Le système canadien de soins de longue durée (SLD) est confronté à d’énormes défis qui devraient s’aggraver dans les années à venir. Au cours des deux prochaines décennies, le nombre de Canadiens âgés de plus de 85 ans devrait augmenter de 145 %. L’Association médicale canadienne prévoit que le coût des SLD et des soins à domicile atteindra 58,5 milliards de dollars d’ici à 2031, soit près du double de ce qu’il était en 2019.

Même aujourd’hui, alors que les conséquences du vieillissement de la population ne se sont pas encore pleinement montrées, le système ne fonctionne pas bien. Les listes d’attente pour accéder aux établissements de SLD sont longues dans tout le pays. La qualité des soins fournis laisse beaucoup à désirer, comme on l’a douloureusement constaté au début de la pandémie de COVID-19. Les soins à domicile financés par l’État sont difficiles d’accès, mais les soins à domicile fournis par le secteur privé sont coûteux. Le système repose en grande partie sur les conjoints, les enfants adultes et les autres aidants, qui déclarent fournir de longues heures de soins non rémunérés et se sentir fatigués et à bout de ressources.

Cette situation place les Canadiens devant trois choix : augmenter les impôts et réduire les dépenses pour financer l’amélioration de la qualité des SLD tout en répondant à la demande croissante ; maintenir les niveaux de financement actuels et assister au coût humain du déclin des soins ; générer de nouvelles sources de revenus en s’inspirant des modèles de financement à long terme utilisés ailleurs.

Cette étude se concentre sur la troisième option. Elle évalue le financement et la répartition des soins de longue durée au Canada par rapport à plusieurs approches internationales. Contrairement aux idées reçues, une grande partie du système canadien de SLD est financée par le secteur privé, sous la forme de soins non rémunérés dispensés par des membres de la famille, de services de soins personnels et d’aide ménagère achetés auprès du secteur privé et de résidences avec service de soutien financés par le secteur privé. Les services financés par l’État sont étroitement rationnés et la quantité disponible est loin de répondre aux besoins en matière de soins.

Cette étude énonce cinq principes pour guider la future réforme du financement des SLD : l’équité, la neutralité, la transparence, le partage des risques et l’adéquation. Les aspects du financement liés à l’équité sont souvent ignorés et pourtant cruciaux. Les choix des gouvernements ont des conséquences sur les inégalités entre les hommes et les femmes, sur les écarts de revenus et de richesse, ainsi que sur l’équité intergénérationnelle.

Ces principes sont utilisés pour évaluer les mérites et les inconvénients de plusieurs approches de financement des SLD adoptées à l’international : assurance nationale des soins de longue durée, facture partagé des soins résidentiels et contributions aux coûts des soins de longue durée basées sur la richesse.

L’analyse fournit des informations importantes qui peuvent éclairer les perspectives fédérales, provinciales et territoriales sur la loi fédérale sur la sécurité des soins de longue durée et l’allocation Vieillir chez soi, ainsi que les délibérations futures sur les paiements de transfert fédéraux.

L’étude formule trois recommandations :

Le Canada est confronté à une crise du financement des SLD. Mais cette crise est aussi une opportunité. Les pressions que le vieillissement de la population exercera sur un système public qui se détériore progressivement et qui est de plus en plus sous-financé pourraient être l’étincelle nécessaire à une réforme substantielle. Nous avons aujourd’hui l’occasion, une fois par génération, d’apporter des changements substantiels au financement des soins de longue durée, afin d’obtenir des résultats plus équitables.

Il est temps d’abandonner l’idée que nous pouvons bénéficier de meilleurs soins tout en payant moins. La réforme du financement doit faire partie de toute stratégie en matière de soins de longue durée.

As the baby boomer generation enters its senior years, long-term care faces enormous financing challenges. The Financial Accountability Office of Ontario (2023) predicts that long-term care (LTC) spending in the province will grow 10 per cent per year over the next five years, the highest growth rate of any component of health care. The Canadian Medical Association (2021) estimates that the cost of providing long-term and home care will nearly double between 2019 and 2031, to $58.5 billion from approximately $29.7 billion. Drummond et al. (2020) predict that the “1.3 percent of GDP spent on LTC [in 2017] will surge to 4.2 percent by 2041” — an increase equivalent to 2.9 per cent of GDP.

These costs are inevitable and unavoidable. Over the next two decades, the absolute number of Canadians over the age of 85 is projected to grow by 145 per cent. The percentage of Canada’s population aged 85 or older will double.[1] Although life expectancies have increased, the portion of people’s lives spent in poor health with mobility problems and pain has not changed. While Canadian women’s life expectancy reached 83.9 years in 2015, the last 13.4 years of their lives are typically spent in fair to poor health. Men live shorter lives on average than women do — 79.8 years — but their healthy life expectancy is not much less than women’s: 69 years versus 70.5 years, respectively (Bushnik et al., 2018). Moreover, the elderly will have fewer close family members available to provide care because of declining fertility rates, increased geographic mobility (Estabrooks et al., 2020), and an increase in the percentage of older Canadians who are single due to a decades-long decline in marriage and cohabitation rates.[2] These factors are all placing, and will continue to place, increased pressure on LTC systems. As a recent report for the Royal Society of Canada argues, “Canada has failed to confront present and future financing of LTC” (Estabrooks et al., 2020, p. 12).

Canadians have three choices. One is to realign fiscal priorities and make major tax hikes or spending cuts. For example, the spending increase projected by Drummond et al. (2020) could be financed by doubling GST revenues as a percentage of GDP. This would require at least a doubling of the GST rate because higher tax rates tend to be associated with more tax avoidance (Finances of the Nation, n.d.).[3]

The second option is to maintain the current level of public LTC funding and live with the consequences: let LTC waiting lists grow and those in need of care and their families fill the gaps in funding however they can. Arguably, Canadian governments have been pursuing this course of action for some time, and its human cost became painfully obvious during the COVID-19 pandemic (Estabrooks et al., 2020).

A third option is to reconsider the allocation of scarce LTC resources and public funding priorities. Part of this may involve shifting the balance between the portion of funding that is covered by governments and that which is covered privately by those receiving care and their families, and part may involve introducing new funding sources and forms of revenue in an equitable and sustainable manner.

This paper explores the third option. It sets out a series of principles to guide LTC financing. It then examines three approaches adopted internationally: national long-term care insurance, co-payments for residential care and wealth-based contributions to LTC costs.

There are valuable lessons to be learned from the experiences of other countries, and I argue that three approaches are particularly worth considering: greater transparency, portability and standardization of public support for LTC costs; changes in the balance between public and private financing of specific types of LTC expenditures; and a more comprehensive assessment of an individual’s ability to contribute to the costs of their care, which would include both income and assets in ability-to-contribute calculations.

The Organization for Economic Co-operation and Development (OECD, n.d.) defines long-term care as day-to-day help with activities such as washing and dressing, help with household activities such as cleaning and cooking, and supportive medical care. Whether a service is considered LTC depends on the characteristics of the recipient: services become LTC when they are “provided to people who are unable to perform basic activities of daily living such as dressing or bathing” (HealthCare.gov, n.d.). Although most recipients are older adults, people of all ages with long-term, ongoing mental or physical challenges may need LTC.[4]

In Canada, long-term care is provided in various settings: people’s homes, government-funded facilities, private retirement residences offering assisted-living services and hospitals. In each of these settings, people receive three basic types of care: personal care (e.g., assistance with bathing and dressing), homemaking services (assistance with cooking and laundry), and professional services (nursing care, physiotherapy and social work visits). These services can be provided by (unpaid) family and friends, by public-sector employees, by non-profit organizations, or by private, for-profit care providers.

As people age, they typically use several LTC services, sometimes at the same time. For example, a person living at home may receive unpaid care from a family member and publicly funded community nursing care and perhaps may pay for a private cleaning service. This care might be co-ordinated by a (paid) social worker or an (unpaid) family member. A person living in a private retirement residence offering assisted-living services might also receive publicly funded home care visits. In a publicly funded long-term care home, family members may visit daily and help with personal care such as shaving and feeding, or a personal support worker may provide additional care.

