Les politiques commerciales du Canada au carrefour des nouvelles réalités mondiales

Aperçu des résultats de recherche

Stephen Tapp, Ari Van Assche et Robert Wolfe

Depuis des décennies, le Canada cherche à renforcer ses liens commerciaux et d’investissement avec des pays autres que les États-Unis et l’Europe, qui sont ses marchés traditionnels. Someshwar Rao et Stephen Tapp examinent dans cette étude les possibilités d’un accroissement des relations économiques entre le Canada et l’Inde au moyen d’un accord commercial. Les deux pays discutent déjà depuis des années d’un accord de partenariat économique global (APEG), mais jusqu’à maintenant, les négociations n’ont que peu progressé. Deux événements, toutefois, ont récemment ravivé l’espoir : l’élection d’un gouvernement majoritaire en Inde qui s’est engagé à réaliser des réformes économiques, et la visite de son premier ministre au Canada.

Déjà engagé dans des négociations commerciales avec plusieurs pays, le Canada devrait-il accorder la priorité à celles qu’il mène avec l’Inde ? Les auteurs rappellent que les échanges économiques entre les deux pays se sont rapidement accrus au cours des dernières décennies, quoiqu’ils restent assez limités. Mais plusieurs facteurs montrent que l’Inde a un potentiel de développement à long terme considérable. Ses perspectives de croissance économique sont même parmi les plus favorables au monde. Sur le plan social, le Canada et l’Inde entretiennent déjà des liens étroit ; les deux pays possèdent également une langue commune, des cadres juridiques similaires et des institutions politiques démocratiques. Cependant, soulignent les auteurs, les espoirs de prospérité économique pourraient ne pas se concrétiser en Inde si ses décideurs politiques ne parviennent pas à exploiter les atouts du pays.

Au Canada, les secteurs qui bénéficieraient le plus d’un APEG avec l’Inde sont ceux des ressources naturelles et des services à valeur élevée (finance et éducation, par exemple). Les consommateurs et les entreprises des deux pays pourraient, pour leur part, avoir accès à une plus grande variété de produits, et à des prix inférieurs. Le Canada par contre devrait relever des défis et procéder à des ajustements dans le secteur des services aux entreprises et le secteur manufacturier à forte main-d’œuvre et aux salaires peu élevés.

Les domaines les plus prometteurs dans un éventuel accord sont aussi ceux qui sont les plus sensibles d’un point de vue politique. Les sujets litigieux sont notamment l’investissement direct étranger, les services et la mobilité de la main-dœuvre temporaire ; c’est dans ces secteurs aussi que les barrières au commerce international sont les plus importantes. Toutefois, le Canada et l’Inde pourraient décider de conclure un accord moins ambitieux, et l’élargir ou le restreindre par la suite. Dans une première étape, le Canada pourrait accueillir temporairement un nombre déterminé de travailleurs qualifiés, en échange d’un meilleur accès des investisseurs et des fournisseurs de services canadiens au marché indien. Et même sans conclure d’accord commercial, les deux pays devraient tirer davantage profit des réseaux personnels et d’affaires qui les relient déjà.

Les auteurs soulignent en conclusion que les attentes doivent rester réalistes, parce que l’élargissement du commerce avec l’Inde ne peut être que le fruit d’un travail à long terme. Néanmoins, les bénéfices sont suffisamment intéressants pour le Canada qu’il ne devrait pas les négliger.

After years of securing trade and investment deals with several smaller countries, Canada’s trade negotiators had a breakthrough year in 2014. They concluded a major trade agreement with the European Union, signed another with South Korea and enacted an investment deal with China. These developments followed the federal government’s release of its Global Markets Action Plan — an updated trade policy approach that emphasizes “economic diplomacy” and aims to diversify Canada’s global economic linkages (Foreign Affairs, Trade and Development Canada 2013a).

The need to diversify has been a concern since at least as far back as the 1970s. At that time, Canada sought a “third option” for its trade and investment, to expand on its traditional American and British markets. This desire has become more urgent as a result of Canada’s poor trade performance, as it fell from being the 6th-largest exporter in the world in 2000 to being the 13th-largest in 2011, where it remains today (World Trade Organization 2001, table 11.3; World Trade Organization 2011, appendix table 3). According to Bank of Canada research, the biggest contributor to this weak export performance was not a stronger Canadian dollar, the poor productivity record or what Canada traded. Rather, it was largely due to where Canada traded, mainly with the slower-growing advanced economies and particularly the United States, rather than with the faster-growing emerging markets (de Munnik, Jacob and Sze 2012).

In this study, we investigate one important component of the market diversification strategy: Canada’s potential for strengthening its economic relationship with India — a relationship that has presented mixed signals in recent years.

On the positive side, there have been several promising developments. In 2007, Canada and India concluded negotiations on a foreign investment agreement. In 2009, Canada opened three new trade offices in India. In 2010, the two countries concluded a bilateral nuclear cooperation deal and launched formal trade negotiations for a comprehensive economic partnership agreement (CEPA). In 2012, they established a high-level chief executive officer (CEO) forum to recommend policies to enhance two-way trade and investment.

As well, the two governments set ambitious bilateral goals with clear objectives and specific timelines. The first was to complete the CEPA negotiations in 2013; the second was to significantly increase their bilateral trade to $15 billion annually by 2015. This would require nearly tripling two-way trade in only three years, from $5 billion in 2012 (Department of Finance Canada 2012, chap. 3.2).

In 2014, an opportunity emerged to refresh this relationship. A new Indian government was elected with a majority mandate — the Bharatiya Janata Party (BJP), led by Narendra Modi. The BJP has begun implementing economic reforms to improve the business environment and attract foreign investment, and it is pursuing a more assertive foreign policy. In April 2015, Canada’s trade relationship with India came into the spotlight when Modi visited Canada — the first official visit to Canada by an Indian prime minister in over four decades. During this historic visit, several commercial agreements were announced, the Canada-India relationship was upgraded to a “strategic partnership,” and the two prime ministers vowed to conclude the CEPA by the end of 2015.

However, on the negative side, despite all the hopes that Modi’s high-profile visit raised, there have been few tangible results, and there are signs that India is focusing its attention elsewhere. One sign of the failure to finalize deals in this relationship was that a 2007 investment agreement was subsequently reopened. In addition, the two governments’ original ambitious objectives were either unmet (CEPA talks by 2013) or are unlikely to be achieved ($15 billion in bilateral trade in 2015 — by 2013 it had not yet reached $8 billion).

Skeptics are asking whether the new goal — to conclude the CEPA trade talks by the end of 2015 — will be any more successful. So far, the trade negotiations have plodded through nine rounds. India appears less keen than Canada to reach an agreement and seems willing to do things its way.

For example, at the 2014 World Trade Organization (WTO) meeting, the Indian government prevented the implementation of an existing multilateral trade facilitation agreement, because it felt that that agreement would restrict its ability to provide food subsidies to its poor.1 In another case, India recently became the second largest shareholder in the Chinese-led Asian Infrastructure Investment Bank, and it and the other BRICS countries (Brazil, Russia, China and South Africa) created the New Development Bank. 2 Both of these moves are seen as attempts by the leading emerging markets to create an alternative to the Western-led Bretton Woods institutions of the International Monetary Fund and the World Bank.

The key question is this: with several other trade negotiations underway — especially the 12-country Trans-Pacific Partnership, which appears to be approaching conclusion — should Canada focus resources on concluding a trade deal with India?

We conclude that yes, India does merit being a priority international market for Canada over the long term, and the CEPA could spark a stronger economic relationship. Nevertheless, the players will need to overcome significant obstacles, especially regarding investment and temporary labour mobility, before a truly comprehensive trade deal can be concluded. The challenge for the negotiators and politicians is that the areas that offer the largest long-term potential gains (investment and services) also raise political considerations that will make it difficult for the two sides to finalize a good deal.

Why should Canada focus on India? For one thing, India’s long-term growth prospects are among the most favourable in the world. The Organisation for Economic Co-operation and Development (OECD 2012) forecasts that India’s real gross domestic product (GDP) will grow faster than that of any other country over the coming decades.3 As well, Canada can leverage its strong social ties with India: 1.2 million Canadians have East Indian ancestry (Statistics Canada 2011),4 and India is the second-largest source country for foreign students studying in Canada (Prime Minister’s Office 2012). Finally, the widespread use of the English language in both countries facilitates communication and business dealings; both countries have legal systems based on British common law; and India has democratic political institutions (in contrast to some other fast-growth emerging markets, such as China).

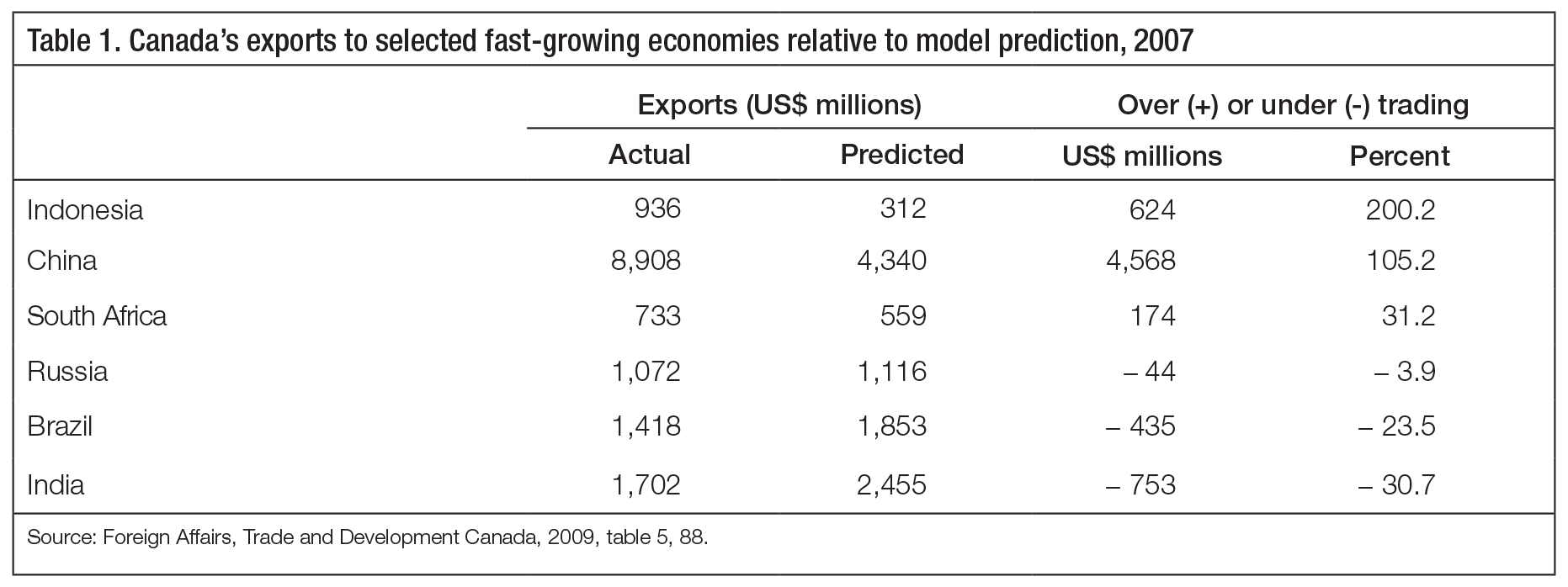

Some estimates suggest there is significant untapped potential to expand Canada-India trade. Canadian exports to selected fast-growing emerging markets in 2007 are shown, with predictions (based on an econometric “gravity” model), in table 1.5 Among the high-growth trading markets with which Canada does not have a trade deal, India was the largest underperformer, according to the predictions. Moreover, these results suggest that Canada is overtrading with China relative to the model’s prediction.6

In this study, we adopt a long-term perspective on the economic opportunities and challenges that stronger economic linkages with India might bring to Canada. After outlining Canada’s trade and investment patterns with India over the past two decades, we present the revealed comparative advantages for both countries in merchandise and services export categories.

We also introduce new perspectives based on recently developed value-added trade data. Based on a review of current trade and investment barriers between Canada and India, we suggest which industries would benefit most from a trade deal, and which would struggle most to adapt to the new trade environment. We find that the Canadian sectors that would benefit most from a CEPA with India are our natural resource and resource-based manufacturing industries, telecommunication services, and insurance and other commercial services (which include engineering, consulting, education and health). Sectors that would face more acute challenges include computer service industries and low- and middle-wage labour-intensive manufacturing.

We evaluate how a CEPA would affect each country’s broader trade strategy and outline the key negotiating issues and potential stumbling blocks to concluding a deal. Our results update and complement previous studies, which include the Foreign Affairs, Trade and Development Canada, and Canada-India Joint Study Group (2010), Goldfarb (2013), Canadian Chamber of Commerce (2012) and Dobson (2009).

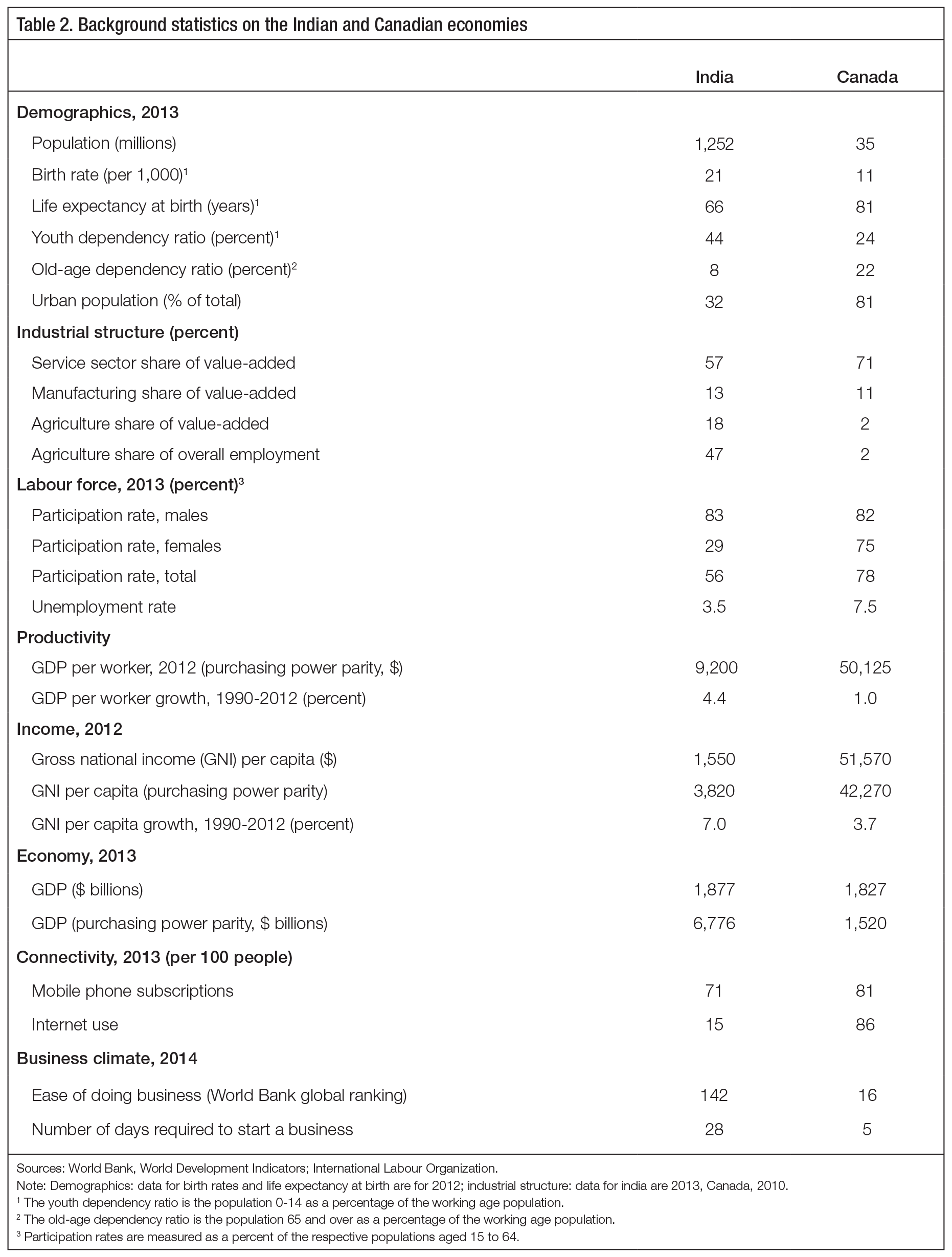

With over 1.2 billion people, India is the second-most-populous country in the world, and it is the world’s largest democracy. In 1991, a balance-of-payments crisis in India prompted a series of policy reforms. Over time, its economic policies have shifted away from an inward-looking, command-and-control approach toward an outward-looking, market-oriented approach and in this process its economy has undergone numerous structural changes. Opening up to the world has benefited the country, which is now one of the fastest-growing economies. Over the past decade, its real GDP grew by a remarkable average rate of 7.4 percent per year, and its long-term growth outlook is among the best in the world. Table 2 provides background statistics on the Indian economy and on the Canadian economy for comparison.

India’s population is enormous and is growing quickly, and these demographics can support its future economic growth. In the past two decades, India’s population grew much faster than Canada’s (36 percent versus 22 percent), and in 2012 — the last year for which comparable data are available — India’s birth rate was almost double Canada’s (see table 2).

At the same time, life expectancy is considerably lower in India than in Canada (66 years versus 81 years). The Indian population is much younger: India’s youth (those 14 years of age or younger) represent 44 percent of the working-age population, compared with 24 percent in Canada. Similarly, while population aging will restrain economic growth over the medium term in Canada, India does not face this challenge.

In fact, much of India’s economic growth acceleration is attributable to demographics (Aiyar and Mody 2011). An analysis of state-level census data indicates that changes in the age structure of the population accounted for about 40 percent of India’s per capita income growth in the 1980s and 1990s. Moreover, in the next two decades, this “demographic dividend” — which increases the share of the country’s population in their prime working-age years — could add nearly two percentage points per year to its per capita GDP growth. This represents a significant advantage in the context of the world’s slow economic growth since 2008-09.

India’s urbanization rate is surprisingly low, at 32 percent (well below Canada’s 81 percent), but its pace of urbanization is accelerating due to push and pull factors. High unemployment in villages, lack of services and social conflict push people from the rural areas to urban areas; job opportunities and higher wages in the cities pull them to urban centres. To support the “pull” process, in 2014 the Indian government announced plans to establish 100 “smart” cities that will have improved town planning, infrastructure and livability.

Urbanization increases emerging economies’ productivity by shifting resources from less-productive sectors in villages (primarily in agriculture) into more-productive sectors in cities (largely services and manufacturing). Urbanization and the associated industrial change are particularly important in India because of massive differences between value-added per worker in the formal and informal sectors (the formal sector has a 10-fold advantage) and in -manufacturing and services relative to agriculture. For instance, the hotel and restaurant sector is 3.5 times more productive than agriculture, and manufacturing is 2.6 times more productive than agriculture (Government of India Planning Commission 2014).7

The share of services in India’s economy has grown significantly, from 44 percent in 1990 to 57 percent in 2013, but it remains well below Canada’s 71 percent. The countries’ shares of manufacturing are roughly similar, and India is keen to increase its manufacturing share in order to employ more of its rapidly growing population in better-paying jobs. Recent government initiatives to this end include the high-profile “Made in India” campaign to boost foreign investment in the manufacturing sector.

Agriculture is a sector where India and Canada differ considerably. Agriculture as a share of India’s economy has declined more than 10 percentage points in the past two decades, but it still represents almost half of its employment, compared with only 2 percent in Canada. The flow of workers out of agriculture sector in India is expected to continue, and it has a long way to go to catch up with other emerging economies such as China in this process.

While Canada’s and India’s male labour force participation rates are comparable (83 percent in India and 82 percent in Canada), their female participation rates are quite different: in India it is 29 percent, compared with 75 percent in Canada.8 Because of this large difference between the two countries’ female participation rates, India’s overall labour force participation rate is much lower than Canada’s (56 percent versus 78 percent).

Furthermore, India’s female-to-male labour force participation ratio, as well as women’s broader economic participation and opportunities, ranked a dismal 124th out of 136 countries in 2013 (World Economic Forum 2013). This limited female participation in the economy has seriously restrained Indian growth. Nevertheless, to look at it more optimistically, if major progress can be made in this area, it could be a considerable source of India’s future economic growth.

Labour productivity growth is a key determinant of economic growth and real income gains. From 1990 to 2012, India’s real GDP per worker grew at an average rate of 4.4 percent annually. This is much stronger than Canada’s 1.0 percent per year. But despite this faster growth, India’s labour productivity level was still only 18 percent of Canada’s in 2012, and only 60 percent of China’s. Closing even part of this productivity gap would increase India’s productivity rate considerably in the coming decades.

These significant differences in Canada and India’s productivity levels help explain the large differences in incomes between the two countries. In 2012, India’s per capita gross national income (GNI), measured in purchasing power parity (PPP) exchange rates,9 was only US$3,820, less than one-tenth of Canada’s. Though India’s real GNI per capita grew almost twice as fast as Canada’s between 1990 and 2012 (7.0 percent versus 3.7 percent on an average annual basis), it is important to keep in mind that the living standards and consumption patterns in India’s rapidly growing middle class are much lower than those in Canada. Moreover, poverty remains a huge challenge in India. The World Bank estimated that in 2012, roughly one-quarter of the Indian population (24 percent) was living on only US$1.25 (using PPP at 2005 international prices) per day, and that more than half (59 percent) lived on only US$2.00 a day.

