Redesigning Canadian Trade Policies for New Global’s Realities

Overview of the Research Findings

Stephen Tapp, Ari Van Assche and Robert Wolfe

Andrew Newcombe is an associate professor in the Faculty of Law at the University of Victoria. Before joining the University of Victoria in 2002, he worked in the international arbitration and public international law groups at Freshfields Bruckhaus Deringer LLP, in Paris. His research focuses on investment law and arbitration. He is associate editor of the ICSID Review, a contributor to the Investor-State Law Guide and Canadian treaty editor for Investment Claims. He is the co-author of Law and Practice of Investment Treaties: Standards of Treatment and co-editor of Sustainable Development in World Investment Law.

Redesigning Canadian Trade Policies for New Global Realities, edited by Stephen Tapp, Ari Van Assche and Robert Wolfe, is the sixth volume of The Art of the State. Thirty leading academics, government researchers, practitioners and stakeholders, from Canada and abroad, analyze how changes in global commerce, technology, and economic and geopolitical power are affecting Canada and its policy.

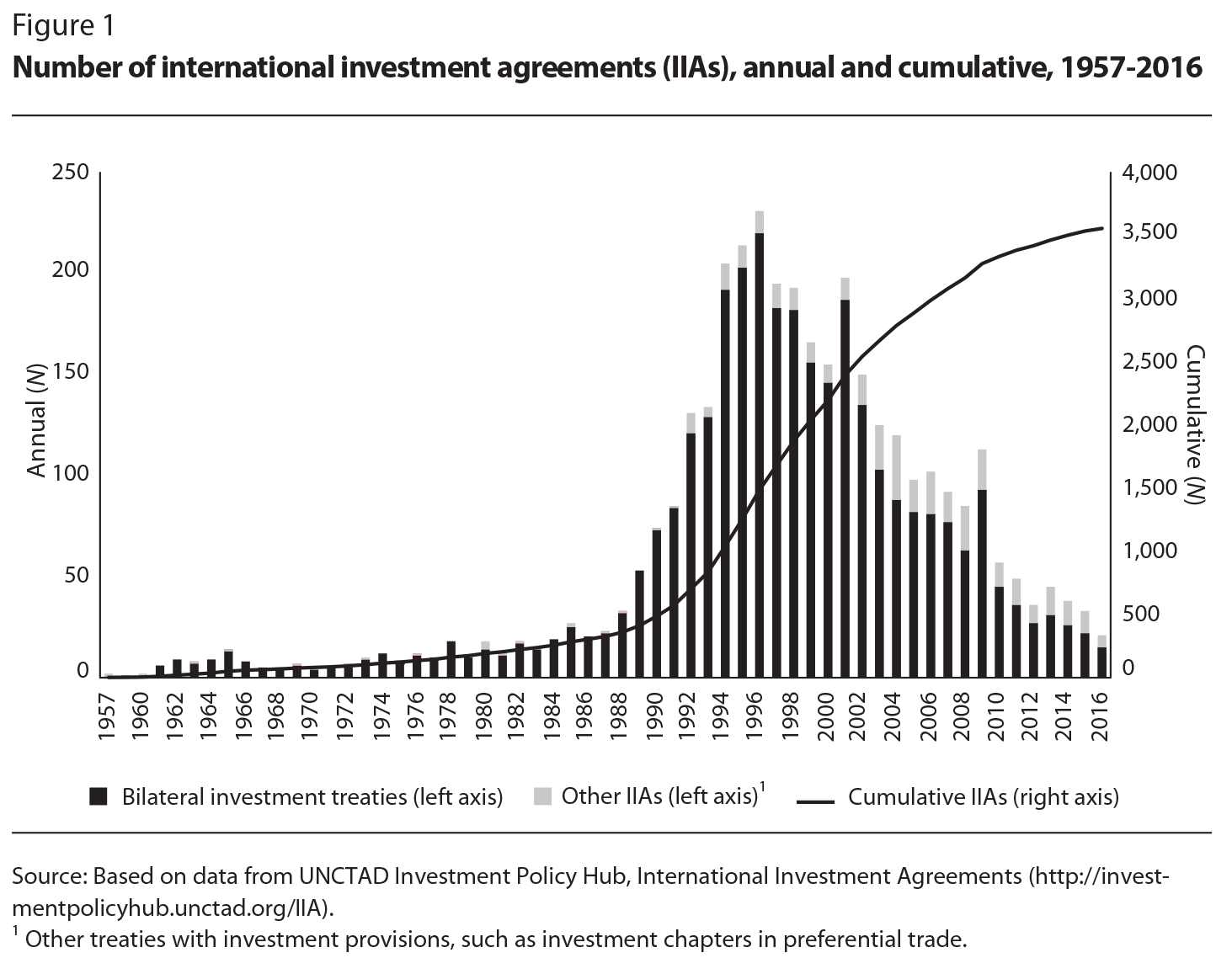

Foreign investment is central to the business strategies of many firms and to financing economic development projects in both developed and developing countries. Governments around the world have responded to the importance of promoting and protecting foreign investment by negotiating well over three thousand bilateral investment treaties (BITs) and other treaties with investment provisions, such as investment chapters in preferential trade agreements. Important and particularly controversial features of such agreements are the mechanisms for settling disputes between foreign investors and host countries — so-called investor-state dispute settlement (ISDS).

Why are investment agreements controversial? Advocates argue that, by requiring adherence to due process, respect for acquired rights and minimum standards of treatment, investment treaties can promote investment, the rule of law and good governance. But criticism of the international investment regime has increased sharply in recent years as the number of ISDS claims has grown, particularly because ISDS tribunals have broad powers to review host states’ laws and regulations — including potentially calling into question domestic policy decisions made by sovereign governments aimed at protecting human health and the environment — as well as powers to order states to pay damages to foreign investors if foreign investment commitments are violated.

A cause célèbre among those opposing the proliferation of BITs and investment provisions in preferential trade agreements — together referred to as international investment agreements (IIAs) — is the claims by cigarette manufacturer Philip Morris. In 2010 and 2011 the company argued that restrictive cigarette package labelling requirements imposed by Australia and Uruguay impaired the use of its iconic trademarks, notably the Marlboro brand, and that such requirements were inconsistent with investment protection standards. Even though ISDS tribunals rejected Philip Morris’ claims in both cases, critics highlight that IIAs provide foreign investors privileged access to ISDS and, unlike domestic investors, foreign investors are not required to litigate in domestic courts. Further, even if some controversial claims have been rejected, others have been upheld. According to critics, the potential for such lawsuits could have a chilling effect on domestic regulation and the lawsuits themselves can require that millions of dollars of public money be spent on legal fees and arbitration costs to defend public policy measures (although a tribunal can order the losing party to pay the winning party’s legal costs). Concern about ISDS has spread in developing countries, many of which are reviewing and renegotiating their IIAs. Some countries — for instance, Indonesia and South Africa — have announced that they will terminate their existing IIAs and instead enact domestic legislation on foreign investment promotion and protection.

Investment protection and ISDS have been particularly controversial aspects of the Canada-European Union Comprehensive Economic and Trade Agreement (CETA) and the Trans-Pacific Partnership (TPP) and of the negotiation of the Transatlantic Trade and Investment Partnership (TTIP) between the European Union and the United States. Indeed, in response to growing public concern, the EU suspended negotiations on ISDS in the TTIP and launched an unprecedented public consultation on investment protection and dispute settlement. Following this consultation, in September 2015, the European Commission proposed the new Investment Court System for the TTIP and other EU trade and investment negotiations. When the revised text of CETA was released in February 2016, its investment chapter was substantially amended to include the EU-inspired Investment Court System and other provisions designed to affirm the host state’s right to regulate in the public interest.1

Even with these changes, the investment chapter of CETA remains controversial. In early October 2016, due to Belgium’s unique constitutional system, the region of Wallonia initially blocked EU agreement to CETA. Shortly after talks between Canada and the EU collapsed, a compromise was reached that allowed Belgium to back CETA, and by the end of October, Canada and the EU had finally signed the CETA text. As part of the compromise, the text is accompanied by an interpretative statement to provide “a clear and unambiguous statement of…a number of CETA provisions that have been the object of public debate and concerns,” notably the investment provisions (Canada 2016c, preamble). Furthermore, unlike most of the treaty, the Investment Court System will not be applied provisionally, and the European Court of Justice will be asked to assess its compatibility with EU law. Even so, five of eight Belgian parliaments have indicated they do not plan to ratify CETA based on the current, updated text. It remains unclear whether CETA will be ratified and, if it is, whether the Investment Court System will be brought into force.

On the other side of the Atlantic, as President-Elect Donald Trump indicated, the United States will not ratify the TPP — which includes ISDS provisions and was signed in February 2016 by the 12 participating countries, including Canada and the United States.2 For its part, the Trudeau government has emphasized the need to promote Canada as a destination for inward foreign direct investment (FDI). In November 2016, the government announced plans to create the Invest in Canada Hub to attract global investment to Canada; to change the Investment Canada Act to encourage foreign investment; and to launch a new infrastructure bank to partner with investors and attract private sector capital to public infrastructure projects (Canada 2016b). Moreover, the Trudeau government now views CETA, with its recent amendments on investment provisions, as a “progressive trade agreement for a strong middle class,” emphasizing that the agreement could promote transatlantic investment and contribute to the Canadian economy (Canada 2016a).

