Redesigning Canadian Trade Policies for New Global’s Realities

Overview of the Research Findings

Stephen Tapp, Ari Van Assche and Robert Wolfe

Hon. John Manley is president and CEO of the Business Council of Canada. A former deputy prime minister of Canada, he was first elected to Parliament in 1988, and he was re-elected three times. From 1993 to 2003 he served as minister in the cabinet portfolios of industry, foreign affairs, and finance. Following 9/11, he chaired the Ad Hoc Cabinet Committee on Public Security and Anti-Terrorism, serving as counterpart to Governor Tom Ridge, the first US secretary of homeland security. Since leaving government in 2004, he has been active in public policy as a media commentator, speaker and adviser to governments of differing political stripes. An Officer of the Order of Canada, he serves on the boards of several publicly traded companies and is active in the not-for-profit sector.

Brian Kingston is vice president of policy, international and fiscal Issues at the Business Council of Canada. He is a graduate of the Accelerated Economist Training Program, a leadership development program that includes placements at the Department of Finance, the Treasury Board Secretariat and the Privy Council Office. In addition to his experience in business and government, he is active in the nonprofit sector as the vice-president of global operations at Young Canadians in Finance and on the board of the Ottawa Economics Association. He holds a bachelor’s degree in economics and a master’s degree in international affairs from the Norman Paterson School of International Affairs, Carleton University.

Redesigning Canadian Trade Policies for New Global Realities, edited by Stephen Tapp, Ari Van Assche and Robert Wolfe, is the sixth volume of The Art of the State. Thirty leading academics, government researchers, practitioners and stakeholders, from Canada and abroad, analyze how changes in global commerce, technology, and economic and geopolitical power are affecting Canada and its policy.

With one in five Canadian jobs linked to exports, international trade is critical to Canada’s long-term prosperity (see De Backer and Miroudot, in this volume). Central to securing this prosperity will be a trade and commerce strategy that positions Canadian firms to take advantage of global markets. Much has changed in the world since Canada and the United States signed a free trade agreement in 1987, so trade policy must be updated to reflect the ever-evolving and increasingly competitive global business environment. With trade negotiations at the World Trade Organization (WTO) largely stalled in recent years, countries instead have sought preferential market access through bilateral and regional trade deals. Canada risks continuing to lose global market share if it fails to keep pace with other countries by aggressively seeking out new market opportunities. An ambitious trade agenda over the past decade has been welcome, but more can and should be done to advance Canada’s commercial interests abroad. This commentary outlines several areas for action to help Canada improve its status as a leading trading nation in the twenty-first century.

