La future réforme du financement des soins de longue durée

Frances Woolley

Dans la conjoncture économique et financière actuelle, les régimes de retraite du secteur public canadien sont plus que jamais scrutés à la loupe. Selon leurs critiques, ces régimes à prestations déterminées seraient inéquitables parce que leurs versements sont beaucoup plus élevés que dans le secteur privé et que leur coût public est à la fois sous-estimé et non soutenable. Certains préconisent donc d’aligner les régimes des fonctionnaires sur les régimes à cotisations déterminées du secteur privé, où les salariés assument les risques de sous-financement. On parle aussi de plus en plus d’augmenter l’âge de la retraite et la part des coûts assumés par les employés.

Autant de questions à mettre en perspective à l’heure où plusieurs gouvernements du pays s’orientent vers une réforme des régimes de retraite du secteur public (Ottawa, l’Ontario et le Nouveau-Brunswick ont annoncé des changements importants cette année, et le Québec examine ses options). Dans cette étude, le spécialiste des pensions Bob Baldwin analyse le régime de pension de retraite de la fonction publique fédérale (RPRFP) en tant qu’étude de cas des grands enjeux de politique soulevés par ces réformes.

Au-delà des comparaisons simplistes entre les secteurs public et privé, l’auteur propose une évaluation critique et sur le long terme des questions de finances, de démographie et de gestion des ressources humaines liées au RPRFP et à l’ensemble de la fonction publique. Le RPRFP est effectivement très généreux, observe-t-il. Toute réforme doit viser à le rendre compatible avec les autres régimes du secteur public et les objectifs de renouvellement des effectifs. C’est donc dire qu’il faut des réformes plus significatives que celles prévues au budget fédéral 2012.

L’un des principaux aspects analysés touche la viabilité financière et le rapport coût-efficacité du RPRFP à l’égard de l’objectif clé de toute épargne-retraite, soit maintenir un certain niveau de vie après la retraite. Or les frais engagés actuellement pour couvrir les prestations du RPRFP au moment de la retraite approcheraient un seuil critique. Le coût des prestations pourrait être trop élevé par rapport à la valeur qu’elles auront à la retraite.

Ce déséquilibre devrait inciter employeurs comme employés à souhaiter des réformes, croit l’auteur. Il faudrait que les décideurs ciblent le coût global du régime (qui devrait atteindre, en 2013, 20 p. 100 de la masse salariale admissible et est à la hausse) et non seulement le mode de partage des coûts entre employeurs et employés.

Pour ce qui est d’établir le montant des prestations dans l’avenir, Bob Baldwin propose de le calculer suivant une approche de rémunération totale (englobant salaires et avantages sociaux) plus systématique que celle employée maintenant. Avec le vieillissement de la population active et la difficulté croissante d’attirer et de retenir du personnel, Ottawa devrait se garder de délaisser complètement la structure à prestations déterminées du RPRFP. Il lui faudrait plutôt adopter un cadre semblable au régime conjointement parrainé et gouverné (avec partage des coûts) qui prévaut dans le secteur parapublic ontarien, à l’exemple du Régime de retraite des enseignantes et des enseignants de l’Ontario. Cette approche permettrait au gouvernement de partager plus équitablement les risques de déficit avec les employés, tout en conservant une influence sur l’âge de la retraite de son personnel.

From time to time, the Public Service Superannuation Plan (PSSP), the pension plan for core employees of the Government of Canada, has been the subject of controversy.1 In the past several years, criticism of the PSSP has arisen again, along the following lines:

The federal budget of March 28, 2012, proposed changes to the PSSP. Documents tabled with the budget indicated that the normal retirement age for new entrants will rise to age 65 (from age 60) and that employer and employee contribution rates will become equal. Employee con- tributions had previously been targeted to reach 40 percent of the combined employer and employee contribution rate by 2014 (Finance Canada 2012). This is not happening in isolation — governments at all levels across the United States, the United Kingdom and Canada (notably, in New Brunswick, Ontario and Quebec) have considered or are currently considering major reforms in their public sector pension plans.