With international investment law currently in a period of acute contestation and transformation, what should Canada do? First, it is important to recognize that investment treaty practice and policy have evolved significantly over the past decade and that Canada has been at the forefront of these developments. Canada should continue to play an important leadership role and make progressive changes to its investment promotion and protection agreements using the updated investment chapter in CETA as a model for future agreements.

Ultimately, the fundamental rationale for the IIA regime is to protect investments by adhering to and enforcing international standards. Canada has a systemic interest in supporting an international standard of ISDS that extends beyond any single agreement. Canada and other advanced economies cannot expect developing and emerging countries to accept the obligations in modern international investment agreements if they themselves are not willing to be bound by these same provisions. In terms of Canada’s experience to date with ISDS, it has globally been the sixth most frequent respondent state to claims, while Canadian investors have made the fifth most claims. In my view, Canada’s legal counsel and advisers have been quite successful in defending Canada against questionable claims. When viewed in the context of the stock of FDI in Canada, awards to date in favour of foreign investors represent a very small fraction (less than 0.025 percent) of those investments. Moreover, there is no systemic empirical evidence to demonstrate that ISDS rules have prevented Canadian policy-makers from regulating in the public interest.

More generally, the emergence of global value chains (GVCs) likely will require longer-term changes to the architecture of international investment law and, ultimately, a multilateral approach. However, even though a multilateral framework to replace the current regime of thousands of international investment agreements clearly would be more efficient and effective, this objective is best viewed as a long-term goal, rather than a short-term priority.

Multilateral legal frameworks to govern trade, monetary affairs and development financing were developed after the Second World War through the General Agreement on Tariffs and Trade (GATT) and the Bretton Woods agreements.3 Notably, however, no corresponding multilateral framework was developed to govern foreign investment. Between the 1950s and the 1970s, the process of decolonization and nationalist policies that emphasized economic independence dominated foreign investment law and policy. During this era many newly independent states looked at foreign investment and international regulation with suspicion. Nationalization of foreign investments and policies that promoted self-sufficiency and less dependence on foreign capital, such as import substitution, were common. In 1974, this general antipathy toward foreign investment culminated in the United Nations Declaration on the Establishment of a New International Economic Order and the Charter of Economic Rights and Duties of States, both of which affirmed the right of states to regulate foreign investment and rejected international standards in favour of individual state policies.

In the absence of a multilateral framework, and in light of political and legal disputes over the existence and application of international legal standards to foreign investment, capital-exporting countries began concluding bilateral -agreements with developing countries in order to promote and protect foreign investment. West Germany launched the era of BITs with an agreement with Pakistan in 1959, but it was not until 1969 that the first BIT appeared with a provision for investor-state arbitration, which has become the defining feature of the modern BIT. In the typical ISDS provision, the parties agree that any dispute regarding a breach of the BIT, including those claimed by a foreign investor, can be arbitrated before an international tribunal chosen by the parties. Typically, the tribunal comprises three arbitrators: one chosen by the claimant investor, one chosen by the respondent state and a chair or president chosen by agreement of the parties. Traditionally, foreign investors have favoured ISDS because it provides a neutral forum for dispute resolution that is not tied to the respondent state.

Beginning in the late 1980s, the ascendancy of Washington Consensus policies that favoured economic liberalism led to exponential growth in the number of international investment agreements (figure 1). For instance, in 1988, there were 360 BITs globally; one decade later, the number had grown more than five times to 1,875. The dominant view then was that, by providing enforceable legal standards of investment protection, BITs would stimulate foreign investment inflows — particularly in countries without a good record of providing foreign investors a stable and predictable investment climate — as the risk of investing would be mitigated by a commitment to the rule of law and independent and impartial courts.

A typical BIT signed in the 1990s was a 6-to-10-page legal document that combined the following:

Although nominally reciprocal in obligation, the earliest BITs were often between developed and developing countries, and the foreign investment was largely one-sided, with developed countries largely exporting capital to developing countries. The quid pro quo was that the host developing countries, by providing investment protection, would reduce the political risks of foreign investment and thereby promote investment flows. Most traditional BITs contained few explicit investment promotion obligations: investment promotion and increased FDI were often assumed to be by-products of investment protection (Salacuse and Sullivan 2005). Although BITs often developed in asymmetric contexts, more recent waves of these agreements have been concluded between developing countries, the number jumping from 42 in 1990 to 679 in 2006, representing 26 percent of all BITs by that date (UNCTAD 2007). These developments reflect the economic reality that developing countries increasingly are capital exporters, accounting for US$426 billion, or nearly one-third, of global FDI outflows in 2012 (UNCTAD 2013).

As of 2016, the international legal regime governing foreign investment consisted of more than 3,100 BITs, along with 370 other international agreements, such as preferential trade agreements that contain investment chapters (for example, the North American Free Trade Agreement, NAFTA), regional investment agreements (such as the Comprehensive Investment Agreement among members of the Association of Southeast Asian Nations, ASEAN) and sectoral agreements with investment provisions (such as the Energy Charter Treaty). The result of all of these investment agreements is a complex and overlapping international regime of investment protection. UNCTAD (2008) aptly summarizes the network of IIAs as

Three structural elements of IIAs reinforce the complexity of the regime. First, almost all IIAs contain MFN treatment provisions. ISDS tribunals have found that these clauses can entitle investors to more favourable treatment accorded in a host state’s other IIAs. When a host state has many BITs, the legal texts of which vary in myriad ways, there is significant legal complexity in determining the most favourable protections to which an investor might be entitled. Although the IIA regime comprises bilateral and regional treaties, broadly worded MFN treatment provisions effectively multilateralize investment treaty protections because, depending on the scope of the MFN clause, an investor might be entitled to the protections of the most investment-protective BIT provisions the host state has agreed to accord to other foreign investors and investments (Schill 2009).

Second, many investment treaties extend protection to foreign investors based on the investor’s place of incorporation. This allows investors to engage in “treaty shopping.” For example, even if Canada does not have a BIT with a potential host state but, say, the Netherlands does, a Canadian investor could establish a shell company in the Netherlands to be considered a Dutch investor and thereby obtain Dutch BIT protection.4 Investment treaty tribunals generally emphasize that there is nothing inherently wrong with treaty shopping; it is part of legitimate business planning, akin to establishing corporate operations in a country that provides favourable tax and regulatory treatment. Treaty shopping, however, can become abusive “forum shopping,” where the foreign investor restructures its investment in order to obtain IIA protection after a dispute has arisen.

Third, many treaties have very broad definitions of investment (including shares in a company) and cover investments made indirectly through third countries. As a result, under many BITs, minority shareholders who hold shares indirectly through a third country are entitled to the BIT’s protections. The effect is that a foreign investor might be able to rely on multiple BITs in a claim against a host country. If the foreign investment in question has a consortium of different foreign owners, additional IIAs might apply.

There is one additional “multilateral” aspect of the international investment regime. In light of the international community’s inability to agree on substantive standards of investment protection, a group of countries created the International Centre for Settlement of Investment Disputes (ICSID) under the auspices of the World Bank.5 Rather than seek agreement on substantive principles, ICSID focuses on process. According to Ibrahim Shihata, former secretary-general of ICSID and general counsel to the World Bank, ICSID provides “a forum for conflict resolution in a framework that carefully balances the interests and requirements of all the parties involved, and attempts in particular to ‘depoliticize’ the settlement of investment disputes” (1986, 4). ICSID is not a permanent arbitral tribunal; rather, it provides a legal and organizational framework for the arbitration of disputes between “Contracting States” and investors who qualify as nationals of other Contracting States.6