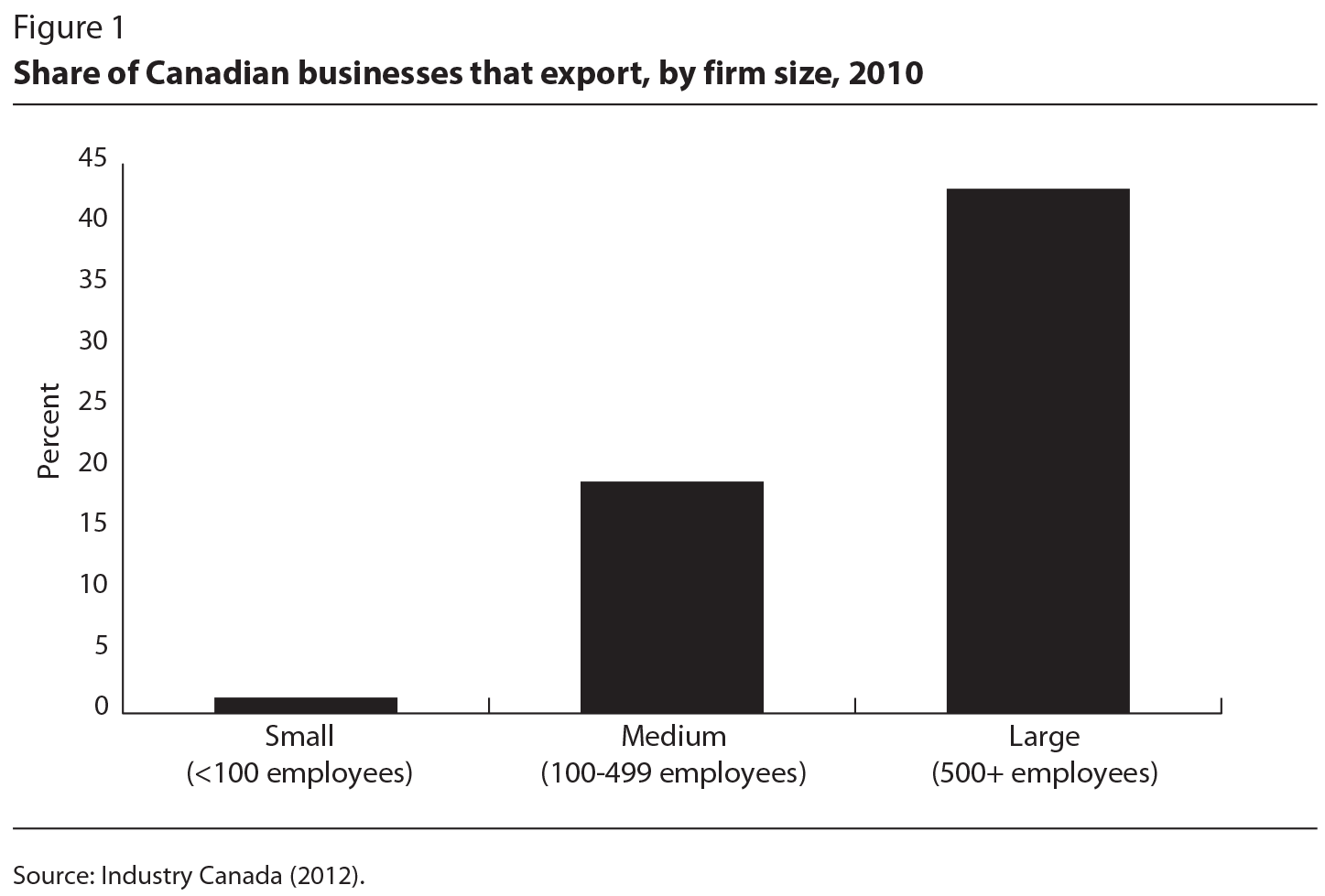

Canada’s trade policy should reflect the reality that large firms drive international trade. Indeed, firm-level research repeatedly has found that the propensity to export increases with firm size (see Lapham, in this volume). As figure 1 shows, the share of Canadian businesses that exported was just over 1 percent for small businesses (defined as those with fewer than 100 employees) in 2010, but 43 percent for large enterprises (those with 500 or more employees); see also Baldwin and Yan’s trade and productivity chapter, in this volume.

These findings reflect the fact that few small and medium-sized businesses tend to be the “first movers” into new international markets; most often, big businesses lead the way. This is not surprising, since the majority of small companies focus on their local markets. As firms grow, they acquire more of the resources and capabilities they need to compete internationally, including legal and linguistic support, access to export financing, greater management depth and access to international networks and partnerships. As a result, larger firms are generally more able to commit significant resources to new markets for a longer period — something that is often essential to succeed.

