Redesigning Canadian Trade Policies for New Global’s Realities

Overview of the Research Findings

Stephen Tapp, Ari Van Assche and Robert Wolfe

This study takes a close look at foreign direct investment (FDI) to and from Canada and concludes that fears about their adverse effects on the domestic economy are largely unfounded. The debate is too often framed around two misleading caricatures: that outward FDI is synonymous with exporting jobs, and that inward FDI is synonymous with excessive foreign control of Canada’s economy.

A dispassionate analysis of the evidence shows that the benefits of foreign investment far outweigh any real or imagined drawbacks. Foreign firms operating in Canada are more innovative and productive than their Canadian counterparts, and they pay higher wages. More importantly, they import significant amounts of technology from their parent companies, and the benefits of these technologies spill over to domestic firms. In addition, though the stock of inward FDI did increase somewhat as a share of GDP in the late 1990s, it has held steady since then at just over 30 percent – the same share as in 1970.

Worries about corporate takeovers and the “hollowing out” of high-value head office functions in Canada are also misplaced. Foreign takeovers have actually increased head office activities in Canada in recent years, because foreign firms typically find it to their advantage to keep such activities geographically close to their Canadian operations.

Despite these benefits, Canada has been losing its attractiveness as a destination for foreign investment, particularly in the wake of continental free trade. Canada’s share of global inward foreign investment has fallen since the mid-1980s, because firms are increasingly locating their production facilities in the United States or Mexico to serve the entire North American market.

The debate about foreign investment in Canada ignores the fact that Canadian multinationals have quietly become major players in the global marketplace. Canadian direct investment abroad has exploded in the past 30 years, and Canadian firms now own more foreign operations (in terms of dollar value) than foreign companies own in Canada. Far from exporting jobs, this investment abroad serves primarily as a beachhead for market expansion, stimulating domestically produced exports and high value added head office activities such as engineering and design.

Policies toward FDI should avoid counterproductive restrictions and focus on fostering a domestic economic environment that enhances the competitive posture of Canadian firms. As expected, domestic innovation and low corporate tax rates are shown to be important levers, but not in the ways that are commonly assumed. Domestic innovation and technology-oriented foreign investment are complements rather than substitutes (i.e., the former helps attract the latter). And low corporate tax rates in fact have little effect on the decision to invest in Canada, but they do help Canadian companies compete more effectively in foreign markets.

There is perennial discussion in Canada over the merits of both inward and outward foreign direct investment (FDI). This debate was quite heated in the 1970s and 1980s, but subsided over much of the 1990s and 2000s. However, the recent high-profile takeovers of some of Canada’s “iconic” companies, such as the steelmaker Dofasco, Hudson’s Bay Company, Inco and Alcan, have rekindled that debate. Some have argued that these foreign acquisitions are resulting in a hollowing out of the Canadian economy, an assertion that has been shown to be inconsistent with the data. The objective of this study is to examine the changing trends in Canada’s inward and outward FDI over the past several decades and to propose how public policies should be changed to ensure that Canada draws maximum benefits from foreign investment flows.

The dramatic rise in energy prices from 2000 to 2008 and the enormous reserves of oil and natural gas in Canada’s West have generated significant investments, or expressed interest, from foreign private companies, foreign state-owned enterprises and sovereign wealth funds (SWFs). These developments have contributed to the perceived urgency of the public debate about FDI. Although the collapse in oil prices during the global financial crisis of 2008 and the virtual standstill in new investments have moved the discussion in other directions, the issue of FDI into Canada, as the world economy begins to recover and with it oil prices, is likely to reemerge.

But what is remarkable about this public concern about foreign takeovers of Canadian companies, and hence investment into Canada (inward FDI), is the fact that Canada has been losing its attractiveness, relative to other countries, as a destination for foreign investment. Canada’s share of global inward foreign investment has been falling since the mid-1980s, and this result holds true whether we include emerging markets in the analysis or not. Given the positive benefits that come with foreign investment, including technology transfer and increased domestic competition, this trend has harmed Canada’s prosperity. Analysis from the Organisation for Economic Co-operation and Development (OECD) points to Canada as one of the more restrictive countries when it comes to foreign investment, noting specifically that three large sectors – finance, transportation and communications – are heavily regulated and limit foreign investment (Golub 2003).

Coincident with these changing patterns on the inward side, Canadian direct investments abroad have been growing at a faster pace than foreign investments in Canada. That is, Canada has moved from being predominantly a host economy for foreign investment to being an important source economy.1 These investments into the global economy, for the most part, have opened foreign markets for Canadian exports, and have thus stimulated Canadian domestic investment and employment. Furthermore, outward FDI increases demand for domestic head-office activities that go beyond straight “exports” (such as engineering and design).

Despite extensive empirical evidence documenting these benefits associated with outward FDI, they remain less well understood among both policy-makers and the general public.

There is a stark difference between the environment today and that of 1970. Expressed as a share of GDP, Canada’s inward FDI is about the same as it was in 1970, but outward FDI is much higher. This means that the cost of “protecting” the Canadian economy by further restricting inward FDI is much higher than before in the sense that any retaliatory restrictions by other countries would have very large adverse effects on the growing stock of Canadian investment abroad. Foreign investment, like trade, flows in two directions, and the Canadian government must be careful to consider the policy responses of other countries when deciding how much, if at all, to “protect” domestic firms.

Using data at the country and industry level, this study estimates two models of FDI. The first is a gravity model that examines bilateral FDI between OECD countries from 1980 to 2004. In addition to confirming the widely understood fact that FDI flows are a function of geographic proximity and size of economies, I measure the impact of the Canada-US Free Trade Agreement (FTA) and the North American Free Trade Agreement (NAFTA) on Canada’s outward and inward FDI. The results robustly show that the impacts of the Canada-US FTA on both outward and inward FDI were small, whereas the post-NAFTA period generated large increases in both outward and inward FDI to and from OECD countries generally. Part of this was due to the creation of the European Union in 1993, which liberalized foreign investment flows in western European countries, all of which are OECD members. Canada saw increases in FDI flows in both directions in the post-NAFTA/EU period, but they were significantly smaller than in other countries.

The second model examines 60 industry groups, and considers the importance of tariffs and free trade agreements in explaining Canada’s FDI. The results, while nuanced, generally indicate that any reductions in FDI designed to avoid tariffs were overwhelmed by the expansion of trade and investment flows brought on by the globalization of supply chains that broader continental free trade agreements enabled.

In addition to these trade effects, the industry-level analysis also yields important findings with respect to corporate taxation and R&D intensity. The results indicate that R&D is robustly important in attracting inward FDI into Canada. This has important policy implications, because it indicates that a fertile innovation environment is important for attracting foreign investment, which in turn leads to additional technology transfer to Canada in a positive feedback loop. Industries that have a high R&D intensity both attract more inward FDI and undertake more outward FDI.

Industry-specific Canadian corporate tax rates are found to be unimportant statistically for inward FDI, suggesting that they are not an important criterion for determining the location of FDI. However, corporate tax rates appear to have a negative effect on outward FDI.

The first section of this study provides definitions of FDI, distinguishes between portfolio and direct investment and highlights the importance of mergers and acquisitions as a type of FDI.

The next section briefly considers the upsides and downsides of FDI, revisits the hollowing-out debate in Canada and discusses optimal policies. The study then reviews the trends in Canada’s inward and outward FDI over the past several decades. The next section presents two empirical models of FDI and estimates the importance of key factors underlying Canada’s changing FDI patterns. The study concludes with a discussion of the policy implications.

Foreign investment, broadly speaking, takes place when financial capital flows across international borders for investment purposes. When capital is invested in financial markets, such as stocks or bonds, but is not accompanied by control of the underlying issuing corporation or organization, the investment is defined as foreign portfolio investment. Examples include Canadian investors buying US treasury bills or US corporate bonds. The Canadian investor would have a claim on the US government or US corporation that issued the bonds, but would not exert control over the decision-making process of those organizations. In such situations, the investors are considered passive.

Total international capital flows are dominated by such “passive” portfolio investment. In contrast to foreign portfolio investment, foreign direct investment (FDI) involves some control over the underlying asset. The classic example of this kind of investment is “greenfield” investment, where a Canadian firm, for example, opens a new facility in a foreign country and hence has full control over that foreign operation; this would be referred to as Canadian FDI abroad. Similarly, when a foreign company undertakes greenfield investments in Canada, this would be referred to as FDI in Canada. The investor exerts full control over such investments, and hence is not passive.

