Canadian Policy Prescriptions for Dutch Disease

Robin Boadway, Serge Coulombe and Jean-François Tremblay

In recent years, the need for tax cuts has risen to the top of the public policy and political agendas. Of the many proposals put forward by political parties of all stripes, the flat and dual tax plans proposed by the Canadian Alliance stand out as the most striking proposals to change the federal tax system. This study assesses these two personal income tax plans in detail and uses them as a springboard for a broader analysis of the requisites to improve taxation policy in Canada.

In reviewing the ensemble of initiatives that make up the flat and dual tax plans, the study notes the surprising degree of commonality among the Alliance, Liberal, and Conservative tax proposals – although the relative emphases on specific measures and speeds of implementation vary. But while there is some agreement on the goals for reform, and even on specific instruments to be used to achieve these goals, there are important distinctions to be made about the tax policy choices now being put to the electorate. The most distinctive part of the original Alliance scheme was its proposed single tax rate for all income levels. This flat tax plan was later shifted to a transitional dual rate tax – which brought the Alliance tax package closer to the mainstream of Canadian tax policy discourse – but it nevertheless makes explicit choices about how the tax system should treat individuals at various levels of income and in various family structures. The changes introduced in the Liberal mini-budget of October 2000 (assessed in an addendum to the paper) also attempt to address some of the important needs for improved tax policy, but in a very different way than would a Canadian Alliance government. All of these policy options are assessed using three key criteria for evaluating a tax system: equity, simplicity, and efficiency. The platforms are then compared and contrasted with a “model” tax plan that, in the author’s opinion, would better respond not just to the need for tax reduction but also to the need for tax reform.

The equity and distributional dimensions of tax policies have been a central focus of recent public discourse. Many assertions have been made about the shortcomings of the Canadian personal income tax system vis-à-vis that of the US. The study subjects these assertions to a critical comparative analysis of the many elements that make up each tax system, with a focus on personal marginal tax rates. Several of the commonly held views are rejected based on the study’s findings, and much of the analysis turns on distinctions between tax rates at the federal versus the state or provincial levels. Top marginal tax rates including both levels of government are found to be much closer in the two countries than is commonly understood.

The progressivity of the flat and dual tax proposals is examined using numerical and micro-simulation analyses. The flat tax is found to carry significant shifts in the tax burden away from those at the lowest and particularly those at the highest incomes toward middle income earners, with the largest tax savings at very high income levels. The dual tax considerably moderates these shifts in tax burdens and almost maintains the distribution of tax burdens across families at various income levels, but it still would significantly reduce the progressivity of the overall Canadian tax system.

Another major dimension of equity – one that motivated the original flat tax plan – is the treatment of single-versus dual-earner families. The study examines the assumptions made to support various positions regarding this dimension of the equity issue, such as the view that single-and dual-earner families with the same total incomes should pay the same tax. Even if one accepts this proposition, the study concludes that this end could be achieved by introducing joint filing or income-splitting while retaining a progressive tax rate schedule, rather than adopting a single-rate tax and abandoning progressivity. On simplicity, the study finds that most of the claims made by proponents of a flat tax scheme are overstated and that the dual tax would further reduce any such benefits.

Another central focus of public discourse about tax policy relates to the changes that would be most conducive to efficiency and economic growth. In particular, reducing the tax burden on savings and capital incomes is deemed critical to enhanced economic performance. Methods of achieving this end include reduced taxation of capital gains, increased access to registered savings plans, and reduced rates of corporate income tax. Most of the parties’ tax proposals include changes in these areas, although the emphasis and speed of change vary. The Alliance plan includes a cut in the capital gains tax inclusion rate to 50 percent, which has been implemented in the 2000 mini-budget. Most of the parties’ plans for increased access to registered savings (both employer-and individual-based) have been relatively restrained, with the Alliance proposing little more than the government’s dilatory plans. In contrast, the model tax plan would provide large increases to registered savings by introducing tax-prepaid plans rather than raising the contribution limits to existing tax-deferred plans. Corporate income tax cuts also are found to warrant greater priority for faster cuts than those proposed by either the Alliance or the Liberal mini-budget. This shortcoming, as well as the failure of all parties to offer faster and deeper cuts to EI premium rates, reflect the political competition to put as much of the surplus funds as possible into highly visible cuts in personal tax rates.

Tax policy must be assessed in the broader context of fiscal policy, including debt repayment and program spending. The Alliance, Liberal, and other tax proposals involve large cuts in tax revenues and thus affect the ability to pay down public debt quickly, unless offset through restraint in the growth of federal program spending. The Alliance policy package includes larger and stronger debt repayment commitments than the Liberals, but the combined tax cuts and debt reduction proposed in the flat and dual tax plans raise questions about the potential distributional impacts of the real cuts in spending necessary to fulfill these commitments. Individuals at the lowest incomes will save little with Alliance tax cuts given that they pay little if any income tax at present. But these individuals are also most reliant on public services and income supports, so they could lose more through spending restraint than they gain through tax cuts.

Federal-provincial policy interactions are also important in assessing the various tax proposals. As the provinces face pressures to cut their personal tax rates, particularly to flatten their top rates following the lead of Alberta and Saskatchewan, maintaining relatively high marginal tax rates on upper earners in the federal tax will be needed to keep the overall Canadian tax system even moderately progressive. In contrast to the proposals currently being debated on the campaign trail, well-designed changes to the tax provisions for savings and capital income such as those presented in this paper’s “model” tax plan would better address issues of Canada-US competitiveness and economic growth while maintaining progressivity in the tax system.

With mounting budgetary surpluses and growing acceptance of the need to improve the economy’s performance, the need for tax cuts has risen to the top of the policy and political agendas in Canada. The most sweeping tax proposals have come from the Canadian Alliance, with a flat tax plan launched early in 2000 (under the Reform Party banner). Subsequently, the Progressive Conservatives also offered extensive plans for tax cuts in the report of their Task Force on Taxation. A federal budget ensued in February that made more modest pledges for tax cuts over the next five years.1 In October, the Alliance shifted its tax plan to a dual rate scheme. The federal government quickly followed with major tax cuts in a mini-budget, a response both to increasing surpluses and the political competition around tax policy. All these tax and related fiscal plans have raised basic questions about the best way to cut personal and business taxes and what tax reforms should complement the rate cuts. This study examines the key tax policy issues via a detailed evaluation of the Alliance proposals. Because the study was completed prior to the mini-budget’s tax changes, these could only be assessed briefly in an addendum. Whether the Liberal or Alliance tax plan continue to dominate the next Parliament, this study contributes to the broader debate around tax reform.

A 17 percent flat tax plan, modified to a transitional dual rate tax plan with the 17 percent rate still covering almost all taxpayers, is part of the Canadian Alliance economic platform.2 The party’s former finance critic described the plan as “the first major policy plank of our new political party.”3 This proposal is unquestionably bold, but is either form of tax good economic policy? Is it good social policy? Does the shift from a single rate to a dual rate tax fundamentally alter the original policy? Would the plan achieve its promised gains to economic efficiency, incentives, and growth at a cost that is acceptable in terms of equity or social justice? And are there superior alternatives that could deliver the same or greater economic benefits with less social costs? The flat and dual tax plans do engage important issues of economic and social policy, and the switch to a dual rate does bring the plan closer to the mainstream of Canadian tax policy discourse. This study proposes an alternative tax policy that would involve significant but lesser rate cuts, and more extensive base reforms, than the Alliance scheme.

The original Alliance plan was called a “single rate tax” rather than a flat tax. One of the “Frequently Asked Questions on Solution 17” on the party’s website asks, “Isn’t this just like the American flat tax idea?”4 The response is that, while a flat tax removes all deductions, this tax would retain all currently allowed deductions (and even expand some). The answer goes on to say that this tax plan would remain “progressive” in the sense that average tax rates would rise with individual incomes. However, all the American flat tax schemes also provide enlarged personal exemptions and therefore are progressive in the same way. Many of them also retain some other deductions, albeit reduced from existing levels. As there is nothing to differentiate the Canadian Alliance plan from many previous flat tax plans, we shall adopt the “flat tax” label for the Alliance proposal.5 The modified plan, which is called a “fair tax plan” in the party’s electoral platform, is a form more commonly called a dual rate tax. For brevity, it will be called a “dual tax” in this study. The flat tax plan also warrants close examination here, both because of its similarities to the dual tax plan and because it remains the stated goal of the Canadian Alliance tax policy.6

This study examines key issues needed to assess the economic and social policy implications of various tax reduction plans. It first compares Canadian and US personal tax rates in various dimensions; this permits an objective evaluation of commonly made assertions about Canadian tax rates and how they depart from US rates.7 Next, the issue of rate progressivity is investigated in the context of claims that have been made about the flat and dual tax plans. A related issue is the jurisdictional level at which progressive rate structures are economically appropriate. The relations between tax structures and equitable family taxation are examined next, followed by a review of the extent to which a flat or dual rate tax would simplify the personal tax system. The analysis then turns to the economic criteria of efficiency, incentives, and growth and to the nature of tax rates and base reforms that would best achieve these three objectives. Two additional issues are the implications of the flat and dual tax plans for tax revenues and public spending – each with its own efficiency and equity effects – and other tax changes that would best accompany such tax schemes. Finally, the study presents an alternative approach to the flat and dual tax plans, a comparison with the tax proposals of other political parties, and a summary of principal findings.8

In assessing these issues, one should begin with a clear view of the goals of taxation policy. A tax system must generate the revenues needed to finance the chosen public purposes. It should extract these funds in a manner that imposes the least deterrent to individual incentives, the efficient use of resources, and the economy’s growth. It should operate in as simple a manner as possible, minimizing the need for tax planning and leaving little room for tax avoidance, but giving due consideration to various equity goals. And its burdens should be spread across those at different income levels and in differing circumstances in a pattern that the public deems to be fair. These three key criteria for taxes – efficiency, simplicity, and equity – are as relevant to tax analysis today as they were when first formulated by Adam Smith over 200 years ago. Of course, conflicts frequently arise in achieving the various goals of tax policy, requiring delicate compromises among them.

