Les politiques commerciales du Canada au carrefour des nouvelles réalités mondiales

Aperçu des résultats de recherche

Stephen Tapp, Ari Van Assche et Robert Wolfe

Sui Sui is an associate professor in the Department of Global Management Studies at the Ted Rogers School of Management. Her research focuses on understanding the behavior of international entrepreneurs from developed countries. Her work has been published in top-tier journals in the field such as the Journal of International Business Studies. She was a finalist for Haynes Prize for the Most Promising Scholar at the 2013 Academy of International Business Conference. She teaches Global Management, Managerial Economics, and International Trade and has also consulted for the Canadian federal government and think-tanks, on projects related to small business internationalization.

Stephen Tapp is a research director at the Institute for Research on Public Policy, and is currently leading a multiyear research initiative on Canadian trade policy. Before joining the Institute, he was a senior economist and adviser for Canada’s first Parliamentary Budget Officer. He has worked as an economist in the research departments of the Bank of Canada and Finance Canada; as a research fellow at the C.D. Howe Institute; and as an economics instructor at Queen’s University. His research, which focuses on the Canadian economy and public policy, has been published in the Canadian Journal of Economics, Canadian Public Policy, and by think tanks and government organizations. He is on the board of the Ottawa Economics Association. Stephen has a PhD and an MA in economics from Queen’s University and a BA from the University of Western Ontario.

Redesigning Canadian Trade Policies for New Global Realities, edited by Stephen Tapp, Ari Van Assche and Robert Wolfe, is the sixth volume of The Art of the State. Thirty leading academics, government researchers, practitioners and stakeholders from Canada and abroad analyze how changes in global commerce, technology, and economic and geopolitical power are affecting Canada and its policy.

Encouraging international trade by small and medium-sized enterprises (SMEs) has recently become a focus for trade policy both in Canada and abroad. For advocates, increased SME participation promises to deliver more inclusive economic growth by sharing the gains from international trade more broadly. Concurrently, there is a related policy push in Canada for businesses of all sizes to increase their engagement with fast-growing emerging markets in order to help diversify trade beyond the default US market, which has long been the primary destination for Canadian exports (see Bank of Canada 2013; Head 2007; and Manley and Kingston, in this volume).

Bringing these two aims together, the Harper government made it a policy objective in 2013 to raise the share of Canada’s exports to emerging markets significantly, with an increased contribution coming from SMEs (Canada 2013).1 In 2015, when the new Trudeau government took office, the mandate letter to the minister of international trade identified as a top priority developing “a targeted strategy to promote trade and investment with emerging markets, with particular attention to China and India,” and added that this strategy, “should include the mobilization of our SMEs” (Trudeau 2015).

Thus, there is now a clear political consensus both to increase Canada’s economic engagement with emerging markets and to boost SMEs’ participation in international trade more broadly — particularly in emerging markets. Before considering how to design policies to support these goals, however, it is first necessary to understand the trade patterns of Canadian SMEs, including how they are evolving and how they differ from those of large firms; the size of the performance premiums for Canadian SMEs that export to emerging markets; and the influence of different globalization strategies and firm capabilities on the likelihood of SMEs’ success in these markets.

There are grounds for optimism on some of these fronts for policy-makers. Since around 2001, for instance, the share of Canadian exports destined for emerging markets has risen, and these markets have increasingly become the first stop for the export journeys of Canadian firms. Moreover, consistent with predictions from firm-level trade theory (for an overview, see Lapham, in this volume) the larger, more productive and more innovative SMEs are more likely to export to, and survive in, emerging markets.

But we must also add some caution to policy-makers’ current enthusiasm: although entering emerging markets might offer bigger rewards for top performers, it generally entails more risk, and can be tremendously challenging, especially for companies that are not well-equipped to compete. Firm-level performance gaps between top and bottom Canadian exporters are particularly pronounced in these markets. Moreover, there is not necessarily a “right way” for Canadian firms to reach emerging markets. In general, the chances of surviving in these markets are better for gradual exporters — older, larger firms that are more experienced in the domestic market and/or that have exported first to other advanced economies. This is not the only recipe for success, however, a smaller number of “born global” firms operating out of Canada have reached emerging markets successfully quite early in their operations. Examples can be found in the higher-technology services sectors.

Research finds that a firm’s export survival in emerging markets depends not only on its own capabilities — including how frequently it introduces new products or its access to external financing — but also on broader market factors, including competition for those markets by Canadian rivals. Firm-level decisions to enter emerging markets are therefore quite complex. Each potential exporter may face large, upfront entry costs as well as its own particular and highly uncertain risk-reward tradeoffs from choosing among alternative export strategies.

These considerations highlight at least two important and complementary roles for government policy. The first role is to provide information to help Canadian firms learn about their options in emerging markets, so they can make well-informed decisions based on their unique circumstances. The second, more general role is to lower the costs of entering and engaging with these markets. Government can pursue the latter in a variety of ways, including by negotiating trade and foreign investment agreements that reduce obstacles and improve market access, and by simplifying customs procedures and promoting cross-border electronic commerce.

In contrasting the experiences of sequential exporters and “born global” firms, the academic literature highlights two broad exporting pathways.

Theories of sequential exporting arise in international business management and economic trade research. In the former, a theory known as the “internationalization process model” describes how firms gradually increase their international activities (Johanson and Vahlne 1990). After building up a strong presence in the domestic market, firms will often export first to a neighbouring market with a similar cultural background before entering less culturally familiar foreign markets farther away (Johanson and Vahlne 1977; Arenius 2005).

In economics, firm-level trade theory emphasizes other (though somewhat related) factors to explain exporting activities. These reasons include productivity differences between firms, the large fixed costs or “investments” needed to enter foreign markets and the uncertainty associated with these investment decisions (Melitz 2003). This theory predicts — and the empirical evidence generally confirms — that, within a given industry, exporters will be the larger and more productive firms, essentially because they are profitable enough to cover the costs of entering foreign markets. Recent research finds a “virtuous cycle” or two-way relationship underlying these results: not only do “better” firms choose to export, but the act of exporting (and importing) also improves their performance (see the chapter by Baldwin and Yan on global value chain participation, in this volume).2

The fixed trade costs that feature prominently in firm-level trade theory also help to explain gradual exporting behaviour. Firms often export first to neighbouring countries because these markets tend to have lower entry costs — say, because of proximity or preferential market access under a free trade agreement. As firms’ exporting activity and profits increase, they can eventually accumulate the resources needed to cover larger investments to enter more “difficult” foreign markets farther away.3

In the 1990s, however, international business studies began reporting quite different findings. This new literature identified firms that were “born global” — or “international new ventures.” Instead of sequentially exporting in a slow and steady manner, these firms derived competitive advantage by using resources from, and selling outputs to, multiple countries at the same time (Oviatt and McDougall 1994). The emergence of these born global firms has been attributed to several factors, including lower communication costs, more efficient global transportation networks and more liberal trade policies (Fan and Phan 2007). Interestingly, born global firms do not necessarily first enter countries that are culturally closer (Benito and Gripsrud 1992), nor are they more successful when they do so (Evans, Lane and O’Grady 1992; Mitchell, Shaver and Yeung 1994).4

An insight from this research is the importance of a firm’s information and systems processes and that these systems generally differ between young and old firms. Older firms that have served only their domestic market will have developed routines and modes of operating that are well-suited to that market, but not to an international environment, leaving them having to “unlearn” established approaches in order to succeed abroad (Santangelo and Meyer 2011). Younger firms are less likely to have developed highly structured operating processes and are better able to incorporate new knowledge from the foreign markets they enter into their business practices (Bruneel, Yli-Renko and Clarysse 2010; De Clercq et al. 2012; Sapienza, DeClercq and Sandberg 2005; Blomstermo, Eriksson and Sharma 2004).

The exporting activities of Canadian SMEs — defined as firms with fewer than 500 employees — can be measured in various ways: by transactions data, firm-level surveys or longitudinal data, each with its own strengths and weaknesses.5 Assembling the evidence from all these sources thus provides a more comprehensive look at Canadian SME trade.

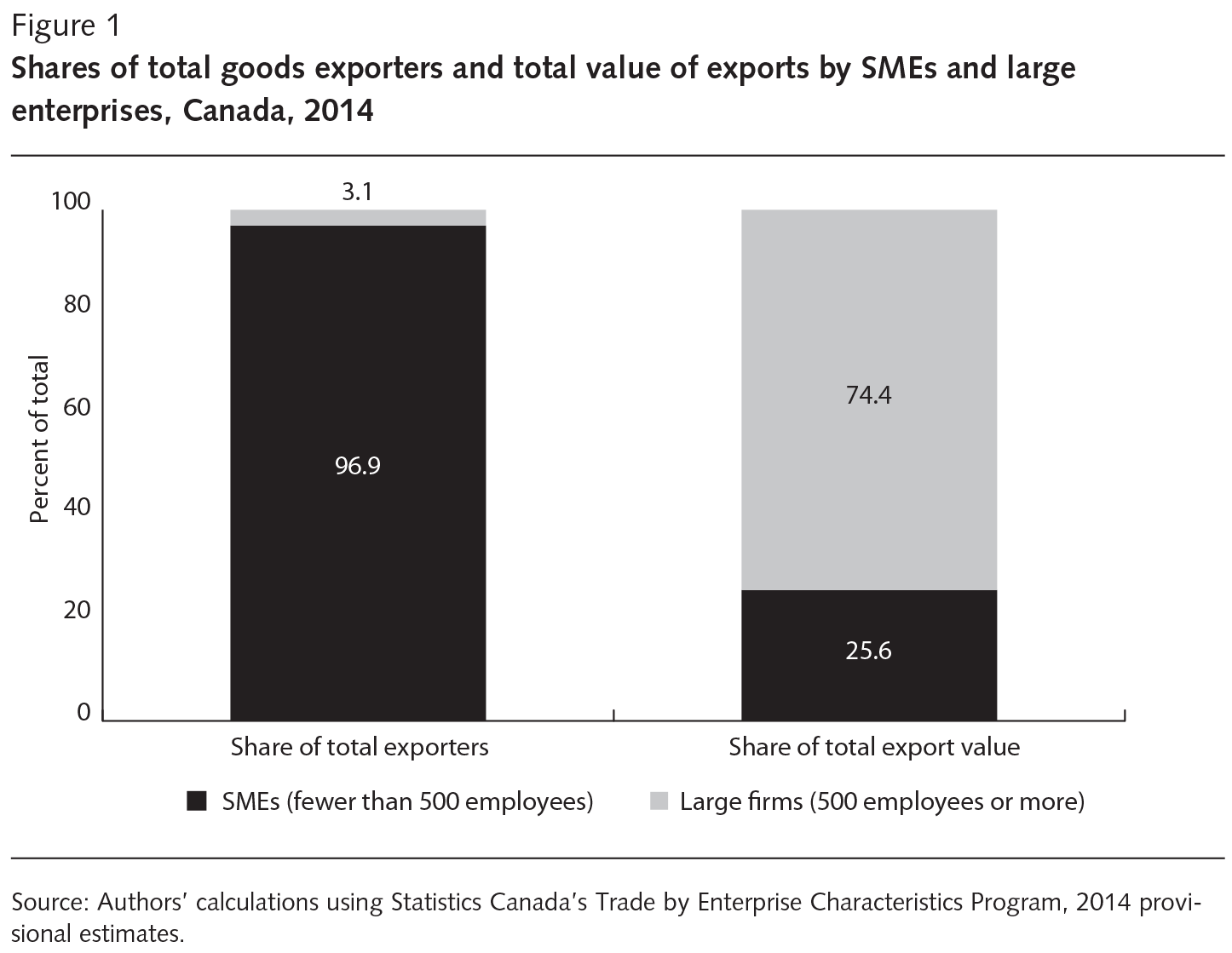

We begin with a detailed snapshot of the recent goods-exporting activities of Canadian firms, reported by employment size, using Statistics Canada’s export transactions data. In 2014, more than 41,000 goods-exporting enterprises were operating in Canada;6 97 percent of them were SMEs — see figure 1. Export revenues, however, were highly concentrated among a handful of large firms,7 which averaged $276,809, compared with only $2,995, on average, for SMEs. Nonetheless, many SMEs are active direct exporters, collectively contributing about one-quarter of the total value of Canada’s exports — leaving aside indirect contributions by small firms that act as domestic suppliers to large firms that subsequent export.

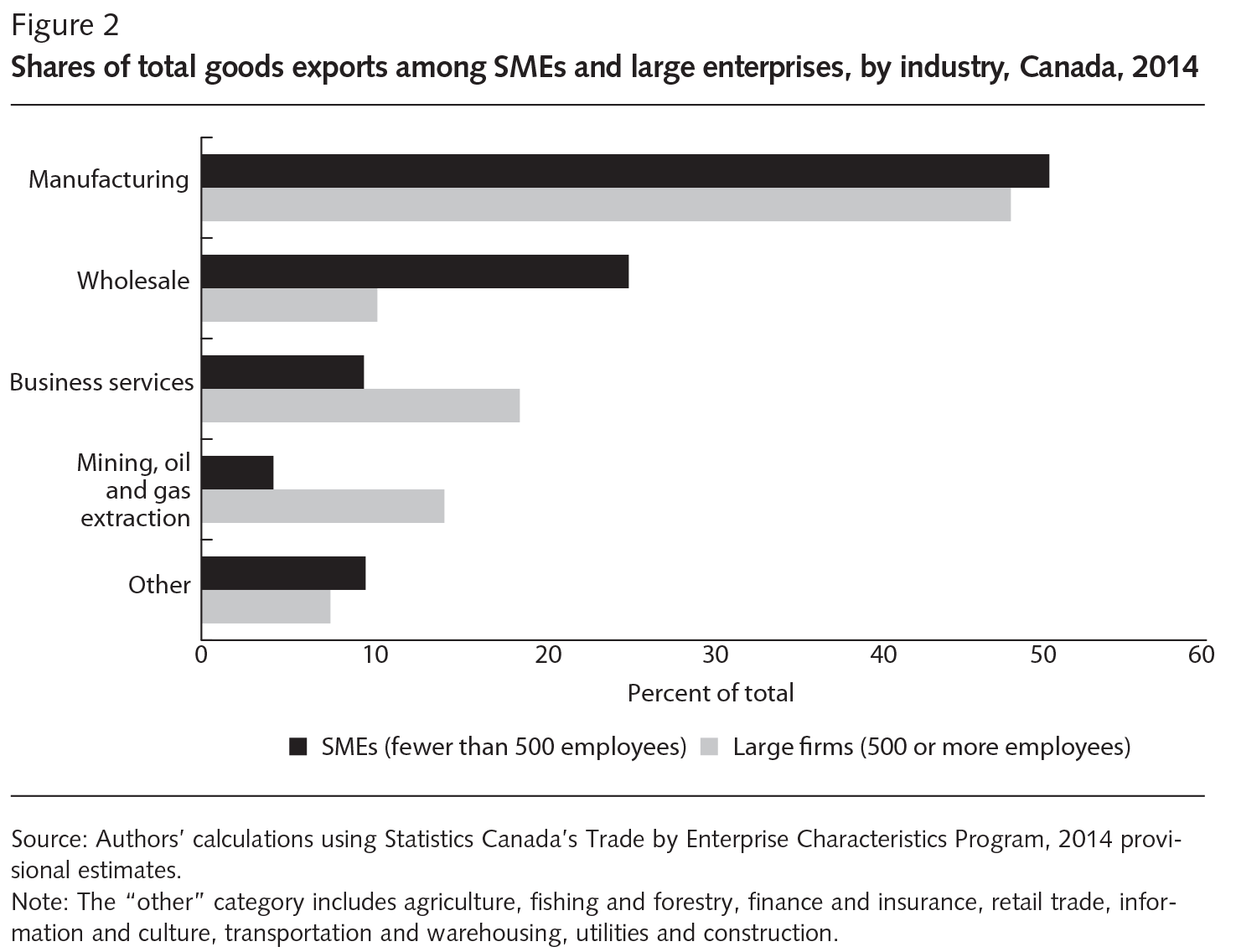

For both SMEs and large firms, manufacturing is by far the largest exporting sector, responsible for roughly half of the value of all Canadian goods exports (figure 2). For SMEs, wholesale trade is the second most important export industry, followed by business services.8 Wholesale trade, however, has a lower average export value than do sectors such as mining, oil and gas extraction, transportation equipment, and finance and insurance, where large firms predominate. In 2014, if the SME export basket had had the same industrial composition as that of large firms, the value of total SME exports would have been 56 percent greater, all else being equal.

