fruits of it. The benefits of an innovation are inappropriable, at least in part, if it can be copied, reverse engineered or otherwise pirated by others. Innovations of this nature might be unprofitable even if they are beneficial to the economy as a whole, in which case, public policy can encourage innovative activities that are unprofitable but likely to yield high economy-wide (social) rates of return.1

Public policy can encourage socially beneficial but unprofitable innovative activities in many ways. Intellectual property rights (patents, copyrights, trademarks) serve this purpose, as do “neighbouring rights” (such as fees paid by users of copyrighted material, taxes on blank audio tapes and CDs rebated to composers and performers). Subsidies and tax incentives can also be used as a top-up when profitability is insufficient but the economy-wide rate of return is high. This is called the “economic efficiency rationale” for the support of innovation. Experience shows, however, that this concept is not easy to operationalize.

The first question to deal with is whether there is a productivity growth problem. Sharpe makes a convincing case that the rate of growth in labour productivity in Canada has been low by international standards and especially in comparison with the United States:

Canada’s productivity growth record has been dismal, both from an historical and an international perspective. Since 2000, Canada’s labour productivity performance has deteriorated relative to both our performance during the second half of the 1990s and relative to the performance of labour productivity in the United States in the 2000s…. Canada’s manufacturing productivity performance since 2000 has been even worse than the business sector performance. Output per hour advanced at only a 0.6 per cent average annual rate between 2000 and 2006, compared to 5.5 per cent per year in the United States. In other words, U.S. manufacturing labour productivity growth has been nearly ten times as fast as that of Canada! (2007, 21)

A number of other commentators have come to the same conclusion. Hodgson, for example, says, “Canada is a laggard on productivity, which directly affects its standard of living. Indeed, Canada has lagged behind most major OECD [Organisation for Economic Co-operation and Development] countries in productivity growth for decades. From 2000 to 2005, Canada’s annual productivity growth ranked 10th among 17 higher income OECD countries” (2007, 3). Statistics Canada reports that Canadian labour productivity was 92.6 percent of US labour productivity in 1994, rose to 94.1 percent of the US level in 2000, then collapsed to 89 percent in 2005, and cites several factors that may have contributed to this decline: “In recent years, the Canadian economy has experienced several shocks, including the severe acute respiratory syndrome crisis, the outbreak of [mad cow disease], the power blackout in Ontario, and the sharp appreciation of the Canadian dollar” (2007a, 3).

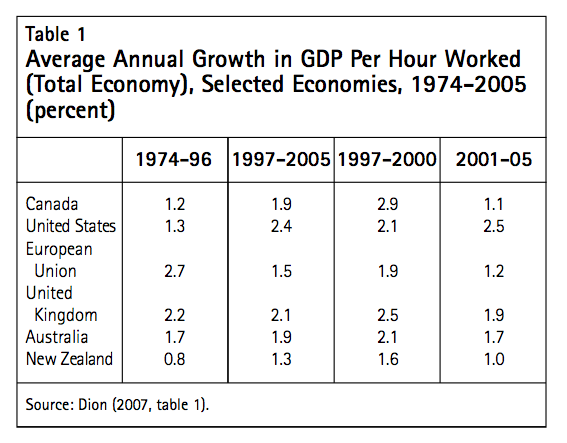

Dion provides more detail (see table 1), also observing that Canadian labour productivity growth accelerated during the late 1990s only to fall back below its (“sluggish”) historic growth rate after 2000 (2007, 20). He notes that one can see a similar though less pronounced pattern in productivity growth rates in the European Union, Australia and New Zealand. The United States, in contrast, experienced an increase in its rate of labour productivity growth after 2000. It is apparent that, while Canada has had favourable productivity growth at times and relative to certain other countries, the general conclusion that Canada has been a laggard is not unwarranted.

Potential solutions to the problem of slow growth in labour productivity vary depending on the reason that growth has been slow. The sources of labour productivity growth are:

Dion attributes the brief spurt in Canadian labour productivity growth between 1997 and 2000 to capital deepening and MFP growth that resulted, first, from the information and communications technologies (ICT) boom and, second, from cyclical factors. The increase in ICT investment increased capital per worker (capital deepening), which increased labour productivity. The ICT boom also increased capacity utilization in ICT-producing industries, which resulted in an increase in MFP in those industries. Other sectors of the economy also experienced MFP growth, as they were able to use their existing capital stock and labour force to expand their output (Dion 2007, 22). Both the ICT investment effects and the cyclical expansion effects on productivity fell off after 2000.

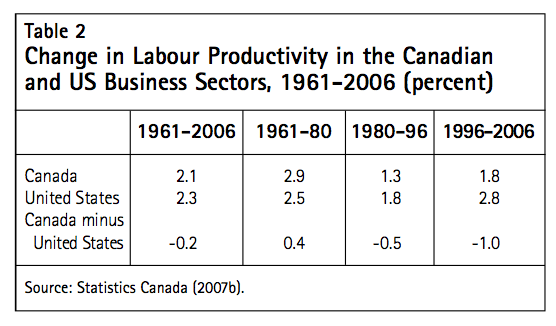

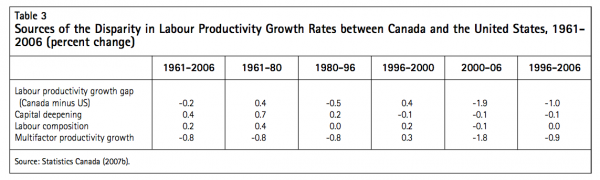

A Statistics Canada study (2007b) provides further insights by comparing business sector productivity growth rates in Canada and the United States over the longer term (45 years) (see tables 2 and 3). The study finds that, although rates of labour productivity growth in the two countries were roughly the same over the entire period 1961 to 2006, Canada’s rate has been lower than that of the United States for the past 26 years and the gap is widening. As well, over the long term, the rate gap is due almost entirely to the much higher rate of MFP growth in the United States. The study also finds that MFP growth was faster in Canada than in the United States between 1996 and 2000 but much slower between 2000 and 2006.

MFP growth is often associated with technological change, organizational change, economies of scale and utilization rates. But, to paraphrase Moses Abramovitz, it is also a measure of our ignorance (1956). In essence, over the period 1961-2006, relative to that of the United States, Canada’s labour force improved in quality, and the amount of its capital per worker increased, yet output per hour grew at roughly the same rate in the two countries. For some reason, the US business sector was able to do equally well with less.

Dion explores three possible explanations for Canada’s relatively low rate of growth in MFP over the period 1996-2006:

Ӣ increased adjustment costs associated with inter-industry shifts in labour and capital due to the change in the exchange rate;

Ӣ diminishing returns in the extractive (mining and oil and gas) industries; and

Ӣ impediments to innovation.

