Les politiques commerciales du Canada au carrefour des nouvelles réalités mondiales

Aperçu des résultats de recherche

Stephen Tapp, Ari Van Assche et Robert Wolfe

Canada’s trade policy priority should not be signing more trade deals, but rather finding alternative ways to support the development of Canadian-based firms that produce goods and services the rest of the world demands, says Jim Stanford. His commentary, which is included in Redesigning Canadian Trade Policies for New Global Realities, comes in the context of ongoing debates in Canada surrounding the implementation of the CETA and TPP trade agreements.

Jim Stanford is an economist and well known economic commentator. He worked for many years as economist with Unifor, Canada’s largest private sector trade union. He is now based in Sydney, Australia, where he is an honorary professor in political economy at the University of Sydney. He still advises Unifor and he is the Harold Innis Industry Professor of Economics at McMaster University, in Hamilton, Ontario.

Redesigning Canadian Trade Policies for New Global Realities, edited by Stephen Tapp, Ari Van Assche and Robert Wolfe, will be the sixth volume of The Art of the State. Thirty leading academics, government researchers, practitioners and stakeholders, from Canada and abroad, analyze how changes in global commerce, technology, and economic and geopolitical power are affecting Canada and its policy.

A sustained deterioration in Canada’s international trade performance has contributed significantly to its generalized macroeconomic weakness over much of the past decade. Growth in Canada’s exports of goods and services has been among the weakest of any industrial country, while the composition of Canadian exports has shifted to unprocessed, resource-based products and away from more sophisticated, higher-value goods and services. As the growth of imports has outpaced that of exports, Canada’s trade balance has deteriorated, and sizable current account deficits are now a chronic feature of its economic record.