This study focuses on how these various LTC services are financed and allocated, and how LTC costs are shared between the recipients of LTC services and governments. Public financing of LTC is not the same as public provision. For example, as of 2021, just over half of Canada’s publicly funded LTC homes — 54 per cent — were privately owned and operated (Canadian Institute for Health Information [CIHI], 2021). However, these privately operated LTC homes are partly publicly funded; that is, the costs of patient nursing care are covered by grants from provincial, territorial, local or other governments. Conversely, in government-owned LTC homes, residents are generally expected to pay for some or all the costs of their accommodation (as distinct from their nursing and personal care). Although the provision of housekeeping and accommodation services in this case is public (i.e., through a government-owned and managed LTC home), the financing is private.[5]

A discussion of whether LTC services are best provided publicly or privately is beyond the scope of this study. The focus here is on who pays for the services. To better understand the nuances of LTC financing and resource allocation — and why reform is needed — it is necessary to take step back and consider how LTC is organized in Canada.

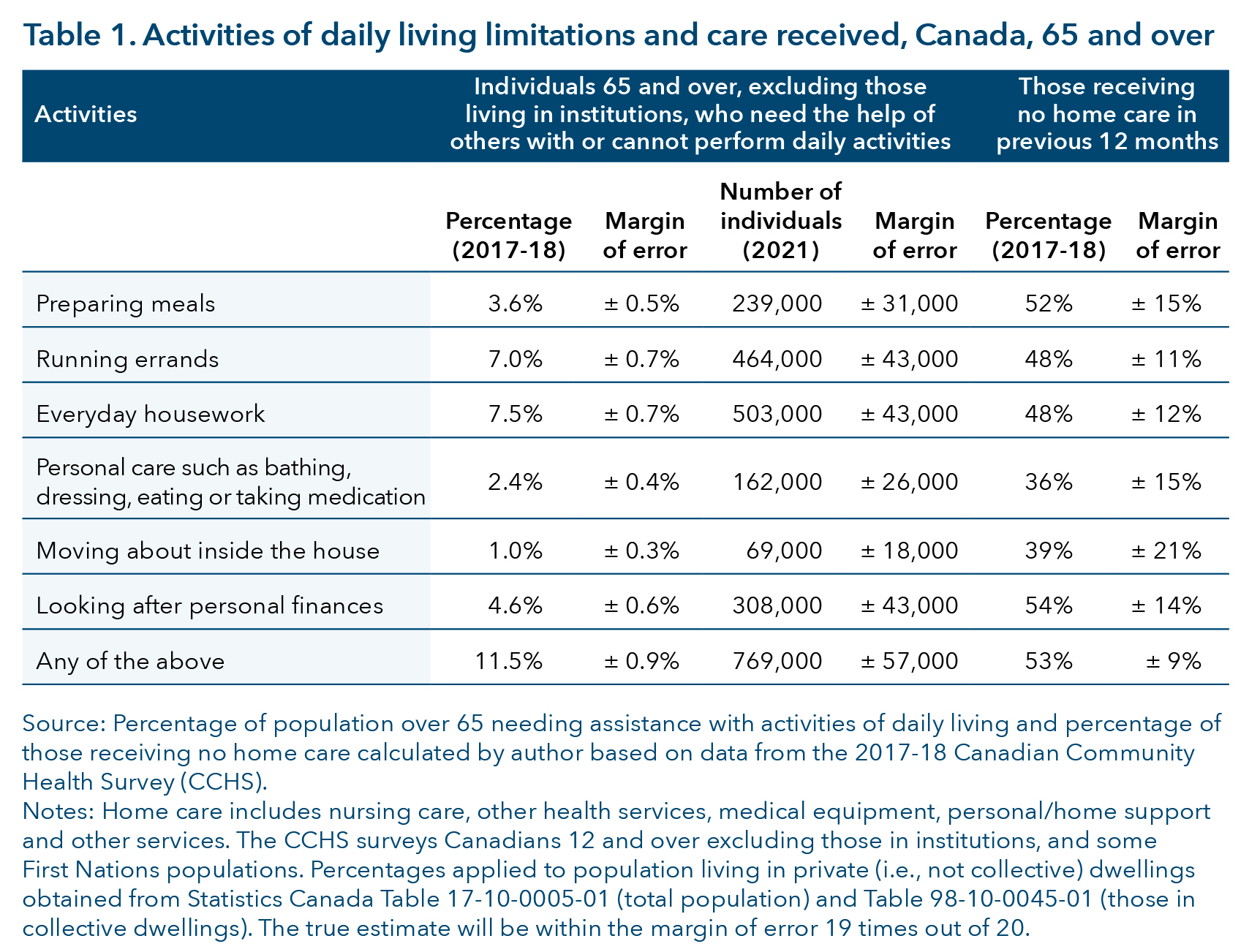

Typically, people begin their long-term care journey while living in their own homes. In 2017-18, 11.5 per cent of Canadians over 65 living in their own homes needed the help of others to perform at least one activity of daily living, such as looking after personal finances or preparing meals; 2.4 per cent (about 162,000 people) could not perform basic personal care such as bathing, dressing, eating or taking medication without assistance (see table 1).[6]

A substantial number of people who need assistance receive no home care; that is, they did not receive home nursing care or other health services, medical equipment or personal/home support in the previous 12 months. According to my calculations using Canadian Community Health Survey data, approximately one-third of those needing assistance to perform basic personal care activities, such as bathing, dressing, eating or taking medication, in 2017-18 did not receive home care (except assistance from friends and family). If we consider individuals who have any care needs, including those who need help with personal finances or meal preparation, the portion receiving no home care rises to 50 per cent.[7]

The care needs of people requiring assistance are typically met by family, friends or community services. More than 33 per cent of 55 to 64-year-olds and 23.5 per cent of those 65 plus provided unpaid care to a care-dependent adult in 2022 (Statistics Canada, 2022). Indeed, in many provinces, there is an expectation that government-financed home care is a last resort, a service to be accessed only when family members are not able to provide support themselves. The government of Saskatchewan (2022), for example, specifies that home care services “do not replace the assistance usually provided by the family or community.” In Manitoba, a person is only eligible for home care services if they “require more assistance than what is available from existing or potential supports” (Manitoba Government, n.d., p. 2). In almost all cases, there is an expectation that this family-provided care will be unpaid. In Nova Scotia and Newfoundland and Labrador, those needing home care can access funds that can be used to hire family members (although in Newfoundland and Labrador the program excludes spouses and common-law partners) (Flood et al., 2021; Newfoundland and Labrador Government, n.d.-a). However, most other provinces do not allow this.

The coverage gaps exist because home care in Canada is not an entitlement. There are no formal maximum and minimum levels of home care available and no guarantee that a certain level of disability will be associated with a guaranteed level of support. The level of home care provided is typically determined by a case manager. Case managers may be given guidelines that dictate how much care to assign in each case, but these are generally not publicly available. Moreover, the number of hours of funded home care are constrained. Thus, home care services are rationed: there is a set envelope, and when the envelope for the fiscal year is used, there is nothing more available. Case managers must manage what they know falls far short of need. One indication of the amount of home care typically provided comes from British Columbia’s Office of the Seniors Advocate (2022), which reported that in 2021-22 the average hours of home care was 250 hours per client per year. A recent study from the Office of the Seniors Advocate (2023, p. 3) reported that “most home support clients do not receive daily service and most receive an hour or less of service on the days they do receive it.”

It is also worth noting that most provinces expect care recipients to cover at least part of the cost of homemaking services and, in some cases, personal care services. For example, in British Columbia there is an income-based charge for home support providing assistance for activities such as bathing, dressing, grooming and toileting (British Columbia Government, n.d.). Given the challenges associated with accessing home care, it is not surprising that family caregivers, and especially caregiving spouses, find themselves putting in many hours of care per week — 20 hours per week for the typical person providing care to a spouse — and many caregivers report feeling tired, anxious or overwhelmed (Statistics Canada, 2022). According to data from the Canadian Institute for Health Information (CIHI, n.d.-a), in 2021, 37.4 per cent of unpaid caregivers — people providing unpaid care to someone receiving home care services — were distressed. In Ontario, the percentage of unpaid caregivers in distress reached 42.2 per cent.

Federal and provincial tax credits are available to support caregivers. However, they are of limited significance in the LTC landscape. First, the take-up rate for these credits is low. The most extreme examples are the disability supports deduction and the Home Accessibility Tax Credit, which was claimed by an estimated 0.2 per cent of people with disabilities in 2017.[8] Second, tax credits do not vary with the extent of a person’s disability or the nature of a caregiver’s responsibilities. For example, a person with Type 1 diabetes and a person with advanced dementia receive the same benefits through the federal Disability Tax Credit. Third, even the most generous tax credits do not amount to much money. For example, Quebec’s caregiver credit can be worth up to $2,598 per year (Revenu Québec, n.d.). To put this number into perspective, for someone providing 40 hours per week of care to a spouse — roughly the level of care provided by the typical caregiver experiencing distress[9] — Quebec’s caregiver credit works out to an hourly wage of $1.25. If the credit is used to buy private home care at $25 per hour, it would pay for about two hours of care per week.