He concludes that adjustment to exchange-rate changes had a negative effect on productivity growth but it is difficult to measure and that diminishing returns in the extractive industries had a significant negative effect on aggregate productivity growth. He sees both these factors as exacerbating what he calls the long-term drag on MFP growth due to the relatively low level of innovative activity in the Canadian economy (2007, 29).

It is important to understand that, while the rate of MFP growth is sometimes called the rate of technological change, it is influenced by many factors and these can dominate over shorter periods of time. In their study of the sources of MFP growth in Canada, Baldwin and Gu (2007) find that, over the period 1961-2002, the rate of sectoral MFP growth (based on value added) varied from 2.02 percent annually in the information and cultural industries sector to -2.48 percent annually in the professional, scientific and technical services sector. Observed negative rates of growth in MFP in some sectors are a little hard to square with the interpretation of MFP growth as technological change (what is “negative technological change”?). Baldwin and Gu suggest that negative MFP growth rates in some sectors might be methodological problems with the measurement of output. It has also been suggested that negative MFP growth in the mining and oil and gas extraction industries could be due to the use of lower-quality resources (such as the oil sands). Of course, Canadians are still better off if the output of this industry (crude oil, for example) can be sold on international markets at commensurately higher prices.

As far as the real income of Canadians is concerned, an improvement in our terms of trade (what our exports will buy on international markets) is as good as an improvement in technology. While MFP growth has lagged in Canada, we have done extremely well in recent years on the terms-of-trade front (see Kohli 2006). Indeed, as Macdonald (2007, table 2) reports, Canada’s real gross domestic income (GDI) per capita – what we can buy with what we produce – increased much faster than US real per capita GDI over the 2002-06 period.

We need to exercise caution before going into crisis mode, but according to the best available evidence, the rate of growth in labour productivity in the business sector has been lower in Canada than in the United States for a fairly long time, due in large measure to Canada’s slower rate of MFP growth. A number of factors could be in play, but one can reasonably conclude that its relatively lower rate of MFP growth over the longer term reflects a slower pace of organizational and technological change than in the United States.

The ultimate result of innovation is MFP growth, but there are many kinds of innovation and they are difficult to measure. Innovation does not have to be technological in nature and it does not have to involve formal R&D. As Nathan Rosenberg wrote years ago, a great deal of innovation is the accumulation of small, unremarkable process improvements. These innovations reduce the costs and increase the profits of the firms that make them but they might not be announced or even be countable.

There are, however, proxy measures or indicators of innovative activity. For example, a rough distinction can be made between innovative output that is potentially commercial (proprietary science) and innovative output that is freely accessible (open science, generally the product of research in universities and public research institutes). A further distinction can be made between inputand output-based measures of innovation. Measures of commercial innovative output include patents granted, triadic patents granted, patents granted and cited, royalty and licensing income, world-first innovations introduced, nationalfirst innovations introduced, sales revenue from worldfirst or national-first innovation, the number of new start-up firms, growth of start-up firms and initial public offerings of innovative start-ups and exports of high-tech or R&D-intensive products.2 With respect to open science, common measures of output are peerreviewed publications, publications in highly ranked journals and both academic and commercial citations. Business use of open science – for example, as indicated by citations of scholarly publications in patent applications – is sometimes referred to as “indirect commercialization” (Australian Institute for Commercialisation 2003). The number of graduate and undergraduate science and engineering degrees awarded can also be viewed as a measure of innovative output. Common input-based measures of innovative activity include employment of scientists and engineers, spending on R&D and investment in advanced manufacturing technologies and information technologies. All these measures are normalized to take account of the size of the industry or economy involved.

Canada is among the several countries that have conducted surveys of commercial innovation. Therrien and Mohnen (2003) compare the results of five national surveys of innovation conducted over the period 1997-99, and find that Canadian firms are more likely to be innovators but derive a smaller fraction of their sales from innovations than firms in Germany, France, Ireland and Spain. They note:

Canada leads the pack by far if we consider the percentage of innovating firms in the respective country samples, however it ranks last if we consider the share in sales of innovative products. It is also among the best, but no longer outdistancing them, if the criterion of performance is the percentage of first-innovators, and again it trails if the criterion is the share of innovative sales among first-innovators. Unfortunately, quantitative data on the share of sales specifically due to first-innovation is not available in Canada. (2003, 368)

One way to gauge innovative activity is through the use of triadic patent intensity measures. A triadic patent family is formed when patent applications for the same invention are filed in Europe, Japan and the United States. Triadic patent intensity can be measured in a variety of ways, including the ratios of patents to gross domestic product (GDP), to gross expenditure on R&D (GERD) and to business expenditure on R&D (BERD). In 2005, Canada ranked fifteenth of 30 OECD countries in triadic patents per dollar of GDP, seventeenth in the ratio of patents to GERD and fifteenth in the ratio of patents to BERD.3 It appears that, by these measures, Canada’s rankings are due less to its relative R&D intensity than to the nature and patentability of the R&D that is done in this country. When it comes to triadic patents, at least, Canadian R&D performers do not appear to be getting a particularly big bang for their buck relative to those in other OECD countries.

A number of countries, including Canada, track indicators of the commercialization of open science research, including inventions disclosed, patent applications, patent grants, licences executed, licence income and start-ups.4 In a comparison of national surveys from 2003 and 2004, Arundel and Bordoy find that, despite the difficulty of such comparisons and the volatility of some indicators, Canadian universities and research institutes do better than their counterparts in Australia, the United Kingdom and Europe with respect to patent grants but worse with respect to licence income (2006, table 3). Not surprisingly, US universities and research institutes tend to do best by most measures.

The Council of Canadian Academies has assessed the quality of open science in Canada through a bibliometric analysis of the quality and relative frequency of scholarly publications by Canadians. The council finds that, whether measured by the rankings of the journals in which Canadian research is published or by the proportion of publications accounted for by Canadians, the publications of Canadian researchers are above the world average in most of the 125 fields of research it surveyed:

When the bibliometric data are viewed in their entirety, Canada’s broad strength in published research is apparent. We note that:

However, the council mentions some areas of disconnect between academic research strength as measured by bibliometric analysis and areas of commercial strength as measured by technometric (patent) analysis: “Canada’s patenting activity is relatively weak in many fields where Canada produces good science. For example, despite excellence in chemistry research, Canada’s patenting metrics are below the world average in chemical products, organic chemicals and petroleumrelated technologies” (14).

The nature of the linkage between bibliometric and technometric quality measures is an obvious topic for future investigation. In addition, the council might wish to extend its peer evaluation to include foreign opinions of Canadian research. It might also be of interest to see whether Canadian quality is above the OECD average rather than the world average.