Nonetheless, because of the population difference — there are 36 Indians for every Canadian — India’s overall economy is already slightly larger than Canada’s when converted at market exchange rates to US dollars, and it is over four times larger at PPP exchange rates.

Over the last decade, India has invested a great deal in research and development, physical and human capital, and technological adoption. Its gross investment in capital (including buildings, engineering construction, and machinery and equipment) as a share of GDP ramped up from 24 percent in 2000 to 31 percent in 2013 and is now higher than Canada’s (24 percent). Yet despite its higher capital investment, India’s research and development spending as a share of GDP in 2011, at 0.8 percent, remains well below Canada’s 1.8 percent.

India has also made great strides in accumulating human capital. In the past decade, the secondary school enrolment rate grew more than 20 percentage points, to 69 percent (in 2011). Tertiary enrolment rates have also increased dramatically (from 10 percent in 2000 to 25 percent in 2012), which has helped to provide India with a large pool of skilled and trained professionals. During the 1990s, for instance, the stock of engineers increased from 4.8 million to 7.7 million (Rao 2011). This was an impressive 60 percent increase. To put this put into context, the 8 million engineers in India in 2000 represented roughly one-quarter of Canada’s total population at that time.

In the past, inadequate public sector investment in infrastructure — highways, railways, ports, airports, electricity generation and transmission, telecommunications and schools — has hindered private sector capital investments and restrained India’s economic growth. But over the last decade, India has improved its physical, telecommunications and knowledge infrastructure. The federal government and state governments are encouraging more private sector and foreign participation in infrastructure projects.

Like people in the rest of the world, Indians have enjoyed improved connectivity in the past decade, and the use of mobile phones and the Internet has increased dramatically. In 2000, cell phone ownership was virtually nonexistent, but by 2013, over 70 percent of the population had a cell phone. But overall Internet use in India, at 15 percent, remains far below that in comparable countries such as China, where Internet use is 46 percent.

Another area of difference between Canada and India is energy. In 2011, India was a net energy importer — imported energy is estimated to be 28 percent of its total energy use, whereas Canada was a net energy exporter — exporting an estimated 62 percent of the energy it generated. In India, only three-quarters of the population has access to electricity, and two-thirds of its electricity is generated from coal. This offers Canada potential trade gains as a more important supplier to Indian markets.

Before 1991, India was largely a closed economy with inward-looking policies, and it was often referred to as the “Licence Raj.” At that time, India’s commercial linkages with the world were weak, and its international trade was subject to steep import tariffs, licences and quotas, and export taxes. Foreign direct investment (FDI) was highly restricted by government approvals, limits on equity participation by foreigners, and technology transfer and export obligations for foreign subsidiaries. As a consequence, its net inward FDI was meagre, averaging only US$169 million annually between 1985 and 1990 (representing a negligible share of Indian GDP; over the same period, Canada’s annual average FDI was $5.3 billion, or 1.1 percent of its GDP).

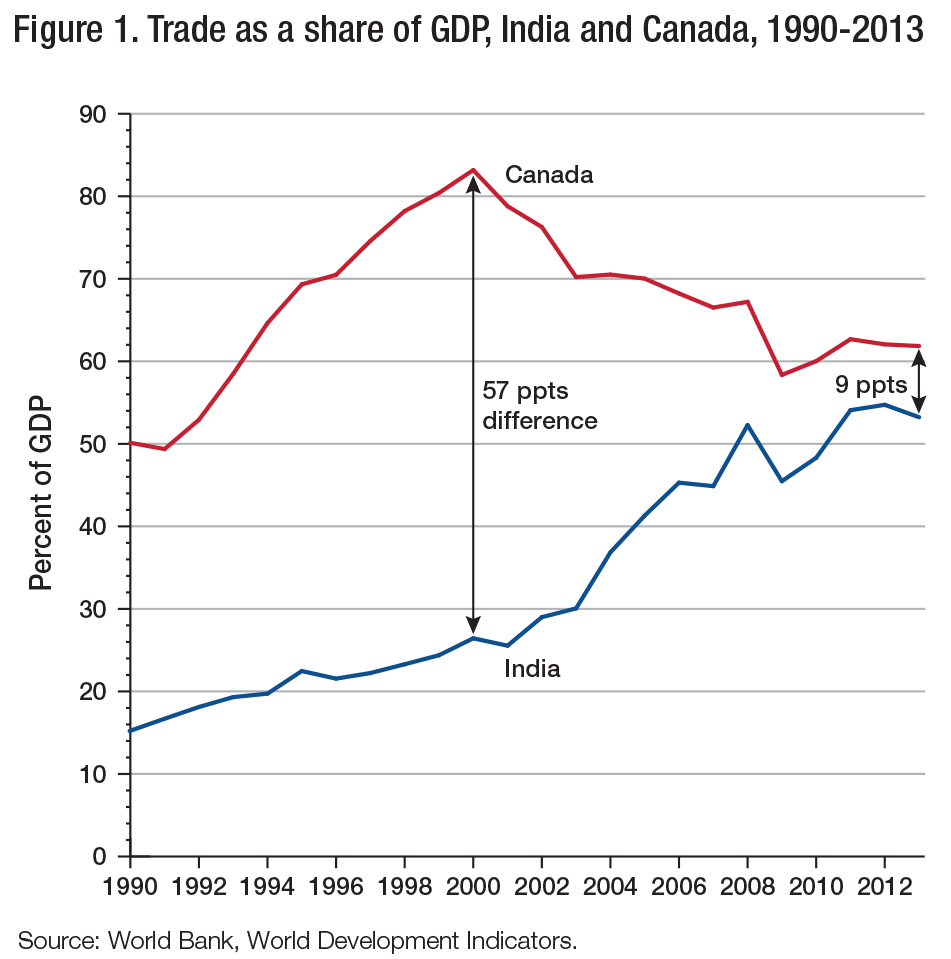

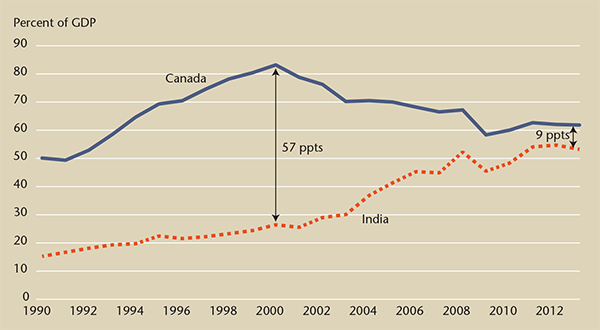

After 1991, India began reducing the barriers to trade and foreign investment. Its overall trade (exports plus imports of goods and services) as a share of GDP increased significantly and approached that of Canada, particularly after 2000 (figure 1). The remarkable growth in India’s trade was driven by a boom in services, particularly information and communications technology (ICT) services exports. In 2013, India was the world’s sixth-largest ICT services exporter — well ahead of Canada, which ranked 17th (WTO Trade Profiles).10

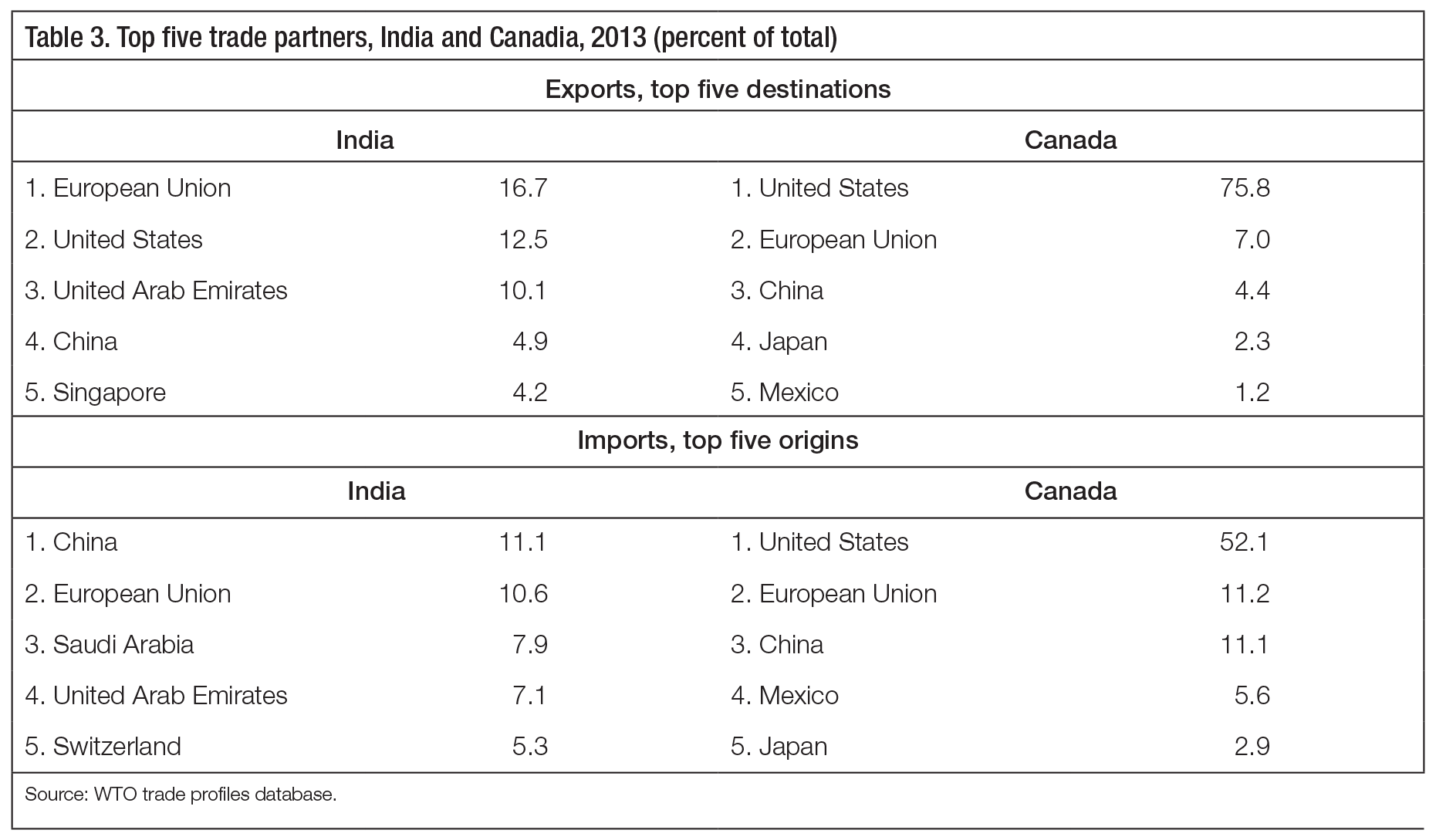

India’s trade is highly diversified, unlike Canada’s, which is much more heavily concentrated one market: the United States (see table 3). The European Union is India’s top trading partner, and the United States, the United Arab Emirates and China are also prominent. Canada is well down the list, ranking 30th in 2008.

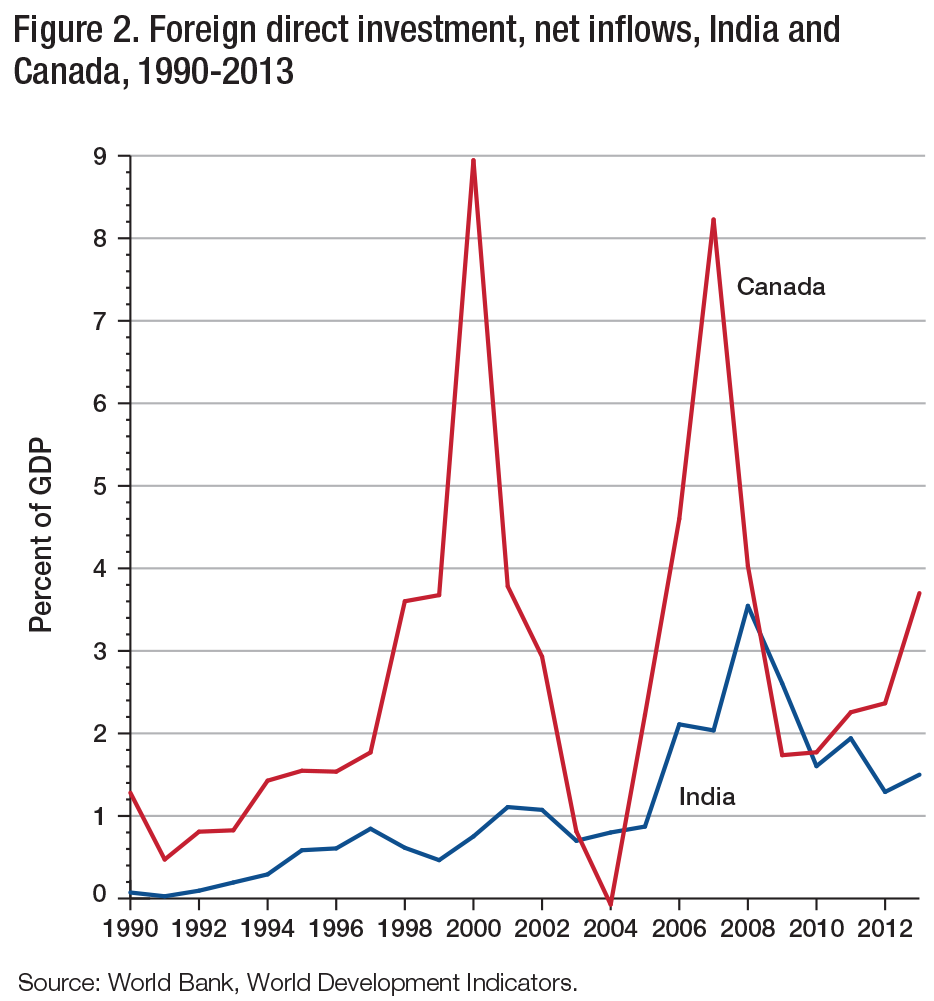

As trade took off in India, its net FDI inflows also steadily increased, peaking as a share of GDP in 2008 before the global recession (figure 2). Its outward stock increased from being virtually nonexistent in 1990 — just 0.1 percent of global outward FDI — to recently reach 1.0 percent of global FDI in 2011 (United Nations Conference on Trade and Development 2012). The experiences of China and other East Asian emerging economies suggest there is substantial room for India to expand its FDI — particularly if it further liberalizes its foreign investment regulations and improves its business climate.

India ranks very poorly in most business climate indicators. In 2014, it placed a dismal 142nd out of 160 countries in the World Bank’s measure of ease of doing business. Recently, the Modi government set an ambitious goal of reaching the top 50 in this ranking by 2017. Canada ranked much better, in 16th place. In a recent survey of business leaders, three factors were cited as the most problematic for doing business in India: inadequate infrastructure, corruption (India ranked 94th in the world on Transparency International’s 2012 Corruption Perceptions Index) and inefficient government (World Economic Forum 2012a, 2012b).

Further increasing the outward orientation of the Indian economy may well improve its business climate and overall economic performance. Research from cross-country business surveys finds that while India has some well-managed firms, the average firm is poorly managed relative to those in other countries (Bloom and Van Reenan 2010). One possible contributing factor is the common tradition in India where companies are passed on to the descendants of the firm’s founder (often sons and grandsons), which can have a detrimental effect on management practices. Interestingly, this study finds that the multinationals in India are much better managed on average than are domestic firms, and that they are operating close to the global knowledge frontier. Thus FDI can help narrow the large cross-country performance gaps by means of improved management practices.

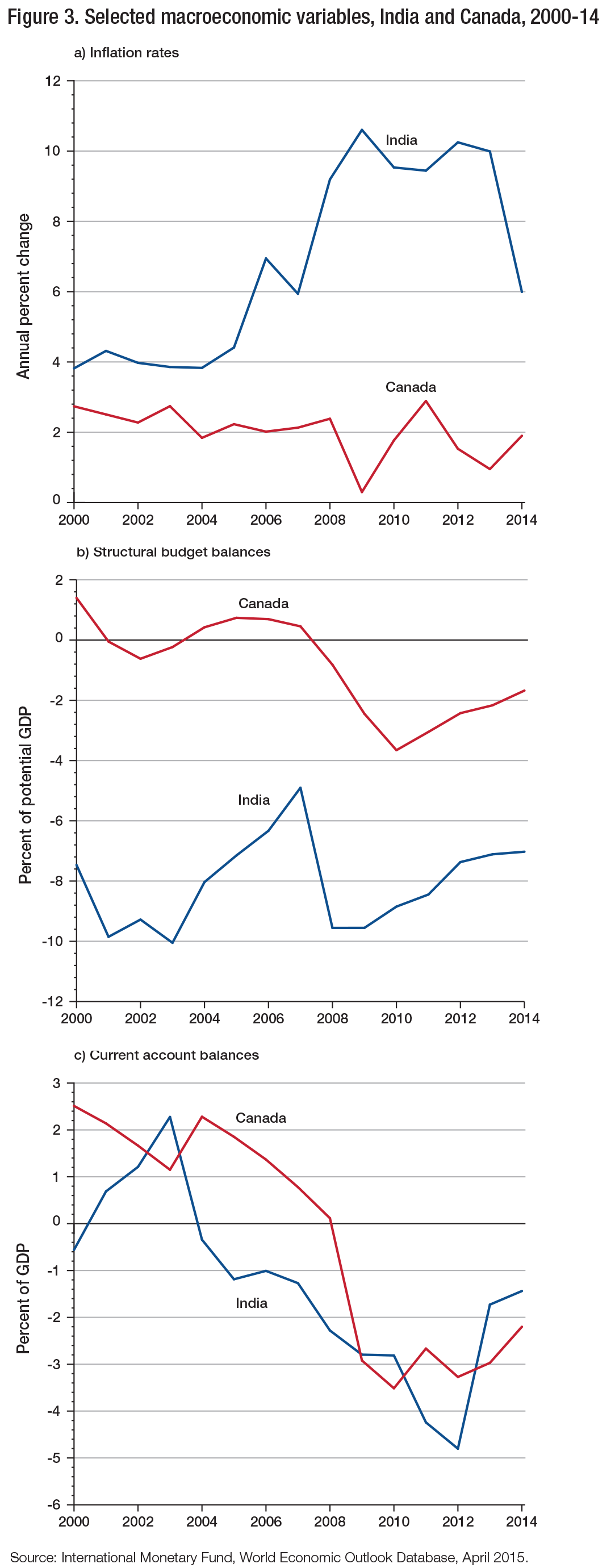

Looking at monetary policy in the two countries over the past decade, inflation has been much more of a concern in India than in Canada, reaching double-digit rates after the global financial crisis began in 2008 (figure 3).11 One key inflationary factor in India has been the persistent difficulty of aggregate supply to keep pace with growing demand, due to bottlenecks and production constraints. More recently, the Reserve Bank of India has managed to bring down the rate of inflation, aided by falling global commodity prices. In the future it will aim for 4 percent annual inflation (within the targeted range of 2 to 6 percent), and it is considering formally adopting inflation targets, as Canada does.

In fiscal policy, budget deficits are also a larger concern in India than in Canada. Over the past decade, the government has run persistent structural budget deficits ranging from 6 percent to 10 percent of GDP.12 Furthermore, in both Canada and India, current account surpluses have turned into deficits over the past decade.

India’s 2015 budget included some important structural economic policy reforms, which were generally well received by economic analysts. For instance, the government will reduce some import tariffs and make some sectors, such as defence procurement, railway construction and insurance, more open to foreign investment. It will introduce a national goods and services tax, which will improve tax efficiency and collection and make trading across states less onerous. With the recent drop in energy prices, it plans to better target public subsidies for energy use via direct cash transfers to people (which can reduce waste due to corruption) and to reallocate spending from inefficient energy subsidies toward much-needed infrastructure projects.

Some international organizations expect India to have among the brightest growth prospects in the world going forward. We share this optimism and have identified several factors that can support India’s future growth: its large domestic market; its “demographic dividend”; its considerable room for continued urbanization and industrialization; its strong ICT services sector; and the potential to narrow the large gaps in productivity, income, technology and business management practices relative to those globally.

But its long-term economic outlook is not entirely upbeat. Many of its potential strengths could turn into weaknesses if they are not properly managed. For instance, the demographic dividend that will bring youth into the labour market in the coming decades means that millions of jobs in the formal sector will need to be created in order to avoid increased unemployment and foregone potential output. This will require improvements to the education system, which is currently failing to provide many students with adequate skills in several regions of the country. Similarly, while urbanization could greatly improve India’s productivity, there will be a need for infrastructure improvements on a large scale and better social programs.

Thus, India’s performance in several critical areas will determine whether its economy realizes its full growth potential. Most importantly, it must improve infrastructure, combat corruption, encourage female labour force participation, and reduce the poor health and education outcomes of the general population. On the macro-policy side, concerted policy efforts are needed to restrain budget and current account deficits, keep inflation stable, and improve the quality of the government bureaucracy.

Revealed comparative advantage (RCA) analysis can identify in each economy the export industries that are more specialized than those in the rest of the world, revealing the sectors where these countries might be more globally competitive.

The Ricardian theory of comparative advantage predicts that a country can increase its economic benefits from freer international trade by specializing its production and exports in products and services where it has a comparative advantage (lower marginal opportunity cost of production) and importing the remaining products and services.

