Canadian Policy Prescriptions for Dutch Disease

Robin Boadway, Serge Coulombe and Jean-François Tremblay

In this study, Jorge Niosi examines the channels by which university-developed technologies are transferred to industry. Canada invests large sums in academic research, but the fruits of these investments are not reflected in more industrial innovation and improved productivity.

To frame the analysis, Niosi lays out a supply-demand model of innovation according to which basic discoveries and advances in frontier science ultimately bear fruit in the form of commercially viable technologies. The supply side is where ideas are organized into useful concepts, research and discovery, and it is dominated by university research. Because the economic benefits of such research are broad in scope and difficult to predict, governments tend to be heavily involved in financing it. Using indicators such as investment in university research and development (R&D), numbers of science and engineering graduates and scholarly publication rates, Niosi concludes that the supply side of university technologies is reasonably healthy in Canada.

At the demand end of the university research pipeline, businesses build on basic technologies to develop commercially profitable products or processes, which often require complementary investments in R&D. Niosi points out that several factors – notably Canada’s relatively small and geographically dispersed domestic market – work against strong demand for technology here compared with in the United States. Despite pockets of strength in the pharmaceutical and electronic equipment industries, demand for university research is surprisingly low. The author notes that most Canadian companies turn to other firms for licensed technology, which is circumstantial evidence that they are not finding the technologies they need in universities.

Niosi terms the grey area between the supply and demand of university-developed technologies the “valley of death,” not only because of the paucity of funding, but also because of mismatched expectations. From the perspective of business, universities provide a potential vehicle for developing early-stage technologies that would otherwise be too risky and costly. However, from the perspective of academia, professors are primarily motivated by scholarly publication of their work, for which commercial potential is typically much less important than originality.

Currently in Canada, most efforts to connect universitydeveloped technologies to potential commercialization opportunities pass through academic offices of technology transfer (OTTs). OTTs are charged with evaluating the commercial potential of these technologies, securing appropriate intellectual property protection and division of royalties, and seeking out potential licensees – essentially a supply-push approach. But they have neither the human resources nor the market knowledge to provide effective technology transfer.

Niosi suggests that a demand-pull approach, by which businesses seek out and cultivate university technologies, would be much more useful, and points to several US initiatives that have proven effective. These include the Small Business Innovation Research (SBIR) and Small Business Technology Transfer Research (STTR) programs, which provide seed funding to smalland medium-sized enterprises for early-stage technology development in cooperation with academic researchers. In addition, the Advanced Technology Program (ATP) helps companies commercialize generic technologies, in part by involving them directly in university research priorities. By contrast, says Niosi, legislation along the lines of the landmark 1980 Bayh-Dole Act, which grants intellectual property rights to the inventors rather than the funders of technologies, would be ineffective in Canada.

In the Canadian context, the key objective in developing a demand-pull approach to university-industry technology transfer would be to involve businesses in the development of academic research agendas without allowing them to dictate those agendas entirely. Many of the Expert Panel on Commercialization’s proposals are lacking in this regard, because they would keep decisions about what technologies to fund in the hands of universities and governments. The author proposes that Canada create pilot programs along the lines of the STTR and ATP under the rubric of the successful and well-regarded Industrial Research Assistance Program.

Two commentators provide university and industry practitioner perspectives. University of Alberta President Indira Samarasekera broadly agrees with Niosi’s diagnosis of the problem, and emphasizes that, given that universityindustry partnerships are currently limited to a small number of large firms, policies must better connect small and medium-sized enterprises to universities. Ilse Treurnicht, head of the MaRS innovation consortium, cautions that the US innovation ecosystem is quite different from that of Canada, which means that a cookie-cutter approach may not be very effective. She agrees, however, that businesses should be involved in developing academic research agendas, because they have the market knowledge that universities and granting councils lack.

Innovation, particularly in science and technology, is the engine of economic growth (Rosenberg 2004). This idea was Robert Solow’s contribution, for which he received a Nobel Prize in economics in 1987. Since then, many national and international studies have confirmed his thesis. Economies grow through the adoption of technological innovations, more than through the incorporation of such inputs as capital and labour. Technological innovation accounts for well over 50 percent of economic growth in Organisation for Economic Cooperation and Development (OECD) countries (Pianta 1995). This occurs in two ways: productivity increases as a result of the wide adoption of new technologies, and new industrial products and sectors are created (Saviotti and Pyka 2004).

Universities are essential contributors to technological innovation. They train the labour force and create human capital. As a result of their research activities, new areas are explored, the frontiers of knowledge are pushed forward and sometimes even the foundations of new industries are laid. Yet the channels through which knowledge flows from universities to the economy and back are not well understood.

Among OECD countries, Canada ranks high with regard to funding university research and the number of graduates in the natural sciences and engineering, as well as on some raw indicators of outcomes, such as academic publications. Although some improvements can be made on the supply side, the main problems lie on the demand side. It is far from clear whether these investments in academic research are bearing fruit in terms of improved business performance and productivity. There are relatively few hightechnology and science-based companies in Canada. And there is a common perception that Canada lags behind in terms of the commercialization of research, and in productivity.

In this paper, I will examine the different channels of technology transfer and compare their contribution in Canada with their contribution in other industrial nations. I will try to answer the following questions:

The production, diffusion, adoption and mastering of technology are most often achieved by industrial firms, but they require a complex institutional and policy environment in order to conduct research and development (R&D) and innovate. This environment – these institutions and policies – are called national systems of innovation (NSIs). NSIs are policies, institutions and organizations devoted to the production and diffusion of new and improved science and technology within the boundaries of states (Lundvall 1992; Nelson 1993; Niosi 2000a; Niosi et al. 1993). Today, the governments of most industrial and some industrializing countries employ the NSI approach in their innovation policies.

Several aspects of the NSI approach need to be outlined. Linkages among the innovators (the focal elements, or nodes, which include research universities, government laboratories and innovative firms) are key. These relationships include personal and financial knowledge and regulation flows among the nodes (Niosi et al. 1993). Most important among these linkages are the interactions between producers and users of innovations, in particular, those between universities, government laboratories and industry (Lundvall 1992). Interaction between the users and the producers is vital because users are among the main sources of ideas for innovation among producers. All of the nodes in the system produce knowledge, and some of them, particularly industrial firms, are also the main users of this technology. The efficiency and effectiveness of the system are heavily dependent upon the fluidity of the linkages, particularly knowledge transfers, between the nodes of the system (Niosi 2002). Thus, the interaction between firms and university and government researchers should send clear signals to the researchers as to the likelihood that a university invention will be commercially useful to the industry.

Universities are central components of the NSI. They create human capital, without which existing technology cannot be absorbed and adapted (Lau 1996). While traditional, low-growth industries demand less education, in the fast-growing new economy of the information technologies – pharmaceuticals and biotechnology, advanced materials and aerospace industries – universities provide the high skills required. In many of these science-based industries, key knowledge is thus created in universities and government laboratories and then transferred to business (Niosi 2000b). Further, in any type of industry, higher education increases the capacity of organizations to adopt high technology and use it efficiently (Lim 1999).

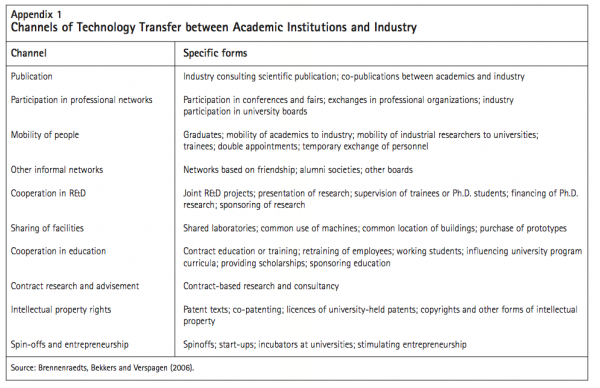

Universities move the frontier of science forward by means of advanced research, and they transfer the results of this activity to industry and society through different channels (see appendix 1 for a more complete list of the channels). Among these channels are:

Researchers have highlighted the impact of academic research on industrial innovation for over two decades. In a pioneering study in the United States, Jaffe found that university R&D had a positive impact on industry R&D, particularly in such areas as drugs and medical technology, electronics, optics and nuclear technology (1989). He attributed this effect to knowledge spillovers from university to industry. He suggested that academic research induced industrial R&D in the same disciplines. Yet he did not try to understand the organizational issues and transfer mechanisms by which academic research spills over and benefits industrial research.

Similarly, Edwin Mansfield, another pioneering scholar who systematically studied the relationships between academic research and industrial innovation in the United States, found that in seven industries (pharmaceuticals, instruments, information processing equipment, electronics, metals, petroleum and chemicals manufacturing) some 11 percent of the products and 9 percent of the processes could not have been developed without university research (1995). Mansfield found that larger firms benefited the most from academic research. Similarly, Cohen, Nelson and Walsh (2002) found that research performed in universities and government laboratories in the US had a major impact on a small number of industries, including pharmaceuticals, glass products, electronics, aerospace and chemicals. They also found that the channels through which technology was tranferred between public and private organizations were both open and codified (publications and conferences) and personal (meetings, consulting and research contracts).

In Canada, an econometric study has estimated that the C$5 billion invested in university research in 1993 increased the gross domestic product (GDP) by over C$15 billion annually, largely through its positive impact on business innovation (Martin and Trudeau 1998).