Turning to input-based measures of innovative activity, various studies (for example, McFetridge 1992; Baldwin and Sabourin 1998) show that Canada has been slower than the United States in adopting advanced manufacturing technologies. Other studies (for example, Institute for Competitiveness and Prosperity 2006, 33; Banerjee and Robson 2007) reveal that Canada has lower levels of investment per worker and investment as a percentage of GDP in machinery and equipment and ICT than the United States. Canada also has a lower ratio of BERD to GDP than many other OECD countries.

With respect to R&D-intensity measures, the story is familiar. Canada ranks in the top four OECD countries with respect to its ratio of nonbusiness R&D to GDP but fourteenth in its BERD to GDP ratio, which pulls its GERD-toGDP ranking down to twelfth among OECD countries. Another way of putting it is that Canada ranks nineteenth among OECD countries in the fraction of its R&D spending accounted for by business (its ratio of BERD to GERD) (OECD 2007, tables 1, 23 and annex 2, table A).

Canada’s undistinguished standing in international comparisons of indicators of commercial innovation and its mediocre MFP growth record support the view that the relatively slow rate of labour productivity growth in this country is attributable, in part, to a relative lack of technological innovation in the business sector. This concern has been expressed in many quarters over the years, but it now seems to be attracting new attention, perhaps because Canada’s productivity growth record has deteriorated in recent years. For example, the Institute for Competitiveness and Prosperity concludes that

Canada has a significant innovation gap. While not a perfect measure, patenting is a good indication of the innovation gap between Canada and the United States. In both countries, patenting rates are strongest in traded industries, but Canada trails considerably. Another measure of our gap is Canada’s poor standing on the World Economic Forum’s Innovative Capacity Index. (2006, 42)

Dion (2007, 25) also concludes that Canada’s innovation performance has been “sub-par,” the result of low demand for innovation rather than lack of ability. After canvassing a variety of indicators, the Expert Panel on Commercialization concludes that Canada is suffering from numerous commercialization and innovation “deficits,” that too little of Canada’s substantial R&D effort occurs in the business sector and that Canadian businesses need to pursue R&D opportunities more aggressively. It, too, sees the problem as one of the “demand for innovation”: “The panel believes that while Canada needs to expand and renew its supply-side measures, it must now focus its efforts on the demand side, reducing the barriers and perceived risks that make businesses reluctant to engage in commercialization” (2006, vol. 1, 2). The Council of Canadian Academies comes to a similar conclusion:

A central conclusion from the evidence in this report is that Canada has built significant strength in many fields of research and there is optimism that we are gaining ground in several of the newer areas. Based on survey commentaries, and in the view of the committee, we do less well in converting strength in basic science into sustained commercial success. This is a long-standing deficiency in Canada’s innovation system which requires resolution for the full benefit of Canada’s considerable S&T strengths to be realized. (2006, 25)

As these commentators recognize, the realization of Canada’s commercial innovation gap is hardly new. The auditor general’s 1999 report cites a series of commentaries that came to this conclusion during the 1990s (Office of the Auditor General of Canada 1999, chap. 19, paras. 19.10-19.11). As long ago as 1970, the Senate Special Committee on Science Policy noted that

Canada is contributing relatively generously to the international pool of knowledge, both through government research and university research but we have neglected to develop our own innovations. In the light of international comparisons, we must conclude that Canada not only plays a subordinate role in the technology race but stands aside as well from the innovation process. (1970, 133-4)5

Concerns about the innovation gap often focus on Canada’s relatively low ratio of business expenditure on R&D to GDP. Framing the issue this way is unfortunate, however, in that commercialization is about much more than R&D. A host of complementary inputs is involved. Innovation is about entrepreneurship in its various forms and the rewards to it rather than about R&D per se. As one practitioner has noted, “[t]echnology is often pushed out of organizations but it reaches the market more successfully when it is pulled out by entrepreneurs.”6

Recognition of the importance of market incentives has come somewhat belatedly. Policies and policy debates frequently have focused on pushing businesses into R&D by various forms of assistance that reduce its cost while ignoring myriad other factors that reduce the profitability of technological innovation relative to other business strategies. Recent assessments of the innovation problem, however, appear to recognize the need to address the demand side – that is, the profitability of innovation, or lack of it.

By a number of indicators, the Canadian business sector is less inclined to engage in innovative activity than might be expected, given the size and sophistication of the Canadian economy. It is important to understand why this might be. Are the indicators capturing the full range of innovative activity that is occurring? Could it be that, although the measures are correct, some of the causes of the apparent dearth of innovation are beyond the reach of remedial public policies?

Traversy (2004) categorizes explanations of the perceived weakness of commercial innovation in Canada into attitudinal factors, structural factors and marketplace factors. Attitudinal factors include societal and managerial attitudes toward science and innovation. Structural factors include Canada’s industrial composition, firm size and ownership. Marketplace factors include market access, rivalry, taxation and regulation.

Attitudinal impediments to innovation can arise at the societal level. Arguments that Canada needs an innovation culture are, in themselves, vacuous and, in any case, as Traversy notes, there are already plenty of cheerleaders. More fundamentally, the political process can become dominated by entrenched interest groups that wish to frustrate change. Governments might talk the New Economy talk but continue to subsidize the old economy.

Science policy is not immune to interest group politics. The Senate Special Committee on Science Policy laid the weakness of industrial innovation in Canada, not at the door of “foreign devils,” but at that of the bureaucracy:

We are left with the model first proposed by the [National Research Council] in 1919 and restated since by most senior science managers in the public service. That pattern…put the emphasis on basic science and fundamental research and denigrated development activities as being of “ephemeral value.” It called for government assistance to help universities expand their research and education facilities in order to produce a growing number of well-trained pure scientists. It involved the creation and expansion of government laboratories to provide job opportunities for the increasing supply of scientists and to carry on R&D activities that would, it was hoped, prove useful to the industrial sector. (1970, 151-2)

Echoes of the situation perceived by the Senate Committee in 1970 persist. The Expert Panel on Commercialization (2006), while professing to recognize the demand-side determinants of innovative activity, nevertheless proposes a series of remedial policies, including distinguished professorships, internships, fellowships, scholarships, academic competitions and prizes that would warm the heart of any university vice president.

As for managerial attitudes, it has been suggested that Canadian managers choose the wrong strategies for the businesses they manage, opting for cost containment rather than innovation and upgrading, perhaps because they underestimate the returns on risky research ventures or are not forced to do so by aggressive rivals or demanding customers. A related line of argument is that, in participating in fast-moving innovative markets, Canadian managers are handicapped by their relative lack of business education and experience (Institute for Competitiveness and Prosperity, 2006, 46). In essence, there is a shortage of skilled managers and entrepreneurs. As the Conference Board of Canada has put it, “Commercialization is driven by entrepreneurship. But a consistent message that emerged from our research is the perceived lack of entrepreneurs and deal-makers in this country” (2005, 2).

