Redesigning Canadian Trade Policies for New Global’s Realities

Overview of the Research Findings

Stephen Tapp, Ari Van Assche and Robert Wolfe

John Baldwin is director of Statistics Canada’s Economic Analysis Division, which also hosts the Canadian Centre for Data Development and Economic Research. The research program makes use of business microdata to investigate issues such as firm turnover, the nature of industrial restructuring, productivity, the impact of trade liberalization, the performance of multinationals, innovation and technological change. He has a PhD from Harvard University and taught at Queen’s University for many years. He has published extensively on firm demographics, industrial organization, innovation, the use of advanced technology, productivity and trade.

Beiling Yan is a senior research economist at Statistics Canada’s Economic Analysis Division. She has published extensively in the areas of productivity, international trade, firm dynamics, exchange rates, labour markets and the income distribution, in academic journals that include the Scandinavian Journal of Economics, Canadian Journal of Economics and Journal of Economics and Management Strategy. She has an MBA and a PhD in economics.

Redesigning Canadian Trade Policies for New Global Realities, edited by Stephen Tapp, Ari Van Assche and Robert Wolfe, is the sixth volume of The Art of the State. Thirty leading academics, government researchers, practitioners and stakeholders, from Canada and abroad, analyze how changes in global commerce, technology, and economic and geopolitical power are affecting Canada and its policy.

Contemporary production processes involve various complex activities, such as product design, manufacturing parts and accessories, assembling final products, marketing and distribution. These activities often occur in different stages and locations, and thus need to be coordinated through arm’s-length transactions or within a vertically integrated firm. In a global value chain (GVC), production processes are subdivided into fine slices that take place across international borders to take advantage of efficiencies in different locations (Globerman 2011).1

The rising importance of GVCs in world trade is illustrated in many studies (see, for instance, De Backer and Miroudot, in this volume), and has been associated with robust international trade of intermediate goods and parts. For example, in the dataset of Canadian manufacturing firms we use in this chapter, we find that intermediate goods account for a substantial share of overall trade — an average of two-thirds (67 percent) of total manufacturing imports and 60 percent of exports over the period from 2002 to 2006.

The scope and speed with which worldwide production has become integrated into GVCs has generated interest into their effects on productivity. A growing theoretical and empirical literature is finding that a country’s integration into GVCs can improve its productivity performance (Grossman and Rossi-Hansberg 2008; Van Assche, in this volume). In this chapter, we examine the impact of GVC participation on firm-level productivity in the Canadian manufacturing sector between 2002 and 2006. We define a GVC participant as a firm that imports intermediate goods and exports either intermediates or final goods,2 and we investigate what happens over time to the productivity performance of Canadian manufacturing firms that enter and exit a GVC.

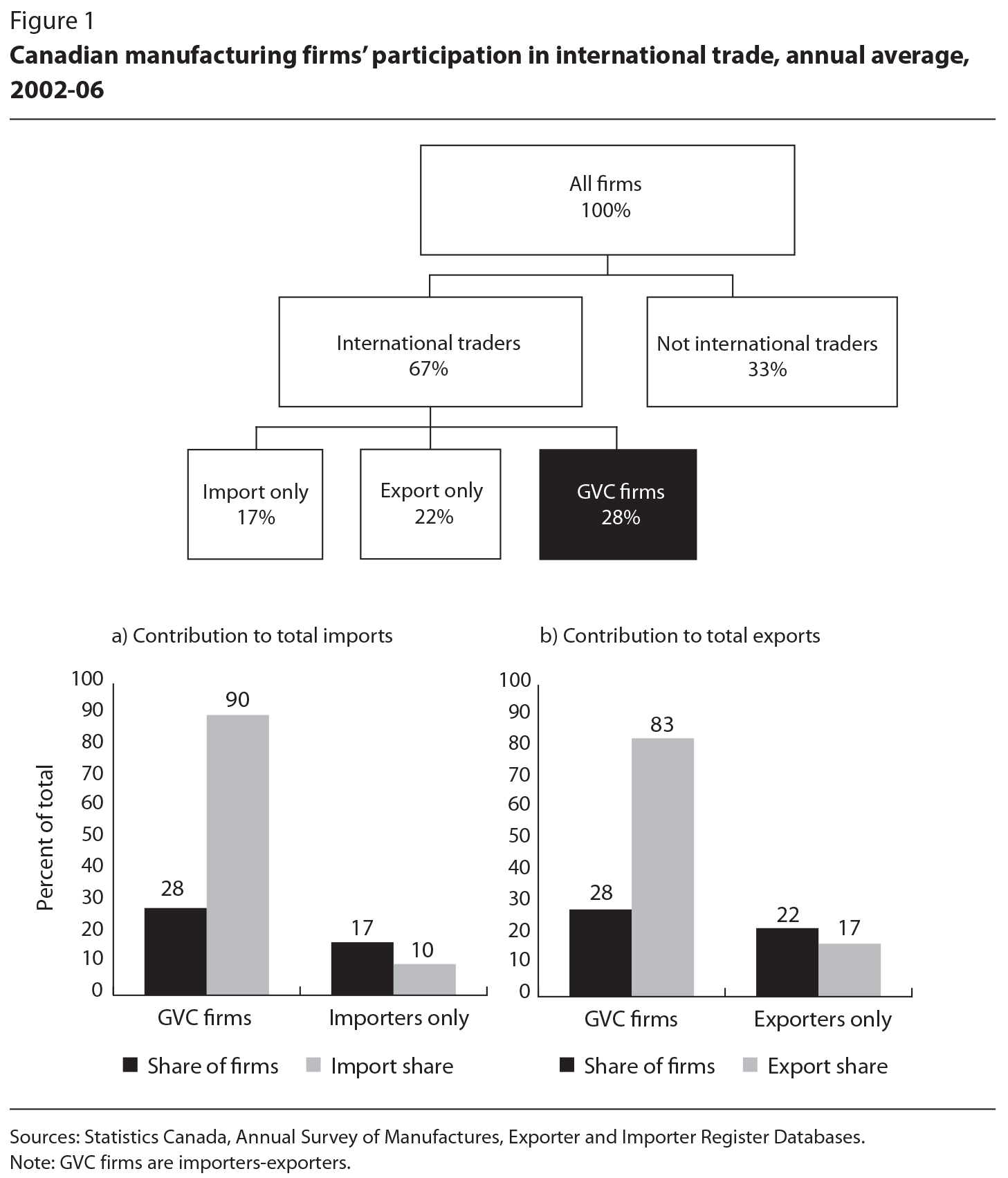

In our estimation approach — of propensity score matching and difference-in-difference regressions; see below — we attempt to account for the self-selection predicted by recent firm-level trade theory (for an overview see Lapham, in this volume): that “better” firms tend to be international traders. In our dataset, nearly one-third (28 percent) of Canadian manufacturers were both importers and exporters (hereafter referred to as GVC firms) between 2002 and 2006 on average. These firms did indeed display better economic performance along several dimensions compared with other firms in their industries. GVC firms were larger (116 percent), more productive (10 percent), had higher sales per worker (14 percent) and paid higher wages (6 percent). They were also more likely to be foreign-controlled. Despite their relatively small population share, they contributed a remarkable 83 percent of total exports and 90 percent of total intermediate imports in Canada’s manufacturing sector over the 2002-06 period.

To distinguish these positive “selection” effects from potential productivity “treatment” effects, we compare groups of firms that joined GVCs (and those that quit them) with firms that otherwise had similar features but did not change their GVC status (the “control” group). Our results offer strong empirical evidence of a causal link between GVCs and firm-level productivity: Canadian manufacturing firms that joined GVCs became more productive than those that did not. This productivity advantage was evident within the first year, and grew over time. Conversely, firms that dropped out of GVCs — by no longer importing, no longer exporting or both — became less productive than firms that continued to belong to GVCs. This loss took longer to materialize, but after the first year the productivity disadvantage was similar in size to the gains enjoyed by GVC starters. These effects were statistically significant and economically relevant, cumulating in firm-level productivity performance gaps of 8 to 9 percent on average after four years.