In the last 10 years, much attention has been focused on entrepreneurial universities, that is, those that nurture new spinoff firms (Rothaermel, Agung and Jiang 2007). Some universities, such as the Massachussetts Institute of Technology in the United States and Chalmers University in Sweden, are presented as models of institutions that promote economic development by means of the creation of new firms (Agrawal and Henderson 2002; Jacob, Lundqvist and Hellsmark 2003; O’Shea et al. 2007).

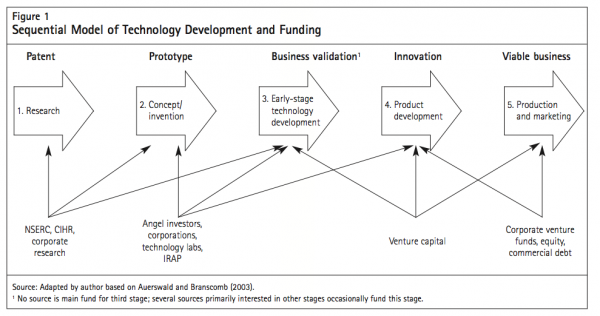

Several authors have mapped the various phases and stages in the innovation process. Figure 1 presents one model that is particularly useful in the Canadian context. The process starts with the first stage, research, which is followed by the second, centred on invention, and the third, focused on early-stage technology development. The fourth stage is product development, and the fifth production and marketing.

The first and second stages I will refer to as the “supply side” of innovation, because this is where ideas are organized into useful concepts, research and discovery. Because the economic value of any given new idea (or group of ideas) is difficult to predict, businesses left to themselves would underfund investments in the supply of innovation. For this reason, governments play a large role in funding (through public and corporate granting councils, governmentfunded laboratories and, to a lesser extent, angel investors)1 and universities play a relatively large role in performing the research. As will be seen later, Canadian policies seem to be slightly biased toward the supply side.

The fourth and fifth stages can usefully be termed the “demand side” of innovation, which is when the commercial potential of basic research and inventions is exploited. Here, the business value of an innovation has been validated, production applications and enduser markets have been clearly identified, and financing has been obtained from venture capital, business equity and commercial debt. With well-functioning capital markets, there should be little or no need for government assistance.

The third stage – which is the grey area between the supply and demand for innovation – has sometimes been called “the valley of death,” because it is funded only laterally and scantily, in both the US and Canada. But the problems go well beyond funding: there is often a mismatch between expectations on the demand side and motivation on the supply side. From the perspective of business, investing in early-stage technologies is risky, because it is difficult and potentially costly to assess their commercial viability. From the perspective of academia, scholars are primarily motivated by a desire to publish in scholarly journals, for which commercial viability is typically not as important as the originality of the discovery. This disconnect between supply and demand of innovation is a major obstacle to effective university-industry technology transfer.

The supply of science and technology by universities, unlike the supply of countable goods such as automobiles, cannot be measured directly. Nevertheless, through indirect indicators we can sketch a partial picture of it, and Canada scores well on some, but by no means all, of these indicators.

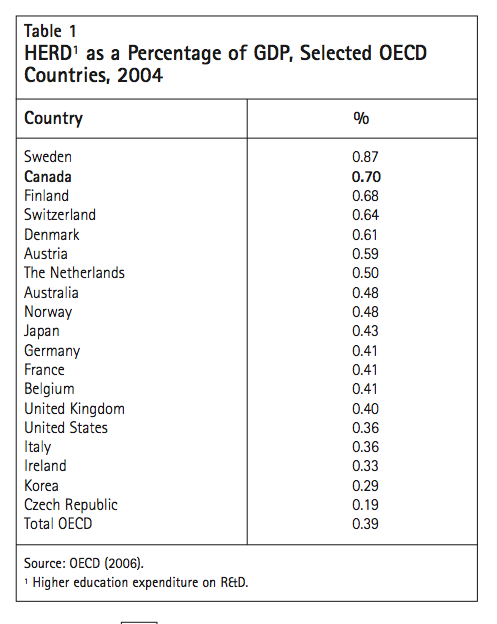

Canada is second among OECD countries in terms of its expenditure on university research and development as a percentage of its GDP (table 1). This figure reached 0.70 percent in 2004; it was second only to Sweden’s and nearly double that of the United States. More significantly, this share has increased steadily from only 0.44 percent in 1997, as successive governments have injected more money into the granting councils.

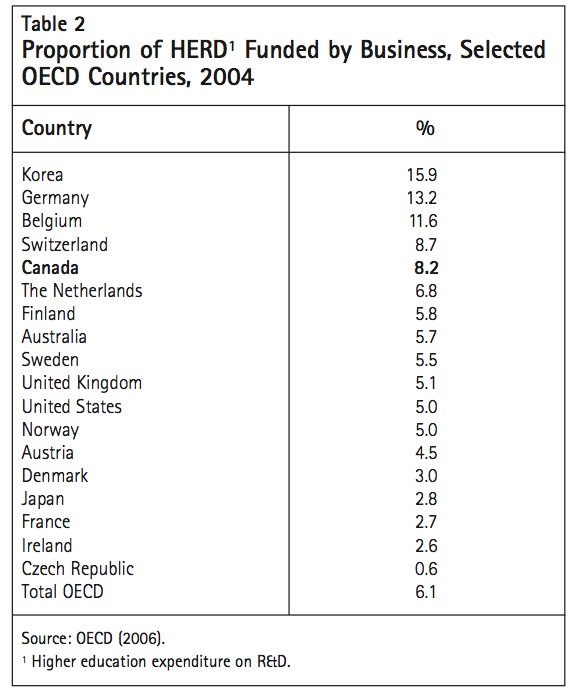

Canada also ranks high in terms of business funding as a percentage of all academic research (table 2). In 2004, businesses funded 8.2 percent of university research (much of which takes the form of industryfunded contracts for specific academic projects). This proportion was the fifth-highest among OECD countries and was considerable larger than the proportions of its major trading partners (the United States, the United Kingdom, Japan, and France). One might expect that the fact that industry has a significant financial stake in university-performed research would indicate that technology transfer channels are well developed, but as I will show later, in Canada this is not necessarily the case.

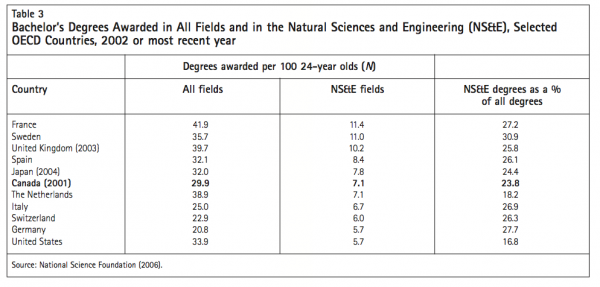

Canada has a fairly high ratio of university graduates in natural sciences and engineering (NS&E) There were 7.1 bachelor’s NS&E degrees awarded in Canada per 100 24-year-olds, more than in the United States and the sixth-highest among major industrialized nations (table 3).2 However, NS&E degrees account for only 23.8 percent of total degrees awarded in Canada. By this metric, Canada’s ranking falls to ninth. To the extent that technology is transferred to industry through the knowledge and training of NS&E graduates, Canada appears to be competitive internationally.

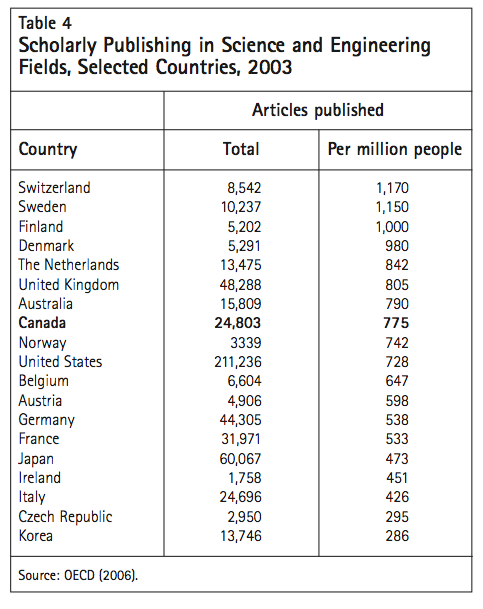

Canada also scores reasonably well in terms of scholarly publications per capita. In fact, it is eighth in the world on this indicator, ahead of the United States, Germany and France, but below Switzerland, Sweden and other Nordic nations (table 4). Publications are widely considered one of the most important channels of technology transfer, and here again Canada appears to perform respectably.