The argument that Canadian businesses cannot attract managers with the requisite skills, experience and entrepreneurial ability to compete in markets characterized by rapid innovation has been made for many years (see Bourgault 1972, 125). Submissions to the Macdonald Commission expressed concerns about a shortage of skills in a wide range of managerial functions, and the commission expressed the view that entrepreneurial effort might also be misdirected into what it called “paper entrepreneurship” (1985, vol. 2, 108-18). More recently, an examination of the weaknesses of the hightech community in the Ottawa region found that early stage technology transfers and spinoffs are quite successful but that small firms had trouble growing. This was attributed to the lack of management and commercialization skills as well as management leadership – in short, to the lack of entrepreneurship (Doutrieaux 2004).

The continued currency of the view that the principal constraint on the supply of commercial innovation in Canada lies in the supply, not of scientists and engineers, but of managerial and entrepreneurial skills raises some fundamental questions. If Canada has a chronic lack of capacity for business education, this has to raise questions about the management and organization of universities themselves. The issue surely runs deeper still. One place to look is the rewards and demands of alternative career choices – perhaps the rewards to entrepreneurship are not great enough or the quiet life in the bureaucracy is too attractive. Another place to look is the demand that government regulatory and reporting requirements place on management’s time and its ultimate effect on the choice of business priorities and strategies. Turning this around, management might perceive that there is more profit in seeking government favour and protection than in upgrading.

Arguments that Canadian company managers have chosen the wrong – that is, the less profitable – business strategy are a different matter. One such argument is that, since Canadian businesses fail to recognize their own self-interest, it is the role of public policy, either by exhortation or financial inducement, to lead them to do so. If it is true that Canadian managers are unable or unwilling to exploit profitable opportunities for innovation and upgrading but must be pushed in that direction by bureaucrats, politicians and policy wonks, then the Canadian economy is in serious trouble and a lack of innovation might be the least of our problems.

It has long been argued that the structure of the Canadian economy militates against commercial innovation. Much of this reasoning stems from a view of Canada as a natural-resource-oriented economy with a small, tariff-protected domestic market. That Canada no longer exists, although its legacy remains. Another version of this argument is that, while the Canadian business sector is innovative, this activity does not show up in conventional indicators such as BERD-intensity.

Structural impediments to innovation are usually thought to include firm size, industry composition and foreign ownership. With respect to firm size, the argument is that, because Canada’s local markets and its national market are relatively small by international standards, small firms account for a greater proportion of economic activity in Canada, and small firms are less inclined toward innovative behaviour. The argument with respect to industry mix is that, for reasons of comparative advantage, Canada’s industrial structure might be relatively weighted toward industries that are not R&D-intensive (which may or may not also imply that they are not innovative). Foreign-owned firms are seen as an impediment to innovation because they do relatively little R&D in the host country, which implies to some analysts that such firms are not innovative and to others that local R&D-intensity is a poor measure of the local innovative activity of foreign-owned firms.

Investment in innovation becomes more attractive the more widely the innovating firm can apply it. This makes innovation less attractive to small firms than to large ones. It is well established that, although some highly innovative small firms become big firms, small firms as a group innovate differently and less frequently than large firms (Baldwin 1997). Although this should not be taken to mean that bigger is always better, innovative activity in a given industry is likely to vary inversely internationally with the proportion of industry output accounted for by small firms.

The role of firm size in explaining international differences in various measures of innovation has been investigated by a number of authors. Baldwin and Sabourin (1998, 27), for example, conclude that the slower rate of adoption of advanced manufacturing technologies in Canada observed in a 1993 survey could be attributed primarily to the smaller size of Canadian markets and plants.7 Canadian plant managers ranked the need for market expansion at the top of their list of impediments to the adoption of new technology, while US plant managers ranked it near the bottom. Canadian plant managers cited improvements in product flexibility and reductions in set-up time as benefits of new technology more frequently than did US respondents. Flexibility and setup time are more important for plants operating in small markets.

Baldwin and Gu find that, holding industry group effects constant, the probability of introducing a product or process innovation in Canada increases with firm size (2004, table 4). This implies that differences between Canada and comparator countries in the incidence of product and process innovation could be attributable to differences in average firm size.

Studies of the relationship between firm size and R&D-intensity generally find that the probability of engaging in ongoing R&D increases with firm size. They also find, however, that, among R&D performers, the elasticity of R&D spending with respect to firm size is no higher than one, implying that among R&D performers, R&D-intensity does not increase with firm size. Taken together, these findings imply that differences in BERD-intensity between Canada and comparator countries could be attributable to differences in average firm size. In particular, firms below the size threshold at which a firm becomes an R&D performer might account for a greater portion of sales in Canada, or the minimum size threshold at which R&D becomes profitable might be higher in Canada. The empirical evidence does not imply, however, that there is much to be gained in terms of R&D-intensity by combining two R&D-performing firms into a mega-firm.

Structural explanations for international differences in various measures of commercial innovation often focus on differences in ratios of business expenditure on R&D to GDP.8 It has long been recognized that differences in aggregate BERD-intensity might be due in part to international differences in the proportion of GDP accounted for by R&D-intensive industries and defence industries (Bourgault 1972, 59-60; Palda 1993, 116-21). In its calculations, the OECD adjusts national ratios of BERD to GDP to reflect the average industrial composition of the G7 countries. This moves Norway up in the rankings considerably, Canada up somewhat and Sweden, South Korea and Finland, in which R&D-intensive industries are more important than in the G7 as a whole, down considerably (OECD 2006, figure 3.3).

In a detailed Canadian study, ab Iorwerth (2005) decomposes the difference between the Canadian and US ratios of BERD to GDP into an intensity effect and an industry mix effect. He finds that, of the 0.88 percentage point difference between the two ratios in 1999, 0.60 was due to the lower research intensity of some Canadian industries relative to their US counterparts and 0.28 was due to R&D-intensive Canadian industries accounting for a smaller share of GDP than their US counterparts.