Our results highlight the important two-way relationship that underlies the positive correlation between GVC status and firm-level performance. Although it is true that firms with superior performance are more likely to participate in GVCs, it is also the case that becoming part of a GVC improves firm performance, and that quitting a GVC hurts firm performance. In other words, “better” firms join GVCs, and joining GVCs makes firms “better.” “Worse” firms avoid GVCs, and quitting them worsens performance. And although our results show, not surprisingly, that GVCs are more prevalent in higher-technology manufacturing industries, their productivity-enhancing effects are found across many manufacturing industries.

The second key contribution of this chapter is to document the pathways by which Canadian firms enter and exit GVCs, and to disentangle the contributions made by exporting versus importing. We show that exporting is generally the more active channel — that is, GVC entry comes primarily from importers that start exporting, while GVC exit comes largely from two-way traders that stop exporting. Moreover, the productivity benefits from exporting are generally larger and longer lasting than the positive effect from importing. Once a firm is part of a GVC, stopping to import is the more immediate driver of productivity losses.

Lastly, we investigate how the results vary for Canada’s manufacturing trade with high-wage versus low-wage trading partners. Although the latter’s share of total Canadian trade grew significantly over the period studied here, high-wage countries remain the major source of Canada’s imported intermediates and the main destination for its exports. We find that productivity gains were larger for firms in Canada that linked to value chains with other advanced economies. This result likely reflects the importance of technology transfer in international trade. We also find that GVC stoppers that ceased importing from lower-wage countries suffered the largest productivity losses (particularly in lower-technology sectors), perhaps due to foregone cost savings. Based on these findings, one might expect a smaller productivity boost from increasing Canadian trade with emerging markets — something which has been a recent policy objective — and a more immediate productivity loss if those trading relationships eventually sever.

In principle, GVC participation can improve a firm’s productivity in at least three ways: via an export effect, an import effect and a combined effect of the two.

Export effect. The positive link between exporting and a firm’s productivity is the best-known effect, and has been documented in a large body of research (such as Greenaway and Kneller 2007; López 2005; Wagner 2007; for Canadian evidence, see Melitz and Trefler 2012, and our other chapter in this volume). Access to larger foreign markets allows exporting firms to exploit scale economies and learn about new technologies and products, and it increases their incentives to invest and innovate.

Import effect. Importing intermediate inputs can also enhance a firm’s productivity by providing access to foreign inputs and technologies that are unavailable or more expensive to obtain domestically (Grossman and Rossi-Hansberg 2009). A smaller but growing number of empirical studies have investigated the impact of importing on productivity, and they too find substantial productivity gains through access to imported inputs, based on data for manufacturing firms in Indonesia, Chile, India and Canada (Amiti and Konings 2007; Goldberg et al. 2010; Gu and Yan 2014; Kasahara and Lapham 2013; Kasahara and Rodrigue 2008; Topalova and Khandelwal 2011).

Combined effect. Finally, firms might benefit from the combined effect of being both an importer and an exporter due to complementarities between importing and exporting. Using plant-level data for Chilean manufacturing industries, Kasahara and Lapham (2013) estimate that both exporting and importing entail large start-up costs, and they find an important interaction between the two. In their counterfactual model exercises, restricting exports of final goods reduces imports (and the share of firms that import intermediates), while restricting imports of intermediates reduces exports (and the share of firms that export). Their estimate of the complementarities between the fixed costs of importing and exporting suggests that “a firm can save between 7 and 26 percent of the per-period fixed costs and sunk costs associated with trade by simultaneously engaging in both export and import activities” (305, emphasis added).

Although there is growing evidence of the positive productivity effects of exporting and of importing at the country, industry, and firm-level — as well as some initial work on the complementarities between the two activities on firm performance — the literature has not extensively examined joint exporting and importing activities at the firm level. Indeed, research has generally focused on estimating the productivity benefits of importing or exporting separately, without taking account of the fact that many firms are both importers and exporters. Since export and import status are positively related, export premiums reported in the literature are likely overestimated because they also partly capture import premiums (and similarly import premiums are overstated because they partly reflect export premiums).

Our analysis uses several micro-datasets that contain detailed information on the characteristics, performance and imports and exports of Canadian manufacturing firms. We begin with some definitions and an explanation of how we constructed our data.

Hummels, Ishii and Yi (2001) use the phrase “vertical specialization” to refer to firms that use imported intermediate parts to produce goods that are then exported. In this chapter, we examine manufacturers that both import intermediate inputs and export intermediate or finished products in a sequentially integrated production process across countries. Although one-way trading firms that only export or only import might, in some cases, also be considered GVC participants, our use of both criteria highlights the sequential, back-and-forth aspect of global economic linkages. Our definition might exclude some firms that are indirectly integrated into GVCs — such as those that effectively use other domestic intermediaries for their imports, or supply domestic firms that in turn export — these limitations, however, are unlikely to affect our results significantly. The reality is that two-way traders in Canada’s manufacturing sector contribute the vast majority of overall trade value, while the contribution of one-way traders is much more modest (as shown later in figure 1). Our joint exporter-importer definition also increases the likelihood that an actual specialization of function occurs in the production process — rather than simply a wholesaling function, supplementary to producing manufactured goods in a Canadian facility. Finally, our definition is consistent with the indicator of GVC participation used by the Organisation for Economic Co-operation and Development (OECD), which focuses on intermediates produced in one country and then included in another country’s exports.

We obtained information at the enterprise (hereafter, firm) level for imports and exports by linking Statistics Canada’s Annual Survey of Manufactures (ASM) with its Importer Register Database. The ASM contains firms’ characteristics, such as their employment, gross and value-added output, total material cost, export status, total export values, ownership, age and 6-digit industry code from the North American Industry Classification System (NAICS). We derived firm-level productivity by removing price effects from firm-level nominal output using available industry-level price deflators. This approach is common, although imperfect, but it is the best one can do when firm-specific price deflators are unavailable to estimate firm-level production volumes. Indeed, a study that uses a special Danish manufacturing dataset finds that international trade premiums are significantly larger when output is deflated with their firm-specific price index, rather than the traditional industry-level price index (Smeets and Warzynski 2013).

We obtained information on export destinations by linking the ASM with Statistics Canada’s Exporter Register Database. On average over the 2002-06 sample period, around 27 percent of firms (54 percent of exporters) in the ASM were linked to the Exporter Register, accounting for the vast majority of total export values in the ASM (96 percent; see Baldwin and Yan 2014, table 1, for details).

The Importer Register contains information on import value at the Harmonized System 10-digit commodity level — that is, with more detail than the legal 8-digit tariff-rate level — and source country. We linked the two micro-databases by matching firm-level identifiers for each year (for details, see Baldwin et al. 2013). This matching technique produces links of imports to manufacturing firms that directly import intermediate inputs. Some intermediate inputs are imported by intermediaries, which then supply domestic manufacturers (for the importance of this phenomenon, see Baldwin et al. 2013). Because they cannot be identified — and because intermediaries that import are not really part of a vertically integrated supply chain, or if they are, it has different characteristics — we omitted these imports from our analysis.

Importers in Canadian manufacturing industries are typically large firms. For the 2002-06 period, 52 percent of firms in the ASM were linked to the Importer Register, accounting for an average of 76 percent of total manufacturing shipments. We assumed that any firms that were not found in the Importer Register were not importers. Imported products comprise intermediate investment and consumption goods. To identify intermediate goods, we used several classification sources, the main one being the United Nations Broad Economic Categories, which distinguishes among intermediate goods, consumption goods and capital goods. We excluded the categories of “motor spirits,” “passenger motor cars” and “goods not elsewhere specified” because they are used extensively for both final consumption and intermediate uses.