Finally, in the area of university spinoffs (a more direct indicator of commercially useful academic research), Canada lags behind the United States, which is often considered a model in terms of new firms founded on the basis of academic research. In its most recent survey of technology licensing, the Association of University Technology Managers (AUTM) reported that the 189 US universities that responded to their survey had launched 628 startups in 2005, an average of 3.3 startups per university (AUTM 2007a). In the comparable Canadian survey, the 34 universities that responded reported just 36 startup companies (AUTM 2007b).3

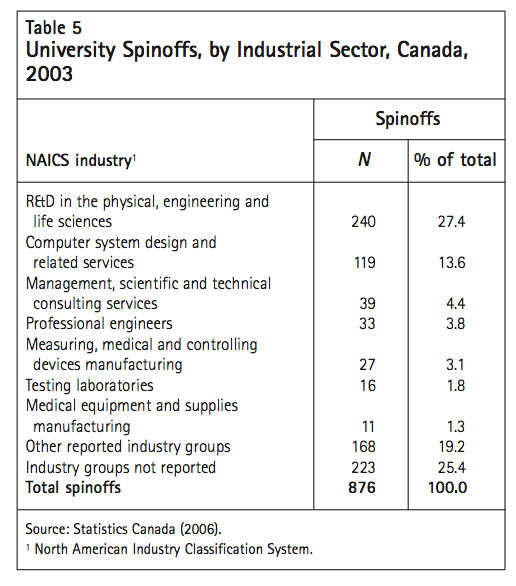

University spinoffs are highly concentrated in technical services fields. Forty-one percent of university spinoffs were in the scientific R&D services industry – most often related to biotechnology – and computer systems design. In terms of manufacturing, the most frequently reported spinoffs were in measuring, medical and controlling devices and medical equipment and supplies manufacturing, but taken together these account for under 5 percent of spinoffs (table 5).

This concentration is consistent with the evidence from other OECD nations: in the last 20 years these nations have witnessed a surge in the number of university patents, licences, academic spinoffs, and university-industry research corporations and collaboration, but this surge was generally concentrated in biotechnology, information technologies, and materials (Mowery et al. 2001).

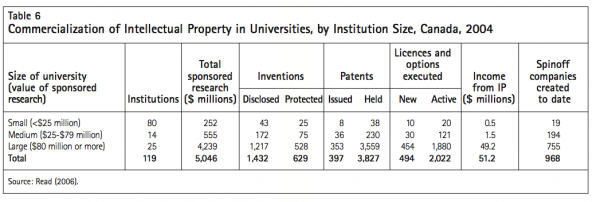

It is important to emphasize the fact that the vast majority of Canadian university technology comes from the largest research universities (table 6). These 25 institutions (defined as those with at least $80 million worth of sponsored research annually) account for 85 percent of all university inventions, over 90 percent of patents granted to universities, 95 percent of intellectual property royalties and 78 percent of spinoff companies. The relative concentration of university-developed technologies reduces the number of relationships that businesses must develop to access academic knowledge. At the same time, these elite institutions are located in 16 different census metropolitan areas, so the supply of university-developed technologies is well distributed across Canada.

Yet, in spite of its outstanding performance along many of these supply-side dimensions, Canada is host to a surprisingly low number of large high-technology and science-based companies. For instance, on the 2006 Fortune Global 500 list of the world’s largest corporations, only 13 are Canadian and of these only 3 are technology-intensive: Bombardier, Magna and Nortel. In Canada, many high-technology companies are created, but few of them reach a large size. This dampens the demand for university technology through all its channels.

Also, Canadian productivity has lagged in recent years, compared with both that in the past and that of the United States. In the 2000s, US productivity growth has accelerated relative to the 1990s to reach an average of 2.9 percent per year, while Canadian productivity growth decelerated sharply to just 1 percent annually. As a result, Canadian productivity levels (measured as GDP per hour worked) slipped from the 82-to-84-percent range in the 1990s to 74 percent by 2006 (Centre for the Study of Living Standards 2007). Large firms are much more productive than small ones (Gu and Tang 2004; Lee and Tang 2001), and Canada has a disproportionately high proportion of small firms. Thus, in spite of Canada’s high rank in the raw quantity of academic research, there is ample room for improvement with regard to its contribution to better business productivity and innovative products.

It is clear from the above that the supply side of academic research is reasonably healthy, particularly with regard to the financial resources devoted to university research. This is not surprising, because historically the policy and research focus has been almost exclusively on promoting and funding basic academic and government research. What is less healthy is the efficacy with which universitygenerated knowledge reaches the demand side – whether due to inadequate demand, bottlenecks in technology transfer or mismatches in supply and demand.

Some demand factors have been closely studied. Canada’s domestic market is relatively small compared with those of its major competitors, such as the United States, the European Union, Japan and, more recently, China. Its domestic market is scattered over 27 metropolitan areas in a very large territory, which affects transportation and communication costs, as well as the transmission of knowledge externalities among universities, public laboratories and business. These universities are located in such places as Halifax, Montreal, Ottawa, Toronto, Edmonton, Calgary, Vancouver, and Victoria. This large geographical spread has advantages – each large city has at least one university – and disadvantages – cooperation among universities is difficult.

Because industry is the main user of universitydeveloped technology, countries with high levels of business expenditures on R&D (BERD) should experience stronger demand for university technology than those with lower BERD intensity. Canada’s BERD intensity is relatively low compared with those of the largest OECD countries, and is lower than the OECD average (table 7), suggesting that industrial demand for academic knowledge in Canada is lower than it is in Canada’s main competitors, including the United States, Japan, Germany and France. Canada hosts many resource-intensive industries whose firms have low or medium R&D intensity, and this is one of the reasons for Canada’s poor aggregate performance.

However, ab Iorwerth (2005) compared the R&D intensity in specific industries in Canada and the United States and concluded that Canada’s lower BERD intensity is due mainly to lower R&D intensity in selected large industries (particularly automobile manufacturing and the service sector) as opposed to differences in industrial structure. Furthermore, key high-technology industries in Canada (such as pharmaceutical products and electronic equipment), while smaller in relative terms than their counterparts in the US, actually have higher R&D intensity. Contrary to conventional wisdom, there appear to be pockets of strength in potential demand for university-developed technologies.

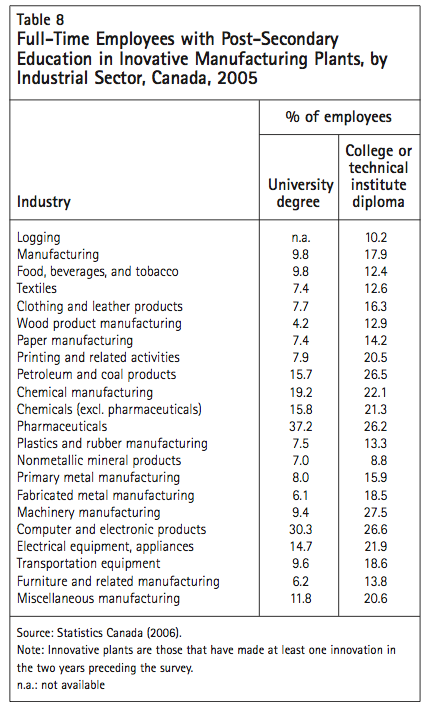

In a much-cited article, Cohen and Levinthal (1990) argued that firms’ ability to recognize the value of external information and apply it to commercial production depends on their absorptive capacity. Human capital is the base of absorptive capacity, and it is unevenly distributed among firms (Zahra and George 2002). In Canada, human capital is concentrated in pharmaceutical, computer and electrical equipment and appliances, chemicals and petroleum and coal products manufacturing (table 8). If the absorptive capacity literature is true, we should expect the demand for academic knowledge to be strongest in these industries.

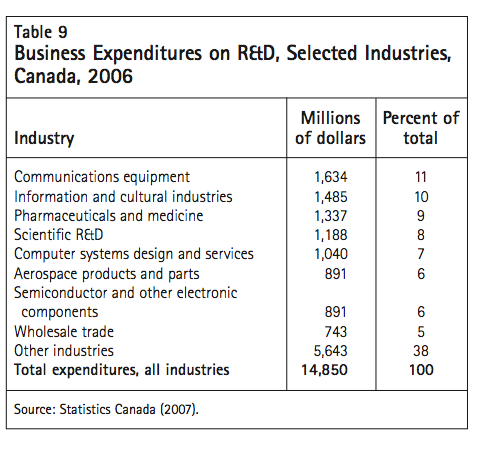

Except in the largest economies such as those of the United States, China and Japan, R&D is typically concentrated in a small number of industries (Archibugi and Pianta 1992). Canada’s R&D is no exception to this rule. Canadian BERD is concentrated in the information and communication technologies industries (communication equipment manufacturing, the information and cultural industries, computer systems design and services, and the semiconductor and other electronic components industries) as well as the medical products industries (pharmaceuticals and medicine and scientific R&D, particularly human health and biotechnology) and the aerospace products and parts industry (table 9). Industrial R&D is also highly concentrated at the firm level: just 100 companies accounted for over 56 percent of the $14.9 billion spent on industrial R&D in 2006 (Statistics Canada 2007). This highly skewed demand for technology is consistent with the fact noted earlier that only three Canadian companies are among the world’s largest technology firms.

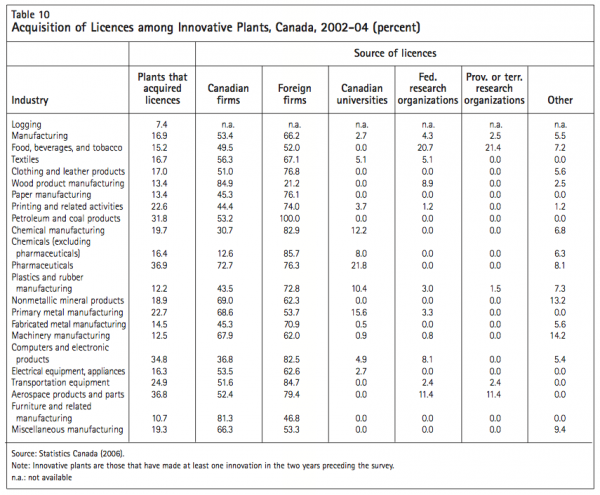

Perhaps most important, universities are not the only source of technology for companies. In fact, for Canadian firms, other domestic and foreign companies are a much more important source of technology than universities (table 10). The greatest users of licensed technology were the pharmaceuticals, computers and electronic products, petroleum and coal products, and transportation equipment (aerospace) industries. While companies in some industries (such as pharmaceuticals and primary metals manufacturing) do acquire technology from universities, they are far more likely to acquire it from other firms.