To assess particular tax provisions or proposals using these criteria, one must use a mix of objective economic analysis and personal value judgments. Personal values are central in considering the desired distribution of the tax burden across income classes, while economic analysis is needed to assess the efficiency implications. Personal values are also critical when judging issues of tax equity across various groups, such as the different types of family units. And personal values will enter into determining how large total tax revenues and government spending should be; this involves balancing the value of private consumption against the value placed on publicly consumed goods and services. Nevertheless, economic analysis is useful both to show the true cost of raising tax revenues and to quantify the trade-offs among various goals and values. Personal values have a necessary role in choosing tax policies, but careful economic analysis can inform the range of tractable choices.

A major theme driving the various tax reduction proposals is that Canadian personal income taxes are no longer competitive with those in the US. The Minister of Finance has stressed that the government’s first priority for tax cuts is personal income taxes. Reasons commonly cited for this emphasis are the brain drain to the US, the need for productivity-enhancing investments, and the retention and generation of productive firms and jobs.9 There has also been widespread acceptance of several assertions about the relative status of Canadian and US income taxes:

This section compares the personal tax levels and MTRs for Canada and the US; the MTRs are particularly relevant for most incentive and efficiency effects of taxes.10 Each of the above assertions is examined using relevant evidence; some are fully or partially rejected. The comparisons are found to turn importantly on the division between federal and state/provincial income taxes. At the federal level, marginal tax rates rise to much higher levels in the US than in Canada. However, this is partially or fully offset by the much heavier reliance on income taxes by the Canadian provinces than by the American states. The relatively heavier income taxes at the federal vis-Ã -vis the state/provincial level in the US compared with Canada stem from a different balance in jurisdictional spending burdens in the two countries as well as the lack of an American national sales-type tax. In 1999, the federal government in the US accounted for 58 percent of all public expenditures; the figure in Canada was just 35 percent. If transfers to other levels of government are included, the figures become 67 percent for the US versus 43 percent for Canada.11 It is hardly surprising that US federal taxes in total must be relatively more burdensome than Canadian federal taxes, even if the total US tax burden is lower than that in Canada.

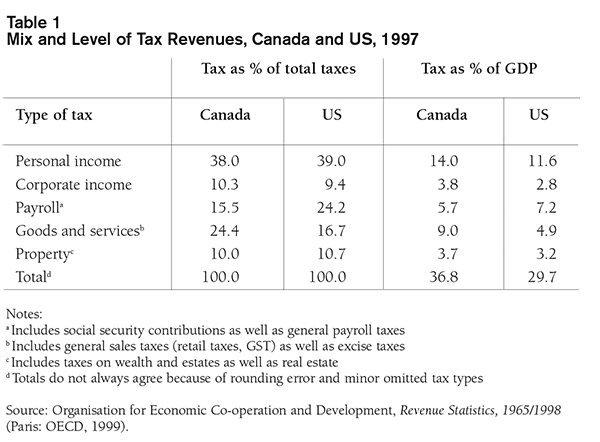

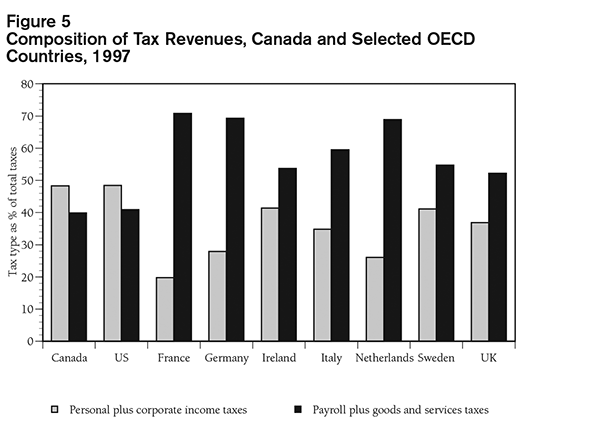

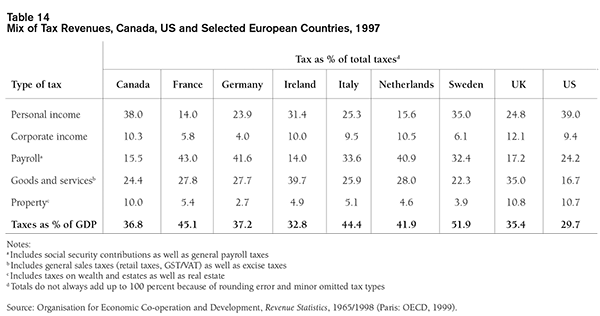

In terms of the mix of revenues across various taxes, Canada and the US rely on personal income taxes to almost the same degree. As shown in Table 1, the US obtains slightly more (39 percent) of its total revenues from this source than does Canada (38 percent).12 Despite this close similarity, the personal tax burden is still heavier in Canada than in the US because the total Canadian tax burden is larger relative to GDP, 37 percent versus 30 percent in the US. Hence, Canadian personal income taxes take 14.0 percent of GDP, compared with 11.6 percent for the US. This makes personal taxes on average 20 percent more burdensome for Canadians than for Americans. Canadian income taxes are the heaviest of the major economies (the G-7) but are exceeded by Nordic countries such as Denmark (25.9 percent of GDP), Finland (15.5 percent), and Sweden (18.2 percent) as well as Belgium (14.3 percent) and New Zealand (15.7 percent).13

Canada’s overall tax mix is also quite similar to that of the US in economically meaningful dimensions. Corporate income taxes make up 10.3 percent of total taxes in Canada versus 9.4 percent in the US. Thus personal plus corporate income taxes make up virtually the same 48 percent of total taxes in both countries. Two major types of taxes – payroll taxes and taxes on goods and services (retail sales taxes, excise taxes, and the GST) – affect only labour income and consumption, but not capital income or savings. Because these two types of taxes do not distort savings or investment decisions, or capital markets, they behave quite similarly in terms of their effects on the economy. Canada and the US each rely to almost the same degree on these taxes taken together, about 40 percent of total tax revenues. However, Canada is much more reliant on the sales-type taxes (since the US has no general sales tax at the federal level), whereas the US leans much more heavily on payroll taxes.

To begin the comparison between US and Canadian federal personal income taxes, let us consider their taxable threshold levels. This is the lowest level of income at which an individual or filer becomes taxable. In terms of competitive pressures (domestic or international) on the Canadian tax system, this issue is relatively unimportant. But in terms of social policy and distributional effects of the tax system, it is of considerable interest. To compare taxable thresholds of the US and Canada in a meaningful way, one needs to take the purchasing-power-parity (PPP) measure of US dollar figures. This is simply how much a US dollar would purchase in Canada in terms of an average person’s consumption bundle. By this measure, the Canadian dollar is sharply undervalued on the exchange markets, as its recent PPP value is 84 cents US per dollar or more than 25 percent above recent market exchange rates.14 Using this metric, taxable thresholds are lower in Canada than the US, and using market exchange rates would sharpen the differences. For example, for a non-aged single person, the Canadian threshold in 2000 is $7,365, whereas the US threshold at PPP is $8,571.15 To compare the effective taxable thresholds for families with children one would need to take into account various refundable credits in both countries – the Child Tax Benefit (CTB)16 and GST credits in Canada, and the Earned Income Tax Credits (EITC)17 (along with both personal exemptions and non-refundable tax credits for children) in the US. Considering all factors, most types of family units become taxable at lower incomes in Canada than the US.

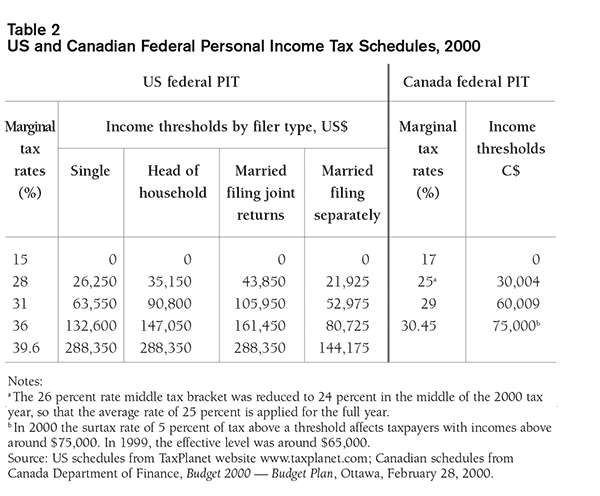

We next compare the income tax rate structures for the US and Canada at the federal level for the 2000 tax year (Table 2). The US offers four separate rate schedules by type of filer (singles, heads of household, and married couples filing either joint or separate returns).18 The bottom-bracket rate in the US is just 15 percent, but this jumps quickly to a second-bracket rate of 28 percent, which is near the top federal MTR in Canada of 29 percent (before surtax). The point at which the US federal MTR rises to 28 percent hinges on the filer type, ranging from US$26,250 for singles to US$43,850 for married joint filers. For married persons filing separate returns, the figure is even lower than for single filers, at just US$21,925, although it is higher at US$35,150 for household heads. Note that this jump between first-and second-bracket MTRs is a sharp 13 percentage points in the US federal tax, larger than the corresponding 8 percentage point jump in Canada for 2000.

