Canadian Policy Prescriptions for Dutch Disease

Robin Boadway, Serge Coulombe and Jean-François Tremblay

With hindsight, the 2009 federal-provincial bailout of GM Canada and Chrysler Canada was a smart one-time move: the companies were able to restructure, become profitable and ultimately repay a significant portion of the bailout funds. However, continuing support of the auto sector via project-based subsidies (about $1.4 billion of which have been awarded since 2004) must be carefully reassessed, especially in a time of tight government budgets.

In this study, Leslie Shiell and Robin Somerville examine the economic rationale for industry subsidies and whether they are a cost-effective way to foster economic development in Canada’s auto sector.

They paint a mixed picture. They find that the bailout of GM Canada and Chrysler Canada was cost-effective in that the cost to the federal and Ontario governments ($14.4 billion) was substantially less than the economic losses that would have occurred without the bailout – about $20 billion, of which almost two-thirds would have been borne by Ontario). They find similar positive results for project-based subsidies, but caution that this does not mean that subsidies are the best way to support auto investment.

Shiell and Somerville argue that because auto workers earn a significant pay premium over similarly skilled workers in other manufacturing industries, subsidies to the auto manufacturers are in fact subsidizing above-market wages. Furthermore, they must be financed by distortionary taxes, whose burden falls on taxpayers, many of whose wages are lower than those of auto workers. Modest concessions on wages would obviate the need for governments to use project-based subsidies to attract new investment in the auto sector. However, in the case of the 2009 bailout, the wage concessions would have been too large to be justified, and for this reason government support was warranted.

The authors thus recommend that governments require competitive wages as a condition for a subsidy for the auto sector as well as for all other industries. This would discourage political manipulation of subsidies and make sure that the direct beneficiaries of new investment projects – the workers who are employed on them – contribute to attracting these projects to Canada.

In a commentary, Jim Stanford, an economist with the Canadian Auto Workers, strongly disagrees with the notion that wage concessions should be a precondition for auto subsidies. He points out that auto-sector wage premiums in Canada are comparable to those in the US and other auto-producing countries, and argues that they are justified because of the workers’ contribution to productivity. Trying to cut wages in the name of attracting investment would, in his view, be self-defeating.

For many Canadians, 2009 may be remembered as the year of the bailout –– the year the federal and Ontario governments spent more than $14 billion1 to rescue the Canadian operations of General Motors and Chrysler. At times, during the months of March, April and May of that year, it seemed as if there were a high-stakes poker game going on involving government, auto workers and the companies, with the whole country watching. Yet the bailout of 2009 was just another phase in a long-running drama concerning the role of government assistance to the automotive sector. Since 2004, the Ontario and federal governments have engaged in a largescale program of public subsidies for specific investment projects in the auto sector. Given the scale of this involvement, it is surprising to note that there has been very little objective analysis in the public domain that could help Canadians assess the effectiveness of either the bailout or project-based subsidies. This study is designed to fill that gap.2

Developments for the bailout recipients have turned decidedly positive since they emerged from bankruptcy. GM turned a profit in 2010 and 2011, following five consecutive years of losses between 2005 and 2009 (GM 2011). The company completed a successful return to the equity market in November 2010. As a result, the US government was able to divest itself of US$11.8 billion worth of shares, and the Canadian and Ontario governments of just over US$1 billion worth of shares. In addition, in April 2010, GM repaid US$9.5 billion in loans to the US government and US$1.3 million in loans to the Canadian and Ontario governments (Keenan and Won 2010). As for Chrysler, in 2011 it posted its first full-year profit since emerging from bankruptcy (Chrysler Group LLC 2012). Further, in May 2011, the company repaid US$7.5 billion in loans to the US, Canadian and Ontario governments (Keenan 2011c).

As a result of these developments, the case for the bailout appears stronger now than it did during the tumultuous spring of 2009. Our intention, however, is not to assess the bailout and subsidy policies in hindsight but to determine whether they represented good policy choices at the time they were made, given the information that policy-makers had at their disposal. For that reason, we have relied only on sources that were available in spring 2009.

We use cost-benefit analysis as our primary tool for assessing the bailouts and subsidies. Costbenefit analysis is designed to rank alternative policy scenarios by calculating the net benefit (total benefit less total cost) of each scenario. The scenario that yields the largest net benefit is deemed to be the superior choice among the set of alternatives considered. Therefore, the choice of the set of alternatives is of utmost importance. Frequently, cost-benefit analysis is conducted for only two alternatives: a new policy under consideration and the status quo. While common, this practice yields a very limited result: either the new policy is deemed to be superior to the status quo or vice versa. This approach cannot reveal which is the best policy choice overall for the economy; that determination requires comparing a very large number of alternative scenarios, which usually is not possible within the limited means available at a given time. Nonetheless, the lesson for policy-makers is that there is significant value in considering multiple alternatives, and typically researchers must rely on their experience of the field to narrow down the list of potential alternatives to make the task manageable.

In our case, we proceed in a two-step fashion. First, we compare the bailouts and subsidies with a hypothetical alternative in which the affected activity is lost. Thus, we compare the GM and Chrysler bailouts, whereby governments provided funding to keep the companies open, with the alternative of the companies closing their operations in Canada. Similarly, we compare the government provision of subsidies to particular investment projects with the alternative of those investments going to other jurisdictions. We use the Centre for Spatial Economics’ Provincial Economic Modeling System to perform these comparisons.

At this step, we conclude that, as structured, the bailouts and the subsidies we consider represented better choices than the alternatives of losing the associated activity – the economic costs of the closure of GM’s and Chrysler’s Canadian operations in 2009 would have far outweighed those incurred by the federal and Ontario treasuries in providing the funding.

In our second step, we compare the bailouts and subsidies with an alternative in which the affected workers provide a greater share of the investment incentive, through concessions in pay. We argue that many Canadian automotive workers (assembly workers, especially) enjoy a significant premium in pay above the competitive level for similar skills and experience. For such workers, concessions in pay do not affect the decision of how much and where to work, and therefore it is analytically sound to consider investment incentives in the form of workers’ concessions. In addition, a key feature of government subsidies is that they must be financed through distortionary taxation; in contrast, pay concessions transfer funds to the companies without any additional distortions. It follows that economic efficiency would have been enhanced if automotive workers had made such concessions, thereby reducing the size of the subsidies by an equivalent amount.

For the suite of project-based subsidies since 2004, we show that it would have been possible to replace the entire value of subsidies – approximately $1.4 billion between the two levels of government – with relatively modest concessions in pay. In contrast, the workers’ pay premium was not large enough to fund the entire gross cost of the bailouts of GM and Chrysler – $14.4 billion. Nonetheless, we estimate that the pay premium was large enough to fund roughly $6 billion through concessions, which would have significantly reduced the governments’ net exposure.

We believe that, in addition to improving efficiency, concessions on pay would have been more equitable than subsidies since average compensation among auto workers exceeds the national average income and thus the income of the average taxpayer. In effect, using subsidies to relieve auto workers of the need to make concessions has the effect of redistributing tax dollars upward to families with above-average incomes. We also argue that such concessions would have improved the sustainability of the Canadian automotive sector, as globalization and an increase in the value of the Canadian dollar have led to increased competition from the United States, Mexico and China for new automotive investments.

Both economic theory and experience indicate circumstances in which the subsidization of internationally mobile private investment can improve social welfare. Nonetheless, it is always preferable to reduce the scale of subsidies required to secure an investment in order to reduce the distortionary effects of the associated taxation. Of course, it is one thing to argue that workers’ concessions would have been preferable to subsidies and quite another to persuade workers to agree to concessions. With this in mind, we provide two recommendations for policy-makers. First, the external benefits of an investment project should be identified, quantified and debated before a subsidy is granted. Second, competitive labour compensation should be required as a precondition for subsidies. Our analysis indicates that both efficiency and equity could have been improved during the past decade if these conditions had been satisfied in the Canadian auto industry.

These issues seem particularly relevant in light of the importance of the automotive sector in Canada, and Ontario especially. In 2009, this sector accounted for 10 percent of Canada’s manufacturing output, 7 percent of its manufacturing employment and 11 percent of its total exports. Moreover, while Canada accounted for only 12 percent of North American new vehicle sales in 2009, it accounted for 17 percent of total North American production of motor vehicles (Industry Canada 2010). Nonetheless, in the final analysis, this story is not about the auto industry per se but about subsidy policy in general. As a consequence, the lessons we derive are relevant to any industry in which large-scale subsidization meets organized interest groups. Other examples include aerospace (Milke 2010) and the aluminum industry (Bélanger and Bernard 2007).

In light of the restrained growth expectations Ontario faces for the foreseeable future, as predicted recently by the Drummond Report (Drummond et al. 2012); now more than ever it is essential that government revenues be used as efficiently as possible. To that end, we believe that our recommendations could improve efficiency in a wide range of industrial support programs in all sectors, not just the automotive sector.

As the backdrop for our analysis, we assume that, in the United States, the Obama administration would have bailed out GM and Chrysler globally, regardless of the decisions of the Ontario and Canadian governments. Therefore, the issue for both Queen’s Park and Ottawa was not whether the companies survived globally, but whether they continued their operations in Canada. We think it is fair to assume that, if Canadian governments had not participated in the bailout, the companies would have faced overwhelming pressure to close their Canadian operations and relocate employment to the United States or elsewhere. This belief is not unique – indeed, it was expressed by Prime Minister Stephen Harper in a June 1, 2009 news conference regarding the assistance to GM (Office of the Prime Minister 2009c).