Between 2002 and 2006, an average of two-thirds of Canadian manufacturing firms were international traders — either an importer, an exporter or both. Based on our definition that a firm participating in a GVC is an importer-exporter, only 28 percent of Canadian manufacturers were GVC firms (figure 1). Despite their small population share, however, these firms contributed 90 percent of all imports intermediate in the Canadian manufacturing sector and 83 percent of exports.3

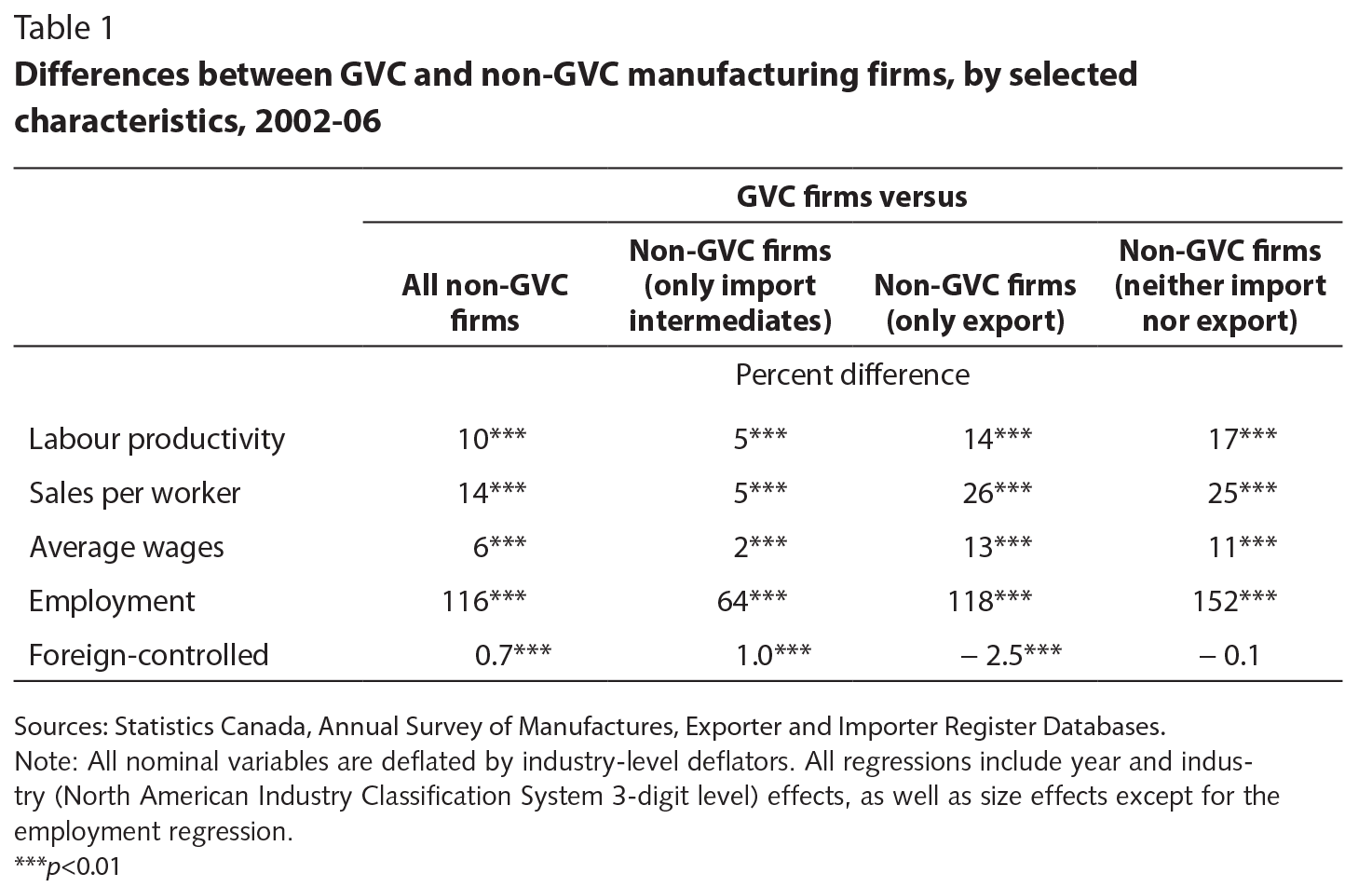

GVC firms also differ from non-GVC firms in other ways besides their trading behaviour. As table 1 shows, Canadian manufacturing GVC firms generally had better economic performance than non-GVC firms: they were larger (116 percent more employment), more productive (10 percent more), had higher sales per worker (14 percent higher), paid higher wages (6 percent higher) and were more likely to be foreign-controlled.4 The performance gaps were even larger when we compared GVC firms to the group that did not trade at all (whereas the non-GVC group also included one-way traders). These findings are consistent with those of Kasahara and Lapham (2013); using Chilean data, they find that firms that both import intermediates and export their output tend to be larger and more productive than those that are active in either market, but not both.

The positive correlation between a firm’s GVC status and its performance might simply reflect the fact that firms with better performance are more likely to participate in a GVC (so-called positive self-selection). But it might also be the case that joining a GVC improves a firm’s performance. To disentangle these two effects — better firms trade versus trading makes firms better — we applied propensity score matching and difference-in-difference methods. These allowed us to examine whether becoming part of a GVC really boosts firm-level -productivity, after controlling for the fact that the generally better-performing firms tend to be those that become part of a GVC in the first place — a self-selection process that would otherwise bias the results (De Loecker 2007). In sum, our estimation approach allowed us to examine the effects of GVC participation on productivity performance (taking into account possible self-selection bias), and to track firm performance over time after a firm enters or exits a GVC (see appendix).

To become an importer-exporter, a firm must incur fixed costs such as direct transportation and tariffs costs, and for developing a logistics network, communicating product specifications, and monitoring and coordinating workers abroad. In heterogeneous firm models of international trade (such as in Antràs and Helpman 2004; and Melitz 2003), fixed sunk costs imply that firms will join a GVC only if the present value of the expected profits from doing so exceeds the fixed costs of entry. Therefore, the more productive firms (typically, larger ones) are more likely to both import and export.

To investigate this hypothesis, we first looked at the 2002-06 period, at the start of which a firm was either part of a GVC or not part of a GVC. At the end of the period, the firm either maintained or changed its GVC status. Because GVC firms are importer-exporters, they might have stopped exporting, stopped importing or both; non-GVC firms might have started exporting, started importing or both.

The probability of entering or exiting GVC status (Ef,t) at time t is modeled as a function of a set of firm-specific attributes (Zf, t–1) at time t-1, time (αi) and industry (αi) fixed effects:

Prob(Ef,t = 1) = Φ(αi + αt + γZf, t-1), (1)

where Zf, t-1 includes productivity (relative to mean productivity in the same NAICS 3-digit industry), employment (relative to average employment in the same NAICS 3-digit industry), age and nationality of ownership (domestic versus foreign controlled) in the previous period.

