Long-Term Care Financing: What’s Fair and Sustainable?

Frances Woolley

Approximately half of middle-income earners over 40 today are expected to see a significant decline in their standard of living upon retirement. While finance ministers have spent the past few years considering the future of the retirement income system, many of the reforms adopted or proposed do not address this impending income gap. For the bulk of baby boomers about to retire, these reforms either will be phased in too slowly to make a difference or they rely too heavily on ineffective voluntary savings plans.

In December 2012, provincial and federal finance ministers agreed to examine options for a “modest” expansion of the Canada and Quebec Pension Plans (CPP/QPP) at their next meeting in 2013. In this study Michael Wolfson, former assistant chief statistician with Statistics Canada, warns these proposals will also miss the mark unless more innovative options can be found.

To find these innovations, Wolfson argues, we must challenge conventional assumptions about pension reform. Most critical is the premise, underlying nearly every proposal to date, that future enhancements to the CPP/QPP must be fully funded. This requirement means new benefits can be drawn only as they are built up over time, thus extending the period for full implementation over nearly a half century.

Removing this condition, Wolfson estimates what would be required to enhance CPP/QPP benefits under an accelerated phase-in plan (over 20 years), while still ensuring the long-term solvency of the pension fund and maintaining affordable and stable contribution rates. Wolfson’s proposal assumes a doubling of the year’s maximum pensionable earnings to $102,200 and an increase in the earnings replacement rate from 25 to 40 percent on earnings beyond $25,550.

Looking at various scenarios using Statistics Canada’s microsimulation model, LifePaths, he finds that these objectives could be readily achieved if the age of eligibility for the enhanced benefits was set between age 68 and 70, three to five years later than the current eligibility age for the CPP/QPP (this would not affect existing benefits).

Wolfson also points out that as it is structured now, the CPP and QPP fall short in recognizing the significant disparities in health and life expectancy that exist between low- and higher–income earners and how these disparities affect the cumulative benefits received. The author proposes ways to adjust benefits to help compensate for these disparities in life expectancy without jeopardizing the solvency of the plans.

Taken together, these reforms would not only go a long way in securing the retirement income prospects of a large cross-section of Canadians, they would also encourage workers to remain in the labour force longer. This would contribute to increased levels of future consumption, higher tax revenues, and lower government spending on income support programs such as Old Age Security and the Guaranteed Income Supplement.

For the past few years, Canada’s finance ministers have been considering options for reforming Canada’s retirement income system, including expanding the Canada and Quebec Pension Plans (CPP/QPP). This was first signalled in June 2010 letters from federal Finance Minister Jim Flaherty, and from Ontario Finance Minister Dwight Duncan, to the other finance ministers. Since then, however, the process toward reform has been slow. The only notable change so far is the introduction of the voluntary, and probably ineffectual, Pooled Registered Pension Plan.1

At their December 2012 meeting, the finance ministers finally agreed that they would examine options for “modest expansion” of the CPP/QPP at their next meeting (Curry 2012). Unfortunately for interested Canadians, if the past is any guide, these discussions will occur behind closed doors. As a result, the range of options they will review is unknown. It is also unclear what detailed technical analyses will be available to inform these discussions. The purpose of this short study is to explore and provide initial assessments of potential options for expanding the CPP/QPP, and thus contribute to a substantive public discussion of the key policy issues involved.

This study relies on a highly sophisticated analytical tool, Statistics Canada’s LifePaths microsimulation model. It builds on my earlier review for the IRPP of the major inadequacies of Canada’s current retirement income system, which projected that half of middle-income baby boomers now reaching retirement age will experience a drop of at least 25 percent in their “net” or “consumable” income after retirement, whereas 100 percent continuity should be the norm (Wolfson 2011).

In the 2011 study, I examined several options to address this income shortfall, including the long-standing Canadian Labour Congress (CLC) proposal to double the CPP/QPP retirement benefit rate, so it replaces 50 percent of preretirement (gross) earnings, up from the current 25 percent (2009). My projection results showed that this would not offer much benefit to baby boomers. The main reason is the assumption in the CLC proposal (and all the proposals so far for expanding the CPP/QPP) that new benefits must be fully funded, as required under the Canada Pension Plan Act.2 Any enhanced benefits would therefore phase in very gradually over a period of almost half a century, thus offering only partial improvements for the impending large waves of retirees.

This study follows up on that analysis. It examines options for expanding the CPP/QPP in which the new benefits, which I call the “new CPP,” are phased in more quickly.3 Clearly, an accelerated phase-in would further increase pension costs. To address this concern, I have explored alternative scenarios that offset these added costs by raising the normal pension age (NPA), the age of eligibility for receiving the new benefits. Today, the NPA for the CPP/QPP is 65, although pensioners can start drawing benefits up to five years earlier or later, on an actuarially adjusted basis. The core idea is to compensate for the costs of increasing benefits and of phasing them in more rapidly by delaying the age at which they become payable, in order to maintain reasonable costs and preserve intergenerational fairness. To be clear, raising the age of eligibility would apply only to the new CPP/QPP (the top-up component), not to the existing CPP/QPP.

Still, raising the age of eligibility for pension benefits raises vertical equity issues within generations, because those with low earnings also have shorter life expectancies. Since the current retirement income system does not take account of these important differences between income groups, this study also explores how CPP/QPP reform might improve equity in this respect.

While these reform options may be considered well “outside the box” of current discussions, they serve to illustrate for finance ministers and Canadians a range of pension reforms that are feasible and meaningful.

The analysis here proceeds in a series of steps. First, I summarize the income adequacy challenges facing Canada’s future retirees, based on the results from my 2011 analysis. I then examine a sequence of CPP/QPP reform options — starting with enhancement, then accelerated phase-in of benefits, followed by raising the age of pension eligibility to offset the added costs and, finally, adjusting the benefit formula to compensate for the shorter-than-average life expectancies of low-earning individuals. For details about the model and the methodo-logy, see Wolfson (2011).