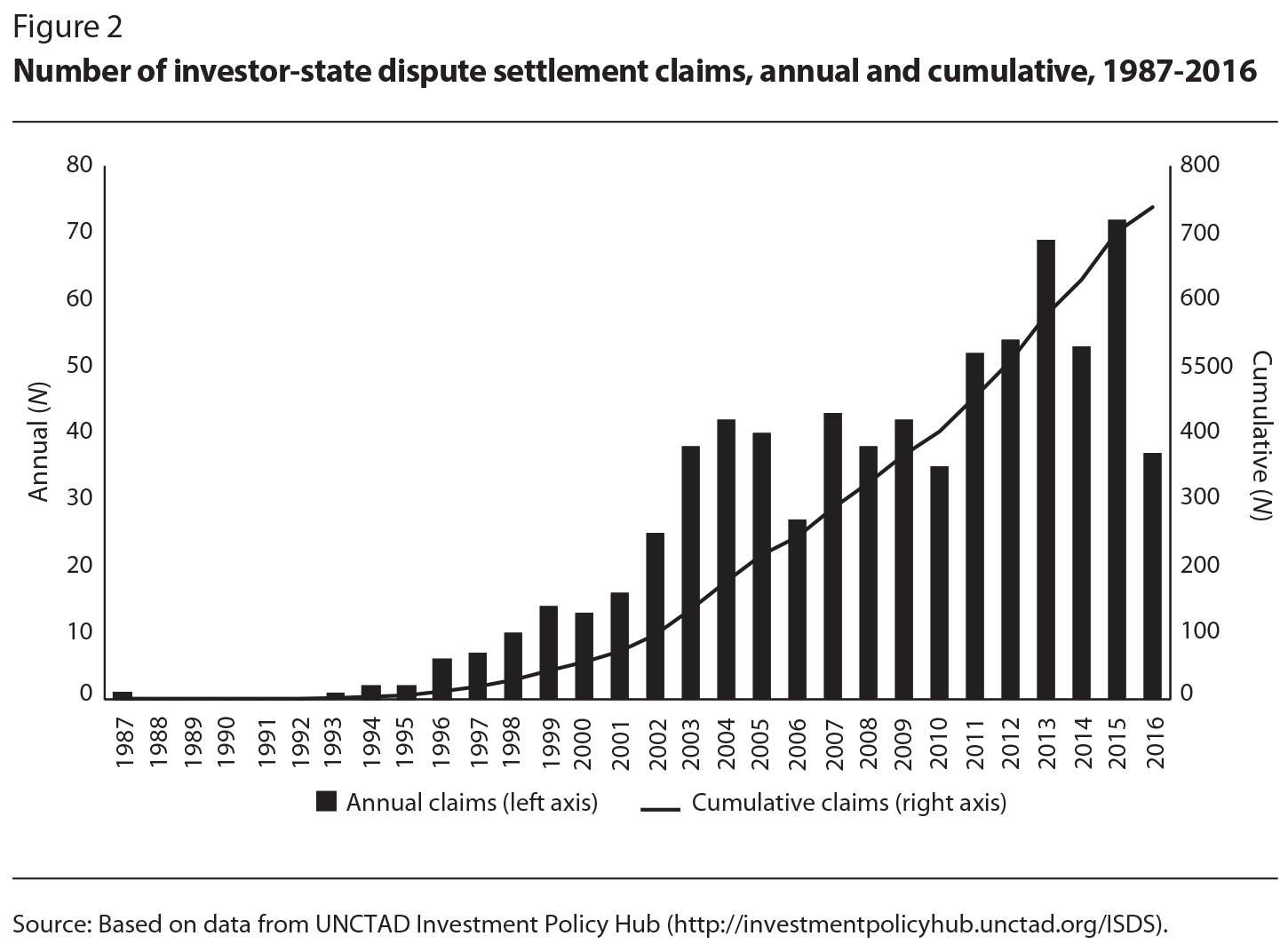

The proliferation of IIAs in the 1980s and 1990s was not accompanied by their immediate “activation” through ISDS claims. Although the first investment treaty award was made in 1990, it was not until the first claims arose under chapter 11 of NAFTA that the potential scope and impact of investment protections became a public policy concern in developed countries. Widespread criticism of the IIA regime first developed as a result of four controversial and high-profile investment treaty claims under NAFTA:

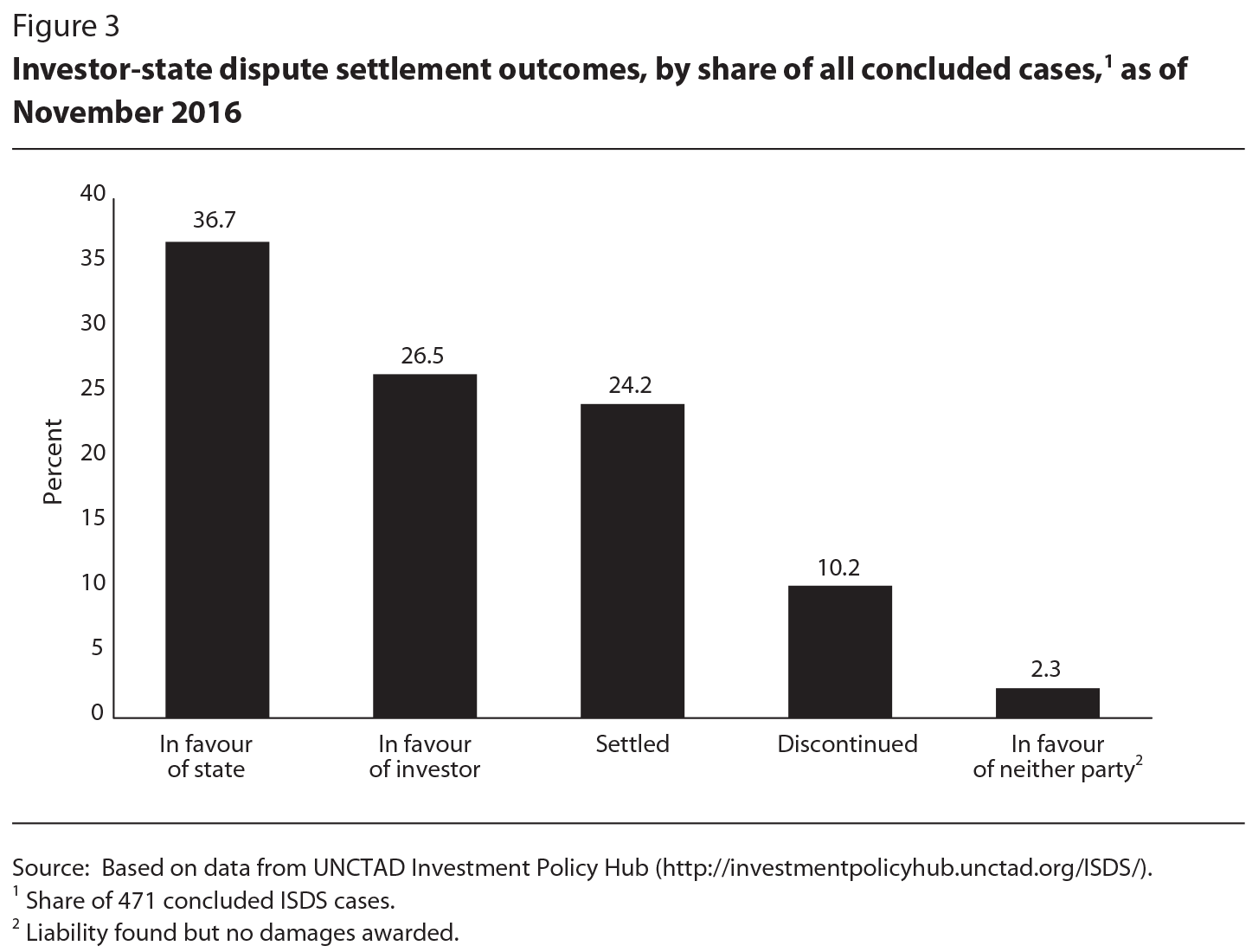

The early 2000s saw a significant rise in ISDS claims (figure 2). As of November 2016, there were 739 known investment treaty claims involving 131 different respondent states; figure 3 shows the categories of outcomes of the 471 claims that have concluded. In 37 percent of the cases, the final decision was in favour of the state, rather than the investor (27 percent of the cases); 24 percent of the claims were settled by the parties; 10 percent were discontinued; and in 2 percent, liability was found, but no damages were awarded.

In Canada, BITs are more commonly referred to as foreign investment promotion and protection agreements (FIPAs).8 Relative to other members of the Organisation for Economic Co-operation and Development (OECD), Canada began its investment treaty program late, signing its first FIPA with the Soviet Union in 1989. Canada had five “first generation” FIPAs, signed with four countries transitioning from Communism and with Argentina (see box 1). After NAFTA was concluded in 1992, the agreement’s chapter 11 legal text became the model for Canada’s 13 “second-generation” FIPAs. The “third-generation” FIPAs followed in 2004, when Canada updated its approach “to reflect, and incorporate the results of, its growing experience with the implementation and operation of the investment chapter of the NAFTA” (Global Affairs Canada 2016b). These third-generation FIPAs — as well as the investment chapters of Canada’s recent free trade agreements — were influenced by, and many of the provisions were similar to, the contemporaneous 2004 US model BIT. Canada’s updated approach had three principal objectives: to enhance clarity in the substantive obligations; to increase transparency in the dispute settlement process; and to discipline and improve efficiency in the dispute settlement procedures.

As of November 2016, Canada had concluded 43 FIPAs: 33 were in force, 5 more were signed but not yet in force, and the negotiations for another 5 had been concluded. Negotiations were ongoing for 9 more FIPAs. Two other relevant developments in Canada’s investment treaty policy are its belated ratification of the ICSID Convention in November 2013 and its ratification of the UN Convention on Transparency in Investor-State Arbitration (the Mauritius Convention on Transparency) in December 2016, which reflects a commitment to openness and transparency in investor-state arbitration.