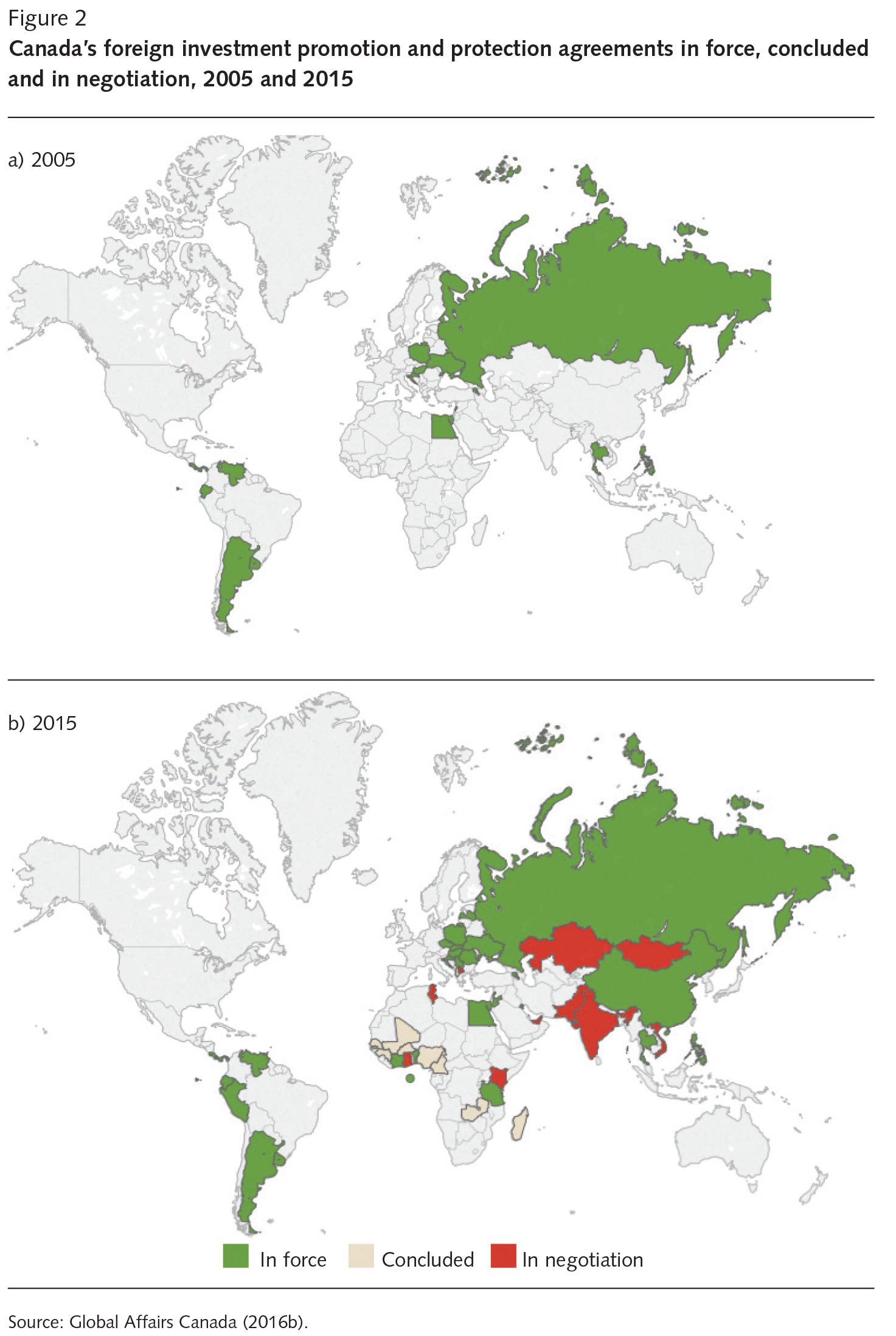

Interestingly, some trade commentators have not interpreted these discouraging results as suggesting that Canada’s current trade strategy is not working. Instead, they effectively recommend that Canada do more of the same — in particular, continue to negotiate more liberalized trade through new free trade agreements (FTAs), which are generally assumed to boost both the quantity and quality of trade (see, for instance, Manley and Kingston, in this volume). Indeed, the previous federal Conservative government followed this strategy from 2006 to 2015, with Canada finalizing new FTAs with 10 countries — more than any other government in Canadian history (figure 1). As well, two mega-regional trade deals — the Comprehensive Economic and Trade Agreement (CETA) with the European Union, and the Trans-Pacific Partnership (TPP) — have been concluded, which, if implemented, will add 35 more countries to Canada’s free trade relationships.1 During the same time, the Conservative government also reached foreign investment promotion and protection agreements with 25 countries, notably including China (figure 2). These agreements are supposed to improve Canada’s trade performance by attracting more foreign direct investment (FDI), including into export-oriented sectors, and facilitating the global business development of Canadian-based firms.

In short, Canada has pursued trade liberalization more aggressively, on more fronts, than ever before,2 yet its trade performance has continued to deteriorate. Moreover, this deterioration has been more marked in bilateral trade flows between Canada and its FTA partners than with its trade with the rest of the world. Such results raise a critical question: Is signing more FTAs really the best way to address Canada’s trade woes, or has it actually been part of the problem?

In my view, Canada’s overarching policy focus should not be on signing yet another blockbuster trade deal, but rather on something else: supporting the development and growth of globally oriented, innovative, technologically intensive firms in Canada — firms that produce goods and services the rest of the world demands. Canada’s abysmal performance in business innovation stands at the centre of this challenge, and I expect it to continue to lose global market share if Canada does not move closer to global best practices of innovation, business development and export promotion.