Public pensions play a number of important roles in promoting income security in old age. One is to reduce poverty by providing all elderly Canadians a guaranteed minimum income. Another is to pool risks, including the uncertainty about how long each of us will live. The focus of my earlier analysis, however, was the fundamental role played by public pensions in enabling individuals to maintain their standard of living after they stop working — in other words, to ensure the continuity of consumption possibilities between their pre- and postretirement years. People generally want to arrange their affairs so that there is no sharp drop (or sharp increase) in their consumption possibilities as they make the transition from paid work to retirement.

Retirement income adequacy is commonly measured on the basis of income replacement ratios comparing pre- and postretirement incomes. As I noted in my 2011 study, it is important to distinguish between income replacement rates that focus only on total or gross incomes before and after retirement (gross replacement rates) and those focusing on consumption possibilities (net replacement rates). For gross replacement rates, the adequacy benchmark is generally considered to be between 60 percent (e.g., Mintz 2009) and 70 percent (e.g., Dodge, Laurin, and Busby 2010) of preretirement income. Gross replacement rates typically measure the percentage of average annual income during the last (or best) five years of earnings that will be replaced by retirement benefits.

Net replacement rates, in contrast, take account of variations in taxes, savings and debt; changes in family size; the need to save for children’s education; housing wealth; and other factors that come into play throughout an individual’s working and postretirement years and affect consumption possibilities over time. (For a fuller description of how net replacement rates are calculated, see table A1 in the appendix of Wolfson 2011). As I showed in my 2011 study, gross replacement rates are generally a poor indicator of the net replacement rates individuals actually face.

The present analysis uses the net replacement rate as the main indicator of future retirement income adequacy. By definition, any deviation from 100 percent in the net replacement rate would indicate a change in consumption possibilities between working life and retirement; a rate inferior to 100 percent would indicate a reduction.

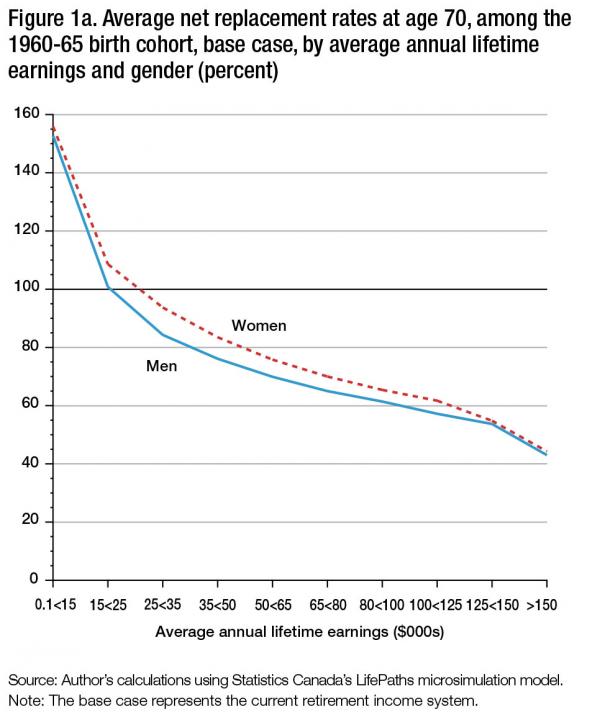

Figure 1a shows projected average net replacement rates, by income group and gender, under the current retirement income system (the base case), focusing on the cohort of baby boomers born between 1960 and 1965. Most of this cohort is now in its 50s, hence nearing retirement.4

As we can see, and as has often been reported, Canada’s retirement income system is very effective in supporting the income needs of low- and modest-income Canadians, and for these groups it certainly achieves adequate income replacement. The prospects for middle-income earners are more uncertain.

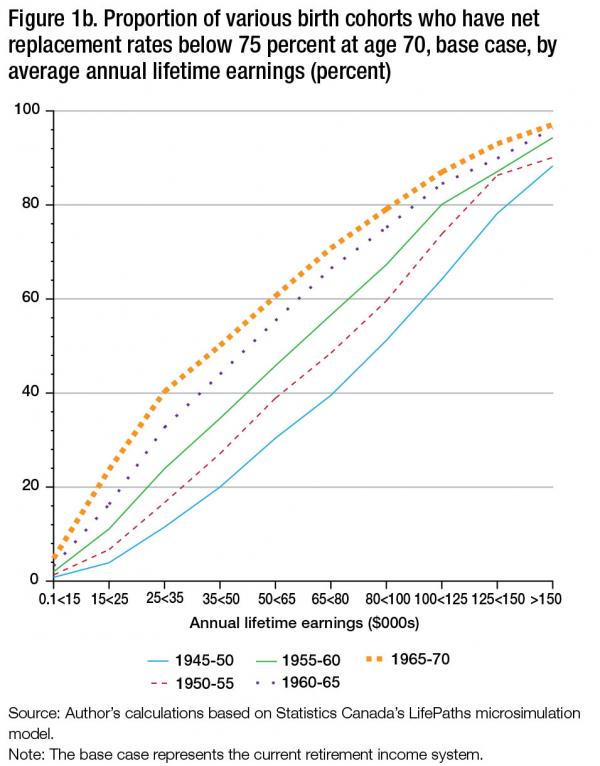

Another way to display the projected outcomes of the current retirement income system is in terms of the proportion of each birth cohort — based on five-year groupings — that is likely to experience a drop of 25 percent or more in their standard of living as measured by the net replacement rate. Figure 1b shows how these results vary across each of the baby boom cohorts (cohorts born between 1940 and 1970) by preretirement earnings. For younger (more recent) birth cohorts, there is an increase in the proportions who can expect a drop of at least 25 percent in their net income at the age of 70, relative to their average net income between the ages of 40 and 65.5

These differences among cohorts are most pronounced for those in the middle earnings ranges — the 50 percent of the population with average preretirement earnings between $35,000 and $80,000 per year.6 For example, for those earning in the $50,000 to $65,000 range, the -proportion projected to experience at least a 25 percent drop in their standard of living doubles from 30 percent for those born between 1945 and 1950 to 60 percent for those born 20 years later, between 1965 and 1970.