The next US federal tax bracket has a MTR of 31 percent, which actually exceeds the highest federal MTR of 30.45 percent including surtax in Canada. This bracket arises for incomes above US$63,550 for singles and US$105,950 for married joint filers. In contrast, the top Canadian federal MTR (excluding the surtax) arises at just over $60,000 for a single adult and just over $120,000 for a married couple with equal incomes. Including the federal surtax, the top total MTR in Canada arises at about $75,000 for singles and $150,000 for married taxpayers (with equal incomes). The comparisons made between US and Canadian income tax rates often ignore the fact that married couples can file jointly in the US but must file separate returns in Canada (for incomes exceeding the taxable thresholds). Hence, the relevant income ranges for Canadian tax rates on married persons are much larger than the statutory tax brackets, as much as double in the case of partners with equal incomes. A proper comparison would be the US tax brackets for married persons filing separate returns; for such filers, the 28 percent rate bracket starts at just US$21,925, and the 31 percent rate starts at US$52,975 of individual income.

The top MTR in the Canadian federal income tax is 30.45 percent, while the US rates rise still further at very high income levels. The sweeping US Tax Reform Act of 1986 sharply reduced the top federal tax rate of 50 percent and collapsed the rate structure to just two brackets – 15 and 28 percent. A 31 percent rate bracket was added at higher incomes in a 1990 deficit-reduction budget compromise by a Democrat-controlled Congress and President George “Read My Lips – No More Taxes” Bush. As of 1992, the top 31 percent rate was applied for incomes above US$51,900 and US$86,500 for single and married joint filers, respectively. Two more brackets of 36 and 39.6 percent were added for still-higher incomes in President Clinton’s deficit-reduction package of 1993 (see Table 2 for the current bracket levels). Additionally, in 1993, the upper earnings limit for the Social Security medicare payroll tax was removed, adding another 1.45 and 2.9 percent to total top MTRs for employment and self-employed earnings, respectively. While it is often mentioned that top US MTRs arise only at much higher incomes than in Canada, this observation ignores the fact that these top MTRs at the federal level are also much higher than in Canada. As noted, US federal MTRs exceed the top Canadian federal MTRs at much lower, albeit upper-middle, income levels.

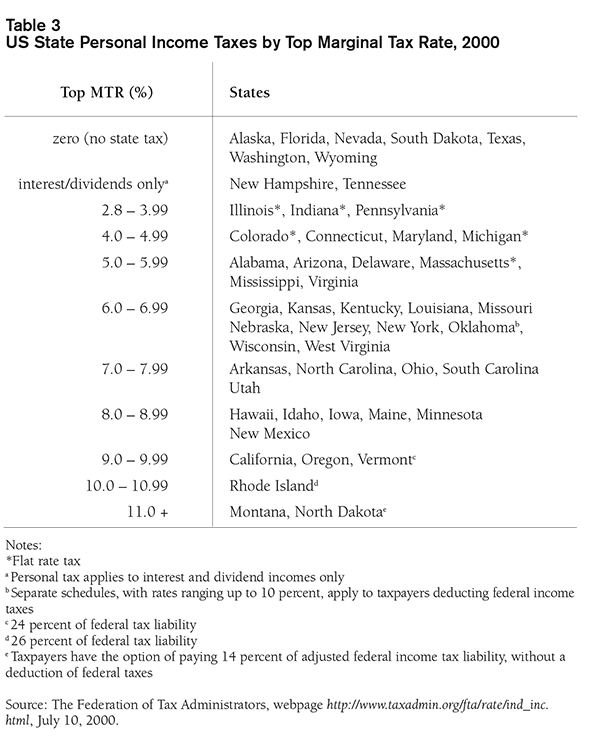

We now turn to comparative personal income tax rates at the American state and Canadian provincial levels. Table 3 shows the top MTRs for the 50 states; not shown in the table are the many cities and counties that also apply income or payroll-type taxes to employment earnings within their boundaries. Seven states do not apply a personal income tax (of which the only populous ones are Florida and Texas); two other states apply a tax only to interest and dividend incomes. The remaining 41 states have general income taxes with top MTRs that range from just 2.8 percent to over 11 percent. Six of the states apply a flat rate of tax above an exemption level, and all of these are among the lower-tax states. The rest of the taxing states employ progressive rate schedules, but without exception they apply their top MTRs at much lower incomes than the threshold used for the federal top MTR. The median top MTR for the states is in the 6 to 7 percent range. California is the most populous state with a high top MTR, at 9 percent.

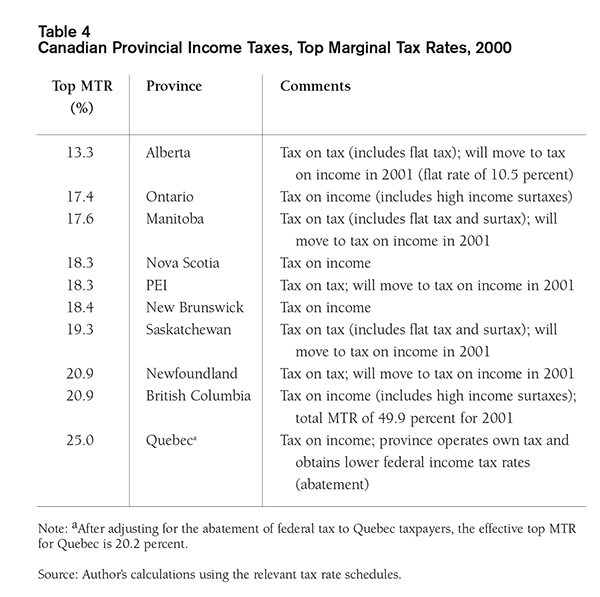

The top MTRs for each Canadian province appear in Table 4, with a range from 13.3 percent for Alberta to 20.9 percent for British Columbia and Newfoundland. The still-higher 25.0 percent for Quebec reflects reduced federal tax rates for taxpayers in that province as an offset for special spending arrangements. In 2001, Alberta will cut its top MTR further with the introduction of a flat tax at a 10.5 percent rate. Even at that rate, which will be the lowest top MTR of all the Canadian provinces, Alberta will just be on par with Rhode Island, Montana, and North Dakota – the three American states having the highest top MTRs. In general, Canadian provincial personal income taxes are much heavier than counterpart American state taxes, not only at the highest but at most income levels. Canadian provincial taxes have typically ranged from around 45 to 60 percent of the individual taxpayer’s federal income tax liability. With the switch from a “tax-on-tax” regime to a “tax-on-income” regime, where the province applies its own tax rate schedule to federally defined taxable income (except for Quebec), one might expect to see greater provincial variation in both top and lower MTRs. Several provinces have already moved to a tax-on-income system for 2000, with the rest to follow in 2001. Saskatchewan is using this opportunity to substantially cut its top MTR, from a current 19.3 percent to 15.0 percent by 2003 (on taxable incomes above $100,000).19

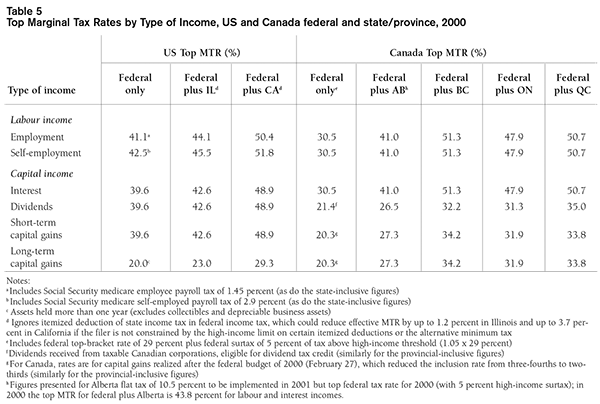

One can add together the top MTRs applied at the federal and state/provincial levels in each country to compare the overall top MTRs. Table 5 presents the results of such an exercise for representative low-and high-tax states and provinces, giving the top MTRs separately for major income types.20 The impact of various tax and benefit phase-out provisions (such as the EITC and phase-out of personal exemptions at high incomes in the US, and the CTB in Canada) is ignored in these figures. For any of the US states without an income tax, the federal-only figures are the relevant total top MTRs. Illinois is chosen to represent the states with low but positive income taxes; California for the states with relatively high income taxes. On the Canadian side, figures are presented for the four most populous provinces, Alberta, British Columbia, Ontario, and Quebec. The Alberta figures use the province’s 2001 flat tax regime to show the effects of this major change; all other figures in the table are for the 2000 tax year. The calculations of top MTRs reflect the tax provisions that apply to particular types of incomes – such as the dividend tax credit in Canada, payroll taxes for medicare on all labour earnings in the US, and special tax rates for capital gains in both countries.