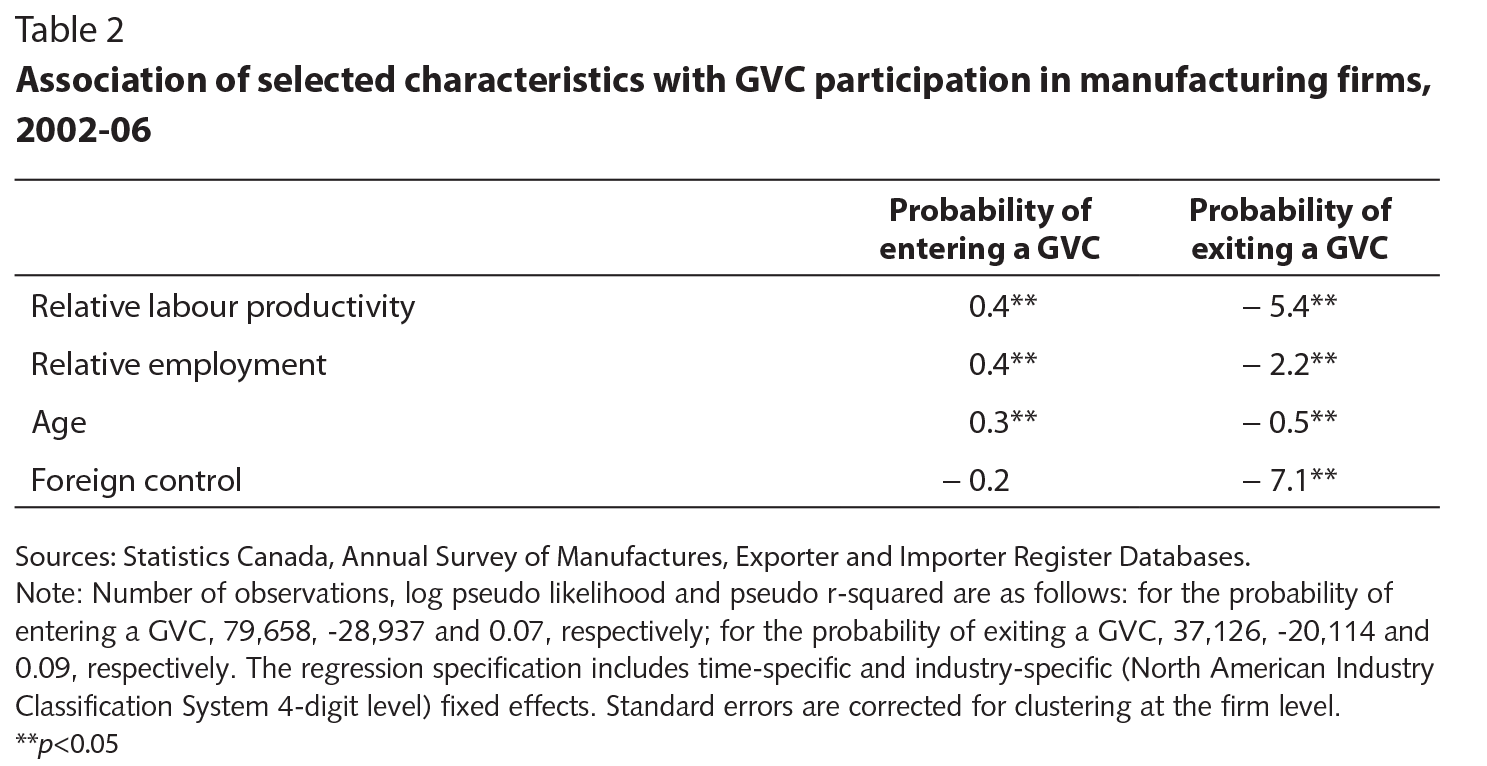

Consistent with self-selection, we find that firms that joined a GVC were significantly more productive than those that did not (table 2 shows that a 1-unit increase in relative labour productivity raises the probability of entering a GVC by 0.4 percent). Alternatively, firms that exited from a GVC were significantly less -productive than those that continued to participate in a GVC (and a 1-unit increase in relative labour productivity decreases the probability of exiting a GVC by 5.4 percent).

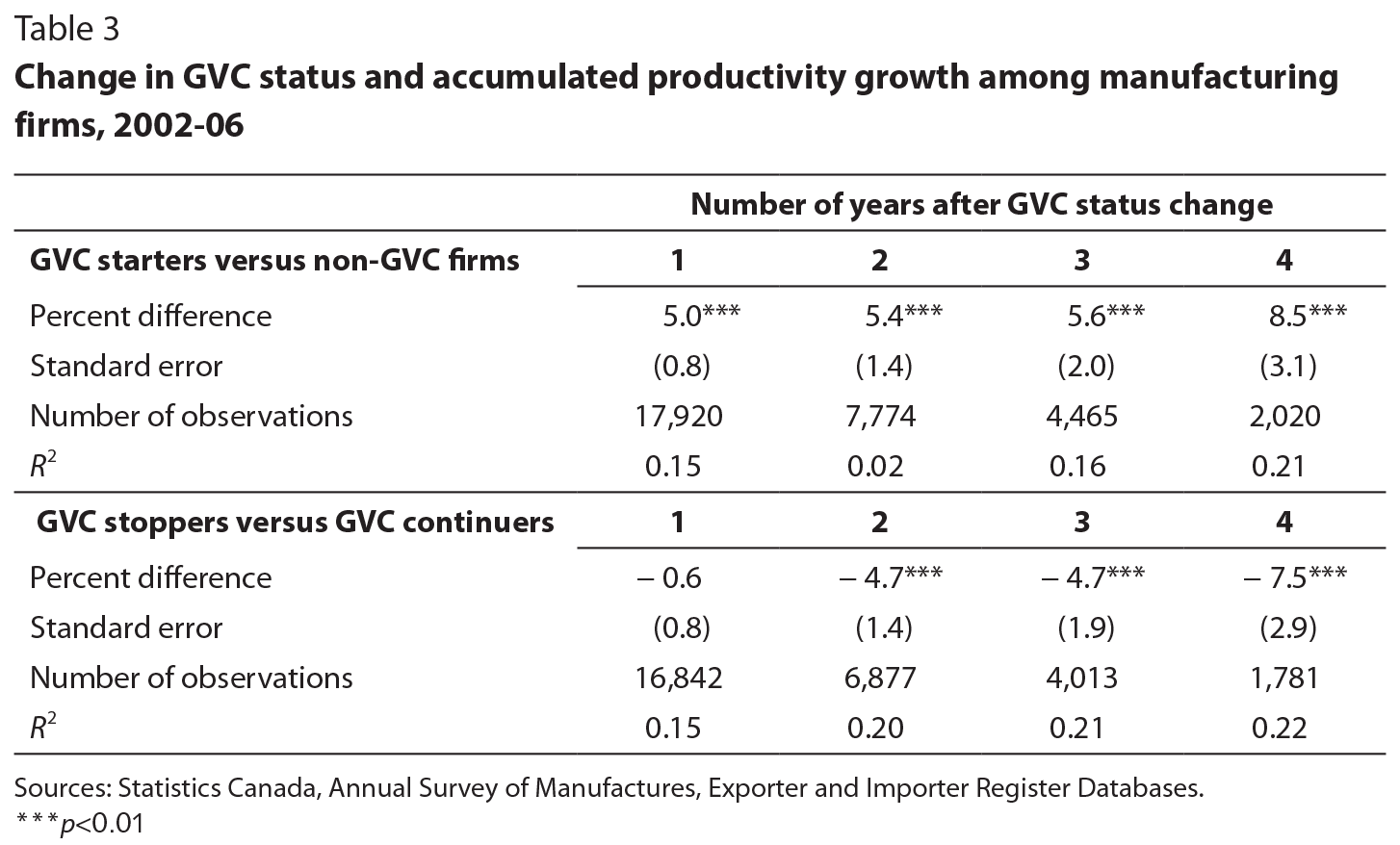

After controlling for the selection effects described above, we find that joining a GVC is indeed associated with higher productivity growth (table 3). During their first year, firms that joined a GVC experienced 5 percent more productivity growth than did firms with otherwise similar characteristics that did not join a GVC. This productivity advantage was statistically significant in each year, and accumulated to 8.5 percent over four years.

Alternatively, firms that dropped out of a GVC experienced only 1 percent less productivity growth in the first year compared with the control group of firms that continued to be in a GVC (a difference that became statistically significant only in the second year). The productivity loss associated with GVC withdrawal soon grew, however, amounting to 7.5 percent after four years — a loss similar in magnitude to the productivity gain from joining a GVC.