Why are these net replacement rates projected to get worse over time? One reason is the anticipated continuing decline in pension coverage and access to defined-benefit workplace pension plans for younger cohorts. Another major reason is the growing impact (with correspondingly larger effects on younger birth cohorts) of the indexing of Old Age Security (OAS) and Guaranteed Income Supplement (GIS) benefits. These programs are indexed to consumer prices, and not to nominal wages, which generally (though not so much in recent decades) rise faster than the Consumer Price Index (CPI). This means that the proportion of preretirement income replaced by these programs will be falling over time.7

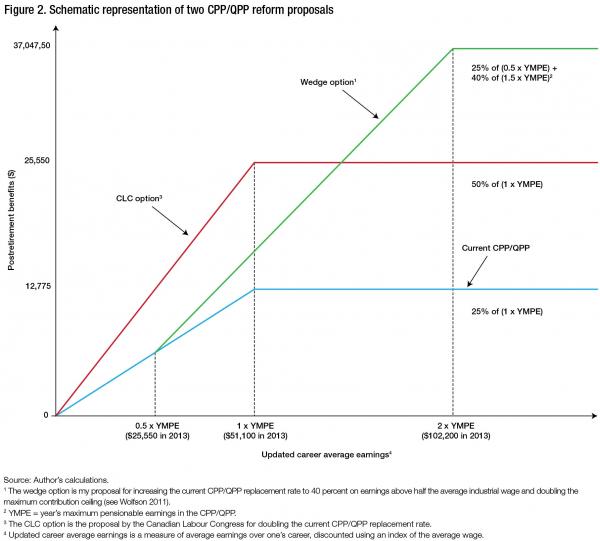

There has been considerable discussion in the last several years of what would be the most appropriate design for expanding the CPP/QPP. The Canadian Labour Congress (CLC) has long advocated that CPP/QPP benefits, presently set at 25 percent of updated career average earnings (i.e., wages and salaries of employees plus income from self-employment updated to current dollars using a wage index) be doubled to 50 percent. Others, aiming to provide better coverage for more workers, have suggested that it is also important to increase the year’s maximum pensionable earnings (YMPE). The YMPE, which is the earnings ceiling on which pension entitlements are calculated, is presently set equal to average annual wages. Further, since the observed and projected replacement rates of those with very low preretirement earnings is very high, a number of analysts have suggested that CPP/QPP benefits and contributions not be raised for these individuals. Indeed, raising pension benefits for this income group would in large part only displace income-tested GIS benefits, funded through general revenues, with benefits funded by a payroll tax.

In my 2011 study, I examined the CLC option as well as one of my own, which I refer to here as the “wedge” option. Figure 2 illustrates these two options, as well as the current CPP/QPP (blue line). The CLC option (red line) starts from the first dollar of updated career average earnings and increases the gross replacement rate from 25 to 50 percent. This proposal does not include any changes to the YMPE.

The wedge option (green line in figure 2), in contrast, would double the YMPE and increase the replacement rate to 40 percent, while also confining the replacement rate increase to those above a low-earnings threshold set at half the average wage. As shown in figure 2, the new incremental benefit is the area between the green line of the wedge option and the blue line representing the current CPP/QPP. 8 This wedge option is the basis for the proposed new CPP. The additional options examined in this study build on this policy scenario.

As I showed in my 2011 study, the wedge option, much like the CLC proposal, has only a modest impact on net replacement rates for members of the baby boom cohort. The key reason for this is the very gradual (almost half-century) phase-in of the enhanced benefit, based on the widely held premise that any expansion of the CPP/QPP must be fully funded, as required under current legislation.

But what would happen if we changed this assumption?

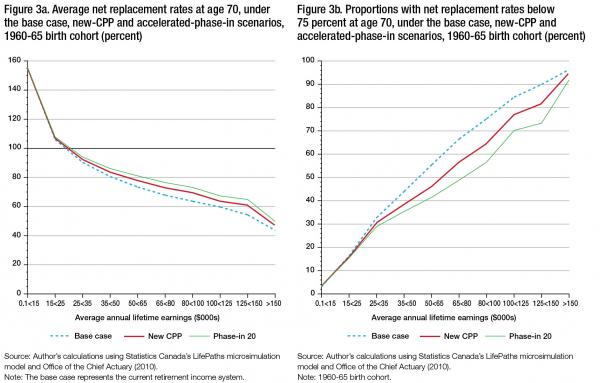

For the purposes of this analysis, I present a second reform scenario where the enhanced benefit is phased in more than twice as quickly, over a 20-year period. For both reform scenarios (new CPP with and without an accelerated phase-in), I assume that the reforms were implemented in 2011, for comparability with my previous analysis. Figures 3a and 3b illustrate these options. The scenario labelled “new CPP” in these figures is the wedge option — that is, the new-CPP option phased in with full prefunding, so that it is mature only after 47 years. In other words, individuals who are 18 years old in 2011 would be the first to receive full benefits when they reach 65 in 2058. Under the second reform option, the phase-in of benefits is accelerated to 20 years, so that full benefits would become payable as of 2031 (“phase-in 20”).

Figures 3a and 3b show how these two reform options differ from the status quo (the base case) in terms of their impact on net replacement rates and the proportion of Canadians (in this case the 1960-65 cohort) who would see a drop of at least 25 percent in their standard of living after retirement. Note that these projections take into account the current CPP/QPP, OAS, GIS, income and payroll taxes, private retirement savings, home ownership, and everything else that was included in figures 1a and 1b.9

The accelerated phase-in clearly has a substantial impact. It improves net replacement rates, especially those of people with mid-range preretirement earnings (figures 3a and 3b). For example, among those with preretirement earnings in the $50,000 to $65,000 range, the proportion who can expect a drop of at least 25 percent in their standard of living at age 70 is projected to decrease from 55 percent under the status quo, to 46 percent with the gradual phase-in of the new CPP and to 41 percent with the accelerated phase-in. For those in the $65,000 to $80,000 income range, the corresponding proportions fall from 66 percent under the status quo to 57 percent and then to 49 percent.