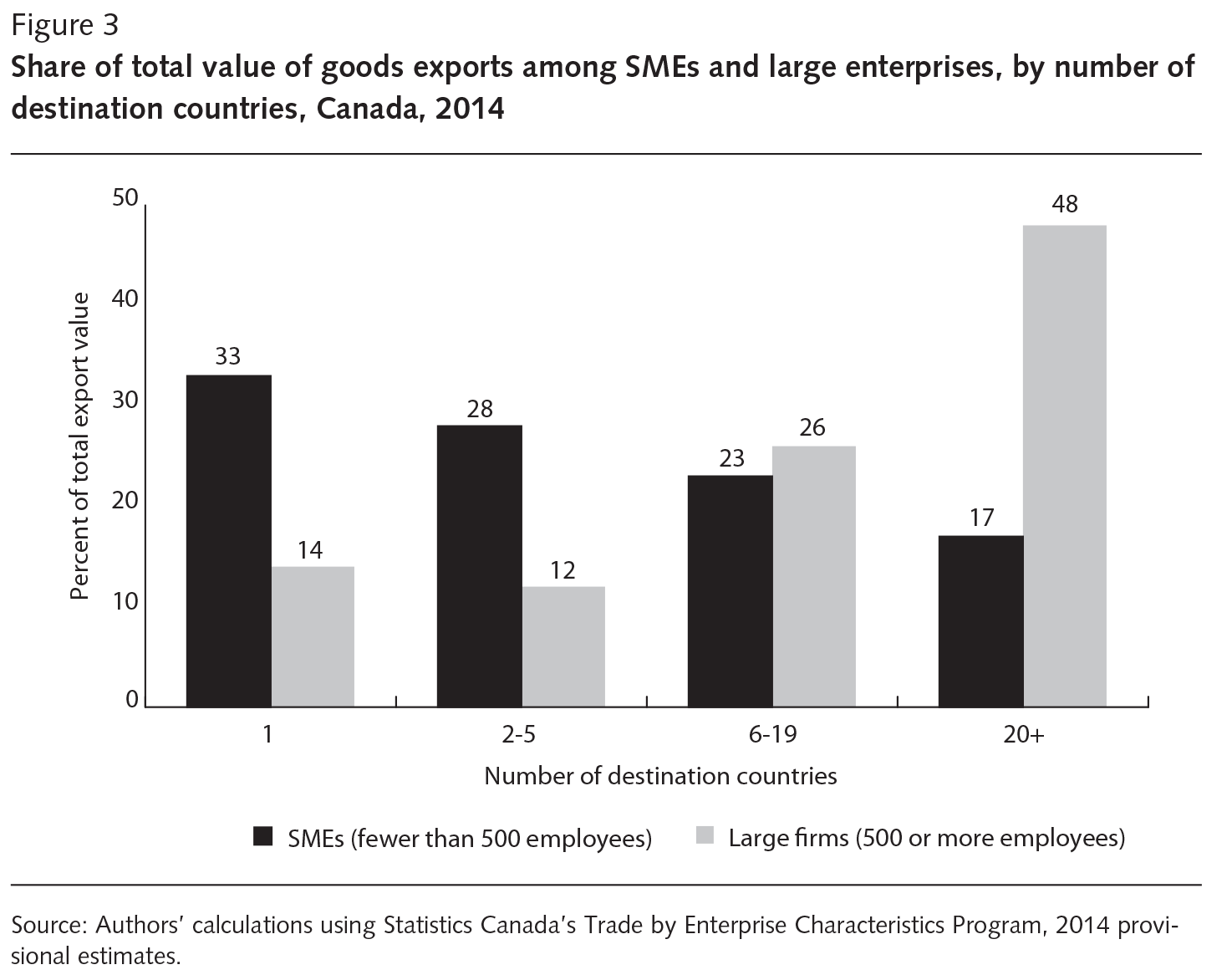

Given the large fixed costs of exporting, it is not surprising that small firms tend to reach fewer export markets than do large firms: in 2014, most served only one, while most large exporters served multiple markets.9 Also, the export revenues of large firms are much more concentrated among those that are active in many markets: those that exported to twenty or more countries in 2014 accounted for nearly half of the export values of large firms, compared with only 17 percent for SMEs (figure 3). For this reason, SME trade may be viewed as “more inclusive” than trade by large firms, as the outcomes are more widely dispersed.

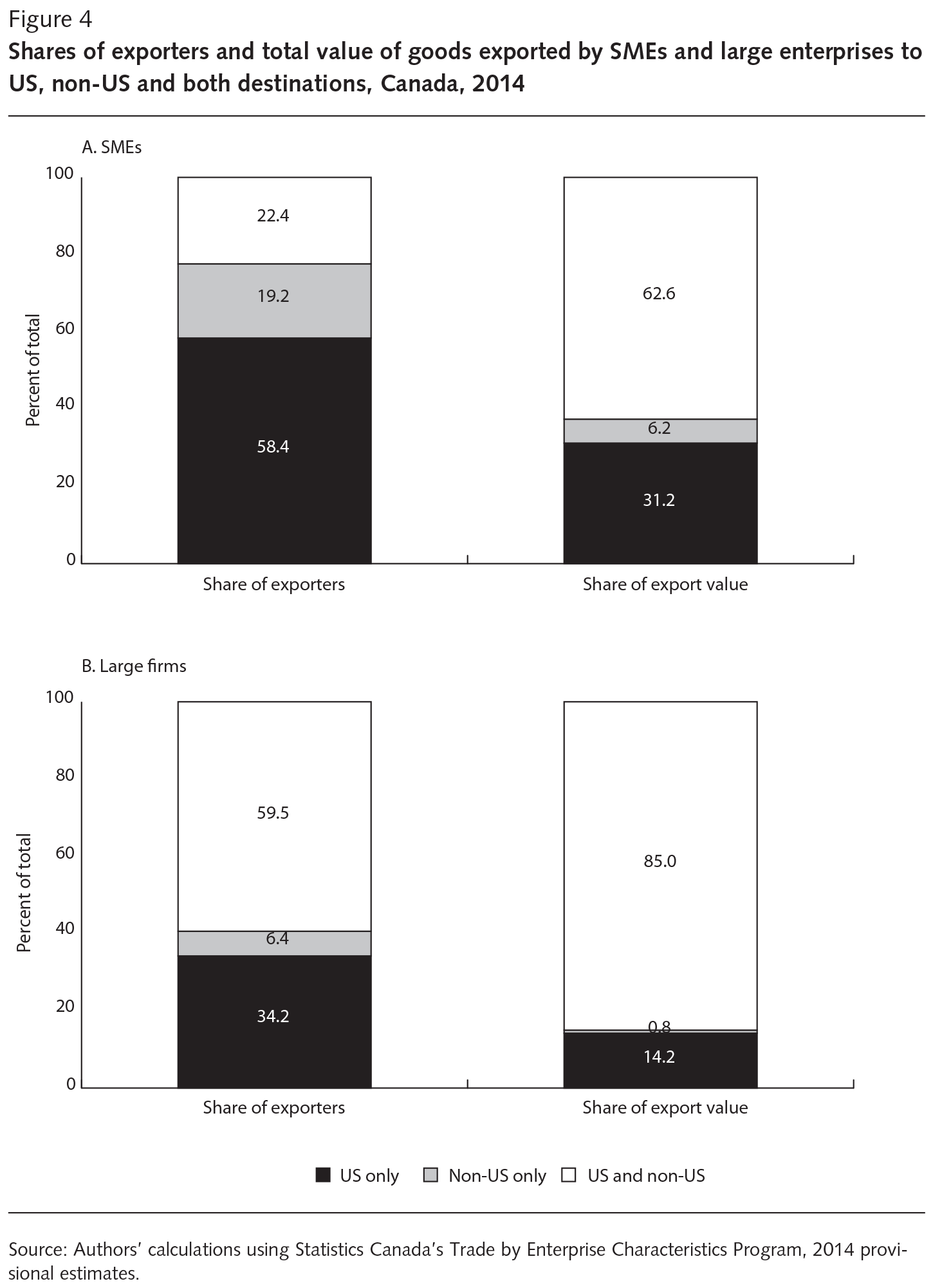

Focusing now on the actual destinations of Canada’s good exports, we first distinguish between the traditionally dominant United States and all other destinations. Consistent with the number of countries SMEs and large firms serve, it is no surprise that SMEs are more singularly focused on the US market than are large firms; as figure 4 shows, more than half exported solely to that market. Again, however, firms that exported to multiple market types were responsible for most of the overall export values — 63 percent for SMEs and 85 percent for large firms.