Canada’s long-standing policy has been to negotiate investment agreements in order to provide a stable, predictable and transparent legal framework for Canadian investors abroad and to address the risks of investing in a foreign state, including political instability, weak legal institutions, uncertain regulatory regimes and the possibility of expropriation. Accordingly, Canada’s FIPAs include a range of obligations pertaining to nondiscriminatory treatment, treatment in accordance with international law, expropriation, transfers of funds, transparency, due process and dispute settlement (Global Affairs Canada 2016d).

Traditionally, Canada’s FIPAs have differed from other model BITs — particularly those in Europe — in several ways. First, most other BITs worldwide provide for national treatment only after an investment has been established, and countries are not prevented from restricting future foreign investment by, for example, deciding that a specific sector of the economy should be reserved for nationals. Canada’s FIPAs, however, similarly to US BITs, provide for national treatment at the establishment phase of foreign investment, meaning that, in principle, no discrimination is allowed between nationals and foreigners when they undertake investments. Nevertheless, the potentially wide scope of this obligation is limited by significant carve-outs or exceptions for both existing nonconforming measures and future measures. The 2004 model FIPA, unlike first-generation FIPAs, provides that existing nonconforming measures may be maintained or renewed, but that, if they are amended, the resulting measure cannot be more restrictive. This provision reflects the Canadian government’s current stated policy that the “FIPA is not an instrument of liberalization,” although it can support the goals of liberalization by ensuring that the host country does not adopt measures in the future that are more restrictive of investment (Global Affairs Canada 2016c).

Second, Canadian FIPAs of the second and third generation include prohibitions on performance requirements: trade-related investment measures and other specific measures that might distort investment decisions, such as local content requirements, which require that locally produced goods or local suppliers be used in production.

Third, the 2004 model FIPA and earlier BITs do not have an observance of undertakings provision or an umbrella clause that allows the enforcement of contractual rights and other state undertakings.9 These types of provisions are -controversial because, if they are interpreted broadly, a breach of any obligation — whether contractual or made by a government authority — could be considered a breach of the provision and thus of the treaty. Some of Canada’s free trade agreements include a special mechanism for investor-state arbitration of “juridical stability agreements” or “legal stability agreements,” but a general observance of undertakings clause is not present in Canada’s FIPAs or in the 2004 model FIPA.

Finally, Canada is one of the few countries to include general exceptions in its BITs, modelled on the general exceptions provision in article XX of the GATT. General exceptions include measures that are necessary “to protect human, animal or plant life or health” or “for the conservation of living or non-living exhaustible natural resources” (Newcombe 2012). Although NAFTA includes general exceptions (in article 2101), this provision does not apply to chapter 11. Neither the United States nor Mexico includes general exceptions in its BITs.

Canada has been a respondent country in ISDS proceedings only under chapter 11 of NAFTA; there are no public reports of Canada’s being a respondent in a claim under one of its FIPAs. As of November 2016, there were 9 active arbitrations against Canada under NAFTA, 13 arbitrations to which Canada was a party and 16 other notices of arbitration, which either had been withdrawn or were inactive (Global Affairs Canada 2016d). Despite many claims, Canada has been found to be in breach of chapter 11 only five times. In four cases, it was ordered to pay damages: Pope & Talbot (US$460,000), S.D. Myers (US$6 million),10 Mobil Investments Canada Inc. and Murphy Oil Corporation v. Canada (C$17.3 million)11 and Windstream Energy LLC v. Canada (C$25 million).12 In the fifth case, Canada was found to have breached the minimum standard of treatment and national treatment as the result of the environmental assessment of a project in Nova Scotia.13 The tribunal decision was made in March 2015, but damages have not yet been assessed. In addition to these five adverse cases, Canada has settled two other claims: Ethyl (C$13 million) and AbitibiBowater (C$130 million).

Although, as noted, all of these claims have been under NAFTA, globally Canada is the sixth most frequent respondent in ISDS claims.14 In my view, however, Canada’s legal counsel and advisers have been quite successful in defending the country against questionable claims. Even including the settlement in AbitibiBowater — which reflects the fair market value of the assets expropriated by the Newfoundland and Labrador government — the total damages awarded to date under NAFTA chapter 11 are less than $200 million. This is not an insignificant amount — and does not include interest and the costs of arbitrations — but it should be considered in the proper context: the stock of FDI in Canada in 2015 was worth $769 billion.15 All told, these awards represent less than 0.025 percent of overall investment — or, in other words, investment is four thousand times larger than these awards.

On the other side of the coin, investors from Canada have brought 32 IIA cases (5.6 percent of all cases globally) against host states, putting Canadian investors in fifth place in terms of all ISDS claims made as of December 2013 (UNCTAD 2014).16 As of 2016, the stock of Canadian direct investment abroad was worth just over $1 trillion, of which 57 percent was in countries with which Canada has an IIA (Global Affairs Canada 2016c).

The growing number of ISDS claims has given rise to a vociferous debate about the legitimacy of the IIA regime (Waibel 2010). The critiques and concerns are wide ranging, spanning the ideological — which opponents sometimes refer to as a “corporate bill of rights for multinational corporations” — to more technical debates among lawyers about the scope and meaning of specific provisions. Critiques of the IIA regime generally highlight the following:

With respect to such criticism, it is useful to distinguish three separate issues: the scope of treaty application, substantive obligations and dispute settlement.

In terms of scope, many IIAs have an open asset-based definition of investment. At the extreme, any type of property held by a foreign investor might be considered a covered investment and subject to protection. Although ISDS tribunals have held that a simple sale of goods contract cannot be considered an investment (it is instead a trade transaction), ISDS tribunals have had to decide whether such things as financial interests in state-issued bonds, hedging agreements and salvage operations are protected investments. Since most IIAs include company shares as an investment, indirect and portfolio investments — not just traditional forms of FDI controlled by the foreign investor — are generally covered under most BITs. Moreover, since many IIAs accord protection to locally incorporated companies and to investments that are owned or controlled directly or indirectly, investors can create very complex corporate structures. Further, investors can invest through third countries and obtain investment treaty protection — the “treaty shopping” noted earlier.

With respect to substantive obligations, concerns are most often raised regarding four types of provisions: fair and equitable treatment, expropriation, MFN treatment and the observance of obligation or umbrella clauses. Many ISDS tribunals have interpreted IIA provisions that require the host country to accord fair and equitable treatment as setting a high standard of investment protection, more demanding than the customary international law standard of treatment of foreigners and their property. Tribunals have interpreted fair and equitable treatment as containing a series of investment protection elements, including the protection of legitimate expectations and the need for a basic level of stability, predictability, consistency and transparency in government conduct. Concerns have been raised that “investor-friendly” interpretations of fair and equitable treatment unduly constrain government regulation, particularly when governments bring in new regulations to deal with environmental and health risks. As a practical matter, almost all ISDS claims now allege a breach of fair and equitable treatment, and respondent countries are most commonly found to have breached such treatment.

The scope of expropriation has also been a matter of significant controversy, particularly in claims of indirect and regulatory expropriation. For example, in the plain-packaging cigarette cases, the claim was made that such legislation is expropriatory because it deprives the investor of the use of its intellectual property (trademarks and trade dress). Expropriation necessarily entails a substantial deprivation, but what amounts to such a deprivation is much debated, as is whether “police powers” can be used legitimately to regulate or suppress commercial activities that cause harm to the general public or the environment.19 The scope and application of this doctrine, nevertheless, remains controversial, and the dividing line between legitimate regulatory measures (for which compensation need not be paid) and expropriation (for which compensation must be paid) is often uncertain, as it is in many domestic legal systems.

MFN treatment obligations in some IIAs have been interpreted to apply to the substantive treatment and ISDS provisions in a host country’s other IIAs. For countries with many IIAs — sometimes 150 or more,20 negotiated over many years with different countries — determining the effect of MFN treatment can be extraordinarily complex, particularly where the host country has changed its IIA policy and models over time.

Finally, clauses that provide for the observance of obligations — for example, “Each Contracting Party shall observe any obligation it may have entered into with regard to investment of investors of the other Contracting Party” (article 3(4) of the Dutch model BIT) — have been interpreted in inconsistent ways. Interpreted broadly, umbrella clauses have the effect of internationalizing all contract claims: an investor with a contract with the host country can make an investment treaty claim where the host has breached the contract, notwithstanding that the contract might provide for dispute resolution before local courts.

Investor-state dispute settlement is the defining feature of modern IIAs. These agreements have proved controversial because, unlike so many other areas of public international law, ISDS provides a mechanism for binding, third-party dispute settlement at the unilateral request of the investor. ISDS results in a final award not reviewable for mere error of law and enforceable in almost every jurisdiction in the world. Simply put, IIAs can have a strong bite. Many government officials have been surprised to discover that an agreement signed long ago and forgotten about can have far-reaching effects.

A general critique of ISDS that picks up its multifarious strands is as follows. International arbitration might be appropriate for commercial disputes between private parties, but inappropriate as a form of judicial review for the conduct of sovereign states. An arbitral tribunal composed of three private individuals lacks the legitimacy and accountability to judge whether a state’s conduct and measures (made in the public interest) violate the IIA. Unlike domestic judges, international arbitrators have little knowledge of the domestic legal and regulatory context. Further, unlike domestic investors, foreign investors are generally not required to seek a remedy in local courts, meaning that international arbitrators do not have the benefit of the local court’s interpretation of the host country’s domestic law.