As shown in Table 5, the top MTRs for even a given jurisdiction vary considerably across the income types. For the US federal tax, these rates range from 42.5 percent for self-employment income (including the Social Security medicare tax) to 20.0 percent for long-term capital gains.21 For the Canadian federal tax, these rates range from 30.5 percent for labour income to 20.3 percent for capital gains (both short-and long-term). Comparing US and Canadian top federal MTRs by type of income, the Canadian rates undercut the American rates substantially for all income types except long-term capital gains (which are just 0.3 percent higher in Canada).22 Alberta with its flat tax in 2001 will undercut even a low-tax state such as Illinois for top MTRs except on long-term capital gains, and it will even be on par with or below the rates in states without an income tax (see the “US federal only” column), again excepting long-term capital gains. Turning next to the high-tax jurisdictions, BC and Quebec are fully competitive with California in top MTRs with respect to labour incomes, a bit higher on interest incomes, much lower on dividends and short-term capital gains, and higher on long-term capital gains. If there is any issue involving Canada’s competitiveness with top MTRs in the US, it arises solely with respect to long-term capital gains.

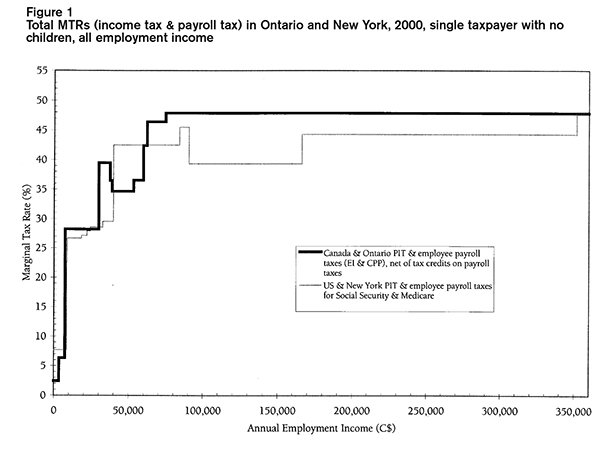

Of course, the overwhelming majority of taxpayers in both countries do not face the top MTR, so the pattern of tax rates across the full income spectrum is relevant when comparing their taxes. We next examine the pattern of MTRs by income level for the US and Canada by taking a large jurisdiction in each country with representative tax rates (New York and Ontario). Before looking at the resulting figures, we note several aspects of this comparison. Ontario has below-average tax rates at low and moderate incomes but applies sharp surtaxes beginning around $55,000, so its top provincial MTR is not atypical. For New York, we take only the state-level income tax and ignore the New York City tax, which applies up to an additional 3.83 percent rate. Like many other states, New York’s tax is quite flat, hitting its top MTR of 6.85 percent at income levels where individuals are still in the bottom bracket of the US federal income tax. American figures have been converted into Canadian dollars using the PPP exchange rate of 84 cents US per Canadian dollar; using recent market exchange rates would only accentuate the findings. These differences would also be increased by considering the more generous deductions and exclusions available to US taxfilers (mortgage interest, property taxes, state income taxes, tax-free state and municipal bond interest, and half of social security receipts above a threshold).23

All our examples take non-aged taxpayers with no children, to avoid the complicating effects on MTRs of various seniors’ and child-related tax credit and benefit provisions.24 The analysis assumes that all income is from employment earnings, the dominant source of income for almost all income groups among the non-aged. Hence, we also consider the impact of employee payroll taxes on total MTRs, with the offsetting tax credits for these payments in Canada; the US does not offer deductions or credits for employee payroll taxes. One reason for the surprisingly high total MTRs in the US at upper-middle incomes is that the high payroll tax rates apply up to US$76,200 of annual earnings (and over US$150,000 for two-earner couples). The analysis for two-earner couples assumes that total earnings are divided equally between the spouses; any differential division of earnings would yield results intermediate between the plotted one-earner and two-earner figures.

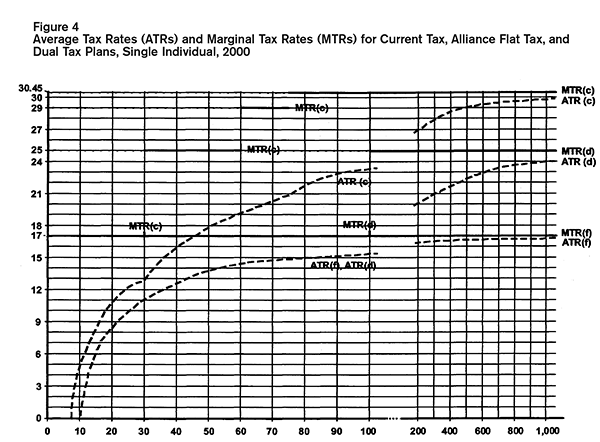

Figures 1 to 3 show the situation for single taxpayers, one-earner couples, and two-earner couples, respectively. As seen in Figure 1, single persons with incomes up to $60,000 face MTRs that are sometimes higher and sometimes lower in Canada than the US. The falling pattern of the Canadian MTRs in the upper $30,000 range reflects the earnings ceilings for Employment Insurance (EI) and Canada Pension Plan (CPP) payroll taxes. From the low $60,000s to higher earnings, the Canadian MTR is consistently, and often significantly, above the counterpart US rates. The only exception is for incomes facing the top US MTR, above roughly $350,000, where the two rates are virtually identical – 47.86 percent in Ontario and 47.90 percent in New York.

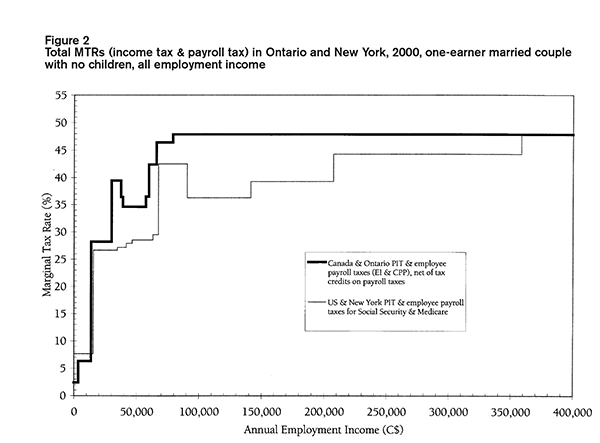

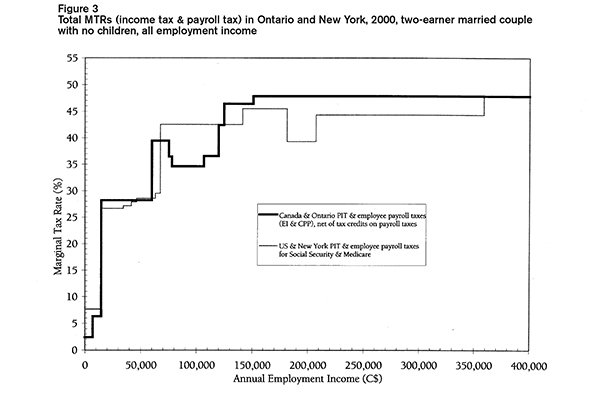

The one-earner married couple, in Figure 2, faces MTRs in Canada that are consistently and often significantly above MTRs in the US for all incomes from the taxable threshold (about $13,700) up to the highest incomes except where the US attains its top MTR equal to the top MTR in Canada. Figure 3 presents the corresponding patterns for two-earner married couples in the two countries; these results differ dramatically from those for the one-earner married couples. The MTRs in this case are very competitive with those in the US for incomes up to the low $60,000s. For all incomes between the upper $60,000s and $120,000, the MTRs are now significantly lower in Canada than the US; this is the income range where each spouse earns between $30,000 and $60,000. For total income above $120,000, this pattern reverses, with the Canadian two-earner couples facing the higher MTRs. The contrast of this pattern vis-Ã -vis the one-earner married couple stems from three factors: (1) in Canada, the tax brackets are in effect twice as wide as those for a single filer, since each spouse files a separate return; (2) in the US, married partners file a joint return but the tax brackets are not fully twice as wide as those for singles to account for scale economies;25 and (3) with two earners, the relatively high US payroll taxes apply to twice as much total earnings, with the full 7.65 percent rate striking more than US$150,000.

Findings about comparative Canadian and US personal income taxes can be summarized as follows:

If Canada wished to compete with the US on personal income taxes – for reasons that should be clearly articulated – there are thus four basic areas that would require change: (1) The income thresholds at which the middle and top brackets apply for federal tax need to be substantially increased, particularly for the top bracket. (2) The tax rates applied in the federal income tax do not present problems, especially after the surtax is fully removed and the middle-bracket rate is reduced further. However, the surtax rates applied to high incomes in some provinces, such as British Columbia and Ontario, could be moderated or removed if they wish to be more competitive with no-tax and low-income-tax US states. Saskatchewan will be following this path, and others may follow. (3) The effective tax rates on long-term capital gains could be reduced further by trimming the inclusion rate to half. (4) While Canada would be well advised not to follow the US with many tax deductions and exclusions,26 the American tax provisions for retirement savings (including both the levels and forms of tax-recognized savings) warrant scrutiny. These issues are pursued in later sections of the study.