Tax credits for caregiving are valuable as a way of improving the equity of the income tax system. They offset some of the costs of caregiving, especially for people with moderate care needs. However, for those with more serious needs — those needing dementia care, for example — federal and provincial tax credits are small relative to the cost of care. The one exception is the Medical Expenses Tax Credit, which can offset up to 20 to 25 per cent of the cost of privately financed personal and nursing home care, depending on a person’s income level and the provincial tax rate.

Aging begins at home but does not typically end there. Older adults tend to remain in their homes until there is a crisis and their families are unable to cope. At this point, a person in need of care should be able to transfer into a publicly financed long-term care home — at least in theory. Once in an LTC facility, they should be able to access publicly financed personal care, with no charge to the care recipient. Residents of publicly funded long-term care institutions are expected to pay a monthly charge that is intended to cover their accommodation (room, board and housekeeping costs), plus the costs of special services.

As of 2022-23, the maximum amount an LTC resident paid in accommodation costs varied from $1,214 per month for a shared room in Manitoba to $3,847.20 for a private room in British Columbia. These charges are income tested. Generally, residents are expected to use most or all their net after-tax income to pay for their LTC accommodation costs (except for a small amount retained for their own use) until they are paying the maximum amount. Only Quebec includes assets in the ability-to-pay calculation; in other provinces, the contribution is based solely on net income, as reported on the previous year’s income tax return.

The bulk of government LTC funding goes to (publicly funded) LTC homes. Residents’ contributions in the form of accommodation, housekeeping and similar charges cover about 25 per cent of the cost of running publicly funded LTC homes. The rest is paid for through government grants. The level of government funding for ongoing patient care and the volume of grants available to support LTC homes’ capital costs varies from province to province, and within provinces it may depend upon the type of LTC facility. Overall, the system is, in the words of the 2020 Royal Society of Canada report, “woefully inadequate” (Estabrooks et al., 2020, pp. 27-28). One indicator of this is the gap between the number of publicly financed LTC beds available and the number of people in need of an LTC place — and the resulting long wait times. These waits vary by region and depend upon a person’s need. Those in less urgent need of care may face longer waits. In B.C., the average wait time for an LTC place in 2022 was 196 days (Office of the Seniors Advocate, 2022). In Ontario, the median time a person living at home waited for an LTC bed was 213 days (2021-22) (Health Quality Ontario, n.d.).

While people wait for an LTC bed, they have several options: try to manage at home, possibly by paying for private homemaking or care services; go into a hospital where they will receive an “alternative level of care” (to the standard hospital care); or go into a privately financed, for-profit, assisted-living facility such as those run by Amica or similar companies. Little is known about nursing homes that operate outside the public system, although the number of residents involved is potentially large: in 2021, there were 67,855 people 65 and older living in retirement residences that offered assisted-living services. Sometimes these assisted-living services may include hotel-type services such as food and housekeeping, while other facilities may offer care of a similar or higher level to that available in a publicly funded LTC facility — at a price. For example, Amica (n.d.) advertises that “a variety of care levels means you’ll always have support to enjoy your life to the fullest, even if your needs change. Our care levels range from Independent Living to Assisted Living/Residential Care to Memory Care.” Unfortunately, little is known about how much individuals in assisted-living facilities pay for their care, or how many are receiving levels of care comparable to that available at a publicly funded LTC institution.[10]

Although there is much that is not known about LTC in Canada, there is widespread agreement on one point: the status quo is not satisfactory. The most common criticisms are that LTC is inadequately funded, placing an undue financial and care burden on people in need of care and their families; that the system of financing is biased toward institutional care; that resources are allocated in a wasteful fashion; and that LTC systems are administratively complex. Below, I discuss each of these issues, and raise others: inequitable funding, gender equity and equity across generations. I argue that LTC funding is inequitable because there is a weak relationship between people’s ability to pay for LTC and the contribution they are asked to make to finance their LTC needs. Moreover, there are questions about the how well current funding models promote gender and intergenerational equity.

Inadequate funding is evidenced by the quality and quantity of LTC provided in

Canada. The Royal Society of Canada study lists more than 150 reports over the past 10 years describing “unacceptable and sometimes scandalous conditions experienced by our older adults in nursing homes” (Estabrooks et al., 2020, p. 9). There are long waiting lists for a place in a publicly financed LTC facility in almost all provinces. These waiting lists are a consequence of a shortage of beds, which is due to a combination of a lack of public investment in new LTC facilities and funding structures that make it difficult to raise the capital necessary to expand private not-for-profit (and, to a lesser extent, for-profit) LTC homes (Estabrooks et al., 2020).

Recent initiatives aim to increase public LTC funding. The federal government is taking steps to use its spending power to negotiate long-term care standards and increase long-term care funding (Health Canada, 2022). At best, one might hope that these funding increases might improve standards of care somewhat, clear waiting lists and satisfy current LTC needs. For example, in April 2022, the Ontario government announced a commitment to provide “31,705 new beds” (Ontario Government, 2022); but as of May 2021, there were 38,000 people on LTC wait-lists in Ontario (Ontario Government, 2021). The announced new beds will at best clear Ontario’s current LTC wait-lists; they are not sufficient to cope with the expected surge in LTC demand associated with population aging.

The state of home care is not as well documented as the state of institutional care, but here too inadequate funding is an issue. As noted earlier, many older adults with activity limitations receive no home care, and when home care is available, only a few hours per week are typically provided.

Some have argued that improving the state of home care would help solve the crisis in institutional care — reforms such as cash-for-care benefits or other policies to encourage aging at home, or increased use of community-based care would make home care more viable, relieve pressure on LTC homes and possibly even generate cost savings (Flood et al., 2021). Yet home-based or community-based care does not necessarily generate substantial cost savings. The OECD estimates that the Netherlands and Germany — leaders in providing publicly supported, home-based, long-term care (Flood et al., 2021) — spend a greater percentage of GDP on LTC than does Canada. Indeed, the Netherlands spends more on LTC as a percentage of GDP than any other OECD country (OECD, 2020). No country has yet discovered a secret formula to eliminate the need for more financial and social resources for LTC over the next two decades.[11]How do we find these resources? Who pays for them? If governments do not raise taxes and cut spending, then they will need to ask those requiring care to pay some of the costs of their care. But how can governments structure these contributions to LTC costs in a fair, equitable and sustainable manner?

It is frequently asserted that Canada’s LTC system favours institutional care over

home-based care. For example, in British Columbia, a senior earning $29,000 in 2023 spent almost $14,000 less per year to live in a long-term care facility than to remain at home and receive one hour of home support a day (Office of the Seniors Advocate, 2023). Huber et al. (2009) found that Canada dedicates only 17 per cent of LTC public financing to home care, far behind most European countries.

There are few careful analyses of the relative cost of providing comparable levels of care in an institution to a home setting, but one exception is Clavet et al. (2022). These authors focus only on Quebec, where they estimate that the average amount of provincial government funding provided to cover an LTC home’s operating costs was $53,500 per resident in 2020. That same year, the provincial funding available for a patient living at home, but with care needs similar to those of a typical LTC home patient, was $16,964 in variable costs plus $6,670 in fixed costs (Clavet et al., 2022). While these numbers abstract away from issues such as the relative quality of home and institutional care, they provide a sense of the potential size of the funding differential between institutionally based care and home care.

Another factor contributing to the prevalence of institutional LTC is the absence of appropriate home care services. The CIHI (n.d.-b) estimates that, in 2022, 9.6 per cent of new LTC home residents could, potentially, have been cared for at home because they had clinical profiles similar to people already being cared for at home. However, many of them were older women living alone who had no family member willing or able to act as an unpaid caregiver. Others lived in rural or remote areas where a lack of in-home care services is particularly acute (CIHI, 2020).