F

The costs of major government programs like the OAS, the GIS and health care are all highly sensitive to changes in the age structure of the population. These programs are all funded from general revenues on a pay-as-you-go, or PAYGO basis. Since they were introduced in 1966, the CPP and QPP have also been funded on a PAYGO basis (but from payroll contributions), and they still are for the most part. Some noteworthy changes were made to the plans in 1997, especially the substantial increase in contribution rates. A major objective of these changes was to increase the extent of prefunding from about twice to about five times annual benefit payouts. This was done to shift toward a “steady-state” funding approach, thereby ensuring stable contribution rates over the longer term. It is important to note that even at this higher level of prefunding, the CPP and QPP are still less than 20 percent fully funded today (Office of the Chief Actuary 2010, 70). The other change was the legislative requirement that any enhancement of CPP/QPP benefits be fully funded.

The first step in this analysis is, therefore, to determine what contribution rate is required to fully fund new-CPP benefits under the first scenario, where the benefits are phased in gradually over 47 years. For this, I have used the Chief Actuary’s estimate of 5.2 percent for the long-run cost of current CPP and associated survivor benefits (based on a 25 percent gross earnings replacement rate).10 To fund the 15 percentage point increase in the CPP replacement rate proposed under the new CPP, additional contributions equivalent to 3.1 percent of pensionable earnings (5.2 × (15/25)) would be required. This means that the current contribution rate would remain the same (at 9.9 percent) up to half the average wage (where the new CPP kicks in). It would increase to 13 percent (9.9 + 3.1) up to the YMPE (the current ceiling on CPP/QPP pensionable earnings) and then be set at 8.3 percent (5.2 × (40/25)) on earnings between the current YMPE and twice the average wage, given the doubling of YMPE for the new CPP.

The second scenario (expansion plus a 20-year phase-in of benefits), if fully funded, would of course require an even greater increase in contribution rates. This is an issue often raised by opponents of CPP expansion. It is therefore preferable to cap the payroll tax rate increases at 3.1 percent and 8.3 percent, respectively, as in the first scenario. While this would entail less than full funding of the new benefits, a very substantial fund would still be built up.

Some would argue that an accelerated phase-in of benefits that are not fully funded would provide a windfall gain to the baby boom generation, who would receive benefits in excess of what they had contributed to the fund. Indeed, this would be similar to what occurred when the CPP and QPP were introduced in 1966, though at that time the phase-in was twice as rapid, with full benefits granted after 10 years, for those retiring in 1976 and after. Such a windfall might be viewed as “undeserved.” However, as I have argued in my 2011 study, this view of intergenerational fairness is extremely narrow. In the first instance, it fails to recognize how the CPP and the QPP interact with other government programs. For instance, the new CPP can be expected to reduce GIS costs and increase income tax revenues. More broadly, a narrow preoccupation with the CPP/QPP in isolation from the rest of the economy fails to recognize the fundamental point that was made by the Chief Actuary: “To be -beneficial, any level of prefunding must lead to an increase in national saving and ultimately in economic output to supply the goods and services consumed by future retirees” (Office of the Chief Actuary 2007, 6). Yet, there is no guarantee that any degree of prefunding of CPP/QPP benefits will be matched by an increase in national savings — a myriad of other factors determine this savings rate.

To offset these arguments, albeit within the narrow ambit of the CPP/QPP (i.e., in isolation from the rest of the retirement income system and the economy more generally), I present a third reform scenario that offsets such a windfall. The trade-off for the baby boom generation is the gradual increase in the NPA, the normal age at which full benefits from the new CPP become payable.

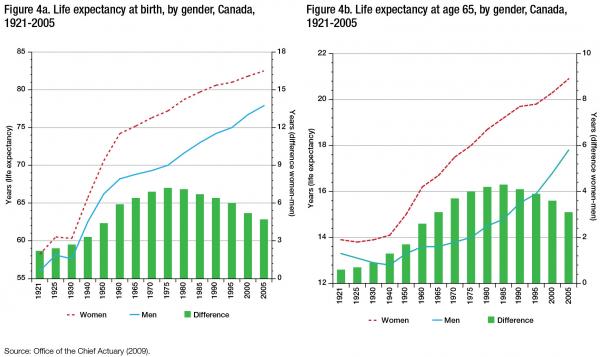

It is worth noting that increasing the NPA is also reasonable in light of the substantial increase in life expectancy. Figures 4a and 4b, taken from one of the Chief Actuary’s special mortality studies, show this demographic trend. Life expectancy at birth has increased by more than a decade per half century, and at age 65 it has increased by three to six years per half century (Office of the Chief Actuary 2009).

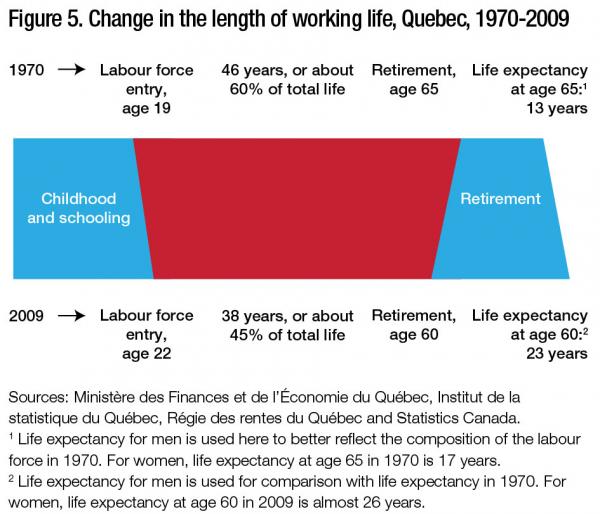

The final report of the Expert Committee on the Future of the Quebec Retirement System11 pointed to these changes in life expectancy and also to the trend toward a shortened working life. This is illustrated in figure 5 with respect to Quebec workers (2013, 13).12 This figure makes it clear that reducing the average number of years Canadians draw public pensions, or even simply preventing further increases (given ongoing increases in life expectancy), is justifiable.