Although greenfield investments are clear-cut examples of FDI, there are many scenarios that are less so. For example, as a Canadian organization increases its stake in a foreign corporation to a point where it has obtained control, its formerly passive role will become active. Once control over the underlying corporation is obtained, the classification of the investment changes from portfolio investment to direct investment. In the case of a publicly traded company, once a Canadian organization has 50 percent plus one share of a foreign publicly traded organization’s voting shares, the Canadian company would unequivocally control that foreign organization, and hence what may have begun as a portfolio investment becomes a direct investment. In reality, given that publicly traded organizations are widely held, one does not need to own such a large stake to exert a degree of control – that is, far less than 50 percent plus one voting share is needed. In Canada, the rule of thumb is 10 percent: that is, once a Canadian investor holds 10 percent of the voting shares in a foreign corporation, the investor has sufficient control to classify the investment as direct. It is important to note that these rules of thumb vary by country. For a discussion of different conventions across countries, see Safarian (1993).

This study does not examine foreign portfolio investment. Rather it analyzes trends in foreign direct investment in Canada (inward FDI) and Canadian direct investment abroad (outward FDI). Furthermore, the analysis will primarily focus on the stocks of inward and outward FDI rather than the flows because the stocks are far more stable and provide a better sense of a country’s total foreign investment position at any point in time.

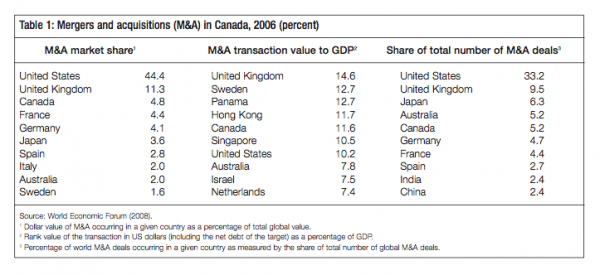

It is important to put mergers and acquisitions (M&As) into the context of FDI. Much of the world’s FDI takes the form of M&As, and this is especially true for Canada. That is, Canadian multinational enterprises (MNEs) establish a controlling stake in foreign companies by merging with a foreign company or acquiring a controlling stake in a foreign company. The same is true for foreign companies that wish to gain a controlling stake in a Canadian company.

It is difficult to calculate the share of FDI flows that are the result of M&As because of differences in data collection and reporting methodologies and because M&A transactions are becoming more complicated. For these reasons, the analysis in this study will not focus on M&As. But, as noted above, many FDI transactions actually take the form of M&As.

Table 1 highlights the role of M&As for the 10 most active markets globally; these figures include domestic and international M&As. Column 1 lists the top 10 markets by global share of M&A activity. On this score, Canada ranks third, following only the United States and the United Kingdom. In 2006, 4.8 percent of the global dollar value of M&A activity occurred in Canada. Column 2 measures M&A activity in each market relative to GDP. On this measure, Canada ranks fifth, with M&A activity equaling 11.6 percent of GDP. Finally, column 3 shows the share of the absolute number of deals globally occurring in a given market. Even on this score, Canada ranks highly, with 5.2 percent of all deals in the world occurring in Canada.2

The debate around foreign direct investment is too often framed around two caricatures: that outward FDI is synonymous with exporting Canadian jobs and inward FDI is synonymous with excessive foreign control of Canada’s economy. To understand more fully and accurately their costs and benefits, it is important to set aside these prejudices and focus on the important effects that trade liberalization has had on FDI flows and their relationship to imports and exports.

Governments have sought trade liberalization policies in general because of the economic gains that accompany the growing trade flows they produce (Coe and Helpman 1995; Dobson 2002; Trefler 2004). Such developments on the trade side, however, have significant impacts on FDI, both inward and outward.

In the absence of trade liberalization, trade and FDI generally substitute for one another. For example, when there were significant tariff barriers between Canada and the US prior to continental free trade, Canadian MNEs found it more cost-effective to open a production facility in the US to avoid the tariffs, and vice versa. As a result, the economic benefits generated by US demand for Canadian products did not accrue to Canada. By the same token, however, Canadian demand for the products of US companies was satisfied by their Canadian affiliates.

However, as tariff and other trade barriers fell generally on the global level and in the wake of the Canada-US Free Trade Agreement, it was no longer necessary for multinationals to locate production facilities in the markets they desired to serve to avoid costly trade barriers. There is a large empirical literature that demonstrates the complementarity of trade and FDI in the absence of trade barriers (Brainard 1997; Hejazi and Safarian 1999b, 2001, 2004a, b; Lipsey and Weiss 1981, 1984; Rao, Ahmad, and Barnes 1996; Safarian and Hejazi 2001). As a Canadian MNE expands its operations in the United States and elsewhere in the world, this enhances market access and increases demand for intermediate inputs, head office activities such as engineering and design, as well as other domestically provided business services.

This should not come as a surprise, given that a large share of the world’s trade occurs inside MNEs. The OECD examined such patterns in five member countries and found that the share of intrafirm exports in the total exports of manufacturing affiliates under foreign control exceeded 50 percent in Canada, the United States, Sweden and the Netherlands, but was only 15 percent in Japan by contrast (Organisation for Economic Co-operation and Development 2005)

There are many economic benefits associated with inward FDI, of which the most important are related to technology transfer. It is well understood that trade flows can facilitate technology transfer across international borders, but Hejazi and Safarian (1999a) and van Pottelsberghe de la Potterie and Lichtenberg (2001) show that FDI channels are much more effective in this regard. This is confirmed by Tang and Rao (2001), who show that foreign firms in Canada are not as R&D-intensive as their Canadian counterparts, yet have much higher productivity. The reason is that they import a great deal of technology from their parent companies.

A second economic benefit from FDI is well-paid jobs. While data are not available for the economy as a whole, almost one-third of Canadian workers in the manufacturing sector work for foreign multinationals. These workers tend to be more productive than their domestic-firm counterparts and earn higher wages (Baldwin and Gu 2005).

Given this evidence regarding the merits of inward FDI, what are the downsides? The arguments made against inward FDI are very much related to the issue of head office activities, including R&D, but especially strategic decision-making. The argument is that when a Canadian company is purchased by a foreign interest, the decisions driving the Canadian operations will be moved to the foreign head office. It is argued therefore that the foreign takeover of the Canadian asset would result in the movement of the high-value-added activities to the head office location in the foreign jurisdiction.

The predictions that flow from economic theory are mixed as to what actually should happen when there is a foreign takeover of a Canadian company. Multinationals are driven by profits: the argument that activities in Canada would be moved to the foreign jurisdiction (the home country) is not supported unless that move would enhance profits for the multinational. In other words, when maintaining those activities in Canada is the most efficient or profitable option for the multinational, then there shouldn’t be anything to worry about. Of course, to the extent that there are agglomeration economies – benefits associated with locating near other head office activities – then the foreign MNE may benefit from moving Canadian head office activities to the home market and locating them near the global head office.

But according to a study on global leaders undertaken by the Institute for Prosperity and Competitiveness, there is no solid evidence that the transformation of a Canadian head office into the regional headquarters of a foreign firm via a takeover has a negative impact on Canada’s prosperity. Head offices, whether Canadianor foreign-owned, are important sources of high-value jobs, and public policy should not discourage foreign takeovers in order to preserve Canadian ownership of head offices (Institute for Competitiveness and Prosperity 2008).

The following quote from a Statistics Canada study is also instructive: “Much of the dynamism in Canada’s head office sector actually comes from foreign-controlled firms. The head offices of foreign-controlled firms contributed to all of the gains in the number of head offices over the past 6 years and accounted for 6 out of 10 new jobs created. The effect of foreign takeovers has not been to reduce the number of head offices in Canada nor head office employment. As a result of foreign takeovers, more new head offices were created than lost and employment in head offices was as high after the takeovers had occurred than before” (Beckstead and Brown 2006, 15; also see Baldwin and Brown 2005).

The evidence thus suggests that, contrary to popular belief, inward foreign direct investment does not reduce the number of head offices in Canada, suggesting that foreign multinationals find it in their best interest to keep such activity geographically close to their foreign operations rather than to their international headquarters.

With the takeover of many “iconic” Canadian firms, there has been extensive discussion of restricting foreign investment into the Canadian economy. However, restricting foreign investment would have several adverse effects.

First, it would remove the discipline imposed on managers of Canadian firms that accompanies the threat of takeover by large foreign companies. When management of any publicly traded company deteriorates, shareholders express disapproval by selling its shares. If share prices fall sufficiently, the company becomes a prime target for a takeover. With the falling stock market value, new owners can buy a controlling stake in the company and replace the management team that has been performing poorly with new managers. When foreign investment is restricted in an economy of relatively small size such as Canada’s, this threat of takeover is very much muted, and with it the discipline of managers. Investment restrictions would have a detrimental impact on the quality of management in Canada, especially in large and influential companies.

