Long-Term Care Financing: What’s Fair and Sustainable?

Frances Woolley

Medications prescribed outside a hospital setting are not covered by Canada’s medicare system. They are financed through a patchwork of private and public drug insurance plans that only provide coverage for select populations, leaving many Canadians with little or no coverage.

Up until the late 1990s, people 65 and older received universal, almost first-dollar public drug coverage in most provinces. But with population aging, the public liability associated with age entitlements has become a major concern for governments. Four provinces have discontinued their age-based programs, which covered most of the cost of medications for seniors, and -replaced them with income-based programs, which protect all residents against catastrophic drug costs. Other provinces have started to move or are considering moving in this direction.

Is this sound policy? Steven Morgan, Jamie Daw and Michael Law assess the performance of -income-based public drug plans against three key policy objectives: access, equity and efficiency. They review the theory and the evidence by comparing Ontario’s age-based and British Columbia’s income-based systems. They find that income-based plans perform poorly with respect to all of these objectives.

First, replacing age-based public plans with income-based drug benefit plans reduces seniors’ access to necessary medicines. The deductibles are a financial disincentive for patients to fill -needed prescriptions and they therefore reduce their adherence to the prescribed therapy. Second, it raises important equity issues. Deductibles under income-based plans impose considerable direct costs, especially on seniors, who are more likely to be high-needs users of prescription drugs. Third, income-based programs undermine cost efficiency because a large share of the residual costs falls to employers, unions and patients. Having multiple payers increases administrative costs and fails to leverage the purchasing power of government as the single payer in the pharmaceutical market place.

Policy-makers have portrayed the adoption of income-based plans as an expansion of previous programs because income-based plans cover patients of all ages, not just seniors. The authors of this study argue that what this really represents is a retrenchment of public drug benefits in Canada.

The authors recommend moving to public plans that offer full and universal coverage of prescription drug costs, financed through personal income taxes. Such plans would ensure better access, equity and efficiency than do those built around income-based deductibles. In particular, they would provide more equitable coverage for high-needs prescription-drug users. This approach would also enable government to achieve greater cost efficiencies and improve health outcomes. As the single payer, government would be better able to lower the price of brand-name and generic drugs, promote the use of generic drugs, help improve prescribing patterns, and take advantage of administrative and other cost efficiencies.

Most Canadians have heard the statistics: no matter how it is expressed, Canada’s population is getting older – and for the next few years, it will do so faster than ever before (Statistics Canada 2012). This will place modest but real financial strains on the current core of Canadian medicare: medical services and hospital care (Evans et al. 2001; Reinhardt 2003; CIHI 2011; Morgan and Cunningham 2011). Recent projections suggest that population aging alone will increase average per capita spending on medical and hospital care in Canada by about 1 percent per year for approximately 20 years – arguably an affordable pressure, even under modest forecasts for economic growth (Morgan and Cunningham 2011). But population aging will also reduce the size of our health care workforce, increase demands on informal caregivers and have significant impacts on certain components of the health care system, such as home care and long-term care (Chappell 2011; CIHI 2011; Keefe 2011). Policy responses to these challenges would ideally promote the health and well-being of the elderly while managing the economic impacts of their rising ranks.

The focus of this study is on pharmaceuticals – a critical component of modern health care. Since the 1970s, a relatively steady stream of first-of-kind drugs have been brought to market to address an increasing variety of health care needs (Morgan, Cunningham, and Law 2012). When prescribed and used appropriately, prescription medicines can prevent illness, aid in symptom management, and even cure disease – making them in many cases the most cost-effective form of health care. Due in part to their increased availability and use, prescription drugs have been one of the fastest-growing components of health care costs for decades: total pharmaceutical expenditure growth outpaced growth in overall expenditure on hospitals and doctors in the 1980s, 1990s and 2000s (CIHI 2013). Despite slower expenditure growth since 2010, pharmaceuticals remain one of the largest components of health care spending in Canada – second only to hospitals in terms of overall cost. Moreover, spending on pharmaceuticals in Canada has outpaced spending in almost all comparators internationally since the 1990s (Morgan, Kennedy, et al. 2009; OECD 2014).

The pharmaceutical component of health care is also an area where the effects of population aging are particularly acute for government-run insurance programs in Canada. Though critically important from a public policy perspective, this cost pressure has less to do with population aging per se than it does with the way in which prescription drugs are financed in Canada’s health care system.

Canada’s medicare system is the only universal health care system in the developed world that excludes universal coverage of prescription drugs. Whereas the Canada Health Act ensures that all residents receive comprehensive public insurance for prescription drugs used in hospital, such universal coverage does not extend to the community setting. Rather, prescription drugs in -Canada are financed by a patchwork of public and private drug plans that leaves many Canadians with little or no drug coverage (Daw and Morgan 2012). Public drug benefit programs in Canada evolved in ways that historically resulted in public coverage for select populations only. Seniors held a privileged place in this system – they received universal, near first-dollar public drug coverage in most provinces through to the 1990s (Grootendorst 2002). But now, in the face of an aging population, public drug benefit programs for seniors are under significant pressure.

The reason is simple: when residents turn 65 in provinces that offer public prescription drug benefits at little or no charge to patients in their senior years, their drug costs shift from being a largely private liability to a largely public one. While the societal costs of medicines used by patients do not change dramatically when they turn 65, the disproportionate number of people who are turning 65 shifts a greater and greater proportion of medicine costs to the public purse. The resulting financial pressure has prompted significant reforms to public drug plans. Indeed, avoiding the public liability associated with such an age entitlement to public subsidies was a stated motivation for the elimination of British Columbia’s seniors drug plan in 2003 and its replacement with Fair PharmaCare, a program providing residents of all ages with income-based public coverage against catastrophic drug expenses (Morgan and Coombes 2006). Thus far, three other provinces – Saskatchewan, Manitoba, and Newfoundland and Labrador – have also eliminated their comprehensive public drug benefit plans for residents age 65 and over, and replaced them with income-based programs. Such programs are accessible to residents of all ages and offer benefits to cover the costs of prescription drugs; benefits are calculated based on the beneficiaries’ household income (Grootendorst 2002; Daw and Morgan 2012). In addition, Ontario took a step in this direction in 2012 by reducing public coverage for seniors with incomes over $100,000 (Ontario 2012), while in 2013, Alberta considered a program modelled on British Columbia’s (Alberta 2013).

In this study, we assess the performance of income-based public drug benefit programs for Canada’s aging population. We first provide a brief history of public drug benefit policies in Canada. We then analyze recent trends in drug coverage, as several provinces are replacing their age-based programs with income-based programs, and we present a portrait of the current arrangements. We take the Ontario and the British Columbia plans as illustrative models. In the third section, we assess the performance of the program types with respect to three key policy goals: access, equity and efficiency. Our analysis shows that income-based public drug benefit programs perform poorly with respect to these goals. In conclusion, we recommend that governments in Canada work toward consolidating the purchasing power of all residents, regardless of age, under a universal, public drug benefit plan that provides full coverage for prescription drugs that are medically necessary and cost-effective. Doing so would improve access to medicines for all Canadians, better protect both seniors and nonseniors from the costs associated with their medical needs, and dramatically improve pharmaceutical cost control in Canada.

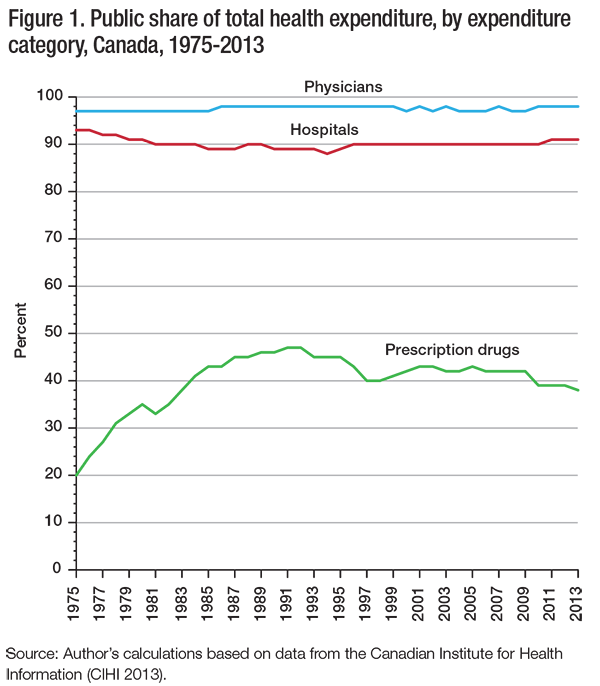

Every developed country with a universal health care system offers universal coverage of prescription drugs – except Canada. While medical and hospital care is almost exclusively publicly funded in Canada, and public health insurance programs have financed nearly all expenditures on physicians and hospitals in Canada since the mid-1970s (figure 1), government drug benefit programs have never financed as much as 50 percent of prescription drug expenditures. In fact, their share has been declining since the early 1990s (CIHI 2013).