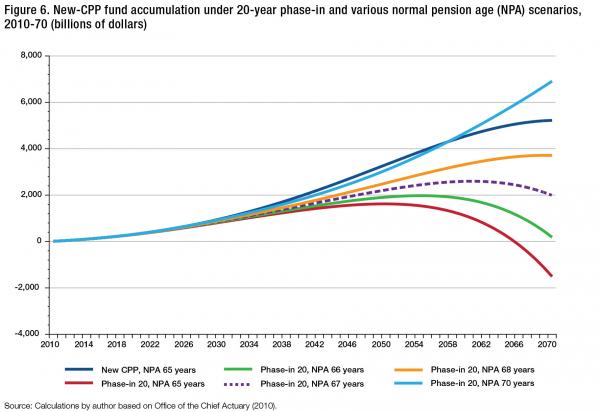

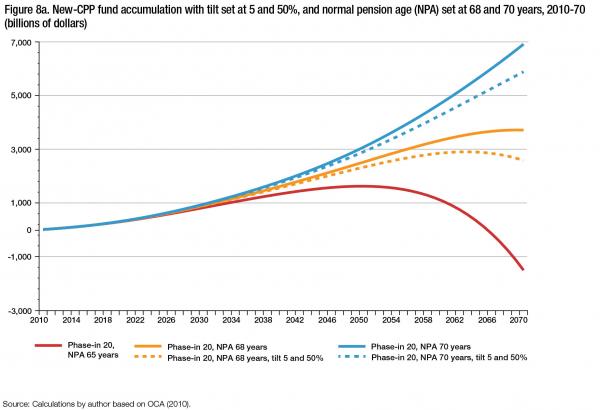

Figure 6 shows the impact that changes in the NPA (currently 65) would have on the fund balances.13 These fund balances pertain only to the new CPP, not to the current CPP/QPP, and are based on the benefit structure and contribution rate assumptions described earlier.

Expanding the CPP/QPP with full funding and without the accelerated phase-in generates a growing fund, though the growth rate slows by 2070. In contrast, a 20-year phase-in with no change in the NPA (maintaining it at 65), results in the projected fund going negative by 2066. But raising the NPA to 70 results in an even larger fund than full funding with no early phase-in at all. Thus, increasing the NPA to 68 appears to provide a reasonable balance. The projected fund size under this scenario is generally consistent with the steady-state funding objectives prescribed for the CPP/QPP under current policies.14

Note that although setting the pension age at 68 does not generate as large a fund as the full funding option, it still results in a huge fund — about $4 trillion. It is beyond the scope of this analysis to discuss the ramifications of such a large pool of capital being generated in the public sector, but this is clearly a major issue.

It is well known that higher-income individuals live longer.15 Indeed, they live longer than upper–middle-income individuals, who in turn live longer than those with middle incomes, and so on. In short, we observe a gradient in mortality with respect to income. The Chief Actuary’s special study on mortality includes a detailed examination of the mortality rates and life expectancies of CPP beneficiaries by preretirement earnings that clearly demonstrates these differences (Office of the Chief Actuary 2009, 43-5). To put this in perspective, a male CPP beneficiary aged 60 who receives the maximum pension available is projected to live nearly three and a half years longer than a male CPP beneficiary of the same age but at the bottom of the CPP benefit distribution who receives a pension equal to 37.5 percent or less of the maximum pension (Office of the Chief Actuary 2009, 47).16

The current CPP and QPP, however, take no explicit account of such differentials in mortality. (A modest exception is the year’s basic exemption [YBE] in the contribution rates.) Raising the NPA may therefore be seen as regressive, because workers with low pre-retirement earnings on average do not live as long as other workers, and would therefore receive a smaller cumulative amount of benefits (i.e., extending over fewer years). It could also raise other concerns regarding low-income workers who are likely to have more difficulty extending their careers.

One might argue, however, that the OAS and GIS are specifically designed to provide income support for low- and modest-income Canadians, so differences in mortality are already compensated to a considerable degree within the retirement income system. Still, to the extent it is preferable to have a retirement income system that emphasizes contributory retirement savings plans over income support programs funded by general revenues, the question of differential mortality is worth analyzing in the context of potential changes to the CPP/QPP. In this section, I set out two options to illustrate how this issue might be addressed.

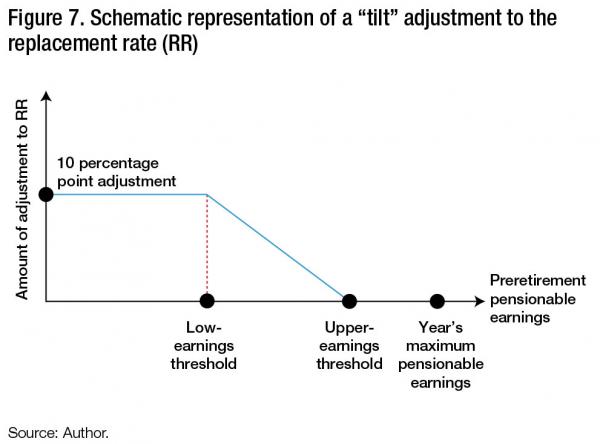

The cumulative amount of pension benefits received by individuals depends on both the benefit rate (dollars per year) and the period over which benefits are received (years). If we wanted to make the total benefits received over the entire retirement period more equitable across earnings groups, one option would be to adjust the earnings replacement rate, so that low-income individuals would receive higher pension benefits to compensate for their shorter-than-average life expectancy. For example, instead of the CPP replacement rate being set at 25 percent of earnings up to half the average industrial wage and at 40 percent of earnings between half and twice the average industrial wage under the expanded CPP, it could be set at a somewhat higher rate for those with low career average earnings. I refer to this adjustment in the replacement rate to compensate for differences in life-expectancy as the “tilt” option.