As the federal government embarks on public service pension reform, this study assesses the PSSP and identifies issues that need to be considered in thinking about possible changes to it. It dis- cusses the PSSP in the context of evolving trends in both the Canadian labour market and federal government employment. It examines the role of the PSSP in relation to the federal government’s wider human resources and compensation objectives, with which the PSSP should be consistent.

The study begins by comparing the PSSP with pension plans in the private sector and in the prov- incial public sector, looking at benefits, contribution rates, related financing and governance provi- sions. The next section examines whether contributions to the PSSP and the liability for it are being calculated and presented properly. This section also outlines the current financial status of the PSSP.

Then the study sets the PSSP in the context of total compensation of federal public employees and reviews research that compares total compensation in the public and private sectors. It also iden- tifies information problems and structural issues that inhibit a clear total compensation approach to the PSSP. Another type of context is the next topic: key trends in the Canadian labour market that will affect the ability of the Government of Canada (and other public and private employers) to recruit and retain employees in the future. The study demonstrates how these trends are re- flected in federal government employment and assesses the likely impact of these developments on the ability of the federal government to recruit and retain employees in the future.

Finally, I turn to matters that must be considered in discussions of reforming the PSSP. These include basic benefit design issues as well as financing and governance issues. The study ends with some general conclusions.

In this study I argue more broadly that changes in the workforce of the federal government and the labour market suggest there is a need for reforms to the benefit design, financial risk sharing and governance of the PSSP. There is also a need for greater clarity on how the PSSP fits within the total compensation of federal government employees.

To understand the context of workplace pensions today, it is helpful to begin with a com- parative analysis of realities in the public and private sectors. Understanding what lies be- hind these differences helps frame the environment in which the PSSP and any changes to it will ultimately operate.

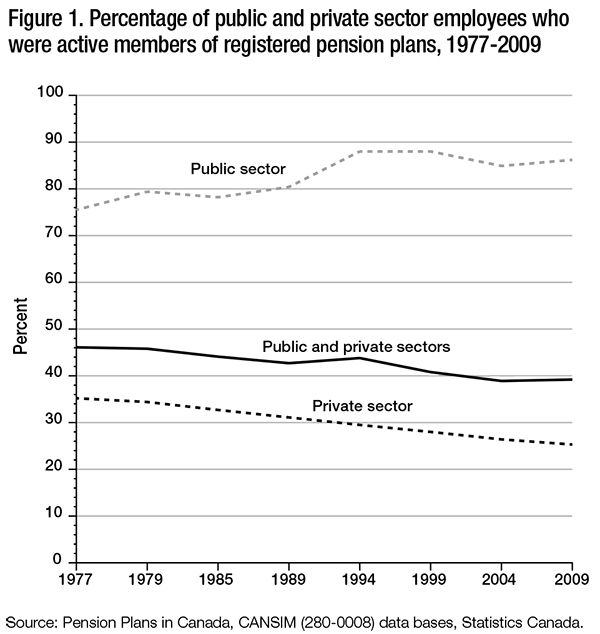

Much of the concern about the “pension advantage” enjoyed by public sector employees stems from two facts: public sector employees are much more likely than those in the private sector to participate in a workplace pension plan, and the form of pension in which they participate is predominantly a defined-benefit (DB) pension plan.

Figure 1 shows the percentage of employed Canadians working in the public and private sectors who were enrolled in workplace pension plans from 1977 through 2009. In neither sector was coverage at a high point at the end of the period. The participation rate in the public sector reached a peak in the early 1990s and has declined somewhat since then, while coverage in the private sector has declined steadily over the entire period.