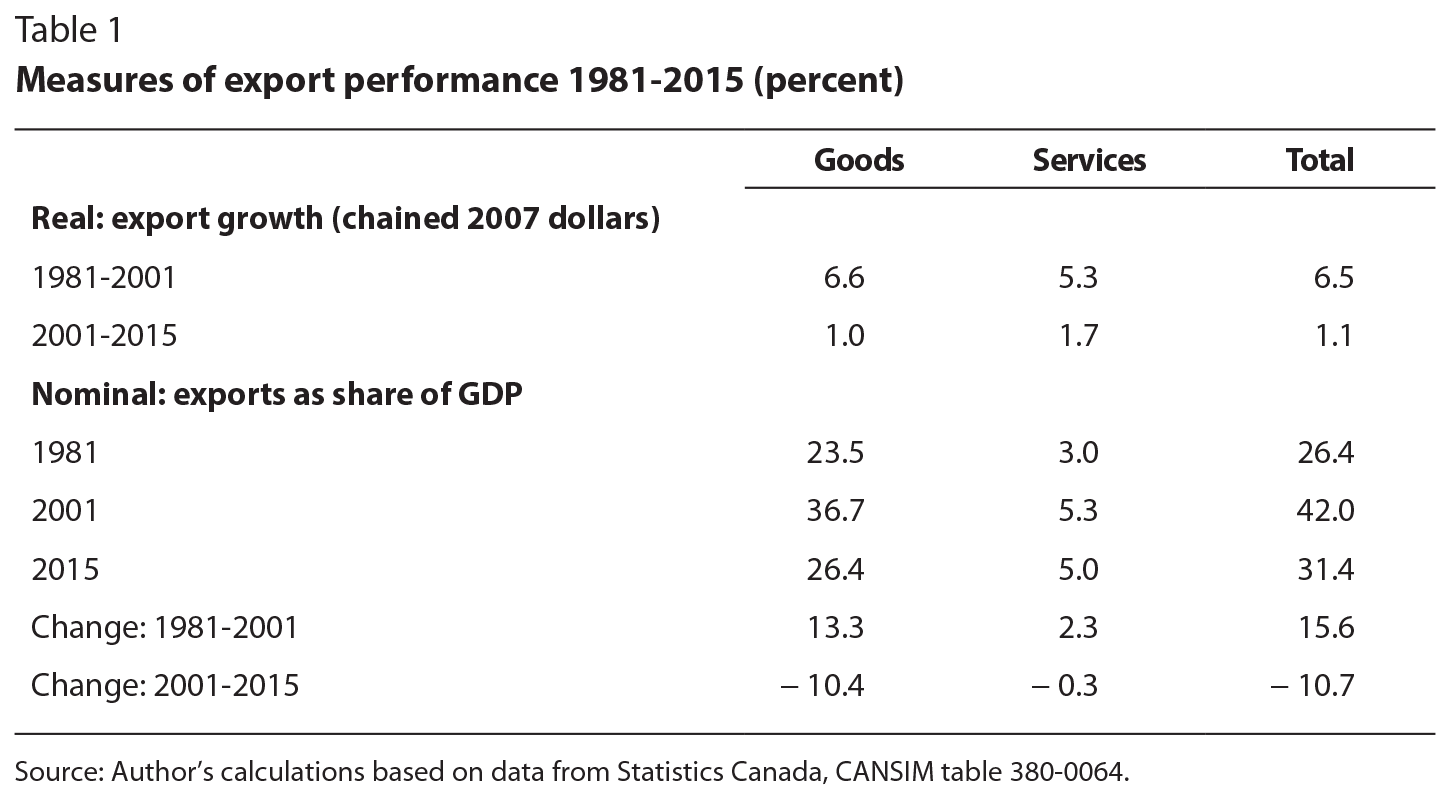

The story of Canada’s export performance since 1981, shown in table 1, indicates that, in the last two decades of the previous century, exports of both goods and services grew robustly, both in real terms and as a share of gross domestic product (GDP). Over that period, total exports grew by an average of 6.5 percent per year, providing a consistent stimulus to total output growth and job creation. Goods exports grew slightly faster than services, but both grew much faster than overall GDP and, as a result, total gross exports grew dramatically, from 26.4 percent of GDP in 1981 to a peak of 42.0 percent in 2001. Adjusting to the new North American free trade zone was clearly one driver of this growing trade intensity, but Canada’s exports to other jurisdictions also grew strongly.

After that point, however, the export engine that powered Canada’s economic growth stalled. Since 2001, exports of goods have grown by only 1 percent per year — the slowest annual growth in Canada’s postwar history. Exports of services have been a bit better, growing almost twice as fast as goods, but less than one-third their pace between 1981 and 2001, and slower than the growth of GDP. As a share of GDP, goods and services exports have shrunk since 2001. By 2015, the share of exports had fallen to 31.4 percent of GDP, in the process undoing most of the increase in trade intensity that occurred between 1981 and 2001. Curiously, by this measure, Canada’s economy has “deglobalized” since the turn of the century.

With imports growing faster than sluggish exports, trade balances and current account balances have deteriorated significantly (figure 3). In the 1980s and 1990s, Canada recorded consistent trade surpluses in goods of close to 3 percent of GDP. These surpluses were more than offset by other current account flows — notably, net outflows of investment income — together with services trade deficits. As a result, overall current account deficits averaged around 2 percent of GDP, financed through net capital inflows, largely associated with rising public debt. Then, in the first decade of the twenty-first century, merchandise surpluses widened, driven largely by higher nominal values for resource exports, and Canada generated modest current account surpluses for a while. But the decline in nonresource exports combined with the eventual collapse in resource prices then created a dramatic deterioration in merchandise trade balances, pushing Canada into merchandise trade deficits — unusual in its history. Current account deficits have been even larger, exceeding 3 percent of GDP on average since 2010 and spurring a sustained increase in Canada’s net foreign indebtedness.