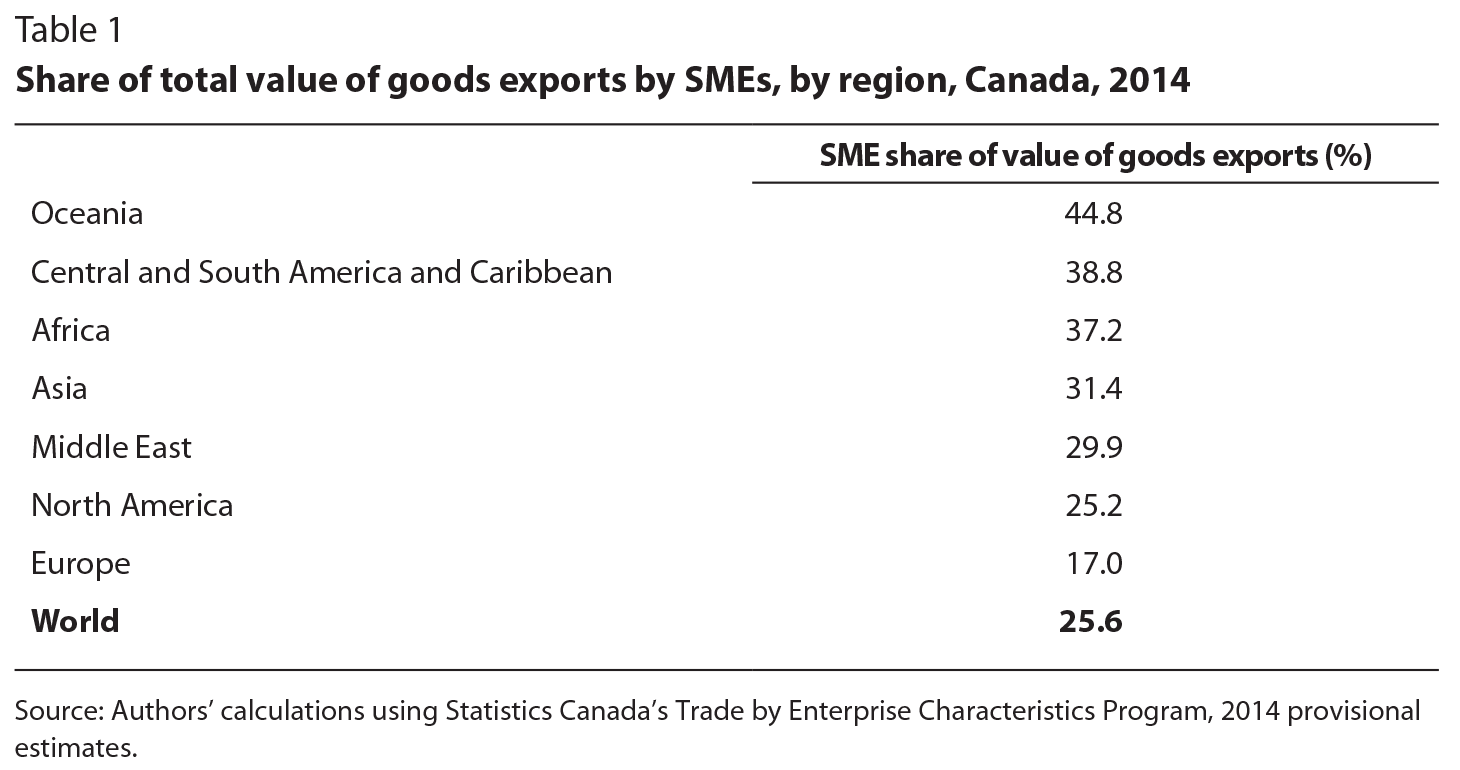

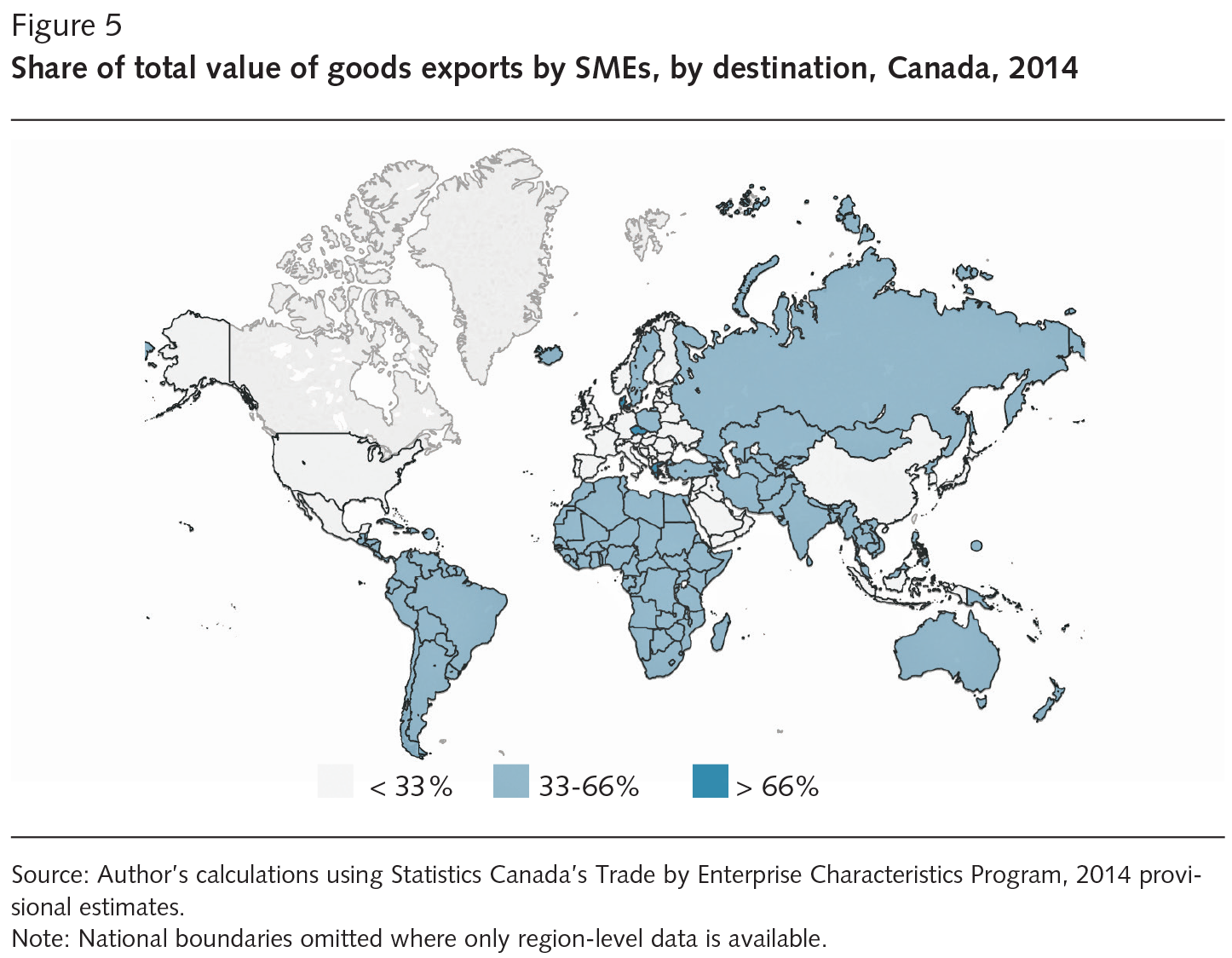

SMEs’ shares of total Canadian export values were generally highest in more distant emerging markets in Oceania, Latin America, Africa, Asia and the Middle East, and lower in closer advanced economies in North America and Europe (see table 1 and figure 5). These results might seem counterintuitive: does this not suggest that smaller firms are more successful than large firms at reaching more distant markets? Not necessarily. Koldyk et al. (in this volume) offer a more likely explanation: many Canadian companies use domestic production facilities to serve closer North American markets via exports, while increasingly serving more distant overseas and emerging markets via outward foreign direct investment (FDI) and foreign affiliates. Although Canadian foreign investment data are not reported by firm size to confirm this hypothesis, it stands to reason that large firms are much more likely than SMEs to undertake FDI (due to the large start-up costs involved) and to use foreign affiliates (which are often part of larger multinational enterprises). That is, large firms’ export shares are generally lower in emerging markets likely because these firms are more able than small firms to serve those markets through direct investment and foreign affiliates, rather than through exports.

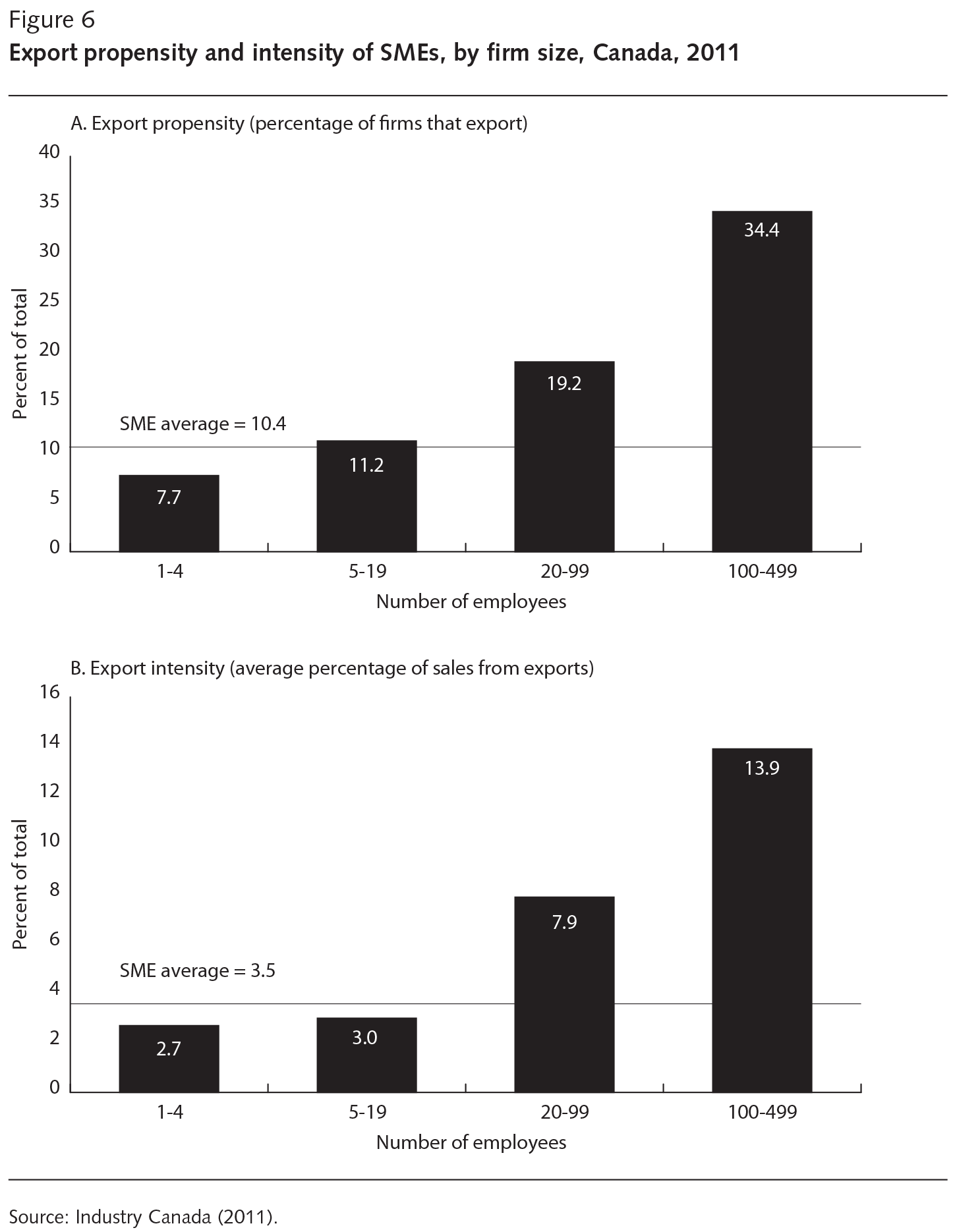

Industry Canada’s Survey on Financing and Growth of Small and Medium Enterprises is less precise on export values than Statistics Canada’s transactions data. It nevertheless provides a useful complementary perspective by narrowing in on SMEs’ overall exporting activities, both goods and services. In 2011, 10 percent of SMEs exported a good or service, but export sales accounted for only about 4 percent of their revenues (Industry Canada 2015); see figure 6.

Even among SMEs, size clearly matters for trade outcomes, as smaller firms trade less than larger firms. Both export propensity (the percentage of businesses that sell goods and/or services abroad) and export intensity (the percentage of total business revenues that comes from exports) increase with firm size, and in 2011 were much higher for medium-sized firms (100-499 employees) than for small businesses (fewer than 100 employees). Industry Canada (2015) attributes these findings to two factors: first, foreign sales can be a source of new growth for larger SMEs when their products are at older and generally slower growth phases of their life cycles; and, second, larger SMEs typically have more capacity to export, including the requisite financial and human resources.

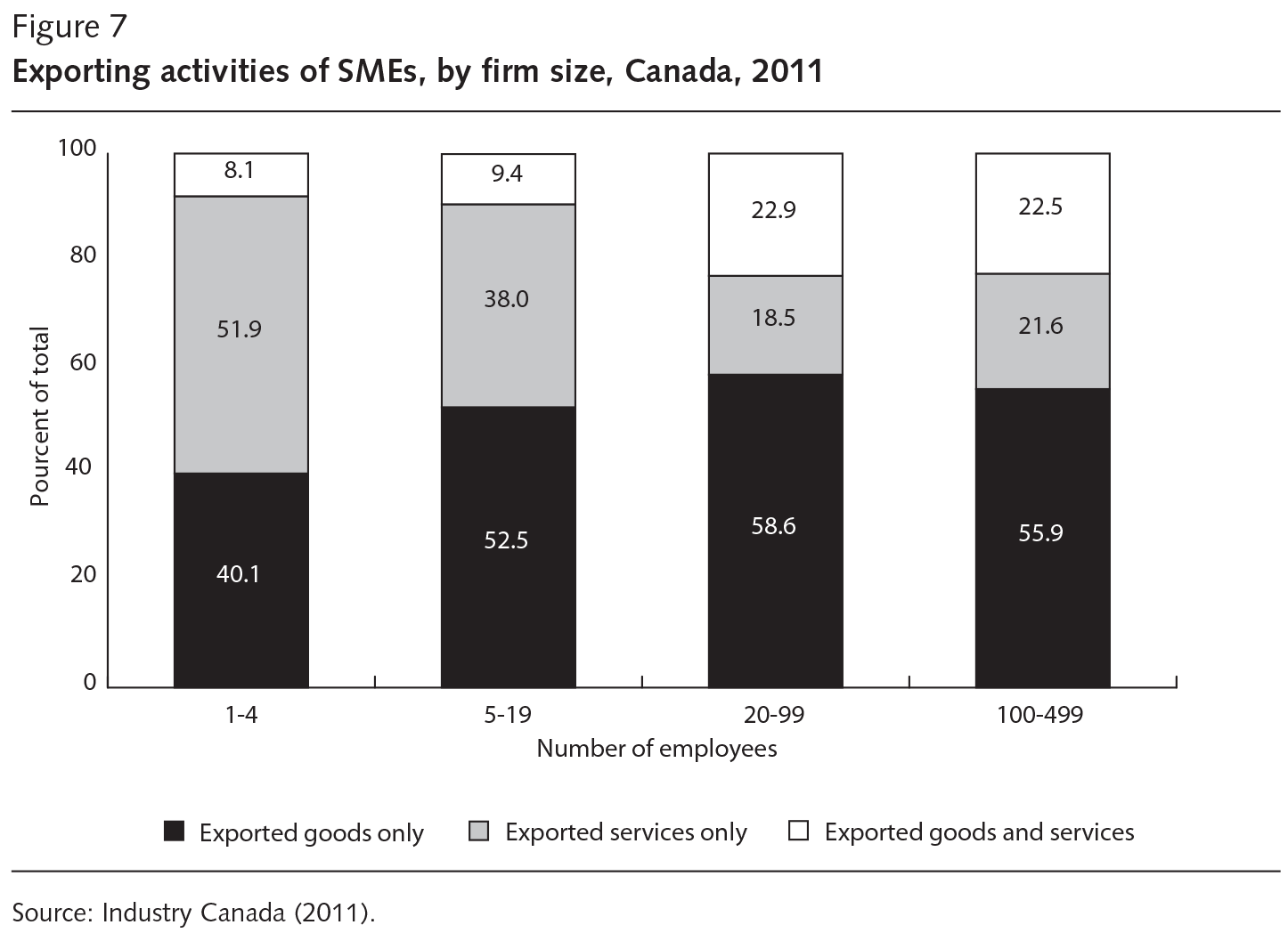

According to the Industry Canada (2015) survey, among all exporting SMEs in 2011, 49 percent exported only goods, 39 percent exported only services and 12 percent exported both. Results by firm size are consistent with the existence of larger economies of scale in goods production than in services. In other words, it is generally easier for small services producers than small goods producers to compete in world markets because goods production -generally requires higher fixed costs to enter. Indeed, exporting goods was more common for larger SMEs, whereas exporting services was more common for smaller firms. Among exporters, “micro” SMEs (those with fewer than five employees) were more likely to export only services (figure 7).