Second, limitations on investment would constrain the amount of capital available within the Canadian economy, thus raising the cost of capital. There is in fact a positive relationship between inward FDI and domestic investment. The majority of domestic credit is sourced locally, but a growing proportion comes from international sources, in the form of FDI or mergers and acquisitions. The ratio of inward FDI flows to domestic fixed capital formation has risen rapidly in Canada, and reached 34 percent in 2007. This is significantly higher than in the United States, where the corresponding proportion is less than 10 percent.

Third, FDI restrictions reduce spillover benefits from foreign companies. We have already seen that in Canada, foreign firms tend to have higher productivity than domestic firms, and in their presence, domestic firms benefit from the advanced technology and management techniques employed by foreign firms operating locally. In order for foreign operations to overcome the hurdles of going international and operate profitably when faced with competition by local firms, they must be more competitive. The domestic economy also benefits from the increased amount of competition that comes with the presence of foreign firms. These spillover effects are significant: some estimates say the spillover benefits that come from FDI are twice those of spillovers associated with trade alone (Hejazi and Safarian 1999b).

Although Canadian FDI abroad has grown at a much faster pace than FDI in Canada over the past few decades, what makes headlines is inward FDI when it takes the form of takeovers of iconic Canadian companies. Many other foreign investments in Canada are not highlighted, nor are the significant Canadian investments abroad. This leads to a very narrow public perception of the issue, which focuses on “hollowing out” – the notion that foreign corporate takeovers reduce the influence of Canadians in their own economic affairs.

But despite the heated rhetoric, there is no rigorous analysis supporting the claims that the Canadian economy is being hollowed out. The Institute for Competitiveness and Prosperity identifies Canada’s global leaders by three criteria: (1) public or private Canadian-controlled companies listed in the Report on Business Top 1000 or the Financial Post 500; (2) companies with revenues exceeding $100 million in 2007; and (3) companies that are among the five largest by revenue globally in a specific market segment. In some cases where global competition is precluded (such as rail service), North America was the yardstick (leading to the inclusion of CN Rail); and in other cases revenue was replaced by a different factor, such as market capitalization in the case of Manulife. The study identified 33 Canadian global leaders in 1985, 86 in 2003, 84 in 2008, and 86 as of April 2009. Thus, over the past two decades, the number of global leaders in Canada has actually increased, and includes companies like McCain, Open Text, and Research In Motion. They have exploited the power of innovation to expand globally, generating prosperity that comes back to Canada.

Bloom and Grant (2008) extensively examined the issue of hollowing out by tracking the evolution of the 200 largest Canadian companies (in terms of 1990 sales) from 1990 to 2007, as well as studying trends in FDI and mergers and acquisitions generally and carefully analyzing 15 foreign takeovers of Canadian firms; 7 Canadian takeovers of Canadian firms; and 8 Canadian takeovers of foreign firms. The report concluded that over the long term, the trend is favourable for Canada in the sense that there is more outflow than inflow of M&A activity, and there is no long-term trend toward large-scale foreign ownership of the Canadian economy, as foreign control has been stable in the range of 30 percent since the late 1990s.

After studying hollowing out in 2006, Statistics Canada concluded, “Despite continuing concerns that rising levels of foreign investment might lead to the hollowing out of corporate Canada, we find little evidence that this is occurring in terms of head office counts or employment. The number of head offices in Canada and the employment found therein continue to rise” (Beckstead and Brown, 15).

Rather than restricting inward FDI, policy-makers should address the factors that give rise to such takeovers of Canadian companies. That is, the relevant question should be, Why are Canadian iconic firms being bought out, and more precisely, why is it not Canadian firms that are buying foreign firms and becoming the global leaders? Potential explanations include thin Canadian capital markets, Canadian managers who lack the skill sets exhibited by managers from other economies on many competitive dimensions, and disadvantages associated with being headquartered in Canada, for example because of tax or other considerations. The best way to “protect” domestic firms is not by restricting foreign investment, but rather by providing those companies with the most competitive environment within which to operate.

When a foreign multinational corporation invests in the Canadian economy, we clearly understand its motivation: it is profitability. That is, the multinational operates the Canadian asset in a way that maximizes the multinational’s global profits. This process results in significantly positive effects on productivity and prosperity for Canada through job creation and innovation. On the other hand, when the investment in a Canadian asset is controlled by a foreign state-owned enterprise or a sovereign wealth fund (SWF), then the motivation for the investment, and hence the objectives pursued by managers, are less clear – they may invest for political or other non-economic reasons.

The evidence seems to indicate that SWFs are for the most part passive investors (Rose 2008), which means Canada would have access to these large pools of money without worries about foreign control. If these pools of capital were deemed off limits for investment into Canada, the cost of capital in Canada would go up. An important side effect that is often lost in the discussion must be highlighted here: to the extent that a Canadian-headquartered corporation is restricted from accessing financing from foreign SWFs, it may have an incentive to move its global headquarters to another country with more permissive access to them. Therefore, restricting investments in Canada by SWFs may paradoxically lead to more takeovers of Canadian companies.3 Furthermore, as discussed above, restricting access to large pools of financial capital could limit Canadian firms’ ability to muster the financial resources to make competitive bids for foreign companies.

The most high-profile SWFs are those located in China, the Middle East and Russia. But what is perhaps less well known is that Canada is itself home to SWFs, such as the Alberta Heritage Savings Trust Fund. Furthermore, pension funds can also be viewed as a form of SWF, and the foreign holdings of Canadian pension funds are far larger than the holdings of SWFs in Canada. As in the case of FDI generally, restrictions on investing by foreign SWFs into the Canadian market would expose Canadian investments abroad by SWFs (including pension funds) to potential restrictions by foreign host governments. To quote from a presentation by Michael Bloom, “Canadian pension funds’ higher level of activity internationally than foreign SWFs in Canada has implications for ”˜level playing field’ discussions/negotiations. ”˜Reciprocity’ as a strategy leaves us open for other complications – our firms make major purchases in sectors we protect at home” (2008, 32).

Although the benefits that accompany inward FDI have been well documented, there is less of a consensus regarding the impact of outward FDI on the domestic economy. Some view the movement of production facilities abroad to be a negative outcome for the Canadian economy – it is seen as tantamount to the export of domestic jobs and investment. In fact, the correct context within which to view this issue has to do with the underlying motivation for undertaking the FDI.

When movement of production abroad is driven by a poor domestic competitive environment, perhaps due to high taxes, a lack of skilled labour or low R&D intensity, then the effects on the local economy are likely to be negative (although positive from the narrow perspective of the multinational). In other cases, particularly in low-value-added, labour-intensive industries, production may move to nations with lower wage rates to exploit cost advantages. This has been true in the Canadian textile and apparel industries, which have been in secular decline for more than a decade. While this adversely affects the industry involved in the short run, over a longer period, it allows the reallocation of the labour and capital investment to higher-value industries (see Hejazi and Pauly 2002, 2003).

However, if investment abroad is driven by the expansion of domestic firms that seek to exploit their competitive advantage in foreign markets, then the impact of these investments on the home country likely be positive over the longer term. As noted earlier, trade and foreign investment are increasingly complementary, as direct investment abroad serves as a beachhead for market access, thus stimulating domestically produced exports and high-value-added head office activities. Empirical analysis later in the paper indicates that most Canadian direct investment abroad provides such domestic benefits.

As is the case with inward FDI, policy in regard to outward FDI should be directed not at regulating foreign investment itself, but rather at making sure to nurture the underlying factors that drive expansion-led investment abroad. When outward FDI is driven by firms pursuing global opportunities, then this is a good outcome for the Canadian economy. But if Canadian companies seek to move operations out of Canada because of high taxes, a poor competitive environment, a lack of skilled labour or poor access to technology, a sound policy would be to identify the factors causing firms to leave and correct them. By doing so, policy-makers would minimize the exodus of firms, while continuing to permit strong Canadian companies to expand their global reach.