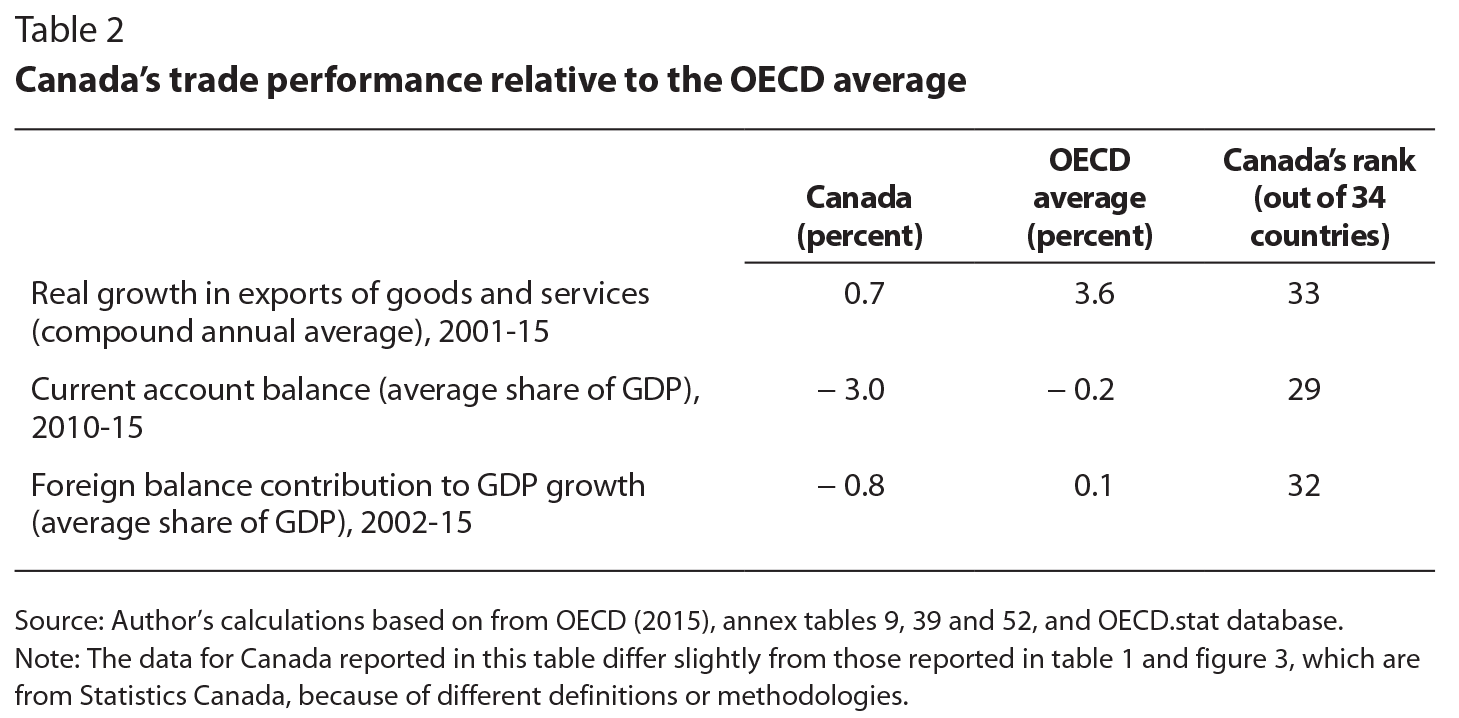

Canada’s export performance since 2001 has also been weak relative to that of other industrial countries, suggesting that its recent trade failures cannot be blamed solely on global macroeconomic conditions. This is confirmed by De Backer and Miroudot (in this volume), who analyze data on countries’ growing participation in global value chains — Canada has not kept pace with developments in the rest of the world over the past 15 years, and this contributes to poor export performance. de Munnik, Jacob and Size (2012) also find that Canada’s export performance since the turn of the century has been among the worst of any industrial country. As table 2 shows, the average annual real growth of Canada’s goods and services exports between 2001 and 2015 was only one-fifth of the average pace for the Organisation for Economic Co-operation and Development (OECD) as a whole, with Canada ranking 33rd out of 34 countries on this indicator. Canada’s average current account deficits since 2010 are also among the worst of any OECD country, and the ongoing drag on total output caused by deteriorating trade balances has been the third worst of any OECD country.