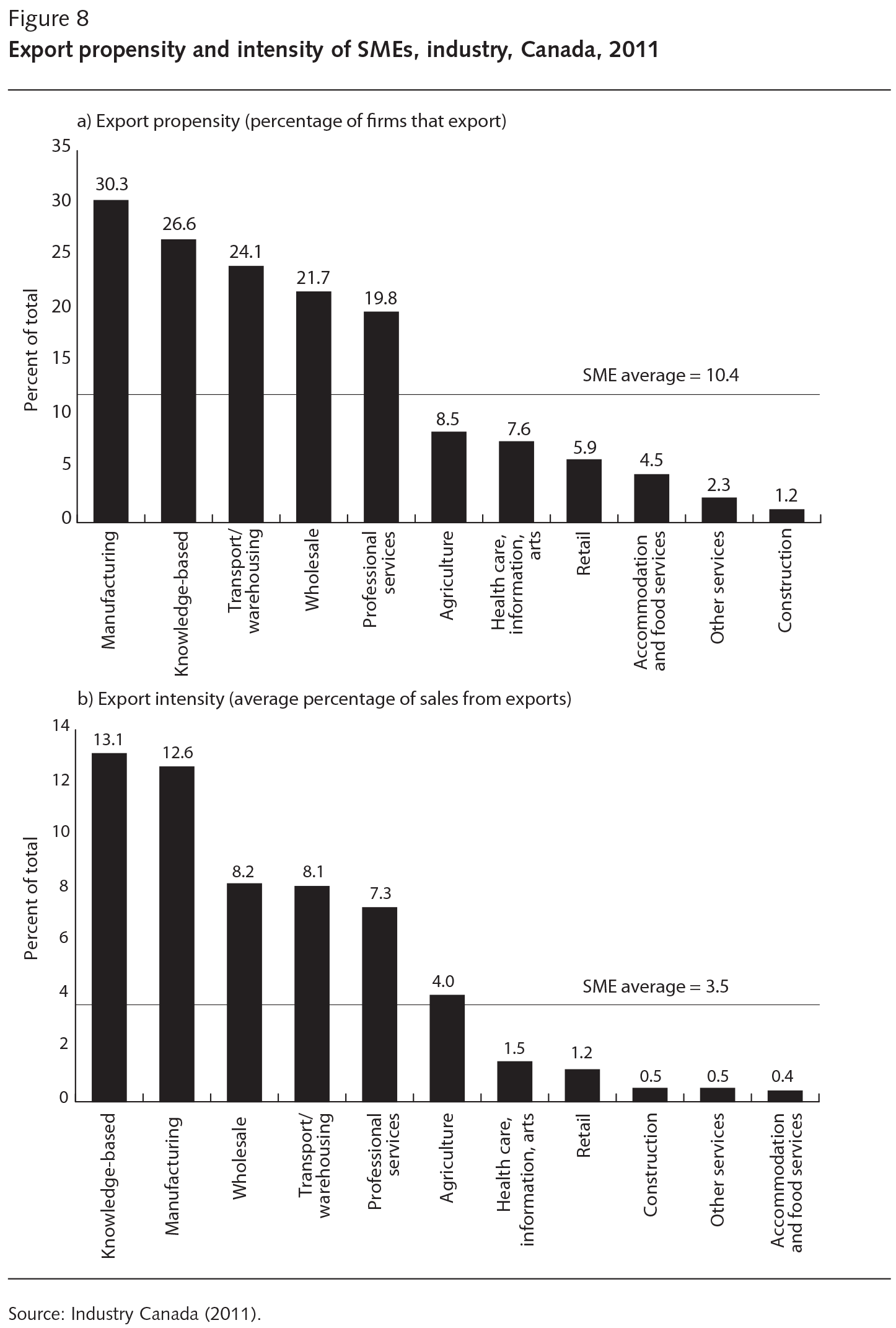

Manufacturing is a key exporting industry for SMEs, but the Industry Canada survey reveals that services-intensive knowledge-based sectors, including information and communications technologies and business consulting, also feature prominently.10 Other important export sectors for SMEs are wholesale trade, transportation and warehousing, professional services and agriculture (figure 8).

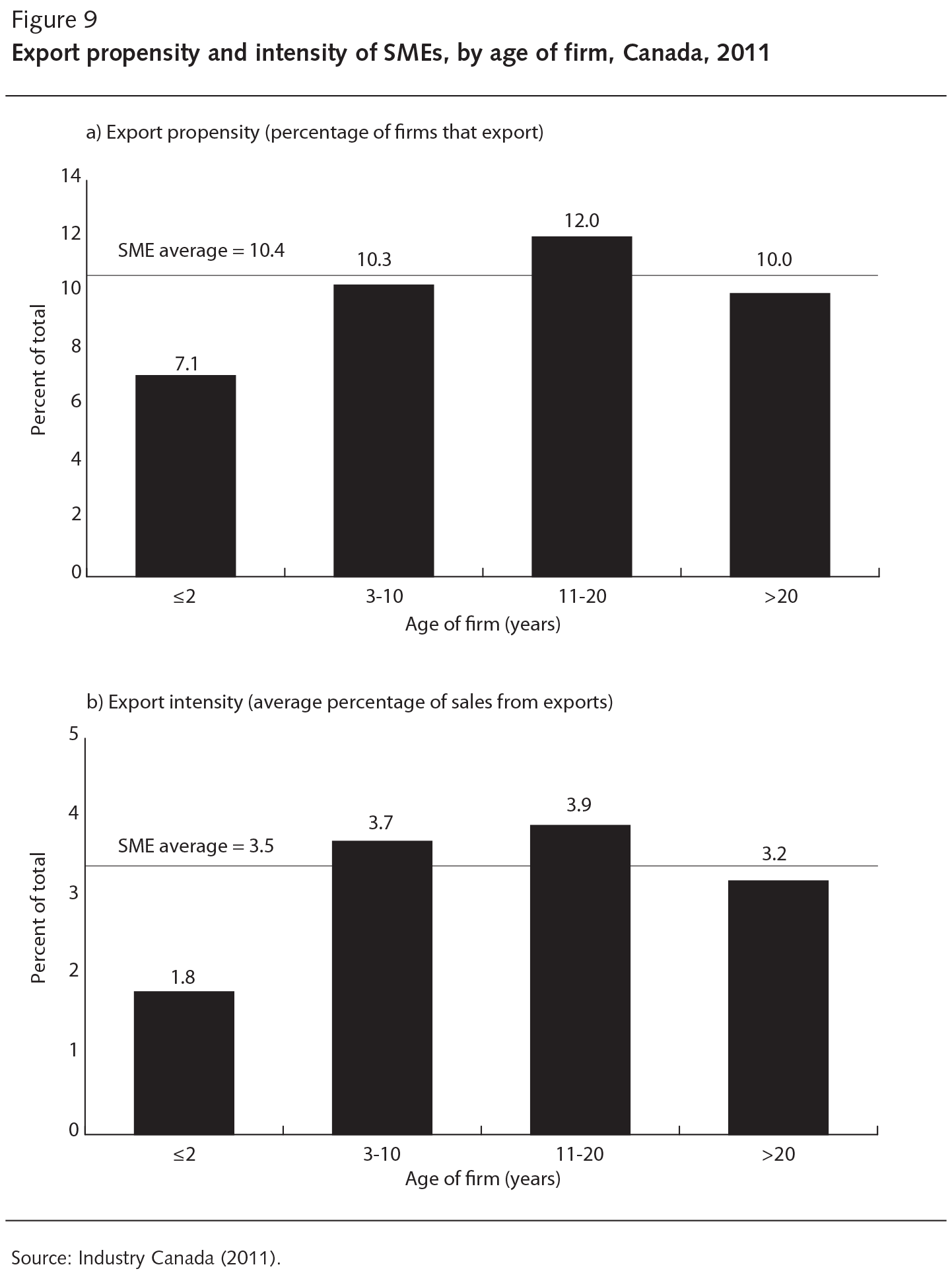

During their first few start-up years, the vast majority of firms focus primarily on domestic sales. Older, more established firms are more likely to export (figure 9). About 7 percent of the youngest SMEs (two years old and younger) — which includes some of the born global firms — exported a good or service in 2011.

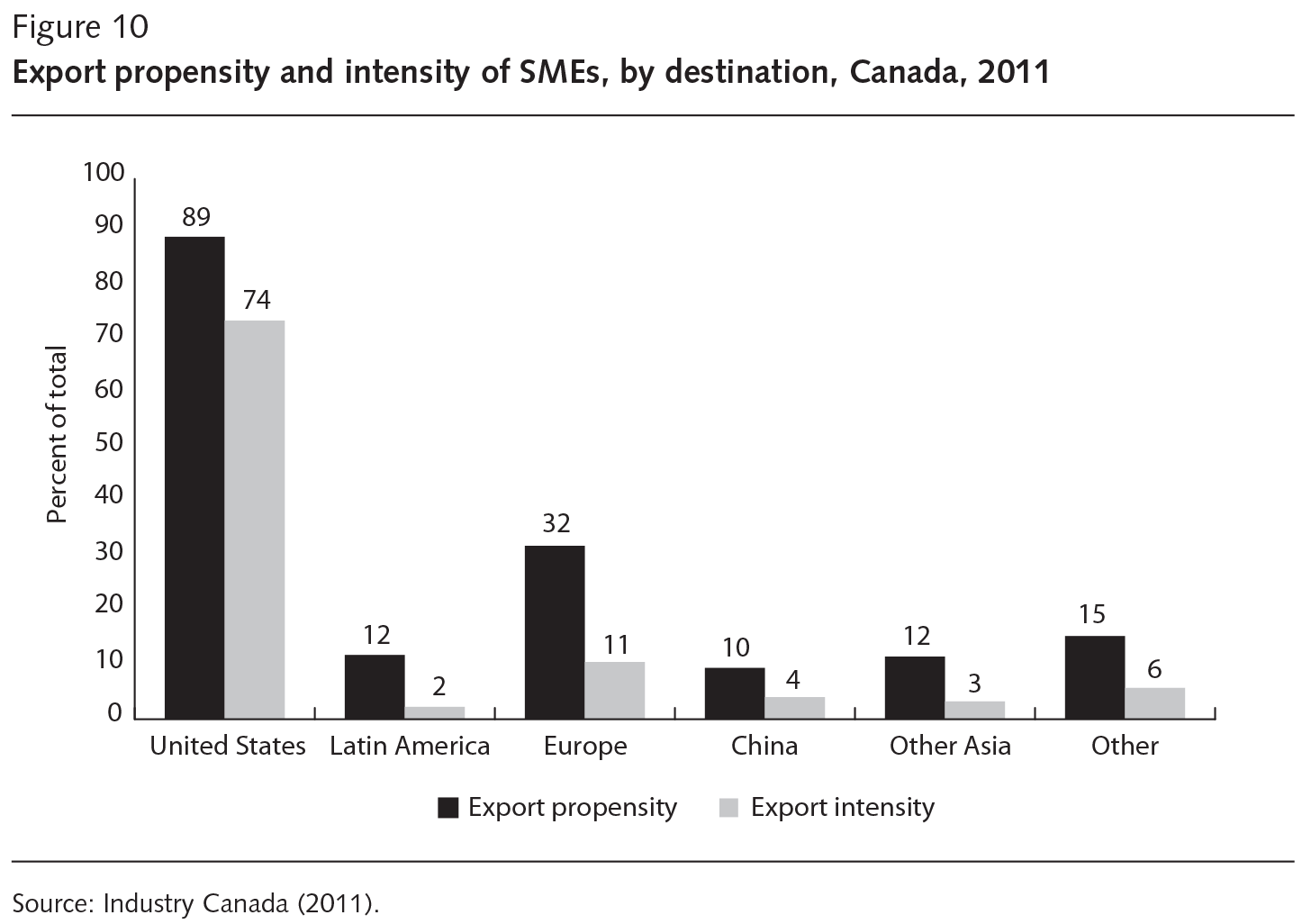

As with the transactions data, the survey data from Industry Canada reveal that exports of goods and services by SMEs are highly concentrated in the US market: 89 percent of SME exporters sold there in 2011, representing almost three-quarters of all export revenues (figure 10). Europe was the second most frequent destination, while around 10 percent of SME exporters sold to what might be considered emerging markets. Within Canada, SMEs trade patterns vary by geography and market proximity. Not surprisingly, firms in British Columbia were more likely to export to Asia, firms in central Canada to the United States and those in Atlantic Canada to Europe. Thus, the export baskets of SMEs in the coastal provinces are more market diversified than those in central Canada (Industry Canada 2015).

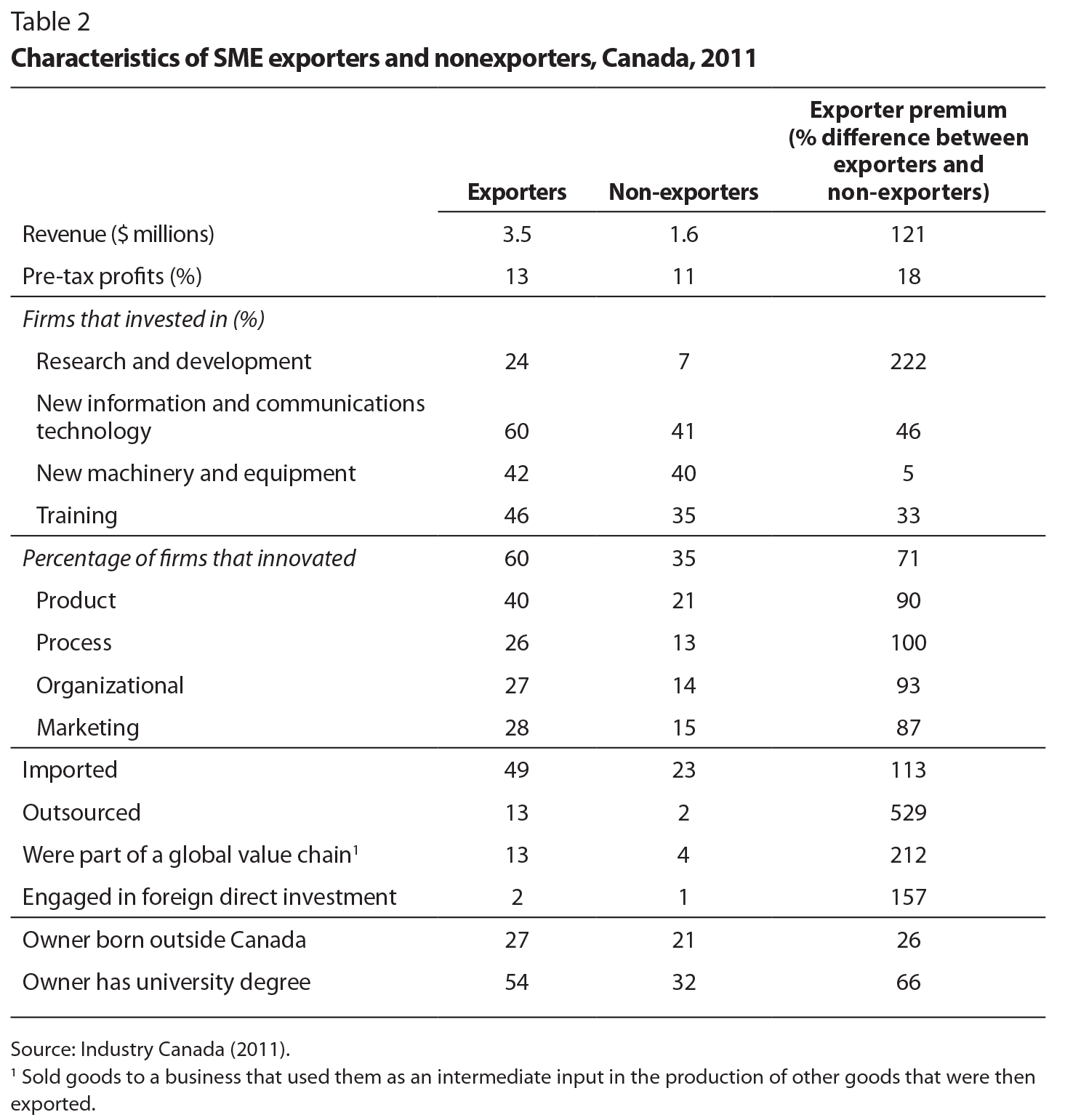

Many researchers have documented that exporters outperform nonexporters according to several measures (see, for example, Baldwin and Yan on trade and productivity, in this volume). As table 2 shows, this general result also holds for Canadian SMEs: in 2011, exporters had higher revenues and profits and invested more in research and development, machinery and equipment, and training. They were also more innovative and more involved in other international activities, such as importing, outsourcing and global value chains. As well, the owners of exporting SMEs were more likely to be born outside Canada and to have higher levels of formal education than Canadian-born owners.