A country’s comparative advantage is shaped by its natural resource endowments, human capital and investments, as well as by other factors, including the effectiveness of its institutions. The theory predicts that a country such as Canada, with its abundant natural resources and educated labour force, will specialize in producing and exporting natural resources products and knowledge-intensive products and services. India, with its large pool of low-skilled, low-wage labour, will tend to specialize in labour-intensive products and services.13

We use export data from the World Trade Atlas and the UN Commodity Trade databases for 96 major commodity and eight service categories and apply Balassa’s (1965) approach to infer comparative advantage by comparing each country’s export shares with global export shares. The RCA index for country i in product or service j is calculated as:

To illustrate the approach, consider the automobile sector, which represents roughly 9 percent of world exports. If automobiles make up more than 9 percent of Canada’s exports, then it has a revealed comparative advantage in cars (RCACAN, Cars > 1). On the other hand, if automobiles represent less than 9 percent of its exports, it has a revealed comparative disadvantage (RCACAN,Cars < 1).

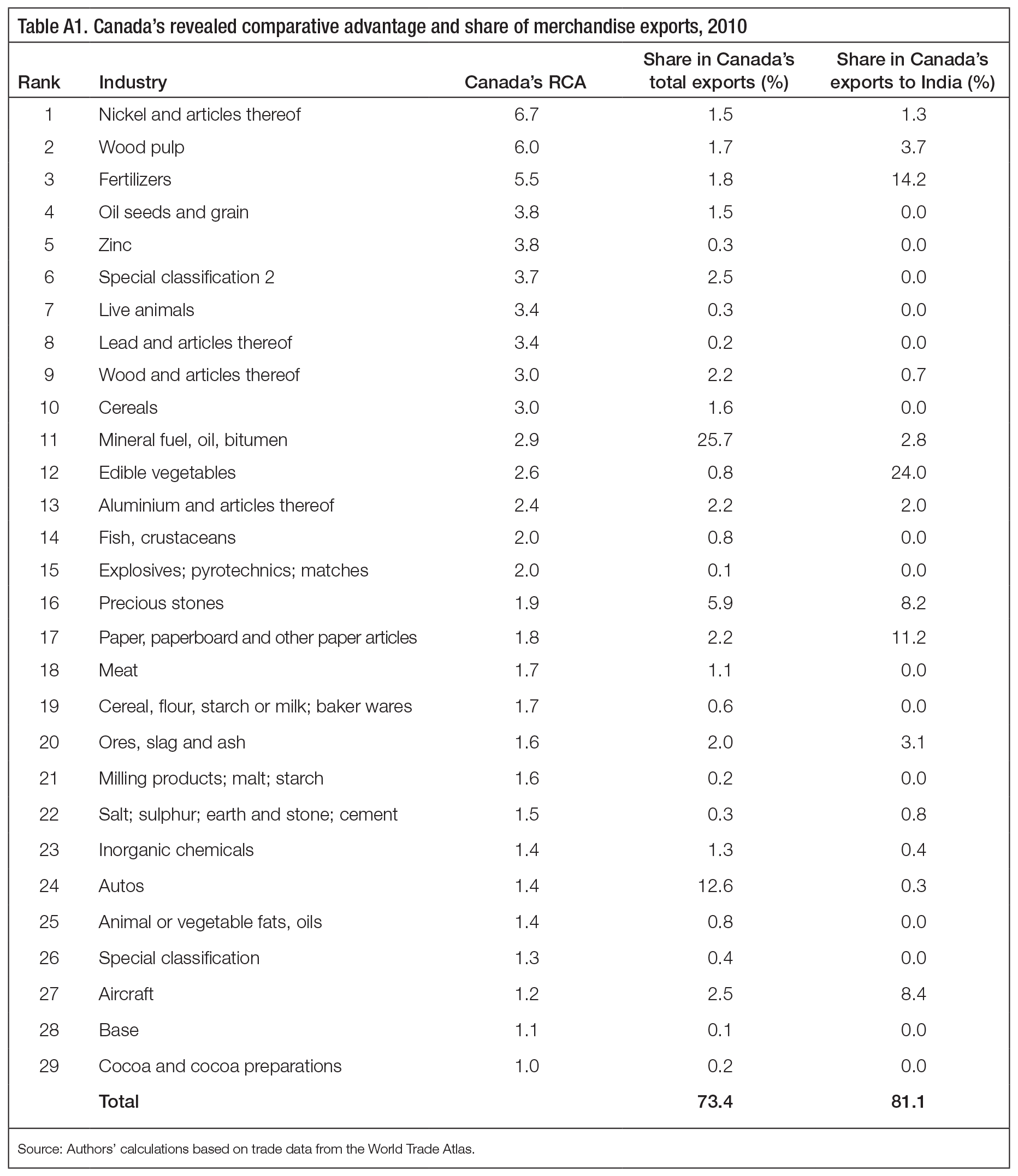

Most of the 29 commodities for which Canada had an RCA in merchandise exports in 2010 involve natural resources, agriculture and related products (see appendix 1). For instance, nickel, wood pulp and fertilizers have RCAs of at least 5, suggesting a strong comparative advantage in these areas. Automobiles and aircraft are also notable. These technology- and capital-intensive products have RCAs under 1.5, indicating Canada has a modest comparative advantage in these industries.14

Together, the 29 commodities for which Canada had a comparative advantage accounted for nearly three-quarters (73 percent) of its total merchandise exports in 2010.15 Of these, the top three exports represented over 44 percent of all merchandise exports: mineral fuel, oil and bitumen (26 percent); automobiles (13 percent); and precious stones and metals (6 percent).

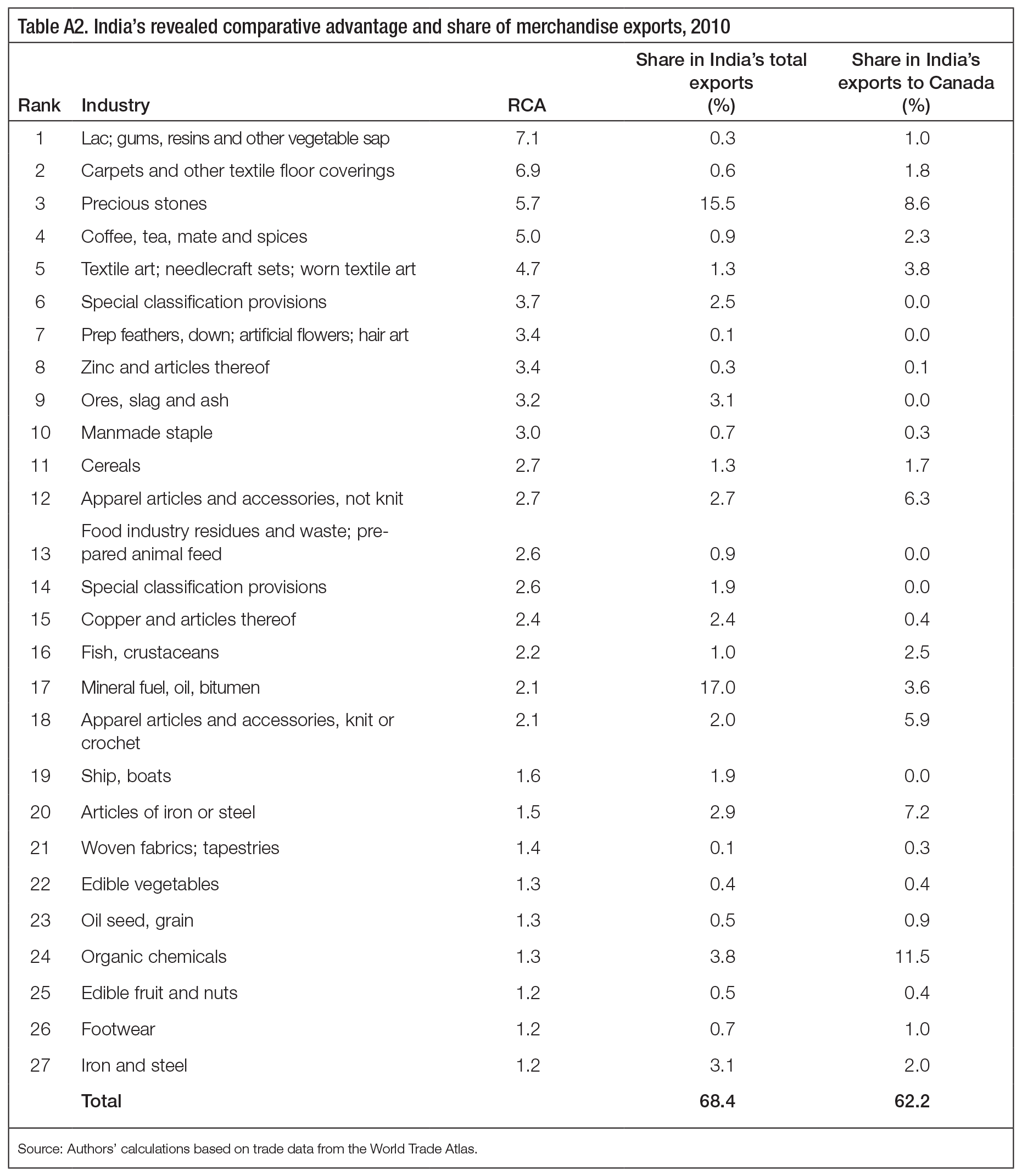

India had an RCA in 27 commodities, which are primarily labour-intensive and natural-resource-based (see appendix 1). Four had a strong comparative advantage, with an RCA of at least 5: lac and vegetable sap; carpets and other floor textiles; precious stones; and coffee, tea and spices.16 India did not have a comparative advantage in any knowledge- and technology-intensive commodity export category.

Overall, India’s RCA commodities made up over two-thirds (68 percent) of its total goods exports in 2010. Much like Canada’s, India’s merchandise exports are highly concentrated in a few major commodities. One-third of India’s merchandise exports came from just two categories: mineral fuel, oil and bitumen (17 percent), and precious stones (16 percent).

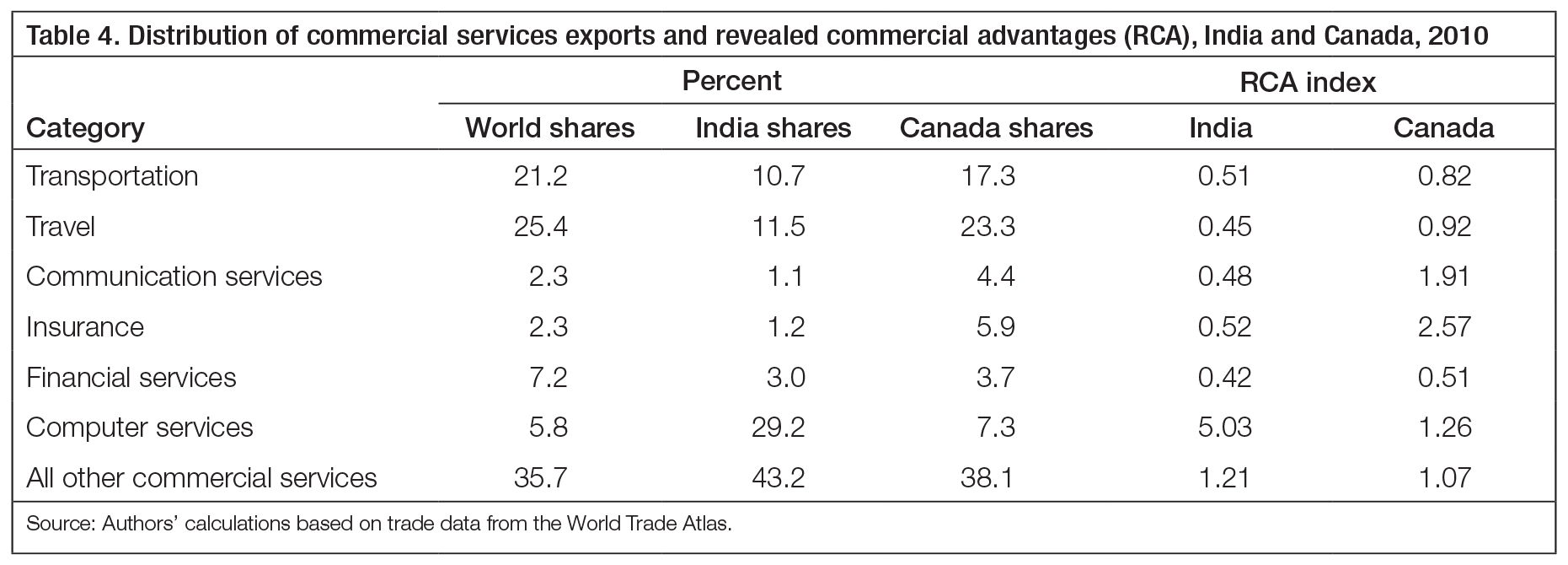

In services trade, Canada is more heavily weighted in the transportation and travel categories (41 percent, compared with 22 percent for India; see table 4). India, on the other hand, is highly concentrated in computer services (29 percent, compared with 7 percent in Canada).

Canada has an RCA in four services categories: insurance, communication, computers, and all other commercial services (management, consulting, engineering, health, construction, -education, and research and development). Together, these categories accounted for over half (56 percent) of its commercial services exports in 2010.

India has an RCA in only two services: computers and all other commercial services. RCA sectors represented a larger share of India’s total exports of commercial services than they did in Canada (72 percent versus 56 percent). India’s comparative advantage in computer services is much larger than Canada’s (of 5.0 versus 1.3). India’s computer services comparative advantage can be attributed to its large pool of labour that has specialized technical training. This abundance of labour results in lower wages for services workers, by global standards.

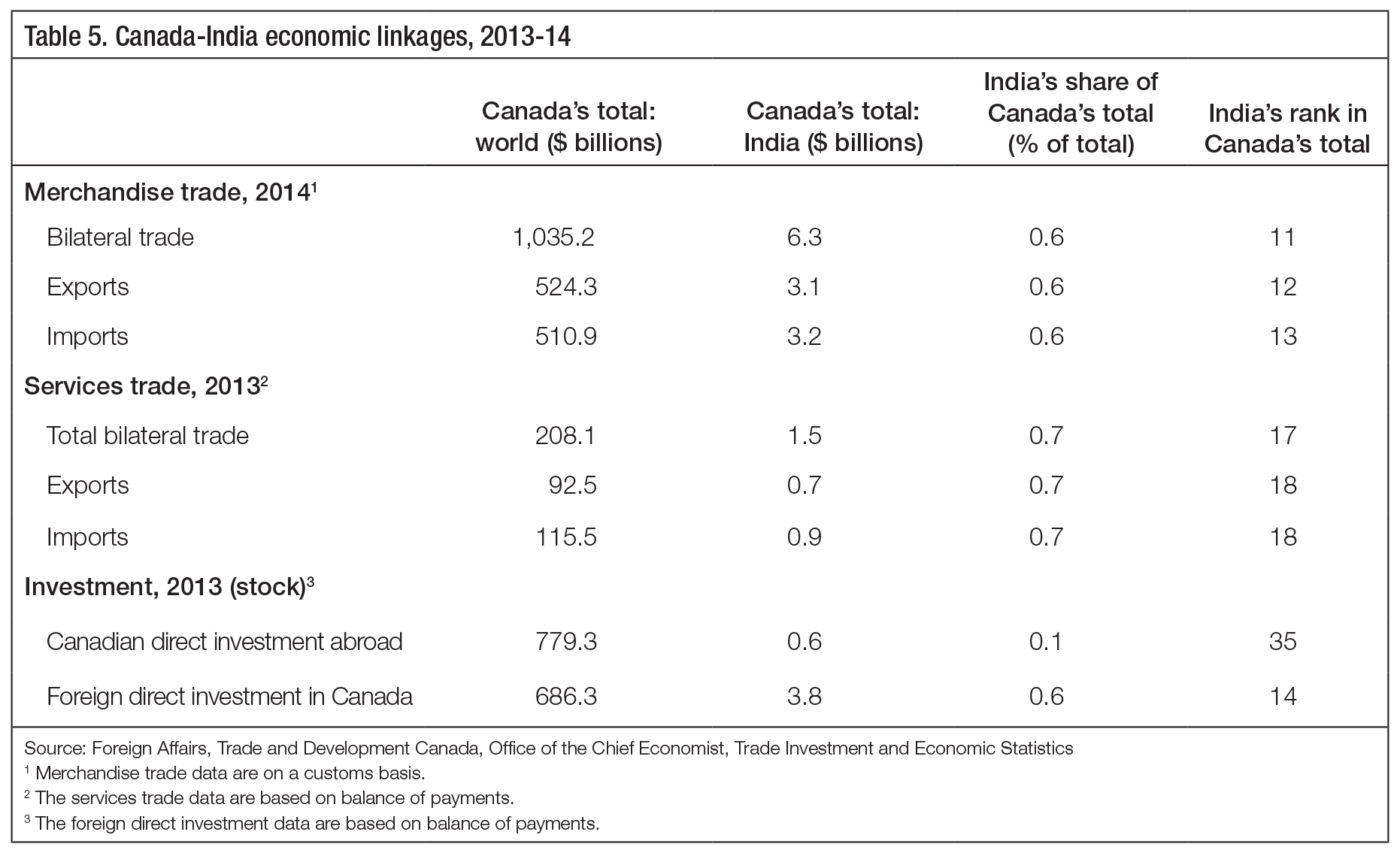

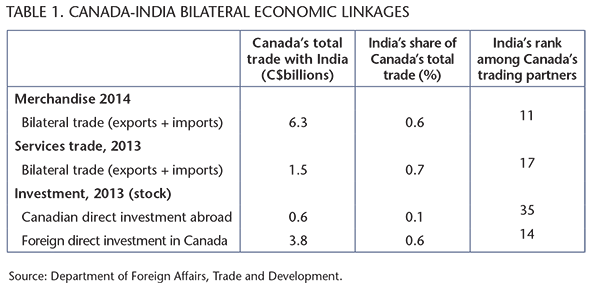

Economic linkages between Canada and India are currently rather weak, but they have grown rapidly over the past two decades. Table 5 reports the most recent data on Canada’s trade and investment, with estimates of bilateral Canada-India linkages and India’s rank relative to other Canadian trading partner countries.

In 2014, two-way merchandise trade was estimated at $6.3 billion. However, these statistics rely on customs data for direct country-to-country transactions. Because trade also occurs indirectly through third countries, they likely underestimate Canada-India trade. For example, a Canadian diamond that goes to India but passes through the diamond district in Antwerp along the way is recorded as a Canadian export to Belgium, not to India.

India’s merchandise trade was just 0.6 percent of Canada’s, and India ranks as Canada’s 11th-largest merchandise trading partner globally. With an estimated $1.5 billion in services trade, India was Canada’s 17th-largest partner in 2013, worth 0.7 percent of the total. Of all of these linkages for Canada, the highest ranked globally is in its merchandise trade with India. By far the weakest link in this relationship is its FDI in India (ranked 35th, and worth only 0.1 percent of its FDI).

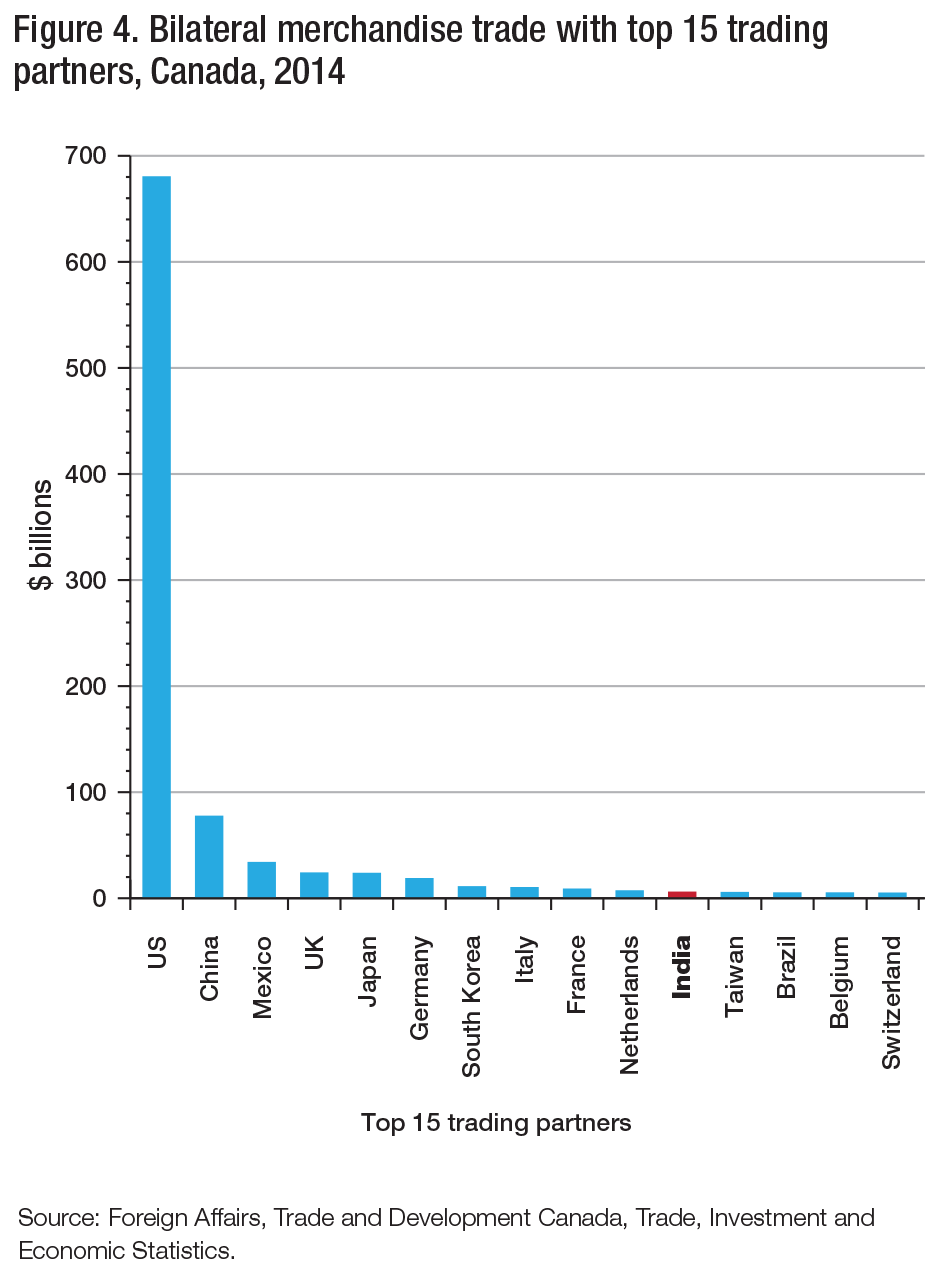

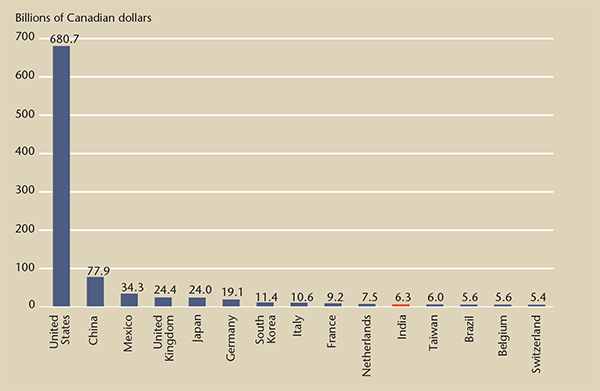

Country rankings do not fully convey the magnitude of the differences between countries, so we can provides additional context by showing Canada’s total bilateral merchandise trade with India relative to its 15 largest trading partners (figure 4). This reveals the paramount importance to Canada of its merchandise trade with the United States. This trade — representing nearly two-thirds of Canada’s merchandise trade — still dwarfs Canada’s trade relationships with other countries by a wide margin, despite considerable diversification in the last decade.