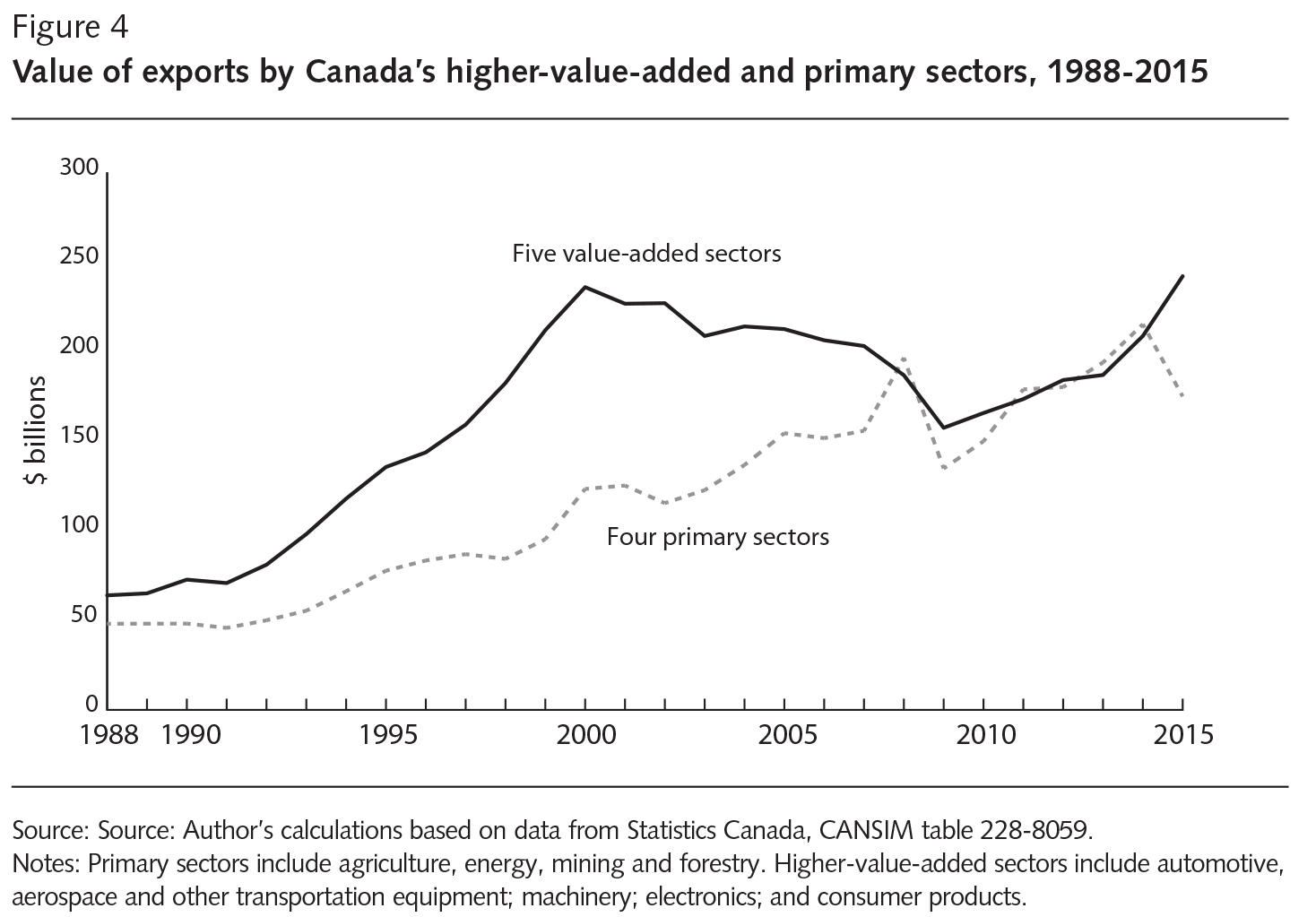

But it is not just the quantity of Canada’s net exports that has been disappointing; there has also been an important and, in my view, troubling deterioration in the overall quality of Canada’s exports. Through the 1990s, exports of sophisticated manufactured products expanded steadily, driven by several factors: the high quality and cost competitiveness of Canada’s production, incoming foreign investment in manufacturing, and strong growth in the US market — the destination for most of Canada’s exports. By 1999, the five high-value-added sectors (automotive, aerospace and other transportation equipment, machinery, electronics, and consumer products) together accounted for almost 60 percent of Canada’s goods exports, while the primary sectors (agriculture, energy, mining and forestry) accounted for just one-quarter.3 Thus, Canada had largely escaped its legacy as a supplier of unprocessed “staples” to the rest of the world (figure 4).

After the turn of the century, however, the global commodities boom shifted capital and policy attention toward extractive industries, a reallocation reflected in the rapid change in the composition of Canada’s exports. By the onset of the global financial crisis in 2008, higher prices and growing real quantities of resource exports made primary products the most important component of total exports. Renewed growth in resource exports (especially oil) continued even as the global and Canadian economies recovered from the 2008-09 recession. By 2014, the four primary sectors accounted for 40 percent of total exports, eclipsing the importance of the higher-value-added sectors.4

Other indicators also suggest that Canada’s economy has been “deindustrializing” — moving down, rather than up, the economic value chain. For example, Canadian innovation activity has fallen steadily since 2001, with business research and development (R&D) spending as a share of GDP falling by over one-third to just 0.8 percent in 2015 — the lowest share ever recorded.5 Other research confirms the failure of Canadian firms to innovate, increase productivity and implement technology (Expert Panel on the State of Industrial R&D in Canada 2013). Both Canada’s absolute score and its relative ranking by the Observatory of Economic Complexity — which quantifies the level of complexity and development of different national economies based on a composite measure of exports, imports, production and technology — have plummeted. From being one of the most technically complex economies in the world, ranking 6th in 1980, Canada had become one of the least technically complex of any OECD country by 2013, ranking 33rd, a decline in relative complexity that was the most rapid of any industrial country (Observatory of Economic Complexity, n.d.). Canada’s growing focus on primary extraction and exports is not the only factor in this worrisome trend, but it is clear that renewed dependence on raw resource extraction has reshaped Canada’s entire economy and reduced its stature in the world as a source of knowledge, innovation and productivity.

Several factors have contributed to these disappointing outcomes in Canada’s external commerce, some tied directly to the temporary boom in global resource prices and resulting reallocation of economic activity. The Canadian dollar soared along with commodity prices6 to levels far above purchasing power parity (PPP),7 which reinforced the erosion of Canadian manufacturing, tourism and tradable services, and accelerated the concentration of exports in resource sectors. The overvalued currency also encouraged a reallocation of resources to nontradable sectors, which were less affected by the loss of competitiveness from the stronger dollar, and this contributed to the decline in trade intensity experienced across the economy. Other factors include the rise of formidable new competitors — especially China, which has undermined Canada’s share of key export markets — the severe recession and slow recovery experienced in the United States, still the destination for over three-quarters of Canadian exports, and Canada’s relatively small export presence in the fastest-growing regions of the global economy, particularly east Asia.

Domestic factors have also contributed to the weak growth in Canadian exports, the concentration of exports in a few resource sectors and Canada’s subsequent vulnerability to the inevitable downturn in global commodity prices. Poor business innovation has undermined the competitive position of Canadian firms in innovation-intensive manufactures and services. Unfavourable patterns of business formation and firm growth have hollowed out the private sector, eroding the role of mid-sized firms, the population of which has actually declined (Business Development Bank of Canada 2013). Compared with other industrial economies, Canada relies more on very small firms (including self-employment) that typically demonstrate weak innovation activity, propensity to export and productivity. Successful Canadian start-ups in globally oriented sectors are often sold to larger foreign companies, rather than continuing to grow organically. As well, numerous foreign takeovers of larger Canadian firms also might have undermined the capacity of Canadian business to project itself successfully onto the global stage.8

Interestingly, this unprecedented and damaging deterioration in Canada’s international trade performance occurred precisely coincident with the most far-reaching agenda of trade and investment liberalization Canada has ever pursued. Yet when policy-makers and political leaders are confronted with these discouraging trade results, they often propose doubling down with further trade liberalization. But what if lack of access to foreign markets has not been the key factor behind Canada’s flagging exports and widening trade imbalance? And what if, given underlying structural weaknesses in Canada’s international engagement, further trade liberalization only makes matters worse?

What are FTAs meant to do? Trade deals in the tradition of the North American Free Trade Agreement (NAFTA) — including those Canada has recently negotiated — contain a wide range of provisions that affect trade and investment. First, they mutually reduce tariffs and nontariff barriers. This, the most straightforward feature of an FTA, will stimulate more trade in both directions — but not necessarily in equal measure. Various trade flows are affected differently by mutual liberalization, depending on the initial size and balance of trade flows, the initial level of tariffs and the speed of their reduction, demand elasticities, macroeconomic and exchange rate effects and other factors. Increases in mutual, balanced trade are believed to facilitate mutual gains in efficiency arising from the reallocation of factors of production. But larger gains in GDP and employment occur if the trade deal results in larger net exports (with exports growing faster than imports), and vice versa when imports are stimulated more than exports.

