Redesigning Canadian Trade Policies for New Global’s Realities

Overview of the Research Findings

Stephen Tapp, Ari Van Assche and Robert Wolfe

The federal government’s effective rejection of BHP Billiton’s bid for Saskatchewan’s Potash Corporation in 2010 was seen as a flashpoint in the recent evolution of the Investment Canada Act (ICA), which many hoped would lead to greater clarity in the rules of the game for foreign direct investment (FDI). But uncertainty persists and, with the introduction of provisions such as “exceptional” circumstances, new questions have been raised. While the federal government has undertaken measures to address specific gaps in the ICA, it has done so without conducting a more general reassessment of the overall policy regime.

What is Canada’s national interest with respect to FDI? Is there a need for further policy reform in light of the patterns and flows of changes in international capital, trade and investment? Where do we stand in relation to other global competitors for investment? In this study, Dany Assaf and Rory McGillis examine these questions as they pertain to the ICA and assess how transparent, clear and coherent the Act is compared with the regimes of 11 other countries.

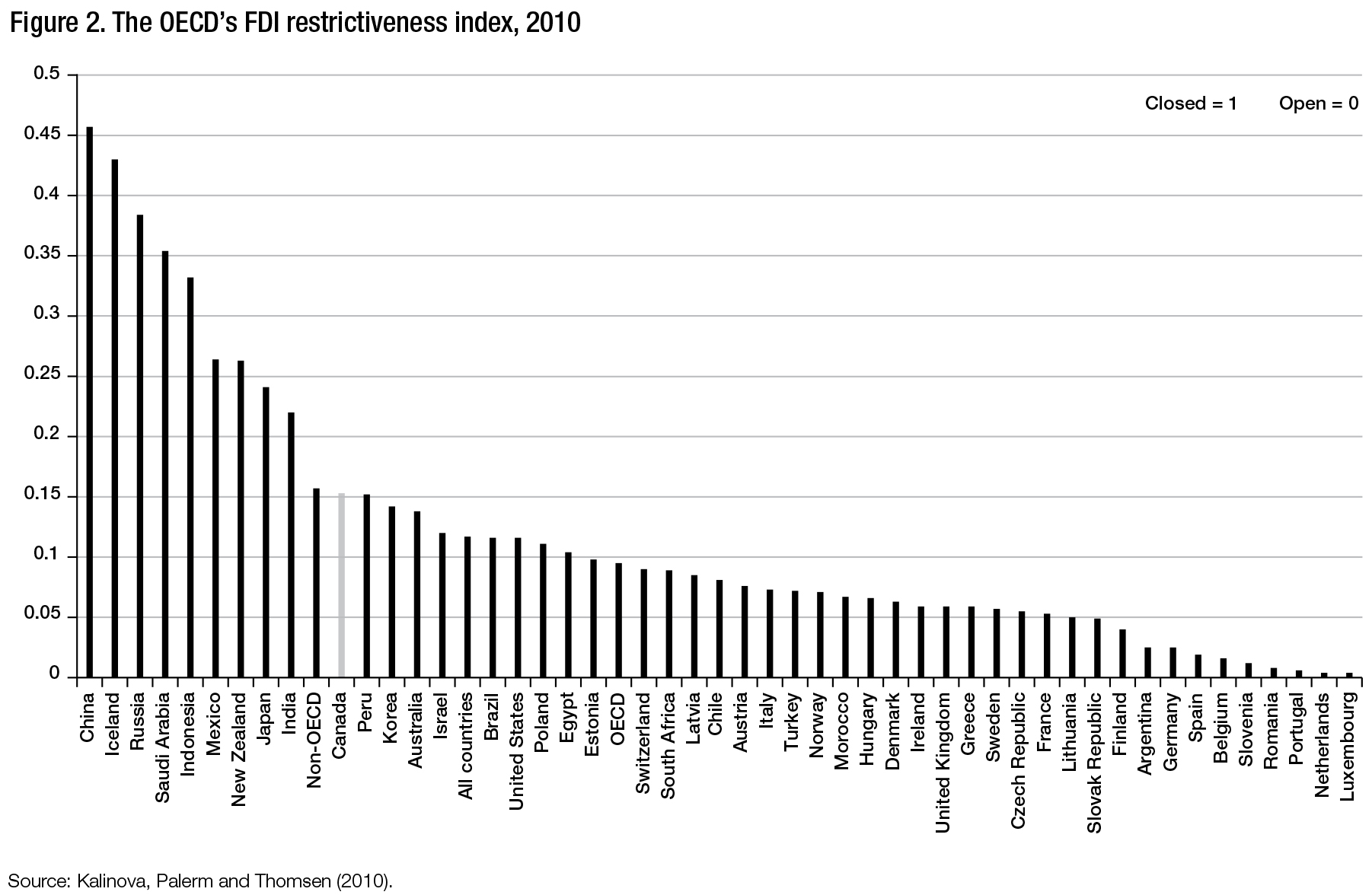

They argue that international rankings like the OECD’s FDI Restrictiveness Index misrepresent Canada as being guarded toward foreign investment, while other countries employ more informal means to reject investments. In practice, since 1985 the ICA has produced only two refusal decisions that have ultimately blocked takeovers (in noncultural industries).

However, the fact that these rejections have all occurred in recent years and are part of a global trend toward greater scrutiny suggests the need for a more transparent review process. This would provide greater certainty for investors and all Canadians alike, and it would avoid the need for drastic policy amendments in reaction to the specific issues raised by high-profile cases, as happened with Nexen and Progress Energy Resources.

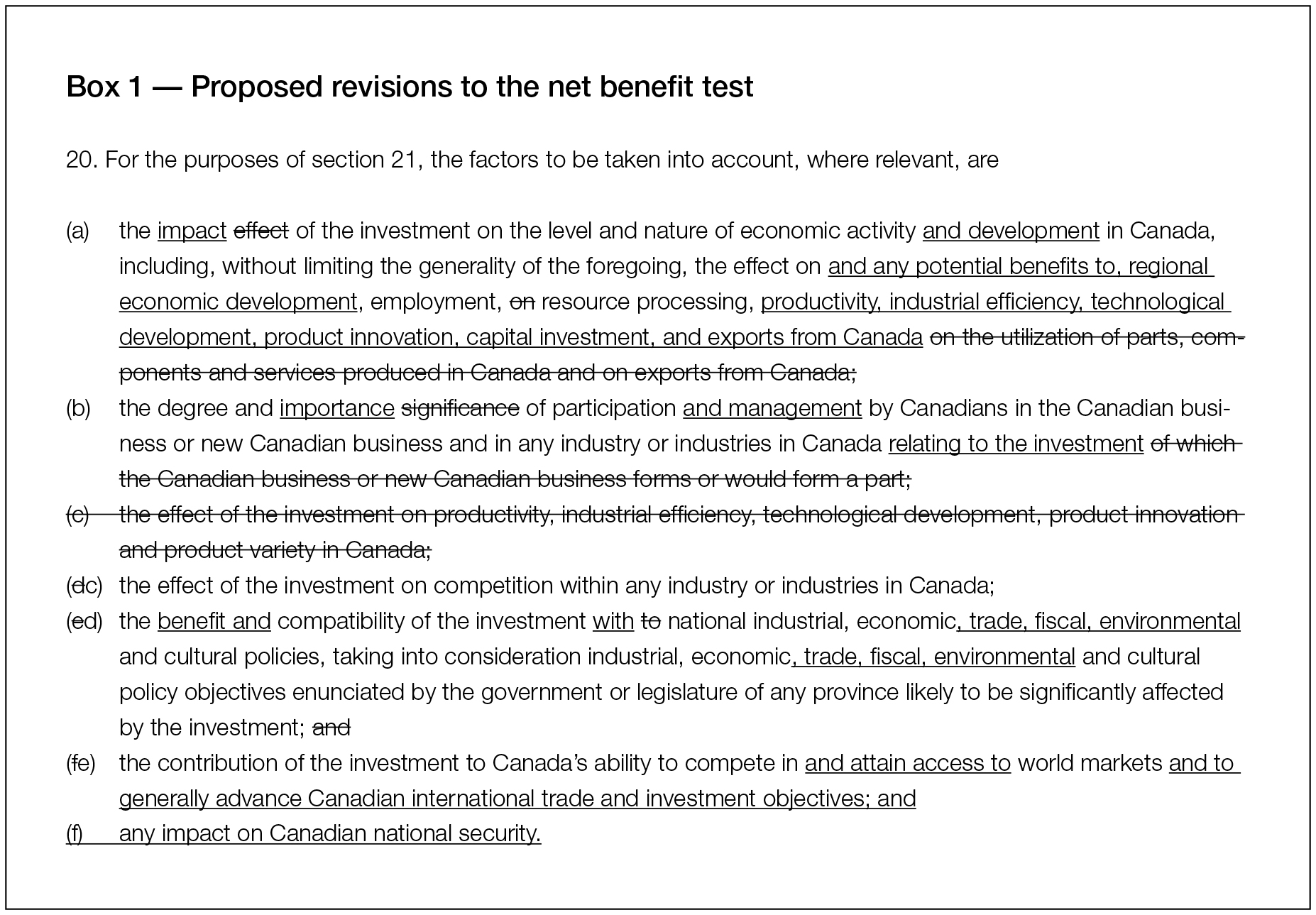

Assaf and McGillis argue in favour of keeping the net benefit test, the centrepiece of the current review process. They argue that it has worked comparatively well over its long history, and investors are familiar with its overall direction. They recommend the government focus instead on better communicating to investors what is expected of them. Among other things, they recommend the government

As a more general comment, the authors note with concern the increasing reference in public discourse to the concept of “strategic assets.” As the term is open to broad political interpretation, they say it is of little practical utility for policy and should be strongly resisted.