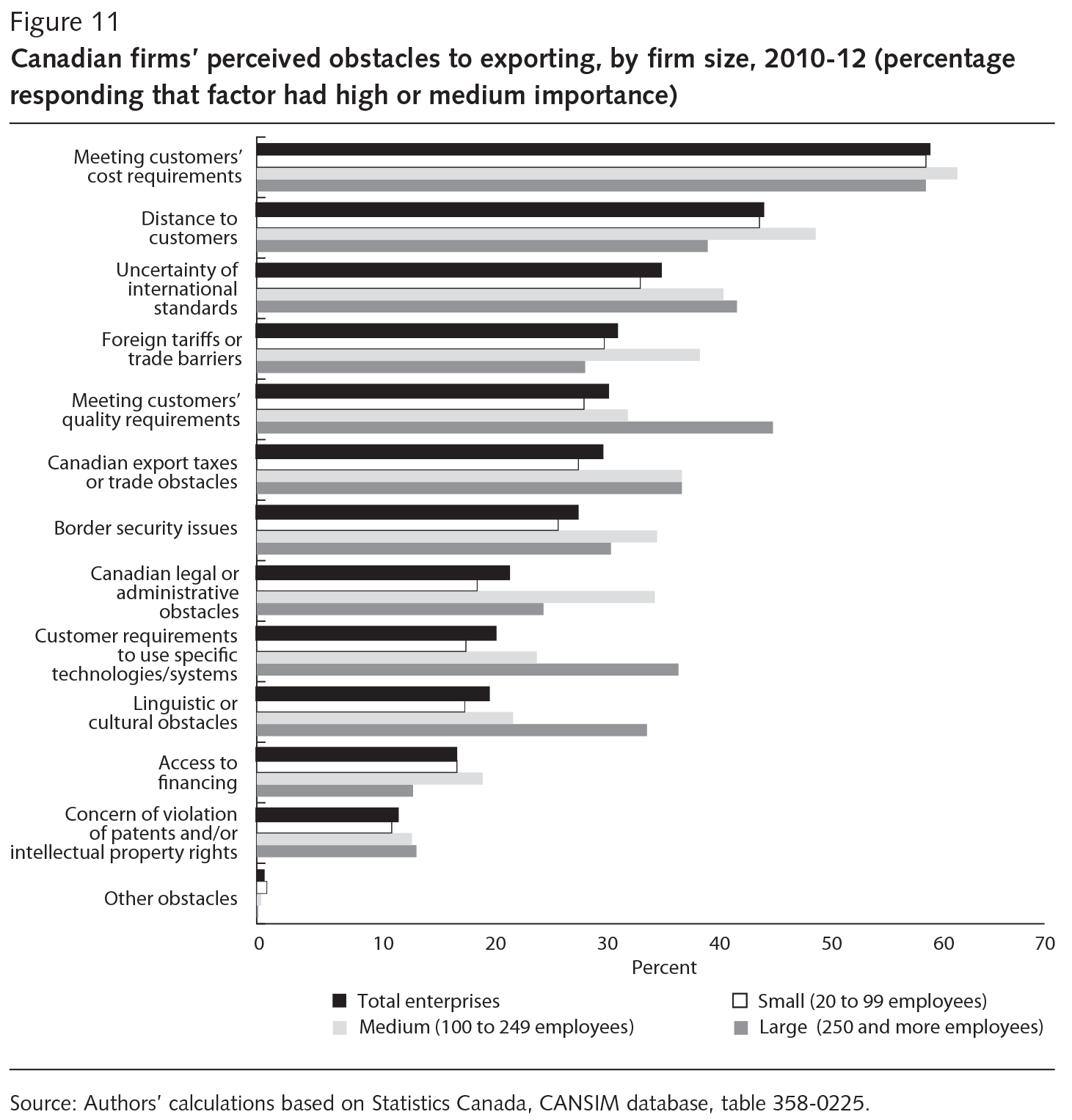

Another Industry Canada survey, the 2012 Survey of Innovation and Business Strategies, provides evidence of what firms perceive to be obstacles to exporting. Some of these factors (for example, tariffs) are more amenable to policy intervention than others, such as geography, which is more of a given — notwithstanding how emerging technologies are reducing the importance of distance for trade; see Ahmed and Melin, in this volume. At the top of the list of obstacles, was meeting customers’ cost requirements, which 60 percent of firms that exported, or attempted to do so, over the 2010-12 period deemed to be of high or medium importance (figure 11). Other often-cited obstacles were distance to customers; uncertainty of international standards; tariffs and trade barriers; meeting customers’ quality requirements; and Canadian export taxes or trade obstacles. Only 21 percent of respondents cited linguistic or cultural barriers as of high or medium importance — despite the emphasis on such obstacles in the international business literature. Moreover, these barriers were much less of a concern for SMEs than for large firms; as we will see later, language is an area of relative strength for SME exporters owned by recent immigrants to Canada. Access to financing was even farther down the list (cited by 18 percent), but was slightly more of a concern for smaller firms. It is noteworthy that, for most obstacles, the responses of small firms did not differ much from those of large firms — defined in this survey as those with 250 or more employees.

In contrast to the transactions and survey data, which provide information on exporting activities in a largely descriptive and static manner — that is, without attempting to control for other factors that affect outcomes, and viewed only at a recent point in time — longitudinal data have the advantage of tracking firms over time.

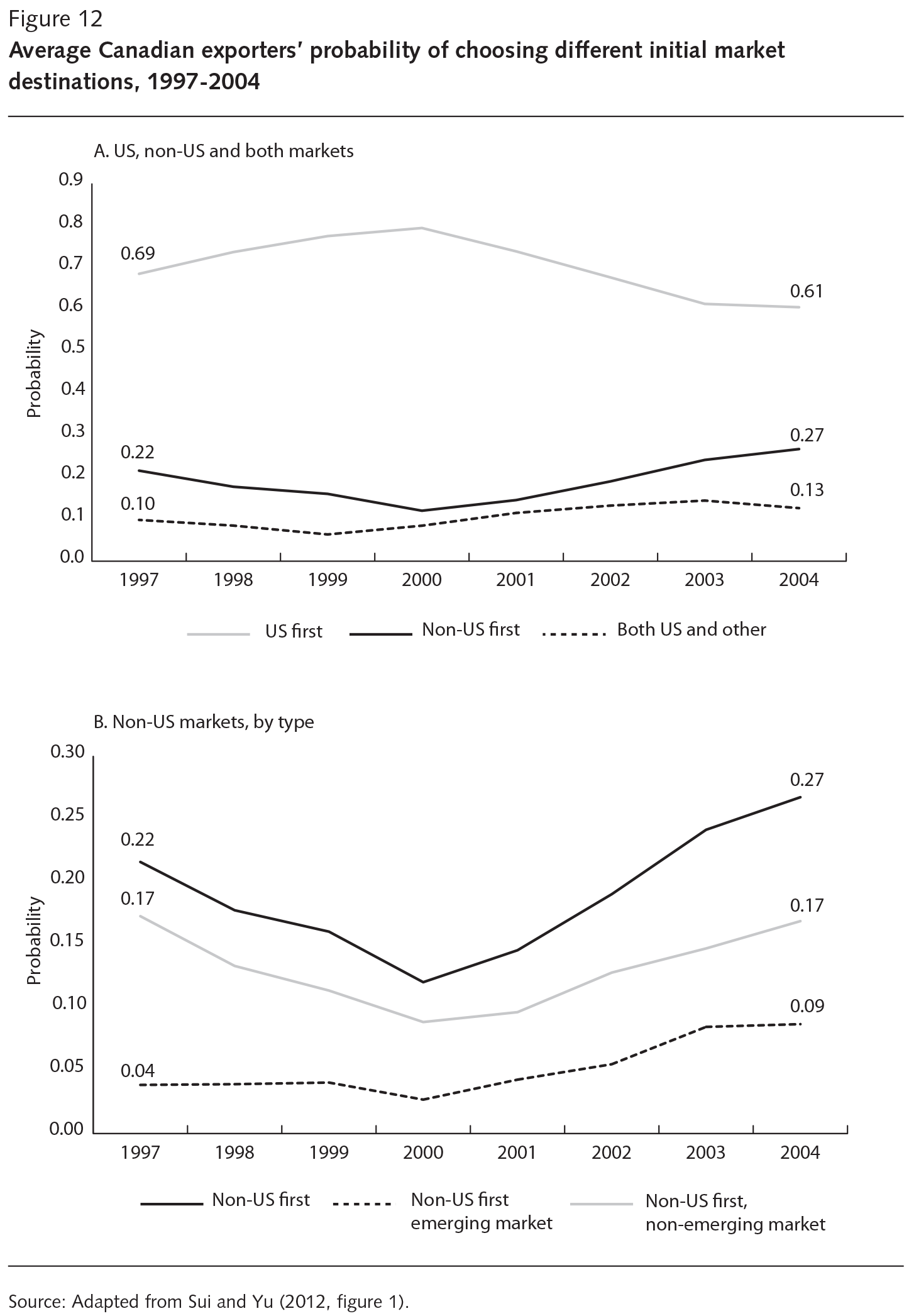

Sui and Yu (2012) find that a distinct shift occurred in the foreign market expansion patterns of Canadian SMEs around 2000.11 On average, over the period between 1997 and 2005, most SME exporters (69 percent) chose the United States as their first export destination (figure 12). This share initially rose from 1997 to 2000, coincident with strong economic growth in the United States and weakness in some emerging markets related to the 1997 Asian economic crisis. After 2000, however, the probability that a new Canadian exporter chose the United States first fell quickly, concurrent with a thickening of the Canadian-US border after the 9/11 terrorist attacks (Burt 2009; Ferris 2010; Globerman and Storer 2009). The “US-first” firms were generally younger, less productive and more likely to be Canadian-controlled, and they exported fewer product varieties.

Meanwhile, a smaller but growing share of SME exporters chose less-traditional export market pathways. On average, between 1997 and 2005, 17 percent of SME exporters chose a market other than the United States (on its own) for their initial destination, with the share rising significantly after 2000, reaching over one-quarter in 2004. These firms were generally the smallest exporters, more likely to operate through a single establishment and to be non-US foreign-controlled.

There was also a slight increase in the proportion of firms that started exporting to both the US and other markets at the same time, rising to 13 percent. These firms were generally the largest and most productive, and were also the most likely to be US-controlled and to have multiple establishments and more diversified products. There was also a clear increase over this period in the share of SME exporters that chose emerging markets as their first export destination.

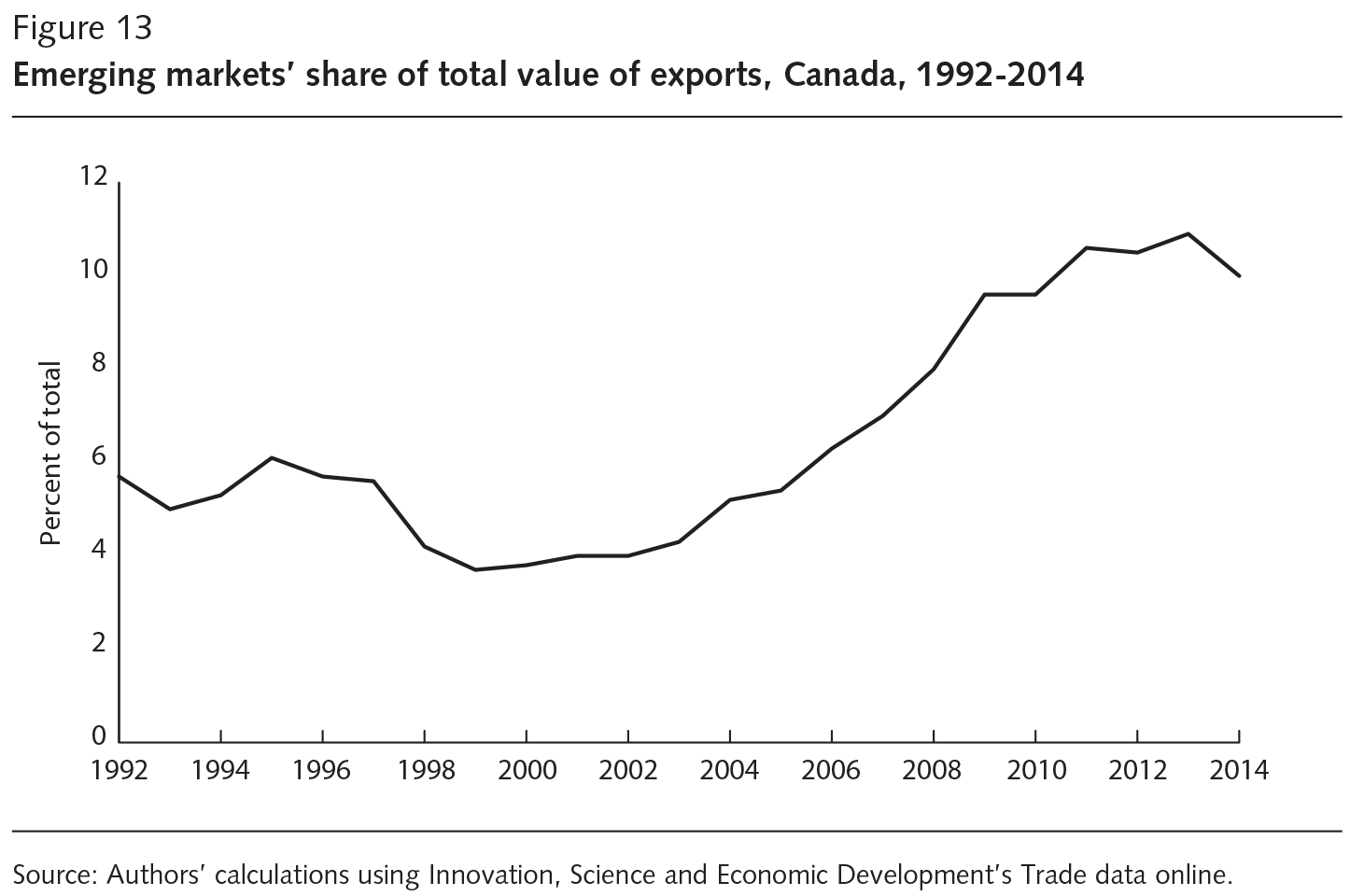

Consistent with the firm-level economic theory, an analysis of the pathways Canadian exporters take to break into emerging markets (Sui and Yu 2013)12 finds that those that did so successfully were the most efficient producers — that is, they had the highest labour productivity and lowest unit labour costs.13 They were also more likely to be foreign-owned. Unfortunately, the detailed firm-level data used in that analysis are not yet available for the period after the global recession that began in 2008. In lieu of that data, we constructed results based on aggregate trade data to investigate whether the general trend of increased Canadian exports to emerging markets has continued — at least overall, if not necessarily for new Canadian exporters or SME exporters. Using the categorization of emerging market “priority countries” identified in the Harper government’s Global Markets Action Plan,14 we find that the overall share of Canadian exports going to emerging markets rose from 4 percent in 2000 to over 10 percent in 2014 (figure 13) — results that are consistent with those of the earlier firm survey presented in figure 10. The upward trend over this period is also consistent with the generally stronger economic growth in emerging markets, such as China, and the slow recovery in advanced economies after the global financial crisis, particularly in Europe. These results suggest that the trend of Canadian firms increasingly choosing emerging markets as their initial export destination likely has continued since the global recession.