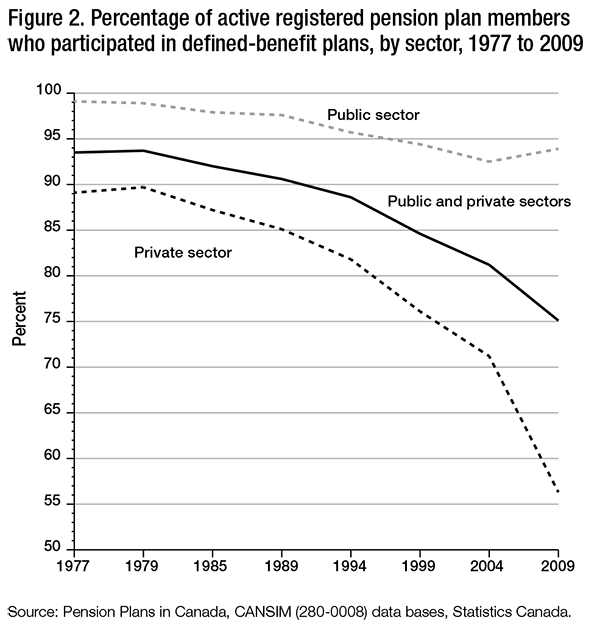

The shift in membership from DB plans to defined-contribution (DC) plans is shown in figure 2. The trend is evident in both sec- tors but has been particularly strong in the private sector since the year 2000.2

The data that underlie figure 2 are derived from plans where all active members are in either a DB plan or a DC plan. They exclude plans that are transitioning from DB to DC by requiring new members to accept DC benefits in a plan that had been DB. Over the relatively brief period from 2005 to 2011, membership in plans of this type grew from only 17,583 to 477,195 and 98 percent of the members of this type of plan were in the private sector. Membership in these plans is almost exactly half the size of the member- ship of plans that are completely DC. These figures also exclude group registered retire- ment savings plan (RRSP) coverage, which has been an increasingly popular method for private sector employers to support re- tirement savings among their employees.3 Data from the 2005 Workplace and Employ- ee Survey (Statistics Canada 2008) suggests that about 2 million employees outside of core public administration4 participated in these plans.

The shift away from DB plan participation in the private sector is clear. At the same time it is striking that DB plans are not yet on the brink of extinction there. According to Statistics Canada (CANSIM 280-0012), there were 11,331 DB plans in the private sector in 2010 with 1,687,904 members. Membership in private sector DB plans was 2.1 million in 2006.5

Much of the debate about the quantity and quality of workplace pension participation in the public and private sectors is conducted as if each sector were homogeneous over time. This is not the case. There have been long-standing variations within the private sector, and increasing variations are emerging within the public sector.

The characteristics of private sector plans depend on the industry and the size of employer. In 2010, the portion of employees who participated in registered pension plans (RPPs) varied significantly across different components of the labour market. Relatively high coverage sectors and participation rates were utilities, at 54 percent; finance, insurance and real estate, 39 per- cent; manufacturing, 37 percent; and construction, 37 percent. Low-coverage sectors included information and cultural industries, 19 percent; retail trade, 18 percent; personal, business and community services, 5 percent; and agriculture, 5 percent.6

Horner notes that coverage rates also vary substantially by the size of employer:

The incidence of RPP coverage rises dramatically with employer size, from 2.7% of the employees in firms with less than 50 employees to 81.6% in firms with over 500 employees. The challenge for expanding coverage under employer-sponsored plans is very clear. Firms with less than 100 employees account for only 4.2% of RPP members but two-thirds of the non-member population. (2007, 45)

An important question that is not sufficiently explored is whether the difference in participa- tion rates in the public and private sectors is purely a sector effect or whether it might reflect different attributes of the employees in the two sectors. On this the Canadian literature is not well developed. A 2009 study by Gougeon for Statistics Canada found that the growth of DC plans has been broadly felt across the private sector and appears to reflect shifts in “employer practices” rather than more structural changes in the labour market (Gougeon 2009). While Gougeon did not address compositional effects, much earlier work by Lipsett and Reesor found differences in RPP coverage to be explained in large part by differences in unionization and education among public and private sector workers (1997).

Some key similarities and differences in the workforce that makes up the membership of the PSSP and the overall Canadian labour market are discussed later in this study.

A lower level of participation in workplace pension plans in the private sector and the much greater likelihood of a private sector worker participating in a DC plan have captured the head- lines in public debate over the differences in pension plans in the private and public sectors. But there are other differences of note as well, particularly in how the plans are designed and how, within the public sector in Canada, pension plan provisions vary across provincial, federal and broader public sector employers.