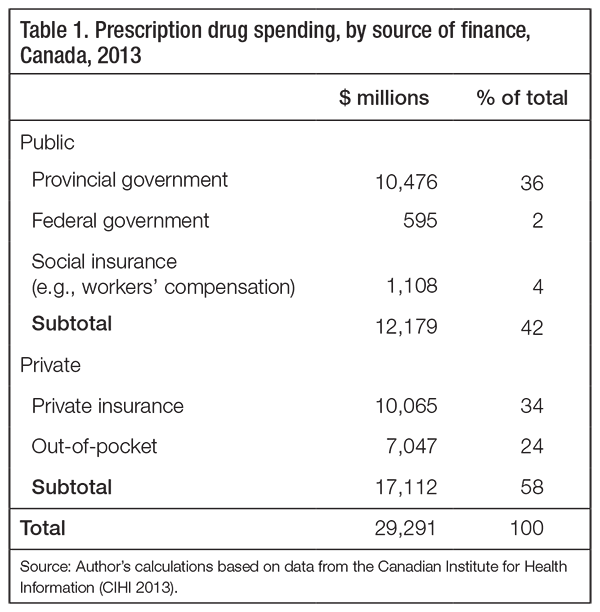

For Canada as a whole the share of prescription drug costs financed by provincial government drug benefit plans is 36 percent; for individual provinces it ranges from 26 percent in New Brunswick to 40 percent in Alberta (table 1). While the federal government does not provide any direct support for provincially run public drug benefit programs, it does administer public drug plans for registered First Nations people and Inuit, veterans, and other specific populations, which account for 2 percent of total prescription drug spending. In addition, drug spending as part of social insurance programs such as workers’ compensation represents a share of 4 percent. In total, the public share thus represents 42 percent of prescription drug financing. The balance (58 percent) comes from private insurance plans (34 percent) and from patients out-of-pocket (24 percent).

One of every two workers (51 percent) has supplemental medical coverage through his or her employer, which would typically include prescription drug coverage (Statistics Canada 2008). Most likely to have such coverage are workers who are university educated, work as managers or professionals, have more than 10 years of work experience and work full-time for a medium- or large-sized employer (Statistics Canada 2008). Because work-related health insurance plans also cover dependants of employees with coverage – and because some people purchase individual policies if they are not eligible for group-based coverage – as many as two-thirds of Canadians are covered in some way by private health insurance plans. Still, Canada’s system of financing prescription drugs leaves many citizens either underinsured or uninsured, despite decades of recommendations to expand drug plan coverage.

The 1964 Royal Commission on Health Services (the Hall Commission) provided a blueprint for developing Canada’s federally supported but provincially run health insurance system. This blueprint included a universal public drug insurance plan, with the commission arguing, “in view of the high cost of many of the new life-saving, life-sustaining, pain-killing, and disease-preventing medicines, prescribed drugs should be introduced as a benefit of the public health services program” (Royal Commission on Health Services 1964). The Hall Commission specified that the federal government should fund half of the cost of the program, that the public drug benefit program should cover only prescription drugs selected on the basis of evidence, and that patient charges should be limited to $1.00 or less per prescription – about $7.50 at today’s rate.

Prescription drug coverage was discussed by the federal government in the 1970s; however, that discussion was shelved because the government did not perceive sufficient public demand to make it a political win (Boothe 2012). In the absence of a national standard, each province independently developed its own public drug insurance program through the 1970s and 1980s (Grootendorst 2002). Most of these programs grew incrementally, starting with targeted programs for subpopulations with the greatest pharmaceutical needs or those with the least means to pay. Seniors received nondeductible coverage under the emergent provincial public drug benefit programs. Indeed, by 1986, all provinces in Canada had established some form of public program to provide prescription drugs at little or no cost to seniors – creating an implicit national standard for public drug benefit programs in Canada (Grootendorst 2002; Morgan, Barer, and Agnew 2003).

In 1997, the National Forum on Health revisited pharmaceutical coverage in Canada. It identified two key problems with the limited nature of provincial drug benefits (National Forum on Health 1997, 1998). First, many nonseniors were believed to be either underinsured or uninsured for necessary medicines. Second, the existence of multiple private and public payers for medicines in each province was believed to be reducing the purchasing power that could be exercised by a universal insurance program. The Forum therefore called for a universal public drug benefit program, arguing that “because pharmaceuticals are medically necessary and public financing is the only reasonable way to promote universal access and to control costs, we believe Canada should take the necessary steps to include drugs as part of its publicly funded health care system (National Forum on Health 1997). It specified that the public program should cover medicines selected based on evidence of comparative cost-effectiveness and that such coverage should be provided to all Canadians at little or no direct charge to patients (National Forum on Health 1997, 1998). As with the nearly identical Hall Commission recommendation in 1964, this 1997 call for universal public drug coverage was not acted on by the federal government and, thus, not acted on by any of the provinces.

Calls for national public drug benefit reform resurfaced in 2002. This time, the recommendations came from Roy Romanow’s report of the Commission on the Future of Health Care in Canada and Michael Kirby’s report on behalf of the Senate Standing Committee on Social Affairs (Commission on the Future of Health Care in Canada 2002; Standing Senate Committee on Social Affairs, Science and Technology 2002). As seniors in most provinces were receiving relatively comprehensive public drug coverage at the time, the Romanow and Kirby reports focused primarily on filling the existing gaps in coverage for nonseniors. Both reports emphasized the importance of ensuring access to appropriately prescribed medicines, with the Romanow report stating, “The current and potential benefits of prescription drugs are undeniable. But the benefits will only be fully realized if prescription drugs are integrated into the system in a way that ensures they are appropriately prescribed and utilized and that the costs can be managed” (Commission on the Future of Health Care in Canada 2002). Both Kirby and Romanow also argued for greater financial protection for patients facing high drug costs. For example, Kirby argued that “no Canadian should suffer undue financial hardship as a result of having to pay health care bills. This basic principle at the root of Canadian health care policy should be applied to prescription drug expenses” (Standing Senate Committee on Social Affairs, Science and Technology 2002).

Rather than call for universal first-dollar drug coverage as the National Forum on Health did in 1997, Romanow and Kirby independently called for incremental expansion by way of public coverage against catastrophic drug costs, defined as household drug costs that exceeded high deductibles. Deductibles could be set either in absolute terms (Romanow recommended $1,500 per household) or as a percentage of income (Kirby recommended 3 percent of household income).

At the time of these recommendations, equivalent or better public drug coverage was available to all seniors and nonseniors in provinces west of New Brunswick, but nonseniors in New Brunswick and the other Atlantic provinces did not receive such coverage. As such, the recommendation for universal catastrophic drug coverage did not represent a significant expansion of public drug benefits. But Romanow’s recommendations, in particular, were for incremental reforms aimed at paving the way for more complete coverage of prescription drugs for all Canadians (Forest 2004). Notably, the Romanow Commission recommended that universal public coverage against catastrophic drug costs be a minimum short-term standard for public drug benefit programs. Romanow’s longer-term vision was that more comprehensive public coverage would gradually be layered on top of that framework, beginning with universal first-dollar coverage for drugs to treat chronic conditions such as asthma, diabetes, cardiovascular problems and mental illness:

Given the expanding role of prescription drugs in Canada’s health care system, a strong case can be made that prescription drugs are just as medically necessary as hospital or physician services. However, the immediate integration of all prescription drugs into a revised Canada Health Act has significant implications, not the least of which would be substantial costs. Therefore, the goal should be to move in a gradual but deliberate and dedicated way to integrate prescription drugs more fully into the continuum of care. Over time, these proposals will raise the floor for prescription drug coverage across Canada and lay the groundwork for the ultimate objective of bringing prescription drugs under the Canada Health Act. (Commission on the Future of Health Care in Canada 2002)

Following the Romanow Commission, provincial premiers called on the federal government to take sole responsibility for pharmacare programs across Canada (Council of the Federation 2004). The federal government did not accept the responsibility at the time. Instead, it incorporated the National Pharmaceuticals Strategy (NPS) into the 2004 Health Accord, a 10-year plan to strengthen health care. The NPS was intended to improve cooperation across jurisdictions and make progress toward a national standard of public drug coverage, lower prices for brand-name and generic drug prices, and better prescribing and drug safety (Health Canada 2005). Progress stalled on these fronts following the 2006 change of federal government; and, as early as 2009, the Health Council of Canada declared the NPS a lost opportunity for meaningful federal and provincial cooperation (Health Council of Canada 2009).

There have been no other major national commissions or inquiries on health care or pharmaceutical policy since the Romanow Commission, but a variety of organizations have recommended reforms to prescription drug benefit policies. These organizations have typically proposed the establishment of a standard of coverage for pharmacare without advancing a clear definition of what it would look like (Daw et al. 2014). But, more importantly, neither the federal government nor any provincial government has yet taken steps to integrate prescription drugs more fully into the public health insurance system.