A funding model that incentivizes institutional care by funding it more generously than home care is one potential source of waste in the LTC system. Another very substantial form of waste is the use of alternative level of care (ALC) beds in hospitals for patients who are waiting for an LTC space. For example, the Financial Accountability Office of Ontario (2023) estimated that in September 2022 about 2,500 hospital patients were receiving an alternative level of care while awaiting either a place in an LTC home (2,000 patients) or care at home (540 patients). In 2019-20, 17 per cent of hospital beds in Ontario were occupied by an ALC patient (Financial Accountability Office of Ontario, 2023). The cost of these LTC beds is considerably higher than the cost of care in an LTC facility. A National Institute on Aging (2019) study estimated that the cost of an ALC bed for a high-needs patient was $730 per day, compared to $177 for nursing-home care and $95 for home care. Multiplying that cost differential by the thousands of ALC beds occupied by patients waiting for LTC and by 365 days a year suggests that the resources wasted through inappropriate placements are in the hundreds of millions of dollars, not including the human costs associated with hospital bed shortages.

A CIHI (2020) study argues that one key factor causing people to enter LTC institutions, as opposed to being cared for at home, is difficulty navigating the home care system: “People experienced confusion and challenges around who to contact, what services were available, the amount of time required to coordinate services and the lack of continuity across the system.”

Clavet et al. (2022) provide further evidence that people have serious challenges accessing LTC. Based on the number of people who reported that they needed assistance with activities of daily living in the Canadian Community Health Survey, the authors estimate, that in Quebec, there were 315,568 people with some kind of care need in 2020, but only 195,800 individuals receiving publicly funded LTC. There are several reasons why people might not receive home care, such as the cost of home care services in provinces like British Columbia, which require clients to make a significant contribution to the cost of home supports (Office of the Seniors Advocate, 2023). However, the fact that over one-third of potentially eligible individuals do not receive care suggests that at least some people are unaware of their right to access care; that they are unable to successfully navigate the system and advocate for the care they need; that safeguards in place to make sure that vulnerable seniors get adequate care — reporting requirements by physicians or community members, for example — are not effective; or that there are simply insufficient resources to provide care.[12]

These coverage gaps are unsurprising given the lack of clear guidelines for what qualifies a person for care, how much care a person is entitled to and what kind of care they should receive. For example, advice found on the website of the Ontario government’s Home and Community Care Support Services on how to “check if you qualify for government-funded services” is that “your case manager will determine if you qualify” (Ontario Government, n.d.). Without clear criteria indicating whether a person can apply, people may not reach out to a case manager. Moreover, in the absence of clear guidelines, individuals cannot know whether they are receiving the care to which they are entitled, or how their care level compares to others in similar situations. These challenges may be an inevitable product of a system where home care resources are rationed. There cannot be set standards for care when the total home care budget is fixed, and the amount of care each person receives is constrained by the total funding available.

Canada’s LTC system has some redistributive elements. Accommodation charges in publicly funded long-term care facilities, for example, are income tested (and, in the case of Quebec, asset tested). In some provinces, there are also geared-to-income charges for some home care services, typically personal care or homemaking services (British Columbia Government, n.d.; Manitoba Government, 2022).

At the same time, there are several ways in which the current funding model is inequitable. One source of inequity is the use of income, as measured for tax purposes, when determining eligibility for public assistance, rather than a combined income and asset test (with the notable exception of Quebec). For older adults, income as measured for tax purposes — the measure used to determine ability to pay for care — is an imperfect measure of total resources available. This is because the income of older Canadians comes disproportionately from capital and investment income. To some extent, those who hold assets like stocks or real estate have a choice about when to sell them and realize capital gains that are counted toward taxable income. Income received within a Registered Retirement Income Fund is not taxed until it is withdrawn, and income that accrues within a Tax-Free Savings Account doesn’t count toward taxable income. Capital gains are not taxed until they are realized. For example, while the interest on a $10,000 Guaranteed Investment Certificate is included in a person’s taxable income as soon as it is paid, the capital gains on $10,000 of shares will not be taxed until the shares are sold, which might not happen until after the asset holder is deceased. Moreover, only 50 per cent of realized capital gains is included in taxable income, and capital gains on a principal residence are not taxed at all. Because the Canadian tax system provides significant scope for deferring or avoiding taxation of investment income, taxable income is an imperfect measure of a person’s financial situation and their ability to pay for services.

A second source of inequity stems frm the fee structure of long-term care. Once the maximum LTC accommodation charge is reached — which happens at income levels ranging from $29,630 in Alberta (Alberta Government, 2023) to $41,245 in New Brunswick (Public Legal Education and Information Service of New Brunswick, 2022) and $77,205 in B.C. — additional increases in income have no impact on LTC costs. Thus, LTC charges are regressive because they account for a much larger percentage of income for low-income individuals than those with high incomes.

Third, older adults — even low-income individuals — may have considerable wealth. According to data from the 2019 Survey of Financial Security, while the median after-tax income of a single person 65 or older was only $28,500, their median net worth was $320,000. If we look only at singles 65 and over whose main source of income was government transfers — in effect lower-income individuals — we find that their median net worth was $121,900. However, 25 per cent of these low-income, older singles have over $390,000 in net worth. One in 10 have net worth above $675,000. Thus, there is considerable wealth that does not enter into calculations to assess one’s ability to pay for LTC in most provinces.[13]

Finally, access to the limited supply of publicly subsidized LTC facilities is not means tested. A senior with millions of dollars in assets can receive publicly funded LTC and pay only for accommodation costs, while someone with far fewer resources may languish on a waiting list, perhaps coping with unpaid help provided by friends and family, and may not be able to enter a privately funded LTC home because of limited financial means.[14]

Thus, access to the most heavily subsidized forms of care — and the need to rely on private resources — is not closely tied to financial need or capacity.

It could be argued that, since Canadians accept the regressivity of hospital care and K-12 education, we should also accept the regressivity of LTC financing. However, LTC is fundamentally different from hospital care and education. It is not possible for children to save sufficient resources to pay for their own education. If a person must sell a home to pay for hospital expenses, it would have serious consequences for themselves and their family. By contrast, people typically enter LTC at the end of their lives. They have had time to accumulate assets to pay for their care. Self-insurance is possible for LTC expenses in a way that it is not for, say, a teenager with appendicitis. Moreover, people who are in an LTC home typically either die in care or go from an LTC facility to a hospital or hospice. The single older adults who make up the bulk of those in LTC facilities are not directly impacted if their material assets are sold, except for having more resources to buy better care. When LTC is provided at a low cost, the primary beneficiaries are the families of those in care, who typically inherit the assets once the person receiving care is deceased. There is a strong argument to be made for providing asset protection for the spouses and dependants of people in LTC. It is much harder to make an equity argument for spending scarce tax revenues to defray a person’s LTC expenses to preserve the value of their estate and their children’s or grandchildren’s inheritances.

As a society, we have chosen not to provide universal publicly funded LTC. Canadians have repeatedly voted for governments that expect LTC to be, at least in part, paid for by individuals needing care and their families, whether through unpaid care provided by family and friends, patient contributions to home or LTC care costs, or privately provided care services purchased by patients and their families. Since we have chosen a mixed public-private financing system, it behooves us to make that system as equitable as possible. Unfortunately, the Canadian LTC system is inequitable from several perspectives.

The current LTC financing system is problematic from a gender-equity perspective because it demands reliance on unpaid caregivers. The principle that family must provide support is best illustrated by the Manitoba government’s statement that, to be eligible for long-term care services, the recipient must “require more assistance than what is available from existing or potential supports” (Manitoba Government, n.d., p. 1). Yet providing unpaid care has a cost. While this cost is borne by both women and men, it impacts women more heavily. Women are somewhat more likely to provide unpaid care for adults than men — 22.9 per cent compared to 19.1 per cent, respectively. Moreover, the type of care that they provide differs. For example, the jobs of providing personal care or scheduling and co-ordinating care are more likely to fall to women, whereas men are more likely to be tasked with home maintenance or outdoor work. Women also put in more hours when they are providing care and are more likely to feel tired and anxious as a result (Statistics

Canada, 2022). There is an irony here: when someone is in a nursing home, there is an extreme reluctance to tax their income or wealth to pay for those nursing costs;[15]

yet there is no reluctance to tax family members, expecting them to sacrifice their time, and possibly their health and earnings, to care for a partner or a parent.