Surprisingly, the aerospace industry – which relies heavily on constant technology improvement – does not draw on universities at all for technology licensing. Aerospace companies in Canada conduct surprisingly little R&D and own few patents compared with their US and European competitors, thus reducing demand for university technology (Zhegu 2007).

Finally, innovation is more frequent in larger firms, and the tendency to collaborate with universities increases with the size of the firm (Hanel and St-Pierre 2006). Most industry-university collaborations involve firms of over 500 employees.

The evidence on the robustness of university technology demand is thus mixed. Canada’s poor performance with regard to BERD has long been documented and lamented, but there are pockets of strength in high-tech industries such as pharmaceuticals and electronic products. At the same time, most Canadian firms turn to other companies for licensed technology – circumstantial evidence that they are not finding the technologies they need in universities.

The fact that universities play such a marginal role in technology licensing in Canada demands a closer look at the mechanics of universityindustry technology transfer.

In most Canadian universities, academic researchers must disclose all inventions they develop or discover that may have commercial potential to the university’s office of technology transfer (OTT) or university-industry liaison office (UILO). The OTT/UILO then evaluates it and decides whether the invention should be protected through patents, copyright (in the case of software), industrial design or other intellectual property legislation. If the OTT/UILO decides protection is needed, the inventor and the university then sign an agreement about the division of the eventual royalties. The OTT/UILO then proceeds to look for potential licensees. If it decides that the invention is not worth protecting, full rights of commercialization are returned to the inventor, who then has entire freedom to commercialize it.

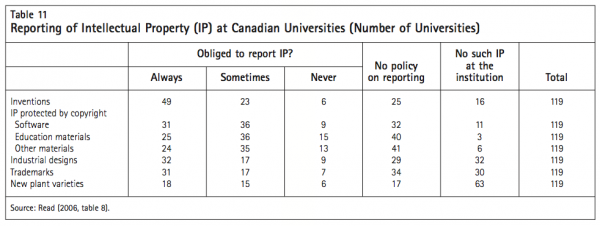

A major difference between the US and Canada is that in the US, university-produced innovations belong exclusively to the university, while in Canada each university has its own rules. There is a trend in Canada toward compulsory disclosure and eventual retrocession of the innovation to the inventor, who could patent or offer the technology to a company. In less than half of Canada’s universities, inventions must always be reported (table 11).

The innovation, whether owned by the academic or by the university, can be licensed to a private company, large or small. In many cases, however, the innovation is produced by the academic under contract with a firm,with the condition that the invention will belong to that firm, and cannot be disclosed or become property of the university.

Under this system, the entire responsibility of locating a potential user of any given innovation falls upon either the OTT/UILO or the researcher – essentially a supply-push model. Yet, evidence suggests that neither is entirely equipped to assess the commercial value of the technology or its potential market. In Canada, the European Union and the US, a large percentage of the patents where academics are the inventors belong to private firms or to the researchers themselves. In several cases, these discoveries were returned to the inventors by the academic institutions. Most OTTs/UILOs are staffed by just a handful of individuals, who simply cannot be expected to stay on top of all potential markets for the inventions that come across their desks. I will suggest later that increasing the demand for university technology, particularly among SMEs, through incentives to seek out universitydeveloped research – a demand-pull model – is a far better way to promote academic technology commercialization. These incentives may substantially help address bottlenecks, match suppliers with demanders and move more university-developed technologies across the valley of death.

In the United States, the Bayh-Dole Act of 1980 represents a landmark in terms of legislative efforts to stimulate the transfer of university-developed technology to industry. It was motivated by the fact that the US government held tens of thousands of patents stemming from its funding of R&D in universities and government laboratories. However, only a tiny proportion of these were commercially licensed, reflecting the fact that governments are not primarily in the business of technology commercialization.

To increase the incentive to commercialize publicly funded R&D, the Act transfers ownership of an invention or discovery from the government agency that helped to pay for it to the academic institution that carried out the actual research. Furthermore, it ensures that the researchers themselves receive a portion of the economic benefits resulting from it. Over the course of time, other jurisdictions have adopted similar legislation; for example, Germany passed such legislation in 2001 and, in Canada, Quebec passed a similar law in 2002.

Evidence on the effectiveness of the Bayh-Dole Act is mixed. The Expert Panel on Commercialization concluded that it was directly responsible for the creation of thousands of new firms and added tens of billions of dollars to the US economy (2006). But an earlier study of Stanford, MIT and Columbia found very little change in these universities’ patent and licensing portfolios in the 10 years following the passage of the Bayh-Dole Act, and concluded that the Act had little, if any, effect on technology transfer (Mowery et al. 2001).

Irrespective of the magnitude of economic benefits from the Bayh-Dole Act and similar legislation, there is concern in some quarters that the incentives they contain encourage undue commercial influence on the direction of academic research. Many scientists, economists and lawyers believe such incentives distort the fundamental mission of universities, diverting them from the pursuit of basic knowledge, which is freely disseminated, to a focused search for results that have practical and industrial purposes.

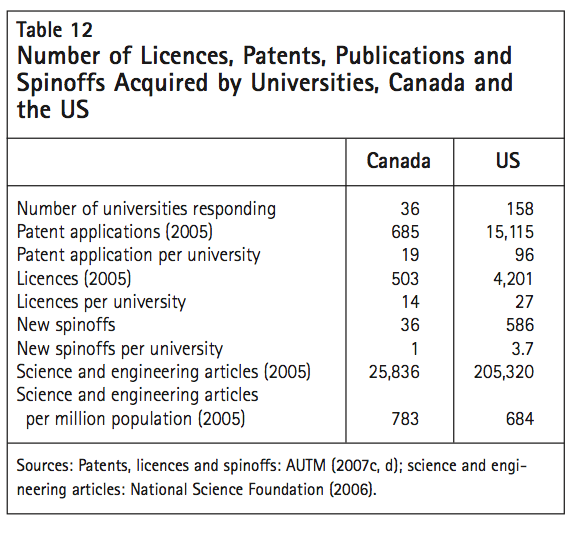

Finally, according to the AUTM surveys, American and Canadian university academic publication rates are similar, controlling for the size of the two countries and the research funds available to academics in the two nations (AUTM 2007a,b). At the same time, wide differences persist among universities in the two countries’ ability to patent, license and create spinoff companies (table 12). It may be that the differences in the experience and the quality of their OTT/UILO personnel, organizational structures, and financial resources, as well as differences in university cultures, explain some of the wide variations among universities (Rothaermel, Agung and Jiang 2007). Lotka’s Law4 may also explain the wide variations: over 60 percent of academic publishing is accounted for by less than 6 percent of academics. It may be that the same law applies to university patenting. Some universities have been able to attract highly productive and entrepreneurial academics who make a difference in the institutions.5

It may be that the rapid increase academic patenting and licensing in both countries since 1990 is due not to the legislative environment, but to the rise of biotechnology, a discipline that reinforces pharmaceutical research and is responsible for over 50 percent of all patents, licences, income and spinoff companies in the two countries (Mowery et al. 2001).

When analyzing the supply of university technology, one has to bear in mind that in Canada the majority of the patents stemming from academic research in the top universities are assigned not to the university but to private firms (Gingras et al. 2004). The figures are similar in Europe (Crespi, Geuna and Verspagen 2006; Geuna and Nesta 2006; Saragossi and van Pottelsberghe de la Potterie 2003). In sharp contrast, over 62 percent of the patents invented by faculty members at the top US research universities were assigned to the institutions, and only 26 percent solely to firms. These figures are important because they show that some technology transfer goes unnoticed because attention is focused on technology owned by universities and transferred to industries, ignoring the submerged part of the iceberg of technologies that are appealing to industry but are either produced under contract by academics or not patented by universities. Even at the famous Massachusetts Institute of Technology, patenting and licensing represent less than 10 percent of all technology transferred from its laboratories (Agrawal and Henderson 2002).

According to Thursby, Fuller and Thursby (2007), patents in the physical and engineering sciences were more often assigned to firms, while those in the biological sciences were more likely to be assigned to universities. Another, similar, study found that 33 percent of the university-invented patents were assigned to firms (Markman, Gianodis and Phan 2006). In both cases, Bayh-Dole and university regulations were bypassed. This is due to the fact that most academic research that results in patents is supported by contract research, not by public funds, and the inventors assign the research results to their sponsors, not to their universities.