This assumption takes off the table a number of “what-ifs” concerning the effect of the bailout on other auto makers in Canada. In particular, since we are talking about relocation rather than the cessation of GM’s and Chrysler’s production, there is no question of whether other Canadian-based manufacturers (Ford, Toyota or Honda) would have been able to pick up extra market share. Similarly, we do not consider the possibility of a collapse of the Canadian auto parts sector which could have impeded production at other companies, a scenario that McAlinden, Menk, and Cooper (2009) model in the context of a global closure of GM and Chrysler. However, our modelling does account for reduced output of domestic supplier companies as a result of the closure of GM’s and Chrysler’s Canadian operations.

Our analysis also highlights the Ontario government’s vulnerability to large private sector pension liabilities through its Pension Benefits Guarantee Fund (PBGF). Bankruptcy filings by GM Canada and Chrysler Canada almost certainly would have led to claims on the PBGF totalling approximately $4.9 billion, dwarfing the fund’s resources by almost two orders of magnitude. The lesson we take is that, when it was most needed, the PBGF was not adequate to the task;3 as a consequence, Ontario taxpayers found themselves effectively liable to make up large shortfalls in corporate pension plans. While it is not our main focus, we nonetheless hope that this experience will serve as a catalyst for a debate among Ontarians about the future of the PBGF, as well as an example to other jurisdictions that may be contemplating public guarantees of private sector pensions (see Davis [2011]).

We begin our analysis with a theoretical discussion of the economics of subsidies. We then apply the concepts to the bailout of GM and Chrysler and the ongoing program of projectbased subsidies. We present the analysis in reverse chronological order – first bailout, then project subsidies – in order to exploit some important lessons from the macroeconomic modelling of the bailout in our assessment of the smaller-scale projects.

The simple argument that investment brings jobs does not provide a compelling rationale for subsidies on its own. Rather, to justify government intervention, there must be some imperfection in the market that can be corrected, or some benefit that is not fully priced and is therefore ignored by private actors. These benefits are referred to collectively as “positive externalities” of the investment. Van Biesebroeck (2010, 536-8) identifies five such positive externalities:

To this list of economic justifications for subsidies, we would add the concepts of debtor-in-possession (DIP) financing, the social costs of adjustment and interindustry productivity differentials:

As Van Biesebroeck (2010) notes, however, there are many caveats for policy-makers who are contemplating getting into the subsidy game. First, tax and regulatory distortions are ubiquitous, and therefore it would be more efficient to reduce them directly, for the benefit of all firms, rather than providing targeted subsidies for only a few. In the Canadian context, the federal and many provincial governments have reduced business taxes in the past decade through, for example, reductions in corporate income taxes and the harmonization of federal and provincial sales taxes. These changes have increased the benefit to firms of operating in a particular jurisdiction and have therefore reduced the need for subsidies.

Second, regarding the argument of rent capture by local workers, Van Biesebroeck observes that net benefits for the locale are reduced to the extent that they are “purchased” with subsidies. Stated differently, rent (extra profit) captured by workers is transferred back to the firms in proportion to the subsidies that governments pay. To this observation, we would add that the North American auto industry has not behaved as an oligopoly for at least the past decade and, as a result, there has been little rent to capture, especially at GM, Ford and Chrysler.

As a third caveat, Van Biesebroeck argues that subsidies likely will be inefficient if locations that benefit from the investment succeed at passing on the costs to higher levels of government, which do not benefit to the same degree. For example, in the context of the auto industry, local players and the Ontario government together frequently have persuaded the federal government to provide subsidies, even though such subsidies probably represent a loss for some federal taxpayers.

Fourth, Van Biesebroeck points to the reputational effect of being known as a jurisdiction that offers subsidies. In such a jurisdiction, all firms have an incentive to structure their operations so that they qualify for subsidies, even if they would not otherwise have relocated. In this soft-onsubsidies jurisdiction, government expenditure increases dramatically, without any significant impact on economic activity. Moreover, in such a jurisdiction, politicians also have an incentive to manipulate the process to buy votes in specific communities, irrespective of economic fundamentals. Van Biesebroeck cites the case of the Harper government’s reversing its opposition to investment subsidies on the eve of the October 2008 federal election. To this example, we would add the case of a $13.9 million subsidy, announced in April 2008 by the Ontario government, for the pharmaceutical firm Sanofi Pasteur. In an interview, the firm’s chief executive officer stated the facility would have been built in Ontario even without the subsidy (Blackwell 2008).

To Van Biesebroeck’s list, we add three caveats of our own about the use of subsidies. First, investment subsidies are financed in the final analysis by distortionary taxes, which entail costs over and above the value of the subsidies. Economists say a tax is distortionary if, by giving a distorted impression of prices, it prompts agents to make less desirable choices about work, savings, consumption or investment than they would otherwise. For example, an increase in the personal income tax reduces the after-tax wage, which discourages work effort and production (in most cases). Therefore, there is a cost to this tax over and above the value of the revenue transferred from households to the government.

Economists measure the distortionary effect of taxation in terms of a concept called the marginal cost of public funds (MCPF).5 For the federal government, Dahlby and Ferede (2011) estimate that the MCPF equals 1.71 for corporate income tax, 1.17 for personal income tax and 1.11 for sales tax (whether goods and services tax or harmonized sales tax), where a value greater than 1 indicates that one dollar of tax revenue costs society more than one dollar in total, due to the distortionary effect of the tax. For example, for every dollar of corporate income tax revenue the federal government raises, an additional 71¢ of value is lost in the economy due to the distortionary effect of the tax.

The fact that taxation involves a distortionary effect means that the cost of a subsidy (or any other government expenditure) is greater than its face value. Using an MCPF of 1.71 as an example, we see that $100 of subsidy implies a total cost to society of $171. If the subsidy results in benefits in excess of $171, then it yields a positive net benefit for society, but if the benefits fall short of $171, then the net benefit is negative, and the subsidy represents a poor policy choice. (The same analysis applies to any type of government expenditure.) Thus, distortionary taxation requires that government spending be held to a higher standard than otherwise.

Our second caveat is that the use of subsidies to procure private benefits for stakeholders – for example above-market pay levels – can raise important issues regarding equity. In particular, using subsidies to procure benefits for stakeholders with above-average incomes violates the principle of vertical equity if it involves transferring resources from taxpayers with average or below-average incomes. Vertical equity holds that individuals with higher incomes should contribute proportionately more to a public endeavour than individuals with lower incomes. A policy that satisfies this principle is said to be progressive, while a policy that violates it is regressive.

Our third caveat about subsidies relates to the effect of globalization on the expected level of benefits that can be extracted from high-productivity industries. Productivity levels of such industries might not be related to indigenous features associated with the locale, such as labour, but might reflect superior technology or management practices that have been developed elsewhere. In such a case, high-productivity industries might have little attachment to a particular locale, especially with increased globalization of economic activity. As a result, we expect competition between jurisdictions for investment by such firms to increase over time, leading to increased demands by firms for investment subsidies.

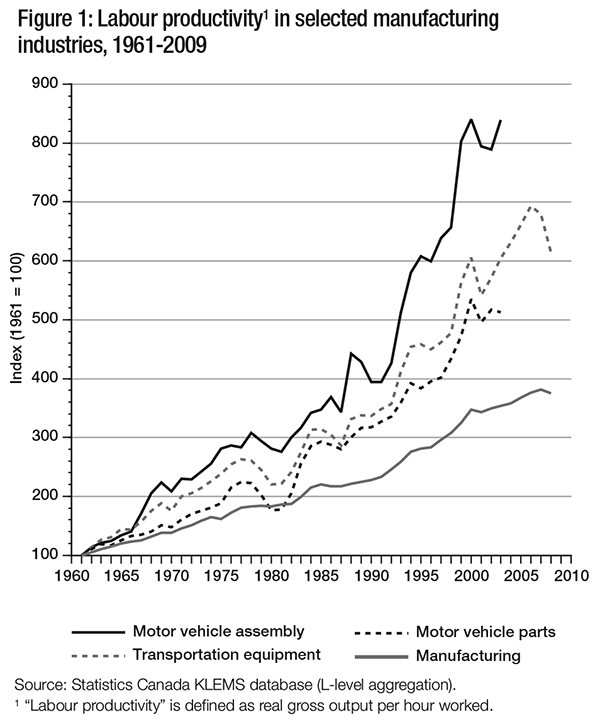

The automotive industry likely falls into this category. Figure 1 confirms that the Canadian automotive industry has indeed exhibited elevated levels of labour productivity growth over the past 45 years. Motor vehicle assembly, in particular, has shown consistently higher labour productivity growth during this period than the rest of the transportation equipment manufacturing subsector, the motor vehicle parts industry or the Canadian manufacturing sector as a whole. In addition, industry monitors such as Harbour Consulting and J.D. Power and Associates frequently credit individual Canadian plants with high ratings in terms of labour productivity and other quality measures (Stanford 2008; Industry Canada 2011).