Until the policy is clarified, it will be understandable if investors believe their money is no longer welcome in Canada. – Financial Times, October 22, 2012

The quote above is the punchline to an editorial in response to the interim rejection1 of the takeover of Progress Energy Resources, a Canadian gas producer, by Malaysia’s national oil company, Petronas – a transaction that ultimately was revised and approved. This case and the high-profile acquisition of Nexen by state-owned China National Offshore Oil Corporation (CNOOC) highlighted important questions about the role of foreign direct investment (FDI) in Canada and the effectiveness of Canada’s investment review process. Since the rejection of the proposed takeover of MacDonald Dettwiler in 2008 and the effective rejection of the proposed takeover of Potash Corporation of Saskatchewan (Potash Corp.) in 2010,2 Canadians have been subjected to many views on the potential benefits and detriments of foreign investment. Although Canada remains a significant destination for foreign capital, a great deal of discussion has ensued regarding the federal government’s approach to FDI.

The Canadian investment review process has also seen significant developments in the past several years, including the introduction of rules for national security review, policy guidelines for acquisitions involving foreign state-owned or -controlled entities (SOEs) and the recent introduction of a new “exceptional” standard of review for SOEs targeting the Canadian oil sands sector. In isolation, each of these changes might be worthwhile, but the incremental process by which they have been implemented has added uncertainty to the overall direction of Canada’s investment policy. Also, the federal government has not yet provided the clarity many had expected on the interpretation of the “net benefit” test – the lynchpin of the Investment Canada Act3(ICA) – a commitment it made in 2010 following the Potash case.

If Canada is to continue to position itself effectively in the global investment climate and if the Canadian public and investors are to have greater certainty and clarity about investment rules, the ICA policy needs to be examined in a forward-looking and comprehensive manner. How, then, does Canada get the most from its investment policy? This study seeks to answer this question by examining both the ICA and how it compares with foreign investment review regimes in 11 leading jurisdictions.4 We begin with a review of the ICA‘s linkages to broader trade policy, its evolution over time and the basic statutory functions it plays today. We then assess the ICA‘s relevance to contemporary investment policy issues, and how it compares in effectiveness and coherence with those of global competitors.

Canada is not alone in facing challenges to its foreign investment review policy or changes in the international investment environment. Leading economies around the world are introducing new guidelines to respond to international developments, scrutiny of proposed acquisitions is increasing and rejections are becoming more frequent. Our findings reveal that, in fact, Canada does comparatively well in providing a rules-based framework for reviewing foreign investments. It is our view that Canada remains committed to FDI and to open and interconnected markets. Building on this foundation, we provide a series of recommendations on how to further clarify the rules and ensure that they remain responsive to Canadians’ concern that foreign investment be of “net benefit” to Canada.

Before going further, it is important to clarify several principles that inform the study throughout. In the face of the uncertain and shifting foreign investment landscape, it can be difficult to discern the best way forward for Canada’s foreign investment regime. In such circumstances, it is best to turn back to the core interests of any policy and work ahead from there.

The core principles surrounding foreign investment in Canada should be viewed through the lens of the Canadian national interest and the benefits and costs to our economy. In this regard, the starting point of analysis is the reality that Canadians benefit from having others invest their capital in our country and help us fund projects and expand our businesses more quickly and cost efficiently than we could on our own. Whether blueor white-collar workers, all Canadians benefit; we all depend on strong businesses operating in Canada.

The reasons for this are simple and compelling: the pool of capital available within the Canadian population of 35 million people is much less than that available within a global population of 7 billion people. If Canadian business were to rely on seeking capital only within Canada, the laws of supply and demand would dictate that our cost of capital would be much higher than the cost for our global competitors, which have access to greater capital resources. This approach would hinder the growth and competitiveness of Canadian businesses and the economy and their potential to create jobs, only making things worse for all of us. These facts are hard to overcome.

Accordingly, there is no logic in turning down or fearing investment capital from any particular country as a matter of principle. This is especially so in a world where significant wealth and capital have accumulated in new places – such as Asia and South America – and will continue to do so for the coming century. Although challenges to the continued growth of global trade and investment remain, it is clear that past and future benefits of global commerce and development are too compelling to developed, emerging and developing countries alike to be seriously reversed at this stage.

At the same time, it is perfectly acceptable for Canada, a strong and prosperous country with attractive assets, to insist on ensuring that significant foreign investments offer specific and tangible benefits to the Canadian economy.

In the face of shifting developments and the increasing public scrutiny of foreign investments, we also approach this analysis with the perspective that policy must seek an appropriate balance between flexibility and clarity in the rules. These goals are not incompatible. It is reasonable that governments need to retain a certain degree of flexibility in foreign investment review to ensure that the national interest is well served and can effectively evolve to deal with new issues and challenges. Recognizing this dynamic at the outset is crucial for both government and investors to understand clearly how the investment review process will unfold.

The art of remaining open to vital foreign investment and maximizing the benefits is in having clear rules that provide certainty to the process and encourage the right kinds of investment. In the true Canadian tradition, the operating principle should be: we generally do not care where you come from or what your background is, but if you are prepared to invest here and act as a genuine partner in the Canadian economy and follow the rules, your investment is welcome.

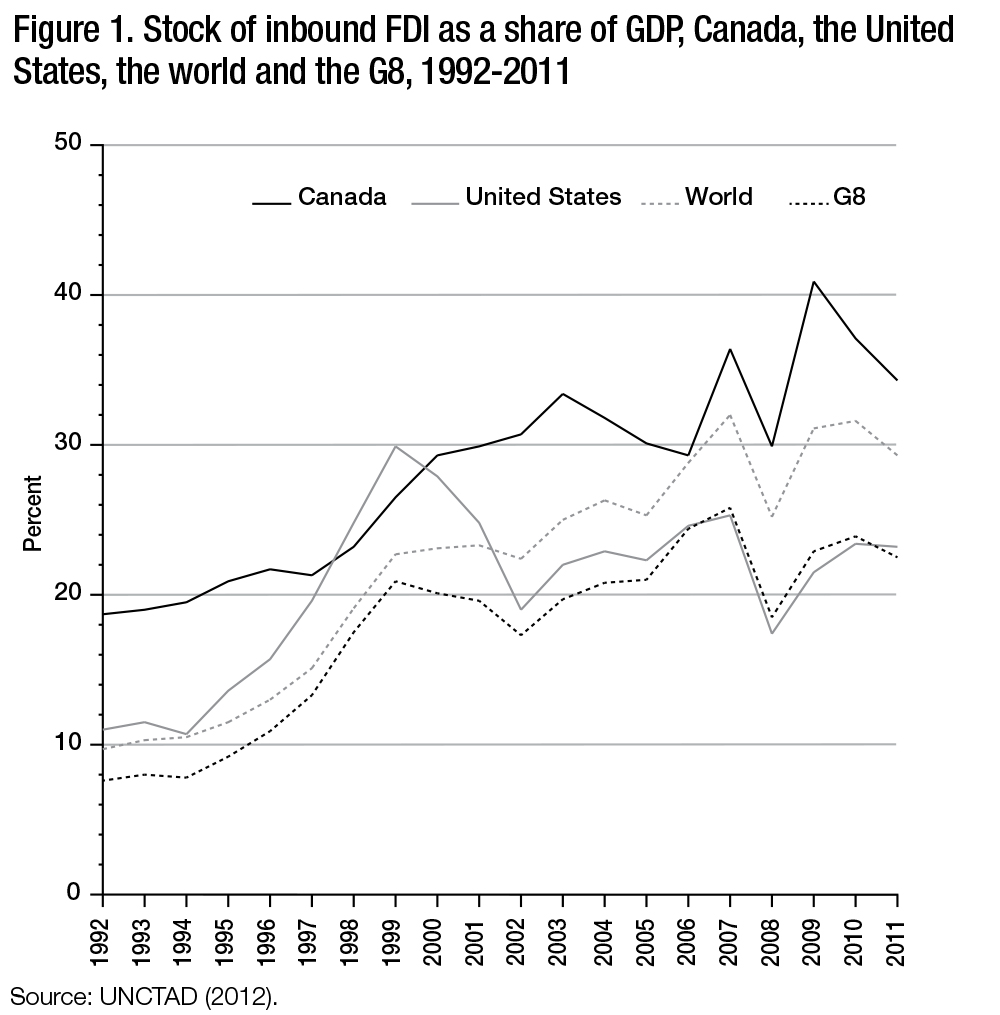

Over the past 40 years, technological advancements in information sharing, communications and transportation, coupled with the movement to liberalize and standardize domestic and international commercial regulation, have supported a dramatic advance in the internationalization of the world’s economies. The flow of global FDI increased from US$13 billion to US$1.5 trillion between 1970 and 2011, an increase of over 12,000 percent (UNCTAD 2012).5 Canada has been an active participant in this internationalization trend, its stock of inbound FDI having grown appreciably over the past two decades and remaining considerably higher than that of our main competitors (figure 1). At the end of 2011, this stock totalled $607.5 billion, equivalent to 34 percent of Canada’s gross domestic product (GDP) (DFAIT 2012b),6 while Canadian outbound direct investment in foreign markets totalled an even greater $684.5 billion (DFAIT 2012a). Canada’s further integration into the global economy is a policy initiative actively fostered by all levels of government and supported by Canada’s demographics.7

International trade and investment has long played a key role in Canada’s economy. We see this in each generation –– trade with Great Britain during our founding ; manufacturing exports to the United States after the Second World War; and new markets in Asia and South America at present. From shortly after the birth of the Canadian nation-state, the Canadian Pacific Railway was moving goods from within Canada to international markets and immigrants from all over the world into the Canadian interior to help build the country. This history set the stage for the key role of international trade in Canada’s modern economy where, in 2011, exports accounted for more than one-quarter of Canada’s GDP ($456.5 billion of $1,720.7 billion) (Statistics Canada 2013; Statistics Canada 2012). Access to international markets and foreign capital has given western Canada the financing – $116 billion between 2000 and 2010 (Alberta 2012) – to develop its capital-intensive oil sands resources. The Alberta government has stated that foreign investment is critical to further development and as a competitive source of capital (Wingrove 2012). As of 2011, Alberta’s oil and gas development and mining sectors employed 151,000 people, and oil sands royalties contributed more than $3.7 billion to the provincial government’s coffers in fiscal year 2010-11 (Alberta 2012). Another $364 billion is expected to be invested in Canada’s oil sands industry between 2012 and 2035, supporting 880,000 direct and 1.45 million indirect person-years of employment; more than 40 percent of the domestic income effects are predicted to occur outside Alberta (Arcand, Burt, and Crawford 2012).