Since most university research in Canada is not patented and licensed by universities, the incentives in Bayh-Dole-type legislation would not capture some key channels of technology transfer from universities to industry. The creators of Bayh-Dole could not have foreseen all the possible channels of technology transfer, such as technologies that that universities do not patent but that nevertheless attract business enterprises, mostly large ones. Canadian surveys of innovation show that large companies have many more links with universities than do small companies. Yet, there are more than a million small companies in Canada. Increases in Canadian productivity is more likely to come from smaller companies than from larger ones (Terajima, Leung and Marsh 2006)

Despite the fact that there are many influential proponents of Canada adopting the equivalent of the BayhDole Act (including the 1999 report of the Advisory Council on Canadian Science and Technology), it would be unwise to do so. The economic benefits of such legislation would likely be very small, and it would have virtually no effect on the large amount of academic research that is contracted directly by industry.

The fundamental challenge of crossing the valley of death is that it is exceedingly difficult to coordinate the myriad research activities in universities with the everchanging technology needs of industry (and, as noted above, excessive coordination may not be desirable). Thousands of academic papers are published annually in hundreds of journals and conference proceedings, and it is beyond the capacity of even the best-equipped university OTT/UILO to identify which inventions are most likely to have commercial potential.

A more promising option is to turn the equation around: businesses are much better equipped to judge the commercial potential of university research, but they are unwilling to shoulder the financial risk of carrying it out. This is particularly true of SMEs. The social benefits of encouraging businesses to do so are potentially large and would justify government support.

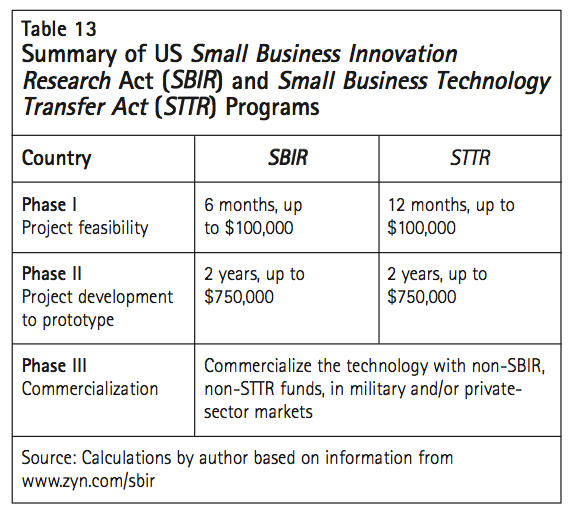

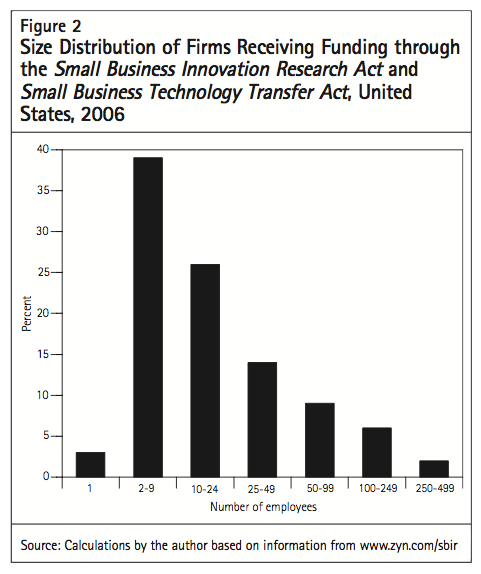

The United States has been innovative compared with other countries in this regard. In 1982, the United States passed the Small Business Innovation Research Act (SBIR) in order to facilitate the absorption of new technology by small and medium-sized enterprises, and in 1992 it passed the Small Business Technology Transfer Research Act (STTR). The SBIR provides up to $850,000 in early-stage R&D to small technology companies or to entrepreneurs who launch a company. The STTR program provides up to a similar sum to small companies working in cooperation with academic researchers at universities or government researchers in public laboratories, in order to explore the commercial feasibility of new ideas emerging from these institutions. The different federal departments that allocate R&D funds to private firms, the most important of which is the Department of Defense, run both programs. In fiscal year 2007, all departments combined, SBIR was funded at US$1.14 billion and STTR at $131 million. In order to qualify for SBIR grants, firms must have fewer than 500 employees and conduct R&D in the United States. In addition, the principal investigator has to work at least half time in the proposing firm. The STTR grants have similar firm-size requirements, but the principal investigator may be employed at either the firm or the research institution. Also, the SME has to be more than 50 percent owned by its managers and/or employees. This prerequisite creates obstacles for companies already financed by venture capital, but has the advantage of concentrating funds in the early stages of technology development. Thus, SBIR and STTR appear as secondto third-stage funds (see figure 1). The programs have three phases (table 13). Small businesses compete in phase I, and at this stage the grant is allocated after peer review of the technology. If phase I achieves promising results, then a second grant is awarded to the firm. Phase III is the commercialization stage, where no SBIR funds are committed. Phase II finishers are supposed to obtain either private or other public funds to continue the R&D process. Also, in fiscal year 2006, over 90 percent of the awardees were firms with fewer than 100 employees (see figure 2). This means that the program, which is aimed at small firms, is reaching its intended target.

SBIR and STTR programs have helped thousands of innovative firms to explore the technical merit of new ideas or technologies, which typically emerge from academic or public laboratory research, by reducing the cost of exploration and conversion of scientific ideas into commercial products (Auerswald and Branscomb 2003; Wessner 1999). An evaluation of SBIR conducted in 2006, while criticizing some of its management routines (and suggesting ways the program could be improved), concluded that it was attaining most of its specific missions (RAND Corporation 2006).

Another American initiative is the Advanced Technology Program (ATP). In 1990, the US Congress created ATP in the US National Institute of Standards and Technology (NIST), part of the Department of Commerce, in order to help US businesses commercialize generic technologies and refine manufacturing methods.6 Companies, or consortia of companies, propose research projects to NIST, and the agency selects the proposals considered to have the largest economic potential. Government and industry share the costs of early-stage technology development. Universities can participate in consortia and propose projects but, significantly, they cannot serve as project leaders.

ATP is more of a demand-pull program with regard to early-stage technologies: the research priorities in funded projects are set by industry, not by the government, academia or public laboratories. Partner companies must pay at least 50 percent of the project costs. ATP funding eligibility is not confined to SMEs; large corporations may also participate, but they must cover at least 60 percent of the costs of the project. The program does not cover product development. Also, like SBIR and STTR, it is not a substitute for tax credits for R&D or venture capital; but smaller companies often do not have any taxable income to benefit from tax credits. Thus, ATP helps emerging companies to explore new technologies in partnership with academic or government researchers. Out of 768 ATP awards granted between 1990 and September 2004, 508 (66 percent) went to small businesses, either as single applicants or leading joint ventures. In this period, ATP committed US$2.2 billion, and private companies committed a similar amount, for an average award of $3 million and 55 awards per year.7

In its 2001 report, the US National Research Council concluded that ATP is a successful program for bringing early-stage technologies to commercial fruition. The council suggested several operational improvements, such as reducing the delays between applications and awards, concentrating on selected areas of science and technology and stabilizing R&D funding (Wessner and STEP 2001).

Programs such as these are an interesting solution to the technology transfer conundrum: a bridge over the valley of death. They can also provide some support to help small firms grow. While it is true that Canada has one of the highest ratios of venture capital to GDP (Baygan 2003), that venture capital is concentrated in the early stages of funding (seed capital). Thus it is spread more thinly and supports more companies than

US venture capital does, and it encourages the proliferation of very small enterprises. Consider the situation of biotechnology, the industry that receives the majority of technologies transferred from universities. In 2005, Canada had over 500 dedicated biotechnology firms (DBFs). This compared with 1,500 in the United States, which has an economy over 10 times larger than Canada’s. Canadian DBFs often live or die with one technology. Introduced in Canada, programs like the American ones described here mght serve to consolidate smaller firms into larger and more viable entities.

Mohnen and Röller (2005) have shown that innovation policies often complement each other: some reinforce the supply of human capital and the production of technology, while others nurture the adoption of technology and the demand for human capital. From the foregoing analysis, it is clear that Canada has much room for improvement in terms of stimulating the demand for university technology. The Industrial Research Assistance Program (IRAP), under the auspices of the National Research Council, is the main vehicle for supporting SME business innovation. IRAP provides four main services: advice, financial support for R&D activities, networking and partnerships. Its total annual budget is about $150 million, of which just under 50 percent is earmarked for R&D activities.

IRAP is generally well regarded, and displays some characteristics of demand-pull technology transfer. It has been evaluated several times and has always obtained high marks (Lipsey and Carlaw 1998). In a study that compared the effectiveness of IRAP and venture capital in stimulating university spinoffs, Niosi (2006) found that IRAP funding was more often linked to rapid growth than is private venture capital. Its funding should be increased.

The SME Partnerships Initiative, proposed by the Expert Panel on Commercialization, would be a commercialization superfund to address SMEs’ commercialization challenges, to expand federal programs that support seed and start-up firms in proving their business ideas, and to increase research funds to SMEs to augment and improve technology transfer to smaller firms. It would differ from the STTR/SBIR programs in one critical respect. Under the American programs, the firms themselves undertake initiatives and applications, and decide which technologies deserve further exploration. Under the proposed SME

Partnerships Initiative, government laboratories and universities would determine the commercial application of their technologies and compete for the funds disbursed by the Canadian SME Partnerships Initiative. Once funds are allocated to universities and government labs, they would then choose their business sector partners, to whom they would transfer funds for feasibility studies and prototype development.