So where do we stand today? All provinces currently offer public drug coverage at little or no charge to people who are on social assistance and to seniors who receive the Guaranteed Income Supplement (Daw and Morgan 2012). Additionally, they offer a myriad of public drug plans for people with specific illnesses – such as cancer, multiple sclerosis, HIV/AIDS, cystic fibrosis and diabetes – and for people receiving palliative care. Public coverage of prescription medicines for other people differs by province; in six provinces it is contingent on the age of the patient; i.e., it is age-based (table 2).

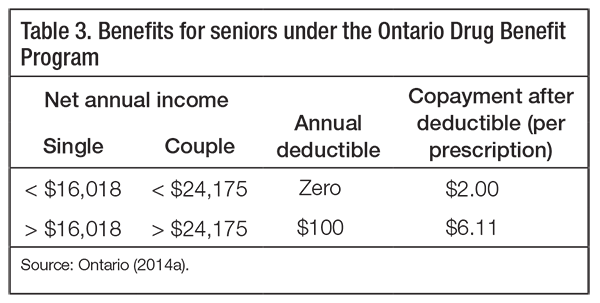

Ontario’s system serves as an illustration of an age-based plan (table 3). This system provides almost all residents over age 65 with near first-dollar public coverage (Ontario 2014b). Seniors with low incomes pay no deductibles and a fixed $2.00 copayment per prescription, and seniors with higher incomes pay an annual $100 deductible and a fixed $6.11 copayment per prescription. Ontario residents under age 65 are eligible for public coverage against drug costs that exceed income-based deductibles equal to approximately 4 percent of their household income (Ontario 2014b).

British Columbia, Saskatchewan, Manitoba, and Newfoundland and Labrador have replaced public drug plans that provided seniors with medicines at little or no charge with income-based public drug benefit plans for everyone. These are programs in which residents are eligible to participate without being charged premiums. They provide benefits to cover the cost of prescription drugs; however, these benefits and the deductibles are calculated based on the household income of beneficiaries. Specific drug plans vary across provinces that offer such coverage, but their general structures are similar. Below the deductibles, patients are required to cover 100 percent of the costs of their prescriptions – either out-of-pocket or through voluntary private insurance, if it is available to them. Once their deductible is reached, patients may still be required to cover a proportion of drug costs by way of coinsurance, which can also depend on their household income. Finally, the total prescription drug costs borne by patients may be limited to a percentage of household income.1

British Columbia is an exemplary case study of the effects of replacing comprehensive public coverage for seniors with income-based coverage. Until 2001, the British Columbia government provided coverage for all seniors’ prescription drugs, subject to small copayments, and all nonseniors received coverage of drug costs over $800 per year. In 2001, the newly elected government put a three-year freeze on Ministry of Health budgets and announced that it would overhaul the program to cut government spending (Morgan and Coombes 2006). While developing the more comprehensive reforms necessary to freeze public spending on prescription drugs, in 2002 the government imposed a $25 copayment on seniors’ prescriptions and raised the annual deductible for nonseniors’ public drug coverage from $800 to $1,000. Then, in May 2003, it implemented its income-based plan for seniors and nonseniors, calling it Fair PharmaCare.

The terms of British Columbia’s income-based public drug benefit program are outlined in table 4. At its outset, British Columbia’s program applied lower deductibles and coinsurance rates for patients in families with one or more member born before 1939. Because residents born before 1939 had received comprehensive drug coverage under the age-based public drug benefit program that existed until April 2003, the British Columbia government decided to provide them with lower deductibles and coinsurance rates under the new plan than all other residents, including those who would turn 65 after 2003 (Morgan and Coombes 2006). Gradually, as residents born before 1939 pass away, the British Columbia program is becoming a truly age-irrelevant, income-based drug plan.

The deductibles and coinsurance costs under British Columbia’s program are the lowest of all of the universal income-based public drug benefit programs in Canada. To the extent that lower deductibles under these plans might better promote certain policy outcomes (for example, access to necessary medicines or protection from financial burden of illness), the British Columbia plan can be viewed as a best case, or as a model for how income-based public drug benefits might play out nationally. Additionally, the British Columbia plan has been more extensively studied than similar programs in other provinces. This allows us to draw on a relatively extensive literature on the effects of the policy.

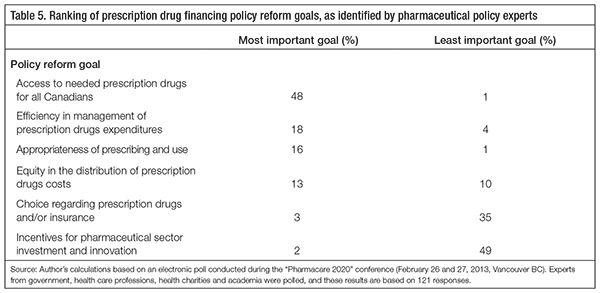

Through an extensive review of research literature, public policy documents, and reports by health agencies and stakeholder groups, Hurley and colleagues have identified key objectives that might be pursued through health care financing systems (Hurley et al. 2003; Hurley 2010).2 Based on their work, we evaluate income-based public drug benefit programs against three of these goals: access to necessary medicines, financial equity and system efficiency. These goals are most germane to prescription drug benefit policy and capture the prescription drug financing policy goals identified through a 2013 poll of pharmaceutical policy experts from government, health professions, health charities and academia (see table 5).3

Arguably, the most important goal of any system for financing prescription drugs is assured access to necessary medicines. This is because prescription drugs are instrumental inputs into the broader health care system that aims to meet patient and population health needs. As such, governments have moral and economic motivations to ensure reasonable access to necessary prescription drugs. Moral obligations stem from the fact that most prescription drugs are used in an effort to restore or protect human health. The United Nations has declared that as health is a fundamental human right, governments are obligated to promote universal access to -necessary health care (United Nations 1966). This could logically extend to prescription drugs; indeed, the World Health Organization has taken the UN declaration to imply that governments have an obligation to create systems to en-sure universal access to necessary medicines (World Health Organization 2001).

Economic motivations stem from the fact that promoting universal access to medically necessary prescription drugs can improve the efficiency of the broader health care system – much of which is publicly financed in most countries, including Canada. When appropriately prescribed and used, many prescription drugs are the most cost-effective way of addressing the health needs of a patient. Evidence suggests that providing effective medicines to patients at little or no direct cost can improve adherence to treatments, improve health outcomes, and thereby lower medical and hospital costs (Adams, Soumerai, and Ross-Degnan 2001; Choudhry et al. 2011; Matsui 2013). For example, a randomized policy trial involving a major private American health insurance program – one covering employees and retirees for medical, hospital and pharmaceutical costs – showed that eliminating copayments for medicines deemed essential for heart attack victims improved patient adherence to treatment and reduced expenditure on medical and hospital care, thereby generating savings that offset the cost of eliminating copayments (Choudhry et al. 2011). For such reasons, health system policy-makers have an economic incentive to promote universal access to medically necessary prescription drugs.

Theory would predict that access to medicines is maximized by financing systems that minimize the out-of-pocket cost of filling prescriptions – that is, patients faced with ordinary budget constraints are more likely to fill the prescriptions their doctors write if the cost to them is low or nil. A vast literature clearly and consistently supports the corollary: even small charges for prescription drugs result in fewer prescriptions filled and lower rates of adherence to long-term treatments (Adams, Soumerai, and Ross-Degnan 2001; Goldman, Joyce, and Zheng 2007; Genmill, Thomson, and Mossialos 2008; Matsui 2013).

Theory would also predict that reduction in use of medicines in the face of patient charges will not always be efficient from a health system or societal perspective – that is, when faced with out-of-pocket charges for prescriptions, patients may discontinue their use of the prescription drugs that are of value to their health, to the health of the people around them or to the health care system from which they receive other forms of care (Evans 1984). This is in part because patients often do not have sufficient knowledge to make reasoned trade-offs between therapies– indeed, the prescription-only category of medicines was created based on the belief that the appropriate selection and use of such drugs require the supervision of specialized health professionals (Temin 1980; Evans 1984). Potentially inefficient patient responses to out-of-pocket charges may also result from rational decision-making in the face of budget constraints if individual patients simply prefer the salient benefits of some medicines (for example, drugs that produce tangible reductions in pain, discomfort or other effects of a disease) instead of the more abstract benefits associated with preventive medicines (for example, drugs that reduce an intangible risk of an illness that a patient may or may not get).4 Thus, charges to patients will likely result in reduced access to both essential and nonessential drugs – a prediction that is supported by a vast body of research (Tamblyn, Laprise, and Hanley 2001; Goldman, Joyce, and Zheng 2007; Genmill, Thomson, and Mossialos 2008).