Figure 7 illustrates how this tilt option would operate. It would be based on three para-meters: a low-earnings threshold, an upper-earnings threshold and a benefit adjustment factor. Contributors with career average earnings equal to or below the low-earnings threshold would be eligible for the full benefit adjustment. In figure 7, I have assumed this adjustment factor to be 10 percentage points, meaning that earners in this group would receive pension benefits based on a replacement rate that is 10 percentage points higher than it would be otherwise. Beyond the low–earnings threshold, the adjustment factor would be progressively reduced, so that it would fall to zero when earnings reached the upper-earnings threshold.17

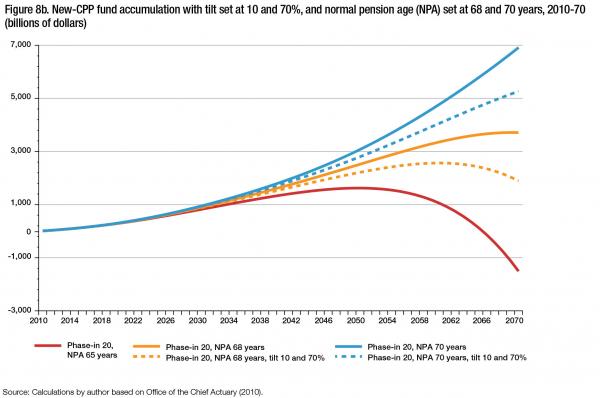

Simulation results for two tilt scenarios show how different parameters might affect the fund balance of the new CPP. In the first -scenario (figure 8a), the low-earnings threshold is set at 5 percent and the upper-earnings threshold at 50 percent of the new (doubled) YMPE . In the second scenario (figure 8b), these parameters are set at 10 and 70 percent, respectively. These thresholds are illustrative; again, both scenarios assume a maximum replacement rate adjustment of 10 percentage points for those below the low-earnings threshold, which declines in a linear fashion as earnings rise and reaches zero at the upper-earnings threshold.

Both tilt scenarios clearly add to the costs of the new CPP, so the fund grows more slowly with a tilt in benefits than without one, and more so in the 10/70 scenario (figure 8b). Still, with the NPA increased to 68, the fund remains substantial until 2070, at over four times annual benefits paid; this is not far off the ratio of assets to benefit payments under the current CPP as it stands today and as projected by the Chief Actuary. Combining an NPA of 70 with the proposed tilt would yield a fund that in 2070 would be over 20 times the amount of annual benefits paid. Overall, this suggests that by increasing the age of pension eligibility to the 68-to-70 range, it would be possible to implement a new CPP with a 40 percent gross replacement rate on a broad cross-section of earnings, a 20-year phase-in and a substantial life-expectancy adjustment for low-income earners that still meets the steady-state funding requirements of the current CPP/QPP.

The addition of a tilt option along these lines (as well as the increase in the age of eligibility) would likely trigger some changes in behaviour, especially among older workers with low earnings. These workers might choose more often to start drawing their new-CPP pension a few years earlier, as is already possible under the current CPP/QPP with appropriate actuarial reductions. Indeed, one of the major arguments for incorporating this kind of life-expectancy adjustment is precisely to give certain low-income older workers — for example, those with health problems, those having difficulty finding a job or those facing extenuating family circumstances such as an ill spouse — the option of taking their (actuarially reduced) pension at an earlier age, even though the NPA would be increased to 68 or 70. Although these questions are beyond the scope of this study, it is possible to explore these types of scenarios using the LifePaths simulation model.

Some economists are predicting that with the slower growth of and even a possible decline in the size of the working-age population, Canada faces a tightening labour market. This could put upward pressure on the wages of older workers. Those with higher preretirement earnings and white-collar jobs, in particular, might find it attractive to continue working to a new NPA of 68 and even beyond. Canada is already seeing an increase in the employment rate among those aged 60 and over. Statistics Canada’s 2005 time-use survey found that most people aged 65 and over find paid work their most satisfying activity. Exploring these potential trends toward later retirement with the simulation model, I have found that they lower the longer-run costs of the reform scenarios, leading to larger fund accumulations at the given contribution rates.

Although the current CPP and QPP offer some flexibility in the age of retirement — actuarially adjusted pensions can be drawn up to five years before or after the NPA — they still embody the presumption that retirement is a discrete event: that individuals transition from being workers to being retired from one day to the next. More to the point, the pension plans are not structured to facilitate the kind of gradual withdrawal from the labour market that is increasingly likely to occur. Although I have not simulated these kinds of scenarios, it would be desirable in the context of pension reform to examine the implications of allowing one or two stages in the retirement process. For example, new provisions might allow an individual to start drawing a half pension at 64 and then a full pension at 68, using proper actuarial adjustments.

It is also important to remember that the CPP/QPP reform scenarios examined in this study would have a broader impact. For instance, enhanced CPP/QPP benefits would generate increased income tax revenues and decreased GIS costs. The precise extent of these fiscal gains will vary with the calendar year, the pace of phase-in, the size and shape of the expansion and the design of any benefit tilt option. These gains can, however, be substantial. My simulations provide some estimates of these broader system-wide effects. In some representative cases, by 2051, GIS costs are reduced by more than one-tenth, while income tax revenues increase by amounts equal to more than one-half the total cost of GIS. More specific analysis of these offsetting fiscal effects should be part of any discussion of the kinds of pension reform examined here.

Canada’s finance ministers are on the verge of discussing potentially major reforms to the Canada and Quebec Pension Plans. But they will likely do so behind closed doors. It is unclear, therefore, what options they are considering. It is also unclear whether they are being provided with detailed policy analysis that considers the projected costs and distributional impacts across income groups of a useful range of feasible and beneficial reforms to Canada’s retirement income system.

In this study I have attempted to inform a broader policy discussion regarding how to ensure Canadians have adequate incomes in retirement. I have outlined a broad range of policy options that show it is possible to have an expanded mandatory defined-benefit pension plan for Canadians that significantly improves the adequacy of retirement incomes, especially for middle-income retirees.

There is wide agreement, though by no means consensus, that only a mandatory approach can be effective. Canada has over half a century of experience in providing very generous tax incentives for increasing private savings, which continue to fail in their basic objective. The substantial unused RRSP “contribution room” (Robson 2010) and the fact that Tax-Free Savings Accounts tend to be used most frequently by higher-income Canadians (Department of Finance Canada 2013) attest to this. Even the federal finance minister acknowledges that “many Canadians are not saving enough for their retirement” (Macleod 2012). And although it has not yet been fully implemented, the voluntary Pooled Retirement Pension Plan is not likely to resolve these problems.