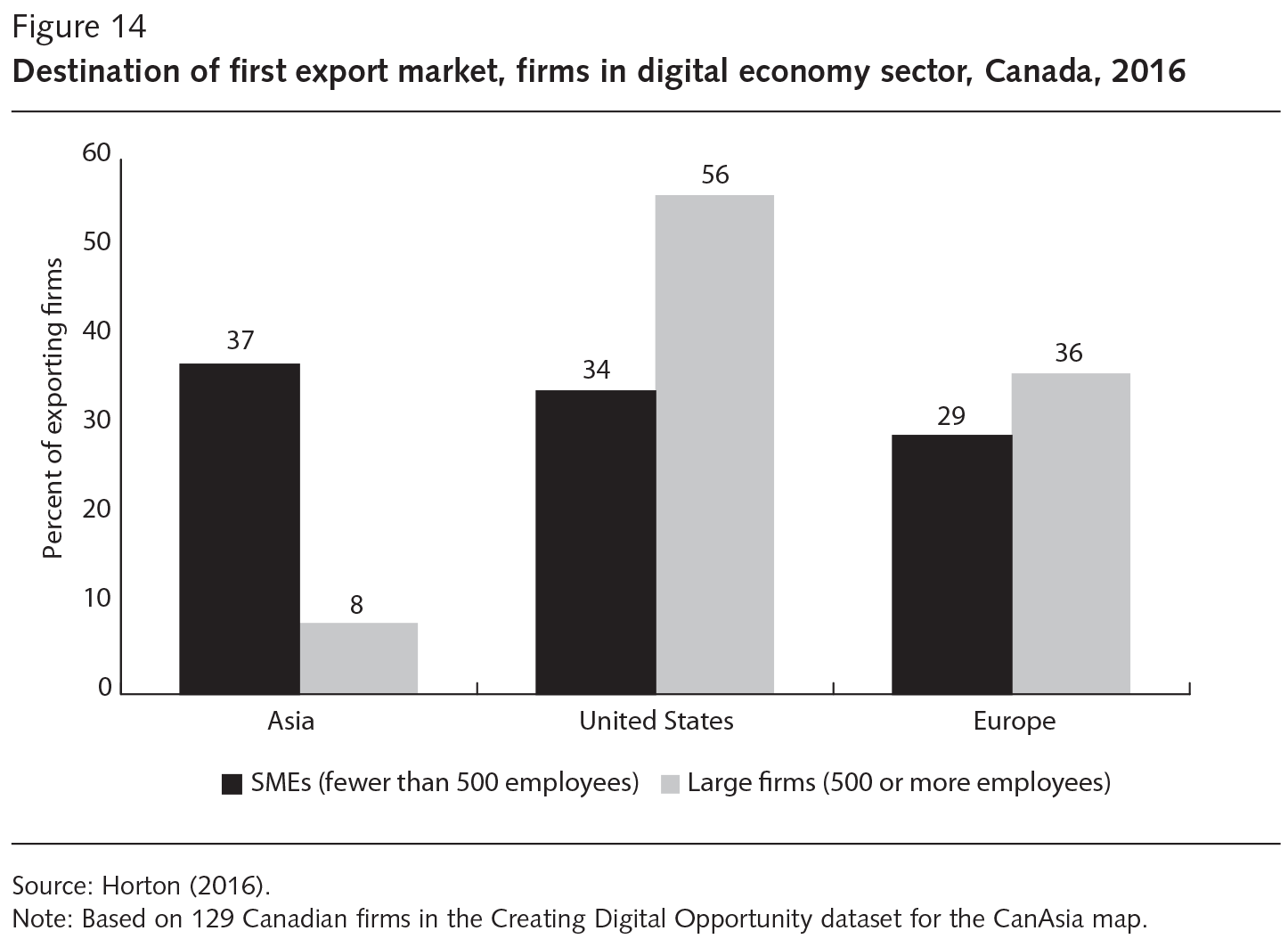

Further suggestive evidence comes from an interesting new data source being developed at the University of Toronto’s Munk School of Global Affairs. This source — the CanAsia mapping project, which maps the locations of Canadian businesses operating in Asia — shows that the export patterns of SMEs are becoming increasingly geographically diverse. Preliminary analysis focusing on firms in the professional and technical services sector, including software companies, finds that SMEs are actually more likely to export first to Asia than to the traditional US export market. By contrast, large digital economy firms remain more likely to export first to the United States, followed by Europe and then Asia (figure 14).

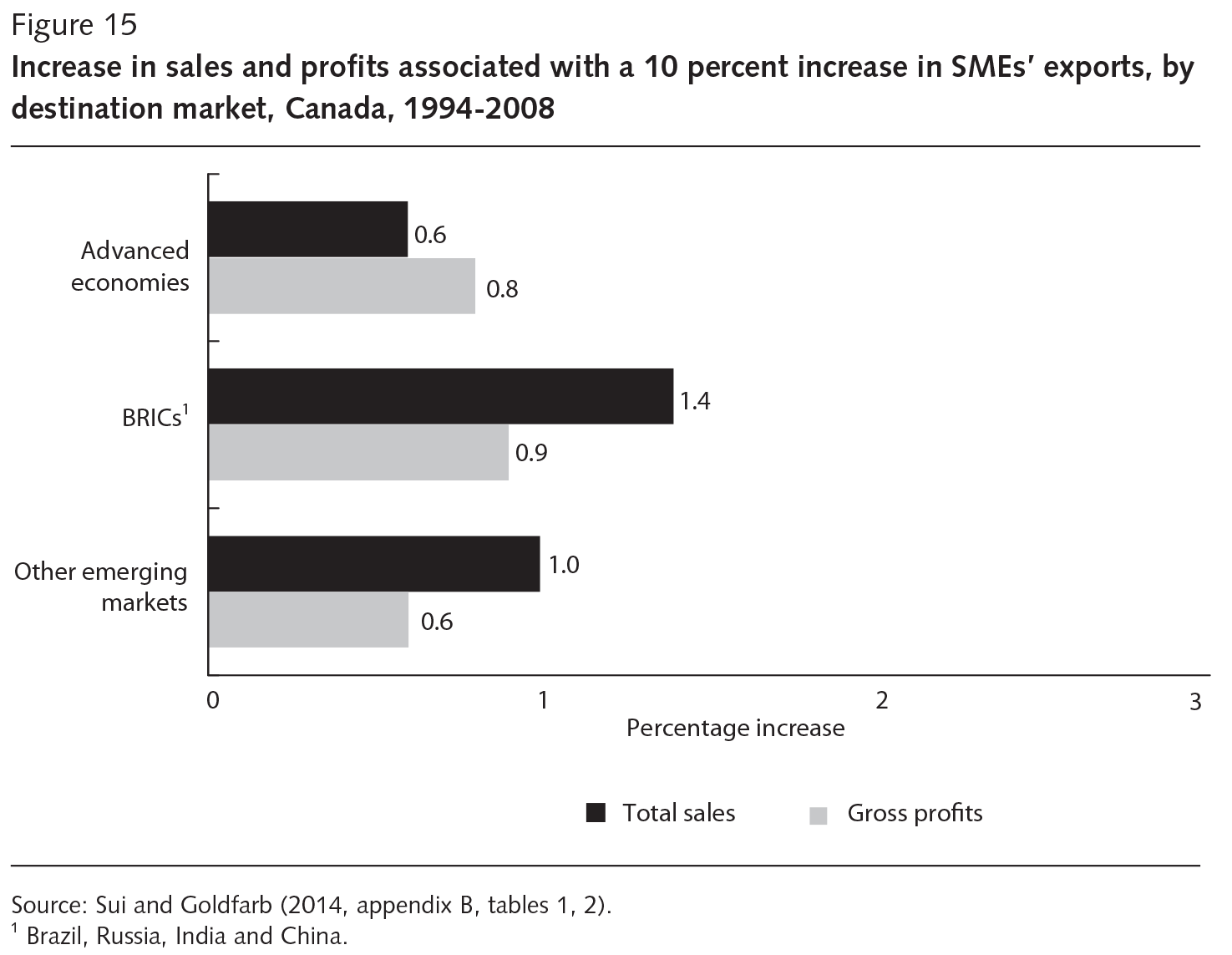

Given the policy focus on getting more Canadian SMEs to export to emerging markets, it is important to know if systematically larger performance benefits are -associated with exporting to these markets. To that end, Sui and Goldfarb (2014) investigate the effects of exporting to different market types on the performance of Canadian SMEs over the period from 1994 to 2008, grouped by those that export to advanced markets (the United States, the European Union and Japan); the BRICs markets (Brazil, Russia, India and China); and other emerging markets. Controlling for other factors, the authors find that exporting is indeed associated with higher sales and profits for Canadian SMEs. And while this holds for all of the export destination groups considered, slightly larger gains came from exporting to the BRICs economies,15 where a 10 percent increase in exports increased SMEs’ total sales and gross profits by 1.4 percent and 0.9 percent, respectively (figure 15).

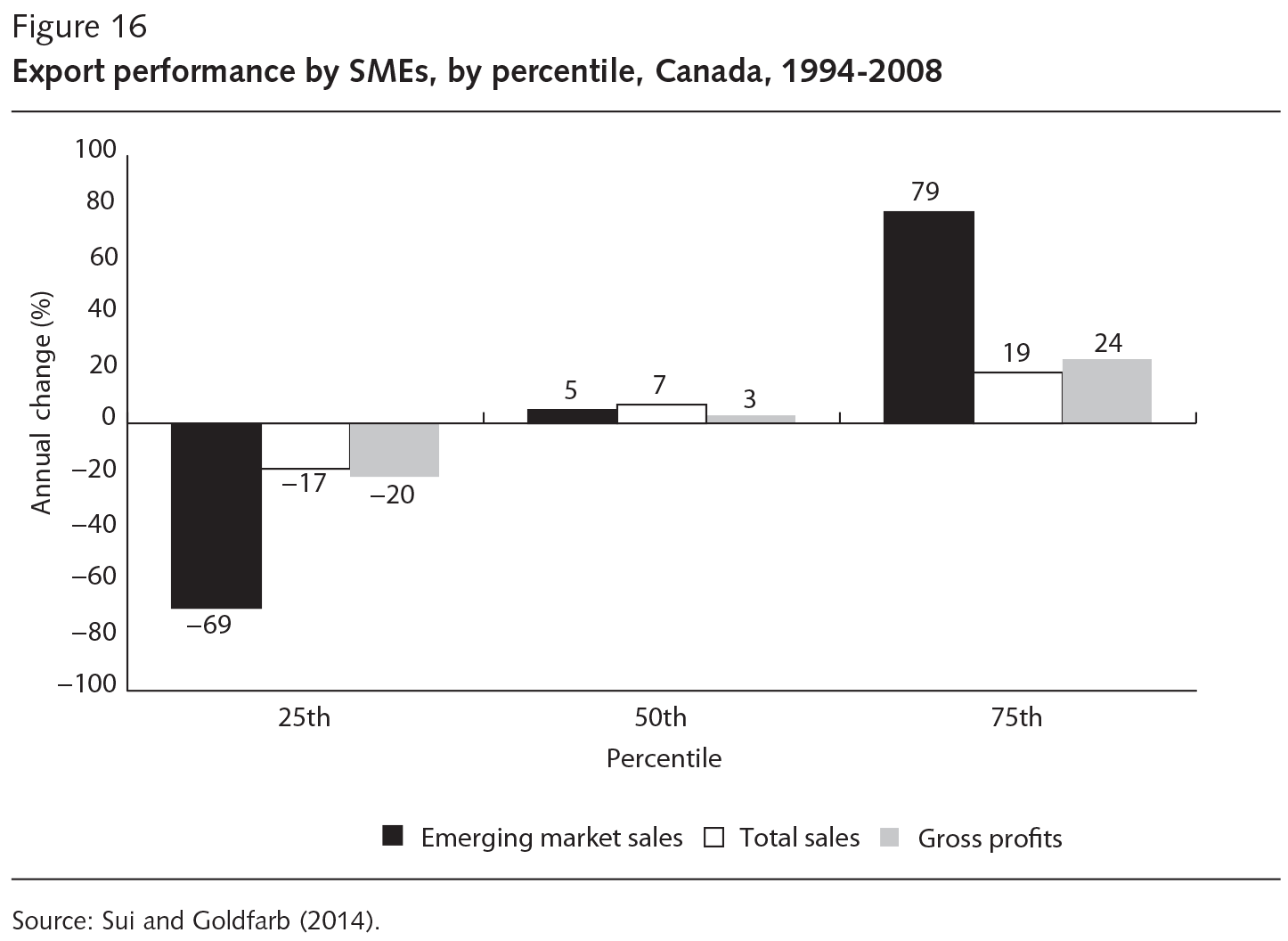

These results suggest that efforts to raise Canadian SMEs’ exports to emerging markets might actually provide a slightly better performance boost than increasing their exports to other destinations — at least on average. But what if emerging markets are riskier? To investigate how closely these results were clustered around the average, the authors examine various performance measures — including the growth of sales and profits and the number of consecutive years operating in the export market — for SMEs that exported between 1994 and 2008, focusing on top performers (those ranked at the 75th percentile of the -relevant -distribution), median performers (at the 50th percentile) and bottom performers (at the 25th percentile), not controlling for firm characteristics.