But channelling technology transfer funds through universities or public research labs is not the best way to commercialize research results. Firms are better equipped to judge the commercial potential of technologies developed in the universities, and they should play a central role in identifying those that are worthy of support. The SME Partnerships Initiative proposal clearly would not permit this.

On the supply side, even if Canadian performance is widely considered satisfactory, there is room for improvement. It has repeatedly been suggested that the development of TTOs/UILOs in universities would help the commercialization of academic research, and that governments should subsidize their growth.8 Although they have existed across Canada since the late 1980s, compared with those in the US, they are understaffed and underfunded. Additional funding would help them to better tackle the complex technical, legal, administrative and economic dimensions of technology transfer.

For a more balanced national system of innovation, policy-makers in Canada should focus on demand-pull policies that encourage businesses to participate more directly in research funding decisions that impinge on university research directions, without going so far as to dictate their specifics. This would be the most effective way to support the commercialization process. University professors are primarily motivated by the attraction of publishing, but knowing that businesses are interested in what goes on in their labs may influence the broad research directions they take, without compromising the integrity and independence of individual projects.

Demand-pull policies are much better developed in the United States than they are in Canada. Although they would be costly to fund and complex to implement in Canada, programs like ATP, SBIR and STTR could increase demand among SMEs for academic and government laboratory technology. These programs have helped thousands of innovative SMEs to explore the technical merit of a new idea or technology, typically one emerging from academia or a public laboratory (Auerswald and Branscomb, 2003; Wessner, 1999). Some demand-side policies would thus help increase the absorptive capacity of high-technology industries, which in Canada mostly consist of small firms.

Canada does not need Bayh-Dole-type legislation. It is far from certain that the Bayh-Dole Act has improved the performance of university-industry linkages in the United States. If the US academic system performs on average better than those of other countries, this may be due to a combination of internal and external factors, including high levels of public funding for academic research, a system based on global recruitment of professors and students, a very active venture capital industry supporting university startups, large internal national and regional markets, and policies stimulating the exploration of public technologies by SMEs. Also, legislating patents, spinoffs and licences would only affect a few of the numerous channels of university-industry technology transfer, without even eliminating the assignment of intellectual property generated by academics to their industrial partners through contractual research and IP protection of all the inventions disclosed by academics.

Canada should, however, establish a program similar to ATP, SBIR or STTR, which would fund the exploration by SMEs of technology produced in public laboratories, and in universities under public funds. Given its excellent track record, a pilot program within IRAP would be a welcome addition to the incentives for firms to use university and public sector innovation, as well as a complement to the different tools IRAP uses to promote technological innovation in Canadian industry. Later on, after due evaluation, the program could eventually be extended to other public departments that subsidize industrial research, as the American government did with SBIR and STTR.

Canada has more SMEs than most other OECD nations. Its sluggish productivity record in the last 20 years is almost certainly related to the slow adoption by SMEs of advanced technology. A coordinated program to increase the demand for innovative technology among these firms and linking them to frontier academic research will certainly have an impact on their productivity, allowing them to become the global technology powerhouses of tomorrow.

ab Iorwerth, A. 2005. “Canada’s Low Business R&D Intensity: The Role of Industry Composition.” Finance Canada working paper 2005-03.

Advisory Council on Science and Technology. 1999. “Public Investments in University Research: Reaping the Benefits.” Report of the Expert Panel on the Commercialization of University Research, Chair, Pierre Fortier. Accessed March 17, 2008. https://acst- ccst.gc.ca/comm/rpaper_html/report_toc_e.html

Agrawal, A., and R. Henderson. 2002. “Putting Patents in Context: Exploring Knowledge Transfer from MIT.” Management Science 48 (1): 44-60.

Archibugi, D., and M. Pianta. 1992. “Specialization and Size of Technological Activities in Industrial Countries: The Analysis of the Patent Data.” Research Policy 21: 79-93.

Association of University Technology Managers (AUTM) 2007a. “U.S. Licensing Activity Survey: FY2006. A Survey of Technology Licensing (and Related) Activity for US Academic and Non-profit Institutions and Technology Investment Firms.” Northbrook, Illinois. Accessed June 9, 2008. https://www.autm.net/events/ file/AUTM_06_ US%20LSS_FNL.p

_____. 2007b. “Canadian Licensing Activity Survey: FY2006. A Survey of Technology Licensing (and Related) Performance for Canadian Academic and Non-profit Institutions and technology Investment Firms, 2006.” Northbrook, Illinois. Accessed March 17, 2008. https://www.autm.net/ events/File/AUTM_06_LS_ Canada_FNL.pdf

_____. 2007c. “U.S. Licensing Activity Survey: FY2005. A Survey of Technology Licensing (and Related) Activity for US Academic and Non-profit Institutions and Technology Investment Firms.” Northbrook, Illinois. Accessed June 9, 2008. https://www.autm.net/events/ File/US_LS_05Final(1).pdf

_____. 2007d. “Canadian Licensing Activity Survey: FY2005. A Survey of Technology Licensing (and Related) Activity for Canadian Academic and Non- profit Institutions and Technology Investment Firms.” Northbrook, Illinois. Accessed June 9, 2008. https://www.autm.net/events/File/05_CanadaFINAL.pdf

Auerswald, P. E., and L. Branscomb. 2003. “Valleys of Death and Darwinian Seas: Financing the Invention to Innovation Transition in the United States.” Journal of Technology Transfer 28 (3-4): 227-40.

Baygan, G. 2003. “Venture Capital Policy Review in Canada.” OECD Science, Technology and Industry Working Paper 2003/4. Paris.

Brennenraedts, R., R. Bekkers, and B. Verspagen. 2006. “The Different Channels of University-Industry Technology Transfer: Empirical Evidence from Biomedical Engineering.” Working paper 06-04, Eindhoven Centre for Innovation Studies, The Netherlands.

Centre for the Study of Living Standards. 2007. “Aggregate Income and Productivity Trends: Canada versus United States.” Ottawa. Accessed March 18, 2008. https://www.csls.ca/data/iptjune2007.pdf

Cohen, W., and D. A. Levinthal.1990. “Absorptive Capacity: A New Perspective on Learning and Innovation.” Administrative Science Quarterly 35 (1): 128-52. Cohen, W., R. R. Nelson, and J. P. Walsh. 2002. “Links and Impacts: The Influence of Public Research on Industrial R&D.” Management Science 48 (1): 1-23.

Crespi, G. A., A. Geuna, and B. Verspagen. 2006. “University IPRS and Knowledge Transfer: Is the IPR Ownership Model More Efficient?” SPRU Electronic Working paper 154, Science and Technology Policy Research, University of Sussex.

Expert Panel on Commercialization. 2006. People and Excellence: The Heart of Successful Commercialization. Final report. 2 vols. Ottawa: Industry Canada. Accessed March 18, 2008. https://strategis.ic.gc.ca/epic/site/ epc-gdc.nsf/en/h_tq00013e.html

Geuna, A., and L. Nesta. 2006. “University Patenting and its Effects on Academic Research: The Emerging European Evidence.” Research Policy 35: 790-807.

Gingras, Y., J. Niosi, J. Cocco, and V. Larivière. 2004. “La prise des brevets au sein des universités canadiennes: la propriété intellectuelle et le bien commun.” Presentation to the annual meeting of ACFAS, Montreal.

Gu, W., and J. Tang. 2004. “Link between Innovation and Productivity in Canadian Manufacturing Industries.” Economics Of Innovation and New Technology 13 (7): 671-86.

Hanel, P., and M. St.-Pierre. 2006. “University-Industry Collaboration by Canadian Manufacturing Firms.” The Journal of Technology Transfer 31 (4): 485-99.

Heher, A. 2006. “Return on Investment from Innovation: Implications for Institutions and National Agencies.” Journal of Technology Transfer 31 (4): 403-14.

Jacob, M., M. Lundqvist, and H. Hellsmark. 2003. “Entrepreneurial Transformations in the Swedish University System: The Case of Chalmers University of Technology.” Research Policy 32: 1555-68.

Jaffe, A. 1989. “Real Effects of Academic Research.” The American Economic Review 79 (5): 957-70.

Lau, L. 1996. “The Sources of Long-Term Economic Growth: Observations from the Experience of Developed and Developing Countries.” In The Mosaic of Economic Growth, edited by R. Landau, T. Taylor, and G. Wright. Stanford: Stanford University Press.

Lee, F. C., and J. Tang. 2001. “Multifactor Productivity Disparity between Canadian and US Manufacturing Firms.” Journal of Productivity Analysis 15: 115-28.

Lim, Y. 1999. Technology and Productivity. The Korean Way of Learning and Catching Up. Cambridge, MA: MIT Press.

Lipsey, R., and K. Carlaw, with a contribution by D. Akman. 1998. “A Structuralist Assessment of Technology Policies: Taking Schumpeter Seriously on Policy.” Working Paper 25. Industry Canada Research Publications Program, Industry Canada. Accessed March 27, 2008. https://www.ic.gc.ca/epic/site/eas-aes.nsf/en/ra01700e.html

Lundvall, B.-A. 1992, ed. National Systems of Innovation. London: Pinter.