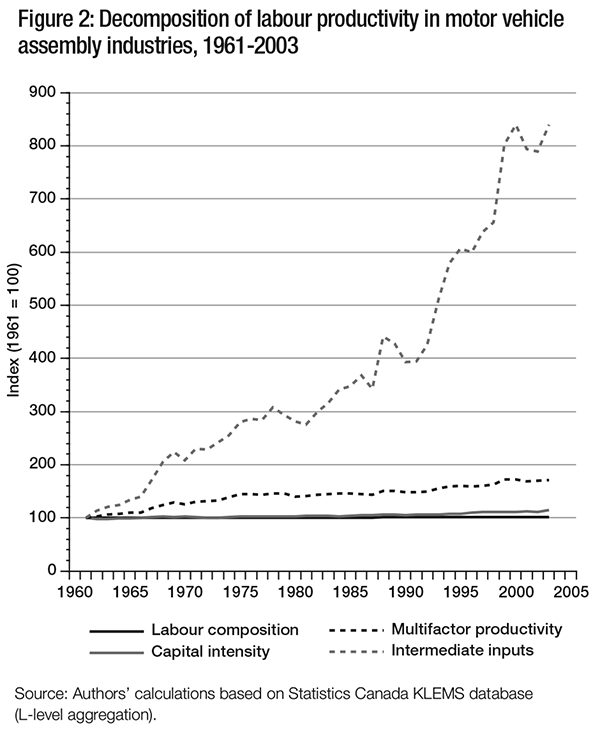

When this growth is decomposed into its component parts, however, as in figure 2, we see that most of it is due to increases in the intensity of use of intermediate inputs, followed in distant second place by growth in multifactor productivity, which is a proxy for technical change. In contrast, the contributions of changes in capital intensity and labour composition to labour productivity growth are very minor. Labour composition measures increases in educational attainment and work experience per hour worked. Therefore, increasing labour quality has not proven to be an important factor in productivity growth in motor vehicle assembly over the past 45 years.6 Similar results are obtained for the motor vehicle parts industry, transportation equipment manufacturing and the manufacturing sector as a whole (not shown). See appendix 1 for a statement regarding the sources of the productivity data.

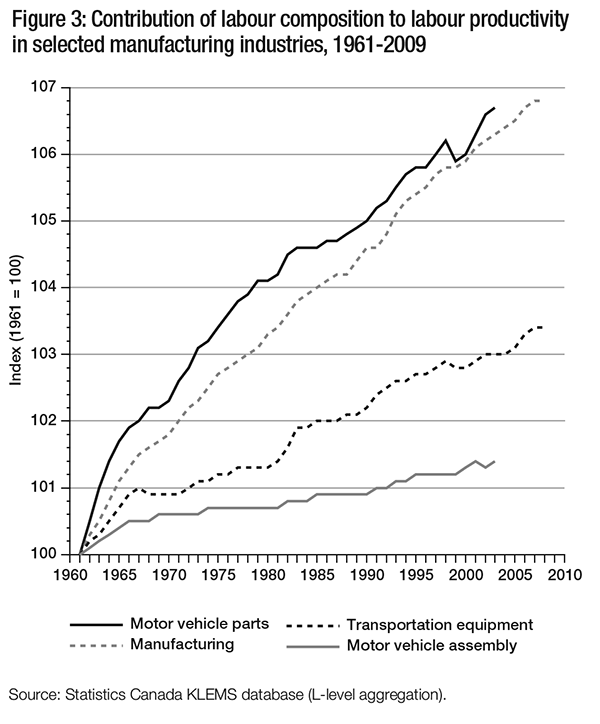

In fact, as figure 3 indicates, in Canada, the motor vehicle assembly industry has lagged behind the motor vehicle parts industry, the aggregate manufacturing sector and transportation equipment manufacturing in terms of productivity growth due to changes in labour composition. Consistent with this result, a study by KPMG (2003) for the Canadian Automotive Partnership Council indicates that companies view workers within a broad class as being more or less interchangeable, while the productivity they actually achieve depends more upon the plant and the product than on workers’ inherent characteristics.

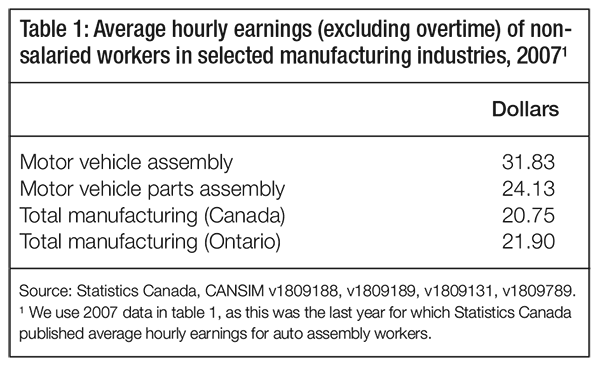

Despite the relatively minor share of productivity growth that is attributable to labour, workers in the Canadian automotive sector enjoy significantly higher pay than does the average manufacturing worker. Assembly workers in particular (as opposed to workers in the parts industry) enjoy roughly a $10 hourly premium compared with the average manufacturing wage (table 1). Although some of this gap may reflect industry-specific skills, we attribute most of this pay premium to union bargaining power. Further, we expect that this disconnect between pay and labour’s productivity performance explains in part the current trend of new automotive investment to low-wage jurisdictions such as southern US states, Mexico and China (Van Biesebroeck 2011; Keenan 2012). Competition from these jurisdictions has also been made more acute by the roughly 60 percent appreciation of the Canadian dollar vis-à-vis the US dollar during the past decade.7

Given this situation, the willingness of automotive firms to continue to pay high wages and benefits to Canadian workers without some offsetting inducement is in doubt. In the absence of significant changes in pay scales, we will likely see increased demands from automotive firms for investment subsidies to offset what they view as uncompetitive labour costs.

Pulling these threads together, we see some important interactions between subsidies, rent capture, distortionary taxation and trends associated with globalization. In the context of increasing global competition, automotive firms will demand increasing subsidies to maintain above-market pay packages for Canadian workers. But the use of subsidies simply transfers an equivalent value of the workers’ pay premium back to the firms. Moreover, the distortionary effect of taxation means that the total cost of the subsidy might exceed the pay premium thus secured. The lesson to be drawn is that policy-makers must be very careful about the use of subsidies to secure private sector investment.

With the conceptual tools in hand, we can now evaluate the decision to bail out GM and Chrysler in 2009 and the ongoing program of project-based subsidies. For the bailout, the most plausible justifications appear to be DIP financing, positive investment externalities (agglomeration effects, technological spillovers, human capital) and the social costs of adjustment. In this case, the role of investment externalities does not lie in building something new but in preserving an existing cluster by supporting firms in the process of restructuring. Such support speaks to the role of DIP financing and minimizing the social costs of adjustment. The high productivity of the automotive industry is also relevant to the decision to participate in the bailout. Indeed, high productivity is intimately linked with the investment externalities associated with the automotive cluster. In addition, high-productivity firms also might be a large source of tax revenues. At the same time, as we argued above, the link between high productivity and wage levels is not automatic.

In this section, we undertake a cost-benefit analysis of the bailout in comparison with the immediate closure of GM’s and Chrysler’s Canadian operations in spring 2009. To the extent that the companies have repaid the federal and Ontario governments, we are in the domain of DIP financing, in which case the governments’ contributions represent investments rather than subsidies. It simplifies analysis in the DIP-financing paradigm to assume that the bailout is accounted for in a separate capital budget, and therefore disbursements and repayments leave no trace in the governments’ annual budgets.8 In reality, the governments might make profits on their investments, which would accrue to the annual budgets (through, for example, interest differentials in the governments’ favour). However, we abstract from this possibility and assume instead that the governments just break even in direct financial terms. This assumption makes DIP financing equivalent to a government loan guarantee for the companies. Then the only task remaining is to determine the scale of the social costs avoided – in the form of, for example, unemployment and forgone gross domestic product (GDP) – as well as the long-term benefit of keeping the operations of these two high-productivity firms in Canada. In contrast, any portion of the bailout that is not repaid represents a subsidy and therefore must be treated as a cost in the analysis.

Given the recent success of GM and Chrysler, it is easy to be optimistic and view the bailout through the lens of DIP financing. The companies’ prospects did not look so promising in spring 2009, however, when the bailout decisions were made. Moreover, it remains unlikely that the federal and Ontario governments will be able to redeem the full value of their contributions to the two companies (Keenan 2011a), which suggests that we should consider a continuum of possibilities, ranging from pure subsidy at one extreme to pure DIP financing at the other. In fact, the modelling is unaffected in terms of the macroeconomic effects (employment, output, prices and productivity). The only difference relates to the effects on government budget balances (and thus potentially the value of the net benefit). Therefore, we can proceed with evaluating the macroeconomic effects and then discuss budget balances separately.

We begin by presenting the details of the bailout packages. We then turn to the macroeconomic modelling and finally to the cost-benefit analysis.