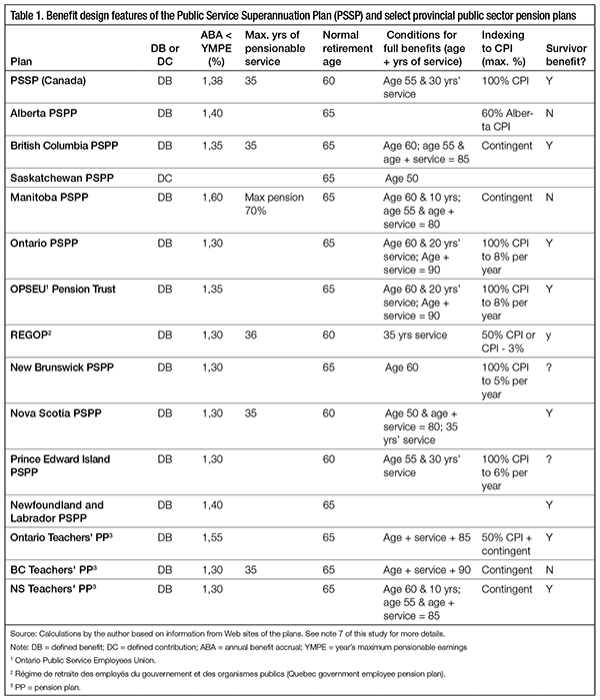

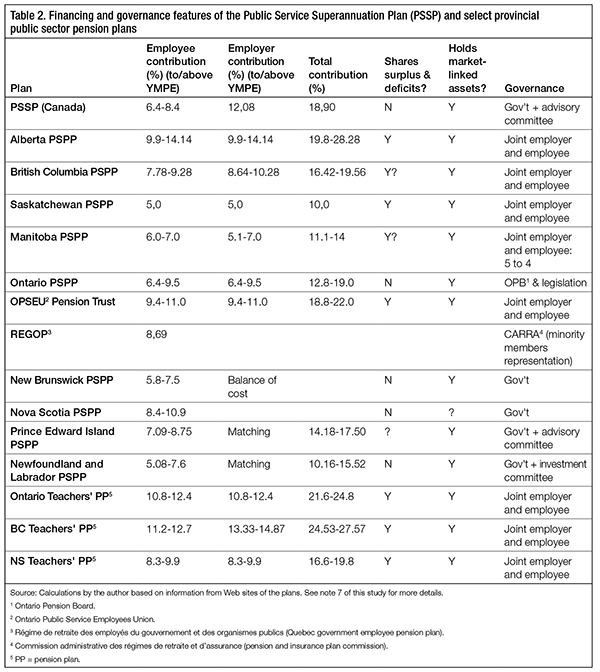

Not all public sector pension plans are the same — especially with respect to financing, gov- ernance and the purity of their DB character. Tables 1 and 27 summarize key data on the PSSP in comparison with the provincial pension plans for core government employees8 and three pension plans for teachers. In the following analysis, comparisons with the private sector rely on data from Statistics Canada’s Pension Plans in Canada (PPIC) dataset.

All but one of these public sector plans are DB plans. The Saskatchewan Public Employee Pension Plan is the notable exception, having been a DC plan since 1977. That so many public service pension plans are designed as DB is indicative, in part, of their significant membership size.9

The benefit structure is fairly common across Canada’s public sector. Plans tend to be integrated with benefits from the Canada and Quebec Pension Plans at age 65, and they base benefits on the best average earnings for five consecutive years. In the private sector, DB plans are, not sur- prisingly, much more heterogeneous. In 2008, the latest year for which the relevant PPIC data is available (CANSIM 280-0016), 45 percent of the private sector DB plan members were in flat benefit (FB) plans, which are common in unionized manufacturing and mining companies.10 Membership in career average earnings (CAE) plans made up 11 percent of the private sector DB membership, while 44 percent were in final average earnings (FAE) or best average earnings (BAE) plans. For a description of the differences in benefit formulas, see the appendix.