The current system of LTC financing compromises intergenerational equity in two respects. First, it is a pay-as-you-go system: current income, sales and consumption taxes finance current expenditures. When an economy is experiencing rising living standards and population growth, a pay-as-you-go system works well. Because each generation is wealthier and more numerous than the last, it can easily afford to pay the costs of caring for older adults. This kind of argument can be used to defend, for example, the introduction of Old Age Security in 1951 — and, in some respects, it is perfectly reasonable.

However, there are powerful arguments against overly relying on pay-as-you-go funding. There are especially strong arguments against using pay-as-you-go funding schemes that impose a significant burden on younger Canadians, such as payroll taxes. First, when the ratio of older adults to younger workers increases sharply — as is the case in Canada currently — continuing to finance LTC purely out of current tax revenues will require the current working generation to pay a substantially higher level of tax than previous generations, without enjoying any concomitant increase in benefits.

One could argue that it may be fair to ask younger generations to pay substantially more taxes than older adults if they can expect greater lifetime wealth than older generations. However, there are good reasons to believe that this is not the case. Population aging is expected to reduce economic growth rates — indeed, Canada’s per capita GDP is lower now than it was in 2019.[16] The millennial generation and generation X have much higher level of indebtedness relative to their after-tax income than did the baby boomers as a result of rising housing prices and higher levels of student debt (Heisz & Richards, 2019). Per capita incomes are higher now than they were decades ago. However, given today’s high housing prices, younger generations may not enjoy the enormous increase in home equity that many baby boomers have. Within the next few decades, climate change could also cause a significant decline in living standards (Swiss Re Institute, 2021).

Moreover, disparities in economic outcomes are rising across generations, with gains in income and wealth being concentrated among the most prosperous in each generation (Heisz & Richards, 2019). This is important when considering LTC financing: when the lowest-income Canadians are seeing little real income growth, is it appropriate to increase their tax burden to pay for the care of an older generation in possession of many billions of dollars of wealth?

A second way in which the current system of LTC financing compromises equity across generations is by perpetuating income inequality. Once an older individual is in a nursing home and no longer able to manage their assets, their children can do so in such a way that they generate as little taxable income as possible, for example by not selling real estate assets or by keeping funds in long-held assets that generate capital gains. In this case, the care the individual receives will be largely publicly financed. Upon their death, the assets will be inherited by their children. The absence of asset tests in the current system of LTC financing serves largely to protect the inheritances of the children of those currently receiving care — and perpetuates income inequality over time.

Canada faces a crisis in LTC funding. Yet this crisis is also an opportunity. The strains population aging will put on a gradually deteriorating and increasingly underfunded public LTC system could be the spark needed for a substantial reform of LTC financing. We now have a once-in-a-generation opportunity to make substantial changes to LTC financing. What should we make of this opportunity?

A system for LTC financing should be built on the same basic principles as taxation policy: it should be fair, efficient, neutral, transparent and not overly costly.[17]

Yet it should also be sensitive to the particular characteristics of long-term care. With this in mind, I propose the following five principles to guide LTC financing: it should be equitable, neutral and transparent, share the risk of catastrophic LTC costs and provide adequate levels of care.

The previous section showed that Canada’s system of LTC financing does a poor job of measuring up to these goals. Can we do better?

While the challenges Canada faces in funding LTC are not unique, the way we have responded to them is. No other country has quite the system of LTC financing that Canada does. Could the practices of other countries hold any lessons for Canada and bring its system of LTC financing into closer alignment with the principles outlined in this paper?

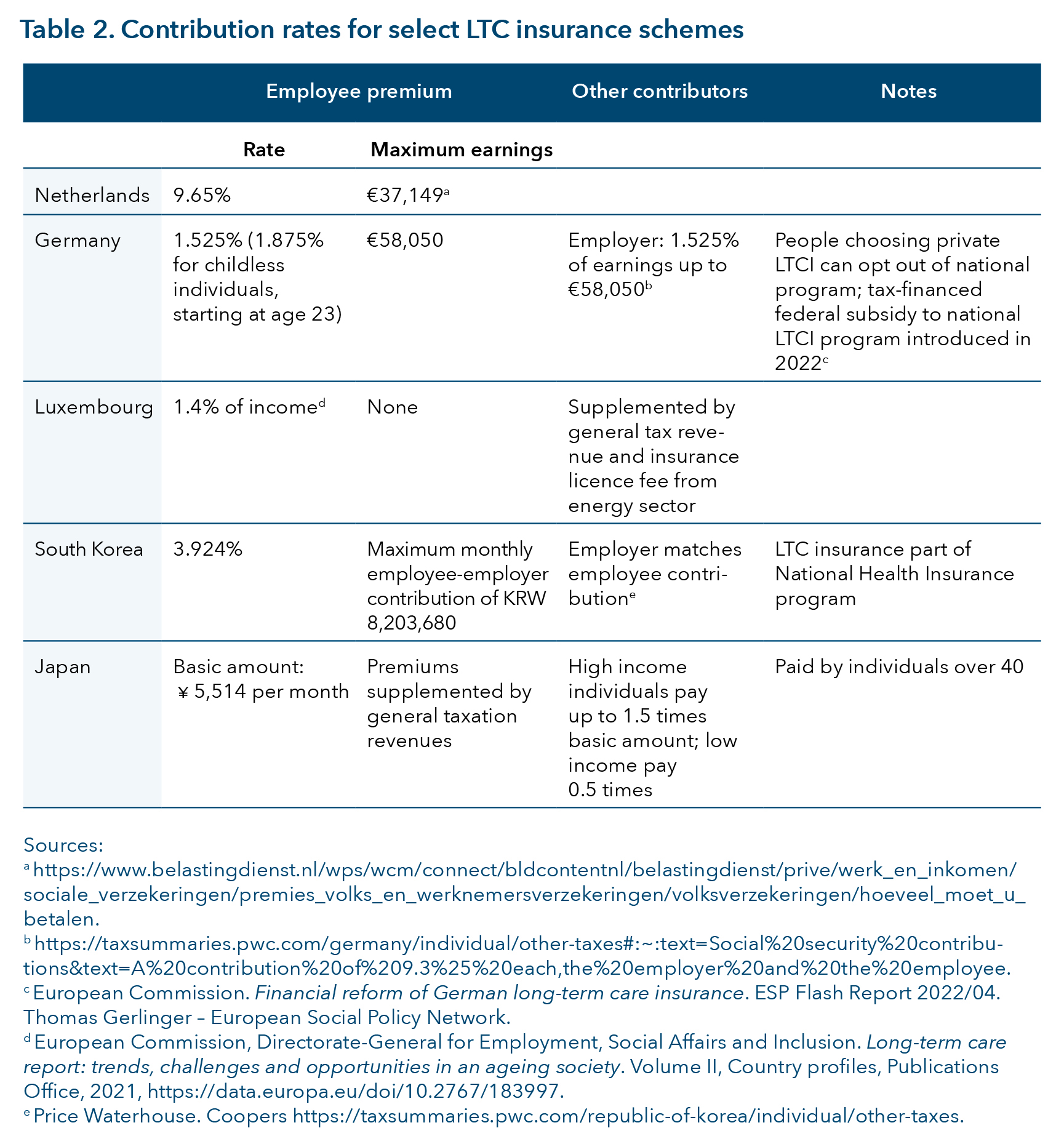

Several countries, including the Netherlands, Israel, Germany, Japan, Luxembourg and South Korea, have a national system of long-term care insurance, either financed by a dedicated LTC insurance premium or payroll tax, or by national health insurance premiums. The first country to adopt this system in the 1960s was the Netherlands, whose system covers those with care needs due to a lifelong disability and other extraordinary health costs, as well as older adults. Israel followed in 1986; Germany and Luxembourg introduced their systems in the 1990s; and Japan did so in 2000. One of the last countries to adopt a national LTC insurance system, South Korea, did so in 2007 (Fischer, 2022).

Table 2 shows the contribution rates for select national LTC insurance schemes. In the Netherlands, Germany and South Korea, LTC is financed in much the same way as the Canada Pension Plan/Quebec Pension Plan and Employment Insurance are in Canada. Employees pay a percentage of their earnings, and their contribution is matched by their employers. There is a maximum earnings or contribution ceiling after which no further contributions are necessary.

From a public finance point of view, these payroll taxes are considered to be regressive, which means that taxes paid relative to income fall as workers’ income rises. Payroll taxes are considered regressive because they are taxes on wages, and people whose income comes from wages have lower incomes, on average, than people whose income comes from investments or capital. Payroll taxes are also usually structured so that employees pay a set percentage of their income in contributions until a ceiling is reached. Because those who earn above the maximum contribution amount make no additional contributions on their earnings, payroll taxes account for a higher percentage of income for people earning below the ceiling than for people earning above it. Although employers are generally responsible for paying part of the insurance premiums, research finds that these costs are often passed, in whole or in part, back to workers in the form of lower wages (Kim et al., 2022).