Logically, because elderly populations have historically received comprehensive public drug coverage in Canada, establishing income-based public drug benefit programs will generally cause an increase in direct charges for the prescriptions they fill. This is because all patients except those with exceptionally low incomes must cover the full cost of the prescriptions they fill until they reach their annual deductibles. Though some patients may be fortunate enough to have private insurance to cover the costs not paid by the public drug benefit program, there is no guarantee that they would have such coverage – especially in retirement. As such, an income-based public drug benefit program will provide less assurance of access to necessary medicines than a public drug plan providing no-deductible coverage for necessary drugs.

Predictions of impacts on elderly patients’ access to necessary medicines are borne out in empirical research on the effects of income-based public drug benefits in British Columbia, which shows that access to several major drug classes is reduced. For example, there is evidence that elderly patients with respiratory diseases were less likely to start indicated drug treatments and less likely to adhere to those treatments after the income-based public drug benefit program was introduced (Dormuth et al. 2006). Similarly, elderly myocardial heart attack patients were less likely to adhere to essential treatments following the policy change (Schneeweiss et al. 2007a,b). There was also a decrease in the rate of antidepressant use among elderly residents after the policy change (Wang et al. 2008). To our knowledge, there is no comparable evidence showing instances of improved access to certain medicines for elderly British Columbians.

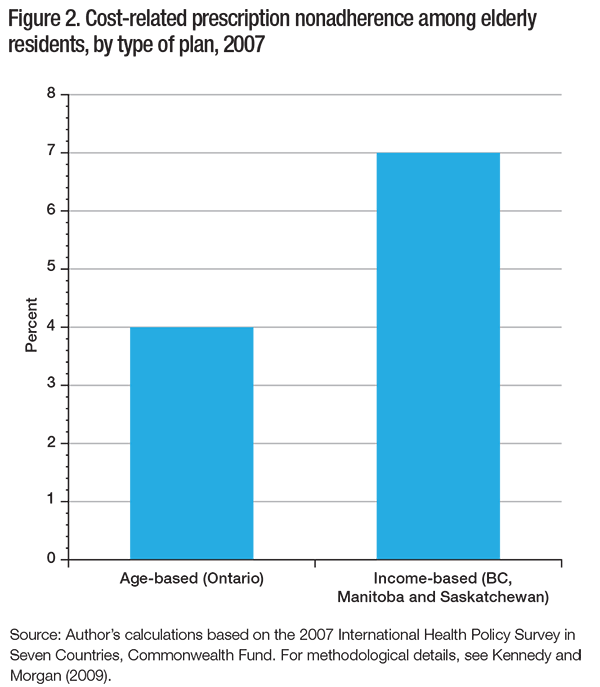

More recent data is also consistent with predictions that income-based drug plans would negatively affect seniors’ access to medicines. The 2007 International Health Policy Survey conducted by the Commonwealth Fund asked respondents whether, in the past year, they had failed to fill any prescriptions or skipped any doses of prescriptions they had filled because of the out-of-pocket cost – also referred to as cost-related nonadherence to prescribed therapy. The Canadian sample of this survey was large enough to allow researchers to compare provinces according to the type of public drug benefit programs they offered (Kennedy and Morgan 2009). As shown in -figure 2, in 2007, the rate of cost-related nonadherence reported by elderly residents of British Columbia, Manitoba and Saskatchewan (all provinces that had income-based drug coverage at the time) was 7.1 percent. In contrast, in Ontario (a province providing coverage at little or no charge to all senior patients), just 3.9 percent of elderly residents reported cost-related nonadherence. A study of a similar question in the Canadian Community Health Survey found that residents of British Columbia were twice as likely as residents of Ontario to report skipping prescriptions in 2007 because of cost, even when patient age, health, income and insurance coverage (private or public) were taken into account in statistical analyses (Law et al. 2012). To put these numbers in perspective, if Ontario had the same rate of cost-related nonadherence among its elderly population as British Columbia, a further 68,000 elderly Ontarians would forgo their prescriptions because of financial barriers. For many of those seniors, stopping treatment would result in worse health outcomes and higher rates of hospitalization. Indeed, there is research evidence suggesting that the age-based entitlement to no-deductible public drug coverage in Ontario improves access to medicines and equity in health outcomes associated with the management of chronic disease (Grootendorst, O’Brien, and Anderson 1997; Booth et al. 2012).

In summary, the predictions are supported by evidence: income-based public drug benefit programs reduce seniors’ access to necessary medicines when they replace programs that cover senior patients at little or no charge. The deductibles create a financial disincentive for them to fill prescriptions and reduce their adherence to prescribed therapy.

The second key objective for a prescription drug financing system is to ensure that the financial burdens associated with necessary medicines are equitably distributed. Considerations of financial equity are, of course, normative. However, there is reasonable consensus in the literature – and observational evidence from health system designs around the world – that health care system financing should protect patients from financial burdens associated with illness (Evans 1984; Wagstaff et al. 1992; Wagstaff et al. 1999; Hurley et al. 2003; Hurley 2010). In addition, the literature on health care financing also suggests that financing necessary health care should not exacerbate prevailing income inequality in a society – especially given that income inequality can lead to inequality in health care needs to begin with (Wagstaff et al. 1999; Hurley 2010).

These normative arguments concerning health care financing would generally apply in the context of prescription drugs because, despite being sold in retail stores where they can be made to seem like ordinary consumer goods, prescription drugs have no intrinsic value to healthy people. No rational person would want to be in a condition to need prescription drugs (except, perhaps, drugs that serve lifestyle or cosmetic purposes).5 The need for prescription drugs arises only when a patient suffers from a deprivation in health status or a risk to future health status that is significant enough to justify the inconvenience and potential for harm associated with the use of medicines (Evans 1984). Moreover, it is often the case that patients with a legitimate need for prescription drugs cannot delay the use of them without suffering or without increasing their risk of harm, or even death.

To protect people from financial disadvantage associated with medical needs, health systems must, as much as possible, separate the payment for health services from their use (Wagstaff et al. 1999). This requires minimizing direct contributions – whether through out-of-pocket expenditures for deductibles under an insurance plan, coinsurance, or other charges faced by people who have exceeded their deductibles. Furthermore, equitable protection against the costs associated with elevated medical needs also requires that the cost of participating in a financing system not be associated with the expected service use of a given patient (Evans 1984). This is because health care needs are often chronic and therefore relatively predictable. In an unregulated insurance market, for example, the cost of an insurance plan would necessarily reflect expected drug costs for prospective insurance plan beneficiaries. Thus, for the elderly and the chronically ill, the insurance premiums themselves – if insurance were available for such populations – would represent a financial disadvantage associated with medical needs (Evans 1984; Wagstaff et al. 1999; Hurley 2010).

Income-based public drug benefit plans are often portrayed as a more equitable way of financing medicines than age-based programs that provide seniors with more comprehensive public coverage for drug costs. Indeed, British Columbia’s income-based drug plan – which replaced the comprehensive age-based drug program in 2003 – was called Fair PharmaCare to encourage this perception. Following the 2003 policy change, the narrative chosen to describe the change in benefits structure was based on the proposition that it was “unfair” for government to provide prescription drug coverage to all seniors regardless of their income (Morgan and Coombes 2006). Similar arguments have recently been made by the Government of Ontario, which has explicitly referred to income-based deductibles as a “fairer drug system for seniors” (Ontario 2012).

Despite the claims that British Columbia’s prescription drug program is fair, rigorous assessments of Fair PharmaCare have found that it does not equitably distribute financial burdens associated with pharmaceutical needs. This is because despite deductibles being equal to fixed percentages of household income, the likelihood of spending such amounts on prescription drugs will differ by income group. People with lower incomes are more likely to have greater medical needs and are therefore more likely to spend the fixed percentage of their incomes on prescription drugs. This is the conclusion of analyses of the financial impact on seniors following the policy change in British Columbia, which have shown that the income-based deductibles are regressive once differences in health care needs are taken into account (Hanley et al. 2011). The only positive impact on equity derived from income-based public drug benefits was a reduction in the average public subsidies for elderly people with high incomes, not an increase in public subsidy for lower-income patients (Hanley, Morgan, and Yan 2006; Hanley et al. 2008).

Perhaps the most troubling equity-related impact of income-based public drug benefits – particularly for the elderly – is the health-related financial burden it imposes on households that include a person with chronic disease. Approximately 80 percent of total costs of prescription drugs are for treatments used by just 20 percent of the population; moreover, the needs of those whose medical requirements are elevated are likely to persist, often until they die (Morgan et al. 2003; Kozyrskyj et al. 2005; Hanley and Morgan 2009).