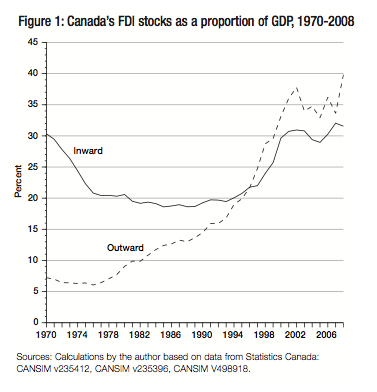

Foreign direct investment has always played an important role in the Canadian economy, though that role has changed substantially over the past several decades. Figure 1 shows the stock of inward and outward Canadian FDI since 1970. At that time, Canada was primarily a host country: the stock of foreign direct investment in Canada amounted to 28 percent of GDP, four times the stock of direct investment held by Canadian firms in other countries. The subsequent three decades saw a secular increase in the stock of outward FDI as a share of the economy, largely due to Canadian firms establishing operations in foreign markets (primarily the United States and Europe). From 1976 to 1999 (the years during which the outward FDI-to-GDP ratio climbed), employment increased by 60 percent and the unemployment rate (while higher during recessions) was essentially unchanged from its 1976 level in 1999, running counter to the notion that large increases in outward FDI have a negative effect on aggregate domestic employment.

Inward FDI to Canada was essentially stable from the mid-1970s to the mid-1990s, and then began inching upward. This reflects the impact of trade liberalization that began with the ratification of the Canada-US Free Trade Agreement in 1988 and was expanded (including liberalization of direct investment) in the North American Free Trade Agreement starting in 1994. More recently, the rise in commodity prices has increased foreign interest in Canada’s natural resources, nearly doubling that sector’s share of total incoming investment from 18 percent to 34 percent since 2000. That has led to a slight uptick in the FDI-to-GDP ratio.

By 1997, Canada moved into a position where its stock of investment into the global economy was larger than foreign investment in Canada. This marked a significant change in Canada’s historic position, from predominantly a host economy to an important source (or home) economy for FDI.

Looking at recent data points, it is noteworthy that in 2008, Canada’s inward FDI actually fell slightly, meaning that foreign firms reduced their presence in Canada (possibly due to the economic and financial crisis) and were less likely to acquire Canadian companies, notwithstanding some high-profile takeovers. In contrast, outward FDI jumped significantly, meaning that Canadian firms were finding profitable production opportunities in foreign markets. This fact seems completely lost in the current public debate around hollowing out, and illustrates the need to base sound policy development on accurate information rather than perceptions.

Relative to the size of its economy, Canadian FDI in both directions has become more important over the past 15 years. But focusing solely on Canada ignores the fact that FDI flows have expanded throughout the world, and it is important to examine Canada’s performance in a broader context.

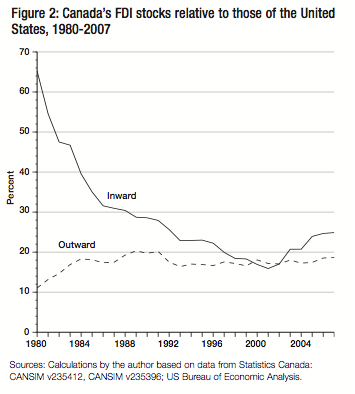

As a starting point, figure 2 shows the stock of inward and outward FDI as a percentage of the relevant stocks for the United States, Canada’s most important trading partner. What immediately jumps out of this figure is that in relative terms, Canada’s inward FDI has fallen dramatically since 1980, from 65 percent of the US level to 25 percent in 2007. Over the same period, Canada’s outward FDI has increased slightly more rapidly than its US counterpart, leading to a slight increase relative to the United States from 11 percent of the US level in 1980 to 19 percent in 2007, with most of the increase occurring in the 1980s.

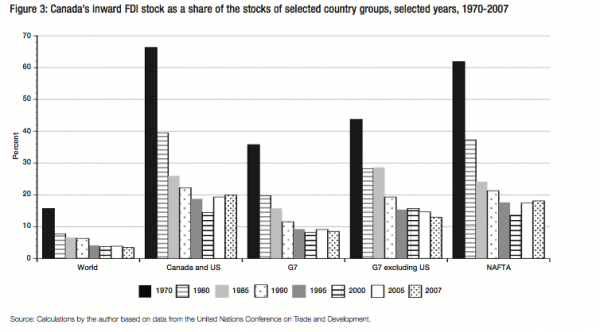

Figure 3 shows Canada’s inward FDI stocks as a share of the total for the entire world as well as for certain groups of countries. The first set of bars shows a considerable decline in Canada’s share of global inward FDI, from 15.7 percent in 1970 to 3.4 percent in 2007. So globally, Canada has become a less attractive destination for foreign investment, at least in relative terms, over the past several decades. Is this because of factors specific to the Canadian economy, or does it simply reflect the fact that fast-growing emerging markets (such as Brazil, Russia, India and China, as well as Eastern Europe) are reducing the share going to industrialized countries?

The remaining bars in figure 3 answer that question indirectly. If Canada’s relative global decline in terms of a destination for foreign direct investment were solely due to the growing importance of emerging markets, then we would expect Canada’s share of non-emergingmarket inward FDI to, at the very least, hold steady. However, Canada’s inward FDI stocks expressed as a share of different sub-groups of industrialized nations – whether it be the G7, the G7 less the United States or the NAFTA signatories – have fallen precipitously since the 1970s.

This general decline has tapered off since 2000, and Canada’s share of NAFTA and CanadaUS inward FDI has returned to the shares seen in the mid-1990s. This is consistent with the data shown in figure 2 and, as discussed later, is largely due to the increasing foreign interest in Canada’s natural resource sector in the context of the recent commodities boom.

This reduction in the attractiveness of Canada as a destination for FDI has not been lost on the federal government, which has worked hard to understand the factors that underlie the decline as well as its impact on the Canadian economy. These trends do, however, seem to be lost on those who continue to argue that the Canadian economy is being inexorably taken over by foreign investors.

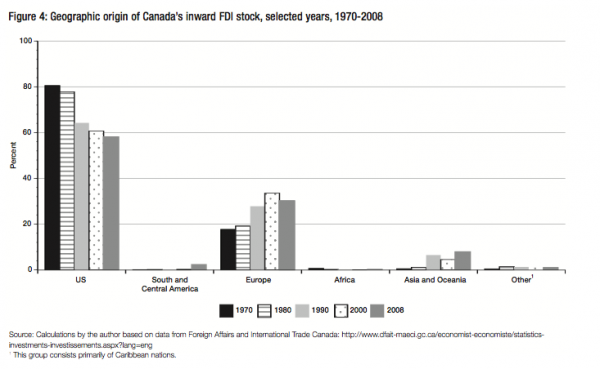

In terms of regional distribution, as figure 4 shows, almost 90 percent of foreign direct investment in Canada comes from the United States and Europe, although the US share declined sharply from almost 80 percent in 1980 to under 60 percent in 2008. As described below, much of this relative decline took place in the wake of the Canada-US Free Trade Agreement, which obviated the need for certain bilateral FDI. With the exception of Oceania (where there are strong linkages with Australia in the natural resources sector), investment from other regions is of marginal importance to Canada.

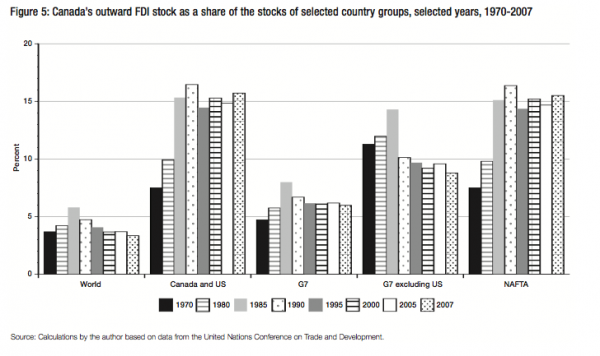

Figure 5 shows how Canada’s share of outward FDI has fluctuated relative to the same groups of countries shown in figure 3, and the results show a marked contrast to the inward FDI trends just discussed. Except for a period in the 1980s, Canada’s share of global outward FDI has been in the 3 to 4 percent range (substantially higher than its 2 percent share of global GDP). This implies that Canadian multinationals are just as active as their global counterparts in seeking out foreign market opportunities, as they have been in the past.

Figure 5 shows that Canadian firms have become significantly more active foreign investors relative to their US and Mexican counterparts (shown by the sharp increase in Canada’s share of Canada-US and NAFTA outward FDI). Most of this increase occurred in the 1970s and 1980s, well before the advent of continental free trade. This has been accompanied by a decline in the share of Canadian outward foreign investment relative to G7 economies other than the US from a peak of 14 percent in 1985 to 8 percent in 2007, implying that Japan, Germany, France, Italy and the UK have collectively increased outward FDI more rapidly than Canada over that period.