Even though the financing of programs such as CPP/QPP is regressive, the contribution structure can be justified because of the linkage between contributions paid and benefits received. For example, for CPP/QPP, people earning over the contribution ceiling pay a lower percentage of their income in premiums but receive a lower replacement rate; that is, CPP/QPP benefits replace a smaller percentage of their pre-retirement incomes. Likewise, eligibility for EI benefits is tied to earnings history; people who are not employees pay no EI premiums but are not eligible to receive EI benefits.

It is too late to start using payroll taxes to fund a German- or Dutch-style LTC insurance scheme for Canadian baby boomers. The overwhelming majority of this generation is at or near retirement age. If a fully funded LTC insurance scheme — one that matched benefits received to contributions paid — were introduced now, it would not pay full benefits until those who are entering the labour force now need LTC. This would do little to solve Canada’s current funding problems.

We could introduce a pay-as-you-go LTC insurance scheme — in which payroll taxes are used to finance long-term care expenses — to cover LTC expenses for baby boomers who have not paid into the scheme. But this option would be highly problematic from an intergenerational equity point of view because it would involve a one-way income transfer from younger generations to baby boomers. The generations born post-1965 have already been asked to pay substantially higher CPP/QPP contribution rates than earlier generations did. For example, someone who entered the labour force in 1966 paid a CPP/QPP contribution rate of 1.8 per cent for the first 20 years of their working career; someone entering the labour force in 2006 started out paying a 4.95 per cent contribution rate — with no corresponding increase in benefit payments (Canada Revenue Agency, 2023). It does not seem fair to ask people born post-1965 to participate in yet another scheme tilted in favour of baby boomers and older generations.

There are two ways in which a national LTC model could be both financially viable and equity-enhancing. One way is to follow the Japanese model, in which those who are at a higher risk of needing care — individuals 40 and over — pay insurance premiums to cover the cost of that care. The great strength of the Japanese model is that it provides national insurance while overcoming, at least in part, some of the intergenerational equity challenges associated with waiting until population aging is well underway before starting an LTC insurance scheme.

Another alternative is funding LTC insurance out of general tax revenues. This could be achieved by raising tax rates or by broadening the tax base, such as increasing the capital gains inclusion rate or reducing the scope of the principal residence exemption. From an equity point of view, this would be superior to introducing a dedicated payroll tax because it would be more progressive and have a broader base. However, financing LTC insurance out of general tax revenues severs the link between contributions and benefits, and, without such a link, it is unclear if the program can be called insurance.

These models present two major challenges in the Canadian context. First, LTC is constitutionally a provincial responsibility. A national LTC insurance system would require the co-operation of all the provinces. Such co-operation is not unheard of. In Australia, for example, a series of agreements between the federal and state/territorial governments in the 2010s led to the Australian government taking over all policy, administration, funding and planning for aged-care services (Royal Commission into Aged Care Quality and Safety, 2021). However, such co-operation may be more difficult in the Canadian context. Moreover, the delivery of LTC typically involves locally provided services, such as those provided by community nurses, social workers and other locally based care professionals. The costs of institutional LTC provision vary substantially across the country, depending on local labour market and real estate market conditions. It is unclear how a national LTC system would respond to local variations in service costs and LTC needs.

A second challenge is that, to the extent that insurance programs provide clear and uniform entitlements to benefits, they can potentially increase public LTC expenditures. For LTC insurance to be a proper insurance scheme, rather than just a dedicated tax, it needs to have a benefit schedule; that is, it needs to pay out benefits according to a clearly articulated set of criteria, as CPP/QPP and EI do. For example, in Japan, a standard 74-item questionnaire as well as a home care visit and a medical doctor’s opinion are used to categorize individuals into five categories of need (Yamada & Arai, 2020). Similarly, in Germany, “the value of benefits varies depending on an assessment of care needs (on a scale of five care grades) and the type of care arrangements needed” (World Health Organization, 2022, p. 16). Under the German system, a person with grade 5 care needs was entitled to maximum benefits of €1,995 ($2,935) per month in 2020 for professional care if living at home, or €2,005 ($2,950) per month if living in an institution (Bundesministerium für Gesundheit, 2020).

The German and Japanese models score highly on the equity and transparency criteria. However, they come at a cost — at least to the public purse. In Germany, costs are mitigated by covering only basic LTC costs, limiting benefits and requiring co-payments for institutional care. Consequently, a rising number of German seniors rely on supplementary social assistance programs to cover LTC costs. In the Netherlands, public expenditure on LTC was 3.7 per cent of GDP in 2019, compared to the European Union average of 1.7 per cent (European Commission, 2021). These high costs are in part driven by LTC expenses for younger people with disabilities (Maarse, 2012). Since 2015, the Netherlands has actively “moved from an integrated national scheme towards a more decentralised scheme involving national, regional and local governance levels, with responsibilities divided between public and private bodies, and between health and social care sectors” (European Commission, 2021, p. 286). Arguably, the Netherlands is stepping away from a national LTC insurance model and becoming more like Canada, with an emphasis on providing care and support in a person’s own home for as long as possible, and with more decentralized and needs-based public support (European Commission, 2021, pp. 285-286).

In sum, there are some advantages to having a national LTC insurance scheme, especially in terms of clarity and transparency around benefit eligibility. However, a pay-as-you-go LTC insurance scheme financed through payroll taxes would score poorly on intergenerational equity and redistributive grounds. At the same time, a scheme that did not provide benefits to today’s seniors would do little to solve the LTC funding challenges Canada faces. One national LTC insurance model worth considering is Japan’s, which finances national LTC insurance by taxing people at risk of needing care. An alternative approach, discussed below, is to take some of the best parts of an LTC insurance system — such as the transparency and clarity around benefit levels — and incorporate them into another system of LTC financing.

One of the long-standing criticisms of Canada’s LTC system is its alleged bias toward institutional care. To the extent that this bias is caused by the more generous public support given to institutional care, it can be eliminated through either more generous funding of home care or a revision of the funding model for institutional care. I consider both options, although I focus primarily on rethinking institutional care financing.

The United States (prior to the expansion of Medicaid coverage under the 2010 Affordable Care Act) was the best example of the government as the payer-of-last-resort model of nursing-home financing, although elements of this model are also found in the United Kingdom. In the U.S., institutional long-term care is covered by Medicaid, a government-funded program that provides health coverage to low-income Americans. It is an income- and, in some states, asset-tested program. Those in need of care are expected to spend down their income and assets by paying the full cost of their LTC, until their income and assets are low enough to entitle them to Medicaid (Medicare.gov, n.d.).[18] Not all nursing homes accept Medicaid payments. However, in those that do, Medicaid-eligible residents are only required to pay supplementary charges for, say, a private room.

The problem with the U.S. government as payer-of-last-resort model — and the reason why many U.S. states are moving away from it, at least in the case of costly, long-term illnesses — is the devastating financial impact it can have on a healthy spouse. When the combined assets of both spouses are considered to determine Medicaid eligibility, most of their assets must be spent before the partner in need of care qualifies for a Medicaid-funded bed — leaving the other partner with few assets. (A family home occupied by the healthy spouse is usually exempt from asset calculations.) This type of asset test creates perverse incentives. For example, it encourages financially motivated divorces, a situation where the healthy spouse divorces the one in need of care to protect their assets.[19]

A variant on the government as the payer-of-last-resort model has been used in the U.K. for social care (e.g., rehabilitation after an accident or an illness). In the U.K., people with financial assets above a set level — £23,250 in 2023 ($40,015) — pay the full cost of their LTC. Any income above the personal exempt amount must also be used to pay for care costs, much like in the Canadian system (AgeUK, n.d.-a). However, in the U.K., asset tests are based on an individual’s assets, not the couple’s joint assets. This system can offer more protection to the healthy spouse than the U.S. system — unless the bulk of the couple’s financial assets are in the name of the spouse in need of care. The U.K. government as the payer-of-last-resort model, like the U.S. system, is unpopular and reforms to the system are planned.