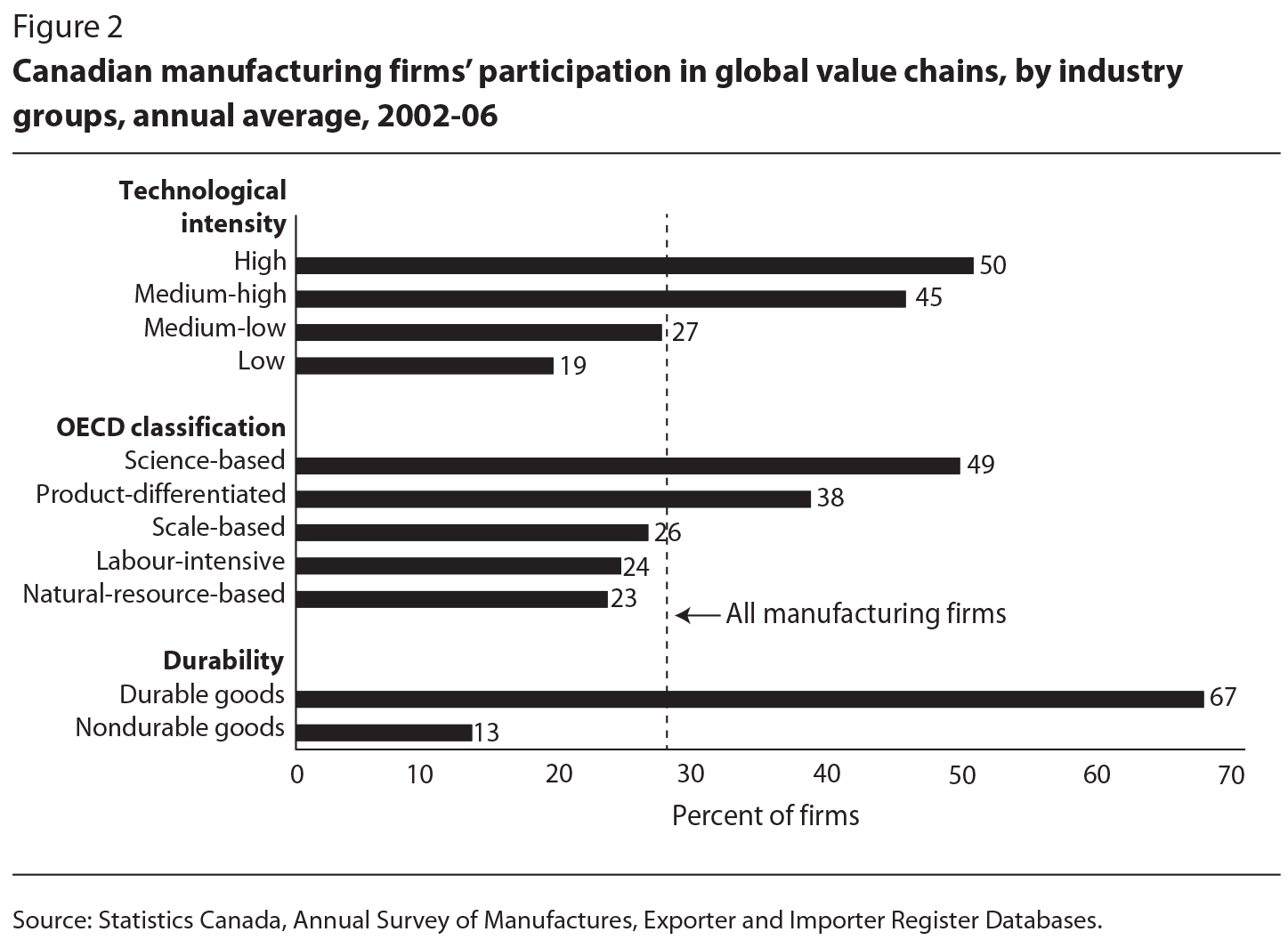

We used three different industry classifications to examine how the benefits of GVC participation differ across industries. The first classification divides -industries into four groups according to technological intensity: high, medium-high, medium-low and low (Hatzichronoglou 1997).5 The second classifies industries into five sectors: science-based, product-differentiated, scale-based, labour-intensive and natural-resource-based (OECD 1987).6 The third classifies industries into durable and nondurable sectors.

GVC participation rates were highest in more technologically advanced industries (figure 2). Roughly half of all firms in high- and medium-high-technology industries were part of a GVC, compared with 28 percent of all Canadian manufacturing firms over the 2002-06 period. In the second classification system, the science-based and product-differentiated sectors had above-average GVC participation rates. And in the third classification, two-thirds of firms in durable goods sectors participated in a GVC, compared with only 13 percent in nondurable sectors.

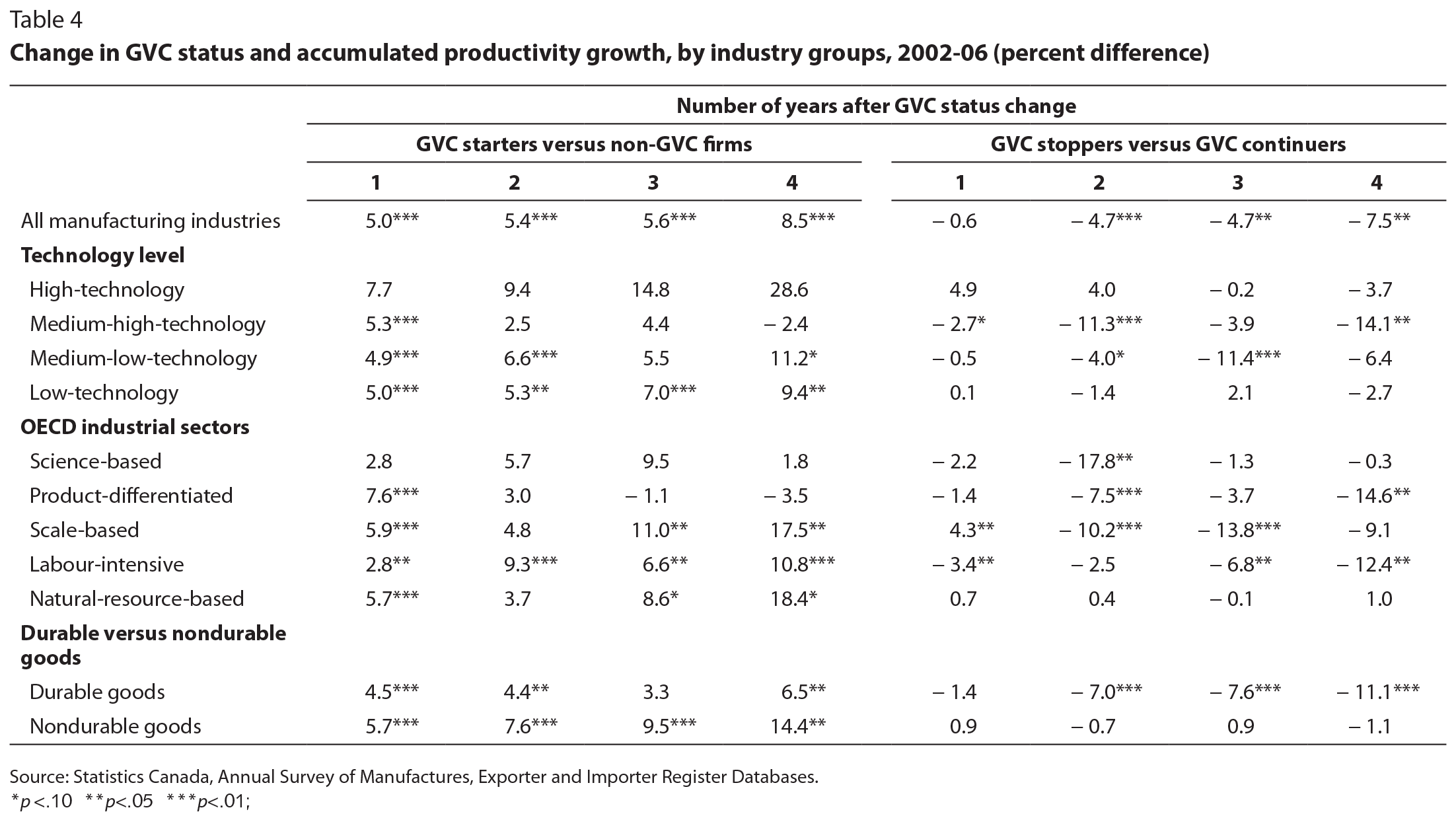

Although GVC participation was more prevalent in high-technology, research-intensive and capital goods industries, the productivity benefits of GVC participation extended across many industries (table 4). GVC starters in high-technology industries (where GVCs are most common) had above-average productivity gains. These gains, however, were not statistically significant, likely because of the smaller number of observations in Canada’s high-tech sector: only about 12 percent of those in other industrial groups. GVC starters in medium-low- and low-technology industries (or, according to the second classification system, the scale-based, labour-intensive and natural-resource-based sectors) had statistically significant gains in accumulated productivity growth for most years. GVC starters in the durable goods sector experienced slightly lower productivity gains than their counterparts in the nondurable goods sector (6.6 percent versus 14.4 percent in accumulated productivity growth four years after joining a GVC).