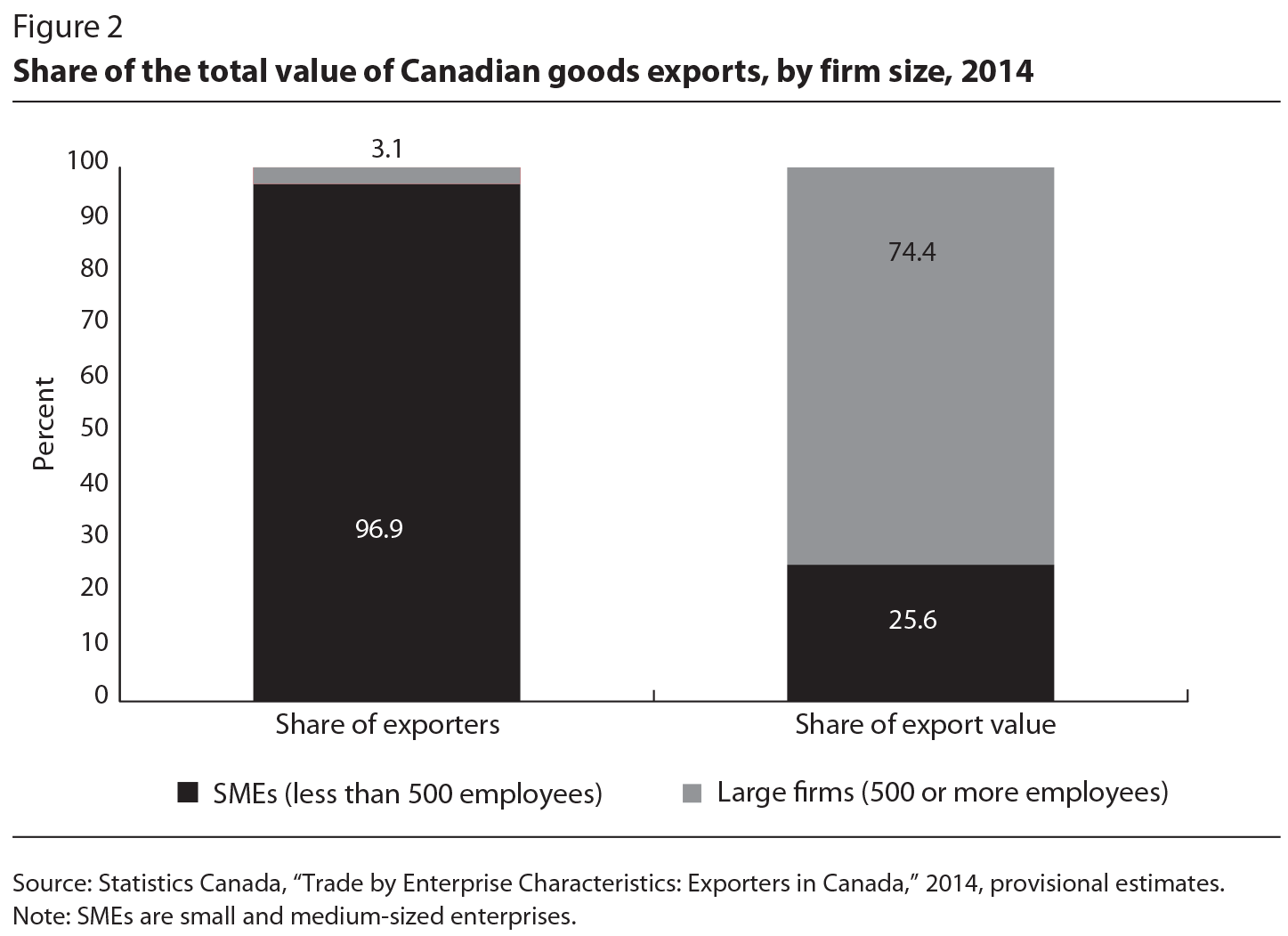

Large firms are not only more likely to export; they are also responsible for a disproportionate share of Canada’s exports. Despite accounting for just 3 percent of Canadian goods-exporting enterprises, large firms contributed almost three-quarters of the total value of goods exports in 2014 (figure 2). Moreover, the top 10 Canadian exporters accounted for almost one quarter (24.8 percent) of the total value of goods exported, while the top 50 firms generated more than half (54.5 percent).1 These results vividly illustrate the paramount importance of large firms for Canadian trade.

A key challenge for Canadian firms is their declining competitiveness in the United States, Canada’s largest foreign market. China, in particular, has gained significant ground on Canada there. Preliminary trade data show that in 2015, the total value of US-China trade reached $598 billion, surpassing US-Canada trade ($576 billion) for the first time in history (US Commerce Department).

Halting Canada’s relative slide in the US market thus should be a key priority. For Canadian firms, this will entail a renewed focus on containing costs and improving the productivity of their Canadian operations. For some, it might involve expanding operations in the United States, where production costs are often lower.

Streamlining cross-border trade would help keep noncommodity exporters based in Canada instead of being attracted south by competitiveness factors. Recent enhancements under the Canada-United States “Beyond the Border Action Plan” — a joint government approach to security and economic competitiveness — such as the eGate pilot project at the Peace Bridge between Fort Erie, Ontario, and Buffalo, New York, demonstrate how technology can make border crossings faster and easier while enhancing security. Meanwhile, improvements to the Customs Self-Assessment program would enable more Canadian firms to take advantage of the opportunities presented by global supply chains.