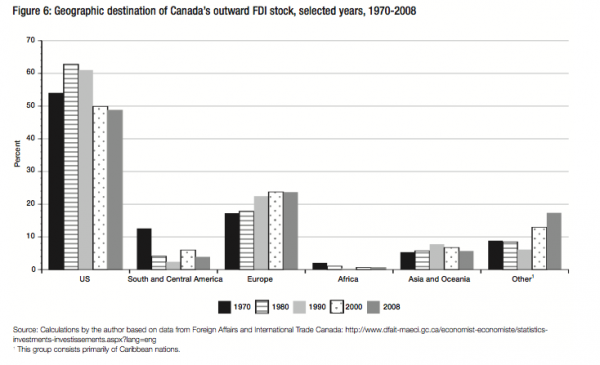

In terms of regional distribution of Canadian direct investment abroad, just under threequarters is destined for the United States (48 percent) and Europe (23 percent), as shown in figure 6. As was the case with inward FDI, the share of Canada’s direct investment located in the United States declined considerably in the wake of continental free trade, since US affiliates were no longer necessary to avoid export tariffs. Most of this decline was offset by an increasing share to Europe.

The sharp increase in Canadian direct investment to the “other” category in figure 6 merits special attention, because it primarily reflects investment that flows through offshore financial centres (OFCs) located in the Caribbean. Over three-quarters of the $110 billion of Canadian FDI destined for the “other” nations in 2008 was invested in three countries – Barbados ($45 billion), Bermuda ($22 billion) and the Cayman Islands ($19 billion).

By moving funds through OFCs (which typically have a zero or very low corporate tax rate), multinationals are able to reduce the after-tax cost of foreign capital, thus facilitating expansion (see box on following page).

The reduction in the share of Canada’s FDI going to and coming from the United States is intimately linked to the reductions in trade barriers between the two countries. Prior to trade liberalization, multinationals from each country operated foreign affiliates inside the other country to avoid paying tariffs – that is, much, but not all, of the FDI between Canada and the US was market seeking. Multinationals from each country would invest in the other to access those markets without having to pay the tariffs that would be required to export into those markets.

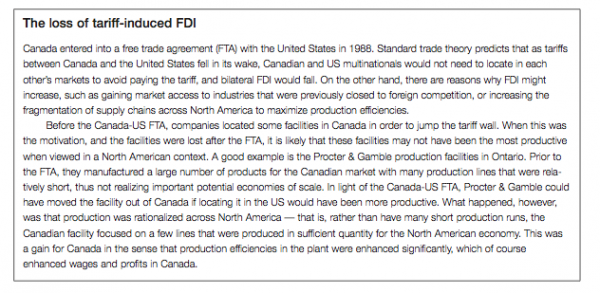

Standard trade theory predicts that the elimination of tariffs in North American markets would encourage multinationals to consolidate production in a single country for export to other nations in the free trade area (thus reducing the need for tariff-avoiding FDI), and this is exactly what has happened. Bilateral Canada-US FDI stocks have become a smaller share of the world total. However, they continue to rise in absolute dollar terms, illustrating that companies invest abroad for reasons other than avoiding tariffs.

There is an important distinction between FDI that is tariff induced, and that which is motivated by other factors. From a North American perspective the realignment of FDI locations that results from tariff reductions leads to more efficient production replacing less productive investments (see box above). These changes improve efficiency within a North American context but may result in the loss of investment for specific markets, most notably Canada.

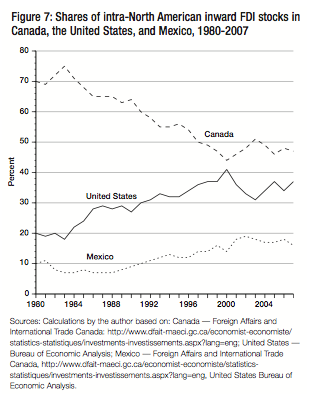

Figure 7 shows trends in intra-NAFTA inward foreign direct investment, and it confirms to a large extent the hypothesis that much FDI in Canada prior to liberalized North American trade was motivated by tariff avoidance. Canada’s share, which exceeded 65 percent through the 1980s, began declining steadily in 1990 (the year after the Canada-US Free Trade Agreement came into force), levelled off in 1992 and 1993, and then declined sharply again for the rest of the 1990s. In relative terms, the United States (and Mexico) pulled back on investment in Canadian production facilities.

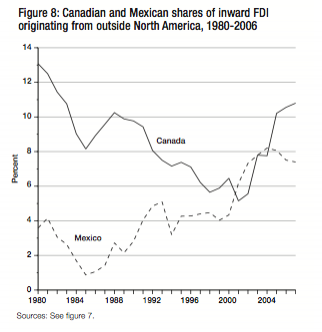

A second effect of continental free trade is on FDI flows from outside the NAFTA area, since multinationals based elsewhere in the world are now free to choose where to locate facilities in any of the three signatory countries to serve continental markets. More than 80 percent of North American FDI originating outside the NAFTA area is destined for the United States, but trends in Canada and Mexico are troubling. In 1980, Canada’s share was more than triple that of Mexico (13 percent vs. 4 percent). But this gap all but disappeared by 2000 (figure 8). The recent uptick in Canada is concentrated in the natural resources sector.

Mexico has become increasingly attractive as a destination for global capital. Why were non-North American MNEs increasingly looking south, not just to the United States, but also to Mexico? The reason was clearly to undertake production (manufacturing), which in turn was used to supply the entire North American market (Hejazi and Pauly, 2003). The fact that this trend began even before the advent of continental free trade suggests that the advantages of locating in Mexico were large enough to offset the tariffs associated with exporting to the United States (and, to a lesser extent, Canada). NAFTA simply accelerated the trend.

The net impact on Canada of the rise of Mexico and the resultant migration of FDI is complex to disentangle. In general terms, the relative loss of inward FDI in the form of new production facilities means fewer domestic jobs, and hence is a negative for the Canadian economy. But to the extent that these investments are lower-value-added activities (such as product assembly) that seek to take advantage of Mexico’s low-cost (and, relative to Canada and the United States, lower-skilled) labour force, the short-run costs may give way to medium-term benefits for Canada as domestic economic activity focuses on higher-value activities such as product design and engineering.

Though the answers to this question are beyond the scope of this study, evidence suggests that the rise of Mexico will be good for Canada and the US. As Mexico develops its manufacturing infrastructure, there will be an efficient supply chain within North America, where high-value-added activities will be undertaken in Canada and the US and relatively lowvalue-added activities in Mexico. Furthermore as Mexico continues to develop, Canada will enhance its trading relationship. In 2008, Canada exported $5.8 billion worth of goods and services to Mexico, up from $2.2 billion in 2003. On the import side, Canada imported $17.9 billion in 2008, up from $12.1 billion in 2003. There are of course costs to this evolution, most notably the loss of lower-skill jobs in Canada’s manufacturing sector, but they can be addressed by targeted government programs to assist displaced workers.

If governments are to formulate effective policy, clarity is needed on factors that drive FDI. The gravity model is the most widely used model for the empirical analysis of international trade and investment.4 The core elements of the gravity model are the size of GDP and distance: the model hypothesizes that trade and FDI between countries will be higher the larger the country’s economies are, as measured by GDP, but lower the farther apart countries are from one another. For the estimation in equation 1, the focus will be on the impact of trade agreements on patterns of Canadian FDI. The model includes measures to capture changes in FDI patterns that are related to trade liberalization.

The estimating equation for FDI (inward or outward) is written as follows:

Variable definitions are as follows:

FDI = FDI to host country i from home country j (in inward model) or from home country i to host country j (in outward model) in year t

GDPHOME = real gross domestic product of home country i in year t

GDPHOST = real gross domestic product of host country j in year t

LANGUAGE = dummy variable equalling 1 if home and host countries share a common official language

DISTANCE = physical distance between home and host countries

ADJACENCY = dummy variable equalling 1 if home and host countries share a common border

XRATE = exchange rate (purchasing power parity-adjusted) between home and host countries in year t

CUSTFTA and NAFTA = dummy variables for years in which the Canada-US FTA and North American

FTA were in force

CAN = dummy variable equalling 1 for Canada

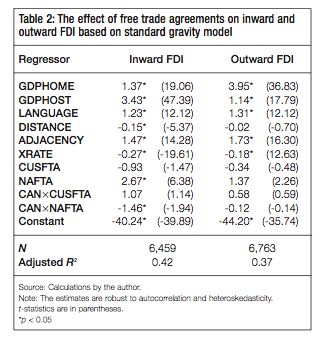

I have assembled a data set for 28 OECD countries (including of course Canada), from 1980 to 2004. It contains each country’s bilateral trade and FDI flows with each other country in the sample, as well as the other variables in the model (noted above). After excluding missing values (primarily the result of data being unavailable for country pairs whose bilateral trade and FDI flows are relatively small), the usable data set contains just under 7,000 observations.