Comparing firms that withdrew from a GVC with those that continued in a GVC, the largest productivity losses were experienced by medium-high and medium-low-technology industries (alternatively, the product-differentiated, scale-based and labour-intensive sectors) as well as by those in the durable goods sectors.

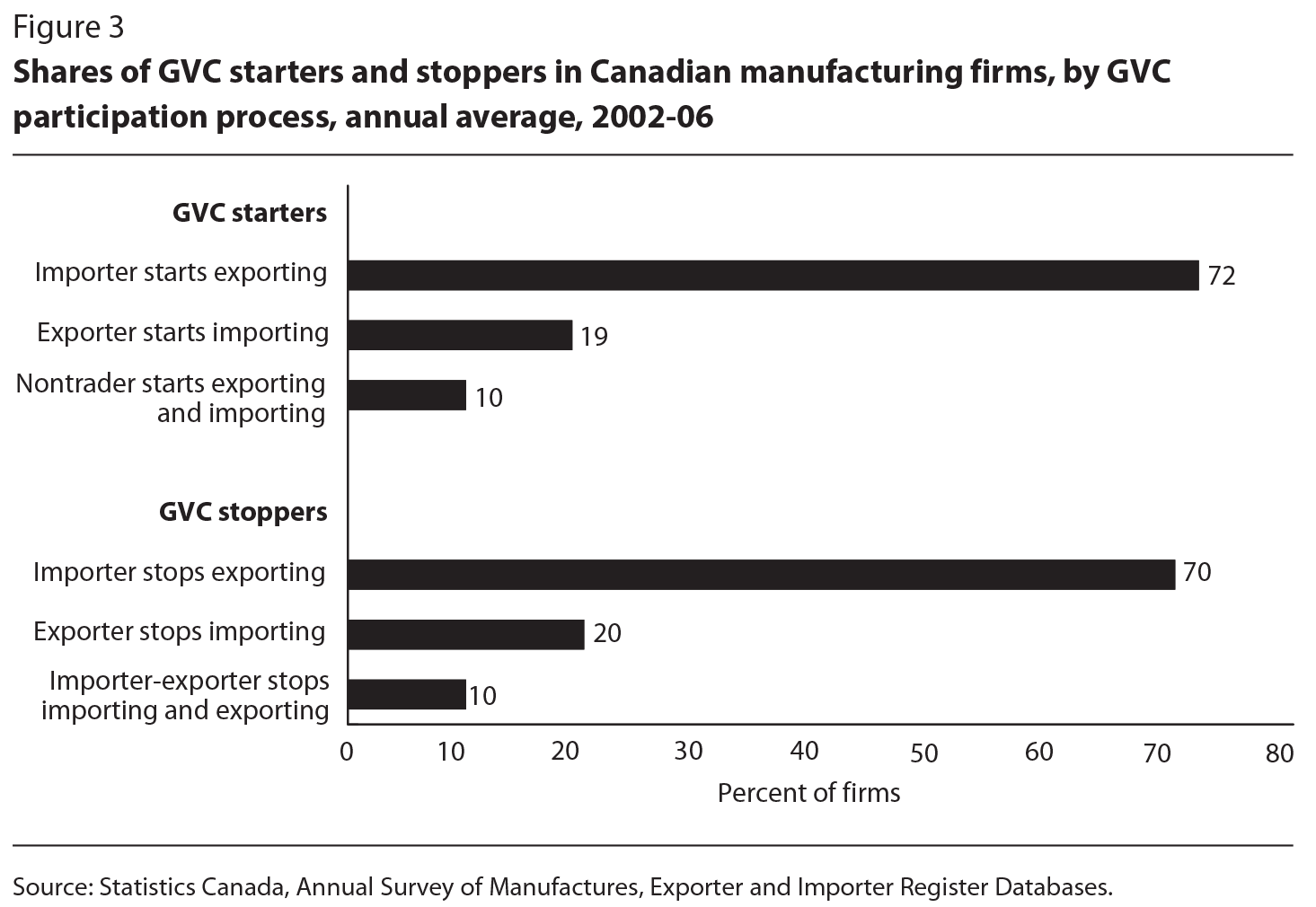

GVC starters fall into three categories: nontrading firms that start importing intermediates and exporting simultaneously; exporters that start importing; and importers that start exporting. Similarly, GVC stoppers comprise three categories: trading firms that cease importing and exporting simultaneously; exporters that cease importing; and importers that cease exporting.

For most firms, GVC entry and exit is a gradual process (figure 3). The vast majority (91 percent) of GVC starters were already one-way traders (either exporters or importers) before becoming two-way traders, while 90 percent of GVC stoppers ceased exporting or importing, but not both. Changes in export activity were mostly responsible for GVC entry (72 percent of starters) and exit (70 percent of stoppers).