But more can be done to streamline cross-border trade (Miller, Dillon and Robertson 2014). Border infrastructure should be improved, and the Beyond the Border pilot projects should be broadened into generally applied border procedures. In the next phase of the work of the joint Canada-United States Regulatory Cooperation Council, the adoption of an “align or explain” mechanism would greatly accelerate efforts to achieve common standards for health, safety and the environment. This more ambitious approach would make it the default to harmonize Canadian regulations with those of the United States, unless a unique Canadian factor (for example, geographic considerations such as colder winters) or a national interest rationale justifies maintaining a difference. Better regulatory cooperation with the United States would give Canadian companies a competitive advantage in global markets.

Although many Canadian businesses are already well-established in global markets, ensuring that Canada does not fall behind other countries is important if Canadian firms are to grow their international presence. The WTO remains the best venue for pursuing global trade liberalization, and a strong, modern, multilateral trading system would be a huge benefit for Canada. In the absence of progress in the WTO’s long-drawn-out Doha Round, however, Canada must seek new markets in other forums, such as through bilateral and regional deals.

The Canada-European Union Comprehensive Economic and Trade Agreement (CETA) is one of the most important trade deals Canada has entered into since the Canada-US deal struck nearly three decades ago. The recently agreed, but not yet ratified, Trans-Pacific Partnership (TPP) is also critical for advancing Canada’s interests in the Asia-Pacific region. In 2013, TPP members had a combined gross domestic product (GDP) of nearly US$28 trillion. The consumer market potential is huge, with TPP countries home to nearly 800 million people. Economic modelling suggests that the TPP could yield annual income gains of US$9.9 billion for Canada (or 0.5 percent of GDP by 2025) and increase exports by US$15.7 billion (2.6 percent of GDP) (Petri and Plummer 2012). Another important step to opening up business opportunities in the Asia-Pacific region would be to conclude the ongoing bilateral trade negotiations with India (the Canada-India Comprehensive Economic and Partnership Agreement, or CEPA; see Rao and Tapp 2015).

Ratifying and implementing deals such as CETA, TPP and CEPA will not be easy, but with them in force, Canada could enhance its position in global trade and commerce networks with preferential market access to some of the world’s largest and fastest-growing economies.