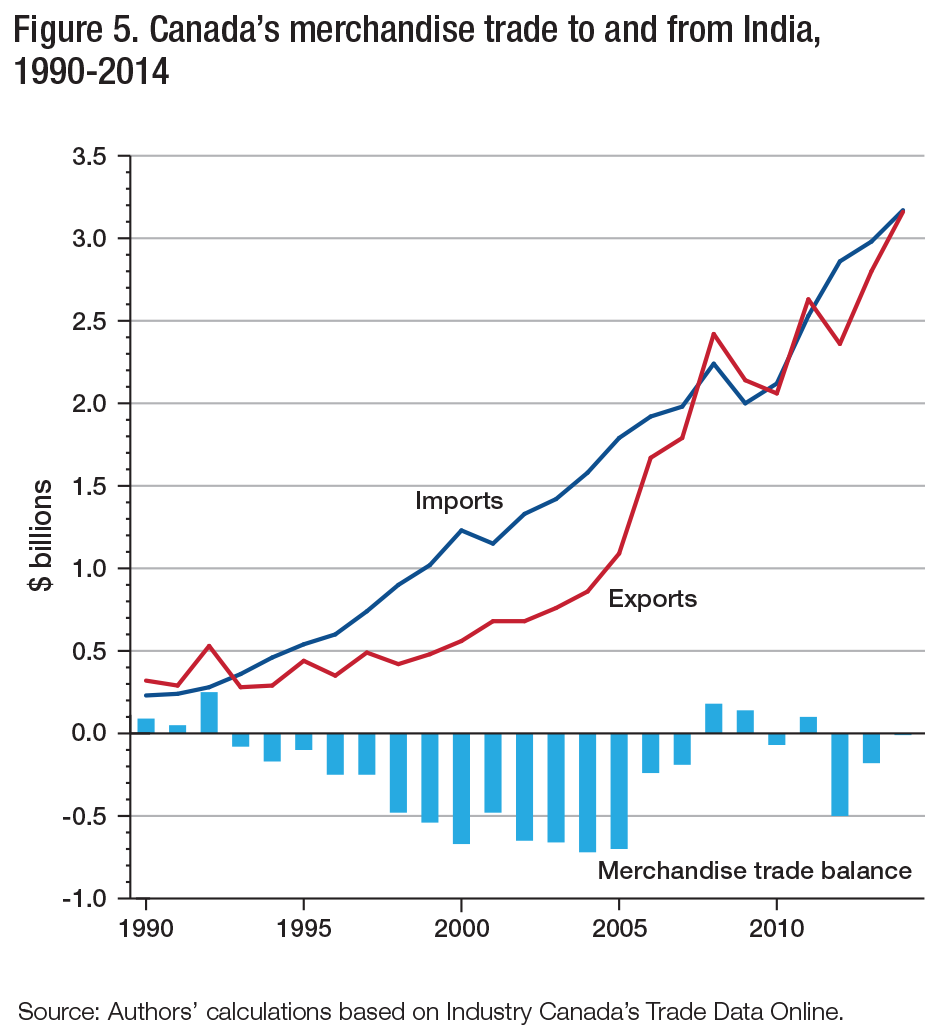

While Canada’s trade with India is currently much less developed than that with countries like the United States, China, Mexico, the UK and Japan, it has grown quickly over the past two decades as India has become more outward-focused (figure 5). From 1990 to 2014, total merchandise trade between Canada and India grew at 10.7 percent per year on average in nominal terms. Canada’s imports from India (11.6 percent) grew more quickly and more steadily than its exports to India (10.0 percent). As a result, in most years Canada ran a modest merchandise trade deficit with India. Also, because Canada’s trade with India grew faster than that with the rest of the world, India’s share of Canada’s trade grew steadily from 0.2 percent in 1990 to 0.6 percent in 2014.

New data from Statistics Canada shows that over 1,500 Canadian enterprises exported to India in 2013,17 and the High Commission of Canada in India reports several concrete examples of Canadian companies that have been successful in the Indian market in a variety of sectors. These include SNC Lavalin, McCain, Bombardier, Magna, RBC, Scotiabank, TD, Manulife, CGI, Open Text and Apotex.18 Some of the larger Indian companies in Canada include Wirpo, Infosys, Tata, Essar and Aditya Birla Group. These companies cover business consulting, information technology, software engineering, outsourcing services, steel and textiles.

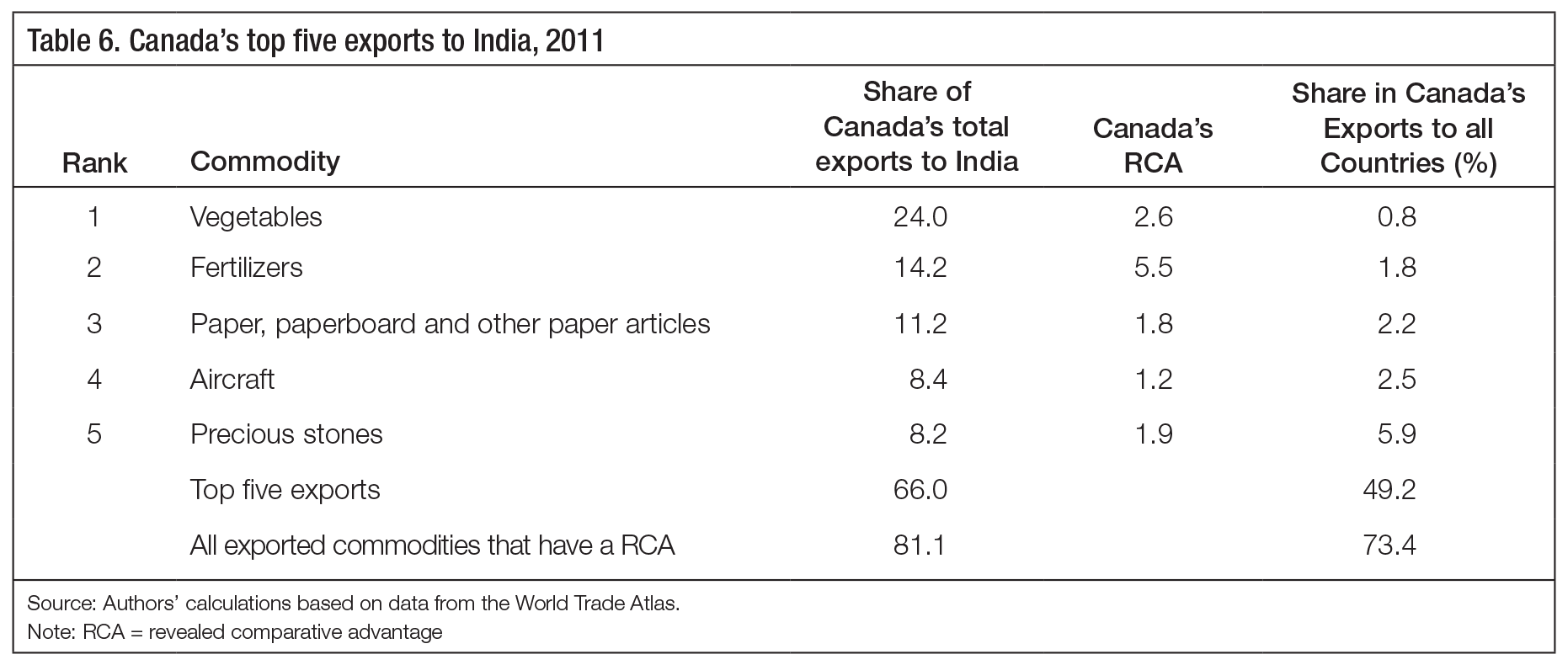

Relative to Canada’s overall exports to the rest of the world, Canadian exports to India are more concentrated in RCA industries. In 2010, 81 percent of Canadian exports to India were in RCA commodities, versus 73 percent of Canada’s exports to the world (table 6). Canada’s top five export categories to India represented about two-thirds of its total merchandise exports to that country: vegetables, fertilizers, paper, aircraft and precious stones. Of these, the largest areas of growth over the past decade for Canadian exports to India were in aircraft, precious stones and fertilizers. The biggest share losers were in wood pulp, edible vegetables, paper and cement.

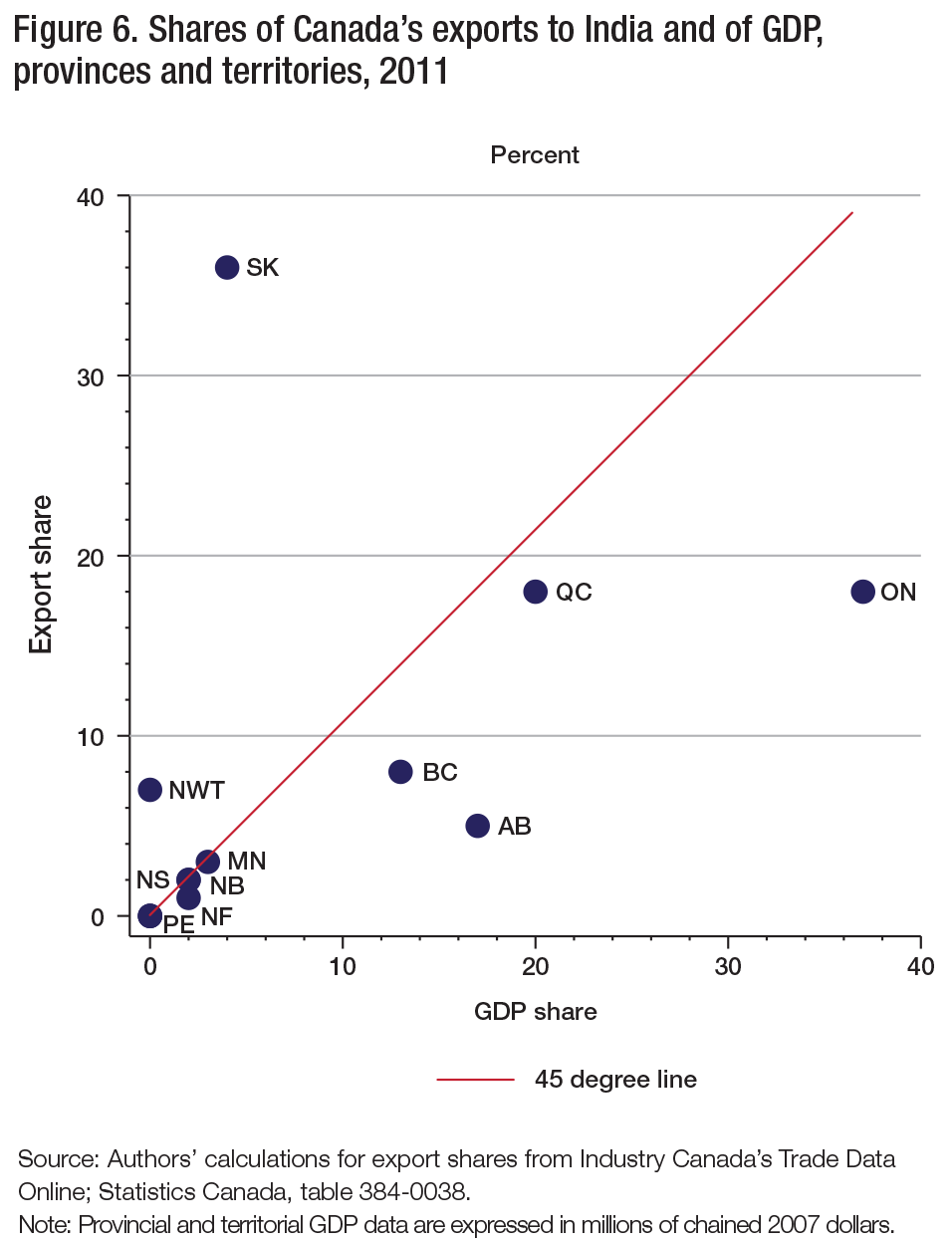

There is a strong regional concentration in Canada’s merchandise exports to India. Disproportionate shares come from Saskatchewan (vegetable products such as pulses, lentils and peas, and chemicals and fertilizers such as potash) and the Northwest Territories (precious stones) (figure 6). Saskatchewan accounts for over one-third of Canada’s exports to India, but only 3.5 percent of Canadian GDP, while the Northwest Territories accounts for over 7 percent of exports from but only 0.2 percent of GDP. Because the shares sum to 100 percent, this implies that other provinces — particularly Alberta and Ontario — export far less than their respective shares of Canada’s GDP.

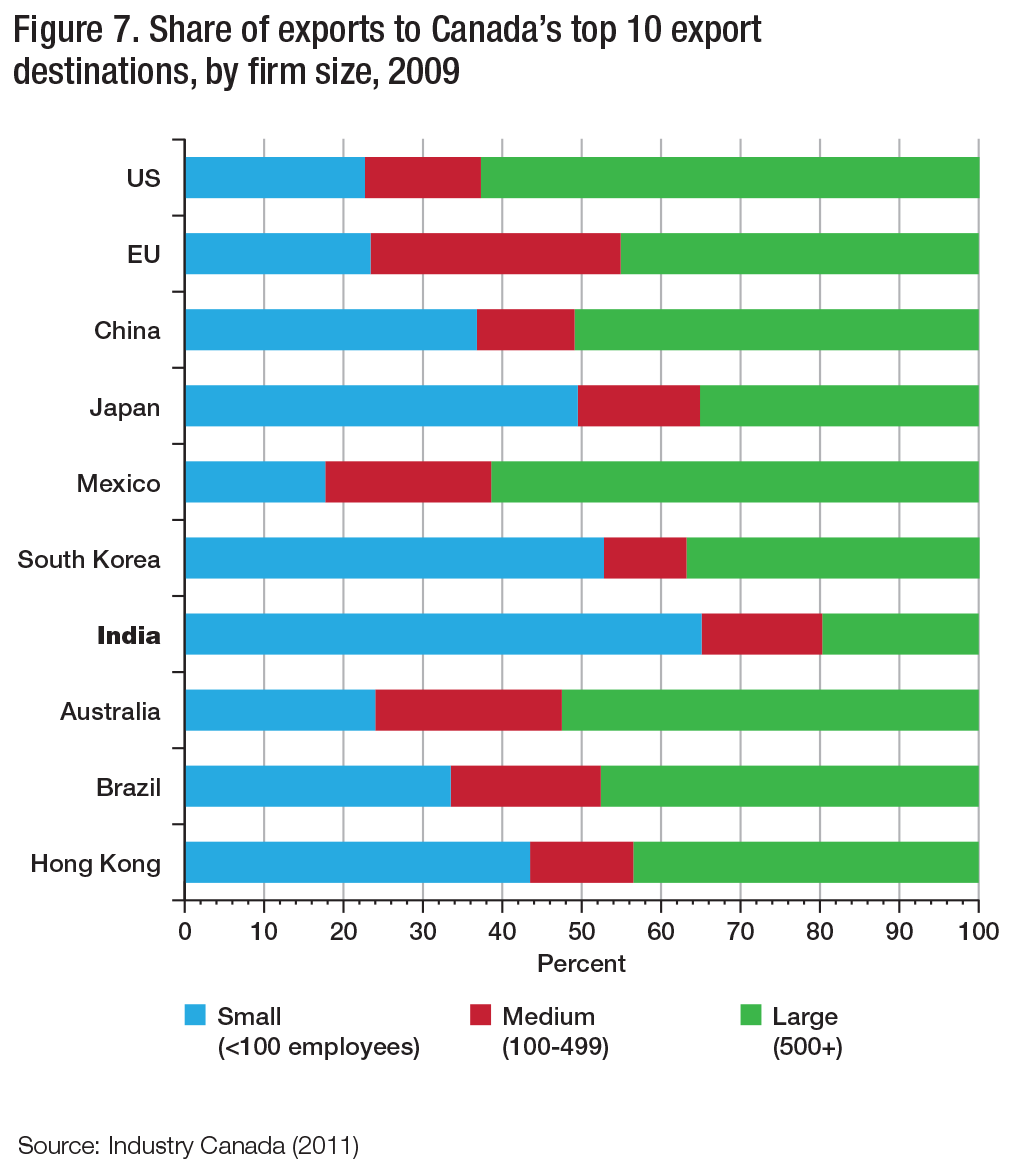

Another noteworthy feature of Canada’s exports to India is the importance of small- and medium-sized enterprises (SMEs). This is in contrast to Canada’s exports to the rest of North America, Europe and even China, where large firms account for a much larger share of total trade. Looking at Canadian export shares by firm size in 2009 (figure 7), exports to India comprise the highest proportion from small firms (fewer than 100 employees), accounting for almost two-thirds (65 percent) of the value of all Canadian exports to India. This is considerably higher than the 26 percent share of exports from small firms in Canada’s overall exports. It is possible that this predominance of trade by small firm relates to the large Indian diaspora. At the same time, it means that large firms (500 or more employees) account for a surprisingly small share of Canada’s exports to India — only 20 percent, compared with 57 percent in Canada’s overall exports. This relative absence of large Canadian firms in India might explain the relatively low export values.

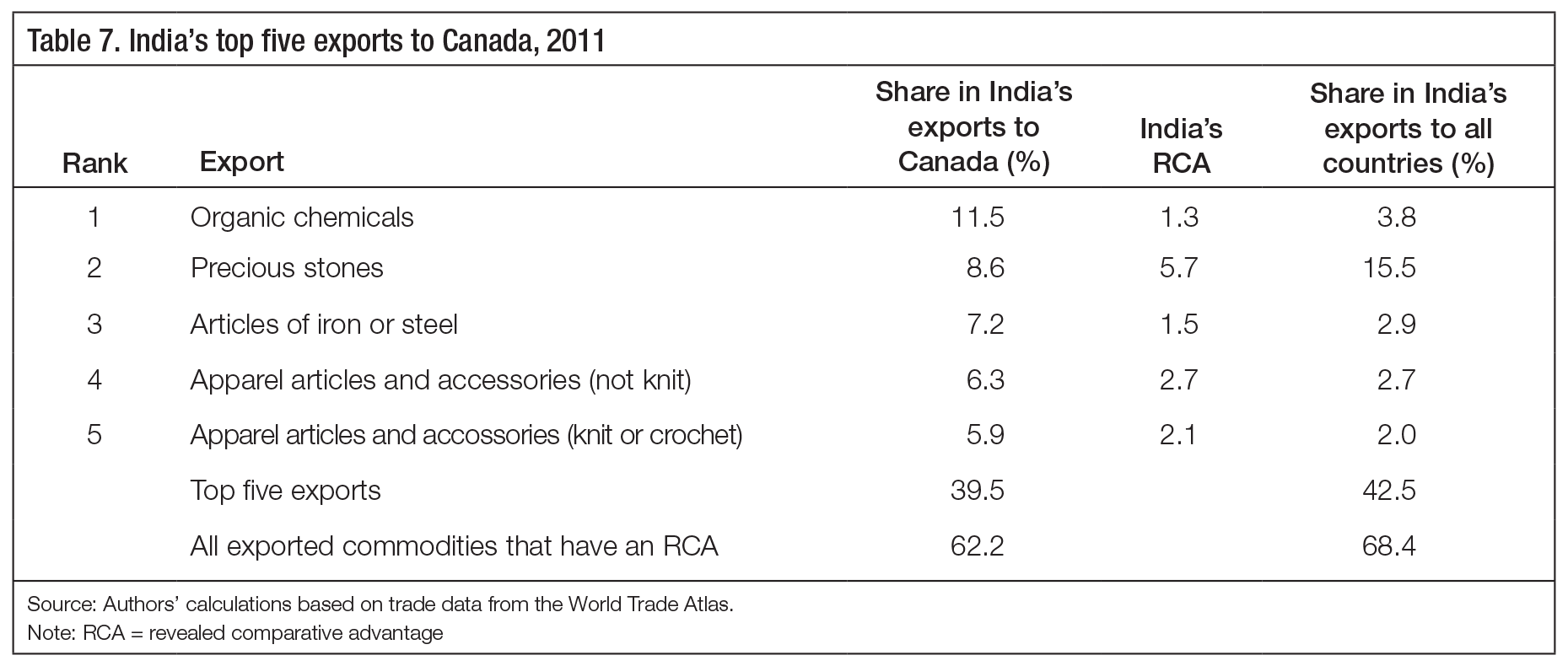

India’s exports to Canada are more widely dispersed. Its top commodity exports in 2010 were organic chemicals, precious stones, iron and steel articles, and apparel and accessories (table 7). These five categories represented 40 percent of India’s total merchandise exports to Canada (versus 66 percent flowing in the opposite direction). Perhaps surprisingly, India’s exports to Canada have become less weighted toward RCA commodities over the past decade — their share fell from 71 percent in 2001 to 62 percent in 2010: the largest decline was in the apparel categories and the largest gains were in organic chemicals and precious stones.