The concentration and persistence of prescription drug needs are particularly important for the elderly, because their needs for prescription drugs are far greater than the average needs. In 2004, nearly 30 percent of the senior population of British Columbia had over $1,500 in individual-level prescription drug needs (Hanley and Morgan 2009). A majority of those drug needs could be expected to carry on for several years, and spousal drug needs are often added, creating even higher total household drug costs. Under an income-based drug plan, such households would bear much of these annual costs by way of deductibles and coinsurance – either directly, out-of-pocket, or indirectly, through voluntary private insurance plans. Thus, in comparison with public programs that provide comprehensive coverage of drug costs, income-based plans for seniors represent an ongoing, though implicit, tax on the deterioration of health status that often comes with old age.

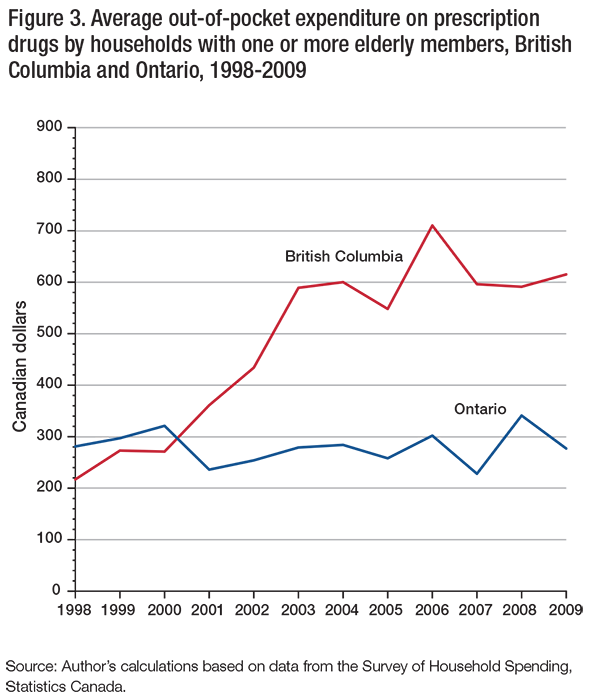

The net effects of income-based drug coverage on costs to the elderly can be seen in figure3, which plots average out-of-pocket expenditure on prescription drugs for households in British Columbia and Ontario with one or more elderly member. From 1998 to 2001, average out-of-pocket costs for prescription drugs borne by households with elderly members in British Columbia were not significantly different from those of their counterparts in Ontario. In reading this figure, one should remember that the BC government imposed a $25 copayment on prescriptions filled by seniors in 2002 while it developed plans for the income-based program that would be implemented in 2003. Following this transition from age-based to income-based public drug benefits, out-of-pocket costs for prescription drugs have been consistently higher for households with elderly members in British Columbia. In 2009, the average of out-of-pocket expenditure on prescription drugs for these households was $615 in British Columbia and $277 in Ontario. It should be noted that these costs are on top of any payments made by private insurance plans under which individuals might be covered and on top of taxes and premiums paid to finance public insurance programs in those provinces.

To recapitulate, theory and evidence indicate that income-based public drug benefit programs fail to provide adequate protection against financial burdens associated with poor health and related medical needs. They are not financially equitable because, by their very construction, they impose considerable direct costs on the users of prescription drugs. Even though such direct costs are limited to a given percentage of total household income, patients with needs sufficient to surpass the annual deductibles will typically have such needs year after year. This persistent private cost of needed medicines makes such patients a high risk in private insurance markets. Unless these patients are employed in workplaces that subsidize their insurance costs on an ongoing basis, persistent high levels of need for prescription drugs will result in higher premium charges in an unregulated insurance market. Thus, when viewed in the context of a public system of financing medically necessary care for all residents, the deductibles under income-based public drug benefit programs are tantamount to an increase in the marginal tax rate for people with chronic disease – including most seniors, whose need for pharmaceuticals can be expected to represent a sizable and ongoing private financial burden. Private sector employers cannot be relied upon to subsidize these costs for the duration of their employees’ retirements, nor should they be responsible for such costs.

The third critical objective for prescription drug financing systems is efficiency. Excess funds spent unnecessarily on medicines or on the system that finances them are funds that cannot be used in other ways to promote the health and well-being of individual patients and the population. Moreover, excessive growth in system-level costs may threaten the sustainability of drug benefit programs. This, in turn, may undermine the other key policy goals of promoting access to medicines and distributing financial burdens equitably.

That said, some cost-control mechanisms – such as prescription limits or copayment – may reduce access to necessary medicines or simply shift financial burdens from one payer to another, potentially diminishing financial equity (Soumerai et al. 1993). As the goal of managing costs is connected to the goals of promoting access and fostering financial equity, some financial arrangements that contain drug costs may not be efficient from a system-level or societal perspective.

Efficient management of pharmaceutical expenditures – at least from a societal, health care system perspective – requires that relevant decision-makers have appropriate incentive to consider the full cost of the benefits of prescription drug use versus other forms of health care for patients. This includes incentive to recognize and encourage the use of prescription drugs when it is the most cost-effective means of addressing patient health needs. It also includes incentive to recognize which prescription drugs are the most cost-effective therapeutic choices for addressing each patient’s needs.

Ordinary consumer theory might suggest that the incentive for weighing costs and benefits should rest with patients. However, levying charges on patients could undermine goals related to financial protection and equity, given that most patients have little control over their need for prescription drugs in the first place, and it could result in undesirable reductions in essential treatments. For these reasons, the decision makers who should be given incentive to consider the costs and benefits of medicines are the health system managers and health care professionals who make key decisions on behalf of patients.

In addition to the requirement that key decision-makers have appropriate incentive to consider treatment costs and benefits, efficient management of pharmaceuticals requires optimally aligned purchasing strategies and evidence-based negotiation strategies to ensure competitive drug pricing in this marketplace. Indeed, effective purchasing power is of increasing importance in today’s pharmaceutical market. The first reason for coordinating drug purchases is that vast numbers of drugs are now available in generic format. The opportunities for savings are considerable; in this decade, patents will expire on drugs worth over US$100 billion in global sales. Regulatory solutions to generic pricing policy are not ideal because regulators cannot know the true cost of producing each individual drug product (Tirole 1988; Competition Bureau Canada 2007). In contrast, well-managed competitive tendering processes can result in prices that reflect production costs while rewarding firms for pricing competitively. Indeed, for many decades, hospitals in Canada have purchased generics in bulk through tendering processes that have effectively reduced prices (Royal Commission on Health Services 1965; Gorecki 1992).

The second reason for coordinating drug purchases in today’s pharmaceutical market is the changing nature of pricing arrangements for brand-name drugs. The Organisation for Economic Co-operation and Development and the World Bank have both observed that the widespread use of international price comparisons is resulting in the harmonization of official list prices for pharmaceuticals and the increased use of confidential negotiations as a means for manufacturers to practise price discrimination across markets and payers (Docteur, Paris, and Moïse 2008; Seiter 2010). These negotiated deals – referred to as “product-listing agreements” in the Canadian context – allow manufacturers to practise price discrimination and are increasingly common in Canada and abroad (Adamski et al. 2010). An income-based public drug benefit program reduces the negotiating power of the drug plan under this paradigm, because the government formulary affects only a minority of patients, and only after they exceed high deductibles. It also forces underinsured and uninsured patients to pay inflated prices for their medicines before their deductibles are reached (Morgan, Daw, and Thomson 2013; Morgan, Friesen, et al. 2013).

Efficiency is more difficult to achieve in prescription drug financing systems that fragment purchasing power and separate purchasing decisions from management of other key components of health care. This applies to income-based drug benefit programs, because residual costs fall to patients and/or independent private insurers. Government’s purchasing power and its incentives to manage the total costs are therefore reduced, because it is not the single payer for medicines.

Evidence from British Columbia is consistent with this theory. When they were first introduced, income-based public drug benefits in British Columbia significantly reduced the public share of drug expenditures by shifting the financial burden to the private sector. This did not change total prescription drug expenditures, which continued on an upward trend in the years immediately following the introduction of the policy (Morgan and Yan 2006). In 2004 alone, the shift to income-based public drug benefits in British Columbia was estimated to have resulted in a transfer of $134 million of spending from the public side of the financial ledger to the private side, which was equivalent to a 16.9 percent decrease in public spending and an 18.1 percent -increase in private spending compared to what would have occurred in the absence of the policy change (Morgan et al. 2006).