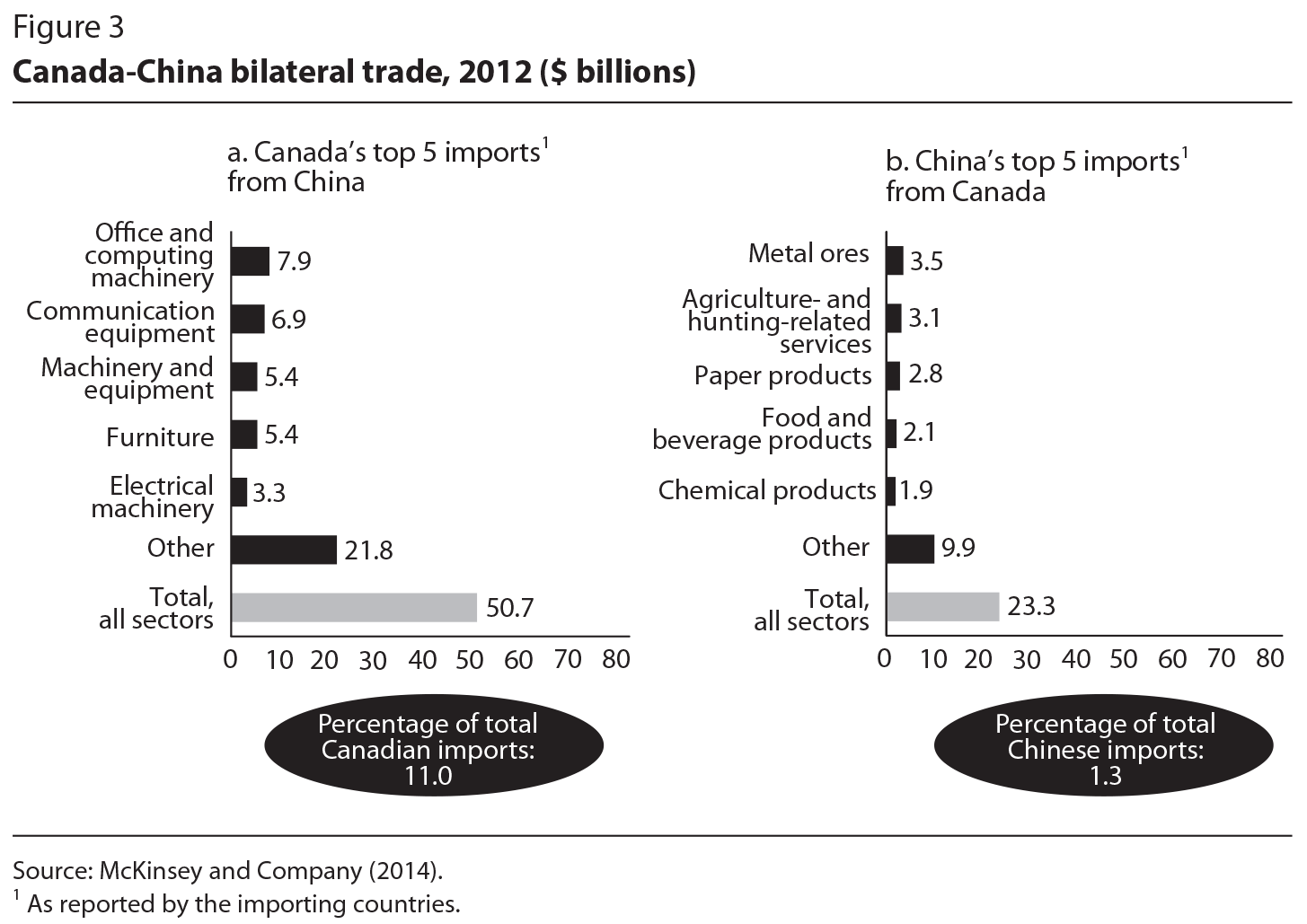

Perhaps the biggest missing element in Canada’s current trade strategy is a cohesive plan to improve the country’s engagement with China (Dobson and Evans 2015). As figure 3 shows, Canada supplies only 1.3 percent of Chinese imports, even though Canada can offer China much of what it needs in terms of food, resources, expertise in infrastructure and clean technology. Canada also has significant opportunities in China’s services sector, including financial services. The recent Foreign Investment and Trade Promotion and Protection Agreement with China is a welcome step toward enhanced relations, as is the new renminbi trading hub in Canada — the first trading hub for China’s currency in the Americas, launched in Toronto in 2015. To take advantage of these opportunities, Canada should seek to negotiate a bilateral free trade agreement with China.