In addition, it is important to remember Canada’s “original” free trade agreement, the iconic Canada-United States Automotive Products Agreement (the Auto Pact),8 signed by the two countries in January 1965 to remove tariffs on automotive products and parts and to guarantee a minimum volume of US automotive manufacturers’ production in Canada. The agreement facilitated investment in, and development of, a world-class automotive industry in Canada, a key part of Ontario’s manufacturing sector for the past five decades. Moreover, the Auto Pact led to generations of quality jobs and livelihoods for Canadians. Between 1990 and 2011, automotive manufacturers made nearly $40 billion in direct investment in Canada. Prior to the financial crises, automotive exports totalled roughly $70 billion in 2007, more than $67 billion of which went to the United States. Trade in finished vehicles with the United States resulted in a $25-billion trade surplus in 2007, accounting for 18.5 percent of Canada’s total trade surplus with that country and 57 percent of Canada’s total industrial trade surplus (Canadian Vehicle Manufacturers’ Association, n.d.).

As we look ahead, we are encouraged by the part that foreign investment could play as Canadians develop other priorities, such as renewable energy and other emerging industries and related employment opportunities. For example, in January 2010, the Ontario government announced an agreement for a consortium led by South Korea-based Samsung C&T Corp. and the Korea Electric Corporation to invest $7 billion in wind and solar power construction and operation in Ontario. This investment is expected to create more than 16,000 green energy jobs in the manufacturing, construction, installation and operation of renewable energy projects, and provide approximately 10 percent of Ontario’s energy needs – although the full extent of these expected benefits might be imperilled by a trade dispute regarding domestic-content requirements in Ontario’s renewable energy program (Ontario 2010).9

FDI continues to be beneficial to the Canadian economy in other ways. It increases the pool, and competitively decreases the cost, of capital available to Canadian business to develop Canadian resources and create employment and training opportunities. It attracts top management talent to Canada and disseminates management training and expertise into the Canadian labour force. It facilitates technology transfer into the Canadian economy from foreign jurisdictions. And it further integrates Canada into international markets with concomitant reciprocal trade and investment accessibility for Canadian businesses (Hejazi 2010).

International trade has not been wholly without challenges, however. There are long-held concerns in Canada that foreign capital, left unchecked, would purchase and control many of the country’s most valuable assets. This, it is argued, would result in a “hollowing out” of Canadian industry and leave a branch plant economy, with management jobs and profits repatriated to foreign corporate headquarters and with Canada’s most talented and ambitious labour in hot pursuit (Dawson 2012). In the postwar decades, this concern grew more acute as US interests increasingly dominated Canadian industry. By 1970, Canadian ownership in certain industries, such as petroleum and rubber, was below 10 percent, and three-quarters of all FDI in Canada came from the United States (O’Sullivan 1980, 177). Public support in Canada for foreign investment and opening its markets was vulnerable to opinion that foreign investors were profiting from their acquisition of Canadian businesses at the expense of Canadians.

An assessment of more recent transactions and rejections reveals that they come on the heels of a string of high-profile foreign acquisitions of Canadian companies over the past decade, rekindling the debate about Canada becoming a branch plant economy. Iconic Canadian companies – among them Alcan, Inco, Falconbridge, Dofasco, Stelco, Ipsco, Molson, Fairmont, Four Seasons and Newbridge (Reguly 2012) – have become foreign owned or subsidiaries of foreign multinationals. Meanwhile, Canada’s unwavering commitment to the rules and principles of open investment in the face of the formal and informal practices of certain countries to protect their industries from foreign acquirors generated media scrutiny and some public criticism. For instance, Scott Hand, then Chief Executive Officer of Canada’s former mining giant Inco (until it was acquired in 2006 by Brazilian-based Vale), said, “Other countries have judiciously exercised their right to stop takeovers; there is no reason why Canada can’t. Canada is a Boy Scout playing among other countries that play hardball” (McNish, Clark and Laghi 2008).

As noted, however, Canada’s stock of outward FDI now significantly exceeds its stock of inward FDI – by almost $80 billion at the end of 2011. Canadians have been increasingly active on the global stage, with investors such as the Ontario Municipal Employees Retirement System (OMERS), the Ontario Teachers’ Pension Plan (OTPP) and the Canada Pension Plan Investment Board (CPPIB), to name a few, that are making significant acquisitions overseas. For instance, in late 2010, OMERS and OTPP teamed up to acquire the rights to operate the high-speed rail link connecting London and the Channel Tunnel (HS1) for $3.4 billion (OMERS 2010), and in April 2012 the CPPIB agreed to pay $1.14 billion for stakes in several major Chilean toll roads (CPPIB 2012). Clearly, foreign investment is not simply a one-way issue for the Canadian public interest. Furthermore, as Walid Hejazi points out, fears of “hollowing out” are not reflected in the facts, which show an upward trend in the number of world-leading Canadian companies (Hejazi 2010, 9).

It is against this historical trade and investment backdrop that it is helpful to view Canada’s foreign investment review legislation.

The precursor to the Investment Canada Act was the Foreign Investment Review Act (FIRA),10 which existed between 1973 and 1985, and required foreign acquirors to prove that their proposed transaction was “a significant benefit to Canada” (section 2(1)). Although no acquisitions were rejected under FIRA, the reviews were often onerous and the acquisitions approved with strict conditions (Spence and Takach 1986, 13). In 1985, the federal government replaced FIRA with the ICA, and the “significant benefit to Canada” test with a less onerous review standard of “net benefit to Canada.” The new legislation was also intended to signal to foreign investors that Canada was indeed open and welcoming to them (Spence and Takach 1986). More than 1,600 applications have been reviewed and approved, and more than 13,000 notifications processed, under the ICA (Industry Canada 2012f). Only two investment applications have not been approved; a third, the Petronas-Progress transaction, was approved only after an initial rejection (Feteke 2012).

Foreign investment reviews under the ICA are handled by Industry Canada or, in the case of investments in the cultural sector, by the Department of Canadian Heritage. To be approved, the investments must be determined to be of “net benefit” to Canada by the relevant minister.

Generally, any non-Canadian investor who proposes to acquire direct control of a Canadian corporation of a certain size and that carries on a Canadian business must file an Application for Review (the “Application”) with the minister of industry. For 2013, the relevant review threshold for World Trade Organization (WTO) investors is $344 million of worldwide value of the assets of the target Canadian business (Industry Canada 2013). Once implemented, recent amendments to the ICA will increase the review threshold to $600 million in “enterprise value”; over the next four years, it will rise to $1 billion, followed by annual GDP-indexed increases thereafter (Budget Implementation Act, section 448).11 The acquisition of indirect control of a Canadian business by an investor from a WTO member country is generally not subject to review and approval – for example, when a Canadian subsidiary is acquired as a result of the acquisition of the shares of a non-Canadian corporation in the context of a global takeover. Investments in certain culturally sensitive areas, such as the publication and distribution of books, magazines, films and music, are subject to a greater level of scrutiny than other transactions, and may be prohibited as a matter of government policy (Investment Canada Regulations, schedule IV).12 The review threshold for cultural investments is $5 million (Industry Canada 2013).

When a proposed acquisition of control of a Canadian business exceeds the review threshold, an investor must file the Application and the industry minister will assess whether the proposed investment is “likely to be of net benefit” to Canada (ICA, section 16(1)). Among other things, the Application describes the investor’s plans for the Canadian business it proposes to acquire, and explains why the investment will likely be of net benefit to Canada. Initially, the industry minister has 45 days to review the Application but this can be extended (ICA, section 22(1)).

When a proposed acquisition of control does not exceed the review threshold, the ICA requires an investor to file a two-page notification form within 30 days of the implementation of the investment (section 11(b)).

The substantive net benefit assessment is made on the basis of policy statements by the industry minister and the following broad economic and policy criteria under section 20 of the ICA: (1) the effect of the investment on economic activity in Canada; (2) the degree and significance of participation by Canadians in the Canadian business and in any industry in Canada of which the Canadian business forms a part; (3) the effect of the investment on productivity, industrial efficiency, technological development, product innovation and product variety; (4) the effect of the investment on competition within Canada; (5) the compatibility of the investment with national industrial, economic and cultural policies; and (6) the contribution of the investment to Canada’s ability to compete in world markets.

Although the “net benefit” test is not perfect, we would not recommend changing it to a new standard for two key reasons. First, by the nature of the exercise, any new foreign investment review test would still incorporate concepts incapable of exact definition. Second, from an enforcement and interpretation perspective, we would have to start all over again to flesh out the practical definition of any new standard. The existing net benefit test is not unreasonable – and our history and experience with it help provide meaningful contours to the concept that are worth preserving.