International arbitrators, moreover, often have commercial, private law firm backgrounds and engage in expansive interpretations of investment obligations. Given the lucrative fees they obtain, arbitrators have a vested interest, both individually and as a group, in maintaining and expanding the ISDS regime. This gives rise to a reasonable apprehension of a conflict of interest. Unlike judges on a permanent tribunal, arbitrators lack security of tenure and often also engage in law practice and counsel work (representing investors and states); such role shifting creates additional conflicts of interest.

In terms of the proceedings, most international arbitrations are private and confidential; the public has access to neither the written record of the proceedings nor the hearings. There is no provision for interested third parties to make submissions, which is particularly controversial where a large-scale foreign investment project affects a local community. There is no system of precedent in international investment law; each tribunal remains sovereign to make its own decision. This has led to inconsistent rulings on cases involving the same facts and the same treaties and contradictions in tribunal reasoning and determinations. Under international arbitration law, moreover, an award is final and binding and not subject to review, even for error of law. Although this might be acceptable to commercial parties in a contract dispute, it is inconsistent with the rule of law for a host country to be held liable to a foreign investor for a public measure where the tribunal decision is incorrect — particularly when awards can be in the hundreds of millions of dollars.

Critics note that IIAs bind states over long periods and even after an IIA has been terminated. For example, the Canada-China FIPA has an initial period of 15 years and continues in force thereafter unless terminated. Upon termination, investment protections for investments made prior to the date of termination continue for another 15 years.

Critics also argue that the broad scope of investment obligations and threats of ISDS claims result in regulatory chill and impede government measures to protect the public interest.21 For example, the preamble to the “Public Statement on the International Investment Regime” (2010), signed by a group of academics, states: “We have a shared concern for the harm done to the public welfare by the international investment regime, as currently structured, especially its hampering of the ability of governments to act for their people in response to the concerns of human development and environmental sustainability.”22 There is, however, little empirical evidence to support the claim of regulatory chill. Côté (2014), for example, not only finds “no consistent observable evidence to suggest the possibility of regulatory chill” in Canada but also notes that, in the case of tobacco control regulations, there has been a global increase in their adoption, including in regions facing ISDS challenges.

At a more fundamental level, critics point to the lack of empirical evidence that IIAs actually increase FDI. The 2003 UNCTAD World Investment Report concluded that “BITs play a minor role in influencing global FDI flows” (UNCTAD 2003). However, the report nevertheless highlighted the “enabling” function of IIAs in allowing a country’s economic determinants to assert themselves:

The policy framework is at best enabling, having by itself little or no effect on FDI flows. It has to be complemented by economic determinants that attract FDI, especially market size and growth, skills, abundant competitive resources and good infrastructure. As a rule, IIAs tend to make the regulatory framework more transparent, stable, predictable and secure — that is, they allow the economic determinants to assert themselves. And when IIAs reduce obstacles to FDI and the economic determinants are right, they can lead to more FDI. But it is difficult to identify the specific impact of the policy framework on FDI flows, given the interaction and relative importance of individual determinants. (UNCTAD 2003, 91)

Although more recent studies support the argument that there is a robust relationship between IIAs and levels of FDI, the existence of a causal relationship remains disputed (Yackee 2011). For example, Brazil has not ratified any traditional BITs, yet it is consistently the largest recipient of FDI flows in South America, in 2015 receiving US$65 billion, or 53 percent, of all inflows to that continent (UNCTAD 2016a). In 2013, Brazil approved a model BIT agreement that differs from traditional BITs by focusing on the promotion and facilitation of investment and on mechanisms to prevent disputes. The model includes only state-to-state, not investor-state, dispute settlement (UNCTAD 2016b).

It is beyond the scope of this chapter to address fully all of the critiques of the IIA regime. Notwithstanding my view that many of the criticisms are misplaced (see Newcombe 2007), the reality is that concerns about the investment treaty regime are not just academic or limited to a small number of fringe nongovernmental organizations. The regime is having serious real-world effects, and a number of countries that have been subject to investment treaty claims are reconsidering their involvement. In Latin America, Bolivia, Ecuador and Venezuela have denounced the ICSID Convention and terminated a number of BITs.23 Australia rejected ISDS in its free trade agreement with the United States, and its previous government announced it would not agree to ISDS in future agreements.24 After a 2009 government report critical of its BIT policy (Vis-Dunbar 2009), South Africa terminated its investment treaties and created a domestic foreign investment protection law. In March 2014, Indonesia announced that it planned to terminate more than 60 BITs (“Indonesia,” 2014).

In the face of criticism of investment provisions and ISDS in the TTIP, the European Commission suspended negotiations on ISDS and launched a 90-day public consultation on the issue. Of the 150,000 replies the commission received, 97 percent were standard-form answers prepared by various anti-TTIP groups. The commission’s report, released in 2015, found there were three general categories of statements: opposition to the TTIP in general; opposition to investment protection and ISDS in the TTIP; and specific views on the proposed EU approach. Within this third category, there was a wide range of conflicting views, but the report highlighted four areas where further improvements should be explored: protecting the right to regulate; establishing arbitral tribunals; the relationship between domestic judicial systems and ISDS; and the review of ISDS decisions through an appellate mechanism (European Commission 2015b).

When the revised text of CETA was released in February 2016, its investment chapter was substantially amended to include the EU-inspired Investment Court System and other provisions designed to affirm the host state’s right to regulate in the public interest.

Widespread concerns about international investment agreements and investor-state dispute settlement over the past decade have resulted in significant efforts to recalibrate such agreements. In 2004, both Canada and the United States, as frequent respondents in NAFTA chapter 11 investment claims, released new model investment agreements incorporating “lessons learned” from NAFTA investment arbitrations.

The 2004 Canadian model FIPA introduced many important substantive and procedural changes to address concerns about the scope of obligations and ISDS, building on chapter 11 of NAFTA:25

The third-generation FIPAs Canada signed with Peru and Jordan in 2006 and 2009, respectively, follow the 2004 model closely. The investment chapters in the free trade agreements with Colombia and Panama also generally follow the model, although they adopt a slightly more streamlined approach, particularly with respect to ISDS provisions. More recent FIPAs are also substantially based on the 2004 model, although the Canada-China FIPA, which came into force in October 2014, diverges significantly from it. In particular, the Canada-China FIPA does not apply national treatment to the establishment of investment, meaning that there are no market access guarantees for Canadian investors other than the general obligation to admit investments “in accordance with its laws, regulations and rules” (article 3). Since existing liberalization is not locked in, the FIPA does not protect Canadian investors from a more restrictive foreign investment regime in the future. With respect to ISDS, the Canada-China FIPA diverges from the 2004 model and Canadian practice by not requiring the release of ISDS claims-related documents or providing for hearings to be public. Instead, the FIPA provides that documents will be publicly available and hearings will be open to the public only if “a disputing Contracting Party determines that it is in the public interest to do so and notifies the Tribunal of that determination” (article 28).

The text of the investment chapter of the Trans-Pacific Partnership is substantially similar to the 2004 model US BIT. The scope of investment obligations in the TPP is comparable to the investment obligations in other Canadian agreements, notably NAFTA. In general terms, the TPP investment chapter does not create anything new in terms of obligations to foreign investors beyond what is already in place under Canada’s existing IIAs. Like the 2004 model FIPA, the TPP includes interpretative annexes defining and limiting the scope of the fair and equitable treatment and expropriation obligations (annexes 9-A and 9-B). In terms of dispute settlement, the basic operation of ISDS remains the same: investors from TPP states can submit a claim to arbitration for breach of investment obligations. The scope of ISDS in the TPP is broader than in NAFTA: in line with the 2004 US model BIT, TPP investors can make claims for breaches of investment authorizations and investment agreements.26 The TPP follows current Canadian and US practice in providing for transparency of the arbitral proceedings and in permitting ISDS tribunals to accept submissions from third parties.

In August 2014, Canada and the EU announced that the CETA text would proceed to the “legal review” and translation stage. The EU also signalled its desire to adopt a new approach to ISDS, with the ultimate goal of working toward a permanent multilateral investment court (European Commission 2015a). The revised text of CETA, published in February 2016, includes groundbreaking changes to the agreement’s previously negotiated ISDS mechanism and represents a significant change to long-standing Canadian and European ISDS practice.

The CETA investment chapter is generally similar to Canada’s 2004 model FIPA with respect to substantive investment protections, but it includes a number of important procedural innovations. The chapter provides prohibitions similar to those in the General Agreement on Trade and Services on specific types of limitations to market access (article 8.4). It also provides for national treatment for the establishment and acquisition of investment, subject to reservations for existing nonconforming and future measures (articles 8.6 and 8.15). The provision on minimum standards establishes an innovative compromise between Canada’s position — that the standard of treatment should be that provided by customary international law — and the position of most BITs between EU members, which provide for stand-alone fair and equitable treatment obligations. Under the compromise, the chapter includes a closed list of measures that would constitute a breach of fair and equitable treatment (article 8.10), although the list arguably reflects the customary international law minimum standard of treatment. The text also includes a number of innovative provisions on the restructuring of public debt and the relationship between intellectual property rights and investment disciplines (annex 8-B, Public Debt, and article 8.12, para. 6).