Equity or fairness has two key dimensions for tax policy – vertical equity and horizontal equity. Vertical equity is a measure of how the overall tax burden is spread across income classes, or how steeply tax burdens rise with income levels. Horizontal equity is a measure of whether individuals or households with the same level of income or “ability to pay” are taxed equally. The flat and dual tax plans raise fundamental questions of both vertical and horizontal equity. This section examines the vertical equity aspects of each approach, while horizontal equity will be discussed in the next section, which examines tax treatment of the family. We begin by assessing tax progressivity under the flat tax and then examine the extent to which applying the dual tax rather than a flat tax would moderate the distributional outcomes. Vertical equity is commonly identified with “progressivity,” which means how quickly the tax burden rises with the income of the taxpaying unit. A tax is said to be progressive if taxes rise proportionally faster than income; that is, the average tax rate (ATR) or tax as a percentage of income rises with income. A tax is regressive if taxes rise proportionally slower than income, which is measured by an ATR that declines with higher incomes. And a tax is proportional if the tax is a constant percentage of income across income levels, indicated by a constant ATR. The ATR pattern of a tax is most relevant for vertical equity, whereas the level and pattern of MTRs are most relevant for the incentive and efficiency effects of the tax. Almost all major types of taxes except for personal and corporate income taxes are regressive in practice. Hence, if one desires some progressivity in the overall tax system or at least to mute the regressive effects of other taxes, the personal tax rates must be structured to provide adequate progressivity. At issue is not only whether the personal tax is progressive, but exactly how progressive it is.

Proponents of the Alliance flat tax maintain that their plan would be progressive even though it offers only a single tax rate above its expanded exemption levels. This approach departs from the typical personal tax rate schedule that consists of a series of successively higher MTRs as income increases. A flat tax does achieve somewhat progressive average tax rates through its basic exemption for taxfilers. This exemption relieves from tax a fixed amount of income, so that the flat or constant MTR on incomes above that threshold strikes a larger proportion of total income as income rises. Hence, the flat tax does produce a pattern of rising average tax rates as incomes rise, which satisfies the most common definition of a progressive tax. This point is made clearly in numerical examples offered by the Alliance in promoting their tax plan. Nevertheless, this type of tax rate structure offers much less scope for rate progressivity than a “progressive” tax rate schedule – one that applies a sequence of increasing MTRs for incomes at higher levels. In fact, the flat rate structure has average tax rates that rise quickly with income but level off as it approaches the statutory single tax rate and do not rise much more even at very high incomes.

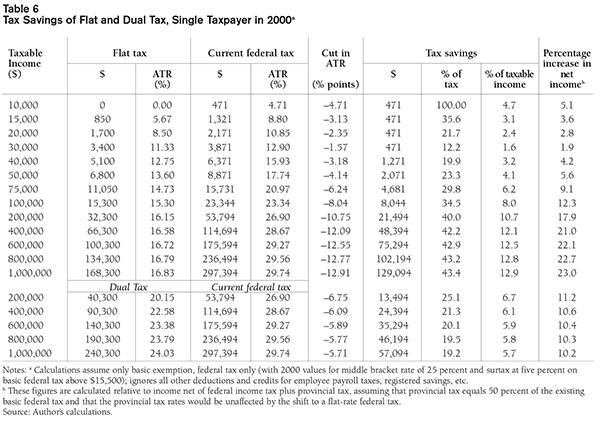

Table 6 illustrates the pattern of average tax rates (ATRs) for the flat tax plan and for the federal income tax in 2000; for now we ignore the bottom panel showing the dual tax. The examples used to examine progressivity in this section are based on a simplified case involving a single taxpayer with no dependants and disregarding any deductions or credits besides the basic credit allowed a taxfiler.27 The proposed flat tax plan would leave in place all other existing tax deduction and credit provisions, although it would increase the dollar and percent ceilings for tax-deductible registered savings. The general comparative properties of the two kinds of tax structure would be little changed by taking more detailed realistic assumptions, although of course the exact numbers would differ. Under the flat tax plan, the ATR rises quickly with income and hits 15.3 percent at a taxable income of $100,000, not much below its maximum value of 17 percent. In fact, a person with $1 million of income faces an ATR that is just 1.5 percentage points more than one with $100,000. In contrast, the existing federal income tax retains substantial progressivity even at very high incomes, with the ATR rising by more than 6.0 percentage points between the $100,000 and $1 million income levels.

Figure 4 shows how the average tax rate quickly levels out at incomes above $100,000 with the flat tax [ATR(f)], in contrast to its continuing rise even at higher incomes under the current federal income tax [ATR(c)]. The successively higher levels of marginal tax rates under the current tax [MTR(c)] act to continually pull up the ATRs at higher incomes. For the flat tax, the marginal tax rate [MTR(f)] is a uniform 17 percent across all income levels. For the current federal tax, MTR(c) is a series of segments: 17 percent up to $30,000; 25 percent from $30,000 to $60,000; 29 percent above $60,000; and an additional 1.45 percentage points for the surtax above $75,000. The gap between ATRs under the flat tax and the current system narrows for incomes as they rise up to $30,000 but widens continually and substantially for all higher incomes.

Material promoting the Alliance’s flat tax stresses the progressive nature of the plan. One of its “Frequently Asked Questions” asks, “Isn’t this [plan] regressive? Aren’t you removing the progressive nature of the tax code?” The reply states, “No. A single rate tax system is truly progressive because it taxes incomes according to ability to pay while completely removing the genuinely poor among us from the tax rolls.” It then proceeds to offer an example of a single parent with one child and a salary of $24,000, which obtains a $10,000 personal deduction plus a $10,000 spousal-equivalent deduction for the child as well as the $3,000 child deduction. Taxable income for that household would be $24,000 – $23,000 or $1,000, which would incur just $170 of federal income tax. It then notes that someone with $1 million of taxable income would pay $170,000 under the flat tax. It concludes, “The millionaire’s income is 40 times that of the single parent but they pay 1,000 times more tax. That’s progressive.”

The difficulties with this notion of progressivity can be illustrated using Table 6 (albeit for a single taxpayer with no dependants). The table presents the tax savings that would result from shifting to the flat tax from the current tax for individuals with income ranging from $10,000 to $1 million.28 At low incomes, below the $30,004 threshold for the current middle-rate bracket, the savings are a flat $471 regardless of income. This reflects the increased basic exemption under the flat tax ($10,000 – $7,231 = $2,769) multiplied by the existing bottom-bracket rate of 17 percent. The tax savings rise for those with higher incomes, as they benefit from the same $471 and also from the reduction in their tax rates to the single 17 percent rate on incomes above the $30,004. At middle incomes, the tax savings become fairly large, but at very high incomes they are truly massive. The tax savings are shown by income level as a percentage of original tax saved and as a percentage of taxable income. Both these measures give the appearance of a progressive pattern of rate cuts – tax savings that decline as a percentage with income – but only for the lowest incomes up to $30,000.29 For higher incomes, taxes saved as a percentage of either taxes or of income rise steadily and sharply with income level. At $30,000, the tax savings are 12.2 percent of tax and 1.6 percent of income, but at $100,000 these figures rise to 34.5 and 8.0 percent, respectively. The last column shows the percentage increase in disposable income (assuming a provincial tax at 50 percent of the basic federal tax) from the tax shift. This increase is 5.1 percent at $10,000, declines to 1.9 percent at $30,000, and then rises to 12.3 percent at $100,000 and 23.0 percent at $1 million. It is notable that the smallest proportionate rise in net income occurs at close to the median taxpayer income.

One can use the results in Table 6 to make comparisons similar to those made in the Alliance’s information material. For example, comparing single persons at $40,000 and $1 million, the tax savings from the flat tax are over 100 times as large for the latter ($129,094 compared to $1,271) although the income is only 25 times as large. This presents a very different picture of the “progressivity” of the flat tax plan, one that reveals that this kind of approach tends to produce greater tax cuts for those at upper incomes relative to those at middle incomes. The Alliance’s “Frequently Asked Questions” include the question, “Doesn’t a single rate tax hurt the middle class?” with its reply, “No! A 17 percent single rate will provide significant tax relief to the middle class…Our plan dramatically reduces the tax burden for all taxpayers – including the middle class.” However, retaining progressivity of MTRs above middle incomes would allow for considerably larger tax cuts for the middle class, with less of the total tax savings going to those at very high incomes. Another “FAQ” asks, “Don’t the rich benefit the most under your plan?” The reply is, “We’re not going to apologize for a plan that lowers taxes for all low, middle and upper income Canadians.” While the statement is factually correct, it excludes alternative ways of dividing the pie that do not unduly favour upper-income Canadians.

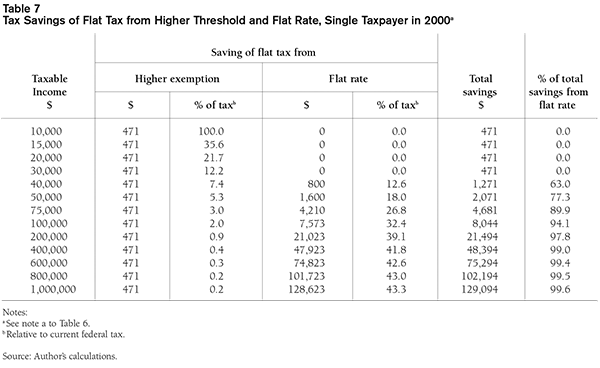

One way to understand the distributional impact of the Alliance flat tax is to decompose the tax savings into its two principal components – the flattening of the tax schedule to a single rate and the large increase in the deductions for filers (and dependent spouse and children). Table 7 shows the results of this decomposition, again using the simplified example of the single taxpayer. The tax savings from the increased basic deduction are a uniform $471 across all income levels, even the highest.30 At $10,000 of taxable income, this represents a 100 percent tax reduction, but this percentage declines steadily and sharply with higher incomes; at $100,000, it is just a 2.0 percent tax cut. Clearly, this component of the flat tax is most important in reducing taxes for individuals at very low incomes. In contrast, the tax savings from the flat tax rate are zero for incomes below the current $30,004 threshold for the middle-rate bracket, but they rise steadily and sharply with higher incomes. At $50,000, the savings are 18.0 percent of taxes; at $100,000, 32.4 percent of taxes; and at $1 million, 43.3 percent of taxes. The amount of tax savings from the flat rates are much greater than the $471 at middle incomes and become massive at high incomes.