Second, FTAs, by enhancing mutual awareness of markets, spurring FDI in both directions, encouraging “gravity effects” (which reinforce the growth of trade through closeness and familiarity) and other indirect effects, can spur structural, nonlinear change in trade patterns above and beyond the normal effects of tariff elimination.

Third, most FTAs include extensive provisions liberalizing the international movement of direct investment and finance. This might facilitate both inflows and outflows of capital spending. As with trade flows, the net benefit for Canada might depend on whether more investment enters or leaves the country because of a trade deal.

Fourth, FTAs contain far-reaching provisions curtailing government regulatory powers in wide parts of the economy, including in less easily traded sectors such as services. The goal of these provisions is to cement a generally market-oriented, business-friendly environment throughout the trading area. This effect is reinforced through provisions such as the investor-state dispute settlement mechanisms pioneered in NAFTA and replicated in recent FTAs — and which have become controversial recently, particularly in Europe (see Newcombe, in this volume).

The coincidence of the sharp deterioration of Canadian trade performance and the aggressive expansion of free trade ties should cast some doubt on the value of trade liberalization for Canadian exports and trade balances. Of course, whether the former was “caused” by the latter depends on a more complex analysis of the causes of Canada’s trade failures and a judgment on what would have occurred in the absence of new trade agreements. Nonetheless, some insight into this relationship can be gleaned by looking at the average annual change in trade flows between Canada and its free trade partners on one hand, and between Canada and the rest of the world on the other (table 3). It should be noted that about two-thirds of Canada’s total trade, including three-quarters of exports and 55 percent of imports, occurs with the United States, about 5 percent of bilateral trade occurs with other FTA partners — Mexico being the most important — and close to 30 percent of bilateral trade occurs with non-free-trade partners.