The standardized, portable public benefits model is epitomized by Germany, where a person with a given level of care needs receives a standard benefit. For example, as of 2020, a person living at home received long-term care benefits of €689 ($1,015) per month if they had grade 2 care needs, and €1,995 ($2,940) monthly if they had grade 5 care needs. These benefits can be used to purchase approved care services from a variety of providers. Part of the funds may also be used to pay a nursing allowance to a family caregiver. The benefits are, to a considerable extent, portable across care settings and providers. For example, as of 2020, a person with grade 5 needs was entitled to only slightly more benefits if they were receiving institutional care than care at home. A person fully resident in an LTC home received benefits of €2,005 ($2,955) per month, just €10 ($15) more per month than someone with the same needs being looked after in their own home (Bundesministerium für Gesundheit, 2020). Note that these public benefits are only for care costs, and do not typically cover the full costs of care, especially institutional care. The care recipient is responsible for paying care charges over and above the benefit (with some provisions made for those in financial hardship). Additionally, in Germany, as in Canada, residents are also responsible for their accommodation costs.

One of the great strengths of the German model is that it largely eliminates the bias toward institutional care that exists in the Canadian system. If people wish to use their funding to buy the care they need to cope at home, they are free to do so if the care provider meets certain standards. It also provides flexibility: individuals who wish to use private resources to pay for higher-quality accommodations or more personal care can do so. The ability to charge residents more for higher-quality care, accommodation and other services could also incentivize investment in the LTC sector.

Yet providing similar funding levels for institutionally and home-provided care, together with keeping program costs at a manageable level, inevitably results in LTC benefit payments that are substantially less than the cost of providing care in an LTC home. In Germany, residents are expected to make up the difference — if they can afford to do so. In both Canada and Germany, provisions are made for those who cannot afford to make the expected contributions to their care costs. In Germany, low-income seniors are eligible for various social benefits that assist with the cost of care, making the system less a pure national LTC model and more a mixed insurance/means-tested benefits model. Germany is also moving away from the standardized portable benefits model and introducing graduated reductions in the private costs of LTC for people residing in LTC facilities for long periods.

There are two major takeaways from Germany’s experience. First is that a system of standardized, portable benefits cannot stand alone. Because grants for care costs are not intended to cover the costs of accommodation and housekeeping — or even the full costs of personal care — every system of standardized grants expects care recipients or their families to contribute to accommodation and personal care costs. However, these contributions must be integrated with some kind of means testing, whether it be income-tested subsidies or grants, to ensure that everyone has access to care. Standardized portable benefits are at most one element of an LTC strategy. Second, if we were to move from a system like Canada’s where a substantial number of people — even those with extensive care needs — receive very little public support, to one where public support for care was a universal entitlement, we would have to either increase government spending on LTC, reduce the amount paid to those receiving the most support (i.e., people in institutional care), or provide a combination of both. One could argue that the right choice is to spend more public money on LTC. However, given Canadian governments’ history of LTC spending, there are limits to the amount of public money one can realistically expect to be forthcoming. Moreover, the experiences of other countries suggests that political support for LTC insurance systems is fragile. The Netherlands is moving away from a pure national insurance model, as is Germany, with more income-tested benefits and more local provision.

The challenges of exporting the German model are exemplified by Australia, which has also adopted standardized needs-based funding levels for home and institutional care. For example, as of 2023, a person with level 4 care needs was eligible to receive a maximum daily home care subsidy of AU$163.27 ($145) per day (and possibly some additional supplements). These payments come in the form of a home care package, which can be used to purchase approved home care services (Australian Government, n.d.-a). However, the Australian government has chosen to limit its LTC spending by limiting the number of care packages that are offered. Consequently, people wait months for care. As of June 2020, people approved for a level 4 home care package could wait over 12 months before being assigned to care at any level (Royal Commission into Aged Care Quality and Safety, 2021). This shows that a system of standardized, portable benefits — like any other kind of LTC system — will not work well if the demand for benefits outstrips governments’ willingness to supply them.

Most countries that have standardized, portable LTC benefits pay for less than the full cost of LTC. Australia — despite the challenges it faces over LTC — is noteworthy for its clear, transparent, well-documented co-payment model. In Australia, charges for institutional long-term care are divided into three components. All care residents pay a basic daily fee, which is set as a percentage of the old-age pension. Two additional means-tested payments cover care and accommodation. Both these fees are based on a resident’s income and assets. Residents with few assets and low incomes pay only the basic daily fee, those with moderate incomes and assets pay for part of their accommodation costs but no care fee, and those with higher incomes and assets pay the full cost of their accommodation and also contribute to the cost of their care. There is, however, both a lifetime and annual cap on care fees. The asset calculation also includes only part of the assessed value of the care recipient’s home, and then only if the home is not occupied by a spouse or a dependent child (Australian Government, n.d.-b).

The Australian model is noteworthy, first, because it demonstrates that it is politically and practically possible to institute a clear, transparent and progressive system of care payments, and second because of the lifetime care payment cap, which we discuss further below.

The U.K. is attempting to emulate Australia’s lifetime cap on care costs, and the experience is an interesting illustration of the challenges associated with importing policy ideas from other countries. The United Kingdom has historically had a government-as-payer-of-last-resort model of LTC financing. Care recipients who have sufficient income and assets to pay the full cost of their own long-term care have been expected to do so. If a person owns a home, and the home is not occupied by their spouse (or another qualifying family member), the home needs to be sold eventually, and the proceeds used to pay for the cost of their care. But dissatisfaction with this system is growing.[20]

In response to widespread dissatisfaction, the British government announced in 2021 that, as of October 2023, there would be an £86,000 ($147,000) lifetime cap on care costs; the date has since been postponed to 2025 (St. James’s Place, 2023). In the U.K., as in Australia, the cap on lifetime care expenses is intended to apply to both residential and home-based care. However, the proposed lifetime cap would apply only to care costs, not accommodation or housekeeping expenses. In a sense, it operates like a deductible in an insurance scheme. The value of the cap was originally estimated to be equivalent to about three years of residential care (Department of Health & Social Care, 2023).

Adopting a cap on care expenses has not proven to be entirely straightforward. To cap care costs, LTC facilities and home care providers in the U.K. would need to distinguish between care costs, and charges for accommodation and housekeeping, with the latter not counting toward the cap (Department of Health & Social Care, 2023). But what counts as care? A recent U.K. consultation document suggested that it “would not be possible for the guidance to specify any specific services that do and do not count towards the [lifetime care] cap, as this may be different for every person” (Department of Health & Social Care, 2023). Yet in the absence of such guidance, it would be challenging to implement a cap. A further complication is the need to find new revenue sources to make up for any revenue shortfalls created by limiting residents’ contributions to the cost of their care. It is not surprising that the U.K. 2022 Autumn Statement announced that the central government had “heard the concerns of local government” and was delaying the implementation of the cap-on-care costs (HM Treasury, 2022).

In Australia, the cap-on-care model works because it uses a standardized, portable benefits model, which includes standard funding levels for home-based care, ranging from AU$9,179.75 ($8,070) per year for someone with basic care needs to AU$53,268.10 ($46,840) annually for someone with high care needs (as of March 2023) (Australian Government, n.d.-c). As for institutional care, there are income- and asset-based co-payments for these care packages, and it is those co-payments that count toward the limits on individuals’ care expenses. Because the funds for care (and the required co-payments) are clearly demarcated, it is relatively easy to determine what expenditures count toward the limits on individuals’ lifetime care expenses. In addition, the number of care packages is strictly rationed. This means that, even with limits on the amount that individuals are asked to contribute to their own care, Australia is able to control total LTC expenditures.

There are important lessons to be learned from the U.K. and Australian experiences. Canadian LTC systems, especially LTC homes, often distinguish between “accommodation,” “housekeeping” and “care,” and expect individuals to pay their own accommodation and housekeeping costs, if they can afford to do so. Yet the U.K. experience illustrates that the division of costs into accommodation and care is somewhat arbitrary. Services are not so easily compartmentalized. For example, the person who helps dress a client might also fold and put away their laundry. If we were to introduce a lifetime limit on care costs, we would need to think holistically about how the costs of disability late in life should be shared between those needing care, their families and the state — and what limits, if any, should be placed on how much individuals or their families pay for care in old age.