The results in table 2 confirm the broad predictions of the basic gravity theory of trade and investment: larger home and host economies tend to have higher FDI flows (shown by the highly significant coefficients on GDPHOME and GDPHOST for both the inward and outward specifications), but these flows diminish with geographic distance (shown by the negative coefficient on DISTANCE and the positive coefficient on ADJACENCY). Additionally, sharing a common official language is, as intuition would suggest, conducive to higher levels of inward and outward FDI, since it facilitates communication.

The exchange rate is also negatively associated with both inward and outward foreign investment flows, a result which merits further examination. With regard to inward FDI, the result is unsurprising: a declining exchange rate makes a country’s assets less expensive to foreign investors, and so should encourage them to increase their investment holdings in that country. Conversely, a strengthening currency (as Canada has seen in the past several years) tends to be associated with declining inward FDI, all other factors equal, and may help explain why Canada’s inward FDI declined as a share of GDP in 2008.

By the same reasoning, one would expect a positive relationship between the bilateral exchange rate and outward FDI, but table 2 shows a negative relationship in the data. This highlights the fact that the FDI-exchange rate link is not as clearcut as one might think. For instance, to the extent that earnings from foreign investments will be repatriated to the parent company, any exchange rate advantage of investing abroad may be offset when the foreign profits are reconverted to the domestic currency. Yet another possibility is that thin capital markets and financing constraints (which, as noted earlier, likely exist in Canada) limit the capacity of multinationals to expand abroad irrespective of exchange rates. The answer to this question is beyond the scope of this study, but further work is needed to understand the net impact of exchange rates on both inward and outward FDI.

Of particular interest in the Canadian context is the role of continental free trade agreements in FDI flows. The coefficient on NAFTA is positive and statistically significant for both inward and outward FDI, meaning that, on average, FDI in both directions increased to all OECD countries after NAFTA came into force in 1994.5

One of the reasons that FDI activity among all OECD nations increased in the post-NAFTA period was due to a landmark economic agreement hammered out on the other side of the Atlantic Ocean. The Maastricht Treaty, which came into force on November 1, 1993 (just two months before NAFTA) created the European Union, which established free movement of capital within its member countries. Thus, the NAFTA variable is more accurately interpreted as the combined effect of those two landmark regional trade and investment liberalization accords.

But if we look specifically at Canada’s post-NAFTA experience with regard to inward FDI, it is worse than the average for the OECD nations in the sample (captured by the interaction term CANxNAFTA, which is negative and statistically significant). In plain English, the results imply that while overall inward FDI has increased dramatically in OECD nations since ratification of NAFTA and the creation of the European Union, Canada has not been a favourite destination.

The results are consistent with the notion that much FDI in Canada prior to NAFTA was tariffinduced rather than due to a superior domestic business and economic environment. Once the tariff walls began to fall, companies began consolidating continental operations to the detriment of investment in Canada (and to the advantage of the United States and Mexico). This explains the trends earlier in the paper that showed a secular decline in Canada’s share of intraNorth American FDI flows in the 1990s.

To provide policy guidance and focus more squarely on Canada, I now turn to a complementary model that examines how factors such as the corporate tax burden, R&D intensity, tariffs and trade agreements influence FDI flows into and out of Canada. Unlike the gravity model, this analysis uses industry-level data, allowing us to examine whether these factors affect specific industry groups to different extents.

The data underlying the model are much richer than for the gravity model. Their primary strength is the industrial detail. Foreign investment flows are available for 60 different industries from 1987 to 2002. However, information concerning some of the explanatory factors (in particular R&D intensity and the corporate tax burden) is not available at such a fine level of detail. These more aggregated data were carefully mapped to the finer FDI industries weighted by industry-level GDP (for details, see Hejazi and Pauly, 2002 and 2003). In terms of geography, the data include Canadian FDI inflows and outflows from and to all regions of the world, but for the purposes of this analysis, those flows are aggregated into two regions: the United States and the rest of the world.6

The industry-level model of FDI flows is estimated as follows:

Variable definitions:

FDI = FDI to Canada from industry i in home region j (in the inward model) or from industry i in Canada to region j (in the outward model)

TARIFF = tariff rate for industry i between Canada and region j

R&D = Canadian R&D in industry i as a percentage of industry GDP

TAXES = Canadian corporate taxes paid by industry i as a percentage of industry GDP

NAFTA = dummy variable equalling 1 for years in which NAFTA was in force

CUSFTA = dummy variable equalling 1 for years in which the Canada-US FTA was in force TRADE = total exports from Canada to the world (outward model) and imports from the world to Canada (inward model)

MFG = dummy variable equalling 1 for manufacturing industries SVC = dummy variable equalling 1 for service industries

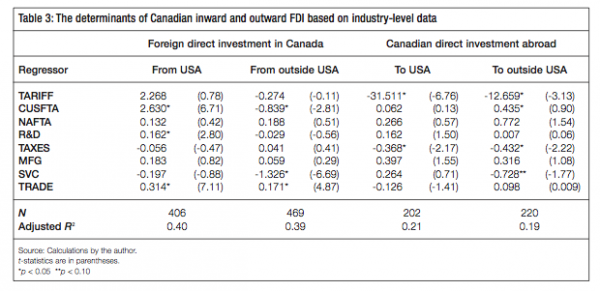

The model is estimated for Canada’s FDI to and from the US and the rest of the world. As the model described in equation 2 indicates, FDI at the industry level is related statistically to industry-level tariffs, Canada’s industry-level trade patterns, the average industry-specific corporate tax rate, industry-specific R&D intensity, as well as dummy variables to capture the impact of the CUSFTA and NAFTA and differences between manufacturing and service industries. The results are reported in table 3.

The effects of trade liberalization are captured in two distinct but related ways. The first effect is captured by the TARIFF variable, which represents US tariff rates facing the 60 industries in the sample (which vary considerably across industries and time periods).

For the inward model, tariffs have little direct effect on FDI to Canada: the coefficients on both US and non-US specifications are not statistically different from zero. The tariff-FDI link is subsumed in the relationship between inward foreign direct investment and imports.7 Essentially, the tariff-jumping effect (which would imply a decline in inward FDI as tariffs decline) roughly offsets the FDI-trade complementarity effect (which would imply an increase in inward FDI as tariffs decline and imports increase).

The outward model shows a strong negative relationship between tariffs and Canadian investment abroad, even after controlling for total Canadian exports. This implies that as US tariffs fell, Canadian multinationals increased their foreign operations. This runs counter to the notion that tariff-jumping was the primary motive for Canadian investment in the United States (or elsewhere in the world, for that matter) and suggests that Canadian firms are using outward FDI as a springboard to expand their reach in foreign markets.

However, free trade agreements go well beyond simple tariff reductions: they permit freer movement of capital and provide protections for foreign investment from treaty partners (known as “national treatment”). The CUSFTA and NAFTA variables capture these changes, and CUSFTA in particular had a significant impact in foreign direct investment in Canada. The positive significant coefficient for FDI from the United States suggests that US firms took advantage of these provisions.

Canadian FDI from outside the United States is, by contrast, negatively affected by the advent of the Canada-US FTA (shown by the negative significant coefficient of CUSFTA in the non-US specification), which suggests that non-US multinationals are generally serving the Canadian market by locating production facilities in the United States and exporting finished goods to Canada.

Tariff reductions alone would predict a reduction in FDI stocks as countries consolidate production to capture economies of scale. However, in reality, tariff reductions were part of a larger vision of continental trade and investment liberalization that enhanced market access and allowed for a disintegration of production networks globally. The results here, while nuanced, generally indicate that any tariff-induced reductions in FDI were overwhelmed by the expansion of trade and investment flows brought on by the globalization of supply chains that the broader free trade agreements enabled.

With regard to the effect of corporate tax rates on FDI, the results run counter to conventional wisdom. The coefficients on TAXES are statistically insignificant for inward FDI originating from the Unites States as well as other countries. It is commonly believed that low corporate tax rates are an important factor in attracting foreign firms to Canada, and that was one of the motivations for the continued reduction in Canada’s corporate tax rate.8 There are certainly many good reasons for low corporate tax rates (such as increased investment, jobs and wages), but this analysis shows that they are unlikely to attract large amounts of additional foreign direct investment.