The total cost of the bailout of GM and Chrysler was $14.4 billion, shared two-thirds by the federal government and one-third by the Ontario government (Office of the Prime Minister 2009a,b; Ontario 2009a,b; GMCL 2009b). General Motors received $10.6 billion and Chrysler $3.8 billion.9 For GM, 14 percent of the package was in the form of loans, 4 percent in preferred shares (with a 9 percent annual dividend; see GM 2009) and 82 percent in equity, the latter amounting to an 11.7 percent ownership stake in the reorganized company. Chrysler’s package was 100 percent loans, although, in exchange for their participation, the two governments also received a 2 percent ownership stake in Chrysler Group LLC. Details of the loans (interest rate and maturity) were not made public at the time of the bailout, either in press releases or personal communications, although a press release by the Obama administration concerning Chrysler indicated that the company would make repayments at 30 months, 7 years and 8 years, and that the “interest will be an appropriate combination of cash and payment-in-kind” (United States 2009).10

The figure of $14.4 billion represents the gross cost of the bailout. To arrive at the net cost, it is necessary to consider liability for pension shortfalls under Ontario’s Pension Benefits Guarantee Fund. Alone among governments in Canada, Ontario provides, through the PBGF, a partial backstop of defined benefit pension plans in the private sector in the event of bankruptcy. We estimate that the PBGF would have been liable for approximately $4.9 billion in pension shortfalls if GM and Chrysler had left Canada through bankruptcy in spring 2009 (see appendix 2).11 In contrast, the PBGF had at that time net assets of less than $100 million.12

We do not believe it is credible to expect that a liability of this magnitude would ever have been recouped from premiums to the PBGF – such a large increase in premiums would have been required that it would have accelerated the recent trend away from defined benefit plans in the private sector. Rather, we think it is evident that this liability ultimately would have fallen to the taxpayers of Ontario. Indeed, in the 2009/10 fiscal year, the Ontario government extended a $500 million grant to the PBGF to deal with other claims related to the recession (FSCO 2010). Moreover, a portion of the bailout funds for GM and Chrysler was earmarked to return the two companies’ pension plans to solvency (Keenan 2009b). Therefore, one way or another (bailout or PBGF), taxpayers were bound to cover at least part of the unfunded pension liabilities of GM and Chrysler. It follows that, for the purpose of cost-benefit analysis, we should consider the cost of the bailout net of the obligations under the PBGF – that is, a net cost of $9.5 billion (14.4 billion minus 4.9 billion).

We consider three scenarios in our analysis of the bailout from the vantage point of spring 2009. In the first scenario, the federal and Ontario governments provide the assistance they actually did, and GM and Chrysler restructure and stabilize their market share along the lines indicated in their restructuring plans. We refer to this scenario as “successful bailout.”

In the second scenario, the federal and Ontario governments refuse to provide assistance. As a result, the Canadian operations of GM and Chrysler are closed, and the associated production and employment are shifted to the United States or elsewhere by the parent companies. The closure is accomplished through filing for bankruptcy protection under the Companies’ Creditors Arrangement Act, which has the effect of lifting responsibility for unfunded pension liabilities from the companies and transferring it in part to the PBGF. The closure is effective in spring 2009, coinciding with the companies’ filings for bankruptcy protection in the United States. Collectively, taxpayers save the net cost of the bailout, $9.5 billion, but they are still liable for the covered pension shortfalls under the PBGF. We refer to this scenario as “no bailout.”

In the third scenario, the federal and Ontario governments provide the assistance they actually did, and GM and Chrysler begin restructuring. However, the two companies experience a rapid decline in their market share, which requires larger reductions in employment and output than anticipated in their restructuring plans, and in 2015 they close their Canadian operations. The effect of the bailout, therefore, is to delay rather than to prevent closure. Unlike in the previous scenario, however, the pension funds of the two companies are fully funded due to infusions from the bailout, and so there are no claims on the PBGF. We refer to this scenario as “bailout resulting in closure.”

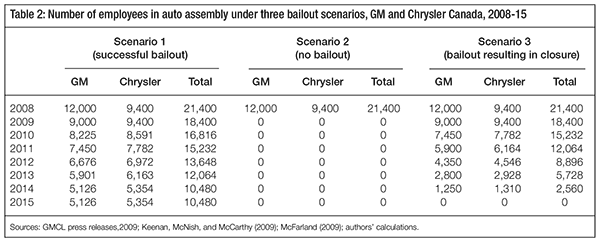

Employment projections under the companies’ restructuring are key data for all three scenarios. Table 2 summarizes this information. The 2008 number for GM is the year-end value as reported in company press releases at year end. The 2009 number for GM reflects changes effective in June of that year (again, from company press releases). The 2014 number for GM is based on information in an April 27, 2009 press release (GMCL 2009a), in which the company stated in particular that, under its new operating plan, its “hourly workforce is expected to go from 10,300 in 2008 to 4,400 in 2014,” a drop of 57 percent. Applying the same percentage reduction to the total workforce (hourly plus salaried) at year-end 2008 yields our estimate of the total workforce in 2014. We then interpolate in a straight-line fashion for 2010 through 2013.

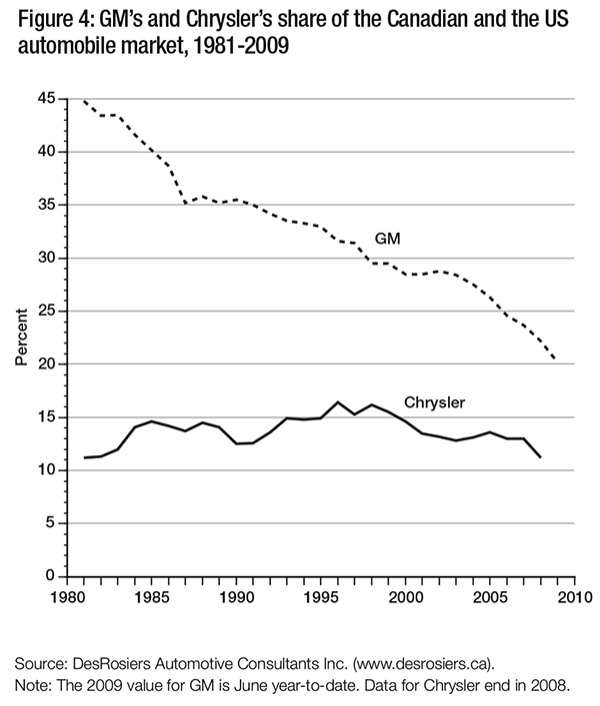

GM’s forecast of its workforce was based upon the assumption of a Canadian-US market share of 18.4 percent in 2009 and “a range between 16 and 17 percent market share in 2010 through 2014” (GMCL 2009a). These assumptions seem reasonable in light of market share trends presented in figure 4.

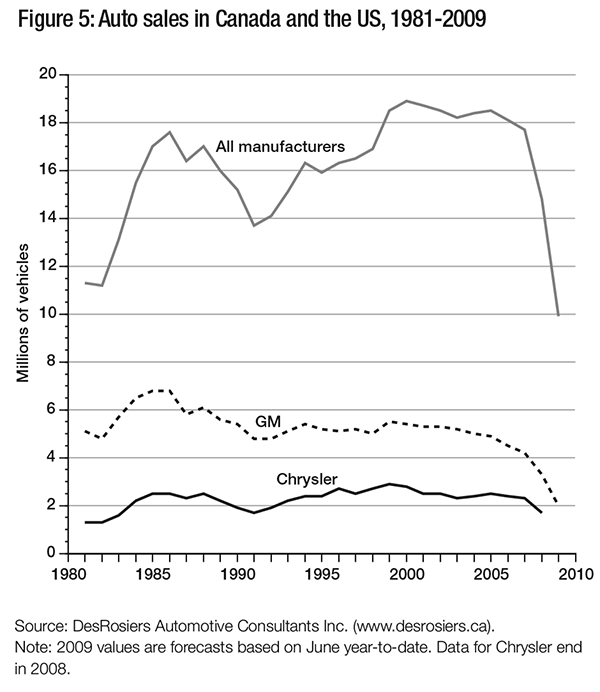

As for Chrysler, since the company did not make public information about its forward-looking operating assumptions at the time of the bailout, the 2008 and 2009 values in table 2 are based on press reports (Keenan, McNish, and McCarthy 2009; McFarland 2009). Figure 4 indicates greater stability in Chrysler’s market share over the past 30 years than is the case for GM, and we note that, as of May 2009, it had not yet laid off workers in Canada. Nonetheless, the shrinkage in total auto sales from 2007 to 2009 (figure 5) combined with the negative publicity associated with Chrysler’s trip through bankruptcy protection suggest that some reduction in employment would have seemed likely. For our purposes, we apply the same reduction factor announced by GM (57 percent) to estimate Chrysler’s employment in 2014. We then interpolate in a straight-line fashion for 2010 through 2013.

Based on these forecasts, we anticipate a combined reduction in employment at the Canadian operations of GM and Chrysler of 7,920 positions between 2009 and 2014 (that is, 18,400 minus 10,480). This reduction is assumed to go ahead in scenario 1 (successful bailout). Employment then stabilizes after 2014.

In contrast, in scenario 2 (no bailout), employment is reduced to zero at both companies effective 2009; in other words, the Canadian automotive assembly sector experiences a direct loss of 18,400 jobs.

In scenario 3 (bailout resulting in closure), we double the rate of job loss indicated by the firms’ restructuring plans (approximately 1,600 per year between 2009 and 2014, as shown in table 2). The result is that the two companies’ Canadian employment falls to zero in 2015.