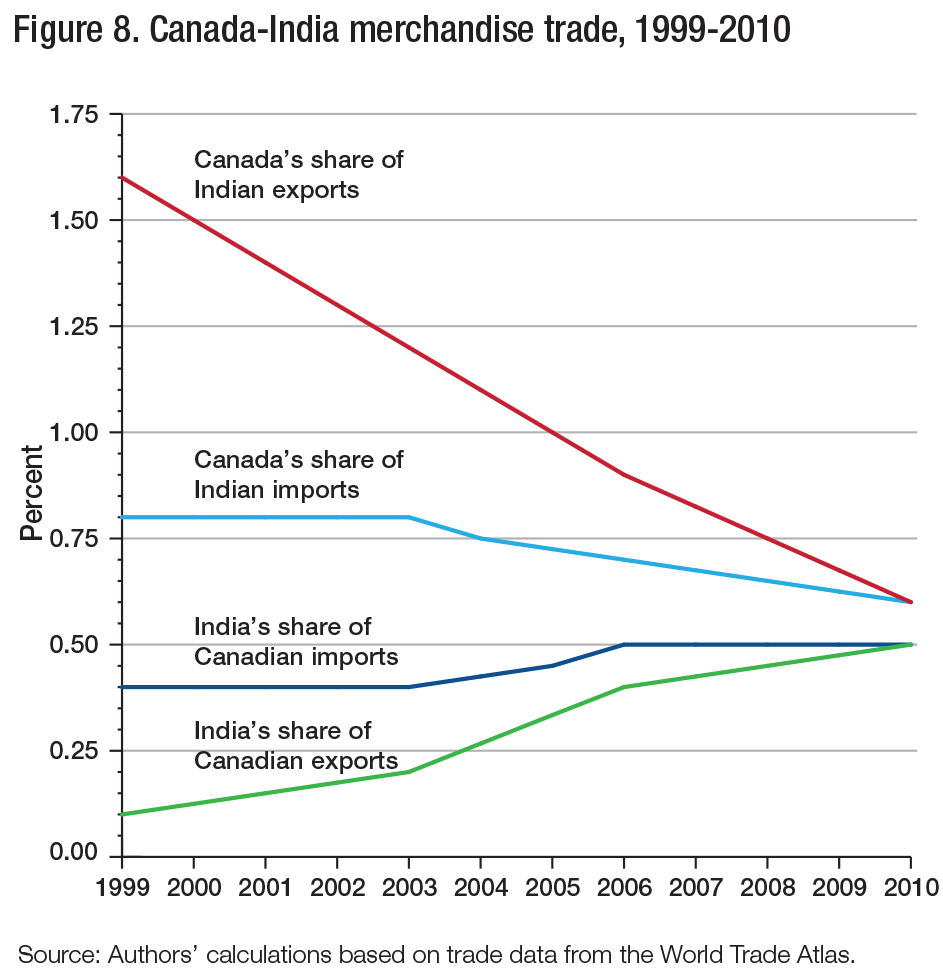

The trade-share data suggest that each country is of roughly comparable importance in the other’s overall merchandise trade — and more specifically, that neither is currently a particularly significant trading partner for the other (figure 8). There have, however, been some relative shifts over the past decade. For Canada, India has become a somewhat more important trading partner: India’s shares of Canada’s overall merchandise exports and imports have grown over time. Conversely, Canada has become a relatively less important trading partner for India: Canada’s shares of its exports and imports have fallen since 1999.

In commodities, the strongest Canada-India merchandise trade is in vegetables and related products and fertilizers. In 2010, Canada supplied almost 30 percent of India’s total imports of edible vegetables (there have been significant gains over the past decade); over 10 percent of wood pulp and paperboard; and roughly 5 percent of textiles, nickel, aircraft and parts, and fertilizers. India supplied over 40 percent of Canada’s silk imports; roughly 20 percent of its vegetable textile fibre, lac and vegetable sap; nearly 10 percent of its fertilizer; and over 5 percent of its textile art, cotton, cereals and organic chemicals.

Our RCA analysis identified specific commodities where Canada and India had revealed comparative advantages in exports. Our calculations (not shown) suggest that for both countries the commodities with a stronger RCA were more successful in penetrating the other country’s markets.

This relationship is stronger for India than for Canada. For India, silk and vegetable textile fibre exports to Canada have been particularly strong. Sectors where Indian exports have been weaker than this simple relationship suggests include cotton, precious stones, coffee and tea, and yarns and woven fabrics. Canadian exports to India of edible vegetables, paper and paperboard, aircraft and parts, and textiles have been strong. Areas that are weaker than predicted include oil seeds and grains, wood, and fish and crustaceans.

It is also worth comparing Canada’s penetration of India’s market relative to that of other comparable countries, such as the US and Australia. Between 2000 and 2010, -Canada’s share of India’s total merchandise imports declined from 0.8 percent to 0.6 percent. While the US’s and Australia’s shares of Indian imports fell faster over this period (from 8.4 percent to 5.4 percent for the US and from 4.4 percent to 3.4 percent for Australia), they remain well above Canada’s, illustrating the strong competition that Canada faces in the Indian market.

In the past decade, Australia’s shares of Indian imports have increased substantially in many of the commodities in which Canada has an RCA, such as nickel (Australia’s share grew from 2.8 percent in 1999 to 20.8 percent in 2010, while Canada’s share fell from 6.7 percent to 5.6 percent in the same period). In 2010, Australia had over 20 percent of the Indian market in six resource-based commodities: cereals; wool and animal hair; milling products; ores, slag and ash; dairy; and nickel. In comparison, the only commodity where Canada’s share of the Indian market was over 20 percent was edible vegetables.

The US is also making inroads in India in many of the natural resources and resource-based commodities. For instance, the US’s share of India’s imports of edible vegetables increased from 0.7 percent in 1999 to 7.0 percent in 2010. In 2010 its share of ores, slag and ash was 23 percent (up from 2 percent); its share of wood pulp imports was 26 percent and its share of paper and paperboard imports was 12 percent. The US also competes with Canada in autos and aircraft. The US’s share of India’s aircraft imports was 44 percent and its share of automobile imports was 4 percent.

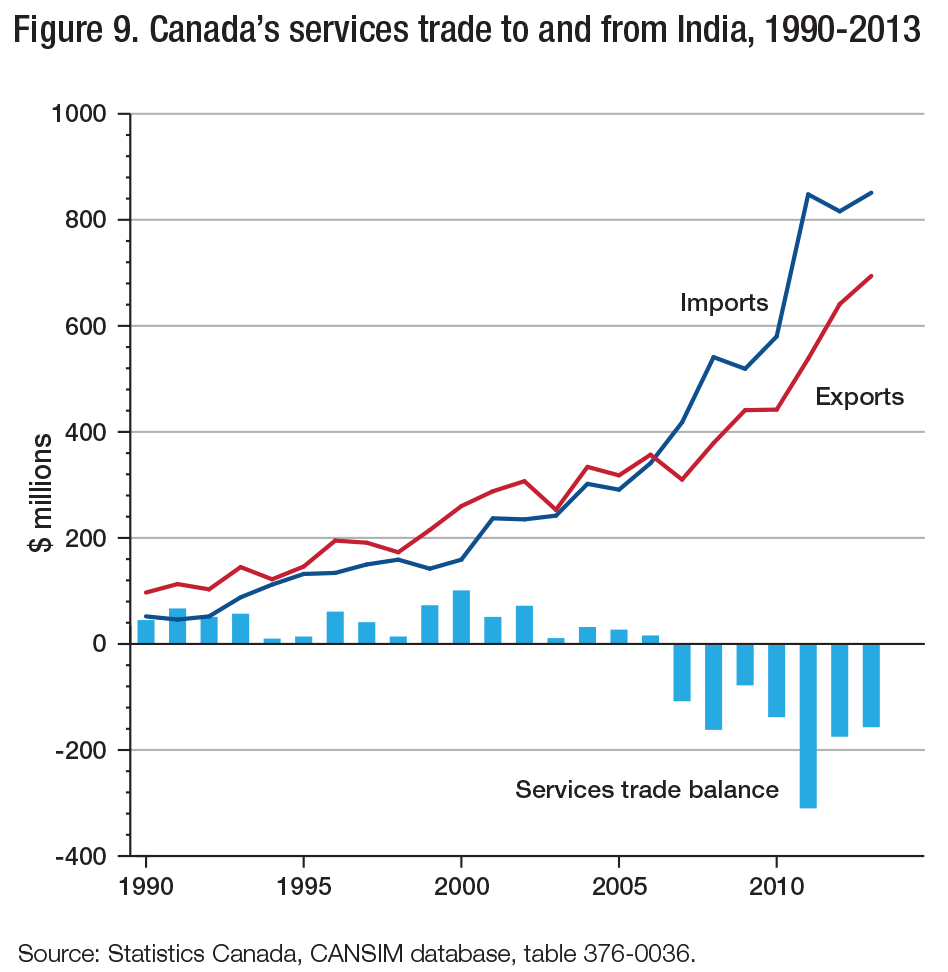

Canada-India services trade was quite small at only $1.5 billion in 2013, representing just 0.7 percent of Canada’s total services trade.19 Once again, growth was strong over the past two decades, starting from a very low level (figure 9). Between 1990 and 2013, total Canada-India services trade grew at 10.7 percent per year on average in nominal terms; services exports grew at 8.9 percent, while imports grew at 12.9 percent. Canada has run small services trade deficits with India in every year since 2007. The strongest growth in bilateral services over the past five years was in Canada’s exports of travel services (includes Indians visiting Canada) and its imports of India’s commercial services (related to strength in Indian computer and other services).

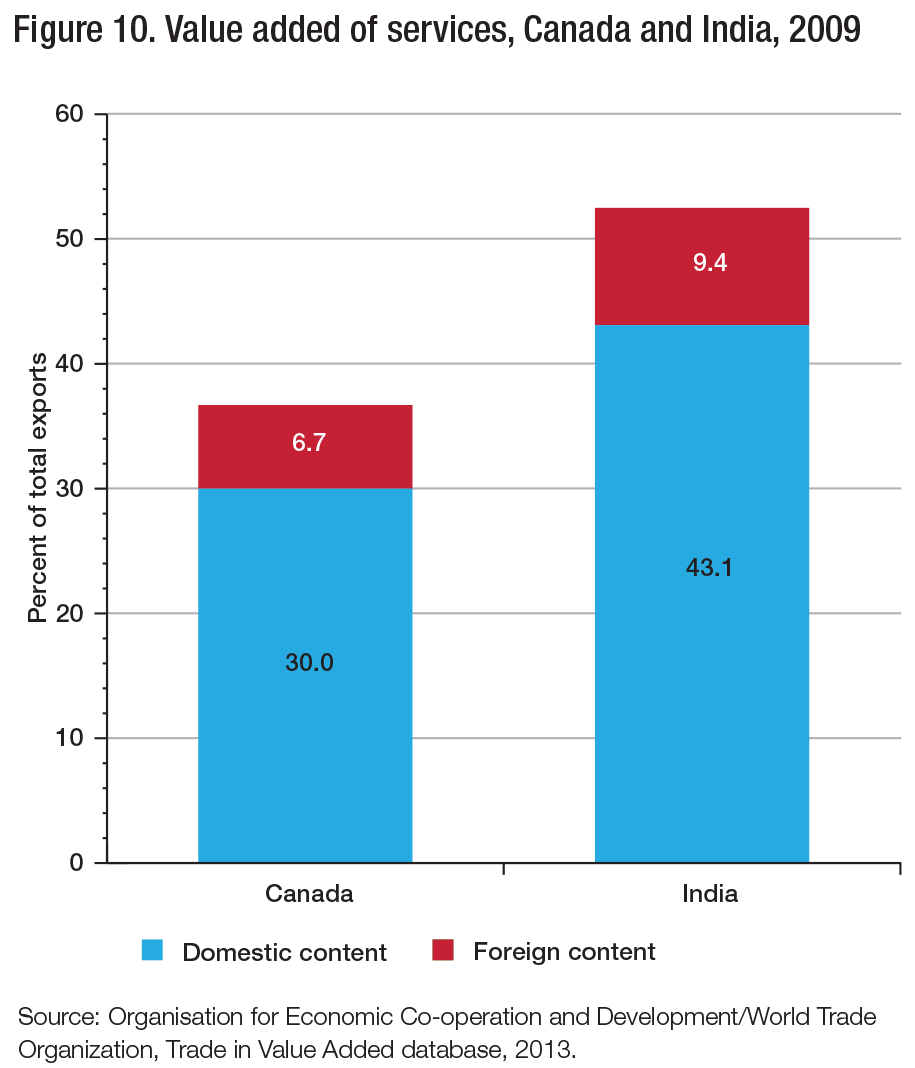

The trade statistics discussed so far attribute the full value of products to the last country of origin when they cross international borders. This approach can result in a misleading view of trade patterns in a world where production processes are increasingly fragmented across international borders as part of global value chains (Van Assche 2015). The new OECD-WTO trade in value-added (TiVA; Organisation for Economic Co-operation and Development 2013) data provide a more nuanced view of global trade patterns. They highlight the often underappreciated importance of services in overall trade flows, which is a particularly important issue for India. For instance, TiVA data for 2009 estimate that India had one of the highest contributions from services in the G20 economies relative to its total exports, when measured on a value-added basis. Services contributed more than half of the value of Indian exports (in rounded numbers, 53 percent overall, with 43 percent domestic and 9 percent foreign components) (figure 10). This is significantly higher than Canada’s services share of 37 percent of its overall export value-added.

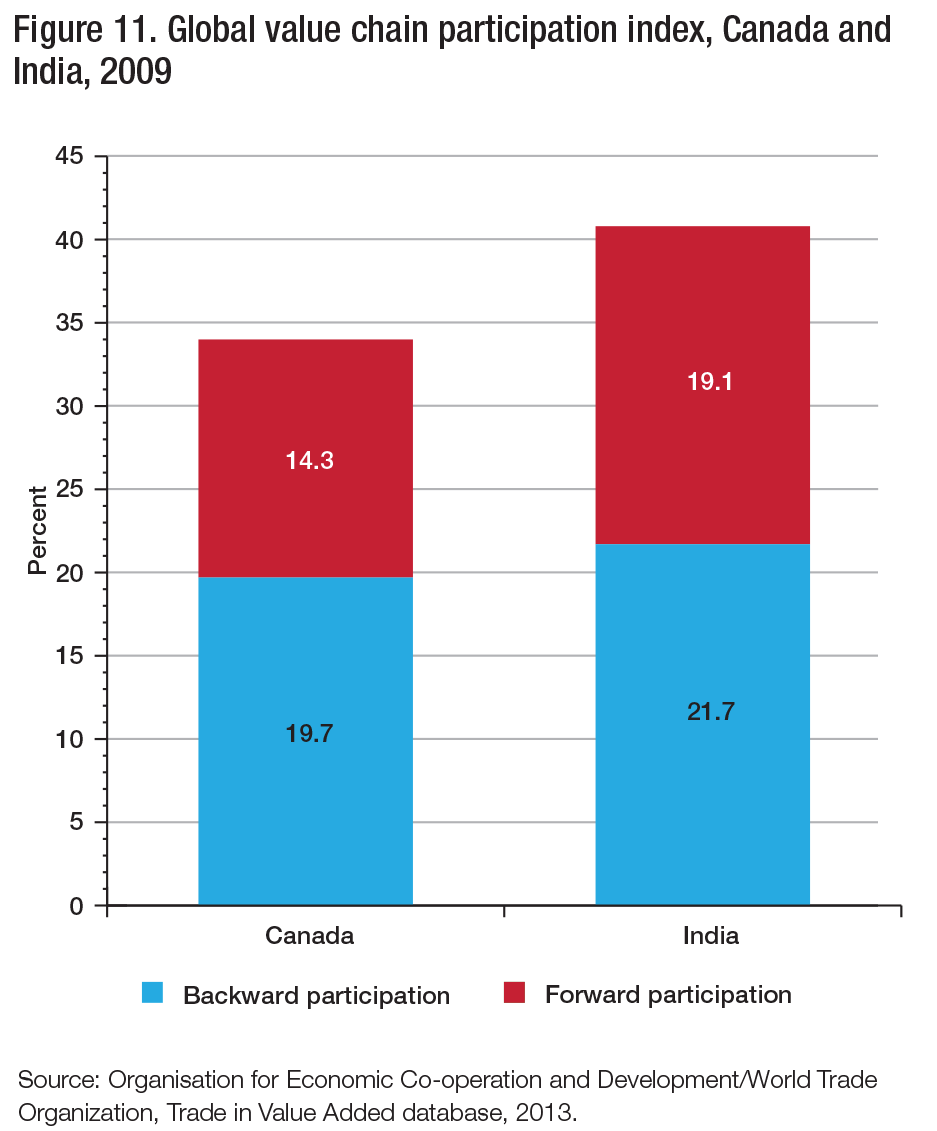

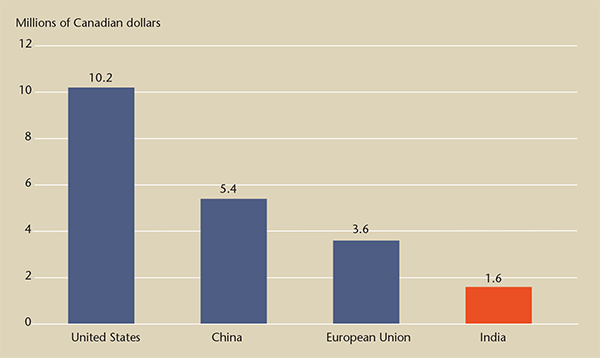

TiVA data include a global value chain (GVC) participation index for each country that takes into account so-called “backward” and “forward” trade linkages.20 Relative to other countries at similar levels of economic development, Canada and India both rank quite low in their GVC participation: in 2009 Canada ranked 33rd among 34 OECD countries and India ranked 14th among 19 non-OECD countries. India’s GVC participation index is somewhat higher than Canada’s, largely because India’s exports are more likely to be used as inputs in other countries’ exports (“forward participation”; figure 11).