As shown in the last column of Table 7, most of the action from the flat tax plan for incomes around $40,000 comes from the flat rate and not the enlarged deductions. At $75,000 incomes, 89.9 percent of the total tax savings for a single person stems from the flat rate. The revenue costs reported by the Alliance for its original flat tax plan confirm that the flat tax rate is a larger part of the package than the increased deductions.31 It puts the annual revenue costs (or tax savings) of the various components as follows: increase in the exemption for filers and spousal/equivalent status, $8.26 billion; introduction of a new $3,000 deduction for children under age 16, $2.37 billion; and cutting all higher tax rates to the flat 17 percent, $17.16 billion. The material also reports that the flat tax would remove 1.4 million low-income Canadians from the tax rolls.32 This result, however, is the consequence solely of the increased exemptions, and it could be achieved without any change in the federal tax rate schedule if that were desired.

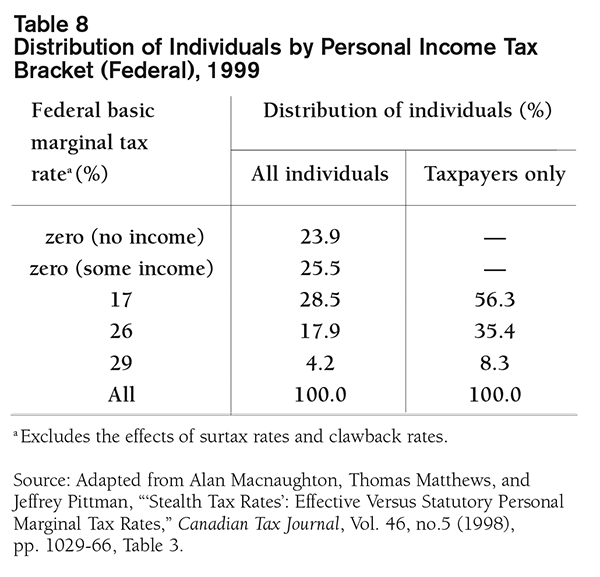

A look at the distribution of taxfilers across the three existing federal tax brackets reveals how the benefits of a single tax rate would be disbursed. Table 8 shows this distribution for all individuals, including non-taxable persons and those claimed on others’ tax returns. Nearly half of all individuals (49 percent) face a zero MTR on any incremental income; only four percent fall into the top bracket. Restricting the count to those who face a positive MTR, as reported in the table’s last column, also shows that taxpayers are concentrated in the lowest tax bracket. More than half (56 percent) of all persons facing a positive federal tax rate are in the bottom bracket of 17 percent. Since the flat tax would reduce all federal MTRs to 17 percent, this group of more than half of all taxpayers (and nearly 78 percent of all individuals) would gain nothing from the reduction in tax rates to a single rate. The middle tax bracket constitutes just over one-third (35 percent) of all individuals subject to federal tax; they will get a modest break from cutting the rate to 17 percent. The largest cut in tax rates from the flattening of rates will go to those now in the top bracket, who represent just eight percent or about one out of 12 taxpayers.

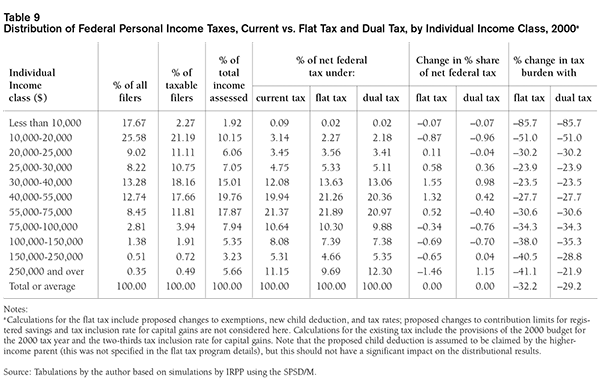

The impact of the flat tax plan on various income groups can be examined with the aid of Tables 9 and 10, which show estimates for individuals and family units, respectively. For now we ignore the columns with figures for the dual tax.33 The results presented here do not take into account the Alliance proposals to raise the contribution limits for registered savings plans and to cut the tax inclusion rate for capital gains. As will be explained later, the higher contribution limits would be of principal benefit only for persons with earnings above $75,000 per year, so that the distributional results would only be exacerbated by including this provision. The reduced tax inclusion rate for capital gains would be of disproportional benefit to persons and households at the highest incomes, where this source of income is highly concentrated. But based on evidence from other countries, the lower tax rate would increase the rate at which capital gains were realized, which would have an offsetting impact on the share of taxes paid.34

If the main features of the flat tax plan were fully implemented in 2000, average individual (or family) federal income taxes payable would fall by 32.2 percent. However, as shown in the next-to-last columns of Tables 9 and 10, these percentage tax savings vary by income level with an overall U-shaped pattern. The percentage cuts are greater than average only for individuals with incomes below $20,000 and above $75,000 and for families with total family incomes below $25,000 and above $140,000. As a result, the relative shares of the total income tax burden are increased under the flat tax for those with moderate to upper-middle incomes – namely, for individuals with incomes between $20,000 and $75,000 and for families with total family incomes between $25,000 and $140,000.35 While the very lowest income groups enjoy the largest percentage cuts in their federal taxes, the percentage cut in the share of total tax revenues is much larger for the much smaller group of very high-income taxpayers. Individuals with incomes below $20,000 (23.5 percent of taxable filers) have their total share of federal tax cut by 0.94 percentage points, but individuals with incomes above $75,000 (just 7.1 percent of taxable filers) have their share cut by 3.14 percentage points. Although the tabulated shifts in tax shares may appear to be small, they are quite significant in relative terms. For example, the 1.46 percentage cut in the tax share of individuals with incomes over $250,000 is 13 percent of its existing 11.15 percent share.

Moreover, these figures mask the massive amount of tax savings from the flat tax that would be provided to the small numbers at higher incomes. For families with incomes above $225,000, which is just 0.9 percent of all families, the aggregate tax savings would be $4.7 billion per year – nearly six percent of the $79 billion in total federal income taxes or 19 percent of the $25 billion in tax cuts under the flat tax plan. At incomes above $1 million, our estimated total tax savings would be in the order of $1 billion per year. Given that there are only about 4,600 individuals or 5,600 families in this income range, the average annual saving per unit would be about $200,000. The tables also indicate why the adoption of a flat tax would entail so much revenue loss even though there are relatively few people at higher incomes. For example, one finds there are just over 9 percent of all families with incomes above $100,000. Yet they receive in aggregate 31 percent of all income assessed under the tax and they pay over 44 percent of all federal income taxes under the current progressive rate structure. And for individuals at very low incomes the aggregate dollar savings are very small despite their large percentage cut in taxes, because they pay little tax at present. For individuals with incomes below $10,000, who pay just $68 million under the current income tax, the 85.7 percent tax savings from the flat tax amounts to only $58 million.

The Alliance’s transitional shift in policy from a flat tax to a dual tax was presented as driven by cost considerations and increased priorities given to federal spending and debt reduction. Most political observers believe that the shift was dictated instead by concern about the political vulnerability of a proposal with tax cuts so heavily weighted to very high income groups.36 Thus a key question is the extent to which the shift to a dual tax would moderate the distributional effects that have been shown for the flat tax. The only significant difference between the flat and dual tax plans is that a second, higher MTR of 25 percent would apply to individual taxable incomes above $100,000. Therefore, for couples with equally divided incomes, the higher tax rate would not bite until family incomes reached $200,000. Based on our simulations, it is estimated that the shift from a flat tax to a dual tax would, if each were applied in 2000, raise net federal tax revenues by just about $2.4 billion, or only three percent of current total federal income taxes.

The bottom panel of Table 6 repeats for the dual tax the earlier analysis of impacts on average tax rates by income. All the results for the dual tax are the same for incomes up to $100,000, so that the upper panel still applies in that range. It can be seen that the dual rate does substantially mute the cuts in ATRs at very high incomes relative to the flat tax. Instead of cuts to ATRs exceeding 12 percentage points for incomes of $400,000 to $1 million, these are reduced by more than half to cuts of 6 percentage points or less. Nevertheless, these cuts are still larger than those for any of the income levels below $75,000. Figure 4 shows the pattern of ATRs for a dual tax [ATR(d)] alongside those for the flat tax and the current federal tax. In dollar terms per individual, the dual tax also cuts the savings, relative to the flat tax, by more than one-third at the $200,000 income level and by well over half at the highest income levels shown. Tax savings under the dual tax as a percent of tax paid under the current federal tax show a declining pattern at the higher incomes, instead of their ever-increasing pattern with the flat tax. Still, these figures at the highest incomes exceed those for individuals with incomes of just $30,000. Tax savings for high earners both as a percentage of their income and the implied percentage increase in their disposable income are dampened by about half when using a dual rate rather than a flat tax. But both of these types of measures still show much larger percentage gains for those at very high incomes than for individuals with incomes of $50,000 or lower – quite apart from the vastly larger dollar savings.