The options I have examined in this study would be far more effective than these measures. They illustrate that a “grand bargain” could well be the best way to proceed — enhancing public pension benefits in an accelerated manner, while delaying the age at which they commence. The simulation results I have presented suggest that an increase in the age of pension eligibility for a new CPP from age 65 to between ages 68 and 70 (while maintaining the option of starting to draw benefits up to five years earlier or later on an actuarially adjusted basis) would be more than sufficient to ensure an adequately funded CPP/QPP expansion that would double the maxi-mum pensionable earnings level, increase the replacement rate from 25 to 40 percent of career average earnings above $25,550 and be phased in over 20 years.

Furthermore, the fact that higher-income individuals live longer than middle-income individuals, who in turn live longer than those with low incomes, need no longer be ignored by the CPP/QPP. I have shown that benefits can be tilted in a way that would help offset this differential mortality and would provide a meaningful option for low-income older workers who are facing difficulty finding or holding a job.

The goal of this study is to help broaden the scope of the discussion on pension reform and arrive at an effective solution for all Canadians. To that end, it is important that we think beyond conventional assumptions and seriously consider all potential avenues for improving the current CPP/QPP. Of course, proceeding with any CPP reform, whether modest or more ambitious, will require broad public support and a large degree of consensus among the provinces.

Lastly, I have also attempted to illustrate the kinds of sophisticated policy analyses that can be carried out using Statistics Canada’s LifePaths simulation model. Although this tool is complex, it is freely available and technically well within the capacity of interested government policy departments. It is also well within the purview of the CPP legislation for the relevant federal government agencies (such as the Chief Actuary’s office and the CPP branch of Human Resources and Skills Development Canada) to fund a unit dedicated to this kind of policy simulation without drawing on general government revenues.

We can only hope that Canada’s finance ministers, as they consider such fundamental issues as retirement income adequacy, avail themselves of the best possible information, and that they do so transparently by making this information public.

Canadian Labour Congress. 2009. Security, Adequacy, Fairness: Labour’s Proposals for the Future of Canadian Pensions. Ottawa: CLC.

Curry, B. 2012. “Finance Ministers Put CPP Reform Back on the Agenda.” Globe and Mail, December 17. https://www.theglobeandmail.com/news/politics/finance-ministers-put-cpp-reform-back-on-the-agenda/article6488900/#dashboard/follows/

Department of Finance Canada. 2013. Tax Expenditure and Evaluations 2012. Ottawa: Department of Finance Canada.

Dodge, D.A., A. Laurin, and C. Busby. 2010. “The Piggy Bank Index: Matching Canadians’ Saving Rates to Their Retirement Dreams.” E-brief no. 95, March 18. Toronto: C.D. Howe Institute. https://www.cdhowe.org/pdf/ebrief_95.pdf

Expert Committee on the Future of the Quebec Retirement System. 2013. Innovating for a Sustainable Retirement System: A Social Contract to Strengthen the Financial Security of All Quebec Workers. Summary Report. Montreal: Régie des Rentes du Québec.

Macleod, M. 2012. “Flaherty: Job No. 1 Is Kill the Deficit.” Hamilton Spectator, December 20. https://www.cybf.ca/cybf_press_media/flaherty-job-no-1-is-kill-deficit/

Mintz, J.M. 2009. Summary Report on Retirement Income Adequacy Research. Prepared for the Research Working Group on Retirement Income Adequacy of Federal-Provincial-Territorial Ministers of Finance. Ottawa: Department of Finance. Accessed March 8, 2011. https://www.fin.gc.ca/activty/pubs/pension/pdf/riar-narr-BD-eng.pdf

Office of the Chief Actuary. 2007. Optimal Funding of the Canada Pension Plan. Actuarial Study No. 6. Ottawa: Minister of Public Works and Government Services.

—————–. 2009. Canada Pension Plan Mortality Study. Actuarial Study No. 7. Ottawa: Minister of Public Works and Government Services.

—————–. 2010. 25th Actuarial Report on the Canada Pension Plan as at December 31, 2009.Ottawa: Minister of Public Works and Government Services.

Peters, P.A., and M. Tjepkema. 2011. “The 1991-2011 Canadian Census Mortality and Cancer Follow-up Study.” Proceedings of the 2010 International Methodology Symposium, October 26-29. Ottawa: Statistics Canada.

Robson, J. 2010. Are Today’s Working Canadians Saving Enough for Tomorrow’s Retirement? Policy Brief. Ottawa: Policy Horizons Canada.

Tjepkema, M., and R. Wilkins. 2011. “Remaining Life Expectancy at Age 25 and Probability of Survival to Age 75, by Socioeconomic Status and Aboriginal Ancestry.” Health Reports 22 (4).

Wolfson, M. 2011. Projecting the Adequacy of Canadians’ Retirement Incomes: Current Prospects and Possible Reform Options. IRPP Study 17. Montreal: Institute for Research on Public Policy. https://www.irpp.org/pubs/IRPPstudy/IRPP_Study_no17.pdf

This study was published as part of the Faces of Aging research program under the direction of Tyler Meredith. Copy editing was by Cy Strom, proofreading was by Barbara Czarnecki, editorial coordination was by Francesca Worrall, production was by Chantal Létourneau and art direction was by Schumacher Design.

Michael C. Wolfson was assistant chief statistician, analysis and development at Statistics Canada. He was awarded a Canada Research Chair in Population Health ModeLling/Populomics at the Faculty of Medicine, University of Ottawa, in 2010. Before joining Statistics Canada he held positions in the Treasury Board Secretariat, the Department of Finance Canada, the Privy Council Office, the House of Commons and the Deputy Prime Minister’s Office. He was a fellow of the Canadian Institute for Advanced Research Program in Population Health (1988-2003). Michael Wolfson is a fellow of the Canadian Academy of Health Sciences and a member of the International Statistical Institute.

To cite this document:

Wolfson, Michael. 2013. Not-So-Modest Options for Expanding the CPP/QPP. IRPP Study 41. Montreal: Institute for Research on Public Policy.