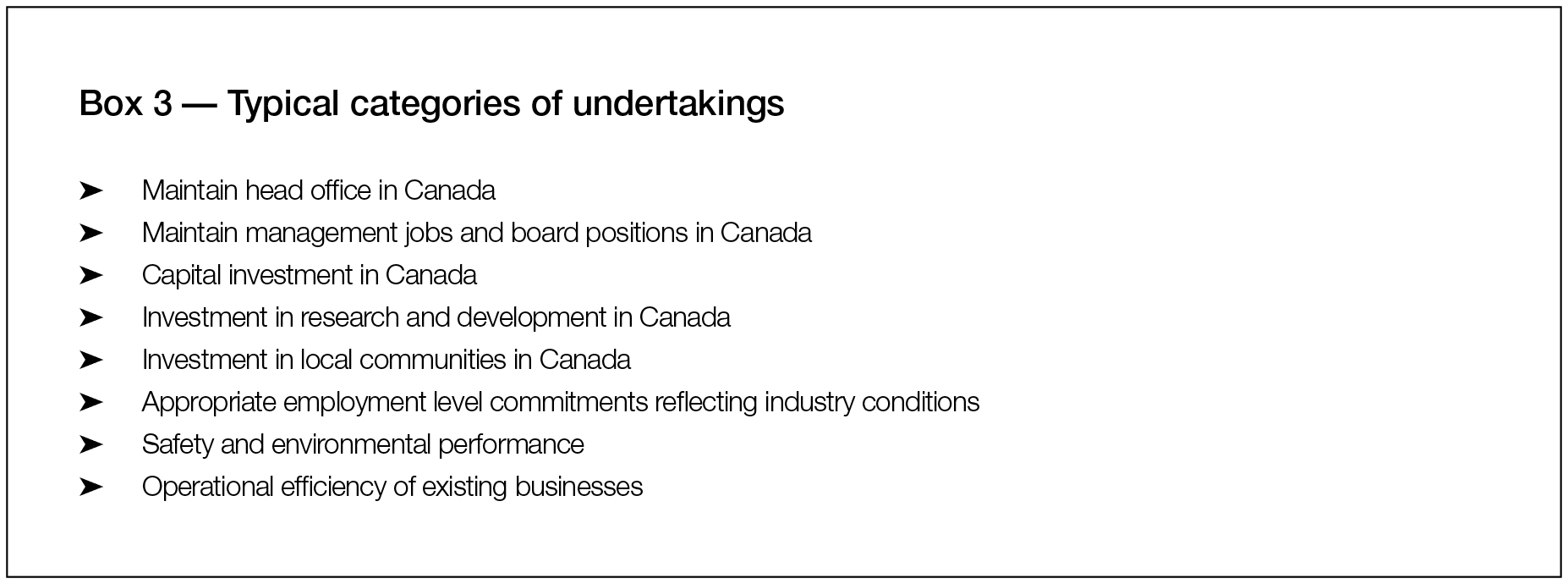

To satisfy the net benefit test, investors typically enter into binding undertakings with the Canadian government regarding certain benefits to Canada that will result from the investment. These undertakings typically include commitments such as maintaining the Canadian head office, making planned capital expenditures and providing ongoing opportunities for Canadians to participate in the management of the business. In addition, undertakings relating to maintaining Canadian production, employment, research and capital expenditures are usually made for a period of at least three to five years. Normally, there are no continuing restrictions on foreign investors after the undertakings expire. In the case of an investment by an SOE, however, undertakings relating to corporate governance and commercial orientation can survive for as long as the SOE controls the Canadian business.

The Investment Review Division of Industry Canada monitors compliance with undertakings by reference to its Guidelines: Administrative Procedures (Industry Canada 2012a). These guidelines provide that a performance evaluation ordinarily will be made 18 months after the implementation of the investment. If the evaluation finds that implementation – subject to subsequent circumstances beyond the investor’s control – is substantially consistent with the original expectations and that no major commitments remain unfulfilled, there is no further monitoring. Failure to comply with an undertaking can result in, among other things, the forced divestiture of the investment or monetary penalties (ICA, section 40(2). The guidelines also provide that, “where inability to fulfill a commitment is clearly the result of factors beyond the control of the investor, the investor will not be held accountable” (Industry Canada 2012b). In practice, and in accordance with section 39.1 of the ICA, the government and the investor may agree to variances or replacement undertakings if an original undertaking is clearly unachievable.

For instance, it has been reported that Industry Canada declined to pursue foreign mining companies Vale, Xstrata and Rio Tinto for apparent breaches of employment undertakings related to their acquisitions of Canadian mining companies – respectively, Inco, Falconbridge and Alcan – although the undertakings have not been made public, and so we are unable to confirm their actual commitments. All these foreign mining companies made significant job cuts to their acquired Canadian businesses in 2009 (Hoffman 2010).

However, Industry Canada’s later efforts to enforce the undertakings of US Steel might signal a heightened sensitivity to this guideline and a limit to Industry Canada’s willingness to accommodate a foreign acquiror in breach of its undertakings (McCarthy 2012; Hoffman 2010). US Steel13 was the first case in which proceedings were brought against an investor for failing to comply with its undertakings. US Steel allegedly failed to comply with undertakings it had made in connection with its 2007 acquisition of Stelco, the large Canadian steel manufacturer, including maintaining a minimum level of steel production and employment at Stelco’s Canadian facilities; US Steel also had made no apparent attempt to renegotiate new or revised undertakings (Wakil 2009). Instead, the company transferred considerable steel production to its US facilities and laid off a significant portion of its Canadian workforce. It is likely that this both invoked the federal government’s displeasure and raised questions about whether the Canadian plant closures were truly “the result of factors beyond the control of the investor,” as US Steel claimed, or a business decision to concentrate production in the United States (Wakil 2009). In any event, the Industry Minister rejected US Steel’s claim that fallout from the 2008 financial crisis rendered it unable to fulfill its undertakings. The parties eventually settled the case on the basis of strengthened undertakings after US Steel failed in its constitutional challenge, which claimed that the ICA process and penalties for enforcing the undertakings violated its constitutional rights to a “presumption of innocence” and a fair hearing.

The past several years have been a tumultuous period for Canadian FDI policy. The context in which Canadians and investors view foreign investment rules and how they are enforced by government has been influenced by the global financial crisis generally and more specifically by issues relating to (1) the first rejections issued under the ICA (outside the cultural sector);14 (2) concerns regarding the sale of so-called strategic assets; (3) the development of national security reviews over the 12 years since the terrorist attacks of September 11, 2001; and (4) the rise of SOEs as active foreign investors.

In the 23 years in which no proposed acquisition was rejected under the net benefit test, criticism of the test was relatively muted. Then, in 2008 and 2010, respectively, came the rejection of the MacDonald Dettwiler and Potash Corp. transactions, which drew attention to Canada’s foreign investment review system and encouraged calls for greater clarity on what exactly constitutes “net benefit” under the ICA and how the test is applied.

The 2008 MacDonald Dettwiler rejection put the net benefit test and decision-making transparency into the spotlight and broke any taboos surrounding the issue of rejection (Assaf 2008). In response, in 2009 the federal government amended the ICA to promote greater transparency. The amendments required that the industry minister provide reasons for any decision to reject an investment (section 23.1), authorized the minister to disclose information on the review process if doing so would not prejudice investors (section 36(4.1)) and required the publication of annual reports regarding the administration of the ICA (section 38.1). Attention to the issue had largely subsided by 2010, when the rejection of BHP Billiton’s bid for Potash Corp. triggered renewed criticism about the uncertainty and the opaqueness of the review process and prompted concern that Canada was becoming a more restrictive economy. The recent interim rejection of the Petronas acquisition has only exacerbated matters.

A by-product of the debate on high-profile transactions such as MacDonald Dettwiler-Alliant Techsystems, BHP Billiton-Potash Corp. and CNOOC-Nexen is the increasingly casual use of the term “strategic asset” by politicians and media commentators in connection with foreign acquisitions. This has led to some politicization of the concept. In fact, although the designation “strategic asset” or “strategic industry” is a notion found in the foreign investment review systems of several major countries, it is not part of Canada’s system. During the debate over the BHP Billiton-Potash Corp. transaction, Industry Minister Tony Clement specifically emphasized that “strategic” does not appear in the ICA and is not taken into consideration in the review of a proposed foreign acquisition (Chase 2010). Continued use of the term, however, perhaps has led to a misperception by the public of certain aspects of the ICA review process.

Another recent development is the federal government’s introduction in 2009 of a national security review provision in the ICA. The review establishes a legal process to assess acquisitions that potentially involve national security issues and to solicit relevant information from the foreign investor. The review does not define or provide guidance on what constitutes a “national security” concern – an omission that could cause uncertainty for investors. When it announced its most recent guidelines on SOEs, Industry Canada also said that amendments to the ICA would provide greater flexibility to extend the duration of national security reviews of proposed foreign investments in exceptional circumstances (Canada 2012). As of this writing, however, the government had provided no further information regarding the amendments.

In 2007 the federal government introduced special review guidelines for SOEs under the net benefit test. It recently announced revisions to those guidelines in response to concerns raised in the context of the CNOOC’s $15.1-billion bid for Nexen and Petronas’ $5.2-billion bid for Progress Energy Resources (Canada 2012). Australia and the United States have also introduced special rules for foreign SOE investors. Interestingly, Australia’s Foreign Investment Review Board (FIRB) chairman, Brian Wilson, announced in August 2012 that the FIRB would also be updating its policy guidelines to clarify when foreign SOE investments need FIRB approval (Australia 2012; Tempone and Campbell 2012).

We explore these developments and their effects in more detail below.