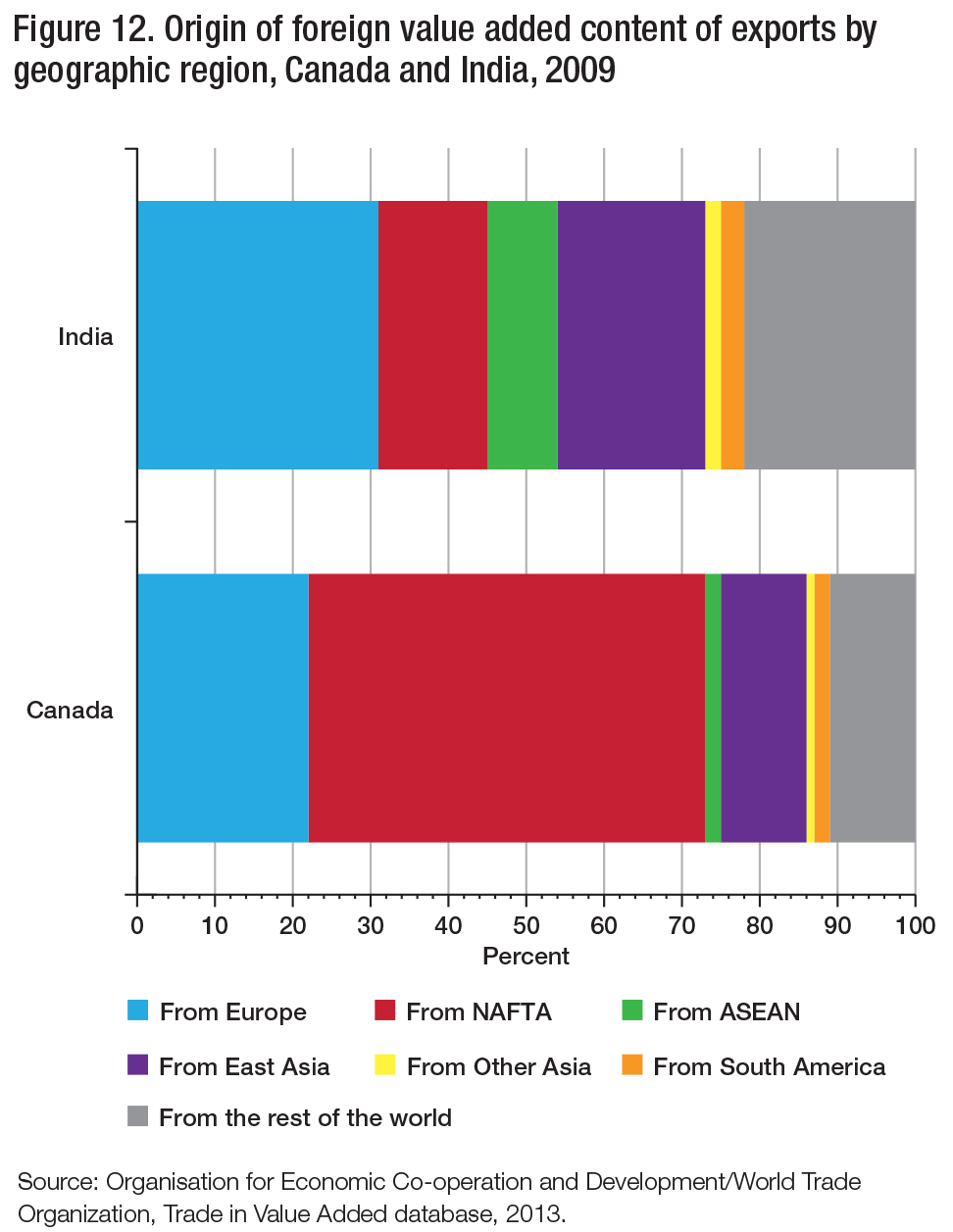

When we consider the geographic origin of value-added in Canada’s and India’s exports (figure 12), not surprisingly, Canada’s rely much more than do India’s on value-added from the rest of North America (51 percent versus 14 percent), whereas India’s contain more value-added from Europe (31 percent versus 22 percent) and from Asian countries (27 percent versus 13 percent).

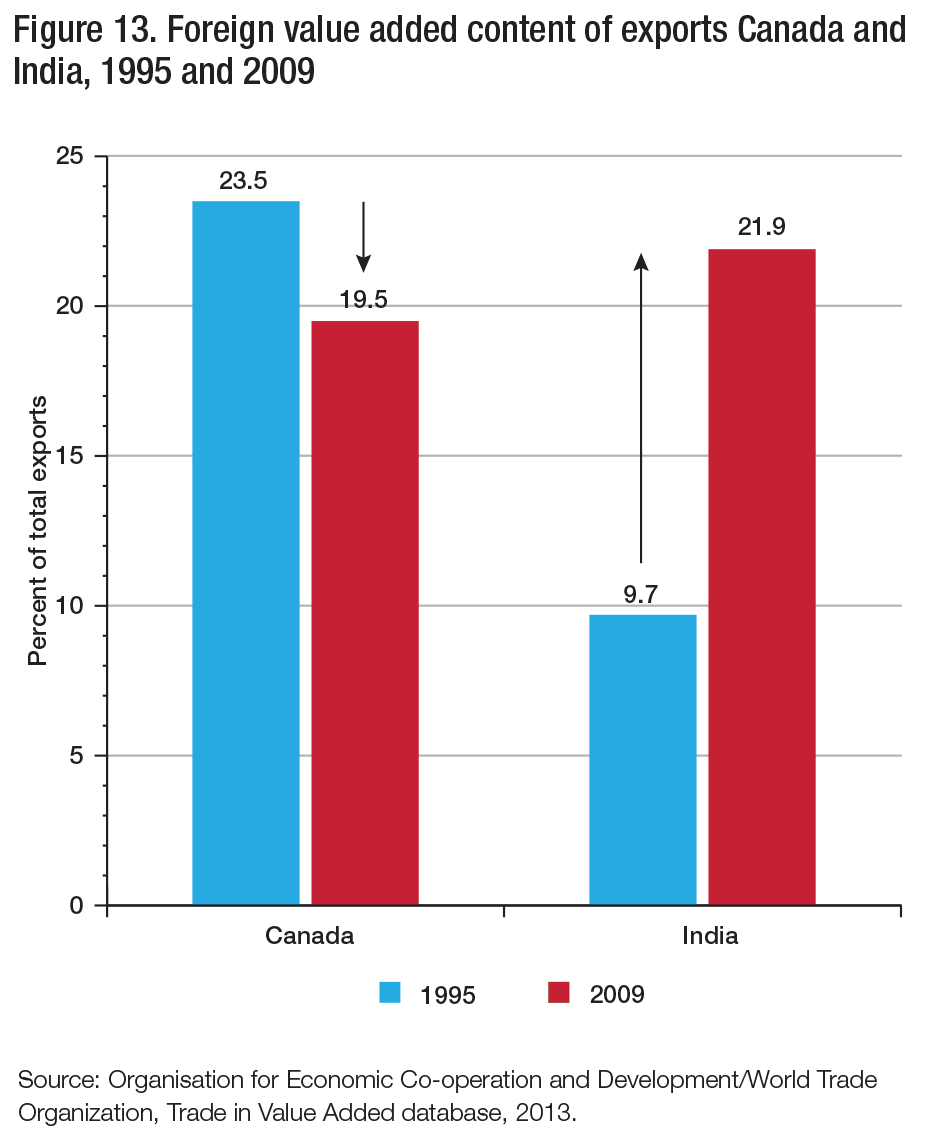

Finally, a longer-term view from the TiVA database reveals divergent trends in the share of foreign value-added in overall exports for the two countries. As in most OECD countries, India’s increased integration into the global economy was associated with a large increase in the share of foreign value-added in India’s exports, from 10 percent in 1995 to 22 percent in 2009 (figure 13). Canada’s share of foreign value-added in its overall exports fell in this period from 24 percent to 20 percent and is now below India’s.21

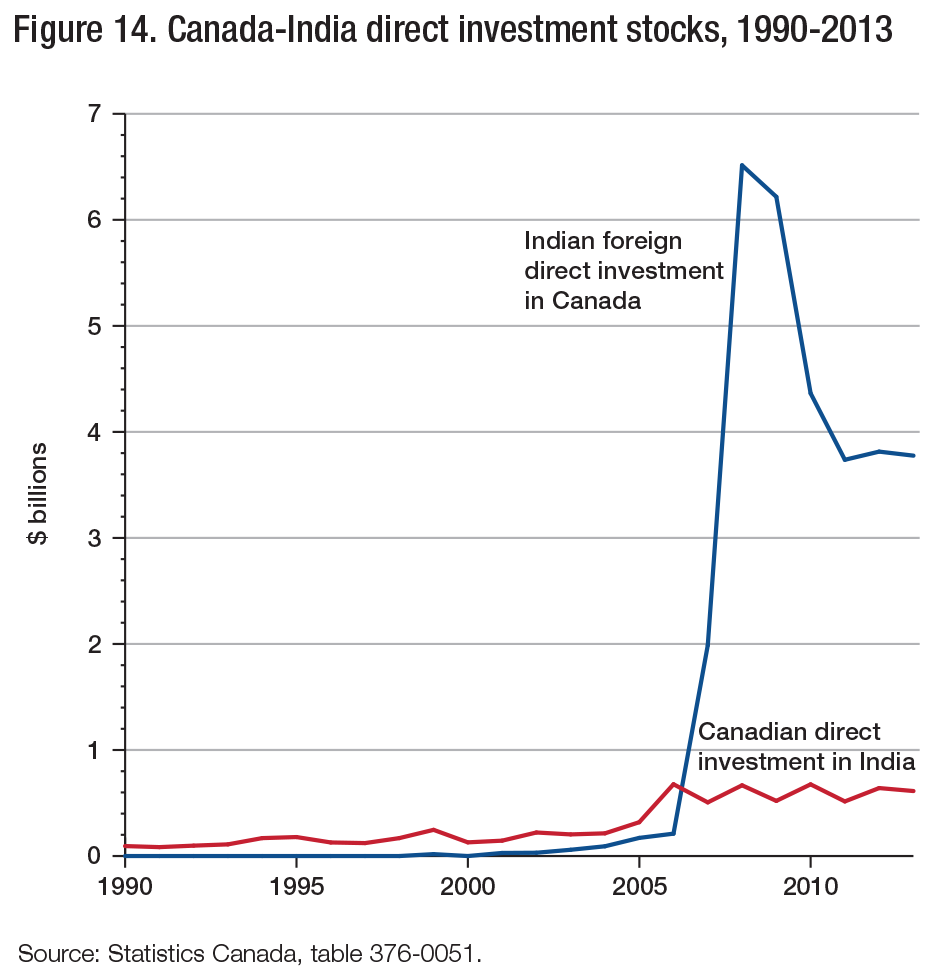

FDI can allow firms to access new markets directly and avoid some at-the-border trade barriers such as tariffs. It can also provide the host country with access to new technologies, intellectual property and international brand names. Official statistics suggest that FDI links between the two countries are currently very weak.22 However, since 2007, FDI from India to Canada has increased substantially, and Canada has become a net importer of FDI from India (figure 14). This pick-up in Indian FDI in Canada can be partly attributed to India’s purchases of Canadian steel and aluminum producers.23

Canadian investment in India occurs in industries such as business services, software and information technology, auto parts, communications and transportation.24 The largest destination cities are Mumbai and Bangalore, and the most frequent motivation for FDI in India is the growth potential of the Indian market.

From the perspective of India’s economic development, longer-term FDI may be preferable to shorter-term portfolio flows (sometimes called “hot money”), which are much more responsive to interest rate or exchange rate fluctuations and can lead to capital flight from the country. FDI may also be preferable to imports, because it could be better for domestic employment.

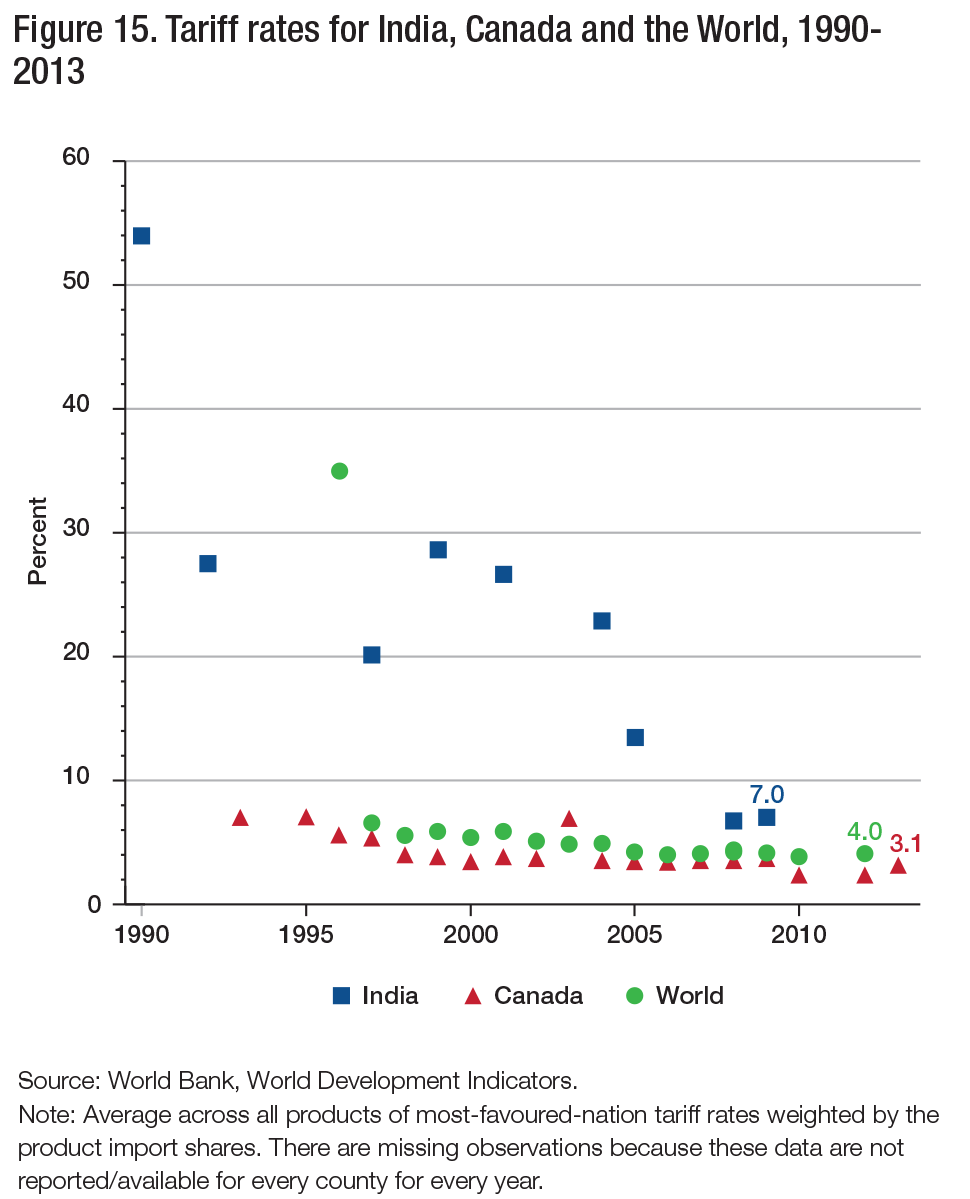

Tariffs across the world fell dramatically after 1996 with the implementation of the Uruguay Round of multilateral trade negotiations conducted within the General Agreement on Tariffs and Trade, which created the WTO (figure 15). Before the policy reforms that began in 1991, India’s tariffs, at over 50 percent on average, were prohibitively high, but since then they have fallen considerably. Nevertheless, its current average tariffs of 7 percent remain above the world average (4 percent) and above Canada’s tariffs (3 percent).25

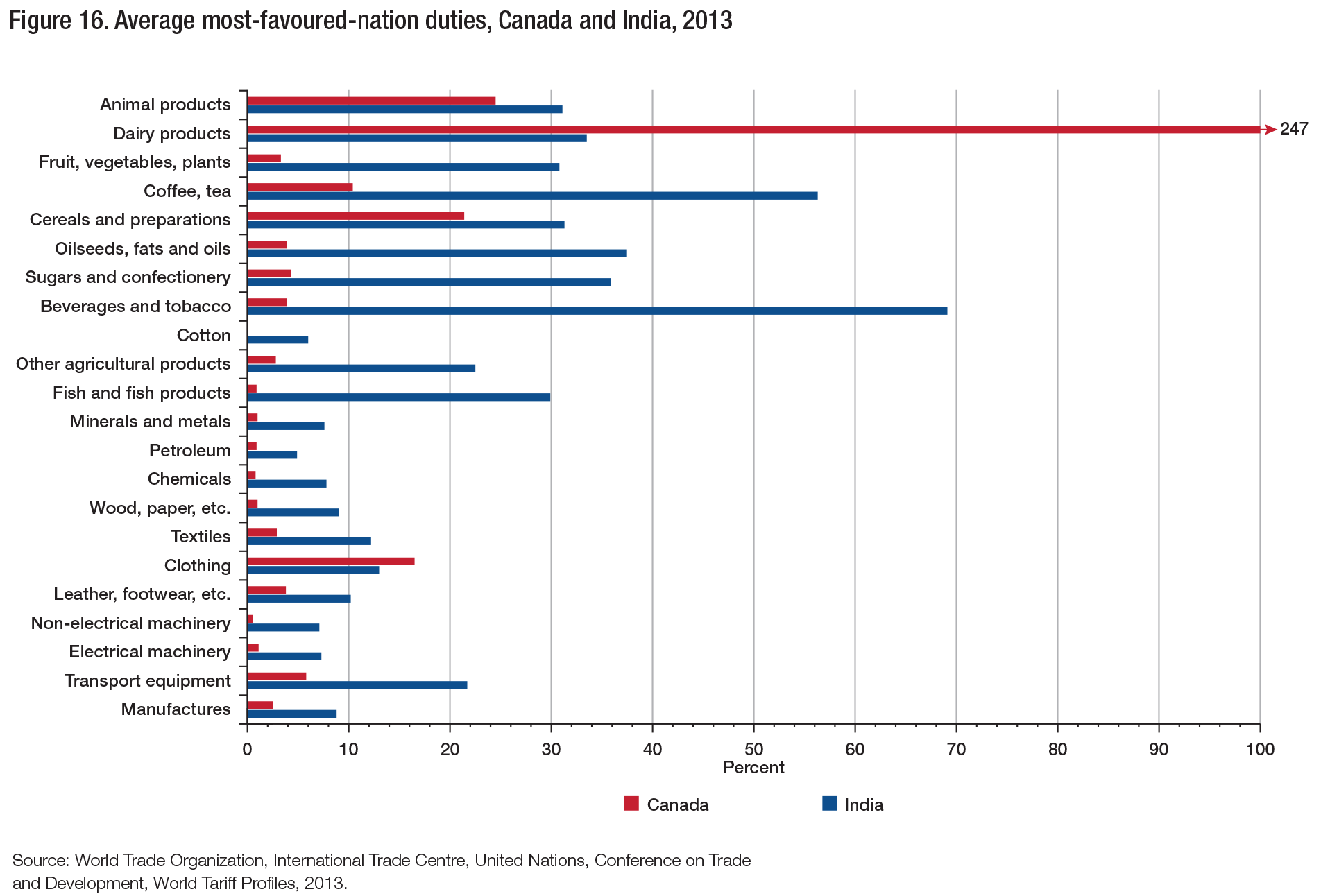

There are significant variations within these averages (figure 16). For instance, Canada has “off-the-charts” tariff-equivalent rates in its supply-managed agricultural sectors (dairy), but has low tariffs on machinery, manufactures, and resources and resource-intensive products. India levies its highest tariffs on alcohol (in the beverages and tobacco category), coffee and tea and its lowest tariffs on petroleum, machinery, minerals and metals, and manufactures. At this level of aggregation, tariffs in India are higher than those in Canada across the board, except for dairy and clothing.

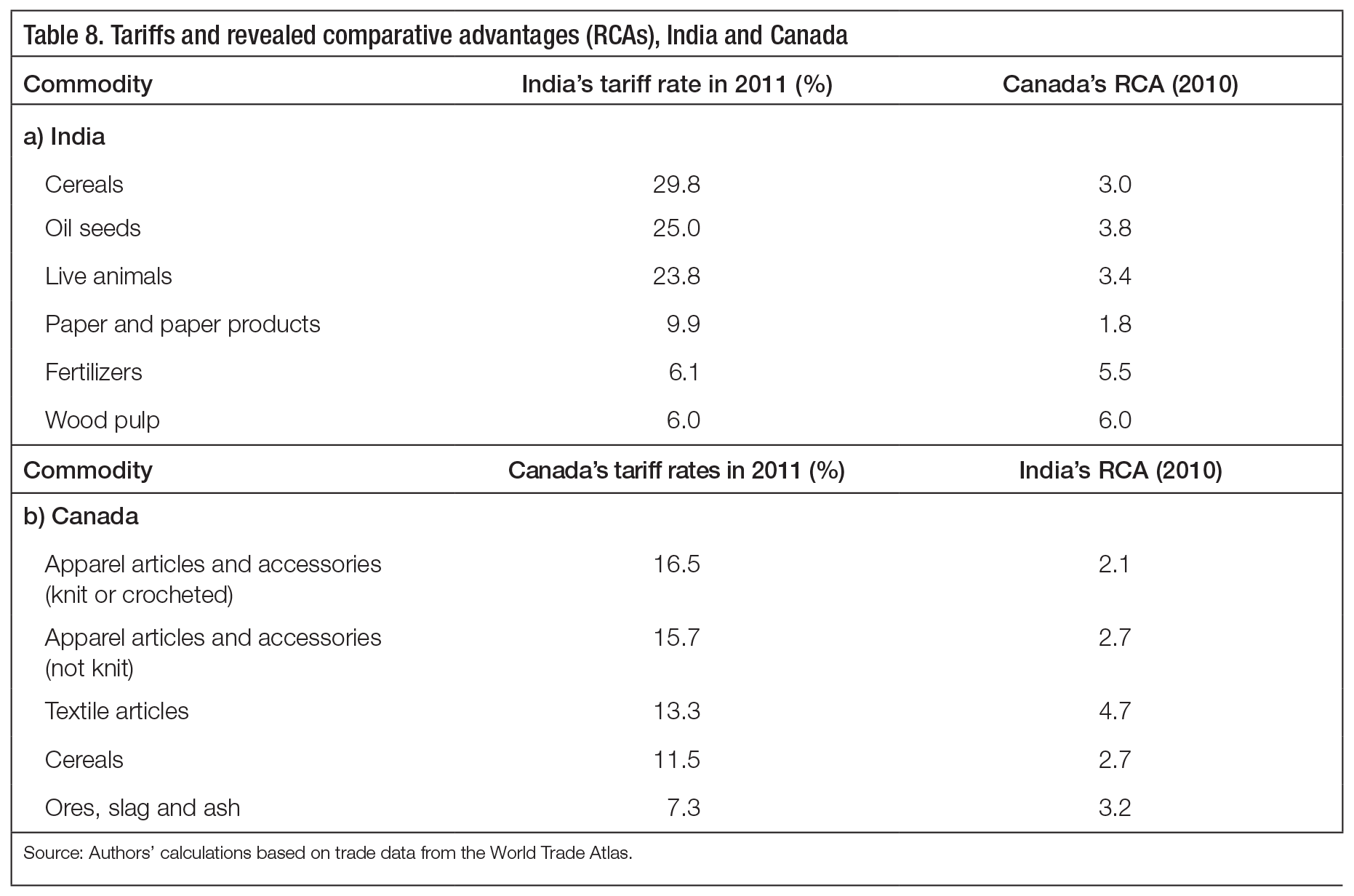

There are several commodities that trade negotiators might target for tariff reductions to unlock trade (table 8). For instance, Canadian businesses could benefit from Indian tariff reductions on cereals; oil seeds; live animals; wood, pulp and paper products; and fertilizers. Indian producers could benefit from reductions in Canadian tariffs on apparel and textiles, cereals and ores.