Many of the plans shown in table 1 provide some degree of indexation of benefits based on changes in the Consumer Price Index (CPI). According to data available through CANSIM 280-0025, 57 percent of public sector pension plans (with 67 percent of the membership of public sector plans) have some form of automatic indexation to the CPI. In the private sec- tor, 96 percent of the DB plan members belong to plans with no automatic indexation, but 65 percent of the plans provide some degree of it. Just over 11 percent of private sector plans provide full CPI indexing to 2 percent of plan members. It is the smaller private sector plans that provide the automatic indexing of benefits.

Table 1 shows that virtually all of the public sector plans whose benefit provisions were surveyed provide benefits for survivors, in addition to the retirement benefits of the worker. The cost of the survivor benefit payments is added to the cost of the retirement benefit payments. In the private sector it is common11 to provide survivor benefits that meet minimum statutory requirements.

The minimum requirements allow survivor benefits in DB plans to be provided on an actuarially equivalent basis. This means that the survivor benefit is “paid for” by a reduction in the amount of a retirement benefit that has a value equal to that of the survivor benefit (i.e., a retirement benefit is calculated according to the benefit formula in the plan and is then reduced so that the combined retirement and survivor benefits have the same value as the original retirement benefit).

In both the public and the private sectors, most workers belong to pension plans with a normal retirement age set at 65. In 2009, 84 percent of all members of public sector RPPs belonged to plans with a normal retirement age of 65, as did 98 percent of members of private sector plans. A minority of plan members, more significant in the public sector than in the private sector, belonged to plans with a normal retirement age of 60: 16 percent versus 2 percent (CANSIM 280-0024).

In assessing the role of retirement age provisions of RPPs in providing incentives to retire early, the normal retirement age is often less important than the other conditions under which “unreduced” early retirement benefits are made available. Table 1 shows that most of these public sector plans provide unreduced benefits before the normal retirement age. Unfortunately, there are no data from Statistics Canada to permit a direct comparison of these provisions between public and private sector plans.12 The availability of unreduced early retirement benefits may be less common in the private sector, but, where available, they may provide as strong an incentive to retire early as is found in the public sector. Schirle (2008) found that spikes in pension wealth13 associated with early retirement incentives in two private sector industrial pension plans were stronger than those in the PSSP and the Ontario Teachers’ Pension Plan (OTPP). The spike in pension wealth is slightly stronger in the PSSP than in the OTPP, partly because of the maximum number of years of service in the PSSP.14

Another area of difference is the treatment of mobile workers. In both sectors, the benefits of workers who leave an employer are established on the basis of the benefits they have earned up to the point when they leave their pension plan. In DB plans that base benefits on earnings — as most do — the benefits for “early leavers” are much lower than for those who stay, because the latter earn benefits based on later years of service and higher earnings.15 Early leavers have the right to receive a benefit from the plan they are leaving at the retirement date or to accept a lump sum transfer to a locked-in retirement savings account.

In the private sector, if plan members choose to receive a pension benefit from the plan they are leaving, typically no adjustment to the amount of the benefit will be made between the date of early leaving and the retirement date. In the private sector, it is also typical that workplace pension plans do not include a provision to accept “inbound transfers” on behalf of employees who come to a company after having participated in the plan of another employer.

On the issue of mobility, two things about the PSSP are important to note. First, the PSSP does pro- vide price indexation for the benefits of early leavers between the date of early leaving and the retire- ment date as well as during the retirement period. Second, the Government of Canada has worked out transfer agreements with more than 90 pension plans. These agreements facilitate the movement of people from one plan to another without a break in their pensionable service. These agreements are primarily but not exclusively with plans in the public and near public sectors (e.g., universities).16

The presence and amount of employee contributions to pension plans differ significantly be- tween the public and private sectors.17 Just over 900,000 private sector employees make earn- ings-related contributions to their pension plans, but only 50,000 contribute 7.0 percent or more. In the public sector, 2.7 million members make earnings-related contributions and 2.3 million contribute more than 7.0 percent of their earnings.18