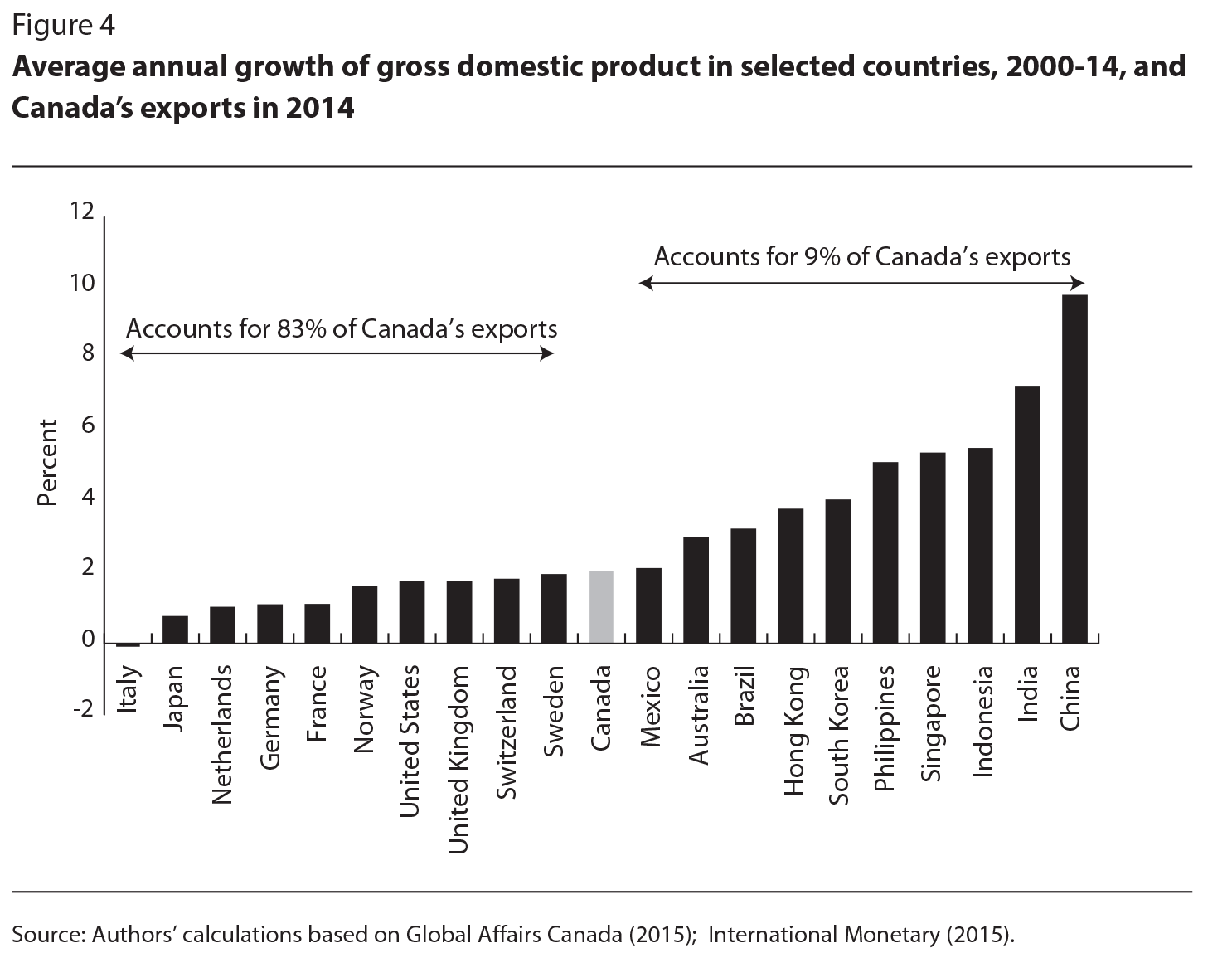

The share of emerging markets — which some forecasters expect to account for over half of the world’s wealth and global trade by 2050 (Gowlings 2012) — in Canada’s overall trade mix remains underdeveloped (figure 4). Rebalancing Canada’s trading relationships thus could offer big payoffs — for instance, the Bank of Canada estimates that, if Canada had the same level of exposure to emerging markets as the United States does, our exports would be $60 billion higher (Macklem 2013).

With Canada’s trade heavily weighted towards slower-growing economies — and much more so than several other advanced economies against which Canada competes — the challenge is for Canadian businesses to recognize the opportunities in emerging markets and for the Canadian government to design policies to level the playing field. As a start, taking advantage of opportunities in emerging markets will require a larger presence by the Trade Commissioner Service in Asia and South America, including in the mega-cities of these regions, where Canada’s commercial relationships are deepening.

Policy-makers need to examine new forms of commerce and consider what Canada must do to remain relevant in a world where economies have become deeply integrated. Global supply chains require firms to import inputs from all over the world in order to be competitive exporters. Outdated trade policies such as protectionist tariffs inhibit the ability of firms to link into efficient, integrated supply chains.

Ciuriak and Xiao (2014) conclude that removing all tariffs on goods entering Canada would boost economic growth, lower prices, attract investment and position Canada as a centre of trade activity. They estimate that unilateral tariff elimination would generate $20 billion a year in economic activity, equivalent to a 1 percent increase in Canada’s GDP — an amount nearly five times greater than the total revenue the federal government collects each year in duties.

As the global economy becomes more integrated, Canadian trade policy must adapt to ensure that businesses can access global markets easily. One way to achieve this is through clearer and more consistent rules of origin. Rules of origin determine which products qualify for preferential tariffs, which are subject to quotas or antidumping rules and whether products are subject to special labelling requirements. Determining where a product “comes from,” however, can be difficult in an era when, as the WTO puts it on their Web site, “raw materials and parts criss-cross the globe to be used as inputs in scattered manufacturing plants” (World Trade Organization, n.d.).

Designing trade policy for a globalized world also requires better data and for the significant gaps in the existing knowledge base to be filled. A better understanding of the Canadian economy and its international linkages is needed, and data collection by Statistics Canada is critical to achieving this end. Recent improvements in the quality and coverage of foreign affiliate sales data are a welcome and important development, but more could be done to include annual sales and employment data on Canadian foreign affiliates by sector and country.