Table 9 shows the same kinds of figures for distribution of the tax burden for the dual tax as were previously examined for the flat tax for individuals. The dual tax offers a total tax reduction of 29.2 percent. Since the flat tax reduced the net federal income tax revenues by 32.2 percent, this is about a one-tenth smaller total tax cut overall. All of this curtailed tax reduction is at the expense of individuals with incomes above $100,000 and families containing any such individuals. The share of net federal tax for income groups up to $150,000 is slightly smaller under the dual tax than under the flat tax. This situation reverses for higher incomes, with the tax share larger under the dual tax than under the flat tax. For individual filers, the tax share for incomes in the $150,000–250,000 range is almost the same under the dual tax as the current tax. For individuals with incomes above $250,000, the tax share is more than a full percentage point higher (12.30 versus 11.15 percent) under the dual tax vis-Ã -vis the current tax. Hence, the dual tax does succeed at the top incomes in preventing an adverse shift in the total tax burden. Nevertheless, in the middle-income range where there are far more taxpayers than at the top, the dual tax still creates an adverse shift in shares of the tax burden for individuals. Those with incomes between $25,000 and $55,000 bear a larger share of the total taxes with the dual tax than with the current tax. The dual tax creates a peculiar shift in tax shares: very low-income groups gain (with smaller shares), middle-income groups lose, upper-middle-income groups gain (by more than those at very low incomes), and very high-income groups lose. This result is unlike the previous finding for the flat tax, where all the “share losers” were found in the moderate-to middle-income group.

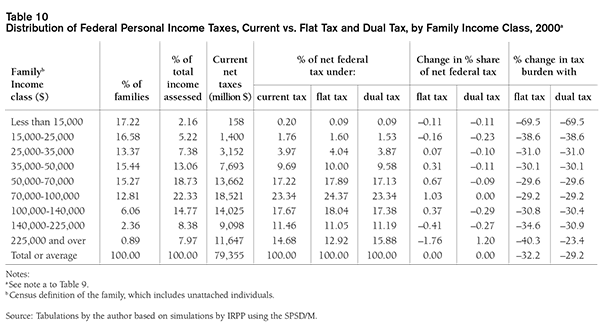

The distributional effects of the dual tax differ significantly when viewed on the basis of family incomes. This arises in part because many upper-middle family incomes stem from the earnings contributions from two (or more) members, each of whom is taxed at the 17 percent rate on earnings below $100,000, even if total family income exceeds this figure. As seen in Table 10, virtually all family income classes below $225,000 gain in the sense that their share of the total tax burden declines with a dual tax. The only exception is the range of family incomes from $70,000 to $100,000, where there is no change, although there are some small gains and losses for income groups more finely divided within this range.37 For families, all of the reduced share in total federal tax revenues that results from the dual tax is enjoyed at the expense of the highest income group – those above $225,000 – who bear an additional 1.76 percentage point share of the total tax burden. Note that these estimates do not include the impact of two other important features of the Alliance plan for personal taxes – the increased contribution limits for registered savings and the reduced capital gains tax rate. It is improbable that taking the former factor into consideration would reverse our findings. The proposed increase in allowable contributions to $16,500 would benefit only individuals whose annual earnings exceed $75,000 but would be of proportionally little benefit for families above $225,000. The capital gains tax cut is potentially of much larger benefit to very high income groups, but it is unknown the extent to which they would realize more taxable gains and thereby pay offsetting amounts of taxes.

These findings indicate that the dual tax would reduce, but not fully eliminate, the negative effect of a flat tax for moderate-and middle-income individuals in terms of their tax shares relative to the current federal tax. It would also substantially increase the tax share of very high-income (above $250,000) individuals. Of course, all individuals would have their taxes cut under the scheme, and it is simply a matter of which groups would have their taxes cut proportionately more. More striking is our finding that the dual tax would almost completely eliminate the adverse shift in tax shares relative to the flat tax when viewing taxpayers on a family income basis. Almost all income groups below $225,000 would have smaller tax shares than exist under the current federal tax, and the increased share would be borne almost solely by families above $225,000 (possibly offset by the capital gains tax cuts). Yet it is critical to understand that even this kind of tax policy change would reduce the progressivity of the overall tax system. The personal tax is the largest and almost only progressive component of the total tax system. A large cut to personal taxes, even if the cuts were completely proportional and thereby left the relative tax shares of all income groups unchanged, would by its nature reduce overall tax progressivity. This is because it would reduce the relative weight of the revenue source that is progressive.

Substantial progressivity of personal income taxes is required if society wishes to have an overall tax system that is even mildly progressive. Most of the other major types of taxes in Canada have been assessed as regressive, with the exception of the corporate income tax.38 Large revenue generators such as general sales taxes (provincial retail sales taxes and federal GST), excise taxes on alcohol, tobacco, and gasoline, municipal property taxes, and federal payroll taxes are all significantly regressive. Because of saving and spending patterns, sales-type and property taxes take a larger portion of lower than of higher incomes. The taxable ceilings for most payroll taxes also make them relatively more burdensome for lower than higher earners. Even with alternative assumptions about who bears the tax or taking a lifetime perspective on burdens, these taxes are at best somewhat regressive.39 Hence, any proposal to sharply reduce the progressivity of personal income taxes, such as a flat tax plan or even the proposed dual tax, risks the creation of an overall tax system that is regressive. If one desires a progressive tax system – and this is a value judgment that one need not accept – then retaining significant progressivity in personal taxes is essential.

A final issue concerning tax progressivity is the proper level of government for applying redistributive taxes. A US empirical study finds that attempts to redistribute through state-level taxes do not succeed.40 States with more progressive tax systems lose higher-skilled workers until their gross salaries rise to offset their higher taxes. In effect, the employers bear the impact of more progressive taxes, and the result is the loss of more skilled and highly paid jobs to other states offering less progressive taxes.41 One might expect similar economic effects to arise in Canada via inter-provincial mobility of labour, although residents of some regions may tolerate higher tax burdens without migrating for reasons of language or culture. Otherwise, the provinces will be thwarted in their attempts to redistribute via progressive taxes. Those provinces that apply more progressive taxes may only be harming their high-tech and growth sectors.42 Yet if the provinces are constrained in this way, this leaves the federal government as the sole jurisdiction that can effectively apply a substantially progressive income tax. Thus, a flat rate tax might be an acceptable prescription for provincial policy (and Alberta will go this route in 2001), but it is inappropriate policy for the federal government if vertical equity is a concern.

In the analysis underlying the Alliance’s original flat tax plan, the primary justification for adopting a single tax rate was horizontal equity between one-earner and two-earner couples.43 Simplicity and efficiency were cited as secondary considerations. The arguments ran as follows:

Simply, the principle of horizontal equity asserts that two individuals earning the same amount should pay the same amount of tax. Similarly, two families earning the same amount should pay the same amount of tax…[A] fundamental breach of horizontal equity in the Canadian personal income tax system…[arises from] the choice of the individual as the unit of taxation and the use of one rate structure with multiple marginal rates. The result is that two families with identical total family incomes will have significantly different tax liabilities if one family has a single-income earner and the other two income earners…44

This section assesses the implicit assumption that equal incomes are equivalent to equal ability to pay taxes when comparing one-and two-earner couples. The ways that the flat tax and dual tax plans address this issue are investigated. We then examine whether there are other solutions to this problem – if it is indeed a problem – that do not fully abandon marginal tax rate progressivity. The horizontal equity issue relating to dependent children in the tax system, and the Alliance approach to this issue, are then assessed.

The analysis outlined by the Alliance assumes that the ability to pay taxes should be judged across taxpaying units based on their incomes.45 This assumption might be valid when comparing taxpaying units of the same size and composition. However, when comparing one-earner couples with two-earner couples, market incomes neglect a major difference – the additional time that a non-employed spouse has available for producing services in the home. These services include cooking, laundry, housecleaning, shopping and other errands, home and auto repairs, and child-minding; all these services are costly to purchase in the market. The two-earner couple needs to purchase much more of these services to be on a par with the one-earner couple. Rational couples will choose to have one partner stay at home to provide these services only when their monetary and psychic value exceeds the net income that could be earned by working in the market.46 Hence, market incomes do not offer a reliable measure of the relative abilities to pay tax, or the relative well-being, of one-and two-earner couples. A one-earner couple with $60,000 of earnings per year is not equivalent to a two-earner couple with individual earnings of $20,000 and $40,000 that total the same $60,000. The latter couple has less time to be productive in the home, greater household expenses, and a lesser ability to pay taxes, and hence should bear a lower total tax burden. And the former couple could have an income above $60,000 if the second spouse took paid work.

The preceding line of analysis has been used in several recent Canadian studies to support the continued taxation of families based on individual incomes.47 Nevertheless, some countries allow various forms of income splitting or joint family taxation; the US and France are examples. One might justify that approach by considering factors beyond those in the cited analysis. First, one-earner couples will in some cases be the result, not of a rational choice to have one partner stay out of the labour market, but of an inability to find a paying job; then much of the home time will be enforced leisure rather than productive time. Second, when one partner is highly paid in a job that is very demanding, it may be rational for the other partner to serve in a supporting role by bearing all of the home and child responsibilities. In effect, the two partners are working jointly for one demanding paid job and one demanding unpaid home job. Some years ago, in terms that today might be regarded as sexist, John Kenneth Galbraith described this as the need for a “wife” for “consumption administration.”48 Yet another factor might be a societal value of having at least one parent at home to help raise and nurture pre-school children.49 In the end, it is a matter of personal values whether these cases support a preference for joint taxation over individual taxation.