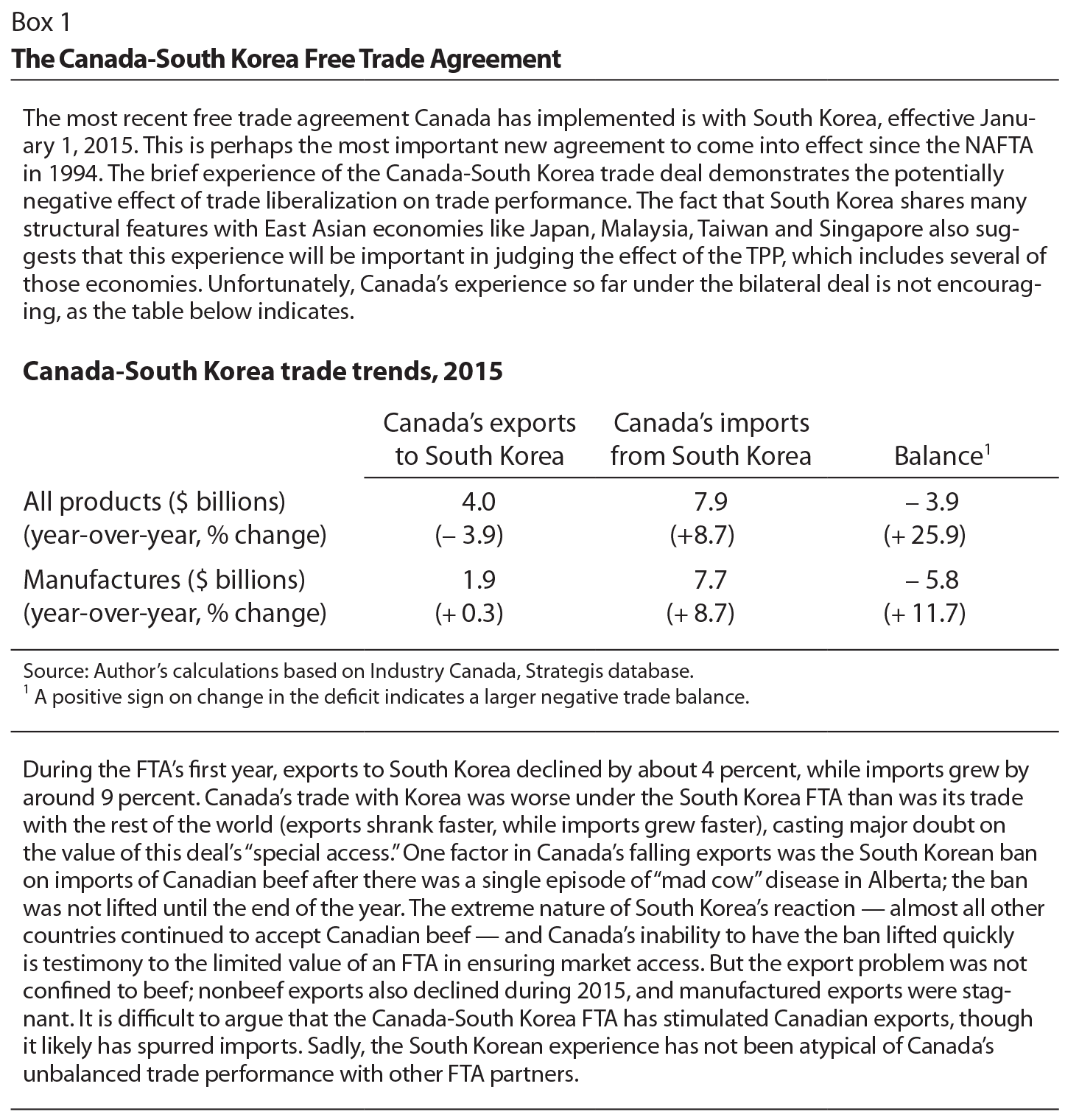

Considering all products, Canada’s exports to FTA partners grew slowly after 2001: by just over 1 percent annually to the United States and only marginally faster to the other FTA partners. Canada’s exports to South Korea, its most recent FTA partner, have actually declined under free trade (see box 1). In contrast, exports to countries with which Canada does not have a free trade deal grew over six times faster. This is certainly an inconvenient result for those who claim that Canadian exports have been held back by a lack of access to foreign markets — access that signing more FTAs is assumed to improve significantly.

Also striking are the results for imports, which grew about twice as fast from Canada’s FTA partners as did exports to them, and were the key driver of Canada’s deteriorating overall trade balance. Imports grew somewhat faster from non-US FTA partners than from the United States, mostly reflecting the rapid growth of imports from Mexico over the 2001-14 period. Imports from non-FTA partners, however, grew twice as fast, while only with non-FTA partners did Canada’s exports grow faster than its imports — again challenging the implicit assumption held by many in the trade policy community that FTAs are necessary to expand trade.9 The difference in Canada’s trade performance between FTA partners and non-FTA countries is even starker for manufactured goods, exports of which to FTA partners actually declined over the period, while imports of manufactured goods from those partners grew by between 1 and 2 percent. In contrast, exports of manufactured goods to non-FTA partners grew respectably, by 4.2 percent per year — almost as quickly as Canada’s imports of manufactured goods from those countries.

In traditional comparative advantage economic theory, trade liberalization stimulates an expansion of two-way trade flows that reflect each trading partner’s relative cost advantages. Efficiency gains from the resulting mutual specialization create the basis for net welfare gains; overall employment is assumed not to change, and output is assumed to be limited only by supply (not aggregate demand).10 Importantly, “competitiveness” is not a relevant variable in this theoretical approach, because every jurisdiction holds a relative cost advantage producing something — and market forces generating full employment of resources (including labour) are assumed to push every jurisdiction in a liberalized context toward specialization in those relatively advantageous goods and services.

In the real world, however, idle resources are a normal state of affairs, reflecting aggregate demand constraints. Shifts in demand, therefore — including those arising from international trade imbalances or net investment flows — can cause gains or losses in output that typically swamp the efficiency gains expected from comparative advantage specialization. One of the factors that can affect demand is international trade, experienced through trade imbalances and international net investment flows. In this case, a country’s “competitiveness” is not automatic and will affect a country’s experience under trade liberalization. Overall competitiveness determines a country’s ability to sell exports into world markets, generate trade surpluses that enhance, rather than subtract from, aggregate demand, and attract FDI in a world where business capital spending is scarce and highly mobile. In this context, trade liberalization might help or hurt a country, depending on whether it stimulates more exports than imports, and more inflows of capital expenditure than outflows.

If we relax the traditional, unrealistic assumptions of neoclassical trade theory, it becomes possible to reconcile Canada’s deteriorating trade performance since the turn of the century with the aggressive trade -liberalization policies the federal government pursued over the same period. It seems clear to me that Canada’s exports were simply not broadly competitive during this period, partly because of underlying structural weaknesses — including a lack of innovation and the growing concentration of exports in unprocessed resources — and partly because of a rapidly appreciating currency. Similarly, apart from short-lived periods of major capital inflows targeted at resource industries, Canada has not been a particularly appealing site for FDI. In fact, despite resource takeovers, more FDI left Canada than arrived over the 2001-14 period, and weak business investment generally — again, apart from temporary surges in resource projects, especially oil — has been a chronic restraint on Canada’s GDP and employment growth.

For an economy that is not adequately competitive in trade and investment on either cost or noncost grounds (the latter include innovation and quality), NAFTA-style trade liberalization, by stimulating export and investment opportunities in both directions without a guarantee of balance in those impacts, can cause more harm than good. Widening trade deficits as new imports overwhelm export growth, and failure to attract sufficient investment spending, might undermine growth and employment through demand-side effects that are more immediate and substantial than the incremental productivity gains projected to be the main benefit of increased two-way trade. Indeed, these reactions have contributed to the unprecedented deterioration in Canada’s trade performance and its weak macroeconomic performance since 2001.