Mansfield, E. 1995. “Academic Research Underlying Industrial Innovations: Sources, Characteristics and Financing.” The Review of Economics and Statistics 77 (1): 55-65.

Markman, G. D., P.T. Gianiodis, and P. H. Phan. 2006. “Full-Time Faculty or Part-Time Entrepreneurs?” Presentation to the annual meeting of the Technology Transfer Society, Atlanta, GA, September 27-29.

Martin, F., and M. Trudeau. 1998. “L’impact économique de la recherche universitaire.” Dossier de recherche 2 (3).

Mohnen, P., and L. H. Röller. 2005. “Complementarities in Innovation Policy.” European Economic Review 49: 1431-50.

Mowery, D. C., R. R. Nelson, B.N. Sampat, and A. A. Ziedonis. 2001. “The Growth of Patenting and Licensing in US Universities: An Assessment of the Effects of the Bayh-Dole Act of 1980.” Research Policy 30: 99-120.

National Science Foundation. 2006. Science and Engineering Indicators. Washington, DC: National Science Board. Accessed June 9, 2008. https://www.nsf.gov/statistics/seind06/pdfstart.htm

Nelson, R. R., ed. 1993. National Innovation Systems. New York: Oxford University Press.

Niosi, J. 2000a. Canada’s National System of Innovation. Montreal and Kingston: McGill-Queen’s University Press.

_____. 2000b. “Science-Based Industries: A New Schumpeterian Taxonomy.” Technology in Society 22: 429-44.

_____. 2002. “National Systems of Innovation Are X-Efficient (and X-Effective). Why Some Are Slow Learners” Research Policy 31 (2): 291-302.

_____. 2006 “Success Factors In Canadian Academic Spin-Offs.” Journal of Technology Transfer 31 (4): 451-57.

Niosi, J., B. Bellon, P. P. Saviotti, and M. Crow. 1993. “National Systems of Innovation: In Search of a Workable Concept.” Technology in Society 15 (2): 207-27.

Organisation for Economic Co-operation and Development (OECD). 2006. Main Science and Technology Indicators, 2006/2. Paris.

O’Shea, R. P., T. J. Allen, K. P. Morse, C. O’Gorman, and F. Roche (2007): “Delineating the Anatomy of the Entrepreneurial University: The MIT Experience.” R&D Management 37 (1): 1-16.

Pianta, M. 1995. “Technology and Growth in OECD Countries, 1970-1990.” Cambridge Journal of Economics 19 (1): 175-87.

RAND Corporation. 2006. Evaluation and Recommendations for the Improvement of the Department of Defense Small Business Innovation (SBIR) Program. Santa Monica, CA: RAND Corporation.

Read, Cathy. 2006. Survey of Intellectual Property Commercialization in the Higher Education Sector, 2004. 2006. Statistics Canada Working Paper 011. Accessed April 1, 2008. https://www.statcan.ca/english/research/ 88F0006XIE/88F0006XIE2006011.pdf

Rosenberg, N. 1994. Exploring the Black Box: Technology, Economics and History. Cambridge, UK: University Press.

_____. 2004. Innovation and Economic Growth. Paris: OECD. Rothaermel, F. T., S. D. Agung, and L. Jiang. 2007. “University Entrepreneurship: A Taxonomy of the Literature.” Industrial and Corporate Change 16 (4): 691-791.

Saragossi, S., and B. van Pottelsberghe de la Potterie. 2003. “What Patent Data Reveal about Universities: The Case of Belgium.” Journal of Technology Transfer 28: 47-51.

Saviotti, P. P., and A. Pyka. 2004. “Economic Development by the Creation of New Sectors.” Journal of Evolutionary Economics, 14: 1-35.

Statistics Canada. 2006. “Survey of Innovation, 2002-2005.” Accessed April 1, 2008. https://www.statcan.ca/cgi-bin/imdb/p2SV.pl?Function=getSurvey&SDDS=4218&lan g=en&db=IMDB&dbg=f&adm=8&dis=2

Statistics Canada. 2007. Industrial Research and Development: Intentions 2006. Accessed February 28, 2008. https://www.statcan.ca/english/freepub/ 88-202-XIE/88-202-XIE2006000.pdf

Terajima, Y., D. Leung, and C. Meh. 2006. The Firm Size Distribution and Productivity Growth. Computing in Economics and Finance 2006, no. 167. Society for Computational Economics. Accessed April 1, 2008 https://comp-econ.org/

Thursby, J., A. Fuller, and M. Thursby. 2007. “US Faculty Patenting Inside and Outside the University.” NBER Working Paper 13256. National Bureau of Economic Research, Cambridge, MA. Accessed April 1, 2008., https://www.nber.org/papers/w13256

Wessner, C. W. 1999. The Small Business Innovation Research Program: Challenges and Opportunities. Washington, DC: National Academy Press.

Wessner, C. W., ed., and Board on Science, Technology and Economic Policy (STEP), National Research Council. 2001. The Advanced Technology Program: Assessing the Outcomes. Washington, DC: National Academies Press.

Zahra, S., and G. George. 2002. “Absorptive Capacity: A Review, Reconceptualization and Extension.” Academy of Management Review 27 (2): 185-203.

Zhegu, M. 2007. La co-évolution des industries et des systèmes d’innovation: l’industrie aéronautique. Ph.D. dissertation, Université du Québec à Montréal.

ATP advanced technology program

AUTM Association of University Technology Managers

BDC Business Development Bank of Canada

BERD business expenditure on R & D

CECR Centres of Excellence for Commercialization and Research

CIHR Canadian Institutes of Health Research higher education R & D

IRAP Industrial Research Assistance Program

NIST National Institute of Standards and Technology

NS & E natural sciences and enginerring

NSERC National Sciences and Enginerring Research Council

NSI national systems of innovation

OECD Organisation for Economic Co-operation and Development

OTT office of technology transfer

R & D research and development

SBIR small business innovation research

SME small and medium-sized enterprise

STTR small business technology transfer research

UILO university-industry liaison office

By almost every measure, Canada is one of the best countries in the world in which to live. Excellent health care, high-quality public education, well-functioning infrastructure systems, consistent economic growth and stable governance – no wonder so many other nations look with admiration at the quality of life we share in Canada. Nor is it a secret how we achieved our current status. Canada has advanced so far in a relatively short history because of careful, considered planning balanced against the pragmatic courage that characterizes societies like ours, built on the survival strategies of First Nations and the pioneering imagination and energy of immigrants.

As Jorge Niosi clearly outlines in “Connecting the Dots between University Research and Industrial Innovation,” Canada in 2008 has enormous knowledge resources, the capacity to produce innovative ideas and the desire to move forward. Yet, in spite of our current strengths, we are progressively falling behind our global economic competitors. In the most recent World Economic Forum Global Competitive Index, we slipped to thirteenth place in 2007-08, down one spot from the previous year (World Economic Forum 2007). In terms of our capacity for innovation, we now rank seventeenth in the world, behind the US and many East Asian and northern European nations.

Why are we slipping? We all aspire to a future in which Canada is a world leader in research, business, industry and the arts. We have spent a great deal of time pondering important questions: What is innovation? How can we promote it in Canada and increase our productivity? How can we position our innovations to compete in a changing global marketplace? In 2002, we created the Innovation Strategy; in 2006, the Expert Panel on Commercialization, of which I was a member, produced recommendations for improving commercialization (Expert Panel on Commercialization 2006); in October 2007, a new panel was struck to perform a competition policy review, now underway; and most recently, the Canadian government drafted its new Science Technology Strategy, laying out plans to stimulate technical innovations and train people to develop and use them.

It is clear that there is general acceptance that innovation, enterprise, productivity and competitiveness characterize an economic world leader. We have discussed, reviewed and proposed many strategies for moving forward, but now it is time to stop planning, be pragmatic and courageous, and act! If we look to our strengths and to the unique characteristics of Canada’s economic and research landscapes, we can use what we know, choose a strategy and put it to work. The key now is to move quickly.

Speed is becoming increasingly necessary. Global trends in research and development are emerging at a pace unknown in the past. Technical and scientific innovations are not innovations for long and an opportunity delayed is often an opportunity missed. In response, many corporations and industries are reducing their in-house R&D capacity and turning away from risky basic and applied scientific research toward fast-moving technology development.

Society’s need for basic research has not disappeared; indeed, it is the root cause of major discoveries that seed the technological innovations that change lives. As private sector R&D changes, it is increasingly critical that governments continue to support curiosity-driven research conducted at universities, which are able to provide the sophisticated infrastructure and expertise to conduct groundbreaking research while also assuming the high risks of such work.

At the same time, however, it is also vital that we develop efficient methods for translating the new knowledge generated at universities into usable products, processes and services. As major corporations and industry move away from in-house R&D, they need universities to help them develop ideas, innovations and inventions they can take to the marketplace. As a result, in countries around the world, new kinds of university-industry partnerships are quickly emerging.