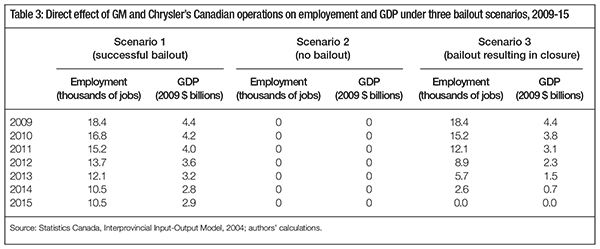

In addition to employment projections, we also require estimates of the contribution to GDP (value added) of GM and Chrysler at different levels of employment (summarized in table 3). The GDP estimates are derived from Statistics Canada’s 2004 Interprovincial Input-Output Model. By testing an arbitrary shock to employment, we obtained the ratio of GDP to employment for the auto assembly sector from the model. We then multiplied this value by 18,400 employees (the total number of employees in the two firms in 2009) to obtain the impact of the two firms on GDP in 2009 (see table 3). We then calculated the GDP impacts for subsequent years in proportion to employment and assuming a 2.6 percent improvement in labour productivity per year.13

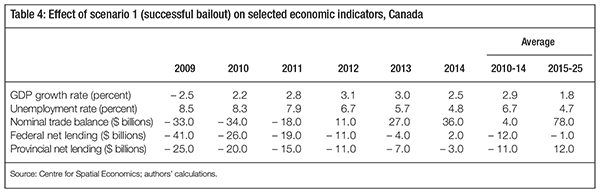

We estimated the macroeconomic effect of each scenario using the Provincial Economic Modeling System of the Centre for Spatial Economics (C4SE), a brief description of which appears in box 1. The inputs to the model consist of the direct impacts presented in table 3, as well as numerous other assumptions underlying C4SE’s summer 2009 economic outlook, which corresponds to the successful bailout scenario. The results of this scenario, summarized in table 4, show economic contraction in 2009, corresponding to the recession, followed by a return to modest growth in 2010. The unemployment rate hits 8.5 percent in 2009, up from 6.1 percent in 2008 (not shown). The unemployment rate starts to fall gradually in 2010, reaching 4.8 percent in 2014. The trade balance is negative during the 2009-11 period as weak demand for Canada’s exports lingers. The trade balance turns positive in 2012 and grows thereafter. Government budget deficits persist until 2013 (federal) and 2014 (provincial), long after the resumption of growth in 2010.

We present the results of our comparisons of scenarios 1, 2 and 3 for the short term (2009), medium term (2010-14) and long term (2015-25). We do not claim that the results for the 2015-25 period are a forecast of what will actually happen in the long term, as new developments obviously will arise before then. Rather, these results provide an indication of the forces set in motion by the different scenarios that, if undisturbed, would play out in the long term.

The primary shocks to employment and GDP in the no-bailout and bailout-resulting-inclosure scenarios are implemented in the C4SE model by reducing the automotive industry’s capital stock consistent with the impacts shown in table 3 – an approach we refer to as “capital scrapping.” This approach is consistent with the view that, in these scenarios, employment and production would be relocated to the United States or elsewhere and therefore some part of the corresponding capital stock would be moved out of the country while the remainder would be permanently idled. Due to this effect on the capital stock, the impacts of these scenarios work through both the supply side and the demand side of the economy. It follows that these scenarios have greater effects on overall employment and GDP than do conventional fiscal stimulus policies that work only through the demand side.

Policy analysis based on static models – that is, models that do not explicitly consider time – usually assume that capital is mobile in the sense that capital released by one firm will be taken up and put to use by another. Automotive capital, however, is typically quite specialized, so that in reality there is limited scope for the reallocation of idled capital in this sector to nonautomotive firms. Further, in the current situation of a global oversupply of automotive production capacity, there is not likely to be much demand among automotive companies for surplus capital (Spector 2010). Moreover, in dynamic models, in which time is taken into account, most analysts recognize that installing or reallocating capital is a costly activity. In this context, our assumption of capital scrapping would be consistent with a high cost of reallocation.

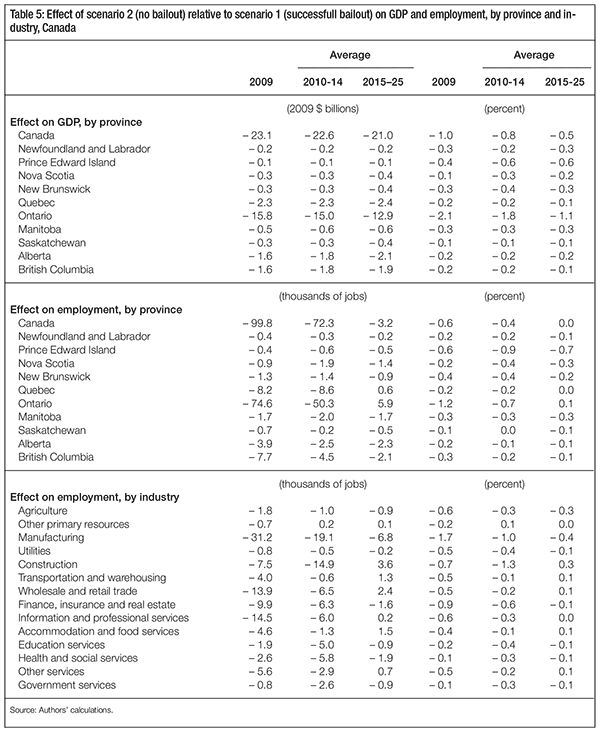

Our first comparison is between scenario 1 (successful bailout) and scenario 2 (no bailout). Table 5 presents the results of this comparison in terms of GDP and employment by province and industrial sector. We see that the effects of GM and Chrysler leaving Canada would have been large, compared with a successful restructuring. If production at the two companies had ceased at the start of 2009, employment in Canada would have contracted by approximately 100,000, or 0.6 percent of total employment.14 Of this amount, approximately three-quarters (74,600 jobs) would have been lost in Ontario, amounting to 1.2 percent of total employment in the province. In terms of GDP, losses would have been proportionately higher (1.0 percent of national GDP and 2.1 percent of Ontario GDP) because of the high productivity of workers in the automotive sector.

The losses would have moderated in the medium and long term, as employment under scenario 1 fell in line with the restructuring (table 3). In the medium term (2010-14), employment in Canada would have been lower by 72,000 on average, compared with scenario 1, and by 50,000 on average in Ontario. Similarly, GDP losses over the 2010-14 period would have been more moderate than in 2009, at 0.8 percent nationally and 1.8 percent in Ontario on average. Not surprisingly, the effects in other provinces would have been much less pronounced than in Ontario.

Almost a third of the employment losses in 2009 would have occurred in manufacturing (31,200 jobs), with information and professional services hit second hardest (14,500 jobs) and wholesale and retail trade hit third hardest (13,900 jobs). Over the medium term, the job losses would have been spread more evenly. Proportionally, the construction sector would have contracted the most sharply over the 2010-14 period, with employment declining on average 1.3 percent per year, largely as a result of a decline in new activity by businesses and a slump in housing construction.15

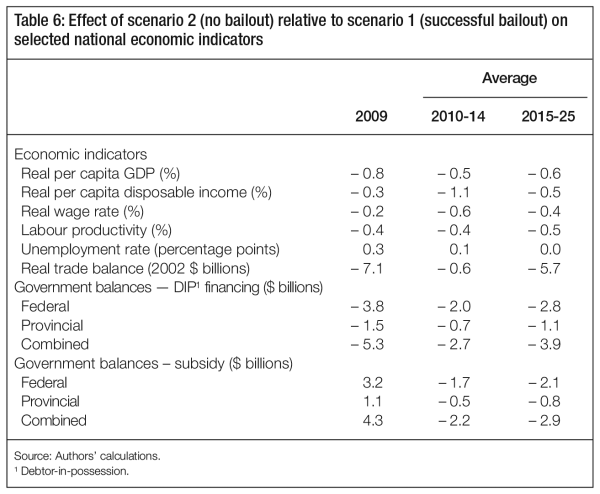

With no bailout, the loss of GM and Chrysler would have resulted in a small but permanent decrease in Canada’s economic prospects, as shown in table 6. Per capita GDP, per capita disposable income, labour productivity and the wage rate all would have fallen in inflation-adjusted terms relative to the baseline (scenario 1) over the short, medium and long term, although the losses would have remained small – less than 1 percent in most cases. The unemployment rate would have increased in both the short and medium terms, and the country’s trade balance would have been reduced permanently due to the loss of export revenues from the automotive sector.

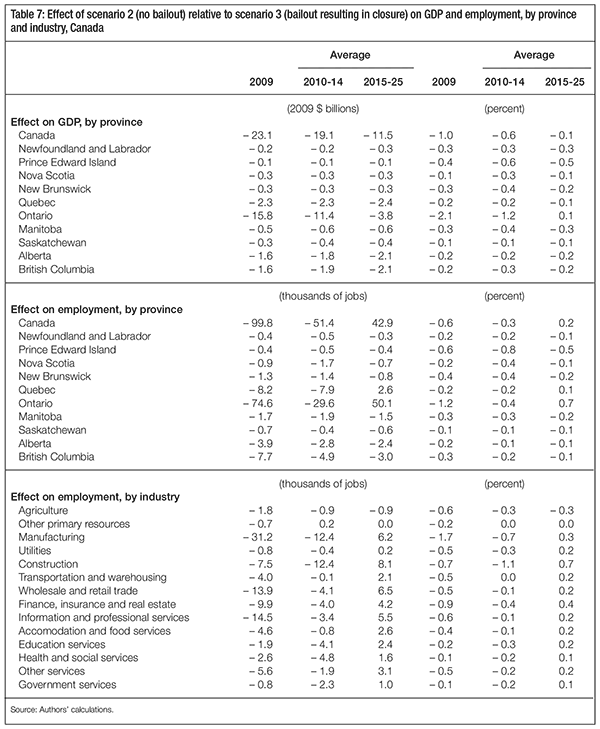

The second comparison is between scenario 2 (no bailout) and scenario 3 (bailout resulting in closure). The results for this comparison are identical in the short term to those of the first comparison (scenario 1 versus scenario 2), since the number of jobs and the output at stake in 2009 are the same for scenario 1 and scenario 3 (see table 3). In the medium and long term, we observe moderate losses (in percentage terms) in most measures under scenario 2 compared with scenario 3 (tables 7 and 8). As expected, these losses are smaller than in the first comparison, reflecting the greater similarity of scenarios 2 and 3.16 Per capita economic performance remains worse under the no-bailout scenario in the long run, as evidenced by lower GDP per capita, lower wages, and worsened trade and government balances (table 8).