The first investment rejection under the ICA occurred in May 2008 when US-based Alliant Techsystems’ $1.33-billion proposed acquisition of MacDonald Dettwiler was denied. MacDonald Dettwiler is a Canadian-based aerospace, information and products company that, among other things, owns and operates RADARSAT satellites that monitor remote areas in northern Canada (MacDonald, Dettwiler and Associates, n.d.). The Industry Minister stated that Alliant had not satisfied the net benefit test but did not provide further explanation (Industry Canada 2008). There was speculation that the federal government’s chief concern was the effect of US national security laws on Canada’s priority access to RADARSAT information (Todd 2011). In addition, there were some concerns that MacDonald Dettwiler’s business development had been supported by federal development funds, and that those benefits would be realized or captured by foreign investors (Harb 2008). Primarily, this case appeared to raise national security concerns, although there was no formal national security review at the time.

In August 2010, Australia-based BHP Billiton’s $40-billion hostile takeover bid for Potash Corp. was denied approval. BHP Billiton’s bid generated considerable controversy over the prospect of one of Saskatchewan’s largest companies and a global industry leader becoming a subsidiary of a multinational company, and the potential consequences to the significant tax and royalty revenue stream that Potash Corp. generates for the Saskatchewan government (Wall 2010). The Industry Minister’s assessment that the proposed transaction was not likely to be of net benefit to Canada was not final – BHP Billiton had 30 days to make additional representations and submit undertakings, which the company did not elect to do (Industry Canada 2010) – so the Minister was not required to provide in-depth reasons for rejecting the acquisition. (Had the decision been final, he would have been required to submit reasons under a 2009 amendment to the ICA.) The Minister did state in a press conference, however, that the acquisition would not have helped Canada to compete in world markets, would not have boosted productivity, efficiency and innovation, and would not have elevated economic activity; moreover, BHP Billiton lacked Potash Corp.’s experience in the potash industry (Todd 2011).

Petronas’ attempt to acquire Progress Energy Resources was initially rejected, in October 2012. Petronas had apparently denied Industry Canada’s request for a delay until December 7 to make a determination of the proposed transaction, even though there had been no indication that approval would have been withheld. In response, Industry Canada abruptly rejected the transaction (Cattaneo 2012b). In the aftermath, Prime Minister Stephen Harper gave Petronas a period of 30 days in which to respond and said that the Canadian government would soon “put out a clear, new policy framework regarding these sorts of transactions” (Cattaneo 2012b). Industry Canada subsequently approved the Petronas acquisition, on December 7 as it had originally requested, and also announced revisions to the policy guidelines relating to SOE investments (Industry Canada 2012c; Canada 2012).

Perceptions that Industry Canada did not provide sufficiently detailed explanations of why these three transactions were not of net benefit to Canada caused concern over the potential uncertainty being communicated to foreign investors interested in the Canadian market (“Closing Canada” 2012). One commentator went as far as to suggest that Saskatchewan was a “banana republic” as a result of the provincial government’s opposition to the Potash Corp. acquisition (Corcoran 2010). Further amplifying this uncertainty was the introduction of the terms “strategic resource” and “strategic asset” in the discussion regarding the ICA review. The rejections, regardless of their merit, broke taboos about using the ICA to reject a foreign takeover, and it is not known what chilling effect they might have had on future investment plans. In our view, therefore, these developments make it necessary for the federal government not only to further clarify the net benefit test, but also to make its current enforcement policy more transparent.

Although neither “strategic asset” nor “strategic resource” is found in the ICA, the terms gained currency in public debate following the MacDonald Dettwiler and Potash Corp. rejections. The general connotation is fairly straightforward: a strategic asset or resource is a company that employs many people, has significant symbolic value and/or controls critical resources or technology and is an important player in the economy. This concept is somewhat analogous to the “strategic industry” protections common in European jurisdictions. It also once formed part of Canada’s foreign investment review regime, attracting special restrictions or review for foreign investment above a certain threshold in certain industries deemed of special importance.15 The current question is whether it is prudent or necessary for Canada to adopt this concept formally, as part of the ICA.

Saskatchewan Premier Brad Wall maintained that BHP Billiton’s bid should be rejected because Potash Corp. was a “strategic resource” (Wall 2010). Premier Wall based his assessment on the expected loss of Saskatchewan’s institutional leverage in the potash sector – Saskatchewan has almost half of proven global reserves (Potash Corporation of Saskatchewan 2011) – and the potential jeopardy to the significant potash royalty revenue stream flowing to the provincial government (Jasinski 2011; Rocha 2010). He also noted that BHP Billiton, as a large multinational for which potash would simply be one of many different business lines, had indicated a weak commitment to ensuring a high potash price (Wall 2010). Furthermore, following the rejection of BHP Billiton’s bid, Gerry Ritz – the federal Agriculture Minister and regional minister for Saskatchewan on behalf of the federal government – stated that “the government rejected BHP’s bid in part because it decided that the mineral is a “strategic resource’ in the global food supply” and that Saskatchewan’s potash reserves give “Canada an influential position in the marketing of a key agricultural commodity” (Reguly, Hoffman and Bouw 2010).

John Manley, a former industry minister and now President and Chief Executive Officer of the Canadian Council of Chief Executives, alleged that Premier Wall’s remarks were politically motivated: “The Premier’s ‘strategic resource’ rationale is a political calculation – one that he is entitled to make if he feels he can justify it to his citizens. But the ICA exists to ensure that Canadians benefit from foreign investment, not to protect resource companies designated as ”˜strategic’ at the 11th hour by provincial governments” (Manley 2010). Industry Minister Tony Clement then clarified the federal government’s position regarding “strategic asset” and “strategic resource,” noting that as neither term appears in the ICA, neither was taken into consideration in the review of the proposed acquisition (Chase 2010).

This case brought to the fore issues of strategic assets and foreign control and implied that Canadians need to control or have access to the supply of these resources. Control would be especially important, if, for example, the owners later exposed themselves as acting to harm Canadian national security or hoarding a resource for their own citizens in times of national crises. The case also highlighted the interests of governments as stakeholders at risk of losing tax revenue that could harm their fiscal health in an era of austerity and deficits.

Despite the federal government’s position, the use of “strategic asset” nevertheless persists. For example, Ontario Finance Minister Dwight Duncan described the TMX Group Inc., the entity that owns and operates the Toronto Stock Exchange and TSX Venture Exchange, as a “strategic asset” and “one of the country’s crown jewels” after the 2011 announcement of a proposed merger between the TMX Group and the London Stock Exchange Group, owner of the Borsa Italiana and the London Stock Exchange (Howlett 2011). In March 2012, Saskatchewan politicians debated in the provincial legislature whether Canada’s grain industry should be considered a “strategic economic sector” following the announcement of potential takeover bids for Viterra Inc., a global Canadian-based agribusiness and successor company to the Saskatchewan Wheat Pool (Saskatchewan 2012). Finally, in July 2012, on the eve of an announcement of a provincial election, Quebec Finance Minister Raymond Bachand called home-improvement retailer Rona Inc. a “strategic asset” and said that, if necessary, the federal government should reject the hostile takeover bid made by US-based Lowe’s Companies, Inc. (Van Praet 2012). Bachand supported this assertion by noting that Rona employs 28,000 Canadians directly, and an additional 90,000 jobs are tied to Rona’s suppliers (“Lowe’s Offer” 2012).

The continued use of the term thus generates uncertainty; it also has the potential to create an informal category of reviewable, easily politicized transactions and to confuse the ICA net benefit analysis. In fact, the concept of “strategic asset” is already subsumed within the “net benefit” framework, as Minister Bachand implied in citing the number of Canadian jobs tied to Rona, as a foreign acquisition’s impact on Canadian jobs is a key part of the net benefit test and associated undertakings. The purpose of the net benefit test is to ensure that foreign investors create value for Canada, whether or not the investment has a high “strategic value.” The test requires that the foreign acquisition be beneficial to Canada on a holistic assessment of factors. A potential acquiror essentially is required to show and confirm that its acquisition of the Canadian business would benefit Canada relative to the existing benchmarks of the business under existing Canadian control. By this standard, there is already consideration of the strategic value of the Canadian-based target of a foreign acquiror, albeit not specifically under that terminology. It is not in Canada’s interest to allow the use of “strategic asset” to become a politicized code to prevent a deal from being approved for political reasons. The consideration of a company’s strategic value should be clearly identified as already subsumed within the net benefit test.

The ICA was amended in March 2009 to add an explicit national security review, which applies to proposed investments to establish a new Canadian business or acquisitions of any size, with no financial threshold (part IV.1). An investment may be reviewed before or after closing (section 25.1). This followed the recommendation of Industry Canada’s 2008 Competition Policy Review Panel that it is “in Canada’s interests in a post-9/11 world to have in place an explicit national security test to support its trade and investment policies” (Competition Policy Review Panel 2008, 30). The introduction of an explicit test brought Canadian policy in line with that of other advanced national economies such as the United States, the United Kingdom, China, Japan and Germany (31). It was speculated at the time that this recommendation was in part prompted by the 2008 rejection of Alliant Techsystems’ attempted takeover of MacDonald Dettwiler. Because an explicit national security test did not exist in the ICA at the time, the federal government was forced to view this question in the light of the net benefit test, which was not explicitly designed for such a purpose (VanDuzer 2010, 22).

National security review under the ICA engages government players other than the industry minister. An investment is reviewable under part IV.1 if (1) the minister considers that the investment could be injurious to national security, after consultation with the minister of public safety and emergency preparedness (to whom the Canadian Security Intelligence Service reports); and (2) the governor in council makes an order for review on the recommendation of the minister (section 25.3(1)). More generally, the ICA provides that the minister shall (where appropriate) use the services and facilities of other departments, branches or agencies of the federal government in exercising powers or performing duties under the statute (section 5(2)(a)).