The most significant change in the February 2016 CETA text is an article reaffirming that governments have the right to regulate, and that expressly acknowledges that investment protection obligations are not to be interpreted as a commitment by governments that regulatory regimes will not change (article 8.9). Further, the signing of CETA in October 2016 was accompanied by the so-called Joint Interpretative Instrument, intended to assuage concerns that the agreement is a threat to social regulation (Canada 2016c). The instrument affirms that CETA is a “a modern and progressive trade agreement which will help boost trade and economic activity, while also promoting and protecting our shared values and perspectives on the role of government in society.” The instrument also affirms the ability of states to regulate in the public interest (article 2) and to provide public services and social security (articles 4 and 5). It is important to highlight that the Joint Interpretative Instrument is not simply a political statement; as an instrument made in connection with the conclusion of the treaty, it provides context for interpreting the CETA text under international law.

With respect to dispute settlement, the instrument emphasizes that the final CETA text “moves decisively away from the traditional approach of investment dispute resolution and establishes independent, impartial and permanent investment Tribunals, inspired by the principles of public judicial systems in the European Union and its Member States and Canada, as well as and [sic] international courts such as the International Court of Justice and the European Court of Human Rights” (section 6(f)). Unlike the ISDS provisions in most international agreements, which use ad hoc international arbitration tribunals to make final decisions on investor-state disputes, the revised CETA will establish a permanent tribunal to decide disputes, backed up by an appellate tribunal that can review the initial decision. The permanent tribunal will have 15 government-appointed members — 5 Canadians, 5 from EU member states and 5 from third countries — who will hear cases in divisions consisting of three members. The appellate tribunal will have the authority to review awards by the permanent tribunal for legal and factual errors. There are also detailed ethical rules for tribunal members to avoid conflicts of interest; most significantly, members will be barred from working as lawyers or experts in other investment disputes. The CETA text and the Joint Interpretative Instrument also commit the parties to pursuing the establishment of a multilateral investment tribunal and appellate mechanism to replace the bilateral systems, such as in article 8.29 of CETA and section 6(i) of the Joint Interpretative Instrument. In December 2016, the EU and Canada co-hosted exploratory discussions on the establishment of a multilateral investment court.

The European commissioner for trade and Canada’s minister of international trade have referred to the revised final text of CETA as a “gold-standard agreement” (Canada 2016d), but academic assessment of the investment chapter has been mixed. VanDuzer (2016, 17), for example, concludes that, “while not perfect, CETA’s approach has the best claim to legitimacy in any treaty to date.” Others, however, see old wine in a new bottle. Schneiderman acknowledges positive aspects of CETA but argues that the agreement does not remedy the principal defects of the international investment regime: “The treaty disciplines enforced by this cadre of investment lawyers remain mostly intact. This is because CETA’s investment chapter looks like almost every other investment treaty” (2016, 2). Likewise, Van Harten (2016) argues that CETA will expand investor-state dispute settlement, thereby undermining democracy and domestic courts.

The CETA investment chapter represents an important evolution in investment treaty practice. It breaks new ground by moving to a permanent tribunal system with appellate review. With respect to the mechanics of tribunal proceedings, however, CETA tribunals will operate much like those of current agreements. The CETA text borrows and builds on experience from NAFTA chapter 11 and the 2004 Canadian model BIT. As Lévesque (2016, 1) puts it, “Not as much of the ‘new’ system is really ‘new’ and much remains of the ‘old’ (although improved in many respects).”

It is in Canada’s interest to continue to support international investment obligations backed up by investor-state dispute settlement. Canadian investment treaty policy should continue to evolve by developing finely calibrated agreements that balance protection of foreign investment with domestic regulatory flexibility. In the longer term, the rise of GVCs and the globalization of investment relationships require a multilateral approach to international investment, one that reflects the complex intersections between international trade and investment.

Countries enter international investment agreements to protect their own investors. Similarly, the overriding priority of Canadian investment treaty policy is to ensure that Canadian direct investment abroad is protected from arbitrary and discriminatory measures by requiring host countries to provide treatment in accordance with international standards and norms. The main justification for IIAs is thus distinct from an economic argument that such agreements necessarily increase FDI — a result that, in any event, has not been definitively demonstrated.

Critics claim that CETA does not need to include ISDS because both Canada and the EU have well-functioning legal systems, good governance and an established tradition of adherence to the rule of law. But the history of foreign investment law suggests that there is always the potential for powerful domestic interests to run roughshod over the legitimate interests of foreign investors. In the context of Canada’s federal system, an instructive and cautionary case is that of AbitibiBowater, where a provincial government passed legislation expropriating the company’s assets, stating that the government would be the sole judge of the amount of compensation it would provide, and depriving the company of the right to seek a remedy in Canadian courts.27 Nor should Canadian investors have complete faith in the legal systems of EU states. Although German and French courts might be paragons of the rule of law, the EU includes states that rank below the 70th percentile in the 2013 World Bank Rule of Law Indicators and below 40th place in the Transparency International Corruption Perceptions Index.

Even if one remains unconvinced of the need for ISDS in the context of CETA, the agreement is important as a model for future treaty practice. The final text of CETA’s investment chapter provides a new approach to balancing investment protection and the regulatory and legal frameworks of the modern state, and ensuring that countries have sufficient regulatory flexibility to protect important public interests without the fear of investor-state claims. Canada and the EU cannot and should not expect other countries to accept the obligations in modern IIAs if they themselves are not willing to be bound by similar provisions. It is not politically tenable for countries that want to protect their investors abroad to take the position that ISDS is not needed with their own borders — presumably due to the superiority of their legal systems. There is a systemic interest in supporting an international standard of ISDS beyond any single agreement.

Some have criticized the Canada-China FIPA because — in contrast to many of Canada’s previous FIPAs, where Canada was the dominant capital exporter — the stock of Chinese FDI in Canada is more than triple the stock of Canadian FDI in China.28 For example, Van Harten argues that the Canada-China FIPA is unique because it “will likely be largely de facto non-reciprocal due to anticipated in-flows of Chinese investment to Canada outstripping Canadian investment in China” (2012, 2). Yet, arguing that investment protection is justifiable only where outward foreign investment exceeds inward investment is based on an outdated mercantilist mindset.29 Van Harten further suggests that the FIPA will give “Cadillac legal status to Canadian investors in China and vice versa. Yet Canada will be much more exposed to claims and corresponding constraints as a result of the de facto non-reciprocity” (2012, 2). This presumes that the investment standards in the FIPA’s protections are too stringent and the risk of Chinese claims too significant to warrant ensuring that Canadian investors in China have investment protection. Clearly, there is a cost-benefit analysis here that depends substantially on one’s assessment of the balance reached in the FIPA. But at any rate, the record in NAFTA chapter 11 cases to date simply does not support the claim that investment disciplines have prevented countries from regulating in the public interest. For example, in Chemtura v. Canada, a case involving the phasing out of the pesticide lindane, the tribunal rejected all claims that Canada breached NAFTA. With respect to the expropriation claim, the tribunal concluded that the Pest Management Regulatory Agency “took measures within its mandate, in a non-discriminatory manner, motivated by the increasing awareness of the dangers presented by lindane for human health and the environment. A measure adopted under such circumstances is a valid exercise of the State’s police powers and, as a result, does not constitute an expropriation.”30

Canada’s investment treaty practice has continued to evolve through time. Its experience as a frequent respondent in ISDS claims under NAFTA chapter 11 highlights the need to ensure, first, that investment protection standards are finely calibrated and that they appropriately balance “offensive” interests (in protecting Canadian FDI abroad) and “defensive” interests (in permitting governments the regulatory flexibility to ensure that economic development is both sustainable and meets the needs of Canadians); and, second, that there is a legitimate, effective and efficient process for the resolution of foreign investment disputes. Here, Canada has been a leader in addressing many of the concerns regarding the scope of IIAs, substantive standards and ISDS. Canada should continue to maintain its balanced policy of investment protection, including the use of ISDS, and to support incremental improvements in treaty practice, as reflected in the innovative provisions in CETA.

The growth of global value chains means that, more than ever, trade and investment decisions are intimately linked — that the effects of international trade and investment practices are not localized. GVCs raise fundamental questions about the utility of the predominantly bilateral approach to international investment law, which is based on the assumption that there is one home country investor making an “investment” in a host country. Although this legal structure might be appropriate for the traditional bricks-and-mortar type of investment, it is not easily applicable to the variety of complex business relationships in GVCs. Contemporary business practices also challenge the distinction between trade and investment that has developed in international economic law as a result of the silos in which trade and investment disciplines have been placed. It is not clear why investors require different or special protections that traders do not have.31 If government conduct has the same economically detrimental effect on both the foreign trader and the foreign investor, what justifies the special treatment accorded to foreign investors?