The results for Canadian direct investment abroad also run somewhat counter to intuition. One might think that high domestic corporate tax rates would encourage Canadian companies to move production facilities abroad to escape an unfavourable fiscal environment, which would imply a positive coefficient on TAXES for the outward model. But the coefficient is negative and statistically significant, meaning higher tax rates in Canada are associated with less, not greater, FDI abroad. Lower tax rates appear to encourage Canadian companies to expand their foreign operations rather than move them back to Canada.

The results are more consistent with the notion that the domestic corporate tax rate affects the overall competitive posture of Canadian firms, and hence their ability to expand in foreign markets (as well as prosper at home). By this reasoning, lower tax rates improve the profitability of firms, which are then able to use these additional resources to develop new markets in other countries, while a higher tax rate reduces this capacity. The results here are suggestive rather than conclusive on this point, and more work is required to understand how domestic corporate tax rates affect the foreign investment decisions of Canadian firms.

Policy-makers tend to regard inward foreign direct investment as a source of innovation. As noted earlier, foreign firms (of which the large majority are American) tend to be more technology-intensive and innovative than their Canadian counterparts. While they do not perform large amounts of R&D themselves, they do import and use the fruits of the R&D performed by their parent companies, and these technologies spill over to Canadian firms. By this reasoning, technology transfer from FDI and domestic R&D are sometimes viewed as substitutes: as long as Canada is successful in attracting technology-intensive foreign firms and adopting innovations developed abroad, it need not worry too much about under-investment in domestic R&D.

The results in table 3 cast considerable doubt on this contention. There is a statistically significant positive link between Canadian R&D intensity and inward FDI originating in the United States, which implies that domestic R&D intensity is a complement to inward FDI rather than a substitute. This highlights the importance of a strong research base. Spillovers from R&D and technology work in both directions, and one of the attractions of locating in a researchintensive country is to benefit from the fruits of its R&D activities.

With regard to domestic R&D’s impact on foreign investment abroad, international business theory suggests that R&D is an important element of developing firm-specific competitive advantages that can then be exploited in foreign markets, either through trade flows or foreign investment. Research In Motion is a classic example: the pioneering technology powering its BlackBerry led to the creation of (and domination of) the market for smart phones. As of late 2009, the BlackBerry had a 20-percent global market share (number 2 behind Nokia) and in North America it is number 1 with a 50-percent share, despite the arrival of the Apple iPhone as a new competitor. RIM has chosen to access global markets largely via exports: other than small operations in Texas and the United Kingdom, its facilities are located exclusively in Canada. The empirical results in Table 3 suggest that this dynamic is the rule rather than the exception for Canadian firms, since there is no statistically significant industry-level relationship between Canadian foreign direct investment abroad and R&D intensity.9

As noted earlier in the paper, there is a large empirical literature that documents a complementary relationship between trade and foreign direct investment, and those complementarities are evident with respect to Canada’s inward FDI, especially from the United States. The coefficient on TRADE (which is the log-level of imports in the inward model) is positive, meaning that industryspecific inward FDI and trade move together. This is entirely consistent with the fragmentation of supply chains that trade liberalization has enabled. US firms operate Canadian affiliates to serve continental markets (which raises inward FDI), but these affiliates source their components from US firms as well as suppliers located outside North America (which increases Canadian imports).

With regard to Canada’s direct investment abroad, this complementarity is not as evident. The coefficient on TRADE (which represents exports in the outward model) is negative for the United States, although it is only statistically significant with 85 percent confidence. This implies that, if anything, US-bound FDI is substituting for exports, suggesting that Canadian firms are less predisposed to develop continent-wide fragmented supply chains than their American counterparts. It may also be the case that the costs of exporting to the US even after the fall of trade barriers (particularly those associated with crossing the border) are high enough to warrant selling into the US market via foreign affiliates rather than exports. The heightened border security measures put into place by the United States since 2001 have likely raised these costs, but the data in this analysis end in 2002, and thus cannot answer this question.

In contrast, the results indicate a weak complementarity between Canadian outward FDI to destinations other than the United States and exports: the coefficient on TRADE is positive but statistically insignificant. The fact that the relationship is not negative is reassuring, because it means that when Canadian firms invest abroad, there is no corresponding decrease in domestic exports. This evidence runs counter to the notion that investment abroad is synonymous with offshoring economic activity and jobs.

The manufacturing and service regressors show how, if at all, FDI flows differ across broad industry groups. Since they are dummy variables, they measure the degree to which FDI from each sector differs significantly from the sector of reference (which in the analysis is the natural resources sector), all other factors being equal. The only marked difference is in the service sector, which receives significantly less FDI from non-US destinations and is the source of significantly less Canadian investment destined for regions outside the United States. This is not surprising, since there are important statutory restrictions on foreign ownership in several large service sectors (most notably banking and finance and telecommunications).

It is clear that North American trade liberalization has transformed the structure of production in Canada, the US and, since ratification of NAFTA in 1994, Mexico. Tariff reductions have enabled firms to operate with a full continental vision, as opposed to a Canadian one, by allowing them to consolidate and operate far more efficiently. The decline in Canada’s share of North American FDI over the past 15 years is a direct consequence of this transformation: less efficient American affiliate plants in Canada were closed and operations were consolidated in the US. Of course, there were instances where Canadian plants were more efficient than their US counterparts, and some firms did use trade liberalization to profitably expand production in Canada. But the analysis in this paper strongly indicates that the former effect dominated: that is, on a net basis, free trade decreased the attractiveness of Canada as a destination for foreign direct investment. At the same time, however, Canadian exports expanded rapidly, leading to growth in domestic investment and employment, which partially offset the negative effects related to lost FDI.

The same dynamic extends to non-North American firms, which no longer need to operate three foreign affiliates to service the North American market. In relative terms, Canada has become a smaller player in North America generally: its share of total inward FDI to the NAFTA countries has fallen from almost 40 percent in 1980 to less than 20 percent today.

Notwithstanding a vocal minority that argues that the encouragement of inward FDI amounts to putting Canada’s economic destiny at the mercy of foreigners, the benefits of foreign investment far outweigh any real or imagined drawbacks. Empirical evidence has consistently show that the presence of foreign affiliates in Canada has positive effects on domestic job growth and, more importantly, contributes to the diffusion of innovation and technology to domestic firms. In addition, though the stock of inward FDI did increase somewhat as a share of GDP in the 1990s, it has held steady since then at just over 30 percent – the same share as in 1970.

Now that Canada cannot depend on trade barriers to attract FDI motivated by tariff avoidance, policy-makers must look to other factors that are conducive to both inward and outward direct investment. As a general principle, the role of government should be to assure the necessary elements (such as a high-quality labour force and infrastructure, stable and predictable macroeconomic environment and strong rule of law and enforcement of contracts) are in place so that domestic and foreign firms can compete on an equal footing, thus optimizing foreign investment flows in both directions. Efforts to further restrict inward FDI in order to “protect” Canadian firms from being taken over by profitable foreign competitors sidestep the more fundamental question of why the Canadian firms are in need of “protection” and the underlying reasons for that situation.

The industry-level empirical analysis in this paper refutes some commonly held assumptions about the drivers of FDI that have important implications for policy development. With regard to corporate tax rates, there is no statistical relationship between industry-specific Canadian corporate tax rates and inward FDI, suggesting that, while the steady reduction in statutory rates since 2001 may bring about a more competitive business environment, they are unlikely in and of themselves to spur large inflows of FDI. On the other hand, lower corporate taxes do have a strong positive effect on Canadian direct investment abroad (a sign of strong international competitiveness), which suggests that a lighter corporate tax burden is one of the factors that reduces the need to “protect” domestic firms from foreign competitors.

A second important finding is that domestic R&D and inward FDI are complements rather than substitutes. While it is true that one of the main benefits of inward FDI (particularly from the United States) is the technology transfer that ultimately spills over to Canadian companies, Canada’s domestic R&D intensity is an important driver of inward FDI. This symbiotic relationship dispels the myth that Canada can “free-ride” off foreign (largely US) research and innovation to offset any shortcomings in its domestic innovation efforts, and only reinforces the conclusions of the recent reports on improving Canada’s innovation and R&D infrastructure (Committee on the State of Science and Technology in Canada 2006; Expert Panel on Business Innovation 2009).

There has been a surge in Canadian FDI abroad in recent years, and the free trade agreements have clearly contributed to this trend. These outward investments can be broken down into two types: firms that are forced out of Canada because of a poor domestic competitive environment, high taxes or low R&D, and firms that expand abroad to exploit firm-specific advantages, and hence represent Canadian success stories. The results presented here indicate that although some of each occurred in the 1990s, the latter effects have dominated: that is, the surge in Canadian FDI abroad has brought benefits to the domestic economy.