The national security review authorizes the industry minister to initiate a review of an investment of any size by a foreign investor if the minister has reasonable grounds to believe that the investment could be injurious to national security (section 25.2). The minister may also require the foreign investor to provide any information necessary to determine whether those grounds exist (section 25.2). The minister must notify the foreign investor that its investment is under review and that the investor has the right to make representations to the minister (section 25.2). A foreign investor who receives this notice may not implement the investment unless it receives either a notice indicating that no further action will be taken in respect of the investment or a copy of an order authorizing the investment to be implemented (section 25.3). In addition, the minister may review an investment that has already been implemented (section 25.1). If the review finds it advisable in order to protect national security, the foreign investor may be (1) prohibited from implementing the investment, (2) authorized to implement the investment on certain conditions or undertakings, or (3), if it has already implemented the investment, required to divest itself of control of the Canadian business or of its investment in the entity (section 25.3).

The national security review has been criticized for its opaqueness and ambiguity because the ICA does not define “national security” or identify sectors of particular concern (McCarthy 2011). The review, however, is consistent with those of major trading nations, which also do not define “national security.” Some jurisdictions, such as the United States, provide guidance on what might be relevant to a national security review, which generally suggests that a very broad category of transactions is potentially reviewable. Industry Canada, however, has issued no such guidance. The most official publicly available discussion of the meaning of the term comes from the testimony of Industry Canada officials before the Senate committee hearing that considered the proposed national security review amendments to the statute. In describing to the committee why “national security” would not be defined in the ICA, Richard Saillant, then Director of Investment Policy at the Market Framework Policy Branch of Industry Canada, stated:

There is an agreement amongst countries that national security issues have evolved since September 11 and they are constantly evolving. Therefore, there has been a tendency to accept that concerns are self-judging. Countries have been reluctant to challenge each other on their definitions of national security because they accept, first of all, that national security is a prime concern but is also something that is evolving. Therefore, there is no explicit definition of the term “national security” in the [ICA], but there is clearly intent to comply and to be consistent with our trade obligations…We need the flexibility to be able to identify threats as they arise. Very few countries have employed an explicit definition of national security. For instance, in the United States they provide examples but, in the end, the illustrative lists being provided covers a very broad swath of the American economy. (Standing Senate Committee on National Finance 2009)

Colette Downie, then Director General of the Marketplace Framework Policy Branch, told the committee, “WTO agreements apply to how national security reviews will be done or potentially done. [The definition of ”˜national security’] must be consistent with those obligations. They define a preset series of national security-related issues” (Standing Senate Committee on National Finance 2009).

The WTO agreements and the North American Free Trade Agreement (NAFTA) are Canada’s most important treaties regarding international trade and protection, but neither provides much additional guidance regarding the definition of national security as it pertains to the ICA review. The WTO incorporates by reference the General Agreement on Tariffs and Trade (GATT), which contains a “security exceptions” clause that allows a contracting party to take any action it “considers necessary for the protection of its essential security interests” relating to fissionable materials, traffic in arms, ammunition and other war materials, or “taken in time of war or other emergency in international relations” (article XXI). GATT does not define “essential security interests,” “time of war” or “emergency in international relations.” NAFTA has a similar “national security” clause, which also allows a party to take any action it “considers necessary for the protection of its essential security interests” relating to traffic in arms, ammunition and other war materials, “taken in time of war or other emergency in international relations” or relating to nuclear weaponry (article 2102).

Maintaining flexibility is key to ensuring for any government that national security can be protected in unforeseen circumstances. At the same time, a national security review should be sufficiently transparent and provide sufficient guidance to promote a predictable and certain investment environment, in which the review is used to assess actual concerns and to mitigate potential egregious politicization of national security issues.

Given the degree of Canada-US integration in national security policy, it is instructive in this context to consider the practice of US authorities in reviewing the national security implications of foreign investments. A more detailed and comprehensive international comparison can be found in appendix A.

The United States introduced its national security review and presidential veto authority of foreign transactions in 1988 through the Exon-Florio Amendment of the Defense Production Act of 1950 (DPA).16 The national security review is undertaken by the Committee on Foreign Investment in the United States (CFIUS), created in 1975 to monitor the impact of foreign investment and coordinate the implementation of US foreign investment policy. The Exon-Florio Amendment authorized the president to review the effect on national security of foreign acquisitions of US entities and to suspend or prohibit acquisitions threatening to impair national security (section 2170(b)). “National security” was not defined in the amendment; the amendment’s cosponsor, Senator J. James Exon, stated before Congress that the meaning of the term was intended to “be read in a broad and flexible manner” (quoted in Fagan 2009, 11). The amendment does, however, provide a list of factors to be considered in reviewing a foreign acquisition for national security concerns. These include the domestic production required for national defence, the control of domestic industries and commercial activity by foreign citizens as it affects US national security, the potential national security-related effects of the transaction on US critical infrastructure or critical technologies and such other factors as the president or CFIUS may determine to be appropriate (section 721(f)) (see appendix A). These factors were supplemented by the USA Patriot Act of 2001, the Homeland Security Act of 2002 and the Foreign Investment and National Security Act of 2007 (FINSA),17 which collectively added “critical infrastructure” and “homeland security” as areas of concern comparable to national security. These statutes also provide substantially further guidance on what constitutes “critical infrastructure” and additional factors by which the president and CFIUS can assess foreign investments.

A foreign investor may voluntarily file a notice with CFIUS for a proposed transaction that might create a national security risk. If CFIUS finds that “the covered transaction does not present any national security risks or that other legal provisions provide adequate and appropriate authority to address the risks,” then CFIUS will advise the parties in writing that they have received a “safe harbour” with respect to that transaction. If CFIUS finds that this standard is not met, it may “enter into an agreement with, or impose conditions on, parties to mitigate such risks or refer the case to the president” (United States 2010). Under the DPA, the president has wide discretion to suspend or prohibit any foreign transaction (section 721(d)).

Although the US government has provided substantially more guidance to its national security review than comparable jurisdictions, it has also attracted criticism alleging it has politicized the national security review. For instance, in August 2005, CNOOC withdrew its US$18.5-billion offer to buy US-based Unocal Corporation after strong and vocal political opposition in the United States, including a 398-15 vote in the House of Representatives for a measure calling on President George W. Bush to review the proposed transaction (CNOOC Limited 2005; Mostaghel 2007, 605). In another infamous example, Dubai Ports World was forced to divest itself of its acquired US port operations the next year, following political pressure (Borger 2006).

The allegations of politicization, if true, also might reflect the disadvantages of an overall foreign investment review regime based on national security grounds. Other than the CFIUS review, the United States has no review regime of general application or of specific application to SOEs. As a result, when a proposed foreign acquisition is thought to be contrary to US national interests, its opponents must fit it into a national security rubric. It is worth noting here that FINSA broadly defines transactions subject to review (a “covered transaction”) as “any acquisition, merger or takeover after the effective date by or with any foreign person, which could result in control of a US business by a foreign person” (section 2(a)(3)). We discuss this as it applies to SOEs in the next section.

Canada should provide at least as much guidance as the United States offers, given that country’s importance to Canada and its renowned pursuit of effective national security protections. As examples of such guidance, Canada could look to the factors to be considered that are listed in the Exon-Florio Amendment, the USA Patriot Act of 2001, the Homeland Security Act of 2002 and FINSA (see appendix A).

The rise of state-owned enterprises has introduced new players and potential issues as wealth moves from West to East. Are SOEs motivated by commercial objectives or by noncommercial objectives that current trade and investment rules did not contemplate and are not really designed to address? A corporation is presumed to be motivated almost solely by the desire to increase its value for its shareholders. An SOE, however, cannot be always presumed to share the same motivation. Thus, there is some degree of uncertainty whether foreign investment review regimes need to be altered to review SOEs and, if so, how.

It is hard to ignore the significant capital resources and prominence of SOEs today; they will continue to play a large role in the global economy. In September 2008, the Economist described the recent rise of the emerging economies as “the rise of state capitalism” (“The Rise of State Capitalism” 2008). Then, in January 2012, the magazine reported that, of the 100 largest companies from emerging markets, 28 were SOEs. China’s 121 biggest SOEs saw their total assets increase from US$360 billion in 2002 to US$2.9 trillion in 2010, and sovereign wealth funds currently account for some of the largest reservoirs of investment capital, controlling approximately US$4.8 trillion in assets, and expected to surpass US$10 trillion by 2020 (“New Masters of the Universe” 2012). Their importance has become apparent in countries such as Canada, which has sizable natural-resource-based industries and requires capital-intensive development. Industry Canada reports that, between 2008 and 2011, SOE investment in Canada grew from a share that was marginal to more than 20 percent of the total asset value of foreign investment subject to ICA review (Industry Canada 2012e).