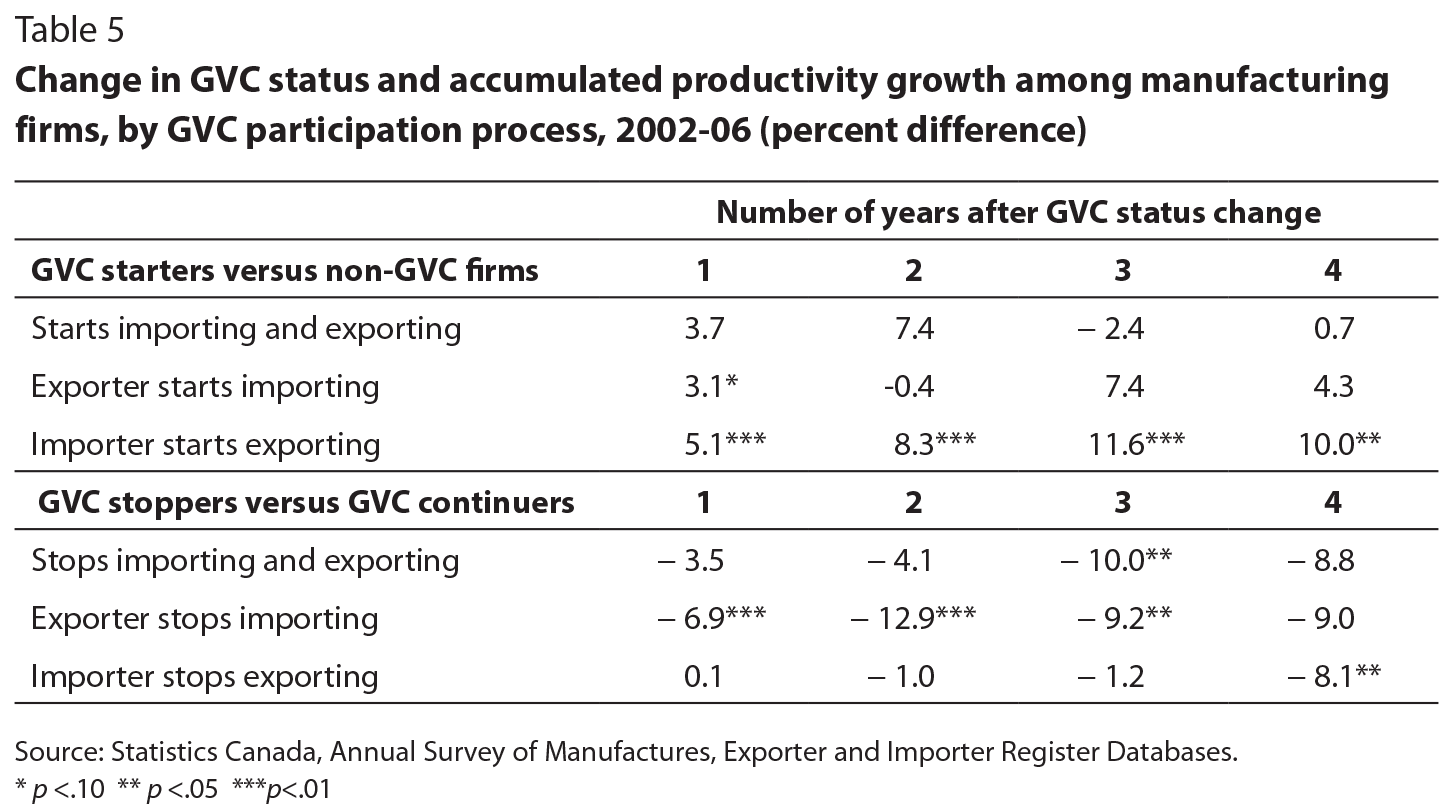

Changes in export status were an important driver of productivity outcomes. Importers that started exporting experienced the largest productivity gains: 5.1 percent gain in the first year, cumulating to 10 percent over four years (table 5). Exporting productivity gains also seemed to be the most persistent, as the higher efficiency levels attained as part of a GVC were temporarily sustained in the short run when the firm stopped exporting: importers that stopped exporting did not experience any statistically significant productivity loss in the first three years, though the loss ultimately accumulated to 8.1 percent four years after the decision to stop exporting. Several studies demonstrate that the productivity gains associated with exporting are connected to investment and technological innovation (for example, Baldwin and Gu 2004; Lileeva and Trefler 2010). This accumulation and the persistence or “stickiness” of the productivity gain over time is consistent with a gradual learning process in exporting.

Contrast this with the GVC firms that stopped importing. They experienced an immediate loss in productivity growth: 7 percent in the first year, 13 percent in the second year and 9 percent in the third year. The immediacy of this productivity loss when a firm stops importing suggests that the firm began forgoing an efficiency that had been incorporated into the production process — perhaps by substituting a domestic technology for the import, or a one-time loss in product quality or cost.

Do the productivity impacts of GVCs differ based on the levels of economic development of the trading partners? To examine this issue, we began by classifying countries as either low- or high-wage using a threshold of $12,000 gross domestic product (GDP) per capita, and re-estimating the results.7 The low-wage category notably includes China and Mexico, which have become key trading partners of Canada’s as well as competitors in other markets (Barnett, Charbonneau and Poulin-Bellisle 2016).

We find that the shares of intermediate imports from, and exports to, low-wage versus high-wage countries were quite similar for Canada’s two-way GVC traders and one-way non-GVC firms. Both groups did the vast majority of their trade with high-wage countries: 95-96 percent of exports, on average, and 85-88 percent of imports (table 6). During the 2002-06 period, however, Canadian firms (both GVC and non-GVC) steadily shifted their trade from high-wage to low-wage countries. Over the period, Canada’s trade with low-wage countries grew at an annual average rate of more than 12 percent, but it fell with high-wage countries by more than 1 percent per year.

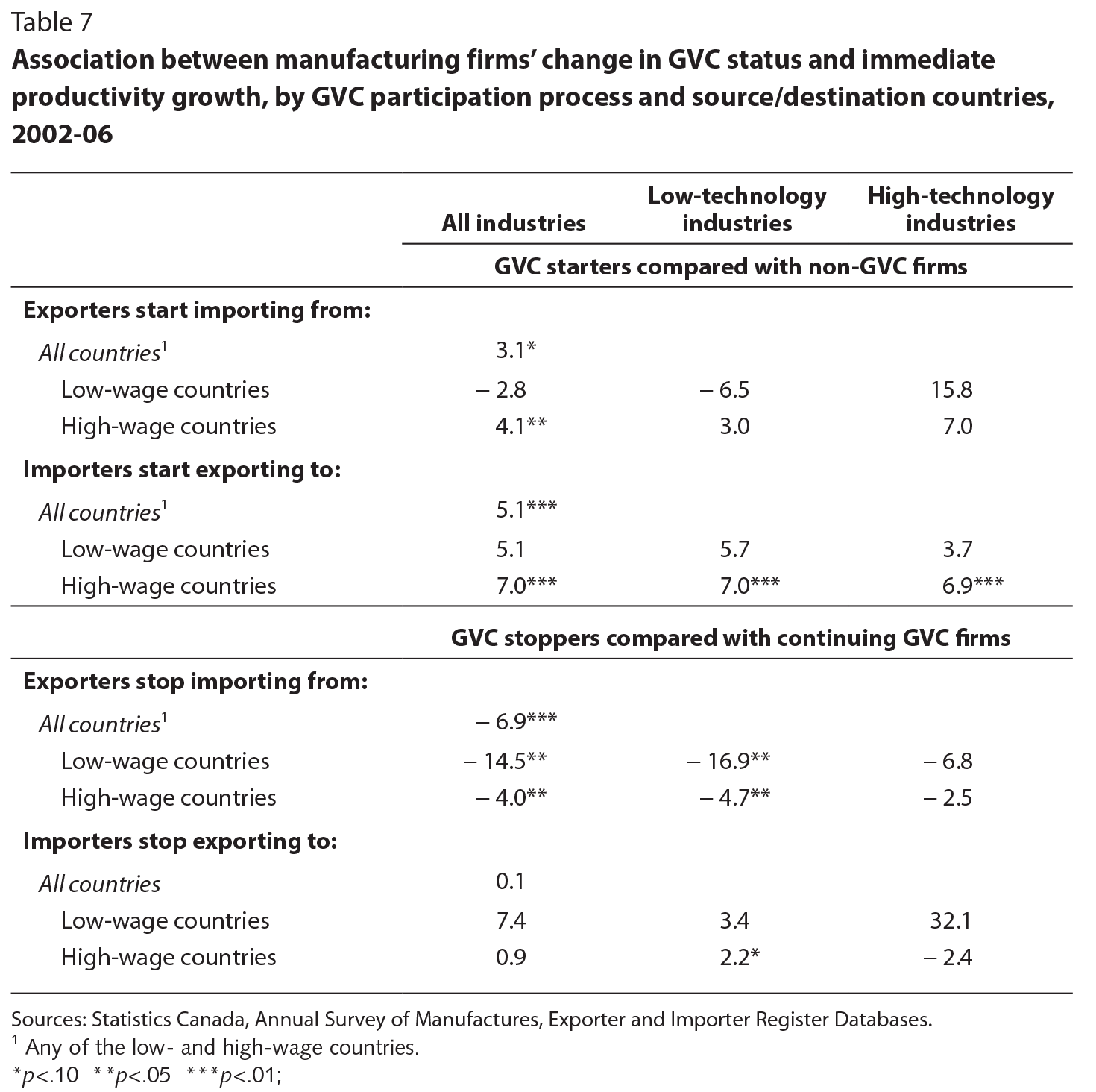

To investigate whether the productivity gain from GVC participation is driven mainly by Canadian firms trading with high-wage countries, we subdivided two groups of GVC starters and two groups of GVC stoppers according to source or destination country. For example, we split Canadian importers into those that began exporting only to low-wage countries and those that did so only to high-wage countries; we excluded firms that began exporting to both low-wage and high-wage countries.8

Table 7 reports estimates of the immediate “within year” productivity changes for each group. Exporters that began importing intermediates from any of the low- and high-wage countries countries had a 3 percent immediate gain in productivity growth compared with non-GVC firms. This gain was entirely due to imports from high-wage countries, which suggests that technology diffusion and learning spillovers might have been driving the benefits of importing (Kelly 2004). Likewise, for exports, those destined for high-wage countries were what drove the productivity gains of the importers that started exporting. Exporting only to low-wage countries also generated immediate gains (5 percent), but these gains were not statistically significant. De Loecker (2007) also finds higher productivity premiums for firms that export to more advanced economies, consistent with the learning-by-exporting hypothesis whereby exporters acquire technological knowledge from buyers in high-wage countries (for other evidence, see Baldwin and Gu 2004).