As noted in the 2013 World Investment Report (UNCTAD 2013, 190), since “investment and trade are inextricably linked in GVCs, it is crucial to ensure coherence between investment and trade policies.” This requires attention to trade measures affecting investment and to investment measures affecting trade, and ensuring close coordination between domestic trade and investment promotion agencies. A fuller analysis of these complex issues is beyond the scope of this chapter, but a fundamental question that remains for any future multilateral investment regime is its relationship to and/or integration with the international trading regime.

Given the proliferation of GVCs and IIAs — and the fact that almost every country in the world is entwined in the IIA regime — it might seem obvious that the time is ripe for a multilateral investment framework. However, in light of the widespread concerns about IIAs, countries still need the flexibility to experiment in adjusting to the IIA regime. The EU has recently obtained new competence with respect to foreign investment, but it will still take several years to more fully develop its approach to IIAs. Eventually, hundreds of individual BITs entered into by EU member states are expected to be replaced by EU agreements.

Regionalism in investment treaty making is on the rise: At the end of 2013, some 110 countries were involved in more than 22 regional and interregional negotiations (UNCTAD 2013).32 Although the structure and content of many regional agreements are similar, and there might be some general policy convergence, significant diversity remains in the legal drafts of specific obligations. Further, there is some evidence that regionalism might lead to overlap and contradiction, rather than to contraction and convergence (Alschner 2014). So even if there is some convergence in practice as major economic powers — particularly the EU, the United States, China and India — develop IIAs between themselves, such negotiations, where they exist, are in the early stages, and final legal texts are not likely to emerge for many years, if at all.

The failure of the negotiations in the 1990s for the proposed OECD Multilateral Agreement on Investment and the 2004 decision by the WTO not to pursue the work on the relationship between trade and investment mentioned in the 2001 Doha Development Agenda suggest that any attempt at a multilateral framework should be approached with caution. In light of the intense debate over investment protection standards and ISDS and the proliferation of bilateral and plurilateral negotiations, it is premature to expend significant diplomatic energy or resources pushing for a multilateral approach. In the short term, countries should continue to innovate at the bilateral and regional levels and take stock of those developments before trying to develop a multilateral framework. In any event, there appears to be no political will to commence a grand new international economic negotiation over the perennially contentious issue of the treatment of foreign investment. For its part, Canada should maintain its engagement with international organizations, particularly ICSID, the OECD and UNCTAD, all of which have programs studying developments in international investment law and policy. Finally, there have been some initial discussions on adopting an additional protocol to the ICSID Convention to provide for an appellate mechanism (de Mestral 2016). This is a promising idea that Canada should support.

The investment treaty framework continues to evolve and improve. An international policy consensus now exists that foreign direct investment is needed in order to reach sustainable development objectives. As highlighted by the United Nations Third International Conference on Financing for Development, “the goal of protecting and encouraging investment should not affect our ability to pursue public policy objectives” (United Nations 2015, para. 91).33 It remains in Canada’s interest to continue to support international investment obligations backed up by investor-state dispute settlement. Canada’s investment treaty policy should aim for finely calibrated agreements that balance the protection of foreign investment with domestic regulatory flexibility. The investment chapter of CETA offers innovative provisions that address that balance with respect to both substantive obligations and dispute settlement, and it should serve as a model for future Canadian treaty practice.

In the longer term, the current, increasingly unworkable bilateral approach to investment disciplines needs to give way to a multilateral framework on investment, given the proliferation of GVCs and the globalization of investment relationships. The current international investment regime, with its proliferating network of over 3,500 agreements, is an uneven, inconsistent and inefficient approach to international investment policy and law. Although Canada and the EU have committed to pursue, with other trading partners, the establishment of a multilateral investment tribunal and appellate mechanism for the resolution of investment disputes, such an initiative is unlikely to be successful in the short term without the support of major economic actors such as China, India and the United States.

The author thanks Stephen Tapp, Robert Wolfe and an anonymous reviewer for helpful comments and suggestions. In addition to his academic work, the author acts as legal counsel advising investors and states on investment treaty law and arbitration. He has also acted as an arbitrator in investment treaty cases. The opinions expressed in this chapter are the author’s independent academic views.

Photo: Chrystia Freeland, Canada’s Minister of International Trade, holds a media availability on the Canada-European Union Comprehensive Economic and Trade Agreement (CETA) in the foyer of the House of Commons on Parliament Hill in Ottawa on Monday, Oct. 31, 2016. THE CANADIAN PRESS/Sean Kilpatrick

Alschner, W. 2014. “Regionalism and Overlap in Investment Treaty Law — Towards Contradiction.” Journal of International Economic Law 17 (2): 271.

Australia. 2010. Productivity Commission. Bilateral and Regional Trade Agreements. Research Report. Canberra: the Commission. Accessed December 14, 2016. https://www.pc.gov.au/inquiries/completed/trade-agreements/report/trade-agreements-report.pdf

Canada. 2016a. CETA: A Progressive Trade Agreement for a Strong Middle Class. Accessed December 14, 2016. https://www.inter national.gc.ca/gac-amc/campaign-campagne/ceta-aecg/index.aspx?lang=eng

_____. 2016b. Fall Economic Statement 2016. Accessed December 14, 2016. https://www.budget.gc.ca/fes-eea/2016/docs/

statement-enonce/chap02-en.html

_____. 2016c. Joint Interpretative Instrument on the Comprehensive Economic and Trade Agreement (CETA) between Canada & the European Union and Its Member States. Accessed December 13, 2016. https://www.inter national.gc.ca/trade-commerce/trade

agreements-accords-commerciaux/agr-acc/ceta-aecg/jii-iic.aspx?lang=eng

_____. 2016d. “Joint Statement by European Commissioner for Trade and Canada’s Minister of International Trade on Canada-EU Trade Agreement.” News release, February 29. Accessed December 14, 2016. https://news.gc.ca/web/article-en.do?nid=1036759

_____. 2016e. Text of the Comprehensive Economic and Trade Agreement. Accessed December 13, 2016. https://www.international.gc.ca/trade-commerce/trade-agreements-

accords-commerciaux/agr-acc/ceta-aecg/

text-texte/toc-tdm.aspx?lang=eng

“Convention on the Settlement of Investment Disputes between States and Nationals of Other States, March 18, 1965.” 1965. International Legal Materials 4: 524-44.

Côté, C. 2014. “A Chilling Effect? The Impact of International Investment Agreements on National Regulatory Autonomy in the Areas of Health, Safety and the Environment.” PhD thesis, London School of Economics and Political Science. Accessed August 11, 2016. https://etheses.lse.ac.uk/897/

de Mestral, A. 2016. Investor-State Arbitration and Its Discontents: Options for the Government of Canada. CIGI Investor-State Arbitration Series Paper 14. Waterloo, ON: Centre for International Governance Innovation. Accessed December 14, 2016. https://www.cigionline.org/sites/default/files/documents/ISA%20Paper%20No.14_0.pdf

European Commission. 2015a. “Commission Proposes New Investment Court System for TTIP and Other EU Trade and Investment Negotiations.” News release, September 16. Brussels: the Commission. Accessed December 14, 2016. https://trade.ec.europa.eu/doclib/press/index.cfm?id=1364

_____. 2015b. Report: Online Public Consultation on Investment Protection and Investor-to-State Dispute Settlement (ISDS) in the Transatlantic Trade and Investment Partnership Agreement (TTIP). Commission Staff Working Document. Accessed August 11, 2016. https://trade.ec.europa.eu/doclib/docs/2015/january/tradoc_153044.pdf

Global Affairs Canada. 2016a. Canada-China Foreign Investment Promotion and Protection Agreement (FIPA) Negotiations. Accessed November 13, 2016. https://www.international.gc.ca/trade-agreements-

accords-commerciaux/agr-acc/fipa-apie/china-chine.aspx?lang=eng

_____. 2016b. Canada’s Foreign Investment Promotion and Protection (FIPAs). Accessed November 13, 2016. https://www.international.gc.ca/trade-agreements-

accords-commerciaux/agr-acc/fipa-apie/fipa-apie.aspx?