Finally, one other important consideration for trade negotiations is the large asymmetry between Canada and India in the fiscal importance of import duties. In 2012-13, customs duties represented only 1.5 percent of central government revenues in Canada but nearly 19 percent in India.

There are also a wide variety of more indirect, nontariff barriers. These include complicated customs procedures and “rules of origin,” which are used in preferential trade agreements to determine which goods are eligible for reduced tariff rates (Tapp 2007), regulations, import licences, health and safety standards, local preferences in government procurement contracts, and voluntary export restraints.

By their very nature, nontariff barriers are hard to quantify. Therefore, there are few estimates of tariff equivalents to help us assess how much they restrict trade flows between the two countries. Nonetheless, we do know that, as tariff levels have fallen over time, the relative importance of nontariff barriers as a hindrance to global trade has increased. Canadian business leaders have expressed concerns that, much like tariffs, nontariff barriers are generally larger in India than in Canada (Canadian Chamber of Commerce 2012, 4, 20). They have said that “Canadian companies face market access issues with India, including the many challenging non-tariff barriers that are encountered in India…[where, for example,] additional customs duties, countervailing and anti-dumping duties…have been employed in the past to protect sensitive sectors in India.” They also suggest that a CEPA could enhance regulatory cooperation between Canada and India by easing the cost of operating businesses in these two markets.

Services represent over half of India’s GDP and more than two-thirds of Canada’s (table 2). As such, even minor improvements in the efficiency of services could result in large income gains.

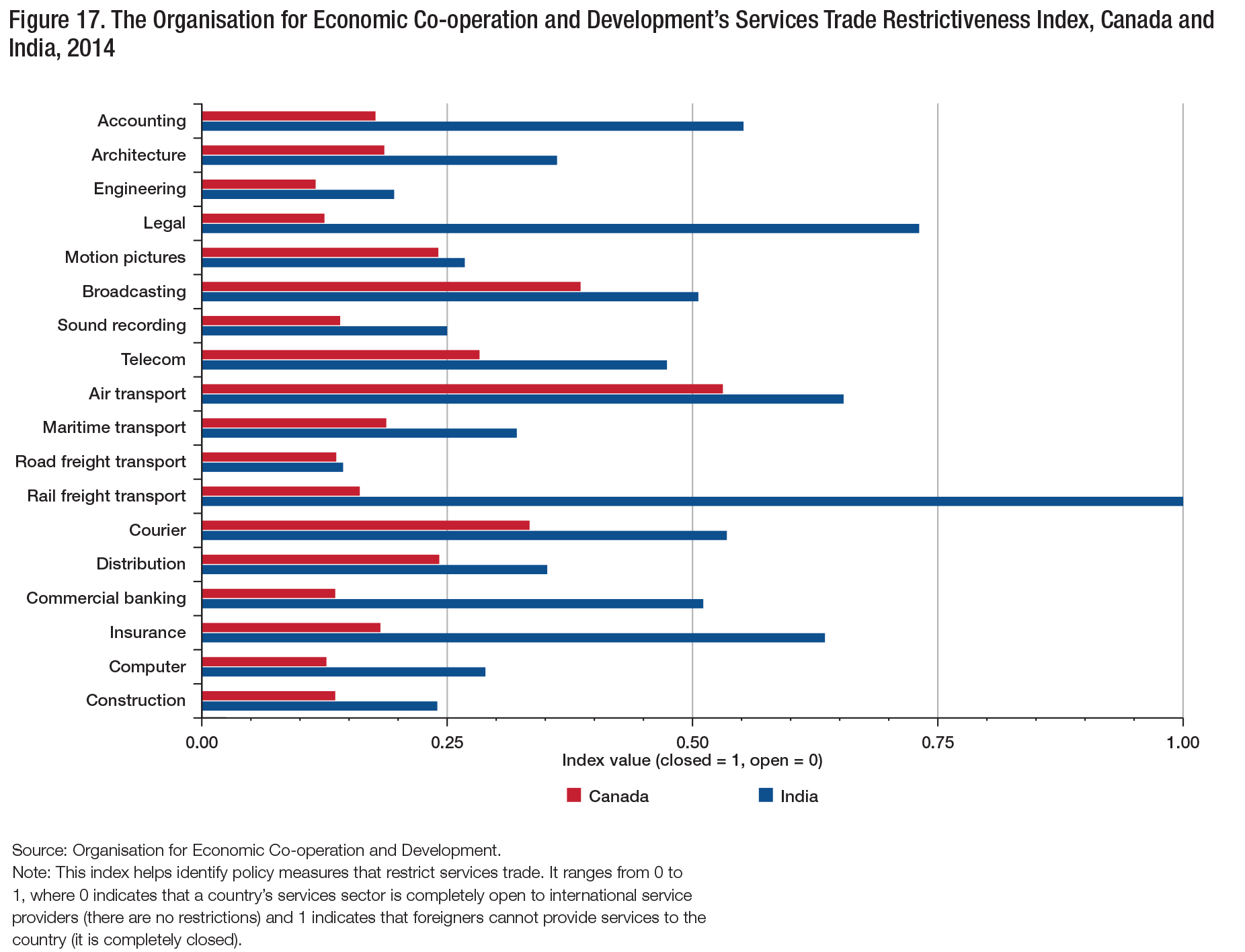

The OECD’s Services Trade Restrictiveness Index allows for cross-country comparisons at the sectoral level.26 It uses composite indices to quantify identified restrictions on services trade in five categories, assigning values between 0 (for complete openness to trade and investment) and 1 (when a country is completely closed to foreign services providers).27 Consistent with the general trend so far, the index suggests that India has more restrictive services trade policies than does Canada — in this case, for all the services sectors considered (figure 17). In fact, of all the 40 countries analyzed, India’s services sectors were more restrictive than the sample average in 17 of 18 cases (road freight transport is the exception). Canada’s services sectors were more restrictive than the average in only 6 of 18 sectors.

In Canada, engineering, legal and computer services are the most open service sectors. They are particularly open to the movement of persons, often allowing foreign professionals to enter temporarily to complete specific projects. Canada’s most closed service sectors are those in which large government-run operations impose strict limits on foreign ownership and investment: air transport (Air Canada), broadcasting (the Canadian Broadcasting Corporation) and courier services (Canada Post).

India’s most open service sectors are road transport, engineering and construction. Its most closed are rail freight transport, air transport and legal services (only Indian citizens can -practise law, and foreign lawyers may enter only on a fly-in fly-out basis if they are practising international or home country law).

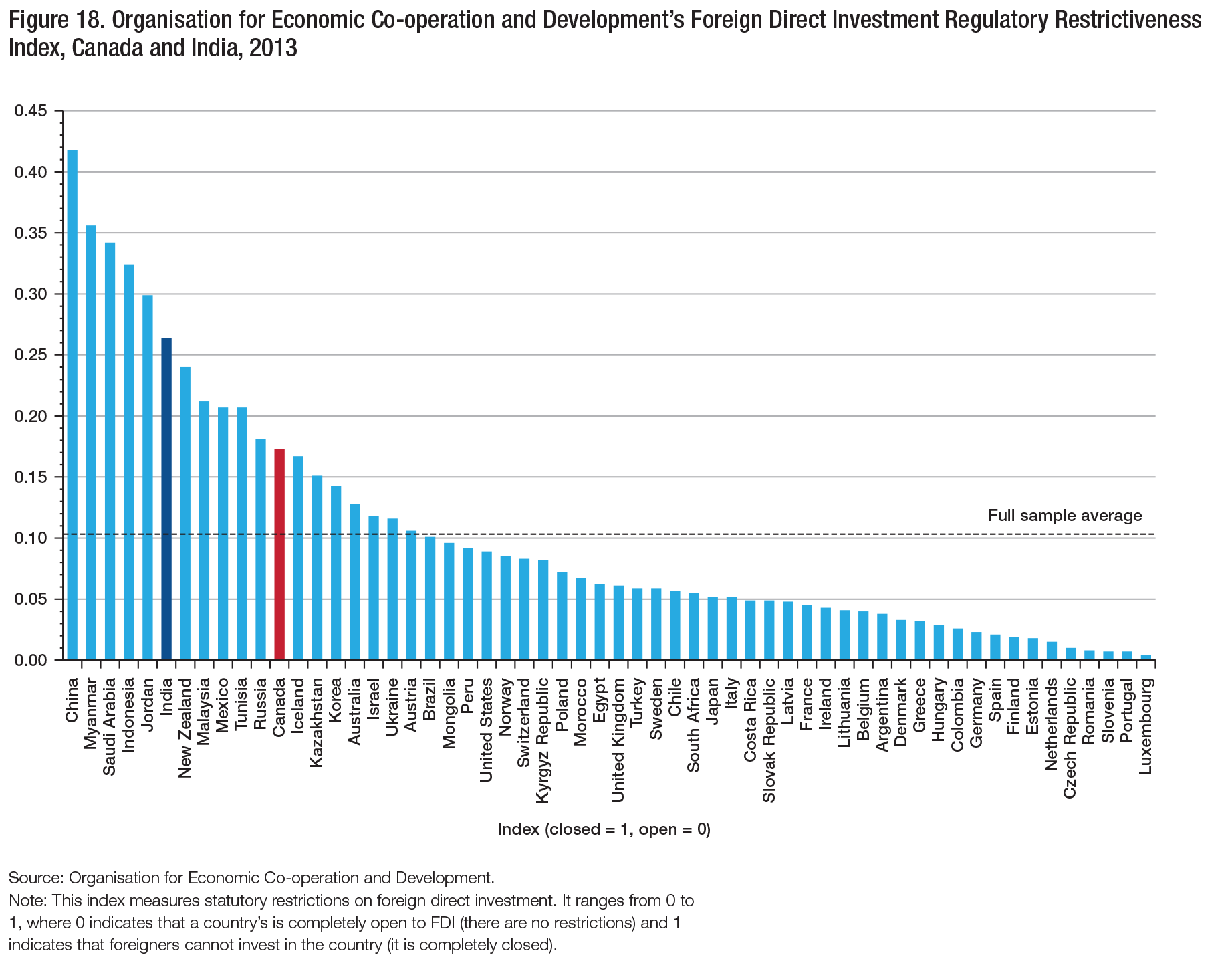

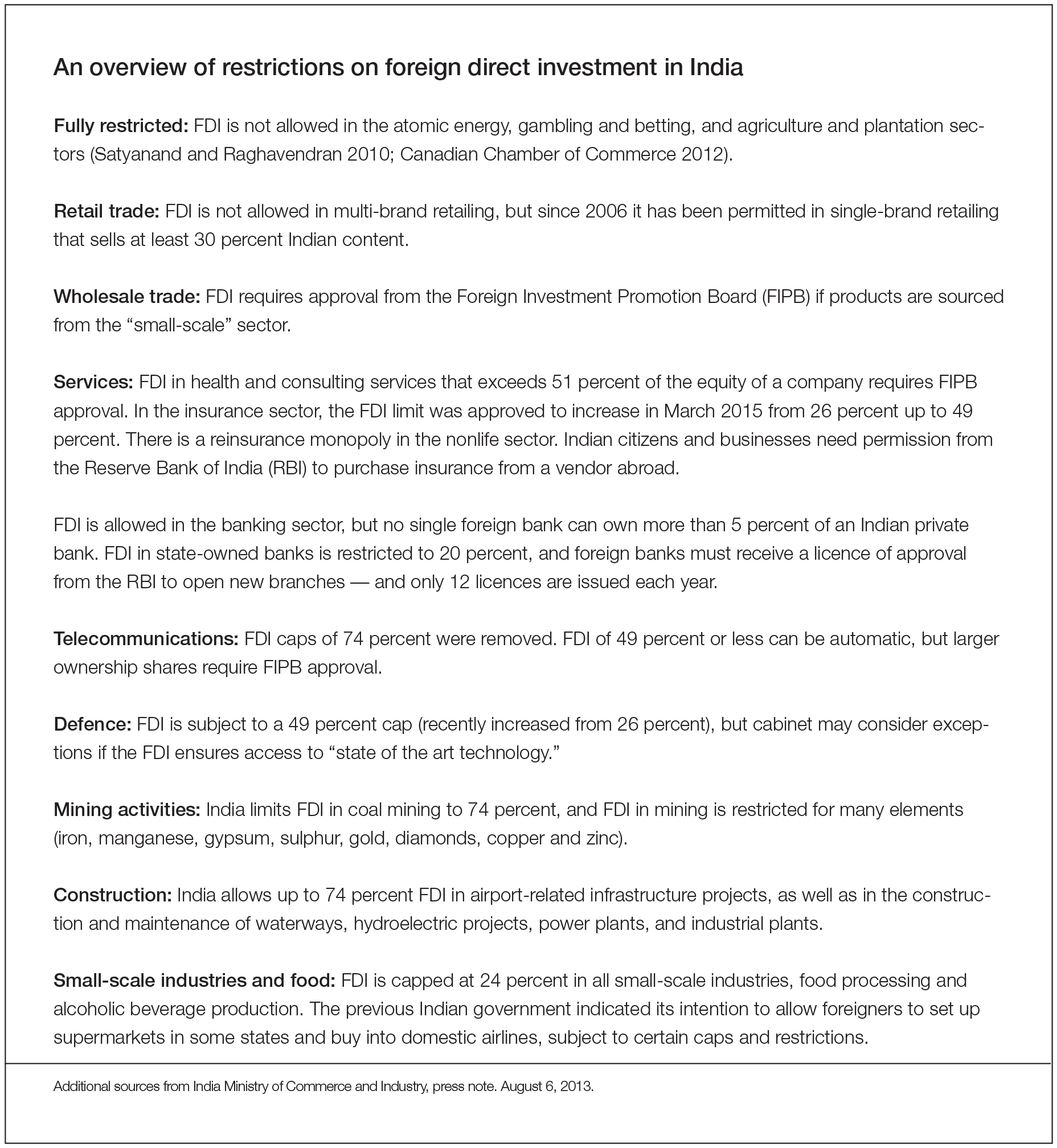

Countries routinely scrutinize and restrict FDI. The OECD compiles an FDI Regulatory Restrictiveness Index, which examines four main types of restrictions on foreign investment (figure 18).28 One important limitation of this index is that it is based on the formal legal frameworks in place, which do not fully reflect the restrictiveness on FDI that occurs in practice (Assaf and McGillis 2013). Bearing this in mind, according to this index, both India and Canada are more closed to FDI than the average country. (For an illustrative but not exhaustive list of India’s FDI restrictions, see appendix 2.)

Canada imposes various FDI restrictions: non-Canadians who acquire a Canadian business or who intend to establish a new business in Canada must comply with the Investment Canada Act (ICA). It relies on sector-specific foreign investment restrictions and retains the power to review sovereign investments that potentially threaten national security (which is distinct from the net benefit test). Recent amendments to the ICA expand the definition of a state-owned enterprise such that certain investments might be subjected to a ministerial review and approval requirement.29

Agreements to liberalize trade impact the economy in various ways. For instance, improving Canada’s access to another country’s market generally increases trade in products that were already exchanged before the trade deal (the so-called intensive margin), but it also encourages the entry of new Canadian businesses and new products into the foreign market (the extensive margin).30

The impact of the Canada-US Free Trade Agreement (FTA) of 1989 is well studied. Trefler (2004) finds that this agreement had significant short-run adjustment costs (primarily for displaced workers and struggling plants), but that it ultimately provided larger, long-run benefits (mainly for more efficient plants and for consumers). For Canadian manufacturing industries that experienced the deepest Canadian tariff cuts — which increased American competition — labour productivity rose by 15 percent, while employment fell by 12 percent, as low-productivity plants shrank. Canadian industries that benefited from the largest US tariff cuts, which improved Canadian access to the US market, saw no employment gains, but their plant-level labour productivity increased dramatically (14 percent). Trefler also finds evidence of lower prices and, importantly, overall welfare gains from this trade agreement.

Lileeva and Trefler (2010) find that the Canadian plants that were induced by the Canada-US FTA to start exporting or to export more increased their labour productivity, engaged in more product innovation, and adopted advanced technologies at a greater rate. Interestingly, the Canadian firms that made the biggest gains were those that were the least productive before the deal and made the largest technological leaps, not the firms that initially were the most productive, because those firms were already using better technologies before the trade deal.

Foreign Affairs, Trade and Development Canada (2013b) finds large gains from one of Canada’s lesser-known trade deals, one with Chile. It estimates that bilateral trade flows grew 12 percent faster than they would have without the agreement. Moreover, the vast majority of these gains came from new trade in products that were not traded before the agreement. In fact, new products accounted for 90 percent of the net increase in the value of Canadian exports to Chile. This highlights the importance of extensive margin for trade agreements, and suggests that it is difficult to predict the outcome of a trade deal beforehand.

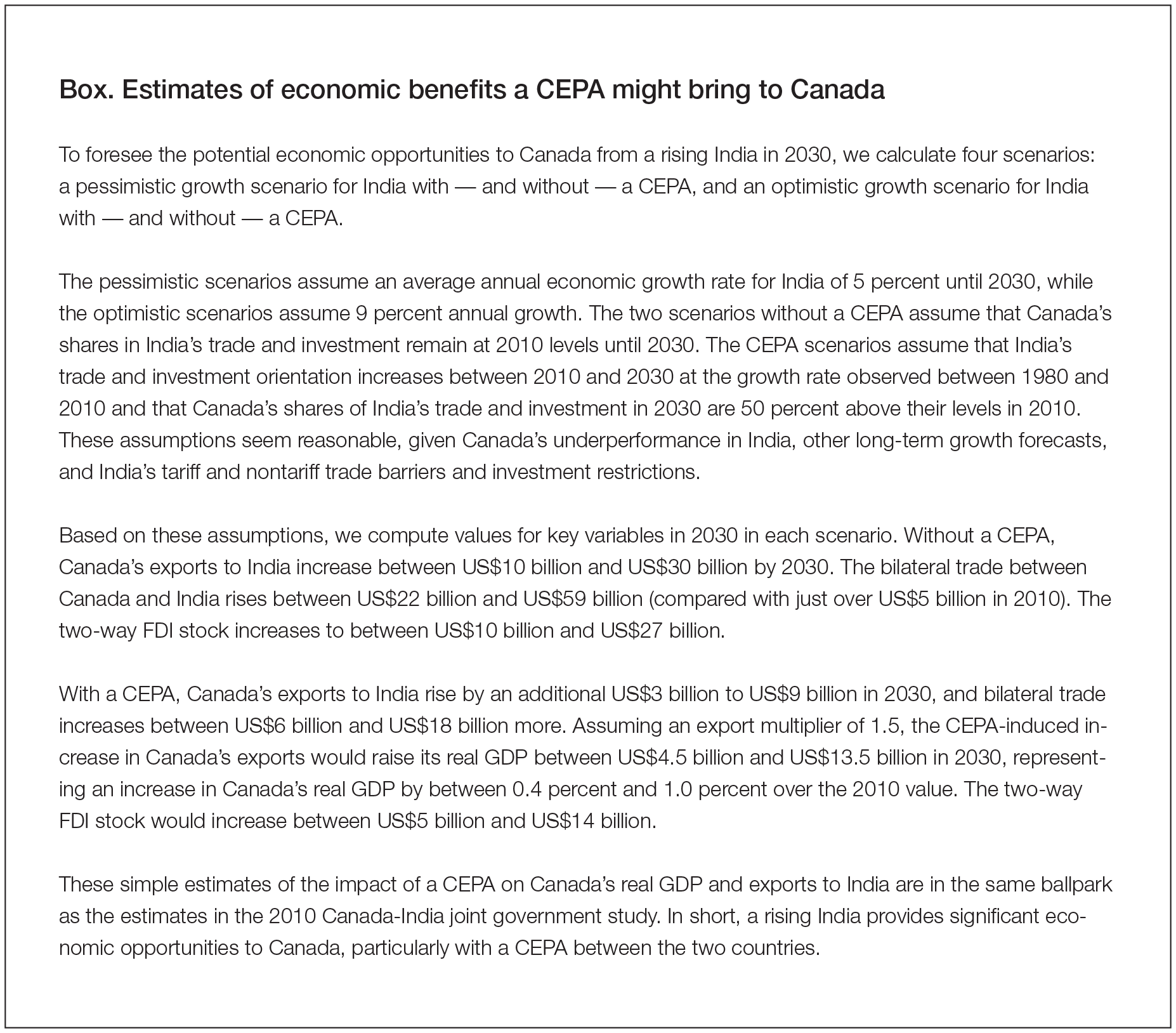

While predictions about trade deals are undoubtedly difficult, they are nonetheless needed to help inform negotiations. In the joint Canada-India government study (Foreign Affairs, Trade and Development Canada, and Canada-India Joint Study Group 2010), the two countries used the global trade analysis project (GTAP, a computable general equilibrium) model to estimate potential economic impacts of trade liberalization under a Canada-India CEPA. The estimated that the GDP gains for each country would be relatively large and roughly equivalent. They range from $6 billion to $15 billion (2008 US dollars) for Canada (or 0.4 – 1.0 percent of GDP) and $6 billion to $12 billion for India (or 0.5 – 1.0 percent of GDP).31 Breaking down these GDP gains, the Canadian government estimates there will be increases in bilateral services trade of 65 percent, which is larger than the estimated increases in goods trade of 50 percent. The biggest estimated increases in goods are in manufacturing and agriculture. These estimates also anticipate large gains for India’s service exports, and also manufacturing, especially textile and apparel exports (Foreign Affairs, Trade and Development Canada, and Canada-India Joint Study Group 2010).