Montreal – As Canada’s finance ministers prepare to consider options for a “modest” expansion of the Canada and Quebec Pension Plans (CPP/QPP), a new study from the Institute for Research on Public Policy (IRPP) makes the case that unless policy-makers are willing to think “outside the box,” these reforms will be of little help to the next wave of retirees.

In the study, Not-So-Modest Options for Expanding the CPP/QPP, the former assistant chief statistician with Statistics Canada, Michael Wolfson, examines the impact of various options for CPP/QPP expansion. He finds that current proposals, which assume that any future benefit enhancement must be fully funded and, as such, would be phased in over a period of nearly half a century, will not address the projected gaps in retirement income.

“Approximately half of middle-income earners aged over 40 today are expected to see a significant decline in their standard of living upon retirement,” notes Wolfson. “A half-century solution won’t help them that much.”

Using Statistics Canada’s Lifepaths microsimulation model, Wolfson develops and assesses several options to improve the effectiveness of CPP/QPP reforms. What is needed, he argues, is a “grand bargain.”

Wolfson finds that if the age of eligibility for the CPP/QPP enhancement was raised to between 68 and 70, it would be possible to

“These reforms would go a long way in securing the retirement income prospects of a large cross-section of Canadians,” he said. Wolfson’s proposal would double the year’s maximum pensionable earnings from $51,100 to $102,200, and it would increase the income replacement rate from 25 to 40 percent on earnings above $25,550. It would reduce by one-quarter the proportion of middle-income earners now facing a significant decline in their postretirement standard of living.

More broadly, his proposed reforms would encourage workers to remain in the labour force longer, provide greater equity between income groups and contribute to higher levels of future consumption. “The options in this analysis provide crucial evidence supporting the kind of public debate that is needed if we are to get it right on pension reform,” said Wolfson.

Not-So-Modest Options for Expanding the CPP/QPP, by Michael Wolfson, can be downloaded free of charge from the Institute’s Web site (www.irpp.org).

-30-

For more details or to schedule an interview, please contact the IRPP.

To receive our monthly bulletin Thinking Ahead by e-mail, please subscribe to the IRPP’s e-distribution service by visiting our Web site.

Media contact: Shirley Cardenas tel. 514-594-6877 scardenas@nullirpp.org

Federal Finance Minister Jim Flaherty and his provincial counterparts, last December, agreed to consider options for a “modest” expansion of the Canada and Quebec Pension Plans in June, 2013. June has come and gone without this meeting. If and when a meeting does occur, it will likely be behind closed doors, and Canadians will not know what kinds of “modest” expansion options are being discussed. However, if the rare tea leaves provided by finance ministers are any guide, Canadians nearing retirement shouldn’t hold out much hope that these reforms will save the day.

In a study released this week by the Institute for Research on Public Policy (IRPP), I have used Statistics Canada’s Lifepaths model to project both the current retirement income system and some more “out of the box” options for meaningful reform. The projections show that about half of middle-income earners over age 40 today will see a significant decline in their standard of living post-retirement. This may come as a rude awakening for many.

Most pension experts agree with Mr. Flaherty when he says: “Canadians are not saving enough for their retirement.” So what’s the solution? All pension reform scenarios put forward so far assume that any new retirement benefits need to be fully pre-funded. This means it would take nearly half a century for any enhanced benefits to be fully phased-in.

Such a “modest” half-century solution won’t help many Canadians. Clearly more creative thinking is needed. My new analysis provides detailed estimates for a series of options that effectively address the retirement income challenges Canada faces today.

First, and most importantly, the Canadian Pension Plan (CPP) and the Quebec Pension Plan (QPP) remain the best vehicles for reforming the retirement income system. If middle-income Canadians want secure and adequate incomes in retirement, voluntary plans won’t do. They will have to force themselves to save more, and we all know this is unlikely to happen.

The most efficient and effective way for Canadians to save, by far, is to legislate the necessary earnings-based contributions to a broadly-based public fund; in short the CPP/QPP.

If we expand CPP/QPP, then it is important to ensure that the reforms effectively target the problem at hand. Full pre-funding of benefit enhancements has been the universal, though implicit, assumption in all recent discussions – in order to ensure contribution rates remain stable and hence the long-run solvency of the fund.

But full pre-funding is not necessarily the only way to accomplish the twin objectives of plan solvency and rate stability. Increasing the age of pension eligibility, combined with an appropriate increase in the contribution rate to pay for these new benefits, would also produce financial stability. For many Canadians, these contribution rate increases would be smaller than those brought in during the 1990s, which had no obvious adverse effect on Canada’s economy.

Increasing the eligibility age to between 68 and 70 (up from 65 today) would be sufficient to maintain financial stability while expanding and phasing-in new benefits more rapidly – over 20 years rather than nearly a half century. We could increase CPP retirement benefits from 25 to 40 per cent of pre-retirement earnings above $25,550 (half the average wage) and double the range of covered earnings from $51,100 to $102,200 (twice the average wage).

It would also be possible within this framework to adjust benefits for lower-income earners to compensate for their lower-than-average life expectancy and their shorter time drawing retirement benefits. This would address the greater impact of raising the eligibility age on lower income groups.

Trading off a later pension age for enhanced CPP/QPP benefits, phased in over a shorter time horizon, is appealing on many levels. This “grand bargain” would significantly improve retirement incomes, do so sooner, encourage workers to remain in the labour force longer, and provide greater equity across income groups.

Taken together, these changes would reduce by a quarter the proportion of middle-income earners now facing a significant decline in their standard of living post-retirement.

These options are probably not “modest” amongst those long opposed to any CPP/QPP expansion, but they illustrate what is possible, and what is needed, if we are to avoid a wide-spread drop in Canadians’ standards of living post-retirement.

It’s time that our finance ministers finally and meaningfully to address longstanding pension policy issues. Letting Canadians in on the discussions might be a good place to start.

Michael Wolfson is an expert advisor with EvidenceNetwork.ca and holds a Canada Research Chair in population health modeling/populomics at the University of Ottawa. He is a former assistant chief statistician at Statistics Canada, and has a PhD in economics from Cambridge.