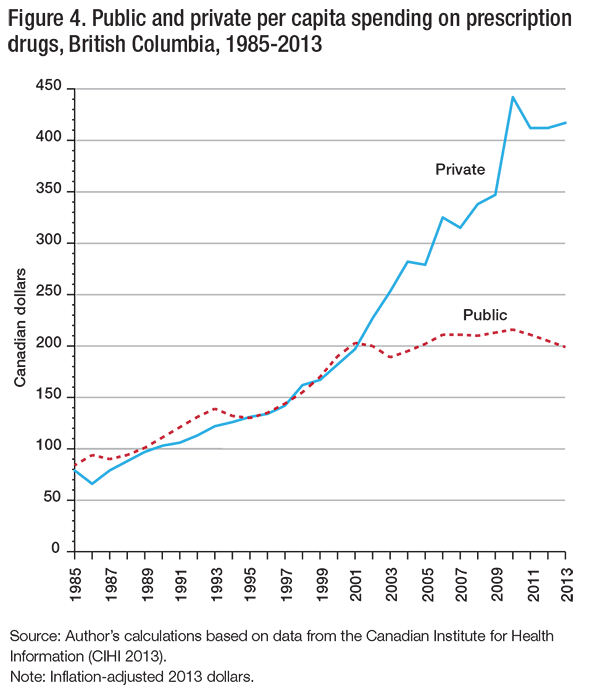

As a result of the cost shifting under British Columbia’s income-based public drug benefit program, average household spending as a proportion of household income increased across nearly all age and income groups between 2002 and 2004 (Hanley, Morgan, and Yan 2006). Figure4 presents a longer horizon, showing how government expenditure on prescription drugs in British Columbia levelled off while private spending grew more rapidly following the transition from age-based to income-based public drug benefits.

One of the reasons that public spending has been relatively well controlled under income-based public drug benefits in British Columbia is that fewer people are qualifying for public subsidies as incomes increase over time with both inflation and economic growth. When policy-makers in British Columbia were planning the program back in 2000, one in five households with elderly members (21 percent) had an income of below $15,000 and could thus qualify for public drug coverage without deductibles; today, the proportion is one in twenty-five households (4 percent).6 Because of effects like this – caused by inflation, nonindexation of the household income thresholds since 2003, economic growth and demographic change – the government is actually liable for a diminishing share of prescription drug costs over time.

Private insurers are not more efficient than governments at financing prescription drugs. Significant nonmedical costs are passed on to premiums for private health benefits: duplicative administrative, actuarial, and marketing costs, as well as profits that must be paid to investors in the private insurance companies competing in the market (Law, Kratzer, and Dhalla 2014; Frank 2014; Nicolle and Mathauer 2010). In addition, and perhaps more importantly, private insurance companies have less incentive and capacity to reduce costs than provincial governments. Incentives are lower, in part, because of the tax subsidy given to employer-provided private drug benefit programs in Canada. Capacity to engage in prudent expenditure management is lower, partly because private insurers operate independently of (and, indeed, in competition with) each other, and independently of the provincial governments that run universal medical and hospital insurance programs. As a result, evidence shows that private drug plans in Canada perform worse than provincial drug plans in terms of promoting generic drug use when generics are available; negotiating price reductions from brand-name manufacturers; limiting the use of high-cost drugs when lower-cost alternatives would do; and encouraging competition and efficiencies in drug distribution channels (Canadian Life and Health Insurance Association 2009; Balaban et al. 2013; Morgan, Smolina, et al. 2013). Moreover, the existence of multiple payers in the market reduces the purchasing power of all drug plans, private and public.

To illustrate the impact of purchasing power differences, we compared generic prices in Canada with those in New Zealand. We chose to compare Canadian prices with New -Zealand ones because New Zealand is a country that uses its single-payer pharmaceutical coverage system to secure generics on sole-source tenders (Morgan et al. 2007); one would obtain similar findings if one used as a basis of comparison the prices obtained by the Veterans Health Administration in the United States (Law and Morgan 2011; Law 2013). Using sales-volume data from the Canadian Rx Atlas and price data from public drug plans in Ontario and New Zealand, we were able to make price comparisons for 35 high-volume prescription drugs that were sold as generics in Canada and New Zealand. The combined sales of these drugs in Canada equalled $5.5 billion, including brand and generic sales. Weighted by Canadian sales volumes, the generic drugs were priced 72 percent lower in New Zealand than in Canada – that is, the Canadian price of these high-volume generic drugs was nearly four times as high as the New Zealand price. At New Zealand prices, governments in Canada could afford to provide all people, regardless of age, with comprehensive coverage of generic drugs at a lower cost to the public than the cost that provincial drug programs are currently assuming.

To sum up, while income-based public drug benefit programs may be effective mechanisms for reducing the public liability for prescription drug costs, they do not result in efficient management of total prescription drug costs. Indeed, any system of financing prescription drugs that involves multiple payers will necessarily increase administrative costs and decrease Canada’s purchasing power in the global pharmaceutical marketplace. This loss of purchasing power is significant – it is likely costing Canadians billions of dollars per year. As a large share of such costs falls upon employers, unions and patients, the burden on the Canadian economy is heavy, even if income-based public drug benefit programs limit public spending. Moreover, fragmenting the system of prescription drug financing among payers that are independent of the management of the rest of the health care system diminishes incentive to manage pharmaceuticals as an integral component of the overall health care system – including the incentive to promote appropriate medicine use.

Overall, the theory and the evidence indicate that income-based public drug plans are not designed to achieve their key policy goals: access to medicines, financial equity and system efficiency. Provinces should provide full and universal coverage of prescription drug costs, financed through personal income taxation. Their programs would then be unambiguously more accessible, equitable and efficient.

The empirical and analytical arguments presented in this paper provide strong support to this recommendation. We saw that the Canadian health care system is unique among those of developed countries insofar as it ensures universal coverage of medical and hospital care but not prescription drugs. Despite repeated calls by national commissions and inquiries for expanded public drug coverage in Canada, the current trend is toward declining public drug benefits. In particular, whereas seniors have historically enjoyed relatively comprehensive public drug benefit coverage in Canada, only three provinces are still covering persons age 65 and older at little or no charge to patients. Four provinces are now offering income-based public drug plans for seniors instead, with similar catastrophic drug coverage for nonseniors.

Our analysis shows that even though these policy changes are sometimes portrayed as an expansion of previous programs, the adoption of income-based plans represents a retrenchment of public drug benefits in Canada. While these policy reforms often do broaden the eligibility for public drug benefits to include all nonseniors, the benefits provided to both seniors and nonseniors target those with very low household incomes. In addition, they impose a heavy burden on individuals with great pharmaceutical needs, who are left to cover substantial costs for drug therapies. The overall result is a decline in the public share of prescription drug financing rather than movement in the opposite direction.

The rationale often provided for moving to income-based prescription drug benefit plans is that seniors should not get free drugs simply because of their age, and that people who can afford prescription drugs should pay for them directly. While potentially appealing on some levels, this would mean adopting a policy stance whereby persons with a chronic need for high-cost pharmaceuticals, many of whom are elderly, would have to bear financial responsibility for a proportion of those costs equalling 3 percent or more of household income, depending on the provincial drug plan, year after year. No other country with a comparable health system to Canada’s imposes such charges.

Expanding public drug benefits into universal programs that offer first-dollar coverage for essential drugs is financially realistic. In 2013, approximately $17.1 billion was spent out of pocket and through private drug insurance for prescription drugs (see table 1). A 1.8 percent tax on net taxable income would generate approximately that amount in new revenues.7 However, implementing a universal, public drug benefit program without deductibles or copayments would likely require less than that amount because of the potential cost and administration efficiencies such a system could provide. Such a system could lead to significantly lower total pharmaceutical costs by enabling lower pricing of brand-name and generic drugs, increased use of generics when available and improved prescribing patterns. It is also important to note that funding the new system would not entail new costs. To the extent they are needed, any additional taxes or contributions would directly replace the costs of private prescription drug programs currently borne by employers and unions and by patients, as these costs would be, for the most part, eliminated under a new public program. As a result, the costs of prescription drug coverage would be borne more broadly by all taxpayers according to ability to pay, which would be more equitable overall. This would bring much-needed relief and security to many Canadians, particularly those with chronic high-cost pharmaceutical needs. Thus, theory and evidence suggest that the optimal policy response to Canada’s fragmented prescription drug coverage system is not to reduce public drug benefits for seniors, but to increase public drug benefits for nonseniors.

This conclusion is not new. Perhaps one of the most remarkable aspects of the Canadian policy debate on prescription drug costs is the consistency with which royal commissions or their equivalents reach similar conclusions. Specifically, it has long been known and repeatedly stated that to achieve the goals of access to medically necessary care, financial protection against the costs associated with ill health and effective management of system costs, we must better integrate pharmaceuticals into Canada’s medicare system. Despite the potential benefits of improved access, greater equity and lower costs, achieving this integration has proven politically difficult – indeed, not one province has managed it. This is partially because implementing a universal program that provides full coverage for essential prescription drugs would require provincial governments to take primary responsibility for managing this large and complex component of the health care system. That would be a daunting challenge, because governments would then bear the full political risk of failure. Such a scenario stands in stark contrast to the current situation – in today’s multipayer system, governments can easily shift costs and deflect responsibility to patients and the private sector. In addition, such a program, if successful, would entail income losses for some stakeholders. Private insurance companies, drug manufacturers and retail pharmacy chains all have something to lose should universal coverage of cost-effective prescription drugs reduce costs as predicted by both theory and international experience. Such interests are unlikely to let this happen unopposed.