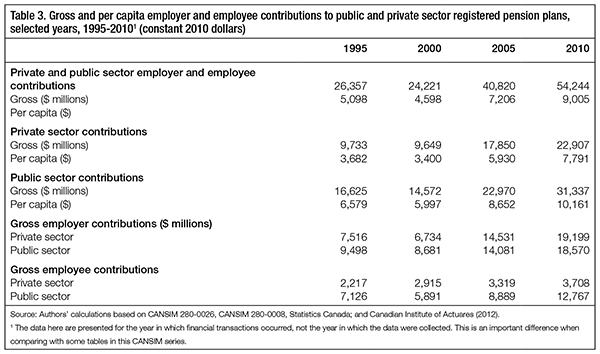

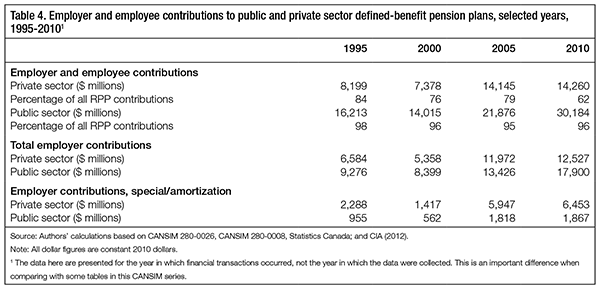

Unfortunately, Statistics Canada’s dataset does not provide sufficient information to calculate employer contribution rates or the combined employer and employee contribution rates across sectors and plans. However, data are provided on the aggregate dollar amounts of contributions and these are summarized in tables 3 and 4 for select years between 1995 and 2010. Table 3 pro- vides information on contributions to all RPP plans, both DB and DC, by sector, while table 4 focuses specifically on DB plan contributions. Several common themes emerge from this analysis:

A final point of difference between private and public sector plans relates to their member- ship. According to Statistics Canada (CANSIM 280-0015), in 2006, 82 percent of all public sector plans, representing 92 percent of all members, provided pension coverage for all classes of employees. Only 29 out of 1,288 public sector plans were exclusively dedicated to executives and management group members, and only 28,000 out of nearly 2.7 million members belong to such plans. In the private sector, a minority of plans (43 percent) are for all classes of employees, and just over half of all members (54 percent) belong to these plans. One-third of all private sector plans are for executives, and these plans include roughly 22,000 of 3 million members.

How does the PSSP compare with its immediate peers within the core public sector? From the data in tables 1 and 2, it is clear that the PSSP provides benefits that differ from many or most of the provincial plans in several respects:

Important differences have also emerged with respect to the governance of pension plans, the allocation of formal and legal responsibilities for surpluses and deficits and, more recently, the commitment to pure DB.

Starting in 1990, a number of pension plans in the broader provincial public sector were trans- formed from “traditional” DB plans into jointly governed plans with joint cost-sharing, known as jointly sponsored plans. Unlike the traditional DB plans in both the public and private sec- tors, these plans share the governance responsibilities between plan members and employers. Surpluses and deficits are also explicitly shared between the plan members and employers. The move to this type of plan was led by the Ontario Teachers’ Pension Plan (OTPP) and is a strong- er trend in the broader public sector than in core government employee plans, although some provinces use this model for core employees.

In their early days of operation, the jointly sponsored plans retained their purely DB benefit structure (all financial risk was being borne on the contribution-rate side of the plan and none on the benefit side). But falling interest rates and poor stock market performance in the early 2000s had the same adverse impact on these plans as on traditional DB plans: required contri- butions began to escalate to the levels noted in table 3.19 Plan governors looked for ways to ease the upward pressure on required contributions. A number of plans responded to the pressure by replacing indexation that was linked directly to changes in the CPI with indexation based, in whole or in part, on some measure of the plan’s financial well-being. Thus, some of the fi- nancial risk was shifted to the benefit side, and from young and future plan members to older active members and retirees. These plans are no longer purely DB. The PSSP has retained full indexation to the CPI and its purely DB character.