Among the Canadian industries that are less R&Dintensive than their US counterparts, two stand out: the services sector and motor vehicle manufacturing. With respect to the services sector, Dion (2007, 27) speculates that its low R&D-intensity relative to the US services sector could be due to the relatively small size of local Canadian markets for (nontradable) services and to regulatory and ownership restrictions on entry by major US retailers and wholesalers into Canada. Other possible explanations for the relatively high R&D-intensity of the US services sector include the relative importance of large electronic retailers and wholesalers in the United States and the reclassification of R&D-intensive manufacturing firms as service firms as a result of the offshore outsourcing of their manufacturing operations. With respect to the low R&D-intensity of motor vehicle manufacturing in Canada, the reason seems to be that the industry is integrated within North America and R&D is centralized in the United States, principally in Michigan. There is nothing to indicate, however, that this has handicapped Canadian motor vehicle manufacturing plants relative to their US counterparts. In any event, Canadian policy historically has been more concerned about production jobs and content than about R&D.

The effect of foreign ownership on business innovation in Canada has been the subject of debate for many years. The recent empirical evidence suggests that, given size and industry effects, foreign-owned firms in Canada are more R&D-intensive than purely domestic firms but somewhat less so than Canadianbased multinationals (Baldwin and Gu 2004). With respect to innovation itself, Baldwin and Hanel (2003) find that, within the core (R&D-intensive) industry grouping, firm size seems to determine whether foreign-owned firms are more likely to innovate (2003, table 10.15). Baldwin and Gu (2004) find that, holding firm size and two-digit industry effects constant, domestic multinationals are more likely than foreignowned firms to introduce a product or process innovation in Canada, but foreign-owned firms are more likely to do so than purely domestic firms (2004, table 4). Moreover, both foreign-owned firms and domestic multinationals are more likely than purely domestic firms to use advanced technologies (2004, table 5). The authors take their results to imply that any innovation gap between Canadian firms and firms in other OECD countries “reflects the poor innovation performance of domestically oriented firms in Canada” (2004, 16).

As for the role of foreign-owned firms in Canadian innovation, the evidence from Statistics Canada surveys suggests that such firms are active participants. As Baldwin and Hanel (2003) note,9

foreign-owned firms do not collaborate less frequently than do domestic firms with Canadian partners (customers, R&D institutions, universities and colleges, and other partners). Thus, as far as R&D collaboration is concerned, there is no evidence to support the once-popular argument…that foreign-owned firms do not develop links in Canada and are thus responsible for a truncated pattern of corporate behaviour in Canadian manufacturing. (2003, 286-7)

The best evidence available is that foreign-owned firms contribute to host-country innovation and productivity growth rather than act as a drag on it. They form linkages with other participants in the hostcountry innovation system and are a potential source of spillover benefits rather than operating as enclaves.

In discussing the effect of marketplace factors on innovation, Traversy (2004) makes the obvious but underappreciated point that commercial innovation is market driven and that the characteristics of markets for innovation should be a central rather than a peripheral concern:

Why are marketplace issues of more than passing interest to advisors on commercial innovation? The reason is that, of all the factors in the commercialization mix, perhaps none has grown in recognition over the past decade more than the importance of well functioning markets. At one level, of course, this is trite, or even tautological, because growing, profitable sales are the litmus test of innovation. Put another way, it has long been accepted that innovation must, ultimately, be market-driven. Despite this recognition, though, trade and marketplace policies have largely been treated as outside the purview of industrial innovation. This is no longer appropriate. (9)

Traversy goes on to suggest relevant marketplace issues, including effective access to international markets, market rivalry, market integrity (uncertain rules regarding regulation, proprietary rights and the limits on collaboration), and rules regarding international markets in the services sector. Taxation is an obvious addition to this list.

Canada’s participation in the liberalization of international trade has improved the access of Canadian firms to foreign markets and increased competition in domestic markets. Considerable room remains, however, for improving effective market access and reducing restrictions on the international mobility of human and financial capital. For example, restrictions on foreign ownership have been cited as inhibiting technological progress in telecommunications markets, and the tax treatment of foreign venture capital funds has reduced the supply of foreign venture capital in Canada. On the domestic front, despite some privatization and deregulation, much remains to be done. Relatively little progress has been made in reducing barriers to interprovincial trade. Government monopolies continue to thwart the introduction of new business models and methods. Concerns remain about domestic rivalry, government regulation and taxation.

Students of competitiveness have long stressed the role of competitive pressure from rivals and from customers in stimulating innovation. The Institute for Competitiveness and Prosperity (2006, 46) is of the view that there is not enough of it in Canada. Competition also plays a central role in stimulating innovation in contemporary growth models (Howitt 2007). Empirical work by Conway et al. (2006, table 2) shows that anticompetitive regulation of nonmanufacturing industries inhibits investment in information and communications technologies. These authors also find that anticompetitive regulation of industries that are intensive ICT users inhibits aggregate investment in these technologies (2006, table 3). Conway et al. find that regulation of ICT-using industries tends to be more restrictive of competition in Canada than in 11 other OECD countries, including the United States, Sweden, Finland and Australia (2006, figure 2).

In their search for causes of the relatively low rate of capital investment per worker in Canada, Banerjee and Robson come to the same conclusion about the innovation-retarding effects of regulation and state monopolies:

Some of the sectors likeliest to yield innovations, competitive products, and rising wages in the years ahead – such as telecommunications, financial services, and healthcare – struggle under regulatory regimes shaped by the economic and political imperatives of the past. Other key supports for the economy, such as transportation infrastructure and the production and transmission of fossil fuels and electric power, are not subject to market pricing and/or have restricted access to funds for investment. (2007, n.p.)

When searching for impediments to commercial innovation, taxation is the first place to look. Moreover, consideration of tax issues should go beyond tax incentives for R&D, which, as I discuss later, are very generous in Canada in any case. It is the stance of the tax system as a whole, including personal and corporate taxes, that matters.

Mintz (2007) finds that Canada’s effective tax rate on capital for marginal investments was the sixth highest in the world in 2006, although reductions in taxes levied on manufacturing firms will have brought the rate down to eleventh highest in 2007. Mintz argues that the corporate tax rate is above the level that maximizes tax revenue and that, together with capital taxes and sales taxes on machinery and equipment, it deters investment in machinery and equipment (2007, 8-11). New machinery and equipment embodies new technology, increases productivity and is complementary to R&D.

Highly progressive tax rates also inhibit both skills upgrading and entrepreneurship (for a thorough discussion, see Gentry and Hubbard 2005). Mintz argues that marginal tax rates on employment income are almost confiscatory over some income ranges (over 60 percent on incomes between $28,000 and $60,000 in Ontario, for example), which discourages investments in skills upgrading and work effort (2007, 4-5). He also argues (2008) that the structure of corporate tax rates discourages entrepreneurs from growing their businesses. Small Canadiancontrolled private corporations (CCPCs) are eligible for a variety of tax benefits, which they lose if they go public or grow beyond a relatively low size threshold. For example, the corporate tax rate on the first $400,000 of a CCPC’s profits is about 17 percent (depending on the province), rising to about 33 percent on profits in excess of that amount or if the corporation goes public. Mintz observes that CCPCs can also spin off part of their R&D operations into new CCPCs in order to remain eligible for the 35 percent (refundable) federal R&D tax credit.