_____. 2016c. Canada’s FIPA Program: Its Purpose, Objective and Content. Accessed November 13, 2016. https://www.international.gc.ca/trade-agreements-accords-commerciaux/agr-acc/fipa-apie/fipa-purpose.aspx?lang=en

_____. 2016d. Cases Filed against the Government of Canada. Accessed November 13, 2016.https://www.international.gc.ca/trade-agree ments-accords-commerciaux/topics-

domaines/disp-diff/gov.aspx?lang=eng

_____. 2016e. Consolidated TPP Text. Accessed December 13, 2016. https://www.international.gc.ca/trade-agreements-

accords-commerciaux/agr-acc/tpp-ptp/

text-texte/toc-tdm.aspx?lang=eng

Godoy, J. 2014. “Defending European Consumers and Public Services against International Corporations.” Independent European Daily Press, June 2. Accessed November 13, 2016. https://www.ipsnews.net/2014/06/defending-european-consumers-and-public–services-against-international-corporations/

Greider, W. 2001. “The Right and US Trade Law: Invalidating the 20th Century.” Nation, November 17. Accessed November 13, 2016. https://www.thenation.com/article/right-and-us-trade-law-invalidating-20th-century?page=0,5

“Indonesia to Terminate More than 60 Bilateral Investment Treaties.” 2014. Financial Times, March 26. Accessed August 11, 2016. https://www.ft.com/cms/s/0/3755c1b2-b4e2-11e3-af92-00144feabdc0.html#axzz

33hpkEHzJ

Italaw. 2015. International Investment Treaty Name. Accessed December 13, 2016. https://www.italaw.com/browse/international-

investment-agreement-name

Lévesque, C. 2016. The European Commission Proposal for an Investment Court System: Out with the Old, In with the New? CIGI Investor-State Arbitration Series Paper 10. Waterloo, ON: Centre for International Governance Innovation. Accessed December 14, 2016. https://www.cigionline.org/sites/default/files/isa_paper_series_no.10_0.pdf

Lévesque, C., and A. Newcombe. 2013. “Canada.” In Commentaries on Selected Model Investment Treaties, edited by C. Brown. Oxford, UK: Oxford University Press.

Newcombe, A. 2007. “Sustainable Development and Investment Treaty Law.” Journal of World Investment and Trade 8: 357.

_____. 2010. “A Brief Comment on the ‘Public Statement on the International Investment Regime.’” Blog post, September 3. Accessed November 13, 2016. https://kluwerarbitra tionblog.com/blog/2010/09/03/public-state ment-on-the-international-investment-regime/

_____. 2012. “The Use of General Exceptions in IIAs: Increasing Legitimacy or Uncertainty.” In Improving International Investment Agreements, edited by A. de Mestral and C. Lévesque. London: Routledge.

Newcombe, A., and L. Paradell. 2009. The Law and Practice of Investment Treaties: Standards of Treatment. Alphen aan den Rijn, Netherlands: Kluwer Law International.

Peterson, L.E. 2016. “Breaking: U.S. Investor Awarded $25 Million for NAFTA Breach by Canada.” IAReporter, October 13. Accessed December 14, 2016. https://www.iareporter.com/articles/breaking-u-s-investor-awarded-25-million-for-nafta-breach-by-canada/

“Public Statement on the International Investment Regime — 31 August 2010.” 2010. North York, ON: York University, Osgoode Hall Law School. Accessed March 27, 2015. https://www.osgoode.yorku.ca/

public-statement-international-investment- regime-31-august-2010/

Salacuse, J., and N. Sullivan. 2005. “Do BITs Really Work? An Evaluation of Bilateral Investment Treaties and Their Grand Bargain.” Harvard International Law Journal 46 (1): 67.

Schill, S. 2009. The Multilateralization of International Investment Law. Cambridge, UK: Cambridge University Press.

Schneiderman, D. 2016. Why CETA Is Unlikely to Restore Legitimacy to ISDS. CIGI Investor-State Arbitration Commentary Series 7. Waterloo, ON: Centre for International Governance Innovation. Accessed December 14, 2016. https://www.cigionline.org/publications/why-ceta-unlikely-restore-legitimacy-isds.

Shihata, I. 1986. “Towards a Greater Depoliticization of Investment Disputes.” ICSID Review 1 (1): 1.

UNCTAD (see United Nations Conference on Trade and Development)

United Nations. 2015. Report of the Third International Conference on Financing for Development. A/CONF.227/L.1. New York: United Nations.

United Nations Conference on Trade and Development (UNCTAD). 2003. World Investment Report 2003. New York: United Nations.

_____. 2007. International Investment Rulemaking. Note by the UNCTAD Secretariat, TD/B/COM.2/EM.21/2, May 22. Accessed December 14, 2016. https://unctad.org/en/Docs/c2em21d2_en.pdf

_____. 2008. The Development Dimension of International Investment Agreements. Note by the UNCTAD Secretariat, TD/B/C.II/MEM.3/2, December 2. Accessed December 14, 2016. https://unctad.org/en/Docs/

ciimem3d2_en.pdf

_____. 2013. World Investment Report 2013: Global Value Chains: Investment and Trade for Development. New York: United Nations.

_____. 2014. Recent Developments in Investor-State Dispute Settlement (ISDS). IIA Issues Note 1, April. Accessed December 14, 2016. https://unctad.org/en/PublicationsLibrary/

webdiaepcb2014d3_en.pdf

_____. 2016a. World Investment Report 2016: Investor Nationality: Policy Challenges. New York: United Nations.

_____. 2016b. Taking Stock of IIA Reform. IIA Issues Note 1, March. Accessed December 14, 2016. https://unctad.org/en/PublicationsLibrary/webdiaepcb2016d3_en.pdf

VanDuzer, J.A. 2016. Investor-State Dispute Settlement in CETA: Is It the Gold Standard? Commentary 459. Toronto: C.D. Howe Institute. Accessed December 14, 2016. https://www.cdhowe.org/sites/default/files/attachments/research_papers/mixed/Commentary%20459.pdf

Van Harten, G. 2012. “China Investment Treaty: Expert Sounds Alarms in Letter to Harper.” Tyee, October 16. Accessed August 11, 2016. https://thetyee.ca/Opinion/2012/10/16/China-Investment-Treaty/

_____. 2016. ISDS in the Revised CETA: Positive Steps, But Is It a “Gold Standard”? CIGI Investor-State Arbitration Commentary Series 6. Waterloo, ON: Centre for International Governance Innovation. Accessed December 14, 2016. https://www.cigionline.org/publications/isds-revised-ceta-positive-steps-it-gold-standard

Van Os, R., and R. Knottnerus. 2011. Dutch Bilateral Investment Treaties: A Gateway to “Treaty Shopping” for Investment Protection by Multinational Companies. Amsterdam: Somo.

Vis-Dunbar, D. 2009. “South African Trade Department Critical of Approach Taken to BIT-making.” Investment Treaty News, July 15. Accessed August 11, 2016. https://www.iisd.org/itn/2009/07/15/south-african-trade-department-critical-of-approach-taken-to-bit-making/

Waibel, M. 2010. The Backlash against Investment Arbitration. Alphen aan den Rijn, Netherlands: Kluwer Law International.

Yackee, J. 2011. “Do Bilateral Investment Treaties Promote Foreign Direct Investment? Some Hints from Alternative Evidence.” Virginia Journal of International Law 51: 397.

Montreal – The new rules to settle foreign investment disputes contained in the recently signed Canada-EU Comprehensive Economic and Trade Agreement (CETA) are a step in the right direction and provide a model for Canada’s future investment agreements, says a new chapter from the Institute for Research on Public Policy’s forthcoming volume Redesigning Canadian Trade Policies for New Global Realities.

Author Andrew Newcombe (University of Victoria) says that through its efforts to create a new Investment Court System that many other countries could eventually join, Canada is playing a leadership role by improving international investment policy in a way that protects foreign investment and maintains regulatory flexibility.

In his chapter Newcombe examines critiques of the international investment treaty regime — an area where public criticism has increased sharply in recent years — and reviews the most significant changes to treaty practice over the past decade in Canada and the United States.

Controversial issues include the fact that investor-state dispute settlement (ISDS) tribunals have the power to review host country laws and regulations, which potentially call into question domestic policy decisions aimed at protecting human health and the environment. Newcombe says there is no convincing evidence that ISDS has prevented Canadian policy-makers from regulating in the public interest. “For the most part, Canada’s legal counsel has been successful in defending Canada against questionable claims,” he says. He emphasizes that when viewed in context, awards to date in favour of foreign investors represent only a small fraction of foreign direct investment in Canada (less than 0.025 percent).

Newcombe argues that Canada and other countries have a strong systemic interest in continuing to support international investment agreements backed up by investor-state dispute settlement, and this interest extends beyond any single agreement. The fundamental rationale for the international investment regime is to protect and promote investments by adhering to and enforcing international standards. “Canada cannot and should not expect other countries to accept the obligations of modern international investment agreements if they themselves are not willing to be bound by these same provisions,” he says.

The author says that the proposed multilateral investment approach that CETA establishes is preferable to the current patchwork of thousands of largely bilateral deals. Nevertheless, he cautions that this objective is probably best viewed as a long-term goal rather than a short-term priority, unless it gains the support of key economic powers, such as the United States and China, which is unlikely in the short term.

“Canadian Investment Treaty Policy: Stay the Course on Progressive Developments,” by Andrew Newcombe, can be downloaded from the Institute’s website (irpp.org).

Redesigning Canadian Trade Policies for New Global Realities, edited by Stephen Tapp, Ari Van Assche and Robert Wolfe, will be the sixth volume in the IRPP’s The Art of the State series. Thirty-one leading academics, government researchers, practitioners and stakeholders, from Canada and abroad, analyze how changes in global commerce, technology, and economic and geopolitical power are affecting Canada and its policies.

-30-

The Institute for Research on Public Policy is an independent, national, bilingual, not-for-profit organization based in Montreal. To receive updates from the IRPP, please subscribe to our e-mail list.

Media Contact: Shirley Cardenas tel. 514-594-6877 scardenas@nullirpp.org