On the other hand, a striking similarity among the public sector plans listed in table 2 is that they all hold marketable assets (stocks, bonds, real estate, etc.). This may seem unremarkable. But even as recently as 1990, few would have held such assets. Most were financed on a “book reserve” basis. A liability would have been created in the sponsoring government’s statements of assets and liabilities, but the assets would have been bookkeeping entries to which interest would have been credited — typically at a long-term government bond rate. Some of the plans listed in table 2 have moved to holding marketable assets in the recent past, so that only a portion of the relevant pension liabilities are matched by marketable assets. The PSSP provides a case in point as it holds such assets to match liabilities that have accrued since April 1, 2000.20

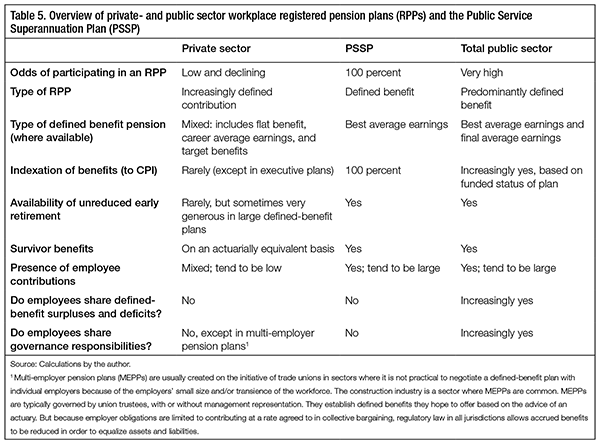

Differences between the pension realities in the private and public sectors are real and signifi- cant.21 Table 5 puts these in context by summarizing some of the key points of comparison between the two sectors, with specific attention to the PSSP.

The relatively good pension plans in the public sector come at a price. The cost of newly accru- ing benefits is higher in the public sector, and the deductions from employee wages and salaries that help pay for pensions are much higher. As can be seen in table 3, in 2010, employee con- tributions accounted for 40 percent of all contributions to public sector RPPs, compared with 16 percent in the private sector. It is also important to try to revisit the question addressed by Lipsett and Reesor (1997): to what extent is the difference in pension arrangements a purely public- versus-private difference, and to what extent is it a difference in attributes of the workplaces (e.g., size of the employee group) and employee attributes (e.g., level of education and earnings)?

The fact that the PSSP and workplace pension plans for other public employees are more generous than those typically available to employees in the private sector is by itself a source of concern to many people. This concern is sometimes accentuated by suggestions that the required contributions to the PSSP and its financial liabilities are underestimated and under- reported in the financial statements of the Government of Canada.22

It is unfortunate but almost inevitable that debates about these estimating and reporting issues involve technical detail that would be nice to avoid. Determining the value today of benefit promises that will be fulfilled decades in the future necessitates making assump- tions about a wide range of matters. In this estimating process, the choice of the discount rate that will be used to establish the current value of future benefit payments stands out as the assumption that will have the biggest impact on both the required contributions and the liabilities. In the most recent triennial report on the PSSP, the Office of the Chief Actuary (OCA) notes that a change of one percentage point in the discount rate changes the required contributions for newly accruing benefits by almost 20 percent (OCA 2012). Moreover, there are important conceptual debates about the correct approach to discount- ing future benefit payments, and these debates invariably lead to different conclusions about the numeric values.

Given the occasional suggestion that the financing requirements and reporting on the PSSP are deliberately hiding the true picture, in this section I examine the legislative and professional standards that guide these practices. The point is not to maintain that the debates related to the discount rate (and other matters) are not appropriate but to suggest that it is wrong to treat existing practice as an arbitrary contrivance that is designed to obscure reality.

In 1985, Parliament adopted the Public Pensions Reporting Act, which requires the Chief Actuary to submit financial valuation reports on the PSSP and other pension plans for public employees, including members of the Canadian Armed Forces and the RCMP. These reports, to be issued at least every three years and tabled in Parliament, are to be prepared in accordance with “the guides and Recommendations” of the Canadian Institute of Actuaries — or, in more contem- porary terms, in accordance with the actuarial standards of practice established by the Actuarial Standards Board. In addition, the public accounts of the Government of Canada include a pension expense calculation in statements of revenues and expenditures, and pension debt is covered in statements of assets and liabilities. These values are calculated in accordance with accounting standards established by the Public Sector Accounting Board.