Mintz also observes that taxes on savings discourage the accumulation of wealth outside of registered retirement savings plans and pension plans (2007, 56).10 The Institute for Competitiveness and Prosperity (2006, 37-40) makes similar observations, and calls for a “smart” tax system that taxes consumption rather than savings and earnings.

While Canada has generous tax incentives for R&D, McKenzie and Sershun (2005) show that the effectiveness of these incentives can be blunted if not offset entirely by other business taxes (see also McKenzie 2006). They conclude:

The obvious implication of these results is that when considering tax policy in the context of R&D governments need to consider not only the impact of direct tax subsidies on R&D, but also the impact of the production tax regime. More precisely, failing to take account of both effects may result in governments giving with one hand and taking away with the other, encouraging R&D by offering generous tax subsidies which lower the cost of undertaking research, but discouraging R&D by imposing high production taxes on the fruits of the R&D, the discovery of new products and processes. (2005, 22)

Instead of reducing tax rates, the federal and provincial governments maintain a panoply of selective tax expenditures and government programs designed to offset the most glaring or politically troublesome adverse incentive effects of these high tax rates. The problem is that it is impossible to anticipate and compensate for the entire range of adverse incentive effects of high tax rates.

There is widespread agreement about the role that markets for risk (venture) capital play in promoting and facilitating commercial innovation. There is no agreement, however, as to whether any shortcomings of the Canadian venture capital market flow from its demand side or its supply side or as to whether the policies of the federal government have aggravated or reduced the market’s deficiencies.

The OECD ranked Canada third behind Israel and the United States among 28 countries surveyed in terms of venture capital investment flows as a percentage of GDP over the period 2000-03. Canada ranked twenty-fourth, however, in the percentage of venture capital investments accounted for by banks, insurance companies and pension funds, which are the major investing institutions in most of the countries surveyed (OECD 2006, figures 3.7, 3.8). The anomalous mix of venture capital financing in Canada reflects the dominance in the market of taxassisted, labour-sponsored venture capital funds.

There is a clear consensus among economists that there is an economic efficiency rationale for government support of innovative activities that have a high social rate of return but a noncompensatory private rate of return. Public discussion of the role of government in supporting innovation often takes an entirely different form – namely, that projects with high private rates of return cannot be undertaken because financing cannot be obtained. It is often argued that there are gaps in the capital market and that this represents a market failure that must be remedied by government lending in some form. While there are acknowledged difficulties in financing investments in intangible capital and capital markets may be thin in spots, it is much less clear that this implies a market failure of a meaningful sort: one man’s market gap is another’s bad investment. The Macdonald Commission (1985) cited submissions claiming both that the supply of venture capital was inadequate and that there was nothing worth investing in. Twenty years later, the Expert Panel on Commercialization stated the same thing:

Many early-stage firms claim that there is a shortage of patient capital to finance development of their ideas, a problem thought to be particularly evident in regions outside of Canada’s major metropolitan areas. Providers of capital, on the other hand, respond that there is a shortage of investor-ready firms (e.g. that too many firms have weak management teams or poor business strategies, or lack general business know-how). (2006, vol. 2, 33)

The panel perceived what it called financing challenges in the seed and start-up phases of firms’ operations and in the late or expansion phases, although it conceded that these challenges exist in all countries. According to the panel, the problem in the start-up phase is a dearth (relative to the United States) of “angel” investors, which it suggested could be ameliorated if government served as co-investor with angels. The Conference Board (2005, 7) has suggested that angel investors receive a tax credit on investments in start-up companies.

There appears to be a consensus that the goal of policies to encourage venture capital financing should be to attract smart and experienced money. This raises questions of institutional design that do not appear to have attracted a great deal of attention. Do large tax credits attract experienced investors, those who exploit profit opportunities that would otherwise have gone unrecognized? Are investment decisions by stakeholder committees likely to result in the identification and exploitation of entrepreneurial opportunities?

Carpentier and Suret (2005) look at a Quebec government program to attract angel investors and other sources of outside equity, the Quebec Business Investment Company Program, and find that it did not attract angels and that the firms receiving support performed poorly relative to the average for their industries. The authors view their results as being consistent with the hypothesis that it is the poorer-quality opportunities that seek out government finance (17). Carpentier and Suret conclude that, although it is not clear the program was necessary in the first place, it nevertheless could have been improved by recognizing the essential characteristics of the financing of small and medium-sized enterprises (SMEs).

With respect to expansion funding, the Expert Panel on Commercialization (2006) concurs with the recommendations of other advisory groups to reduce impediments to participation by US venture capital investors in the Canadian market. One such impediment, section 116 of the Income Tax Act, significantly delays the realization of the proceeds of the disposal of shares in Canadian private corporations by foreign investors, a problem that is addressed in the 2008 federal budget (Stikeman Elliott 2008, 3).

The Institute for Competitiveness and Prosperity (2006, 43-5) takes the view that the problem with the supply of venture capital in Canada is not the quantity but the quality.11 According to the institute, laboursponsored venture capital funds have attracted unsophisticated individual investors and earned low returns while possibly crowding out more skilled institutional investors. To tackle the problem, the institute advocates changing the mix of venture capital sources by eliminating the preferential tax treatment of labour-sponsored funds. It also joins others in calling for the end of tax impediments to the participation of US venture capital investors in the Canadian market.12

Some analysts support a modest role for government in filling the capital market gaps through an appropriately qualified lending agency. A summary of an expert international symposium on funding gaps (Cressy 2002) cites “controversial” evidence that small high-tech firms whose assets are largely intangible might be financially constrained and suggests that there is a role for government if it can mimic the best practices of the venture capital industry and if it focuses on firms likely to generate positive externalities (2002, F13-14). Lerner (2002) advocates government venture capital financing but only to viable firms that promise R&D spillovers. Economic efficiency arguments confine the subsidization of innovative activities to instances in which the social rate of return on investment is high but the private rate of return is insufficient to attract capital. The arguments just cited, however, imply that there might also be a role for the government financing of R&D investments that yield a significant positive externality but are unable to attract investors even though their expected private rate of return is compensatory. Whether these situations are common and whether a government venture capital lender could correctly identify and manage them is another question.