The larger impact of the no-bailout scenario is explained in large measure by the effect on the country’s capital stock and by the high productivity of the automotive industry. The sudden closure of GM and Chrysler would have led to an immediate idling of productive capital and, therefore, to an immediate loss of income, savings and investment. Reduced investment would have put the country on a permanently lower growth trajectory. In contrast, even though GM and Chrysler still close under scenario 3, Canada benefits from more person-years of production from the companies’ existing capital stock. This production yields consumption for workers, tax revenues for government and savings that contribute to new investment. New investment increases the national capital stock and puts the country on a higher growth trajectory, compared with the no-bailout case. Finally, the preservation of employment in a high-productivity sector helps to sustain incomes, output and tax revenues. In the long run, a dynamic economy will put unemployed workers back to work regardless of what happens, but likely at a lower level of average productivity than in the automotive sector.

As discussed above, in the DIP-financing paradigm, we do not record disbursements and repayments of bailout funds in the annual budgets of the federal and Ontario governments. Instead, we assume the bailout transactions are recorded in separate capital budgets. This approach allows us to abstract from the timing of disbursements and repayments and reflects the fact that the bailout does not represent a cost to government if the funds are repaid. It follows therefore that differences in annual budget balances between the no-bailout scenario and the two bailout scenarios under DIP financing are due solely to differences in macroeconomic performance. Since the no-bailout scenario exhibits the worst macroeconomic performance, it also exhibits lower government balances – that is, larger deficits and smaller surpluses – than either the successful-bailout scenario or the bailout-resulting-in-closure scenario (see tables 6 and 8).

In particular, for the first comparison under DIP financing (no bailout versus successful bailout – table 6), the combined federal and provincial budget balances would have been $5.3 billion lower per annum in 2009, reflecting reduced tax revenues and increased social assistance expenditures under the no-bailout scenario. This gap narrows in the medium term, as the economy recovers, but it never disappears. In the long term (2015-25), the combined federal and provincial budget balances are on average $3.9 billion lower under the no-bailout scenario than under the successful-bailout scenario, which reflects the reduction in GDP and consequent loss of tax revenue under this scenario. Both scenarios indicate a deficit during the years 2009-13 for the federal government and 2009-14 for all provincial governments combined (not shown). However, the figures in table 6 indicate that these deficits would have been larger under the no-bailout scenario than under the successful-bailout scenario, and subsequent surpluses would have remained smaller.

The budget figures under DIP financing for the second comparison (no bailout versus bailout resulting in closure – table 8) show similar forces at work. In fact, the figures for 2009 are identical for both comparisons (table 6 and table 8) because the two bailout scenarios result in the same macroeconomic performance in 2009. In subsequent years, however, the macroeconomic performance of the bailout-resulting-in-closure scenario lags behind that of the successful-bailout scenario. Therefore, in the medium and long term, the gap in budget balances between bailout resulting in closure and no bailout (table 8) is less than the gap between successful bailout and no bailout (table 6).

In the pure-subsidy paradigm, there is no repayment by the companies, so the bailout represents a cost that must be charged to the governments’ annual budgets. The results for this case are also shown in tables 6 and 8. Focusing on the first comparison – no bailout versus successful bailout (table 6) – we observe that government balances would have been better in the short term under the no-bailout scenario, due to the saving of the net cost of the bailout. In particular, the federal budget balance would have been $3.2 billion higher in 2009 and the provincial budget balances would have been $1.1 billion higher – that is, the governments would have had lower deficits – under the successful-bailout scenario.17 In subsequent years, however, this situation would have reversed owing to reduced tax revenues and increased spending on employment insurance and other transfers. Moreover, the situation would have become progressively worse, reflecting the permanent reduction in GDP under the no-bailout scenario. Combined federal and provincial budget balances would have been $2.2 billion lower per annum in the medium term and $2.9 billion lower per annum in the long term under the no-bailout scenario. The budget figures for the second comparison under the subsidy paradigm (no bailout versus bailout resulting in closure – table 8) show similar forces at work, although the differences post-2009 are smaller than in the first comparison owing to the greater similarity of the two scenarios.

By definition, the bailout did not cost the federal and Ontario governments anything under the DIP-financing assumption. Since keeping GM and Chrysler in Canada was shown to entail substantial economic benefits, it follows that the bailout represented a good policy choice in this framework.

In contrast, under the pure-subsidy assumption, we must compare the cost of the bailout with the macroeconomic benefits that flowed from the avoidance of the immediate closure of the two companies’ Canadian operations. Our analysis indicates that those benefits would have far outstripped the net cost of the bailout even if the companies were to close in 2015 (see table 7). For Canada as a whole, the loss of GDP under the no-bailout scenario, compared with the bailoutresulting-in-closure scenario, would have been $23.1 billion in 2009, $19.1 billion per year on average over the 2010-14 period and $11.5 billion per year on average over the 2015-25 period. Of course, the relative losses would have been even greater compared with the successful-bailout scenario ($23.1 billion, $22.6 billion and $21.0 billion, respectively; see table 5). Thus, in the standard cost-benefit sense, the bailout represented good policy from the vantage point of 2009, compared with the immediate closure of GM’s and Chrysler’s Canadian operations. Indeed, the avoidance of lost GDP in 2009 alone was enough to cover the net cost of the bailout.

Even if we limit our analysis to the implications for government budgets, we conclude that the bailout was preferable to the immediate closure of GM and Chrysler in the pure-subsidy case. Immediate closure would have caused a deteriation in the combined federal and provincial budget balances of $2.2 billion on average over the 2010-14 period and of $2.9 billion on average over the 2015-25 period, compared with the successful-bailout scenario (table 6). These numbers reflect increased expenditures, especially for employment insurance, and reduced tax revenues due to the reduced economic activity under the no-bailout scenario. At this rate, the net cost of the bailout ($9.5 billion) will be paid for, in terms of avoided deficits, by the end of 2015.18 Compared with the bailout-resulting-in-closure scenario, immediate closure would have caused a deterioration in the combined federal and provincial budget balances of $1.4 billion on average over the 2010-14 period and of $1.3 billion on average over the 2015-25 period (table 8). At this rate, the net cost of the bailout would have been paid for by the end of 2020.

Our conclusion that the bailout was preferable to the immediate closure of GM’s and Chrysler’s Canadian operations is not materially influenced by the pension liabilities under the PBGF, since even the gross cost of the bailout, $14.4 billion, is significantly less than the GDP losses associated with immediate closure (tables 5 and 7). In terms of government finances, it would take longer to pay for the gross cost of the bailout than for the net cost, but since budget balances would have remained lower in all years under the no-bailout scenario than under the baseline scenario (with the exception of 2009), the bailout still would pay for itself over time, even if measured in terms of the gross cost. In particular, under the successful-bailout scenario, the gross cost would be paid for in terms of improved budget balances by 2017. Under the bailout-resulting-in-closure scenario, the gross cost would have been recovered in terms of improved budget balances by 2023, even if the firms closed in 2015.19 This analysis indicates that, even if the PBGF did not exist – that is, if Ontario did not have any obligation for GM’s and Chrysler’s pension shortfalls – and if there was no expectation of repayment by the firms (the pure-subsidy paradigm), the bailout as structured still would have passed the cost-benefit test compared with the immediate closure of GM’s and Chrysler’s Canadian operations.

In principle, when assessing the bailout under the subsidy paradigm, we should take account of the distortionary effect of the taxation necessary to pay for it. As a macroeconomic model, C4SE’s Provincial Modeling System accounts for some but not all of the distortionary effects of taxation. To address this issue, we could make ad hoc adjustments to account for the missing effects by applying an appropriate value of the marginal cost of public funds where needed.20 However, in addition to the cost of the bailout, we would also need to make adjustments for increased government expenditure – on increased employment insurance payments, for example – and borrowing in the no-bailout scenario. Since increased government expenditure and borrowing in this scenario exceed the cost of the bailout in the medium and long term (tables 6 and 8), it follows that adjusting for the marginal cost of public funds would only reinforce our conclusion that the two bailout scenarios are preferable. Therefore, in the interest of brevity, we do not undertake such adjustments. We return to the subject of the MCPF, as it relates to the bailout, in a subsequent section.

The results of our cost-benefit analysis of the bailout will prove useful in assessing the program of project-based subsidies that began in 2004. In terms of potential economic rationales, the most plausible justifications for these subsidies would appear to be positive investment externalities – in the form of agglomeration effects, technological spillovers and human capital – as well as the high productivity level of the automotive sector, and the opportunity to avoid the social costs of labour market adjustment that would have resulted from the loss of specific projects. The social costs of adjustment are likely to be particularly pronounced in the case of brownfield projects – that is, the refurbishing of existing operations – since established workers have significant investment in human capital that might not transfer easily to other employers or occupations.