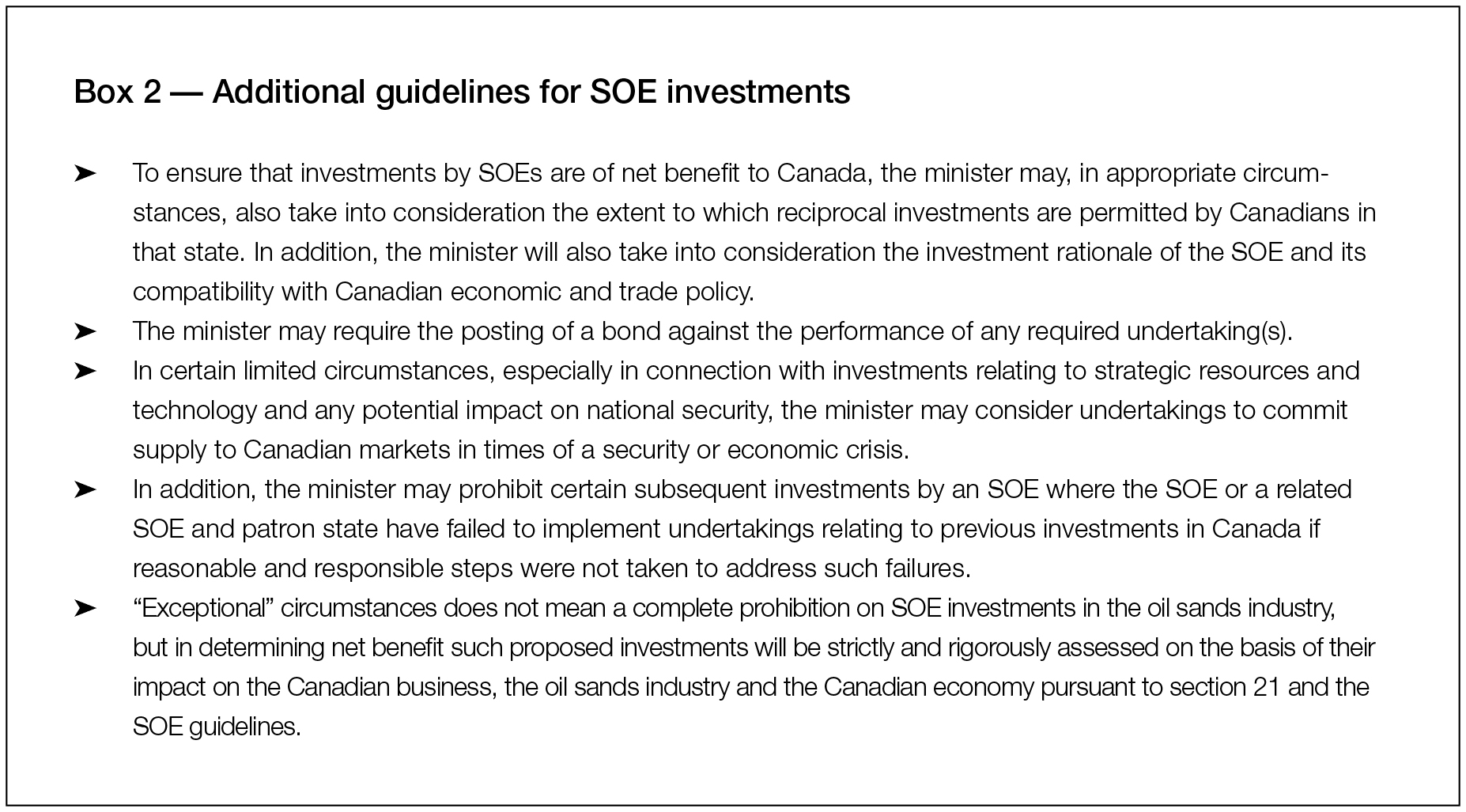

In December 2007, Industry Canada released guidelines to inform investors how a proposed SOE investment might attract additional scrutiny regarding governance and commercial motivations in determining “net benefit” (Industry Canada 2012d). Then, on December 7, 2012, concurrent with the approvals of the CNOOC and Petronas acquisitions, Industry Canada announced revised SOE guidelines (Canada 2012), which it described as necessary for the federal government to be clear and transparent in its oversight and application of the ICA following a significant increase of SOE investment activity since 2008 and the increasing interest of SOEs in the resource sector (Industry Canada 2012e). The trend, the federal government had decided, raised a range of issues about the open market orientation, productivity and industrial efficiency of the Canadian economy. As Prime Minister Stephen Harper said in an accompanying statement, “To be blunt, Canadians have not spent years reducing the ownership of sectors of the economy by our own governments, only to see them bought and controlled by foreign governments instead” (Harper 2012). Accordingly, the revisions expanded the definition of SOEs to include enterprises that are “influenced” (directly or indirectly) by a foreign government (in addition to “owned” or “controlled”); they also indicated that the current review threshold for SOE investments will be maintained – the threshold for private sector investors, in contrast, is set to rise to $1 billion (as described above) (Canada 2012).

According to the guidelines, SOE investors, in their business plans and undertakings, are expected to address whether “they are susceptible to state influence,” and they “will also need to demonstrate their strong commitment to transparent and commercial operations” (Industry Canada 2012a). In applying the net benefit test, the industry minister will examine the extent to which the SOE is owned, controlled or influenced by a foreign government. The minister will also examine the corporate governance and reporting structure of the SOE, including whether the foreign investor adheres to Canadian laws and practices (including adherence to free market principles), as well as to Canadian standards of corporate governance. These standards may include commitments to transparency and disclosure, independence of members of the board of directors, independence of audit committees and equitable treatment of shareholders. Furthermore, the “minister will assess the effect of the investment on the level and nature of economic activity in Canada, including the effect on employment, production and capital levels in Canada” (Industry Canada 2012a).

Regarding the commercial orientation of an SOE, the minister will assess whether the Canadian business to be acquired can continue to operate on a commercial basis with respect to the destination of its exports; place of processing; the participation of Canadians in its operations in Canada and elsewhere; support of ongoing innovation, research and development in Canada; the appropriate level of capital expenditures to maintain the Canadian business in a globally competitive position; and, particularly, the impact of the investment on productivity and industrial efficiency in Canada (Industry Canada 2012a). The guidelines also encourage specific undertakings to supplement the SOE’s plans for the Canadian business to help ensure that the acquisition would be of net benefit to Canada. These undertakings include appointing Canadians as independent members of the board of directors, employing Canadians in senior management positions, incorporating the business in Canada and listing shares of the acquiring company or the Canadian business being acquired on a Canadian stock exchange (Industry Canada 2012a).

An accompanying statement also announced that the industry minister would carefully monitor SOE transactions throughout the Canadian economy, particularly in regard to the degree of control or influence a SOE would likely exert on the Canadian business that is being acquired; the degree of control or influence a SOE would likely exert on the industry in which the Canadian business operates; and the extent to which a foreign state is likely to exercise control or influence over the SOE acquiring the Canadian business. Where due to a high concentration of ownership a small number of acquisitions of control by SOEs could undermine the private sector orientation of an industry, and consequently subject an industrial sector to an inordinate amount of foreign state influence, the Canadian government will act to safeguard Canadian interests. (Industry Canada 2012d)

Most significant, however, was the federal government’s announcement regarding future SOE involvement in the oil sands. Statements by both the Prime Minister and Industry Canada indicated that, due to the high level of “foreign state control” of oil sands development, going forward, the government would operate on the principle that an application for control of a Canadian oil sands business by an SOE will pass the net benefit test only on an “exceptional basis” (Industry Canada 2012d; Harper 2012). Industry Canada’s statement emphasized the global importance and “immense value” of the oil sands “to the future economic prosperity of all Canadians,” and highlighted Canada’s interest in maintaining a high concentration of private sector ownership in the oil sands, in contrast to the vast majority of global energy deposits, which are state controlled (Industry Canada 2012d). The department, however, gave no further details on the circumstances that would constitute an “exceptional basis”; an SOE’s unacceptable degree of “control or influence” over a Canadian business or relevant industry; or a foreign state’s unacceptable degree of control or influence over the SOE that intended to acquire the Canadian business.

Soon after, Natural Resources Minister Joe Oliver told reporters that the CNOOC-Nexen deal would not have been approved under the new policy (Tait and McCarthy 2012). Indeed, that acquisition – the largest foreign acquisition by a Chinese company – and the acquisition of Progress Energy Resources by Petronas merely followed a number of very large acquisitions of control of Canadian oil sands businesses by SOEs. These include Korea National Oil Corporation’s $4.1-billion acquisition of Harvest Energy Trust in 2009, PetroChina’s $1.9-billion acquisition of a 60 percent interest in two oil sands projects from Athabasca Oil Sands Corp. in 2009 and a $680-million acquisition of the remaining 40 percent interest in 2012, Sinopec’s US$4.65-billion acquisition of ConocoPhillips’ interest in Syncrude in 2010 and $2.2-billion acquisition of Daylight Energy in 2011, and CNOOC’s US$2.1-billion acquisition of OPTI Canada Inc. in 2011 (Feteke 2012; Lally et al. 2012; Cattaneo 2012a).

In making these changes, Prime Minister Harper reiterated that the Canadian government would continue to strongly encourage inward investment in Canada and that it would maintain an open, market-based approach to foreign investment (Harper 2012). The new policy does not affect non-SOE private sector investment in the oil sands, or minority investments, joint ventures or greenfield investments in any sector of the Canadian economy by or involving SOEs; nor does the “exceptional basis” policy currently apply to SOE investment in any sector of the Canadian economy other than the oil sands. Indeed, on December 13, 2012, less than a week after the policy announcement, Canadian energy company Encana Corporation announced a $2.18-billion deal with PetroChina to develop an Alberta natural gas project; since PetroChina’s share will be 49.9 percent, the investment is not subject to ICA review (Encana Corporation 2012).

Again, before commenting on the additional measures and guidelines Canada could offer in this area, it is helpful to review what other major players and trading partners are doing.

The United States provides for a review of investments by SOEs within the framework of its national security review under CFIUS. In 1992, Congress amended the Exon-Florio Amendment to require CFIUS to investigate proposed mergers, acquisitions or takeovers in cases where two criteria are met: first, where “the acquiror is controlled by or acting on behalf of a foreign government,” and, second, where “the acquisition results in control of a person engaged in interstate commerce in the United States that could affect the national security of the United States” (Byrd Amendment, section 837(a)).18 The 1992 amendments followed two transactions involving SOE parties in which the foreign state ownership of the acquirors raised more concern than a national security review would have otherwise (Mostaghel 2007, 597-600). The first was the November 1989 acquisition by the Chinese National Aero-Technology Import and Export Corporation (CATIC) of MAMCO, a US producer of metal parts for civil aircraft. President George H.W. Bush ordered CATIC to divest itself of its holdings in MAMCO, which caused investor uncertainty regarding the definition of “national security” and what would constitute a threat to national security (597). The second transaction was an attempted acquisition in 1992 of LTV Corporation’s Missile Division by French SOE Thomson-CSF. The further uncertainty regarding CFIUS review of that investment demonstrated a pressing need to clarify US legislation regarding the investment review of SOEs (599-601).