Research on national systems of innovation emphasizes the importance of linkages in the innovative process. Key linkages are between innovating firms and their customers, suppliers, competitors and research universities as well as among research institutions. Formal linking organizations include consulting firms, industry associations and research institutes, extension services, university technology transfer offices, business incubators and research parks as well as federal and provincial agencies. Customers are generally thought to play a pivotal role both in facilitating incremental product and process improvements (learning by using) and by requiring suppliers to meet ever-higher quality and performance standards. In some industries (agriculture, for example), suppliers of machinery and equipment and key inputs drive innovation. In general, linkages involve knowledge transfer, which can occur in a variety of ways, including exposure to scientific and technical publications, employee mobility, licensing, joint venturing and reverse engineering. (For a study of the incidence of various types of linkages in Canada, see Baldwin and Peters 2001).

Commercialization of university research is often viewed in terms of patents, royalties or spinoff businesses but it also occurs when students are employed in business in co-op programs, when university faculty and business personnel are interchanged or when commercial users access open science. Perhaps the most important linkage occurs when graduates trained in the newest technology are employed in business. Mike Lazaridis, president of Research in Motion (RIM), stressed the importance of this link in 2004 by noting that, over the preceding 20 years, RIM had hired 5,000 students while licensing only two technologies from universities (quoted in Lougheed 2004, 2).

Historically, there has been concern about the limited linkages between both business and university research and business and government research. The Senate Special Committee on Science Policy (1970) devoted considerable attention to what it viewed as the problem of the isolation and lack of relevance of government laboratories. The Macdonald Commission (1985, vol. 2, 102) noted the lack of business support for university research and suggested that measures be taken to encourage it.

Numerous government programs have been introduced over the years to promote better linkages among formal R&D performers.13 The Natural Sciences and Engineering Research Council’s Research Partnerships Program supports joint research (basic to pre-commercial) and knowledge transfer among universities, science-oriented federal departments and the private sector. The auditor general’s 1999 evaluation of the program found that funding decisions took proper account of the scientific merit of projects supported but were unexpectedly thin in terms of both the commercial or pre-commercial significance of the research and the need for funding (Office of the Auditor General of Canada 1999, chap. 19, paras. 19.75-19.90). The auditor general was unable to determine whether industry partners made use of the results of completed projects.

Another federal government initiative intended to support the formation of research networks among university, industrial and other research institutions is the Networks of Centres of Excellence (NCE) program. Introduced in 1989, its objective is to link the academic, private and volunteer sectors to create commercial opportunities (see NCE 2004). The program’s annual budget was $82.3 million in fiscal year 2005-06.14 The auditor general evaluated the NCE program favourably in 1999 (Office of the Auditor General of Canada 1999, chap. 19, paras. 19.92-19.96), and an evaluation on the program’s behalf by KPMG Consulting (2002) found that it was successful in achieving its goals and objectives, including knowledge and technology transfer. The evaluation noted, however, that other support programs also encourage linkages, that reporting and application costs were high and that the program sometimes forced linkages. Respondents to a 2006 Council of Canadian Academies survey ranked the NCE program among the top three programs or organizations that support the commercialization of innovation in Canada.

The Expert Panel on Commercialization (2006) recommended further support for linkages between busi-

ness and universities and other nonprofit institutions in the form of a Commercialization Superfund that would subsidize nonproprietary research in fields in which Canadian businesses could become market leaders. The panel also recommended a program of subsidies to joint research carried out by federal government departments and SMEs.

It is important to separate arguments that linking institutions could be better designed from arguments that their scale should be increased. Experimentation with alternative linking institutions is ongoing in many countries (see, for example, Gulbranson and Audretsch 2008). Whether universities and government laboratories should be more commercially oriented is a whole different question. Some argue for a greater commercial orientation – for example, Stanley (2007) argues that there is insufficient reference to industry needs in current programs supporting academic research, and that some academic research needs to be coordinated with industrial research by a “go to” agency focused on inducing firms to upgrade. Others are wary of viewing the role of universities in the innovation process narrowly in terms of the (direct) commercialization of their research (Conference Board 2005, 2).

Linkages among innovative firms are ubiquitous, and the most important role for public policy is to accommodate them. Since many of the most productive linkages are likely to be international, continuing efforts are needed to reduce barriers to the mobility of human resources and capital. The development of linkages involving government laboratories, universities and the business sector has required more proactive public policies, and this has indeed received considerable attention. The continuing lament that Canada produces good science but seldom commercializes it implies that this linking capability is underused by business. It need not be the case that “if you build it, they will come.” Rather than expanding linking capabilities even further, it might be more productive for public policy to focus more closely on the fundamental driver of business participation: the opportunities and rewards for commercial innovation.

The federal government has provided income tax incentives for R&D since 1944 (Department of Finance 1997, 4) and special allowances or credits for current R&D expenditures virtually continuously since 1962. A 1977 study found that Canadian tax treatment of R&D was the most generous in the world at that time (McFetridge and Warda 1977, 76). Since then, many countries have introduced special tax incentives for R&D and some have surpassed Canada’s generosity over the years. The federal government has also enriched tax incentives for R&D in various ways over the years, augmented by a number of provincial incentives. An OECD ranking of tax subsidies for R&D as of 2004 put Canada fourth (behind Spain, Mexico and Portugal) of 24 countries (OECD 2006, figure 3.12).

The heart of federal tax assistance for R&D is the Scientific Research & Experimental Development

( S R&ED) tax credit.15 There are currently two rates of S R&ED: a general rate of 20 percent and an enhanced rate of 35 percent for CCPCs with prior-year income under $400,000. These credits are taxable, and there is a ceiling on the expenditures eligible for the 35 percent rate. A partial tax credit, equal to one-half the normal credit, is also available for expenditures on new equipment used primarily for SR&ED in Canada.

Investment tax credits may be deducted from federal taxes otherwise payable. A standard concern about tax credits is that they are of little value to firms with no taxable income. This problem has been addressed in several ways. First, unused tax credits can be carried forward (currently ten years) or back (three years). Second, tax credits can be made refundable – partial refundability provisions were introduced in 1983, and refundability of some sort has been a feature of the tax credit ever since. Currently, the SR&ED credit earned at the 35 percent rate is fully refundable on up to $2 million in current SR&ED expenditures and 40 percent refundable on expenditures in excess of $2 million; SR&ED credits earned at the 20 percent rate are not refundable.