The number one reason why LTC is a critical policy challenge now is population aging: older people now make up a larger share of Canada’s population than they did in the past, and their population share will continue to grow for the next two decades. If we believe that intergenerational fairness requires that the taxes paid relative to the government benefits received should be roughly the same across generations, then it would be unfair to ask a shrinking pool of young people to bear the entire burden of LTC for a growing elderly population. Moreover, there are practical limits to this strategy. Placing high taxes on a shrinking pool of workers could start to compromise economic efficiency and discourage the labour supply when it is most needed. A 2022 OECD analysis of the revenue impacts of population aging notes that payroll taxes, along with personal and corporate income taxes, are most likely to have a negative impact on economic growth. Inheritance and property taxes are some of the least harmful for growth, followed by consumption taxes (Crowe et al., 2022). Thus, a key part of any sustainable LTC financing strategy is likely to involve asking for greater contributions from older individuals most at risk of needing care. Since older people tend to have higher levels of assets and lower levels of income than younger ones, wealth-based financing strategies could play a major role in finding the resources to solve Canada’s long-term care crisis.

Several of the countries discussed so far — Australia, the U.K., the U.S. and the Netherlands[21] — at times base an individual’s expected contributions to the cost of their long-term care on their assets. In this section, I summarize these three models of wealth-based contributions and describe a possible third alternative: inheritance and estate taxation.

Wealth-based cut-offs for assistance in LTC financing

One type of wealth-based financing is the eligibility cut-off. For example, in some parts of the U.S., people are not eligible for Medicaid if their assets exceed eligibility thresholds. In Canada, wealth-based cut-offs are used in Quebec, where the contribution de l’adulte hébergé — a resident’s contribution to the cost of their nursing home accommodation — is based on both assets and income. A person who holds more than a set minimum amount of assets must pay the full price for their LTC home accommodation — for example, $1,737.60 per month for accommodation in a shared, two-bed room in 2023 (Régie de l’assurance maladie, n.d.). The asset thresholds are set separately for each class of assets: a person who owns a home worth $200,000 would be eligible for reduced-cost accommodation, whereas a person with $200,000 in liquid assets would not be (Ministère de la Santé et des Services Sociaux, 2020). The system is similar to many provincial social assistance programs, such as Ontario Works, which take into account both assets and income when considering eligibility for benefits.

However, wealth-based eligibility systems are not always popular. Newfoundland and Labrador, which at one time had wealth-based eligibility for LTC assistance, moved to an income-only based assessment model in 2018.[22] California has recently passed legislation that would eliminate asset limits entirely for seniors and disabled persons as of January 1, 2024 (Justice in Aging, n.d.). Introducing new asset tests could be a politically fraught endeavour. Moreover, from an equity point of view, such tests do poorly in terms of differentiating between moderate-wealth and high-wealth individuals — all individuals with assets above a set threshold are treated alike.

Wealth-based cost recovery

A wealth-based cost-recovery model, a variant of the wealth-based cut-off, is used in the U.K. Under this model, people are assigned care services based on their level of need, as assessed by a social care professional working for the local government (AgeUK, n.d.-b). However, the cost of those services may be recovered through income- and asset-based co-payments. For example, if a single person with low income and substantial assets enters an LTC home, the local authority would pay for the bulk of that person’s care costs up front. However, when the person’s assets are sold, some of the proceeds would be claimed by the local authority and used to defray care costs. Likewise, in France some payments to the elderly are “cash advances,” recoverable from an individual’s estate. However, in France the recoverable benefits are typically those targeted to low-income older adults, not those to assist with care needs.

Mandated wealth-based contributions

An alternative type of wealth-based financing is the Australian model. A care recipient’s assets are assessed, and the recipient is expected to contribute a percentage of their asset holdings above a minimum threshold to the costs of their long-term care. The advantage of the Australian model over the U.S. or Quebec model is that it achieves a higher degree of equity between those with moderate asset holdings and those with more substantial holdings because people with more assets pay more. The advantage of the U.S. or Quebec model is that public subsidies are targeted to the neediest.

Inheritance taxation

One of the drawbacks to any model that asks individuals to pay for their own LTC care is that it reduces risk-sharing. It places the burden of paying for care on those who need care and their families, rather than sharing the cost collectively. However, wealth-based contribution models could be modified to achieve a greater degree of risk-sharing by using inheritance taxes to finance long-term care. Instead of recovering the costs of LTC from the estates of people resident in LTC homes, we could recover the costs from a tax on all estates. Inheritance and estate taxes score well on the standard measures of tax design. A recent OECD report concluded:

well-designed inheritance taxes can raise revenue and enhance equity, at lower efficiency and administrative costs than other alternatives. From an equity perspective, an inheritance tax, particularly one that targets relatively high levels of wealth transfers, can be an important tool to enhance equality of opportunity and reduce wealth concentration. (OECD, 2021a, p. 10)

Inheritance taxes would be a way of achieving some of the benefits of LTC insurance while still respecting intergenerational equity: those in need of care could receive standardized benefits, as in other LTC insurance schemes, but the program would be paid for out of the estates of those at risk of needing care. The cost would still fall on the living, but it would fall on those in their 50s, 60s and 70s, who would inherit less than they might otherwise expect to do, rather than younger people who are attempting to enter the housing market and decide whether they can afford to have children. Inheritance taxes also have redistributive potential because the wealthier have larger estates. Although no country has currently adopted this model, it has merit from an equity and efficiency — if not necessarily a political — point of view.

As shown in figure 1, in 2019, the year immediately prior to the pandemic, the three countries spending the most on LTC as a percentage of GDP were the Netherlands (4.1 per cent), Norway (3.7 per cent) and Denmark (3.6 per cent) (OECD, 2021b). These countries can finance such levels of long-term care spending in part because they raise more tax revenue than Canada — and, indeed, most other countries. According to OECD data, total 2019 tax revenues were 39.3 per cent of GDP for the Netherlands, 40.1 per cent for Norway and 46.9 per cent for Denmark. By way of contrast, total tax revenues made up 33.1 per cent of GDP for Canada in 2019.[23]

A substantial tax increase is one way of putting LTC financing on a sustainable footing. While arguments could be made for various tax increases — increasing the capital gains inclusion rate, for example (Smart & Hasan Jafry, 2022) — one option particularly worth considering in the long-term care financing context is increased inheritance and estate taxes.

In Canada, much of LTC is privately provided and financed, whether in the form of unpaid care provided by friends and family, privately purchased personal care and homemaking services, or privately funded assisted-living facilities. Yet because this care is, for the most part, excluded from official data on LTC spending, we cling to the myth that LTC in Canada is publicly financed. It is not.

Moreover, Canada’s existing LTC system is not working well. In many parts of the country, there are long waiting lists for admission to publicly funded LTC institutions. The quality of care in some institutions leaves much to be desired. There are low levels of support for home care. A significant minority of people with activity limitations receive no care at all. Many caregivers, particularly those caring for a spouse, report providing long hours of care and feeling tired and overwhelmed.

We can do better. But how?

The first priority is greater transparency around eligibility for benefits and service levels provided. This could be achieved by the following:

Greater transparency is important for several reasons. First, to improve take-up of benefits: if people do not know what benefits they are eligible for, they are less likely to apply for them. Second, to increase fairness: if information about typical levels of service provision is readily available, people will be better able to advocate for themselves. Finally, transparency is a prerequisite to system change. Fixing Canada’s LTC system will require money and political commitment. People would be more likely to support change if they knew just how little support the system provides for many of those in need.

Greater transparency will tend to lead to greater standardization of benefits because transparency allows people to learn how funding levels are set and advocate for funding that matches their needs. I would argue that Canadian provinces should provide benefits that are more standardized and portable to reduce the current disparity in the funding of home-based and residential care, to promote fairness in funding levels and to provide people with more choice about how to meet their care needs. For Canadian provinces, following the Australian lead and making a less ambitious attempt to narrow the home-based/residential care funding gap might be more manageable than following the German model and attempting to fund home and institutional care equally.

Yet if a Canadian province wants to provide funding levels for home care that are comparable to those available for institutional care, it has two choices. First, it can redistribute existing funding, providing more for home care and less for institutional care. At present no Canadian province requires people in an LTC home to pay for their care (as opposed to their accommodation). If we were to replace this system with one that funded home and institutional care more equally, there would be less public funding for institutional care. Residents of LTC homes would have to make a larger contribution to the cost of their care. This would necessitate an expanded system of subsidies, grants and income-testing to ensure that the overall system is financially sustainable, and that those with few resources would still be able to access care. The Australian system of income- and asset-based contributions to care costs stands out as a clear and transparent model to follow.