As figure 16 shows, the median Canadian exporter enjoyed decent performance, but there were huge performance gaps between the top and bottom exporters, particularly in emerging markets. As expected, the top exporters performed quite well: their sales grew by 19 percent and their total profits by 24 percent annually; emerging market sales grew much faster, by 79 percent per year. Bottom-performing exporters, however, had far worse outcomes, with their profits and sales falling by similar amounts to the gains of top performers. This result implies that, in attempting to achieve the slightly bigger rewards in emerging markets, Canadian exporters incur significantly higher risks.

How do export strategies, together with firms’ characteristics, affect the survival of Canadian SMEs in export markets? As Sui and Baum (2014) document, most Canadian exporters (69 percent in their sample) used a “gradual internationalizer” approach, while 25 percent were “born regional”; only a very small proportion (6 percent) were truly born global.16 Born global firms had the highest probability of exit from exporting, followed by those born regional, suggesting that born global firms incur more risk. However, once the authors control for different types of firms generally having chosen different strategies, no particular export strategy seemed to be strictly superior. Sui and Baum conclude that no easy, generic guidance can be offered on which strategy firms should pursue, as it depends on their circumstances. The authors do find, however, that being larger, more innovative and more productive is associated with better export survival, particularly for Canadian exporters operating in non-US markets.

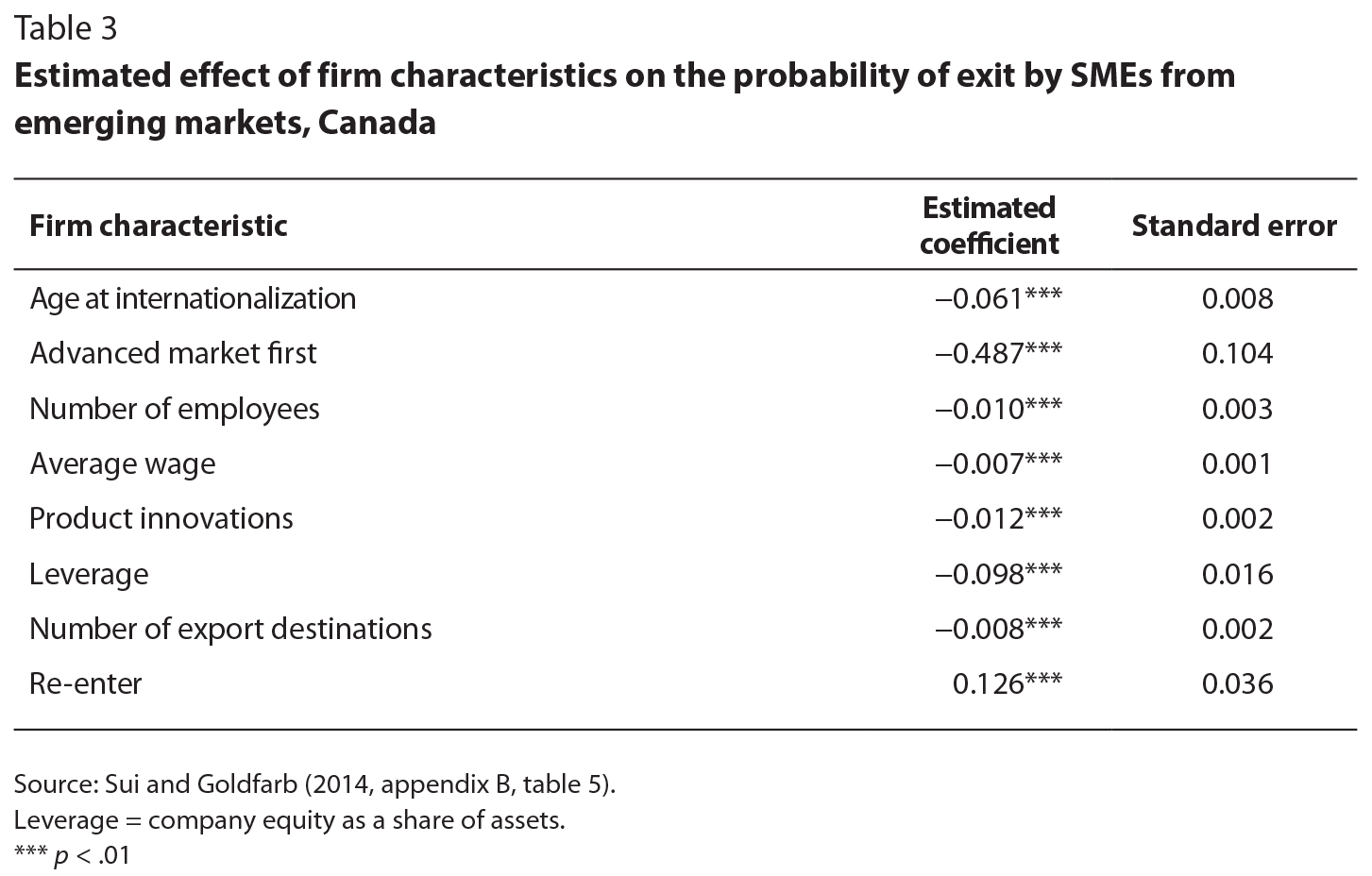

Sui and Goldfarb’s (2014) results highlight the importance of prior experience as well as on-going innovation for export survival. Specifically, they find that Canadian SME exporters generally had a better chance of surviving in emerging markets if they were older when they entered (that is, if they had spent more time operating in the domestic market before exporting), had exported to an advanced economy first (consistent with the gradual exporting approach), were larger (had more employees), paid higher average wages (an indicator of a more productive firm with higher-skilled employees), were more innovative (that is, if they introduced new products more often into emerging markets), had more access to external financing (leverage) and exported to more destinations (table 3).

Recent immigrants possess many vital skills that might help Canadian exporters tap into nontraditional markets, including language skills, social networks and knowledge of local cultural and business practices.17 Sui and Morgan (2014) find that SMEs whose majority owner is a recent immigrant were more than twice as likely as other firms to export to non-US markets. The authors note that this is a rather small group to draw from, representing only about 3 percent of all Canadian SMEs. Moreover, SME exporters owned by recent immigrants were generally less profitable than other exporters, perhaps relating to the industrial composition of the former’s exports: recent-immigrant-owned-exporters are more active in sectors such as wholesale and retail trade, which, as we have seen, tend to generate less export revenue on average.

Building on the finding that sharing a common language often promotes trade relationships (see, for example, Anderson and van Wincoop 2004), Sui, Morgan and Baum (2015) confirm that language influences firms’ internationalization strategies. After controlling for other factors, SMEs owned by recent -immigrants were more likely to export to non-US markets, particularly when the owners’ mother tongue was not English.

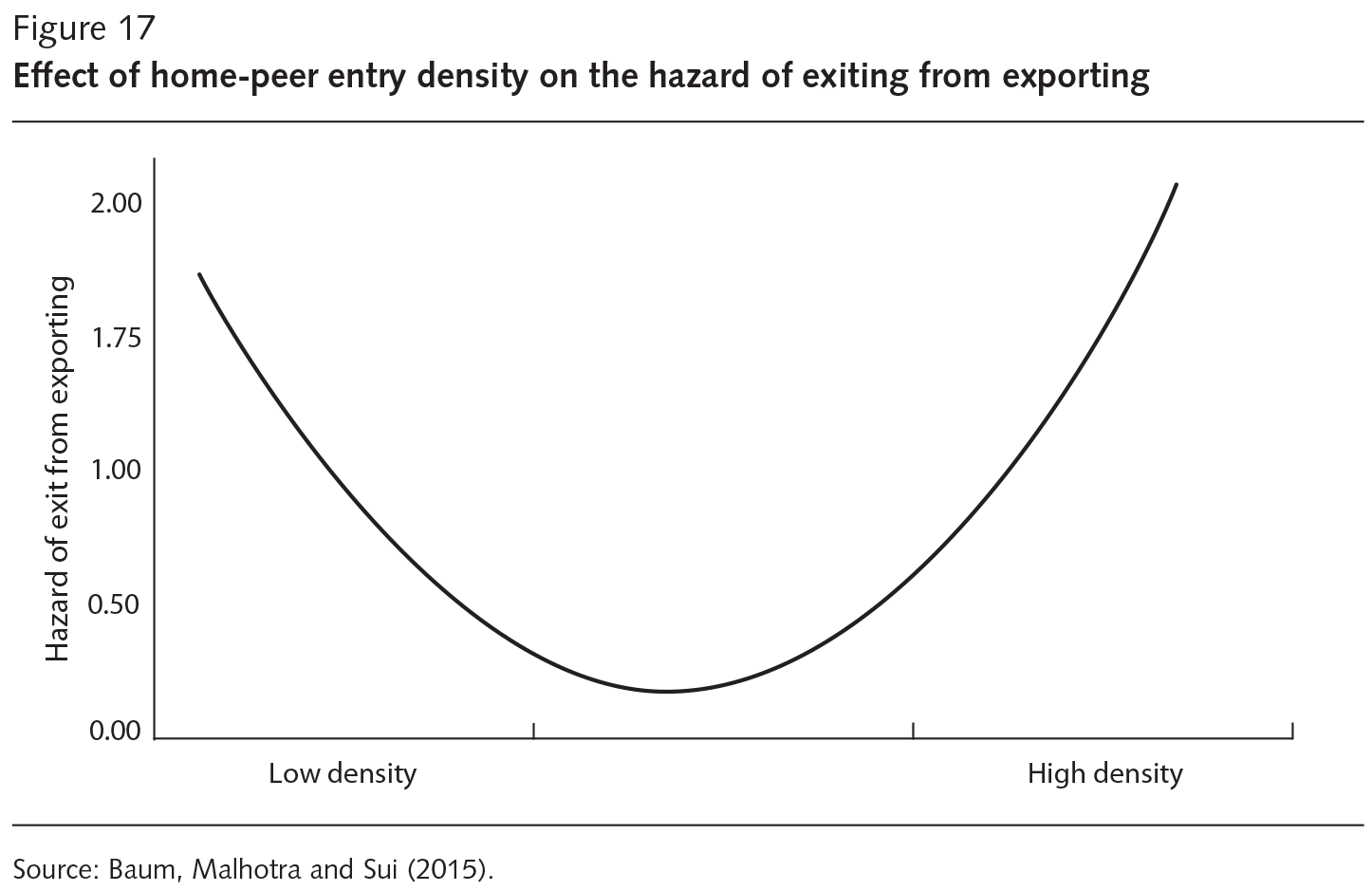

Recent research by Sui, Baum and Malhotra (2015) complements the findings that specific firm characteristics influence internationalization strategies. The authors examine so-called home-peer entry density — that is, whether the number of other domestic firms in the same industry that export to the same foreign market when the firm starts exporting there — affects firms’ survival in that market. Consider the case of Canadian firms trying to export ice wine to China. This attempt might be particularly risky for the first few firms that try to break into the market with little brand awareness. At first, the entry of other Canadian ice wines might help the chances of survival of similar Canadian brands. If too many enter, however, the Chinese market eventually might become crowded with Canadian ice wines, and this tougher competition for market share might make it harder to distinguish among specific products, and thus for their makers to survive in the new market. Indeed, Sui, Baum and Malhotra (2015) find a U-shaped relationship between the probability that a Canadian SME will leave an export market and home-peer entry density, controlling for firms’ characteristics and competition from all other countries.

This work highlights two competing effects from the entry of new firms into the foreign market. For the first few firms to enter, the likelihood of exit is high. Initially, as other firms enter (moving to the right in figure 17), this might help “grant legitimacy” and build awareness of the Canadian brand in the new market, which lowers the likelihood that Canadian firms will leave the market. At a certain point, however — when sufficient numbers have entered to establish awareness of the Canadian brand — a “competition effect” takes over, and more firms entering increases the chances of leaving. Interestingly, Sui, Baum and Malhotra (2015) find that the firm’s age at entry affects the strength of peer-firm effects, and that younger Canadian SME exporters are more responsive. On the plus side, the younger firms benefit more by being among the first to introduce their products, but they are also hurt more by the increased competition of additional firms.

Unfortunately for policy-makers, there is little direct evidence to guide the role that Canadian government policy should play to encourage exports. Van Biesebroeck, Yu and Chen (2015) is one important recent contribution that examines the effectiveness of Canada’s Trade Commissioner Services (TCS), which include “information provision” — for instance, on market prospects, local companies, key contacts and face-to-face briefings — and “troubleshooting” services — such as solving problems with customs clearance or unfair business treatment. Interestingly, only about 5 percent of Canadian exporters use TCS, and these clients have certain characteristics. Relative to exporters who do not use TCS, these firms tend to export more and to export multiple products to multiple destinations beyond the United States, and their export performance often deteriorates before they seek government help.

In a careful econometric analysis, the authors find that the Trade Commissioner Services were effective in increasing exports for client firms, with a positive, one-time boost of about 10 percent in export values. It is important to note that this study does not evaluate whether the services helped firms become first-time exporters. Rather, it examines the impact of these services for existing exporters, and finds that the services helped existing exporters to raise sales of products they were already selling in destination markets that they already served (the so-called intensive margin of trade), and that trouble-shooting was more effective than information provision services. (It is likely the case that, for first-time exporters, the information provision role would be more important.) The positive effects of TCS were larger for older, more experienced firms. Moreover, the duration of government support also influenced its effectiveness, as exports increased more for firms that received sustained support over several years.18

On an encouraging note, Canadian exports have reached increasingly -diversified markets over the past decade and a half, with the share of total exports destined for emerging markets rising from around 4 percent in 2001 to around 10 percent in 2014. Moreover, SMEs increasingly have chosen emerging markets as their first export destination. Despite these shifting trade patterns, however, the United States remains Canada’s largest export market by a wide margin.

SME trade differs systematically from the trade of large firms in several ways. Although there are many more SMEs than large firms exporting, they are far less likely to export than large firms, their average export revenues are much lower, they reach fewer markets (often only the United States) and their activities are more concentrated in industries with lower export revenues. The bad news, then, is that SME trade is much less productive, on average, than trade by large firms. The silver lining is that SME trade is naturally more inclusive, with many more participants and much more dispersed market outcomes — features that help explain the strong political appeal of targeting policy support to SMEs.

Exporting has long been associated with better firm performance, and Canadian SMEs that exported to emerging markets performed slightly better on average than those that exported to other destinations. Unfortunately, in seeking the larger rewards in these markets, Canadian firms may incur higher risks and higher entry costs.