Canada is and will always be a trading nation, and foreign investors will continue to play an important role in the domestic economy. But by the same token, Canadian firms are increasingly important players in foreign economies, and with the right policies in place, Canadian firms will have nothing to fear from the increasing globalization of the economic marketplace.

Anderson, J. E. 1979. “A Theoretical Foundation for the Gravity Equation.” American Economic Review 69: 106-16.

Baldwin, J. R., and M. Brown. 2005. “Foreign Multinationals and Head Office Employment in Canadian Manufacturing Firms.” Economic Analysis Research Paper Series, no. 034, cat. no 11F0027MIE, Statistics Canada

Baldwin, J.R., and W. Gu. 2005. Global Links: Multinationals, Foreign Ownershipand Productivity Growth in Canadian Manufacturing. Canadian Economy in Transition Series, cat. no. 11-622-MIE2005009. Statistics Canada.

Beckstead, D., and W. M. Brown. 2006. “Head Office Employment in Canada, 1999 to 2005.” Insights on the Canadian Economy, no. 014. Statistics Canada, cat. no. 11-624-MIE.

Bergstrand, J. H. 1985. “The Gravity Equation in International Trade: Some Microeconomic Foundations and Empirical Evidence.” Review of Economics and Statistics 67: 474-81.

——————. 1989. “The Generalized Gravity Equation, Monopolistic Competition, and the Factor Proportions Theory of International Trade.” Review of Economics and Statistics 71: 143-53.

——————. 1990. “The Heckscher-Ohlin-Samuelson Model, the Linder Hypothesis and the Determinants of Bilateral Intraindustry Trade.” Economic Journal 100 (403): 1216-29.

Bloom, M. 2008. “Hollowing Out: Myth and Reality.” Presentation to the International Trade and Investment Centre, January 2008. Accessed January 6, 2010. https://www.conferenceboard.ca/Libraries/ITIC_PUBLIC/ HollowingOut_MichaelBloom.sflb

Bloom, M., and M. Grant. 2008. “Hollowing Out”– Myth and Reality: Corporate Takeovers in an Age of Transformation. Ottawa: Conference Board of Canada.

Brainard, S. L. 1997. “An Empirical Assessment of the Proximity-Concentration Trade-off between Multinational Sales and Trade.” American Economic Review 87 (4): 520-44.

Coe, D., and E. Helpman. 1995. “International R&D Spillovers.” European Economic Review (May): 859-87.

Committee on the State of Science and Technology in Canada. 2006. The State of Science and Technology in Canada. Ottawa: Council of Canadian Academies.

Deardorff, A. V. 1998. “Determinants of Bilateral Trade: Does Gravity Work in a Neoclassical World.” In The Regionalization of the World Economy, edited by J. A. Frankel. Chicago, IL: University of Chicago Press.

Dobson, W. 2002. “Shaping the Future of the North American Economic Space: A Framework for Action.” C.D. Howe Institute Commentary 162 (April).

Expert Panel on Business Innovation. 2009. Innovation and Business Strategy: Why Canada Falls Short. Ottawa: Council of Canadian Academies.

Feenstra, R. C., J. R. Markusen, and A. K. Rose. 2001. “Using the Gravity Equation to Differentiate among Alternative Theories of Trade.” Canadian Journal of Economics 34 (2): 430-47.

Finance Canada. 2006. Advantage Canada: Building a Strong Economy for Canadians. Ottawa: Finance Canada. Accessed January 21, 2010. https://www.fin.gc.ca/ec2006/pdf/ plane.pdf

Golub, S. S. 2003. “Measures of Restrictions on Inward Foreign Direct Investment for OECD Countries.” Working paper no. 357, Economic Department, Organisation for Economic Co-operation and Development.

Head, K., and J. Ries. 2004. “Judging Japan’s FDI: The Verdict from a Dartboard Model.” Working paper, University of British Columbia.

Hejazi, W. 2007. “Offshore Financial Centres and the Canadian Economy.” University of Toronto working paper, February. Accessed January 6, 2010. https://www.rotman.utoronto. ca/f acbios/file/Hejazi%20Barbados%20Study%20Rotman %20Website.pdf

Hejazi, W., and P. Pauly. 2002. “Foreign Direct Investment and Domestic Capital Formation.” Working paper no. 36, Industry Canada.

——————. 2003. “Motivations for FDI and Domestic Capital Formation.” Journal of International Business Studies 34: 282-9.

Hejazi, W., and A. E. Safarian. 1999a. “Modeling Links Between Canadian Trade and Foreign Direct Investment.” Perspectives on North American Free Trade, no. 2, Industry Canada.

——————. 1999b. “Trade, Foreign Direct Investment, and R&D Spillovers.” Journal of International Business Studies 30 (3): 491-511.

——————. 2001. “The Complementarity between U.S. FDI Stock and Trade.” Atlantic Economic Journal 29 (4): 420-37.

——————. 2004a. “Explaining Canada’s Changing FDI Patterns.” Working paper, University of Toronto.

——————. 2004b. “NAFTA Effects and the Level of Development.” Working paper, University of Toronto.

Institute for Competitiveness and Prosperity. 2008. “Flourishing in the Global Competitiveness Game.” Working paper 11. Accessed January 8, 2010. https://www.competeprosper.ca/ images/uploads/WP11.pdf

Leamer, E. E. 1974. “The Commodity Composition of International Trade in Manufactures: An Empirical Analysis.” Oxford Economic Papers 26: 350-74.

Lipsey, R. E., and M. Y. Weiss. 1981. “Foreign Production and Exports in Manufacturing Industries.” Review of Economic Statistics 63 (4): 488-94.

—————–. 1984. “Foreign Production and Exports of Individual Firms.” Review of Economics and Statistics 66 (2): 304-8.

Organisation for Economic Co-operation and Development. 2005. Measuring Globalisation: OECD Economic Globalisation Indicators. Paris: OECD.

Rao, S., A. Ahmad, and C. Barnes. 1996. “Foreign Direct Investment and APEC Economic Integration” Working paper no. 8, Industry Canada.

Rose, P. 2008. “Sovereign Wealth Funds: Active or Passive Investors?” 118 Yale L.J. Pocket Part 104. Accessed November 13, 2009. https://www.yalelawjournal.org/content/ view/725/23/

Safarian, A. E. 1993. Multinational Enterprise and Public Policy: A Study of the Industrial Countries. United Kingdom and United States: Edward Elgar.

Safarian, A. E., and W. Hejazi. 2001. Canada and Foreign Direct Investment: A Study of Determinants. Toronto, ON: Centre for Public Management, University of Toronto.

Statistics Canada. 2009. “Activities of Foreign Affiliates.” The Daily, July 9, 2009. Accessed January 13, 2010. https://www.statcan.gc.ca/daily-quotidien/090709/ dq090709c-eng.htm

Tang, J., and S. Rao. 2001. “R&D Propensity and Productivity Performance of Foreign-Controlled Firms in Canada.” Working paper 33, Industry Canada.

Trefler, D. 2004. “The Long and Short of the Canada-U.S. Free Trade Agreement.” American Economic Review 94 (4): 870-95.

van Pottelsberghe de la Potterie, B., and F. Lichtenberg. 2001. “Does Foreign Direct Investment Transfer Technology Across Borders?” Review of Economics and Statistics 83 (3): 490-7.

World Economic Forum. 2008. The Financial Development Report 2008. Geneva: The Forum.

This publication was published as part of the Competitiveness, Productivity and Economic Growth research pro- gram under the direction of Jeremy Leonard. The manuscript was copy-edited by Barbara Czarnecki, proofreading was by Zofia Laubitz, editorial coordination was by Francesca Worrall, production was by Chantal Létourneau, art direction was by Schumacher Design and printing was by AGL Graphiques.

Walid Hejazi is professor of international competitiveness; teaches in the MBA, executive MBA and custom exec- utive programs; and is academic director of international programs at the University of Toronto’s Rotman School of Management. He has worked extensively with the Canadian and with foreign governments on international trade, foreign direct investment and international competitiveness, and has published extensively in leading academic and business journals. Recent studies (2008) include “Assessing the Costs and Benefits of a Closer Canada-EU Economic Partnership” (Canada-EU summit), and “Foreign Direct Investment and the Canadian Economy” (Competition Policy Review Panel Secretariat).

To cite this document:

Hejazi, Walid. 2010. “Dispelling Canadian Myths about Foreign Direct Investment.” IRPP Study, No. 1.