In some cases, government assistance for specific projects has taken the form of loans. Insofar as these loans are made on strictly commercial terms, there is no net cost to government (as in the case of DIP financing for the bailout), and so we ignore them in our analysis. In the real world, of course, there is always the risk of default, which represents a cost to government (as with conventional loan guarantees). Furthermore, the fact that government, rather than commercial lenders, is called upon to provide a loan suggests there is likely a problem with the company’s creditworthiness or the project’s business plan. Thus, in such cases, the risk of default might be especially high. Nonetheless, we set aside the issue of loans and focus instead on the case of subsidies.

Some assistance has taken the form of interest-free loans, which represent a hybrid of loan and subsidy. To the extent that the recipient pays back the principal, the cost to government is reduced. In this case, the subsidy is limited to the forgone interest, including the appropriate risk premium.

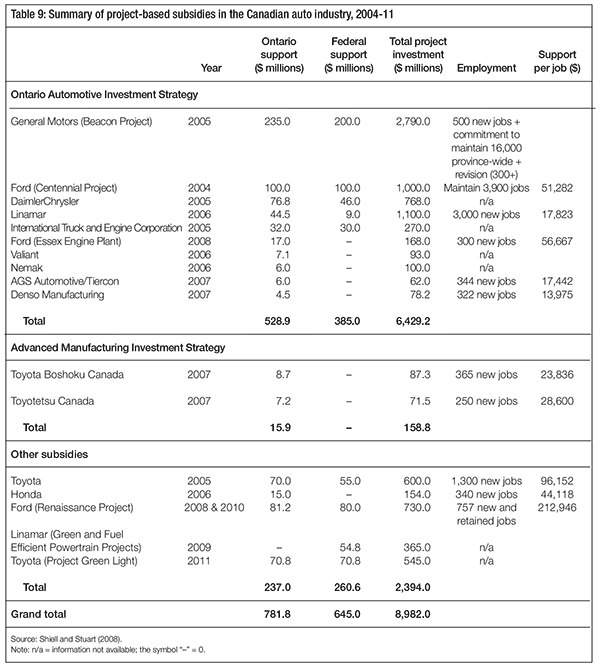

In April 2004, Ontario’s newly elected Liberal government announced the Ontario Automotive Investment Strategy (OAIS), a $500 million fund to attract new investments in the province’s automotive sector.21 Ten agreements were eventually reached under the aegis of this fund. In December 2005, the Ontario government announced a second $500 million fund, dubbed the Advanced Manufacturing Investment Strategy (AMIS), focusing on technological innovation in manufacturing, including the automotive sector. Queen’s Park has subsequently created a number of other funds, many with an environmental or technology focus – examples include the Next Generation of Jobs Fund and the Strategic Jobs and Investment Fund. In addition, the Ontario government has contributed to certain automotive projects on an ad hoc basis. Table 9 summarizes the details of subsidized projects in the auto industry.

Under the OAIS, assistance took the form of either a grant (a pure subsidy) or a loan, the duration of which varied from one agreement to the next. Under the AMIS, all agreements took the form of interest-free loans for up to five years. Penalties for nonfulfillment included the requirement to repay grants and the accelerated repayment of loans. In practice, however, these terms proved to be quite soft: loans were converted into grants after the fact, and penalties proved to be meaningless, as we demonstrate below in the case of GM.22

Some projects have also received funding from the federal government (see table 9). Prior to 2008, federal contributions typically were made on an ad hoc basis through Industry Canada. Then, in 2008, the federal government created the Automotive Innovation Fund, a five-year, $250 million initiative to support research and development (R&D) in the automotive sector, with a particular focus on green technologies and fuel efficiency.

Both the Ontario and federal governments have tended to place increasing emphasis over time on technological R&D and environmental innovation in their choices of industry projects. This tendency is significant, as the economic case for subsidies for R&D and innovation is well understood and quite distinct from the case for investment subsidies that focus on production facilities. Economists argue that private firms typically underinvest in technological R&D because they cannot appropriate all of the benefits that result, and that subsidies can help correct this problem. This argument is similar to Van Biesebroeck’s (2010) discussion of technology spillovers, except that he focuses more on spillovers from production – such as the gaining of experience with new types of machinery – than on spillovers from R&D. For this reason, in table 9, we leave out projects that are solely focused on R&D. However, some projects receiving funding combine both R&D and production components, and their press releases do not separate the two components’ funding commitments; in such cases, we include the entire project in table 9.

The level of detail regarding employment varies among agreements. Certain projects are described in Ontario and federal government press releases as maintaining or creating “hundreds” of positions; obviously, such claims are too imprecise for meaningful analysis, and we therefore exclude them from table 9.

The largest subsidy to date has been awarded to GM for its Beacon Project, which received $235 million from the Ontario government and $200 million from the federal government. Originally, both components took the form of interest-free loans (Howlett 2008), but these were subsequently converted into grants (Chase and Keenan 2008). Most of the employment impact of this agreement took the form of a commitment to maintain 16,000 jobs province-wide over a nine-year time frame, a commitment that was breached in 2008 with the onset of the automotive crisis.23

The second-largest agreement involved $200 million to Ford for its Centennial Project, which led to the transformation of its Oakville assembly complex into a flexible assembly plant. Half of this assistance was provided by Ontario and half by the federal government. While the Ontario government’s press releases are not entirely clear, we have determined that the province’s assistance took the form of a grant, as indicated in the Public Accounts of Ontario (Ontario 2007). The federal assistance took the form of a loan, although its terms were not made public. According to the federal government press release (Industry Canada 2004), this initiative was expected to “maintain some 3900 direct jobs as well as thousands of other jobs in the area that depend on the Ford assembly plant.”

We consider two scenarios in this section. In the first scenario – the actual case – the government pays the subsidy to secure the investment (the “subsidy” scenario). In the second scenario, the government does not pay a subsidy and the investment is lost (the “investment-lost” scenario).

The example of the bailout suggests that there are likely projects for which paying the subsidy is preferable to losing the investment. As a general rule, projects should be assessed on a case-bycase basis, using a macro model such as C4SE’s Provincial Modeling System. In the present case, however, the example of the bailout is sufficiently instructive that we can bypass a case-by-case analysis of the projects listed in table 9. Instead, we calculate the support per direct job claimed for each project – that is, for each project with a credible job claim – and compare it with the figure for the bailout. The last column of table 9 presents these figures for the projects for which precise estimates are available. We observe that the value of the subsidy per job ranges from $13,975 to $212,946. The value for the bailout of GM and Chrysler is $516,304 ($9.5 billion divided by 18,400 jobs) – an order of magnitude larger than the value for most of the projectbased subsidies. Yet despite its higher cost, the bailout was shown to be preferable to the nobailout scenario. Therefore, we conclude that the subsidies listed in table 9, for those projects with credible job figures, were all preferable to the alternative of losing the investments.24

As with the bailout, we ignore the implications of distortionary taxation, since investment lost is expected to involve higher government expenditures than the subsidy anyway. We see here the importance of avoiding the social costs of adjustment from losing the investment – in the form of unemployment, lost tax revenue and social transfers – as well as the significance of the high productivity of automotive activity, as these factors dominate the cost of the subsidy.

In the previous sections we argue that the bailouts and project subsidies offered to the Canadian automotive sector during the past decade represented good policy choices, given the information available at the time, compared with the option of losing the related investments. Yet this conclusion is limited in scope, since it involves comparing only two scenarios and does not consider any alternative uses for the funds involved. As a general rule, in order to determine the optimal policy choice for government at any given time, it would be necessary to compare a very large number of alternative policy proposals, but such an exercise is beyond the scope of this study. Nonetheless, we are interested in considering one additional scenario – one in which the workers in the affected companies provide a greater share of the inducement for investment through concessions on wages or benefits.

This scenario raises the important concept of the workers’ “opportunity cost,” in the present context defined as the amount a worker would earn in his or her next best employment relative to the amount the worker receives at his or her current position. It therefore establishes a floor under what the worker would be willing to accept in the current position.

It is widely accepted that the opportunity cost of Canadian automotive workers is significantly below the level of compensation they earn in the industry. Perhaps the greatest proof of this statement is that few workers who lose their jobs at automotive plants in Canada are able to find work at comparable levels of pay elsewhere in their communities. Keenan (2011b) provides a typical example of unionized parts workers at a plant in Ajax, Ontario. Initially employed at a base wage of $28 per hour, the workers lost their jobs when the plant was closed during the crisis of 2009. Subsequently, the plant was reopened and the workers agreed to return to work with a 32 percent reduction in pay, to $19 per hour.

In table 1 we provided a useful comparison of wage levels of assemblers, parts workers and average manufacturing employees. While not a precise exercise, it nonetheless seems reasonable, based on media reports and discussions with industry insiders, to consider the average manufacturing wage ($21.90 in Ontario) as an approximate measure of the typical automotive worker’s opportunity cost. This approach assumes that the average manufacturing wage represents the equilibrium or competitive wage level for the affected workers; therefore, the difference between this level and the actual wage earned in the industry represents an above-market premium for the workers.

It might be tempting to argue that the relatively high level of pay in the automotive industry reflects high productivity. As our earlier discussion indicated, however, most of the productivity growth in the automotive industry over the past 45 years has been due to factors unrelated to the labour force, and therefore we do not find the productivity argument compelling. Rather, we believe that the pay premium enjoyed by Canadian auto workers is due primarily to union bargaining power.