Are there ways to improve the chances of success in these markets? The evidence shows that Canadian SME exporters generally have better chances of surviving in emerging markets if they are older when they enter, export to an advanced economy first, are larger, are more productive, introduce new products more often, have better access to external financing and export to more destinations. Clearly, there is scope to encourage and assist high-potential SMEs with these particular characteristics in their efforts to expand into emerging markets — and to help firms acquire these characteristics. Less experienced or less competitive SMEs should not be pushed into emerging markets too soon. Often, a gradual export strategy is more appropriate, focusing first on the local or regional market, while building up capabilities, resources and knowledge before trying to expand into riskier emerging markets, if at all.

At the same time, an alternative path is being followed by a small, but growing proportion of Canadian firms that are “born global,” serving emerging markets in their first few years of operations. There is also preliminary evidence of the emergence of smaller, services-based firms in the high-tech sector that are making progress exporting into Asian markets. This is consistent with the findings of Ahmed and Melin (in this volume) that technology-enabled small businesses export into far more markets than do traditional exporters.

Some government policies appear to have played a supportive role in increasing Canadian exports — at least for existing exporters, though their effectiveness in helping first-time exporters is still unknown. Those designing government support programs could benefit from having additional robust empirical evidence on what support works best (not only for the Trade Commissioner Services, but also for other programs),19 for which types of Canadian firms and in which markets.

It seems clear that government has important roles to play as both “trouble shooter” to help address problems for existing exporters and as “information -provider” to survey market conditions. In so doing, it could help potential entrants reduce their risks and learn more, and more quickly, about their chances of success in a given market. In fact, without government intervention, the private sector will generally collect insufficient market information because of the “free rider” problem, whereby firms are reluctant to collect information themselves due to worries that their potential competitors could “free ride” on their initiative by soon after exporting similar products to the same market.20

Government information should be tailored to the needs of firms, particularly those that are younger and smaller, that generally need more external assistance and that also might be more receptive to implementing the information and process changes needed to succeed in emerging markets. Given the surprisingly low take-up of government supports in Canada among exporters (only about 5 percent), policy-makers should continue their efforts to increase awareness of existing programs and design them better to the needs of SMEs (as Mallett, in this volume, suggests). “Go Global” workshops for SMEs introduced in 2014 are an example of efforts to increase the visibility and use of government programs; although firms likely cannot explore all of the relevant information in a single session, these interactions can be a useful start to the learning process.21

Another important and complementary role for government, as suggested by the firm-level trade literature, is to lower the costs for Canadian firms to enter emerging markets. This could be done, for instance, by negotiating free trade agreements with these countries, which would directly lower tariffs and generally improve market access. Here, the recently concluded Trans-Pacific Partnership (TPP) could play a supportive role;22 bilateral negotiations with the largest emerging markets (China and India) could also help — on China, see Wolfe, in this volume, and Dobson and Evans (2015); on India, see Rao and Tapp (2015).

Much like trade deals, foreign investment agreements could also offer similar benefits. Most Canadian export revenues come from firms that export to multiple destinations at the same time. These firms tend to be the largest and most productive and to have multiple establishments and more diversified products. They are also more likely to be foreign-controlled, which suggests that complementarities might well exist between increasing inward FDI in Canada and boosting Canadian exports abroad.

Applying additional policy scrutiny and questioning conventional wisdom can often be a good thing. Some strategies might sound good in theory, but -further empirical investigation could reveal important limitations. For instance, most analysts would support the idea of leveraging the skills of recent immigrants from emerging markets, since this group is already more likely to export to these markets and to have the necessary language skills and social networks. Unfortunately, there are limits to this approach because these entrepreneurs are relatively few in number and their firms tend to be less productive than other Canadian exporters on average.

Finally, trade policy discussions in Canada should not simply focus -narrowly on how to increase SME exports to emerging markets, but take a broader view. This approach could start by acknowledging that exporting directly to emerging markets is not the only way for SMEs to seize the benefits of growth in those markets. Other strategies might provide similar benefits with less risk — for example, helping SMEs build up their resources and capabilities in Canada or in less challenging foreign markets first, with a long-term goal of getting into emerging markets. Canadian SMEs also could participate effectively in global supply chains by selling intermediate goods or services to multinationals based in Canada or the United States that are active in emerging markets. Taking part in international joint ventures, or franchising or licensing arrangements also could be a promising initial way for many firms to gain market entry. Gaining a better knowledge of these types of activities and of the importing behaviour of Canadian SMEs remain promising avenues for future research.

In this chapter, and following the definition used by Innovation, Science and Economic Development Canada, SMEs are classified as firms with 500 or fewer employees. Sui and Yu (2012), Sui and Yu (2013), and Sui and Baum (2014) construct a unique longitudinal (1997-2004) dataset by linking Statistics Canada’s Exporter Register (1993-2005), Business Register (1993-2005) and Longitudinal Employment Analysis Program (LEAP) (1997-2004). This dataset includes all Canadian exporters that had at least one shipment to a foreign market between 1993 and 2005.

The Exporter Register, the main source, is an authoritative, customs-based database that includes all officially registered Canadian merchandise trade transactions. These data are obtained from the Canada Revenue Agency and US customs documents. The Exporter Register allows one to track the year a firm started exporting, the value of its exports, the products it exported each year and the destinations of those exports. The Business Register includes all active businesses in Canada that have corporate income tax accounts, are employers or have goods and services tax accounts. The Business Register provides annual information on each firm’s revenue and ownership (over the 1997-2005 period). The third data source, the LEAP, provides annual information on firms’ employment (1997-2004) and includes all firms incorporated in Canada that legally hire employees.

The dataset used in Sui and Goldfarb (2014), Sui and Morgan (2014) and Sui, Baum and Malhotra (2015) was constructed by Statistics Canada’s Centre for Data Development and Economic Research by linking the Exporter Register (1993-2008) and T2-LEAP (1993-2008). This dataset includes all incorporated Canadian firms that legally hired employees or filed a corporate income tax return in at least one year between 1993 and 2008, and is the most authoritative and best suited to study the behaviour of SMEs. T2 LEAP was created by merging two administrative databases: (1) the LEAP, which provides information on the firm’s employment, wages, industry and location; and (2) the Corporate Tax Statistical Universe File (T2SUF), which provides information on the firm’s sales, assets and equity.

It is important to emphasize that all of the above studies exclude firms that were established before 1994 — which therefore excludes some older, more established Canadian exporters — because important variables of interest in these studies, such as the firm’s first export destination, its age at internationalization, its initial size and so on, were unavailable for firms established before that date.

We thank the editors and Loretta Fung for helpful comments and suggestions. Colin Chia and David Deault-Picard provided excellent research assistance.

Anderson, J., and E. van Wincoop. 2004. “Trade Costs.” Journal of Economic Literature 42 (3): 691-751.

Albornoz, F., H. Calvo Pardo, G. Corcos, and E. Ornelas. 2012. “Sequential Exporting.” Journal of International Economics 88 (1): 17-31.

Arenius, P. 2005. “The Psychic Distance Postulate Revised: From Market Selection to Speed of Market Penetration.” Journal of International Entrepreneurship 3 (2): 115-31.

Bank of Canada. 2013. “Global Growth and the Prospects for Canada’s Exports.” Remarks by Tiff Macklem, Senior Deputy Governor, to the Economic Club of Canada in Toronto, October 1. Accessed October 4, 2016. https://www.bankofcanada.ca/wp-content/uploads/2013/10/remarks-011013.pdf

Benito, G.R.G., and G. Gripsrud. 1992. “The Expansion of Foreign Direct Investments: Discrete Rational Location Choices or a Cultural Learning Process.” Journal of International Business Studies 23 (3): 461-76.

Blomstermo, A., K. Eriksson, and D.D. Sharma. 2004. “Domestic Activity and Knowledge Development in the Internationalization Process of Firms.” Journal of International Entrepreneurship 2 (3): 239-58.

Bruneel, J., H. Yli-Renko, and B. Clarysse. 2010. “Learning from Experience and Learning from Others: How congenital and Interorganizational Learning Substitute for Experiential Learning in Young Firm Internationalization.” Strategic Entrepreneurship Journal 4 (2): 164-82.

Burt, M. 2009. “Tighter Border Security and Its Effect on Canadian Exports.” Canadian Public Policy 35 (2): 149-69.

Canada. 2013. Global Markets Action Plan: The Blueprint for Creating Jobs and Opportunities for Canadians through Trade. Accessed June 19, 2016. https://international.gc.ca/global-markets-marches-mondiaux/assets/pdfs/plan-eng.pdf

De Clercq, D., H.J. Sapienza, R.I. Yavuz, and L. Zhou. 2012. “Learning and Knowledge in Early Internationalization Research: Past Accomplishments and Future Directions.” Journal of Business Venturing 27 (1): 143-65.

Dobson, W., and P. Evans. 2015. The Future of Canada’s Relationship with China. IRPP Policy Horizons Essay. Montreal: Institute for Research on Public Policy.

Eaton, J., M. Eslava, M. Kugler, and J. Tybout. 2008. “The Margins of Entry into Export Markets: Evidence from Colombia.” In The Organization of Firms in a Global Economy, edited by E. Helpman, D. Marin, and T. Verdier. Cambridge, MA: Harvard University Press.

Evans, W., H. Lane, and S. O’Grady. 1992. Border Crossings: Doing Business in the United States. Scarborough, ON: Prentice Hall Canada.

Fan, T., and P. Phan. 2007. “International New Ventures: Revisiting the Influences behind the ‘Born-Global’ Firm.” Journal of International Business Studies 38 (7): 1113-31.

Ferris, J.S. 2010. “Quantifying Non-Tariff Trade Barriers: What Difference Did 9/11 Make to Canadian Cross-Border Shopping?” Canadian Public Policy 36 (4); 487-501.

Globerman, S., and P. Storer. 2009. “Border Security and Canadian Exports to the United States: Evidence and Policy Implications.” Canadian Public Policy 35 (2): 171-86.

Head, K. 2007. “Engage the US, Forget the Rest? Comments.” In A Canadian Priorities Agenda: Policies to Improve Economic and Social Well-Being. Montreal and Kingston: McGill-Queen’s University Press.

Horton, D. 2016. “Big Data, Small World: Keep Calm and Go Global.” Presentation to “Trading at the Speed of Light,” Canadian Chamber of Commerce conference, May 19, Toronto.

Industry Canada. 2011. Small Business Branch. Canadian Small Business Exporters. Special Edition: Key Small Business Statistics, June. Accessed October 4, 2016. https://www.ic.gc.ca/eic/site/061.nsf/vwapj/KSBS-PSRPE_June-Juin2011_eng.pdf/$FILE/KSBS-PSRPE_June-Juin2011_eng.pdf

Industry Canada. 2015. SME Profile: Canadian Exports, January. Accessed October 4, 2016. https://www.ic.gc.ca/eic/site/061.nsf/vwapj/SMEPCE-PPMEEC_2015_eng.pdf/$file/SMEPCE-PPMEEC_2015_eng.pdf

Johanson, J., and J.E. Vahlne. 1977. “The Internationalization Process of the Firm: A Model of Knowledge Development and Increasing Foreign Market Commitment.” Journal of International Business Studies 4 (1): 20-9.

Johanson, J., and J. E. Vahlne. 1990. “The Mechanism of Internationalisation.” International Marketing Review 7 (4): 11-24.

Knight, G.A., and S.T. Cavusgil. 1996. “The Born Global Firm: A Challenge to Traditional Internationalization Theory.” In Advances in International Marketing, vol. 8, edited by S.T. Cavusgil and T. Madsen. Greenwich, CT: JAI Press.

Melitz, M.J. 2003. “The Impact of Trade on Intra-industry Reallocations and Aggregate Industry Productivity.” Econometrica 71 (6): 1695-725.

Mitchell, W., J.M. Shaver, and B. Yeung. 1994. “Foreign Entrant Survival and Foreign Market Share: Canadian Companies’ Experience in the United States Medical Sector Markets.” Strategic Management Journal 15 (7): 555-67.

Oviatt, B.M., and P.P. McDougall. 1994. “Toward a Theory of International New Ventures.” Journal of International Business Studies 24: 45-64.

Rao, S., and S. Tapp. 2015. The Potential to Grow Canada-India Economic Linkages: Overlooked or Oversold? IRPP Study 53. Montreal: Institute for Research on Public Policy.

Santangelo, G., and K.E. Meyer. 2011. “Extending the Internationalization Process Model: Increases and Decreases of MNE Commitment in Emerging Economies.” Journal of International Business Studies 42 (6): 894-909.

Sapienza, H.J., D. De Clercq, and W.R. Sandberg. 2005. “Antecedents of International and Domestic Learning Effort.” Journal of Business Venturing 20 (4): 437-57.

Sui, S., and M. Baum. 2014. “Internationalization Strategy, Firm Resources and the Survival of SMEs in the Export Market.” Journal of International Business Studies, 45: 821-41.

Sui, S., M. Baum, and S. Malhotra. 2015. “The Influence of Entry Density on the Survivability of SMEs in International Markets.” Academy of Management Proceedings (1), 11401.

Sui, S., and D. Goldfarb. 2014. Not for Beginners: Should SMEs Go to Fast-Growth Markets? Publication 5936. Ottawa: Global Commerce Centre, Conference Board of Canada.

Sui, S., and H. Morgan. 2014. Selling Beyond the US: Do Recent Immigrants Advance Canada’s Export Promotion Agenda? Briefing.Ottawa: Conference Board of Canada.

Sui, S., H. Morgan, and M. Baum. 2015. “Internationalization of Immigrant-Owned SMEs: The Role of Language.” Journal of World Business 50 (4): 804-14.

Sui, S., and Z. Yu. 2012. “The Pattern of Foreign Market Entry of Canadian Exporters.” Canadian Public Policy 38 (3): 341-59.

Sui, S., and Z. Yu. 2013. “The Dynamics of Expansion to Emerging Markets: Evidence from Canadian Exporters.” Review of Development Economics 17 (3): 510-22.

Sui, S., Z. Yu, and M. Baum. 2013. “Resource Differences between Born Global and Born Regional Firms: Evidence from Canadian Small and Medium-Sized Manufacturers 1997-2004.” International Business: Research, Teaching and Practice 7 (1): 57-73.

Trudeau, J. 2015. “Minister of International Trade Mandate Letter.” Accessed October 4, 2016. https://pm.gc.ca/eng/minister-international-trade-mandate-letter

Van Biesebroeck, J., E. Yu, and S. Chen. 2015. “The Impact of Trade Promotion Services on Canadian Exporter Performance.” Canadian Journal of Economics 48 (4): 1481-512.