In 2007, FINSA was passed following the failed 2005 CNOOC bid for Unocal and the 2006 Dubai Ports World divestiture. A 2007 Senate Committee on Foreign Relations report supporting legislative reform (such as FINSA) stated that “over the last several decades, and in particular after September 11, 2001, it has become more challenging to balance a strong national security while remaining open to foreign direct investment from all regions of the world. It is vital to achieve the correct balance for many reasons” (United States 2007). FINSA requires an extended 45-day investigation if a CFIUS review reveals that an investment may result in the transfer of control of a US business to a foreign government or to an entity controlled by a foreign government (section 2(b)(1)(a)). Control is broadly defined as the direct or indirect power to determine, direct or decide important matters affecting an entity (Fagan 2009, 11). FINSA applies to government-controlled entities even when these operate as commercial entities (LaRussa and Raisner 2012, 117-18). CFIUS assesses the potential threat posed by the investor and the vulnerability of the US assets and business, and determines the balance between the two (Fagan 2009, 12). Additional nontransaction-specific factors must be considered, including the particular foreign country’s compliance with US policy on counterterrorism, non-proliferation and export control (West et al. 2007, 8).

In Australia, foreign investment is reviewed pursuant to the Foreign Acquisitions and Takeovers Act (FATA).19 In February 2008, the Australian government introduced into its Foreign Investment Policy special guidelines governing investments by foreign governments and their agencies (Swan 2008). All SOEs are required to notify the government and get prior approval before making a direct investment in Australia, regardless of the value of the investment (Australia 2012). The guidelines also state that proposed investments by SOEs will be assessed on the same basis as private sector proposals – namely, that of Australia’s national interest. Investments by SOEs, however, raise additional factors that also must be examined out of a concern that “investors with links to foreign governments may not operate solely in accordance with normal commercial considerations and may instead pursue broader political or strategic objectives that could be contrary to Australia’s national interest” (Australia 2008).

The Australian guidelines require notification for prior approval of a foreign SOE direct investment of any size (Australia 2008). A foreign SOE is statutorily defined as an entity in which a foreign government owns a 15 percent interest or more (FATA, section 5). The guidelines suggest that the review of such investments will cover whether (1) the investor’s operations are independent of the relevant foreign government; (2) the investor is subject to and adheres to the law and observes common standards of business behaviour; (3) the investment may hinder competition or lead to undue concentration or control in the industry or sectors concerned; (4) the investment may have an impact on Australian government revenue or other policies (such as the environment); (5) the investment may have an impact on Australia’s national security; and (6) the investment may have an impact on the operations and directions of an Australian business, as well as its contribution to the Australian economy and broader community (Australia 2012). Mitigating factors in determining that a proposal is not contrary to the national interest include (1) the existence of external partners or shareholders in the investment; (2) the level of nonassociated ownership interests; (3) the governance arrangements for the investment; (4) ongoing arrangements to protect Australian interests from noncommercial dealings; and (5) whether the target will be, or will remain, listed on the Australian Securities Exchange or another recognized exchange (Australia 2012).

In Russia, the Strategic Investments Law and the Foreign Investments Law20 contain specific rules applicable to foreign state-controlled investors. Under the Strategic Investments Law, foreign state-controlled investors are subject to lower review thresholds than ordinary foreign investors; any acquisition of more than 25 percent of the shares of a strategic company, or the right to block the decisions of a strategic company, must be cleared in advance (Polonsky and Pozdnyakova 2012, 86). Foreign state-controlled investors are also not permitted to obtain “control” over strategic companies – that is, those carrying on business in any of 42 strategically significant areas, including defence and natural resources (Syrbe, Pavlovich and Nogovitsyna 2012, 3). “Control” is defined to include having more than 50 percent of the voting shares; having the right to appoint a sole executive officer or more than 50 percent of the management body; having the right to appoint more than 50 percent of the board; or being entitled to make decisions on behalf of the company. Under the Foreign Investments Law, acquisition by a foreign state-controlled investor of more than 25 percent of any company’s shares or the right to block any company’s decisions is also subject to a clearance requirement (Syrbe, Pavlovich and Nogovitsyna 2012, 3).

Although foreign investment filings are not disclosed to the public, the Strategic Investments Law restrictions were engaged in the Megafon case. Under a joint venture agreement, TeliaSonera and Altimo agreed to combine their shares in Turkcell and Megafon in a new corporation (Polonsky and Pozdnyakova 2012, 88; Syrbe, Pavlovich and Nogovitsyna 2012, 7). The arbitration court in Moscow held that the agreement violated the Strategic Investments Law. On appeal, the ruling was upheld, the court finding that TeliaSonera was controlled by foreign states (Sweden and Finland) and that the agreement was therefore void because it would have permitted a foreign state-controlled investor to establish control over a strategic entity (Syrbe, Pavlovich and Nogovitsyna 2012, 7).

Canada and Australia are close comparative examples of countries that have moved to formalize their policies on SOEs. As both countries explicitly state, these policies reflect each economy’s strong natural resource base and attractiveness to SOE investment, and the two countries’ efforts to ensure transparency and guidance and to remain welcoming and open to foreign investment (Australia 2012; Industry Canada 2012a).

In comparison with other players, it would appear that Canada has transparent, clear and measured guidance. However, there are improvements that can be made and, in the following section, we propose a series of changes to the ICA, including several recommendations that could be used to further refine the SOE guidelines. Recognizing that SOEs are an increasingly significant presence in global capital markets, we believe these changes are necessary to help assuage Canadians’ concerns regarding SOE investments and to prevent a backlash against SOE investments.

While the Financial Times editorial cited in the epigraph focuses on Canada, there are similar general trends toward stronger enforcement in other countries.

Criticism of the ICA regarding a lack of certainty and transparency in the review process as well as charges of the review’s vulnerability to politicization is mirrored in other jurisdictions. A variety of foreign investment review systems are used throughout the world, authorizing national governments to block foreign acquisitions. Our survey results reveal that this authority attracts strong criticism from various quarters whenever exercised (see appendix B for a comparison of foreign investment review systems).

In 2011, for example, the Australian government rejected the proposed A$8.4-billion acquisition of the Australian Securities Exchange by Singapore-based Singapore Exchange Ltd. on the grounds that the transaction was not in Australia’s national interest because it ran counter to the objectives of maintaining a strong and stable financial system and building Australia as a global financial services leader in Asia (Swan 2011).

In 2006 a bipartisan majority in the United States Congress effectively pressured United Arab Emirates-based Dubai Ports World to divest the US port operations it had recently acquired from P&O Steam Navigation Co., despite previous CFIUS approval (Mostaghel 2007, 613-14). President George W. Bush publicly stated that the transaction posed no national security concerns and that “it would send a terrible signal to friends and allies not to let this transaction go through,” and he threatened a potential veto (“Bush Threatens Veto in Ports Row” 2006).

In recent years, CFIUS national security reviews have become more frequent. Only 25 such investigations were triggered between the enactment of the Exon-Florio Amendment in 1988 and the 2007 amendments, but there were 40 CFIUS investigations in 2011 alone (United States 2011) – a decade into the post-9/11 era. Some proposed investments did not pass the review. In 2009, CFIUS blocked the acquisition of a 51 percent stake in a Nevada gold mining corporation by Northwest Nonferrous, a Chinese SOE, because some of the properties owned by the target were close to an Air Force base (Corr, Erb and Burke 2010). In 2011, CFIUS blocked Huawei Technologies Co., a Chinese company, from purchasing US$2 million in assets from a US company because of Huawei’s ties to the Chinese military (Ikenson 2011). In 2012, President Barack Obama ordered the China-based Ralls Corporation to divest four small wind farm projects that were located too close to a US Navy weapons systems training facility in Oregon (Forden 2012).

In France, Prime Minister Dominique de Villepin told a news conference in 2005 that he had assured French yogurt company Danone that the French government would support Danone in fending off unwanted suitors: “A group like Danone is obviously one of our industrial treasures and we will of course defend the interests of France” (Fuller 2005). The statement came amid market rumours that Pepsico Inc. was planning to bid for Danone (Matlack 2005). The French government had identified 11 strategic sectors in which a foreign investment would be subject to review to determine its potential harm to French public order, public security or national defence interests.21 These sectors include casinos, companies involved in developing pathogens or toxic substances and companies involved in developing military technology. Additionally, the French government has taken active steps to protect strategic industries, forming a US$25-billion state investment fund to protect strategic industrial assets (Bennhold 2008). The fund is managed and controlled by the Caisse des Dépôts et Consignations, of which the French government owns a 49 percent interest (Bennhold 2008).

In the United Kingdom, the a 35-billion merger of British defence company BAE Systems and European Aeronautic Defence & Space Co. (EADS) was withdrawn in October 2012, reportedly because of the German government’s opposition to the transaction and the potential resulting loss of German jobs (Pickard, Jones and Wiesmann 2012). Days before the withdrawal announcement, UK Defence Secretary Philip Hammond also publicly announced that his government would not support the proposed transaction unless the French and German governments were limited in the potential interest they could acquire in the combined entity (Pickard 2012). The French government maintains a 15 percent interest in EADS and the German government retains indirect control through its shareholdings in Daimler AG (Michaels 2012). The UK government, meanwhile, holds a golden share in BAE Systems, which provides it effective rights over the corporation, including the right to block the merger (USGAO 2008, 102).

Another example comes from Israel, where, in November 2012, the government asked Canada’s Potash Corp. to explain how its proposed US$13.5-billion acquisition of Israel Chemicals (ICL) – in which the Israeli government holds a golden share – would secure Israel’s interests (Jordan 2012; the issue was unresolved at time of writing).