There are some important limitations to this type of analysis. For instance, it considers only the expansion of products that are already traded bilaterally (the intensive margin), whereas recent theory and empirical research emphasize the importance of also considering the extensive margin. Moreover, the potential effects on investment are not captured in the model; as the study notes, these estimates “likely…underestimate the benefits…from a CEPA.”

The Canadian government performed a similar exercise using the GTAP model for another current trade negotiation, the higher-profile 12-country Trans-Pacific Partnership (Foreign Affairs, Trade and Development Canada 2014). Those simulations suggest that the potential economic gains for Canada of a deal with India would be similar to that of the TPP (roughly 0.4 percent of GDP in both cases).

We think that the greatest opportunities that a CEPA would offer for strengthening economic linkages between Canada and India lie in services32 and investment. These are the two areas where bilateral linkages are currently the least developed, where barriers to international commerce are the highest, and where the gains from further developing and exploiting each country’s comparative advantages are the strongest. Of course, realizing this potential depends on the details, scope and breadth of any agreement provisions in these areas. For our “back-of-the-envelope” estimates, see the box below.

Canadian service industries such as insurance, banking, telecommunications and other commercial services (such as engineering, health, education and tourism) could benefit considerably from a CEPA with India. In goods trade, natural resources and resource-based industries (such as agriculture and related products, energy, fertilizers and precious stones), as well as transportation industries (automobiles and parts), could be the biggest winners.33

Regionally, if existing trade patterns continue, then Saskatchewan and the Northwest Territories would disproportionately benefit from a deal with India.

At the same time, Canadian firms would have to adjust to increased competition from India as a result of a CEPA, particularly in business services (computer, software, ICT, outsourcing and call centres) and in some lower-wage labour-intensive manufacturing (such as textiles and apparel, chemicals and steel). The overall net effects would not necessarily be negative for these sectors, since innovative firms stand to gain in these areas, as do Canadian businesses that use these Indian services as production inputs.

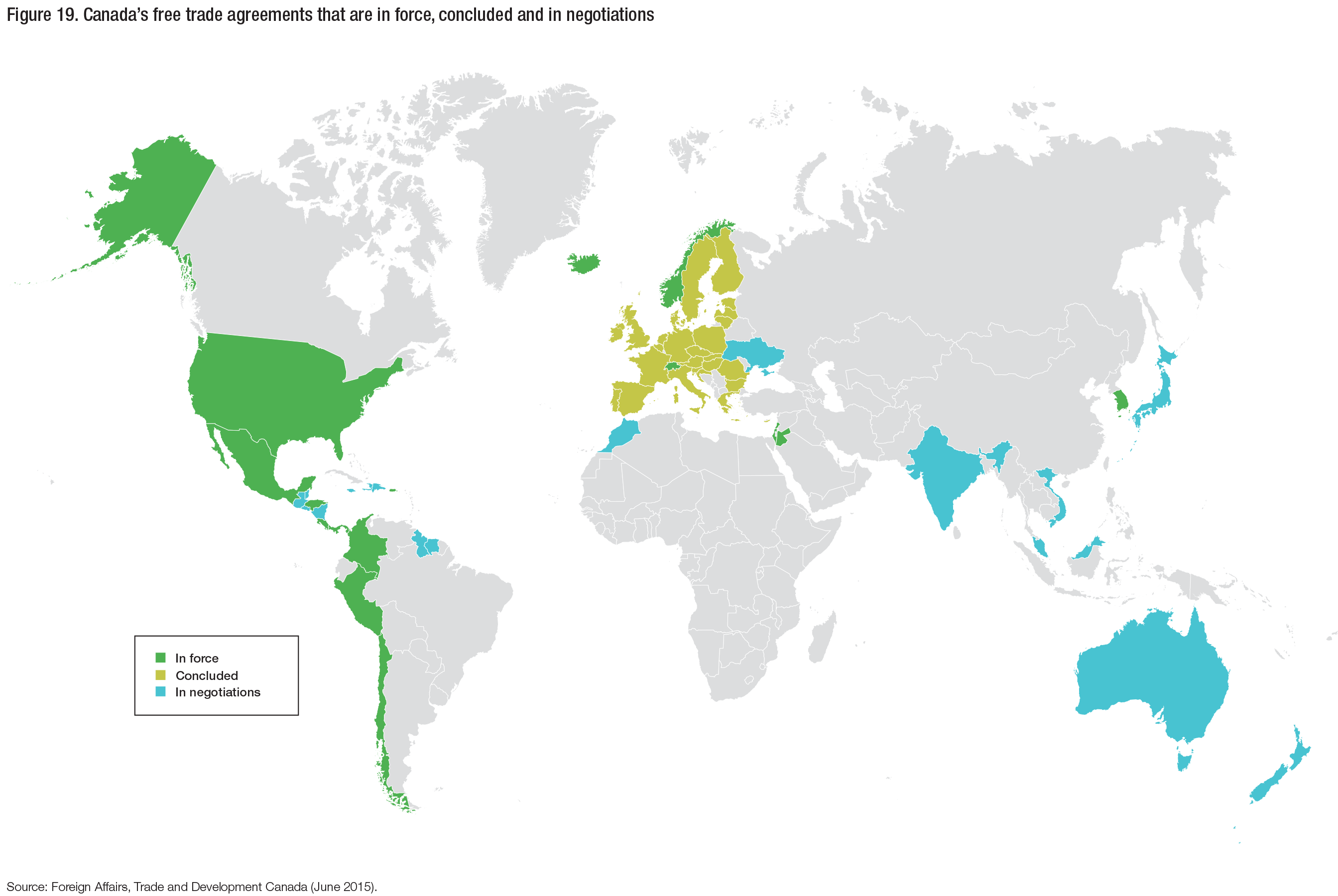

The status of Canada’s free trade agreements (FTAs) that are now in force as well as those for which negotiations have been concluded or are ongoing is mapped in figure 19. The North American Free Trade Agreement (NAFTA) with the US and Mexico is clearly the foundational agreement. The government is finalizing the text of the Comprehensive Economic and Trade Agreement (CETA) with the European Union and is in the later stages of talks in TPP negotiations.34 Canada also has trade negotiations underway with Japan (Canada-Japan Economic Partnership Agreement, launched in March 2012), among others.

The US is leading the TPP talks and is also involved in important negotiations with the EU (the Transatlantic Trade and Investment Partnership, known as the TTIP). Some Asian countries, including India, are negotiating the Regional Comprehensive Economic Partnership (RCEP), an attempt to consolidate previous bilateral agreements in the region.35

In the broader context of global trade negotiations, multilateral talks at the WTO have largely been stalled since the Doha round began in 2001. There was some optimism in December 2013 when there was a breakthrough trade facilitation agreement that includes measures for cooperation between customs authorities and provides technical assistance and capacity building for developing countries. In summer 2014, this agreement was temporarily blocked by countries led by India due to their concerns about restrictions on governments’ ability to provide food subsidies to their poor. However, it was salvaged at the end of 2014, and is currently being ratified by individual member countries. Whether the Doha round can officially be concluded in the near term, with a smaller deal achieved and a promising new round launched, remains to be seen.

Finally, two other noteworthy plurilateral negotiations are underway among a subset of WTO members. The first is the Trade in Services Agreement, which has 24 parties, including the US and the EU; the second is negotiations to eliminate tariffs on environmental goods, which includes 14 parties that account for over 85 percent of global trade in environmental goods.

The Canada-India CEPA negotiations were launched in 2010. Substantial progress seems to be slow in coming, with the ninth round of negotiations having been held in March 2015. If completed, the CEPA would be Canada’s second trade deal in the Asia-Pacific region — after the recently announced South Korean deal — and, importantly, its first deal with a BRICS (Brazil, Russia, China and South Africa) emerging market country. If we take into consideration NAFTA (North American links), CETA (Atlantic links) and a potential TPP (Pacific links), the addition of a Canada-India trade deal (CEPA) would mean that much of Canada’s trade would enjoy specific trade preferences.

In that scenario, one major missing piece of the puzzle is improved Canadian engagement with China. Some renewed momentum resulted from the bilateral investment deal that came into force in October 2014 (figure 20). However, although a joint Canada-China complementarities study has been completed (Foreign Affairs, Trade and Development Canada 2012), formal trade talks have not been launched. Recently, Canada and China agreed to establish a panel of experts to examine potential next steps in the trade relationship.

The Canada-India CEPA would be a significant element of Canada’s longer-term trade and foreign policy strategy. It would also offer the potential for Canada to secure first-mover advantage in the Indian market over the US and the EU. For these and other reasons, including the considerable long-term growth potential in India, even given the difficulties and the possibly long time horizon to finalize negotiations, these talks should be a priority for Canada.

Over the past decade, India has negotiated trade agreements with several countries (though some of them are very limited in scope and ambition), including Sri Lanka, Singapore, Japan, South Korea, Nepal, Malaysia, Bhutan, Afghanistan, the Association of Southeast Asian Nations (ASEAN, a political and economic organization of 10 Southeast Asian countries), Chile and MERCOSUR (a trading bloc of Latin American countries).

In his first year in office, Prime Minister Modi expended much effort on foreign policy objectives and on raising India’s profile abroad. India is currently negotiating with many partners in the hope of concluding a wide variety of trade agreements. The most important of these is with the European Union (the broad-based bilateral trade and investment agreement, for which negotiations began in 2007). It is also part of the RCEP Asia-Pacific negotiations, an important element in its “Look East” policy. It is also in trade talks with Switzerland, Norway, Iceland and Liechtenstein (ETFA), Australia, New Zealand, Pakistan, Indonesia, Thailand and Israel, among others.36 The Canada-India CEPA would be India’s first deal with a North American country.

If Canada concludes the CEPA with India, Canadians should expect a deal that is far less ambitious and much more limited in scope than the CETA. There are large differences between the two countries’ levels of economic development, their previous trade deals, and the fiscal importance of customs duties in overall government revenues. Here are three important (and likely the most contentious) areas to watch:

Major liberalizations in this area would be highly controversial, and it seems unlikely they would be achieved. After the CEPA negotiations began, Canada’s Temporary Foreign Worker program (TFWP) came under significant domestic criticism, and there were claims that it reduces job opportunities and depresses wages for Canadian workers. In 2014, Canada temporarily stopped allowing temporary foreign workers in the food sector, and the government is now reconsidering its broader policy direction for the TFWP (see Worswick 2013).

Of course, it is possible that these controversial issues could be resolved to forge a deal. For instance, one could imagine an arrangement where Canada allowed increased temporary migration of labour — subject to a certain cap, as Worswick (2013) recommended in the context of the TFWP — in exchange for improved access to the Indian market in investment or important services sectors.

One final consideration is that politically a Canada-India trade deal may be difficult if there is only weak public support for it. Opinion polls conducted by the Asia Pacific Foundation of Canada have found less public support in Canada for trade deals with Asian countries than for deals with partners such as the US, EU and Australia. For instance, its 2014 poll found that only 38 percent of Canadian respondents supported a Canadian trade deal with India, versus 46 percent who opposed it. Canadians have concerns about competing with countries that have lower wages or lower labour or environmental standards.

This paper has provided a detailed analysis of Canada’s economic relationship with India, including the potential to strengthen that relationship through a formal trade agreement. While negotiations have been underway for several years, despite some promising developments, a significant breakthrough has remained elusive.

This might be about to change, however, as India is increasingly being viewed as a more serious trade partner in negotiations (Goold 2015). The Indian majority government elected in 2014 has a mandate to further open its economy to the world and is pursuing a more activist foreign policy. These developments, together with Modi’s recent visit to Canada, have provided an opportunity to focus on this often overlooked relationship.

In the context of Canada’s long-standing desire to increase its exposure to high-growth regions beyond traditional markets in North America and Europe, India is a natural choice. We find that Canada-India economic linkages are weak — Canada’s trade with India is much more likely to occur through small businesses than is the case with its trade with other emerging countries — but that these links have grown quickly in recent decades. The fact that the two countries’ trading relationship has not been overly important could result in a lack of urgency to conclude a deal, but it could also provide an opportunity to experiment with policy changes to be scaled up or down over time, based on each country’s assessment of the results.

We identified several fundamental factors that point to significant untapped growth potential for this relationship over the long term. India’s economic growth outlook is among the most favourable in the world. At the same time, however, many of its potential strengths could turn into weaknesses if they are not properly managed. Action is required to improve the country’s infrastructure, combat corruption, improve government bureaucracy, encourage female labour force participation, and enhance education and health outcomes. But Canada has strong social ties with India because of its large Indian diaspora; both countries have a common business language, similar legal systems, and democratic, federal governance structures.

We concluded that among the high-growth Asian countries India merits being a priority international market for Canada over the long term, and that finalizing the CEPA could provide a much-needed spark for a stronger economic relationship. This deal would be Canada’s second in the Asia-Pacific region and its first with a BRICS emerging market country. Seen together with NAFTA (North American links), CETA (Atlantic links) and possibly the TPP (Pacific links), the CEPA with India would mean that much of Canada’s trade would benefit from explicit trade preferences.

At the same time, we identified considerable obstacles that need to be overcome to conclude a truly comprehensive trade deal. The key challenge is that the areas that offer the greatest long-term gains are the most politically challenging, making it difficult for both sides to -conclude a good agreement. The most contentious areas are likely to be in FDI, services and temporary labour mobility, where bilateral linkages are the least developed (particularly regarding Canadian investment in India), where barriers to international commerce are the highest, and where the potential gains from further developing and exploiting each country’s comparative advantages would be the greatest.

For Canadian exports, natural resources and resource-based industries (agriculture and related products, energy, fertilizers and precious stones), as well as transportation industries (autos and parts), could be big winners in a trade deal. There would be adjustment challenges in Canada, particularly in business services (computer, software, ICT, outsourcing, call centres) and in some lower-wage labour-intensive manufacturing (such as textiles, apparel, chemicals and steel).

If a Canada-India trade deal is concluded by the end of 2015 as hoped, we expect a deal that is far less ambitious and much more limited in scope than the Canada-EU deal. And if the deal is not wrapped up at that point, we see a compelling case for Canada to remain at the negotiating table to conclude a deal, even if it cannot be struck as quickly or as comprehensively as some would like. One way to jump-start the relationship is for the two countries to agree to a less ambitious and less inclusive package, sooner rather than later, on a subset of issues where there are larger gains to be had. The details of that agreement could then be strengthened or weakened over time as each country learns through experience what does and does not work. This smaller deal might see Canada allow some temporary migration of skilled labour in exchange for Indian concessions in other areas such as services or FDI.

We also should not forget that a formal trade deal is not the only way to improve the Canada-India relationship. Efforts could be increased to leverage the personal networks of the Indian diaspora living in Canada, Canadian expats living in Asia or Indians who have studied in Canada and returned home. This could be done through Canadian universities’ alumni networks; educational exchanges among students, professors and researchers; and by strengthening business networks through, for instance, the India-Canada CEO Forum.

It is important to set reasonable expectations for what can be accomplished in the near term. Improving Canada’s engagement with India is a long-term project that requires a long-term perspective and sustained effort. Thus, Canadian policy-makers and the public need to adopt a long-term horizon for the growth of this trade relationship and set their expectations accordingly. If implemented, this trade agreement should not be viewed as a deal that could be fully evaluated in 2015, but rather as something that could be more properly assessed in a decade or two. The biggest opportunities will likely emerge gradually as the relationship becomes closer, more open and more competitive for businesses in each market. Engaging commercially in India has already been a long process for Canada. There is still a long way to go, but the potential rewards are large and they should be neither overlooked nor oversold.

We acknowledge the excellent research assistance of Shehyaar Ahmad, Emad Mahadavi, Edvins Ripa and Colin Chia. We benefited from discussions with Peter Hall, Rana Sarkar, Don Stephenson, Aaron Sydor, Yuen Pau Woo and Sara Wilshaw. We also thank Graham Fox, Tyler Meredith and the external reviewers for helpful comments on preliminary drafts.

Acharya, R. 2008. “Analysing International Trade Patterns: Comparative Advantage for the World’s Major Economies.” Journal of Comparative International Management 11 (2): 33-53.

Aiyar, S., and A. Mody. 2011. “The Demographic Dividend: Evidence from the Indian States.” Working paper no. 11/38. IMF. https://www.imf.org/external/pubs/ft/wp/2011/wp1138.pdf

Asia Pacific Foundation of Canada. 2014. “National Opinion Poll: Canadian Views on Asia.” https://www.asiapacific.ca/sites/de fault/files/filefield/national_opinion_poll_2014_final_0.pdf

Assaf, D., and R. McGillis. 2013. “Foreign Direct Investment and the National Interest: A Way Forward.” IRPP Study No. 40. https://irpp.org/wp-content/uploads/assets/research/competitiveness/foreign-direct-investment-and-the-national-interest/IRPP-Study-no40.pdf

Balassa, B. 1965. “Trade Liberalisation and Revealed Comparative Advantage.” The Manchester School 33: 99-123.

Batra, A., and Z. Khan. 2005. “Revealed Comparative Advantage: An Analysis for India and China.” Working paper no. 168. New Delhi: Indian Council for Economic Research on International Economic Relations.

Bloom, N., and J. Van Reenan. 2010. “Why Do Management Practices Differ across Firms and Countries?” Journal of Economic Perspectives 24 (1): 203-24.

Burange, L.G., and S.J. Chaddha. 2008. “India’s Revealed Comparative Advantage in Merchandise Trade.” Working paper no. UDE28/6/2008. University of Mumbai.

Canadian Chamber of Commerce. 2012. Canada-India: The Way Forward, January.

De Backer, K., and S. Miroudot. Forthcoming. “New International Evidence on Canada’s Participation in GVCs.” In Adapting Canadian Trade and Commerce Policies to New Global Realities, edited by S. Tapp, A. Van Assche, and R. Wolfe. Montreal: Institute for Research on Public Policy.

De Munnik, D., J. Jacob, and W. Sze. 2012. “The Evolution of Canada’s Global Market Share.” Working paper no. 2012-31. Bank of Canada. https://www.bankofcanada.ca/wp-content/uploads/2012/10/wp2012-31.pdf

Department of Finance Canada. 2012. “Economic Action Plan 2012: Jobs, Growth and Long-Term Prosperity.” https://www.budget.gc.ca/2012/plan/pdf/Plan2012-eng.pdf

Dobson, W. 2009. “Gravity Shift: Thinking about China and India in 2030.” Toronto: C.D. Howe Institute.

Foreign Affairs, Trade and Development Canada. 2009. “Canada’s State of Trade: Trade and Investment Update.” https://www.international.gc.ca/economist-economiste/assets/pdfs/per formance/SoT-CIdC_2009/SoT_CIdC_2009-ENG.pdf

—————–. 2012. “Canada-China Economic Complementarities Study.” https://www.investtoronto.ca/InvestAssets/PDF/Can ada-China-Economic-Complementarities-Study.pdf

—————–. 2013a. “The Economic Impact of the Canada-Chile Free Trade Agreement.” https://international.gc.ca/economist-economiste/assets/pdfs/research/canada_chile-can ada_chili-eng.pdf

—————–. 2013b. “Global Markets Action Plan: The Blueprint for Creating Jobs and Opportunities for Canadians Through Trade.” https://international.gc.ca/global-markets-marches-mondiaux/assets/pdfs/plan-eng.pdf

—————–. 2014. “Trans-Pacific Partnership (TPP) Free Trade Negotiations: Initial Environmental Assessment.” April. https://www.international.gc.ca/trade-agreements-accords-commerciaux/agr-acc/tpp-ptp/env-ea.aspx?lang=eng#a06

Foreign Affairs, Trade and Development Canada, and Canada-India Joint Study Group. 2010. Exploring the Feasibility of a Comprehensive Economic Partnership Agreement. July. https://www.international.gc.ca/trade-agreements-accords-commerciaux/agr-acc/india-inde/study-edude.aspx?lang=eng

Goldfarb, D. 2013. “Hottest Prospects for Canadian Companies in India.” Briefing. Ottawa: Conference Board of Canada.

Goold, D. 2015. “Canadian Companies That Do Business in India: New Landscapes, New Players and the Outlook for Canada.” April. Asia-Pacific Foundation of Canada. https://www.asiapacific.ca/sites/default/files/filefield/canadian_companies_that_do_business_in_india_ small_format.pdf

Government of India Planning Commission. 2014. “Sectoral Break-up of Employment and Value Added per Worker (93-94, 99-00)” 117. https://planningcommission.nic.in/data/datatable/0814/table_117.pdf

Industry Canada. 2011. “Canadian Small Business Exporters: Special Edition; Key Small Business Statistics” June. https://www.ic.gc.ca/eic/site/061.nsf/vwapj/KSBS-PSRPE_June-Juin2011_eng.pdf/$FILE/KSBS-PSRPE_June-Juin2011_eng.pdf