Corporations are setting up laboratories close to major research universities in order to facilitate the speedy transfer of knowledge. Intel, for example, now has laboratories adjacent to the Universities of California, Washington and Cambridge, as well as Carnegie Mellon University. GlaxoSmithKline, BP, Exxon Mobil and Chevron have invested millions in integrated university-industry partnerships with major US research universities, creating frontline access to university expertise and innovations.1

As Niosi tells us, studies over the last two decades have shown that university research has a significant positive impact upon industrial innovation, and so the move to more highly integrated partnerships between universities and industry seems a promising strategy for promoting innovation (5). In spite of this promise, Canada, unlike the US, has been slow to move in this direction. The reasons for this are, as Niosi suggests, complex, and they arise from a combination of factors, such as our strong reliance upon “resource-intensive industries whose firms have low or medium R&D intensity,” and the existence of lower R&D intensity compared to our main G8 competitors “in selected large industries (particularly automobile manufacturing and the service sector)” (9). The fact that Canadians own very few large technology-intensive companies adds to the problem.

As Niosi suggests, given the scarcity of large Canadian firms, a focus on building university partnerships with major industrial firms, while important, can only take us so far. We must also pay particular attention to the potential for research partnerships with small and medium-sized enterprises (SMEs), which have fewer than 500 employees and are far more prevalent in Canada than large firms. This idea is not particularly new, but it has failed to gain widespread traction in the Canadian economic imagination and so still needs the analysis and explication that Niosi brings to bear in his study. Like many an innovative idea in this country, the idea that SMEs have a huge role to play in the commercialization of ideas and inventions seems to be in its own sort of “valley of death,” unable to bridge the gap between idea and action.

This failure to bridge the gap certainly is not indicative of an inability to recognize the problem. In fact, in the past two decades, a number of government initiatives designed to foster commercialization through partnerships between university research and SMEs have been put into place in Canada. We have the National Networks of Excellence, the National Research Council’s Industrial Research Assistance Program (IRAP), 4th pillar organizations, and the more recently established Centres of Excellence in Research and Commercialization. Small pockets of funding for early-stage commercialization have long been available through the tri-council funding agencies. In addition, provincial governments have acted; in Alberta, for example, Alberta Ingenuity has just launched the new Ingenuity Centres for Research and Commercialization program.

All of these programs have led, or promise to lead, to significant successes, but so far have failed to stimulate the widespread growth in innovation or the increases in productivity that Canada needs to effectively compete in the emerging global marketplace. When I served as a member of the six-person Expert Panel on Commercialization in 2005-06, we evaluated the programs that were then in existence, such as IRAP, 4th pillar organizations and programs in the tricouncil agencies. Each has strengths and weaknesses; each provides valuable insight into how we might move forward. Yet none, in itself, is the solution.

Part of the problem is that almost all our existing commercialization programs focus on the supply side of the commercialization process, putting the onus on universities and researchers to create or search for demand. But, as Niosi argues, “Firms are better equipped to judge the commercial potential of technologies developed in universities, and they should play a central role in identifying those that are worthy of support” (16). If we agree with this assessment – and the Expert Panel on Commercialization certainly did – the question that must be answered is this: How do we induce Canada’s numerous SMEs to play this role – to partner with universities in identifying the commercial potential of technical discoveries? It won’t be easy, because, as Niosi also notes, for most “Canadian firms, other domestic and foreign companies are a much more important source of technology than universities” (10).

To ascertain how we might make it happen, Niosi points us to the model offered by the US Small Business Administration’s Small Business Innovation Research program (SBIR), a model that I too believe is worth a closer look. If we agree that a new commercialization model is needed – and all the evidence suggests that we do – then we should consider the successes that the SBIR has had in creating the access to top-quality university-level research that entrepreneurs need to advance their business goals.

The SBIR illustrates how a national program can create opportunities for SMEs to engage in and take advantage of high-level basic and applied research. This program, introduced in 1982, has now weathered more than a quarter century of scrutiny and assessment, including a comprehensive review requested by the US Congress and conducted by the US National Research Council. According their recently released findings, the SBIR plays a significant role in both stimulating innovation and promoting the growth of SMEs,2 as well as effectively linking both public and private markets to high-level research3 and enabling the dissemination of knowledge through a variety of means, ranging from patents and licences to spinoff companies and human capital (Wessner 2008).4

The SBIR has the focus on the demand side of the commercialization process and the national mandate and breadth that Canadian programs have so far lacked. The US federal government’s Small Business Administration (SBA) administers the overall SBIR program by distributing funds through 11 US government funding agencies.5 Each agency solicits funding proposals from SMEs in response to very specific topics determined by agency needs. Thus, the proposals and research are directed to national priorities, and the economic feasibility of proposals and research is determined by the SMEs, which have the best knowledge of market needs.

Only SMEs located in the US are eligible to respond to solicitations. Proposing companies are strongly encouraged, though not required, to contract a university-based researcher to evaluate or conduct the basic research. Proposals are peer reviewed, to ensure relevance and quality, by program managers and their research teams working in the national laboratories of each agency.6

As Niosi outlines, winners of an SBIR award follow a three-phase process: phase I is proof of concept (six months, up to $100,000, deliverable is a more extensive research plan); phase II is development of prototype (two years, up to $750,000, deliverable is prototype); and phase III is unfunded government assistance in capitalizing the advancement of the project. Many SBIR winners do not compete for phase II or phase III as their innovations, based on a strong research plan or proof-of-concept document, are picked up by investors, venture capitalists, or large corporate licensees who are interested in seeing the concept developed and taken to market faster than the SBIR process allows.

SBIR succeeds in achieving three major commercialization objectives that we, in Canada, want to attain. First, it effectively links SMEs to the research community, with the SMEs, rather than universities, identifying technical and scientific innovations that have the greatest potential to respond to market demands. In this, the SBIR model shares important characteristics with the “open innovation” model emerging in large corporations across the world.7 Second, SBIR provides entrepreneurs and SMEs with a way to bridge the “valley of death,” which often prevents a concept from progressing from the prototype stage to product development. Third, when successful, the process leads to the development of new companies or the growth of established ones, the latter being of major concern in Canada.

To attain our objectives, there are important elements of the SBIR model that could be emulated. The recipients of an SBIR award can each play to their strengths. While the commercial aspects of the venture are handled by entrepreneurs with the right expertise, researchers are able to focus on their strengths and conduct research without distraction. The SBIR process provides the credibility of rigorous peer review – which validates the quality of the research plan while also controlling the entrepreneur’s risk in pursuing an innovative idea. Intellectual property rights are held by the SME with a royalty-free licence to the federal government in return for providing the initial funds. Last, but far from least, the SBIR puts the research and commercialization process on a clear and accountable timeline.

Is it possible for Canada to do the same? Can we put the commercialization process on a predictable, speedy timeline? Can we develop a standard national policy on intellectual property rights that will allow SMEs – or the larger organizations they may sell their innovations to – clear and defensible ownership of rights for ongoing development and international marketing purposes? Can we develop a commercialization model that will make the best use of peer reviewers from industry, university and government to evaluate proposals and select those that are most responsive to market demands and have the highest scientific merit and highest potential for success?

Although very successful in the US, the SBIR’s model cannot simply be cloned directly in Canada. We do not share the same kind of broad and diverse federal R&D structure through which funds can be distributed, and thus a model would need to be developed to suit Canada’s unique situation. The Expert Panel on Commercialization recommended that a business-led Commercialization Partnership Board be created to play both an advisory role to the Minister of Industry on identifying and setting national commercialization goals, and an oversight role on the development and implementation of commercialization policies, initiatives, investments and programs. Likewise, the Conference Board of Canada’s Leaders’ Roundtable on Commercialization proposed the creation of industryled collaborative research networks.

The emphasis in both of these proposals on industry leadership indicates that whatever administrative model we devise, it must have leadership from industry and business, and demand from them active participation in setting commercialization priorities and in evaluating specific projects’ commercial viability.

Tom Brzustowski, in his book The Way Ahead: Meeting Canada’s Productivity Challenge, suggests that all existing and new provincial and federal research and commercialization programs be operated within one umbrella system. This would require harmonization of general administrative policies, criteria and processes across provincial and federal barriers and among various funding programs, but it would still allow for the regional or disciplinary differences between them. Brzustowski admits that implementation of his proposal would be difficult, but it would not be impossible if leadership in government, universities and industry were committed to making it happen (Brzustowski 2008).

There is no doubt that the development of a Canadian solution will require strong and decisive action from industry and business, government and universities working together. It will require us to identify the areas and markets in which Canada has the greatest potential to be a global leader, and put into place government policies and programs that strategically promote investment and innovation in these areas of national interest and stimulate the innovation capacity and growth of Canada’s numerous SMEs.

If we can succeed, we will inject new energy for seeking discoveries and breakthroughs throughout all sectors of the Canadian economy, and we will connect the SME community to a larger vision driving innovation. We can break out of the endless planning cycle we seem to be caught in and reawaken the pragmatic courage that built this nation. We can create both a system for success and a mindset of success – a mindset that prompts us to be highly connected and highly competitive. That strategy must be unique to Canada – putting the pressure on us, first and foremost, to be innovative in designing a strategy that connects and serves all the players in the innovation game: government, industry, universities, researchers and entrepreneurs.

Brzustowski, T. 2008. The Way Ahead: Meeting Canada’s Productivity Challenge. Ottawa: University of Ottawa Press.

Expert Panel on Commercialization. 2006. People and Excellence: The Heart of Successful Commercialization. Final Report. 2 vols. Ottawa: Public Works and Government Services Canada.

Huston, L., and N. Sakkab. 2006. “Connect and Develop: Inside Procter & Gamble’s New Model for Innovation.” Harvard Business Review 84:58-66.