The SR&ED tax credit has both its critics and its supporters. Critics say that, first, since it is generally available, the credit does not direct resources to the innovative activities with the largest spillover benefits. Second, its relative generosity, taken together with the relatively low level of Canada’s ratio of business expenditure on R&D to GDP, implies that the credit must have been ineffective in inducing recipients to undertake additional R&D (see Institute for Competitiveness and Prosperity 2006, 45). Third, qualifying for and receiving the credit can be a costly and slow process. Fourth, tax credits earned by foreign-owned firms may be taxed back in part when profits are repatriated to the parent.16 Fifth, a likely consequence of the marked discrepancy between the 35 percent SR&ED credit available to CCPCs with prior year income under $400,000 and the 20 percent credit otherwise available, together with the ceiling on expenditures eligible for the 35 percent rate, is the fragmentation of R&D operations (Mintz 2008).17 Some critics (such as Head and Ries 2004; Harris 2005) favour relying more on direct support (subsidies). Mintz (2008) suggests reducing the discrepancy between the enhanced (35 percent) and the general (20 percent) SR&ED credit rates, while the Institute for Competitiveness and Prosperity (2006) favours a tax regime with generally lower taxes on investment, earnings and savings and no special R&D tax treatment.

Supporters of the SR&ED credit maintain that Canada’s ratio of BERD to GDP would be even lower without it and that, as a practical matter, the information required to target support to projects with high social rates of return but low private rates of return is seldom available. They also argue that a tax credit program is less costly to administer than a program of direct subsidies, that it minimizes political interference and does not involve the government’s picking winners. Some would extend the credit to cover other aspects of innovation and commercialization such as market assessment (Conference Board 2005, 8); others would enrich the credit in various ways, perhaps by extending its partial refundability provisions to corporations other than CCPCs (Wensley and Warda 2007, 1; see also Toms and Watters 2006). Among other things, this would make the SR&ED credit more relevant to the R&D decisions of Canadian affiliates of US-based multinationals.

The ongoing concern about the SR&ED credit and its predecessors is whether and to what extent it induces recipients to increase their R&D expenditures beyond what they would have done in the absence of the incentive. This responsiveness of R&D spending to tax credits is known as “incrementality.” Some tax credit regimes focus support on R&D that is deemed to be incremental; that is, R&D in excess of some base amount. Since a dollar of R&D spending ceases to be eligible for a tax credit once it is fully reflected in the base, however, incremental credit or allowance schemes provide less inducement (given the credit or allowance rate) for ongoing R&D spending than do credits or allowances based on the level of R&D spending.18

Many attempts have been made to measure the responsiveness of R&D spending to tax incentives. One measure is the “bang for a buck”: the additional R&D induced per dollar of tax revenue foregone. An evaluation for the federal Department of Finance (1997) estimates that the SR&ED credit induces $1.38 per dollar of tax revenue foregone and that responsiveness to the credit does not vary systematically by type of recipient. In another study, Dagenais, Mohnen and Therrien (2004) estimate that the SR&ED credit generates 98 cents of additional R&D for every dollar of tax revenue foregone.19 Dahlby (2005, 53) concludes that responsiveness to R&D tax credits is in the range of $1.00 to $1.38 per dollar of tax revenue foregone.

Another stream of analysis estimates the effect of the SR&ED credit on innovation itself.

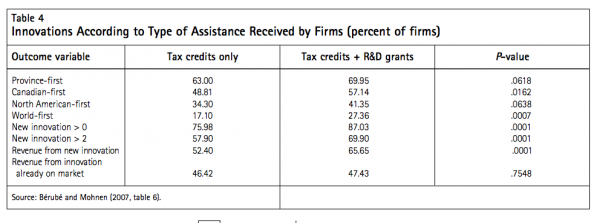

Czarnitzki, Hanel and Rosa (2005) find that, when they compare firms that match in all relevant respects except that some receive an SR&ED credit and others do not, firms that receive the tax credit are more likely to introduce new product innovations, world-first new product innovations and Canada-first new product innovations, and to derive a larger fraction of their sales from new product innovations. This difference is sustained even when the sample is confined to innovating firms. Despite their superior innovative performance, the firms that receive the tax credit are no more profitable and do not have a higher market share than nonrecipients.

A qualitative survey of institutions and programs that support the commercialization of innovations ranked the SR&ED tax credit second of sixteen forms of support (Council of Canadian Academies 2006); among business respondents to the survey, the SR&ED ranked first. There is also some anecdotal evidence that the SR&ED credit has been instrumental in the growth of some Canadian firms:

RIM has also been a constant beneficiary of SR&ED which was described as “vitally important” by Dave Jaworsky, RIM’s director of government and university relations. “(SR&ED) is key to our future growth…It justifies everything,” says Jaworsky, adding that the program is currently in an “antagonistic mode” that needs to change. “It’s an incentive to stay local.” (Research Money 2007)

The view of the federal Department of Finance is that the SR&ED (or any other subsidy) is cost effective if it induces a dollar or more of the desired activity per dollar of tax revenue foregone. Dahlby (2005) shows, however, that the issue is not as simple as this. The essential question is whether the subsidy moves resources to a higher-valued use – that is, whether it increases productivity in the broadest sense – which, in fact, depends on the social rate of return on the R&D induced and the value of the activities crowded by the taxes levied in order to finance the subsidy (the cost of public funds). Dahlby finds, for example, that an Alberta provincial R&D tax credit would not be efficient (2005, 55); his analysis could be extended to other provinces and to the federal SR&ED tax credit and to subsidies as well.

The federal government has been offering direct subsidies for industrial R&D since the early 1960s. Of the many programs over the years, the discussion in this section pays special attention to two that have existed throughout the entire period: the Industrial Research Assistance Program and a program for defence and related industries that has gone through several incarnations but for most of the period was called the Defence Industry Productivity Program.

The Industrial Research Assistance Program (IRAP), which supports technology development in SMEs, has been operating continuously since 1962. IRAP assistance historically has taken the form of paying the salaries of scientists, engineers, technologists or technicians participating in approved projects. The assistance is generally limited to one-half of project costs.

IRAP is administered by the National Research Council Canada (NRC). Approved projects are supported by an industrial technology advisor employed by the NRC, provincial research councils or other agencies. IRAP expenditures in fiscal year 2005-06 were approximately $145 million, of which roughly half were contributions to nearly 2,700 firms (clients). IRAP also contributes to and coordinates a network of researchand technology-based organizations (National Research Council Canada 2006).

IRAP has many friends. Respondents to the Council of Canadian Academies’ 2006 survey ranked IRAP and the SR&ED tax credit first and second, respectively, in terms of their effectiveness as government programs for commercialization support,20 with 82 percent of business respondents and 76 percent of all respondents giving IRAP a “strong” rating, some of the highest in the survey (2006, fig. 10). This ranking echoes a long line of informal assessments of IRAP over the past 25 years, which Lipsey and Carlaw (1998, 90-1) found were “almost universally favourable.” Among the reasons given for this favourable evaluation were the expertise and experience of those charged with program delivery and administration, the businesslike manner in which the program was administered and its coordination with other sources of technological information.