The policy implications of this alternative understanding of the working of trade liberalization are important. The typical approach of signing more free trade agreements with more and larger trading partners must be interrogated critically. So must be the widely held belief — informed in part by trade models that are not applicable to a demand-constrained world — that trade liberalization is mutually and universally efficiency enhancing and welfare improving. Repeated (and rather repetitive) debates in Canada about whether to sign the next trade agreement have been largely beside the point in improving our understanding of the causes of and remedies for Canada’s global underachievement. Lack of access to foreign markets is not the main thing holding back Canada’s exports. We need measures other than the signing of FTAs to effectively boost exports, investment and innovation. As for evaluating the likely effects of new trade deals, we need a more pragmatic and empirically based approach, rather than taking it for granted that trade -liberalization is always mutually beneficial thanks to the working of market-driven comparative advantage processes. Here are some of the main conclusions I take from the preceding analysis:

At the very least, we should be open to the possibility that FTAs are not a magic bullet for Canada’s trade ailments. Their effects can be positive or negative, depending on their provisions, the trading partners involved and the readiness of Canadian industries to grow exports and attract mobile investment. In my view, in the past 15 years FTAs have probably done more harm than good to Canada’s trade and foreign investment record. Developing Canadian-based firms that produce goods and services the rest of the world demands, and helping them to upgrade their activities and project themselves more effectively onto the global stage would do far more for Canada’s trade performance than carrying on the quest for yet another blockbuster trade deal.

The author thanks Stephen Tapp and two reviewers for very useful suggestions.

Business Development Bank of Canada. 2013. What’s Happened to Canada’s Mid-Sized Firms? Montreal: Business Development Bank of Canada.

de Munnik, D., J. Jacob, and W. Sze. 2012. “The Evolution of Canada’s Global Export Market Share.” Working Paper 2012-31. Ottawa: Bank of Canada.

Expert Panel on the State of Industrial R&D in Canada. 2013. The State of Industrial R&D in Canada. Ottawa: Council of Canadian Academies.

Global Affairs Canada. 2016a. Canada’s Free Trade Agreements. Accessed March 9, 2016. https://www.international.gc.ca/trade-agreements-accords-commerciaux/agr-acc/fta-ale.aspx?lang=eng

———. 2016b. Foreign Investment Promotion and Protection Agreements (FIPAs). Accessed April 1, 2016. https://www.international.gc.ca/trade-agreements-accords-commerciaux/

agr-acc/fipa-apie/index.aspx?lang=eng

Observatory of Economic Complexity. n.d. “Economic Complexity Rankings (2013).” Accessed March 14, 2016. https://atlas.media.mit.edu/en/rankings/country/2013/

OECD (see Organisation for Economic Co-operation and Development)

Organisation for Economic Co-operation and Development (OECD). 2015a. National Accounts at a Glance. Paris: OECD Publishing.

———. 2015b. OECD Economic Outlook, December. Paris: OECD Publishing.

Stanford, J. 2003. “Economic Models and Economic Reality: North American Free Trade and the Predictions of Economists.” International Journal of Political Economy 33 (3): 28-49.

Montréal – Au lieu de multiplier les accords commerciaux, le Canada doit prioritairement trouver de nouveaux moyens de soutenir l’essor des entreprises du pays qui produisent les biens et services les plus en demande à l’échelle mondiale, affirme Jim Stanford. Son commentaire, qui sera publié dans un prochain ouvrage de l’IRPP, s’inscrit dans les débats en cours sur la mise en œuvre de l’Accord économique et commercial global (AECG) et du Partenariat transpacifique (PTP).

Bien que le Canada ait activement cherché à libéraliser ses échanges depuis une décennie, observe Jim Stanford (professeur d’économie à la Chaire Harold Innis Industry de l’Université McMaster et conseiller économique du syndicat Unifor), sa performance commerciale globale s’est fortement détériorée durant cette période, et de façon plus prononcée encore avec les partenaires des accords auxquels il participe.

« Nous devons absolument réexaminer cette conviction quasi religieuse — partagée par la plupart de nos décideurs et observateurs — selon laquelle la conclusion d’accords de libre-échange avec des pays toujours plus nombreux et importants est indispensable à l’amélioration de notre performance commerciale », soutient Jim Stanford.

Lorsqu’on examine nos échanges et nos investissements étrangers de la dernière décennie, explique-t-il, il ressort que ces accords ont probablement fait plus de mal que de bien à notre économie, car notre compétitivité à l’échelle mondiale a été très faible en termes de coûts, de qualité et d’innovation. Le Canada s’est placé à l’avant-dernier rang des 34 pays de l’OCDE au chapitre de la croissance réelle des exportations depuis 2001, une position lamentable.

« Nous continuerons de perdre des parts du marché international tant et aussi longtemps que nous tarderons à susciter des innovations à la hauteur des exigences mondiales en matière de produits et de procédés, prévient Jim Stanford. En aidant véritablement nos entreprises à s’imposer à l’étranger, conclut-il, nous pourrions dynamiser nos échanges et nos investissements de façon bien plus efficace qu’en signant d’autre accords spectaculaires.

On peut télécharger ce chapitre sur le site de l’Institut (irpp.org/fr).

Publié sous la direction de Stephen Tapp, Ari Van Assche et Robert Wolfe, Redesigning Canadian Trade Policies for New Global Realities sera le sixième ouvrage de la collection L’art de l’État de l’IRPP. Trente éminents experts (universitaires, chercheurs du gouvernement et autres spécialistes) d’ici et d’ailleurs y analyseront l’incidence de l’évolution des échanges commerciaux, des technologies, et du pouvoir économique et géopolitique sur les politiques canadiennes.

-30-

L’Institut de recherche en politiques publiques est un organisme canadien indépendant, bilingue et sans but lucratif, basé à Montréal. Pour être tenu au courant de ses activités, veuillez vous abonner à son infolettre.

Renseignements : Shirley Cardenas tél. : 514 594-6877 scardenas@nullirpp.org