But stakeholder opposition is not necessarily insurmountable in a policy move that stands to generate a health care win-win-win: improved access, better quality of care, more equitable financing and lower cost to society. Delivering this to Canadians could even represent a major political win, as it would, arguably, fulfill a long-overdue promise of Canada’s cherished medicare system. Nevertheless, getting there will require committed political leadership and a pragmatic step forward.

Provinces with age-based public drug plans offering coverage at little or no cost to seniors would be well advised to keep these plans intact while gradually building up public coverage for nonseniors. If financial pressures and/or perceived intergenerational inequity spark demands to scale back public subsidies for seniors’ drug programs, it would be wiser to implement a funding mechanism based on ability to pay (probably an earmarked surtax collected through the personal income tax system) than to impose income-based deductibles that penalize those who need coverage most. A similar approach might be used to expand drug coverage for seniors in provinces that have already imposed in-come-based deductibles.

The concept of replacing income-based deductibles with contributions to the sys-tem based on ability to pay is important in that through such a change, the system could promote access to necessary medicines and equitable distribution of financial burden. Moving toward a universal system of full public coverage would also put the government in the position of being a single-payer, which would dramatically improve Canada’s capacity to control the cost of cov-ered medicines.

Expanding public coverage in this way does not mean covering all medicines. To ensure the financial viability of the public drug plan and the efficient allocation of funding across pharmaceutical and nonpharmaceutical forms of health care for Canadians, a universal system of full coverage should only apply to medicines of proven value-for-money from the societal perspective of Canada’s universal health care system. As proposed by the Romanow Commission, such a system could be established gradually. Particularly in the case of generic drugs, which can be had at a fraction of the current cost when purchased in bulk, such an expansion need not cost much more than public drug plans do today.

In the near term, the provinces will have to take the lead in improving public drug benefit programs in Canada. Ultimately, however, sustaining the reforms necessary to better integrate prescription drugs into the Canadian health care system will require significant federal involvement, both politically and financially. We can draw this conclusion based simply on the history of the Canadian health care system as we know it today: each stage in the evolution of our universal public health insurance program has been led by an innovating province then nationalized by federal legislation that has provided federal funding for provincial programs meeting national standards (Taylor 2009). Importantly, the powerful incentive of federal cost-sharing brought many provinces further than they would have gone on their own and likely sustained provincial commitment to related programs and underlying principles during periods when it might have been politically or economically tempting to reduce public coverage for medical and hospital care.

The case for this approach to policy development – provincial innovation sustained and nationalized through federal commitment to programs and principles – is as strong, or perhaps even stronger, for pharmaceuticals as it was for other components of the health care system. First, though the provinces have jurisdictional responsibility for most health care delivery in Canada, the federal government is much more directly involved in policy issues related to the pharmaceutical sector than to those related to the hospital and medical care sectors. The federal government has considerable impact on the availability, cost and use of medicines – as well as on the availability and transparency of scientific data on the safety and efficacy of medicines – primarily through its responsibility for the regulation of drug products, marketing and intellectual property (Anis 2000). It is arguable that the federal government would have greater incentive to balance the full societal benefits and costs of changes in such policies if it were more directly involved in the financing of medicines affected by them.

Additional benefits could be gained by coordinating provincial programs to create a more -cohesive system for negotiating prices and making decisions about drug coverage with the assistance of the federal government. For instance, regional variations in drug coverage can generate profound interprovincial inequities in health and economic well-being. Current interprovincial differences in drug coverage typically involve specialized medicines, which often come at a very high cost per patient treated (Menon, Stafinski, and Stuart 2005; Morgan, Hanley, et al. 2009). With the growing number of specialized, high-cost medicines coming to market, provincial differences in population health needs, economic opportunities and even political priorities may result in even greater coverage disparities than we are already seeing. This could spur undesired interprovincial migration based on health care needs and provincial coverage policy. It would certainly undermine a core principle of Canada’s medicare system – that all Canadians in all parts of the country should receive equitable access to necessary care.

Efficiency in drug pricing is also an important motivation for sustaining collaboration among provinces. The modern pharmaceutical-pricing paradigm is based on negotiated but confidential pricing for patented medicines and competitive mechanisms for off-patent drug pricing, including bulk purchasing through competitive supply contracts. For pricing of both patented and off-patent drugs, market size matters because it directly affects the willingness of manufacturers to compete by lowering prices in order to secure greater sales under (ideally, universal) public drug benefit programs. Because of this, the wide variations in provincial population size are problematic. Total expenditure on prescription drugs in Ontario in 2013 ($11.6 billion), for example, was larger than total expenditure in eight other provinces combined ($10.1 billion in total for British Columbia, Alberta, Saskatchewan, Manitoba, New Brunswick, Nova Scotia, Prince Edward Island, and Newfoundland and Labrador), and more than 10 times larger than expenditures in six individual provinces (Saskatchewan, Manitoba, New Brunswick, Nova Scotia, Prince Edward Island, and Newfoundland and Labrador). These differences in market size could generate significant differences in the prices that could be achieved through negotiations and/or tendering on behalf of drug plans at the provincial level. Though pan-Canadian approaches, such as negotiating pricing agreements that can be shared among participating provinces, do help in this regard, it would be difficult to sustain such horizontal cooperation on politically and economically challenging coverage decisions without some integrating policy framework (Morgan, Thomson, et al. 2013). In federations like Canada, the integrating policy framework often comes by way of some form of vertical integration with standards and opportunities created with the federal government.

For these reasons, initiating the long-recommended expansion of public drug benefit programs will likely require leadership on the part of one or more provinces, but achieving and sustaining such a goal for the country as whole will require federal leadership. Several provincial premiers have been calling on the federal government to take responsibility for pharmacare across Canada for at least a decade now. And Ontario is currently one of the most enthusiastic cheerleaders for a federal pharmacare strategy (Goodman 2014). Whether these calls for action will translate into a coordinated movement toward a meaningful national standard remains to be seen. The substantial cuts in federal health transfers slated to start in 2017 could provide the necessary motivation for the parties to enter negotiations, although the challenge remains quite considerable, given the myriad of drug plans that the provinces currently run. Nevertheless, the expansion – rather than contraction – of public drug benefit programs would bring Canadian prescription drug coverage policy in line with that of every other comparable country. It would generate better access to medicines, more equitable financial protection for the sick and the elderly, and lower costs for Canada as a whole.

Adams, A.S., S.B. Soumerai, and D. Ross-Degnan. 2001. “The Case for a Medicare Drug Coverage Benefit: A Critical Review of the Empirical Evidence.” Annual Review of Public Health 22: 49-61.

Adamski, J., B. Godman, G. Ofierska-Sujkowska, B. Osińska, et al. 2010. “Risk Sharing Arrangements for Pharmaceuticals: Potential Considerations and Recommendations for European Payers.” BMC Health Services Research 10: 153.

Alberta. 2013. “Building Alberta: Health a Priority in Budget 2013.” Edmonton: Government of Alberta. Accessed October 1, 2014. https://alberta.ca/release.cfm?xID=3377946A8CD70-C069-7894-1D9786D5EBBD7C8E

Anis, A.H. 2000. “Pharmaceutical Policies in Canada: Another Example of Federal-Provincial Discord.” Canadian Medical Association Journal 162 (4): 523-6.

Balaban, D.Y., I.A. Dhalla, M.R. Law, and C.M. Bell. 2013. “Private Expenditures on Brand Name Prescription Drugs after Generic Entry.” Applied Health Economics and Health Policy 11 (5): 523-9.

Booth, G.L., P. Bishara, L.L. Lipscombe, B.R. Shah, et al. 2012. “Universal Drug Coverage and Socioeconomic Disparities in Major Diabetes Outcomes.” Diabetes Care 35 (11): 2257-64.

Boothe, K. 2012. “How the Pace of Change Affects the Scope of Reform: Pharmaceutical Insurance in Canada, Australia, and the United Kingdom.” Journal of Health Politics, Policy and Law 37 (5): 779-814.

British Columbia. 2014. Ministry of Health. “Fair PharmaCare Plan.” Victoria: Ministry of Health. Accessed October 1, 2014. https://www.health.gov.bc.ca/pharmacare/plani/planiindex.html

Canadian Institute for Health Information (CIHI). 2011. Health Care in Canada, 2011: A Focus on Seniors and Aging. Ottawa: CIHI.

—————–. 2013. National Health Expenditure Trends, 1975 to 2013. Ottawa: CIHI.

Canadian Life and Health Insurance Association (CLHIA). 2009. CLHIA Report on Health Care Policy: Towards a Sustainable, Accessible, Quality Public Health Care System. Toronto: CLHIA. Accessed April 2, 2012. https://www.clhia.ca/domino/html/clhia/CLHIA_LP4W_LND_Webstation.nsf/resources/Health+Care/$file/CLHIA_Report_on_Health_Care_Policy_ENG.pdf

Chappell, N.L. 2011. Population Aging and the Evolving Care Needs of Older Canadians: An Overview of the Policy Challenges. IRPP Study 21. Montreal: Institute for Research on Public Policy.