On the other hand, exporters that stopped importing suffered an immediate 7 percent drop in productivity growth overall. These losses occurred for importers from both high- and low-wage countries, but they were considerably higher for those that stopped importing from low-wage countries (14 percent versus only 4 percent from high-wage countries), with the losses concentrated in the low-technology manufacturing sectors.9 Once again, the losses appear to be consistent with some immediate forgone cost savings in production, perhaps due to offshoring to low-wage countries.

Finally, importers that stopped exporting did not suffer a decline in productivity growth immediately, but gradually over time (table 5). The lack of immediate effect was independent of the income level of the destination of exports (table 7).

The fragmentation of production in global value chains has led to a finer division of labour and specialization across countries. Increasingly, Canadian manufacturers are integrating into GVCs — importing intermediates to produce goods they later export.

More productive firms tend to “self-select” to join GVCs. Indeed, the 28 percent of Canadian manufacturing firms that were GVC participants during the 2002-06 period were generally larger, more productive and paid higher wages. Controlling for this self-selection, we find that firms that joined a GVC became more productive, and their better performance continued into future years. Conversely, firms that stopped participating in a GVC suffered a similar-sized loss in productivity.

The magnitude and timing of the productivity effects of GVC status varied by industrial sector, the route taken to join a GVC and the level of economic development of the trading partners involved. Almost half the firms in high- and medium-high-technology industries (also product-differentiated and science-based sectors) were integrated into GVCs, compared with the overall average of 28 percent. Although GVCs are more prevalent in high-technology, R&D and capital goods industries, the benefits of GVC participation extend across many industries.

For around 90 percent of Canadian manufacturing firms that entered or exited a GVC over the 2002-06 period, the process was incremental. Many began first by importing, and then became importer-exporters. GVC firms that started or stopped exporting experienced significant long-run changes in their productivity growth. In contrast, GVC-firms that stopped importing experienced an immediate loss of productivity growth. The positive export effect on productivity, moreover, was larger and more persistent than the import effect — consistent with the idea that the learning effects of exporting are more permanent and the cost-saving effects of importing intermediates more immediate.

Although Canada’s trade with low-wage countries has been increasing, high-wage countries remain the major source of imported intermediates and the major export destinations. Productivity benefits were higher for Canadian GVC firms that imported intermediates from high-wage countries and exported products to them, which is also consistent with the learning-by-exporting hypothesis and the idea that imports provide a channel of technology diffusion: firms learn more by dealing with buyers and sellers in countries with higher levels of technological and managerial sophistication. Combined with the finding that productivity gains were greatest for new GVCs in the high-technology sector, this suggests that technology transfer is a major source of benefit from joining a GVC.

Firms in lower-technology industries that stopped participating in a GVC by ceasing importing from low-wage countries suffered the largest loss in productivity within the same year. This suggests a separate benefit from being a GVC participant that is primarily restricted to imports from lower-wage countries that offer greater potential cost savings.

Based on these findings, smaller productivity gains might be available from increasing Canadian trade with emerging markets — which has been a recent policy objective — and a more immediate productivity loss might occur if those trading relationships eventually sever.

The authors thank participants at the IRPP Art of the State trade symposium held June 16-17, 2014, in Ottawa, two anonymous referees, as well as -Stephen Tapp, Ari Van Assche and Robert Wolfe for helpful comments and suggestions. An earlier version of this paper was published as “Global Value Chains and the Productivity of Canadian Manufacturing Firms,” Statistics Canada Economic Analysis Research Paper Series, March 2014.

Amiti, M., and J. Konings. 2007. “Trade Liberalization, Intermediate Inputs, and Productivity: Evidence from Indonesia.” American Economic Review 97 (5): 1611-38.

Antràs, P., and E. Helpman. 2004. “Global Sourcing.” Journal of Political Economy 112 (3): 552-80.

Baldwin, J.R., and W. Gu. 2004. “Trade Liberalization: Export-Market Participation, Productivity Growth, and Innovation.” Oxford Review of Economic Policy 20 (3): 372-92.

Baldwin, J.R, W. Gu, A. Sydor, and B. Yan. 2013. Material Offshoring: Alternate Measures. Economic Analysis Research Paper 86. Ottawa: Statistics Canada.

Baldwin, J.R., and M. Rafiquzzaman. 1994. Structural Change in the Canadian Manufacturing Sector (1970-1990). Analytical Studies Branch Research Paper 61. Ottawa: Statistics Canada.

Barnett, R., K. Charbonneau, and G. Poulin-Bellisle. 2016. “A New Measure of Canada’s Effective Exchange Rate.” Discussion Paper 2016-01. Ottawa: Bank of Canada.

De Loecker, J. 2007. “Do Exports Generate Higher Productivity? Evidence from Slovenia.” Journal of International Economics 73 (1): 69-98.

Globerman, S. 2011. “Global Value Chains: Economic and Policy Issues.” In Global Value Chains: Impacts and Implications, edited by A. Sydor. Ottawa: Department of Foreign Affairs and International Trade Canada.

Goldberg, P., A. Khandelwal, N. Pavcnik, and P. Topolova. 2010. “Imported Intermediate Inputs and Domestic Product Growth: Evidence from India.” Quarterly Journal of Economics 125 (4): 1727-67.

Greenaway, D., J. Gullstrand, and R.A. Kneller. 2007. “Firm Heterogeneity, Exporting and ùForeign Direct Investment.” Economic Journal 117 (517): F134-61. [cited in text as Greenaway and Keller; journal’s archives list only these two names as authors of article with this title and date; do you mean a different article?]

Grossman, G., and E. Rossi-Hansberg. 2008. “Trading Tasks: A Simple Theory of Offshoring.” American Economic Review 98 (5): 1978-97.

Gu, W.L., and B. Yan. 2014. Productivity Growth and International Competitiveness. Canadian Productivity Review series. Ottawa: Statistics Canada.

Hatzichronoglou, T. 1997. “Revision of the High-Technology Sector and Product Classification.” OECD Science, Technology and Industry Working Papers 1997/02. Paris: OECD Publishing.

Hummels, D., J. Ishii, and K.-M. Yi. 2001. “The Nature and Growth of Vertical Specialization in World Trade.” Journal of International Economics 54 (1): 75-96.

Kelly, W. 2004, “International technology diffusion.” Journal of Economic Literature 42(3): 752–782.

Kasahara, H., and B. Lapham. 2013. “Productivity and the Decision to Import and Export: Theory and Evidence.” Journal of International Economics 89 (2): 297-316.

Kasahara, H., and J. Rodrigue. 2008. “Does the Use of Imported Intermediates Increase Productivity? Plant-Level Evidence.” Journal of Development Economics 87 (1): 106-18.

Lileeva, A., and D. Trefler. 2010. “Improved Access to Foreign Markets Raises Plant-Level Productivity…for Some Plants.” Quarterly Journal of Economics 125 (3): 1051-99.

López, R.A. 2005. “Trade and Growth: Reconciling the Macroeconomic and Microeconomic Evidence.” Journal of Economic Surveys 19 (4): 623-48.

Melitz, M.J. 2003. “The Impact of Trade on Intra-industry Reallocations and Aggregate Industry Productivity.” Econometrica 71 (6): 1695-1725.

Melitz, M.J., and D. Trefler. 2012. “Gains from Trade When Firms Matter.” Journal of Economic Perspectives 26 (2): 91-118.

OECD (see Organisation for Economic Co-operation and Development)

Organisation for Economic Co-operation and Development (OECD). 1987. Structural Adjustment and Economic Performance. Paris: OECD Publishing.

Rosenbaum, P.R., and D.B. Rubin. 1983. “The Central Role of the Propensity Score in Observational Studies for Causal Effects.” Biometrika 70: 41-55.

Smeets, V. and F. Warzynski. 2013. “Estimating productivity with multi-product firms, pricing heterogeneity and the role of international trade,” Journal of International Economics, 90 (2), 237-244.

Topalova, P., and A. Khandelwal. 2011. “Trade Liberalization and Firm Productivity: The Case of India.” Review of Economics and Statistics 93 (3): 995-1009.

Wagner, J. 2007. “Exports and Productivity: A Survey of the Evidence from Firm-Level Data.” World Economy 60 (1): 60-82.