A great deal of media attention focused during the 2009 crisis on the large gap in labour costs between unionized and nonunionized workers in the sector. For example, Keenan (2009a) reported a $19 per hour difference in “all-in costs” for assembly workers in shops represented by the Canadian Auto Workers union (CAW) (namely, GM, Chrysler and Ford) and those in nonunion shops (Toyota and Honda). Stanford (2009) argues, however, that most of this gap was the result of differences between union and nonunion firms in terms of “legacy costs” for current retirees (health care and pension), demographics (the older cohort of workers at union shops were entitled to higher pay and longer vacation time) and shutdown time (with fewer hours worked at GM, Chrysler and Ford due to weaker demand for their product at the time). Other sources have corroborated this argument. Indeed, according to one confidential industry source, with these factors stripped out of the calculation, the difference in hourly wage costs between unionized GM and nonunion Toyota in 2008 was less than five dollars. This result reflects the view – widely accepted in the industry – that nonunion assembly firms base their wage and benefits packages on the union template. The differential in all-in costs in 2009, then, reflects the fact that nonunion shops had younger workers and very few retirees. Moreover, the reduction of this differential during the bailout negotiations in 2009 (GMCL 2009b) resulted primarily from the use of bailout funds to cover unfunded pension liabilities and to create new health care trust funds for retirees, rather than to obtain concessions from active workers. It follows that the above-market pay premium – the difference between the actual level of compensation earned and the workers’ opportunity cost – applies to all workers in the industry, both union and nonunion.

Since automotive workers have long enjoyed this premium, and since it does not appear to be related to their underlying productivity performance, it seems appropriate to ask whether more of the investment incentive for past projects and the bailouts should have been provided by the workers themselves, through concessions on pay. Since a dollar is a dollar, regardless of its source, we argue that the firms would have been indifferent to whether they received assistance in the form of subsidies from the government or in equivalent concessions from workers. We are interested to explore the economics and ethics of this proposal. First, we demonstrate the mechanics for establishing equivalence between subsidies and workers’ concessions on pay. Then we consider the effects of such concessions in terms of economic efficiency, vertical equity and sustainability of the firms’ operations.

We consider Ontario’s grant of $100 million to Ford for its Centennial Project in 2004 to demonstrate the methodology for establishing equivalence between subsidies and concessions in workers’ pay (we ignore the federal contribution, as it was structured as a loan). It was claimed that the Centennial Project would secure 3,900 jobs (table 9, item 2). Dividing the $100 million grant by 3,900 jobs, we obtain a value of $25,641, which represents the present value of the concession that would have been required from each affected worker to provide an equivalent amount of assistance to Ford. The corresponding annual value is $1,641, assuming an annual borrowing cost to the company of 6.4 percent.25 This annual value is equivalent to 79¢ per hour (assuming 40 hours per week, 52 weeks per year); in other words, if each of the 3,900 affected workers had given up 79¢ per hour, this would have yielded enough savings for Ford to cover the borrowing costs on $100 million worth of new bonds to make the Centennial Project viable without assistance from the Government of Ontario. This concession would have represented a 2.5 percent reduction in pay from the average automotive assembly wage of $31.83. While not insignificant, it would still have left these employees well above the assumed value of their opportunity cost – that is, the average manufacturing wage in Ontario of $21.90 (table 1). As table 9 shows, calculations with other projects reveal similar results.

In contrast, performing this type of calculation for the bailouts of GM and Chrysler (a net cost of $9.5 billion divided among 18,400 workers) yields an equivalent hourly concession on pay of approximately $16. Since we estimate the above-market premium in pay for automotive workers at approximately $10 per hour, it would not have been possible for workers to fund the entire cost of the bailout. Nonetheless, by reducing compensation to the competitive level – that is, a reduction of $10 per hour – workers could have funded approximately $6 billion of the bailout (the capitalized value of the concession). In terms of implementation, the federal and Ontario governments still would have had to provide the initial funding, as bond markets were frozen due to the financial crisis. Over time, however, the increased profitability flowing from such a concession would have enabled the companies to reimburse this portion of the bailout.

This point is significant since, as the bailout is actually structured, the Ontario and federal governments do not expect to recoup its full value; they have recouped $4.2 billion of the principal and still hold approximately $4.9 billion in shares of GM and Chrysler (Keenan 2011a). Assuming the two governments eventually redeem these shares at the estimated value, they will recoup $9.1 billion of the bailout principal, leaving a shortfall of $5.3 billion on the total gross cost of the bailout of $14.4 billion. Our calculation above shows that this shortfall could have been covered by workers’ concessions on pay.26

Obviously, the affected workers would prefer the subsidy arrangement to making concessions on pay. Nonetheless, as long as their pay remains above the level of their opportunity cost, the workers have no incentive to change employers. Thus, we can view the subsidy as a transfer that has had the effect of relieving workers of the need to make concessions on pay that would not have changed their decision about how much and where to work. Stated differently, the subsidy indirectly supports the workers’ above-market pay premium. This arrangement echoes Van Biesebroeck’s (2010) scenario in which subsidies are used for the purpose of rent capture – in this case, helping workers appropriate some of the firms’ profits or, rather, paying the firms to pay the workers a larger share of the firms’ profits.

Of course, as we have already observed, there were many years during the decade prior to 2009 in which none of the big three unionized shops had much profit to capture. And in any case, regardless of the firms’ profit levels, it is important to assess the impact of such transfers in terms of overall economic efficiency. The issue of distortionary taxation is key in this assessment: while concessions in pay are equivalent to a one-to-one transfer from workers to the firms, the use of subsidies entails additional economic costs in the form of the distortionary effect of taxation.

For example, using Dahlby and Ferede’s (2011) estimate that the MCPF equals 1.71 for the federal corporate income tax, we calculate that the total economic cost of each dollar of subsidy to automotive firms is $1.71. But since the subsidy can be viewed as a transfer to support workers’ above-market pay, it follows that each dollar of benefit workers receive from the subsidy costs society $1.71 in total.27 We conclude, therefore, that it would be more efficient if workers provided the assistance, through concessions on pay, since such concessions would not entail any additional cost to the economy.

The key to this observation is that money saved by reducing subsidies is passed back to taxpayers by reductions in the appropriate tax rate. Thus, income lost by auto workers is gained by other taxpayers in the form of a reduced tax burden. This outcome is plausible when government budgets are balanced or are in surplus, but when government budgets are in deficit, savings in expenditures would not be passed back immediately to taxpayers through tax cuts. In that case, wage concessions by workers would have a contractionary macroeconomic effect. Under those circumstances, governments might wish to provide additional stimulus to offset the contractionary effect of wage concessions. Additional stimulus would not add to the long-term debt, since, with the wage concessions, governments would recoup more of their financial contribution. Alternatively, wage concessions could be phased in gradually to spread out the macroeconomic impact and allow more time for adjustment.

What about the vertical equity considerations of the wage concessions proposal? To evaluate this aspect, we estimate the average annual gross income for an auto assembler in Canada in 2007 at approximately $66,000, based on average hourly compensation of $31.83 (table 1) and employment of 40 hours per week over 52 weeks (2,080 hours).28 In contrast, the average annual market income (that is, excluding government transfers) of working-age Canadians (those aged 25 to 64), expressed in 2007 dollars, was $44,271.29 The gap between the two levels of income suggests that the automotive subsidies and bailouts were regressive, as they redistributed income from lower-paid taxpayers, on average, to higher-paid auto workers.

One could obtain another perspective on equity by comparing automotive subsidies with wage subsidies for low-income workers. For example, since 2007, the federal government has offered the Working Income Tax Benefit (WITB), which provides a 25 percent benefit on income earned in excess of $3,000, up to an annual maximum; above a threshold level of net income, the WITB is clawed back at a marginal tax rate of 15 percent. Since tax revenues are finite, offering funds for one type of subsidy necessarily reduces the funds available for another. Therefore, in the vein of analyzing alternative scenarios, it might be useful to compare automotive subsidies with a program to increase benefits under the WITB by an equivalent amount – for example, by using the funds that were allocated to subsidies to reduce the clawback rate of the WITB instead. We leave such a comparison for future research. However, on the surface, at least, it seems plausible that subsidizing the wages of low-income workers would be preferable in terms of vertical equity to subsidizing the wages of higher-paid automotive workers.

A final advantage of the proposal for wage concessions relates to the sustainability of the companies’ operations in Canada. Given competition from lower-wage jurisdictions such as those in the southern US states, Mexico and China, as well as the companies’ view that the productivity advantage of Canadian workers is overstated (KPMG 2003), we believe that the above-market wage premium Canadian auto workers currently enjoy is not sustainable. In this light, we believe that proactive behaviour by Canadian workers to agree to concessions on pay would be more successful in preserving jobs in the industry than reactive behaviour focused on resistance.

Pulling these threads together, we conclude that concessions on pay by auto workers would have been a superior outcome in terms of efficiency, equity and the sustainability of the auto firms’ operations. In this way, we make a distinction between good policy choices (such as subsidies for investment projects and the bailouts), which yield a positive net benefit for Canada, and better policy choices (such as investment assistance provided through workers’ concessions on pay, rather than subsidies), which yield even higher net benefits overall. By exploring a much larger number of alternative policy proposals, one eventually could arrive at the best or optimal policy choice, the one that maximizes the net benefit attainable.