Choudhry, N.K., J. Avorn, R.J. Glynn, and E.M. Antman. 2011. “Full Coverage for Preventive Medications after Myocardial Infarction.” New England Journal of Medicine 365(22): 2088-97.

CIHI (see Canadian Institute for Health Information).

Commission on the Future of Health Care in Canada. 2002. “Prescription Drugs.” Chap. 9 in Building on Values: The Future of Health Care in Canada. Final Report. Ottawa: Commission on the Future of Health Care in Canada.

Competition Bureau Canada. 2007. Canadian Generic Drug Sector Study. Ottawa: Competition Bureau Canada.

Council of the Federation. 2004. Premiers’ Action Plan for Better Health Care: Resolving Issues in the Spirit of True Federalism. Ottawa: Council of the Federation.

Daw, J.R., and S.G. Morgan. 2012. “Stitching the Gaps in the Canadian Public Drug Coverage Patchwork? A Review of Provincial Pharmacare Policy Changes from 2000 to 2010.” Health Policy 104 (1): 19-26.

Daw, J.R., S.G. Morgan, P.A. Collins, and J. Abelson. 2014. “Framing Incremental Expansions to Public Health Insurance Systems: The Case of Canadian Pharmacare.” Journal of Health Politics Policy and Law 39 (2): 295-330.

Docteur, E., V. Paris, and P. Moïse. 2008. Pharmaceutical Pricing Policies in a Global Market. OECD Health Policy Studies. Paris: Organisation for Economic Co-operation and Development.

Dormuth, C.R., R.J. Glynn, P. Neumann, M. Maclure, et al. 2006. “Impact of Two Sequential Drug Cost-Sharing Policies on the Use of Inhaled Medications in Older Patients with Chronic Obstructive Pulmonary Disease or Asthma.” Clinical Therapeutics 28 (6): 964-78.

Evans, R.G. 1984. Strained Mercy: The Economics of Canadian Health Care. Toronto: Butterworths.

Evans, R.G., K.M. McGrail, S.G. Morgan, M.L. Barer, et al. 2001. “Apocalypse No: Population Aging and the Future of Health Care Systems.” Canadian Journal on Aging 20 (S1): S160-91.

Federal-Provincial-Territorial Ministerial Task Force on the National Pharmaceuticals Strategy. 2006. National Pharmaceuticals Strategy Progress Report. Ottawa: Health Canada.

Forest, P.G. 2004. “To Build a Wooden Horse…Integrating Drugs into the Public Health System.” Healthcare Papers 4 (3): 22-6.

Frank, S. 2014. “Correcting the Record.” Canadian Medical Association Journal 186 (10): 779.

Genmill M.C., S. Thomson, and E. Mossialos. 2008. “What Impact Do Prescription Drug Charges Have on Efficiency and Equity? Evidence from High-Income Countries.” International Journal for Equity in Health 7 (1): 12.

Goldman, D.P., G.F. Joyce, and Y. Zheng 2007. “Prescription Drug Cost Sharing: Associations with Medication and Medical Utilization and Spending and Health.” Journal of the American Medical Association 298 (1): 61-9.

Goodman, L.A. 2014. “Call Growing Louder for National Prescription Drug Plan.” Globe and Mail, October 5.

Gorecki, P.K. 1992. Controlling Drug Expenditure in Canada: The Ontario Experience. Ottawa: Economic Council of Canada.

Grootendorst, P. 2002. “Beneficiary Cost Sharing under Canadian Provincial Prescription Drug Benefit Programs: History and Assessment.” Canadian Journal of Clinical Pharmacology 9 (2): 79-99.

Grootendorst, P.V., B.J. O’Brien, and G.M.Anderson. 1997. “On Becoming 65 in Ontario: Effects of Drug Plan Eligibility on Use of Prescription Medicines.” Medical Care 35 (4): 386-98.

Hanley, G.E., and S. Morgan. 2009. “Chronic Catastrophes: Exploring the Concentration and Sustained Nature of Ambulatory Prescription Drug Expenditures in the Population of British Columbia, Canada.” Social Science and Medicine 68 (5): 919-24.

Hanley, G.E., S.G. Morgan, M.C. Barer, and R.J. Reid. 2011. “The Redistributive Effect of the Move from Age-Based to Income-Based Prescription Drug Coverage in British Columbia, Canada.” Health Policy 101 (2): 185-94.

Hanley, G.E., S. Morgan, J. Hurley, E.K.A. van Doorslaer, et al. 2008. “Distributional Consequences of the Transition from Age-Based to Income-Based Prescription Drug Coverage in British Columbia, Canada.” Health Economics 17 (12): 1379-92.

Hanley, G.E., S. Morgan, and L. Yan. 2006. “Income-Based Drug Coverage in British Columbia: The Impact on the Distribution of Financial Burden.” Healthcare Policy 2 (2): 170-86.

Health Canada. 2005. “National Pharmaceuticals Strategy (NPS).” Ottawa: Health Canada. Accessed October 1, 2014. https://www.hc-sc.gc.ca/hcs-sss/pharma/nps-snpp/index_e.html

Health Council of Canada. 2009. A Status Report on the National Pharmaceuticals Strategy: A Prescription Unfilled. Toronto: Health Council of Canada.

Hurley, J.E. 2010. Health Economics. Toronto: McGraw-Hill Ryerson.

Hurley, J., J. Abelson, J. Butler, D. Cobb-Clark, et al. 2003. Public and Private Finance: Analytics, Dynamics and Decision-Making. Hamilton: Centre for Health Economics and Policy Analysis, McMaster University.

Keefe, J. 2011. Supporting Caregivers and Caregiving in an Aging Canada. IRPP Study 23. Montreal: Institute for Research on Public Policy.

Kennedy, J., and S. Morgan. 2009. “Cost-Related Prescription Nonadherence in the United States and Canada: A System-Level Comparison Using the 2007 International Health Policy Survey in Seven Countries.” Clinical Therapeutics 31 (1): 213-19.

Kozyrskyj, A., L. Lix, M. Dahl, and R.A. Soodeen. 2005. High-Cost Users of Pharmaceuticals: Who Are They? Winnipeg: Manitoba Centre for Health Policy, University of Manitoba.

Law, M.R. 2013. “Money Left on the Table: Generic Drug Prices in Canada.” Healthcare Policy 8 (3): 17-25.

Law, M.R., L. Cheng, I.A. Dhalla, D. Heard, et al. 2012. “The Effect of Cost on Adherence to Prescription Medications in Canada.” Canadian Medical Association Journal 184 (3): 297-302.

Law, M.R., J. Kratzer, and I.A. Dhalla. 2014. “The Increasing Inefficiency of Private Health Insurance in Canada.” Canadian Medical Association Journal 186 (12): E470-4.

Law, M.R., and S.G. Morgan. 2011. “Purchasing Prescription Drugs in Canada: Hang Together or Hang Separately.” Healthcare Policy 6 (4): 22-6.

Matsui, D. 2013. “Medication Adherence Issues in Patients: Focus on Cost.” Clinical Audit 5: 33-42.

Menon, D., T. Stafinski, and G. Stuart. 2005. “Access to Drugs for Cancer — Does Where You Live Matter?” Canadian Journal of Public Health 96 (6): 454-58.

Morgan, S.G., M.L. Barer, and J.D. Agnew. 2003. “Whither Seniors’ Pharmacare: Lessons from (and for) Canada.” Health Affairs 22 (3): 49-59.

Morgan, S., and M. Coombes. 2006. “Income-Based Drug Coverage in British Columbia: Toward an Understanding of the Policy.” Healthcare Policy 2 (2): 92-108.

Morgan, S., and C. Cunningham. 2011. “Population Aging and the Determinants of Healthcare Expenditures: The Case of Hospital, Medical and Pharmaceutical Care in British Columbia, 1996 to 2006.” Healthcare Policy 7 (1): 68-79.

Morgan, S.G., C.M. Cunningham, and M.R. Law. 2012. “Drug Development: Innovation or Imitation Deficit?” BMJ 345: e5880.

Morgan, S., J. Daw, and P. Thomson. 2013. “International Best Practices for Negotiating ‘Reimbursement Contracts’ with Price Rebates from Pharmaceutical Companies.” Health Affairs (Millwood) 32 (4): 771-7.

Morgan, S., R.G. Evans, G.E. Hanley, P.A. Caetano, et al. 2006. “Income-Based Drug Coverage in British Columbia: Lessons for BC and the Rest of Canada.” Healthcare Policy 2 (2): 115-27.

Morgan, S., M. Friesen, P.A. Thomson, and J.R. Daw. 2013. “Use of Product Listing Agreements by Canadian Provincial Drug Benefit Plans.” Healthcare Policy 8 (4): 45-55.