Since 2000, Canada’s position as a leading trading nation has eroded, with its share of global merchandise trade falling from 4.3 percent to 2.5 percent in 2014, losing ground to China, South Korea, Russia, Hong Kong, Italy and the Netherlands (World Trade Organization 2015). Over the same period, Canada’s share of global commercial services trade slipped from 2.6 percent to 1.7 percent. Canada must act now to modernize its trade policy and attempt to reverse this troubling trend.

Expanding trade and accessing new markets is not the federal government’s responsibility alone. It is imperative that Canadian firms develop a global mindset and be ready to share information and collaborate with government — as our competitors are doing — to compete and win new international business.

Burney, D., T. d’Aquino, L. Edwards, and F. Hampson. 2012. Winning in a Changing World. Ottawa, ON: Norman Paterson School of International Affairs. Accessed January 21, 2016. https://www.gowlings.com/knowledgecentre/publicationPDFs/20120626_Winning-in-a-Changing-World-EN.pdf

Ciuriak, D., and J. Xiao. 2014. Should Canada Unilaterally Adopt Global Free Trade? Ottawa: Canadian Council of Chief Executives. Accessed January 21, 2016. https://www.ceocouncil.ca/wp-content/uploads/2014/05/Should-Canada-unilaterally-adopt-free-trade-Ciuriak-and-Xiao-May-20141.pdf

Dobson, W., and P. Evans. 2015. The Future of Canada’s Relationship with China. IRPP Policy Horizons Essay. Montreal: Institute for Research on Public Policy. Accessed January 21, 2016. https://irpp.org/wp-content/uploads/2015/11/policy-horizons-2015-11-17.pdf

Global Affairs Canada. 2015. “Trade Investment and Economic Statistics.” Accessed January 28, 2016. https://www.international.gc.ca/economist-economiste/statistics-statistiques/index.aspx?lang=eng

International Monetary Fund. 2015. “World Economic Outlook Database 2015.” Washington, DC: International Monetary Fund Accessed January 28, 2016. https://www.imf.org/external/pubs/ft/weo/2015/02/weodata/index.asp

Macklem, T. 2013. Global Growth and the Prospects for Canada’s Exports. Speech to the Economic Club of Canada, October 1. Ottawa: Bank of Canada. Accessed January 21, 2016. https://www.bankofcanada.ca/2013/10/global-growth-and-prospects-canada-exports/

McKinsey & Company. 2014. Canada-China Relations: Keeping Up the Momentum. Ottawa: Canadian Council of Chief Executives. Accessed January 21, 2016. https://www.ceocouncil.ca/wp-content/uploads/2014/06/June-2014-Keeping-up-the-momentum-CCCE.pdf.

Miller, E., J. Dillon, and C. Robertson. 2014. Made in North America: A New Agenda to Sharpen Our Competitive Edge. Ottawa: Canadian Council of Chief Executives. Accessed January 21, 2016. https://www.ceocouncil.ca/wp-content/uploads/2014/12/Made-in-North-America-paper-Nov-2014-FINAL-2-Dec-2014.pdf

Petri, P., and M. Plummer. 2012. The Trans-Pacific Partnership and Asia-Pacific Integration: Policy Implications. Policy Brief 12-16. Washington, DC: Peterson Institute for International Economics. Accessed January 21, 2016. https://www.iie.com/publications/pb/pb12-16.pdf

Rao, S., and S. Tapp. 2015. The Potential to Grow Canada-India Economic Linkages: Overlooked or Oversold? IRPP Study 53. Montreal: Institute for Research on Public Policy. Accessed January 21, 2016.

https://irpp.org/wp-content/uploads/2015/08/study-no53.pdf

US Census Bureau. 2015. “U.S. Trade in Goods By Country. “ Accessed January 26, 2016. https://www.census.gov/foreign-trade/balance/index.html#C

World Trade Organization. n.d. “Rules of Origin.” Accessed January 15, 2015. https://www.wto.org/english/tratop_e/roi_e/roi_e.htm

____. 2015. “International Trade Statistics 2015.” Accessed January 28, 2016. https://www.wto.org/english/res_e/statis_e/its2015_e/its15_toc_e.htm