If one accepts the validity of these arguments for assessing ability to pay based on the joint incomes of married couples, then horizontal equity requires changes to the current tax system. The Alliance analysis identifies two distinct remedies to restore equity and opts for the single tax rate solution.50 First, couples could be allowed to file joint returns with modified tax schedules to allow income splitting; one form of this would provide joint married tax brackets twice as wide as the brackets allowed for single filers. This method would retain progressivity of MTRs and continue to serve vertical equity. Alternatively, a single tax rate combined with equal and transferable exemptions for both spouses could be another way to achieve this view of horizontal equity. The latter is the Alliance’s preferred solution to the issue of one-earner couples and, unlike the other approach, would fully eliminate MTR progressivity.

The essential choice is between some form of joint filing with modified but still progressive rate schedules and retaining individual filing but adopting a single tax rate. The Alliance analysis rejects the joint filing method for three reasons. First, it asserts that joint filing would compromise privacy: “spouses may prefer some economic autonomy and keep their financial matters private.”51 Yet, their plan would also require the exchange of information within the couple in that transferring the lower-income spouse’s unused exemption reveals their income. Moreover, the tax package keeps the existing Child Tax Benefit, which requires that the incomes of both partners be disclosed.52 Second, it argues that joint filing would require solving a technical problem called “adult equivalents,” which is the question of how much income splitting to allow. Two adults living together can achieve scale economies – savings from shared costs of housing, furnishings, car and appliances, phone and utilities, and from volume purchases of food and household supplies. If horizontal equity is based on well-being or ability to pay, rather than a simple income measure, then less than full income splitting is appropriate.53 Studies by Statistics Canada offer answers to the issue of adult equivalents, but the Alliance solution assumes that there are no scale economies. Third, the Alliance analysis states that joint filing “would lead to greater complexity, making administration and compliance more difficult.” This point is assessed below and is found to have little substance.

Several other arguments can be cited for adopting joint taxation with at least partial income splitting for married couples in Canada. First, joint filing substantially reduces the complexity of financial planning and accounts for married couples, and it also reduces the complexity of their tax planning and filing. Under the current system, married partners must do complex calculations for many decisions to determine their jointly optimal investment strategies. Second, joint filing would restore a different aspect of horizontal equity – between married couples with only labour earnings and those with significant amounts of self-employment or capital incomes and savings. The latter are already able to pursue many legal strategies to achieve income splitting: (1) deposits to spousal RRSPs; (2) the lower-earning spouse doing all of the couple’s savings with the higher-earning spouse doing all their spending; (3) interspousal loans, which can escape the attribution rules with respect to capital gains; and (4) the self-employed and those with incorporated businesses shifting income to their spouse via paid positions and dividends. Joint filing would extend similar benefits of income splitting to those with only employment earnings. Introducing joint filing in Canada would also make the tax burdens for highly paid workers with either an at-home or lower-earning spouse more competitive with the counterpart US tax burdens.54 The bottom line is that joint filing could achieve the same horizontal equity as the flat tax while retaining progressivity.

The flat tax plan would raise the basic taxfiler exemption from the current $7,231 to $10,000 and the spousal/equivalent-to-spousal exemption from its current $6,140 to $10,000.55 Equalizing these two figures is necessary to achieve the plan’s asserted horizontal equity between single-and dual-earner couples while using individual tax filing. As with the present tax system, a spouse with income below the taxable threshold could transfer the unused part of the exemption to their spouse, which is a limited form of joint filing. While this approach achieves horizontal equity based on a simple income notion, it does not achieve equity based on ability to pay. As explained previously, two persons living together can live more cheaply than two persons living alone at the same real living standard. The Alliance plan ignores this dimension and creates horizontal inequities between married couples (whether one-or two-earner) and single adults. The couples are taxed relatively lightly, the singles comparatively heavily. In the US system of joint filing, these scale economies are recognized by the use of a standard deduction for married couples that is less than double that for singles (US$7,350 versus US$4,400)56 and tax brackets for joint filers that are less than double those for single filers (see Table 2).

It should be noted that the transitional shift of policy from a flat rate to a dual rate scheme would compromise its ability to achieve the asserted form of horizontal equity for couples. Namely, for those couples with at least one partner earning above the proposed $100,000 threshold for the higher tax rate, one-and two-earner couples with the same total incomes would still bear different total tax burdens. Even though such one-earner couples could transfer the full enlarged spousal credit to the earning spouse, this would not achieve the same result as income splitting. The dual tax could claim that the problem would then be restricted to the very small proportion of all taxpayers where one partner of a couple has earnings above $100,000. And the dual tax plan’s diminished spread between the unchanged bottom rate of 17 percent and the reduced top MTR of 25 percent would also reduce the degree of horizontal inequity. As with any tax structure that is progressive in MTRs, the dual tax would need some form of joint filing or other income splitting to fully achieve the asserted goal.

The flat tax plan would introduce a $3,000 deduction per dependent child.57 This would restore some degree of horizontal equity between taxpaying households with and without children at upper-income levels. With the tax changes that accompanied the Child Tax Benefit scheme in 1993, taxpayers with children and high incomes face the same tax burdens as other taxpayers with the same incomes but no children.58 This situation ignores the fact that families with the same incomes but more dependants have a lower ability to pay taxes, as they have less discretionary income. We next examine whether this plan offers the best remedy for this situation, but first an anomaly of the Alliance proposal is noted. The plan would allow a single parent to claim both this child deduction of $3,000 and the equivalent-to-spouse exemption of $10,000 on behalf of the same child; hence the single parent’s total deductions including the filer amount would be $23,000. In contrast, when the federal tax system allowed non-refundable tax credits for children before 1993 and exemptions for children before 1988, a sole parent could claim the equivalent-to-spouse amount only in lieu of the child amount. By allowing sole parents to claim both, the Alliance scheme would create a tax inequity vis-Ã -vis two-adult households with no children. The latter would be able to claim deductions of only $20,000, even though their essential spending needs are likely comparable to those of the one-adult, one-child household.

One feature of the proposed new child deduction is noteworthy. The plan proposes to disallow the first $3,000 of expenses that can be claimed as child care expense deductions, while leaving the upper limits unchanged ($7,000 annually per child under age 7 and $4,000 for ages 7 through 16). The goal here was to “universalize” the tax recognition of the costs of child care, including care provided by at-home parents for their own children. The $3,000 deduction would be allowed for all parents regardless of whether they incurred cash expenses for child care. This provision would raise the relative cost for parents (typically mothers) working in the paid labour force versus staying home to care for their children, as they would no longer get an extra tax deduction by incurring the first $3,000 of child care costs. For those who wish to encourage more parental care of children at home, this is a desirable effect; those who prefer to promote the labour force skills and financial independence of women might deem this an undesirable effect.59

Several studies have examined the tax treatment of dependent children, as well as structural problems with the Child Tax Benefit (CTB). They warrant comparison with the solution put forward by the Alliance tax plan, which has a $3,000 per child deduction along with the existing unreformed CTB system. The alternatives proposed by others include various combinations of: (1) instituting a child exemption within the income tax;60 (2) instituting a non-refundable child tax credit;61 (3) instituting a universal child benefit (or a refundable child tax credit without any income test);62 (4) moderating the rates of benefit phase-outs in the existing CTB;63 and (5) combining the last two elements by reducing and stopping the CTB phase-out at a median income level, so that a partial child benefit remains for higher-income families.64 These schemes have sought to remedy the tax recognition of children at all incomes for horizontal equity and reduction of the high effective MTRs that arise with the CTB and some related provincial schemes. Combined with the MTR of the tax system, these total MTRs rise into the 60 percent range for incomes of $20,000 to $30,000, and for certain incomes rise as high as 70 percent in British Columbia and 91 percent in Saskatchewan.65

Normally, an exemption and a non-refundable tax credit have differing values depending on the taxfiler’s income level. This is a result of progressive MTRs, and the difference vanishes when considering a flat tax system. Under the flat tax plan, the provision of a $3,000 deduction per child is worth $510 in federal tax savings (0.17 x $3,000) for those families who have taxable incomes. These savings would be added to benefits currently received by families under the CTB, and they would be a new tax benefit for those at incomes above the levels that qualify for the CTB. However, the plan does nothing directly to correct the problem of very high MTRs that arise under the CTB scheme.66 Indirectly, it does moderate the problem for these households who either become non-taxable because of the larger exemptions (thus dropping their federal tax rate by 17 percentage points) or are shifted into the flat 17 percent tax rate from the middle bracket. Nevertheless, some households would still face total MTRs of 60 percent or higher under the flat tax plan with an unreformed federal CTB and provincial benefits.67

A more satisfactory solution could be achieved under the current progressive federal tax and CTB scheme by instituting several reforms. The CTB payments could be subjected to considerably lower phase-out rates, which could be accomplished by: (1) lowering the incomes at which the phase-outs begin; (2) raising the income level at which the high phase-out rates of the National Child Benefit Supplement (part of the CTB) cease; and (3) stopping the phase-outs entirely above median family incomes. The last of these steps would leave in place a flat dollar amount per child at the higher incomes, which would be a form of universal child benefit.68 The largest benefits would continue to be directed to children in families at low and moderate incomes. Since the CTB would no longer vanish at high incomes, the phase-out rates could be correspondingly reduced, which means lower effective MTRs for beneficiaries. The phase-out rates of the reformed CTB would be completely eliminated above median family incomes – below $60,000 for two-parent families with children – so that they would no longer overlap the top federal MTR. A reformed scheme could also consolidate the GST tax credits for children with the CTB.69