The Auditor General (2012) recently reviewed debt reporting of the Government of Canada and included public sector pension debt in his analysis. He concluded:

Canada is a leader among member countries of the Organisation for Economic Co-operation and Development (OECD) in recognizing in its financial statements the obligations arising from public sector employee pension plans. In fact, very few other countries report these obligations on their financial statements. However, while complete financial information on the pension plans is available, it is dispersed among several reports and not presented in easy-to-read formats. (chap. 3)

Notwithstanding this favourable assessment and the conformity of accounting and actuarial reports with professional standards, financial reporting on the PSSP continues to be a subject of controversy and adverse publicity.

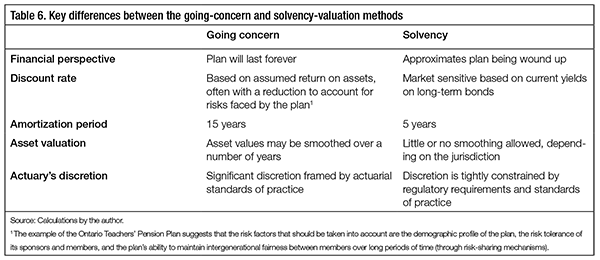

Since the late 1980s, all jurisdictions have required private sector workplace pension plans to prepare two balance sheets in their regular actuarial valuations: a going-concern balance sheet, as has always been required, and a new solvency balance sheet. Details of the solvency valua- tions vary among the jurisdictions, but some key differences between going-concern and sol- vency valuations are summarized in table 6. The financing requirements of the PSSP are based exclusively on a going-concern balance sheet.23

Because the solvency discount rate is based on current bond yields, it changes over time with bond yields. The going-concern rate does not change automatically with changes in financial market conditions but may be adjusted from time to time to reflect changing economic condi- tions and changes in the demography of a plan’s membership.

The greater volatility of the solvency measure that stems from its use of a market-sensitive dis- count rate is accentuated by the reduced scope for asset smoothing24 and, more importantly, the shorter amortization period for the solvency deficits: 5 versus 15 years. The result is that both sides of the balance sheet and the resulting actuarial balance are less stable on a solvency basis than on a going-concern basis.

Whether the solvency discount rate is higher or lower than the going-concern discount rate will depend on the relationship between current long-term bond yields and the longer-term assumptions used in going-concern valuations. In the late 1980s and early 1990s, when solvency valuations were first required, the solvency and going-concern dis- count rates were quite similar and the solvency valuations seemed quite benign. But as bond yields have fallen, solvency liabilities have risen. In addition, relatively weak stock market performance since 2000 has had a negative impact on the asset side of the balance sheet. Not surprisingly, solvency balance sheets have been a source of difficulty for plan sponsors throughout most of the period since the year 2000.

In its report for 2011 the Financial Services Commission of Ontario (FSCO) (2012) states that the median funding ratio for DB plans registered in Ontario was 98 percent on a going-concern basis, compared with 88 percent on a solvency basis. In addition, 52 percent of the plans were underfunded on a going-concern basis, compared with 88 percent on a solvency basis. Because solvency deficits have to be amortized over periods of no more than five years, the emergence of solvency deficits has driven up the required contributions of employers, as is indicated in table 4.

The fact that the going-concern valuations used in assessing the financial requirements of the PSSP are less volatile than private sector solvency valuations and that they generally give rise to higher discount rates in the current financial environment does not mean that going-concern valuations always create an easy financial hurdle to get over. The most recent triennial actuarial valuation of the PSSP is instructive in this regard.

The valuation of the PSSP assesses its financial status in two separate parts: an “Account,” which includes the value of assets acquired before April 1, 2000;25 and a separate “Fund,” which invests contributions made after that date — net of benefit payments due to service after that date — to a fund managed by the Public Sector Pension Investment Board. The Fund is designed to match the liabilities of the PSSP that arise from service after April 1, 2000.

According to the OCA (2012), as of March 31, 2011, the Account had an excess of assets over lia- bilities of $2.87 billion, while the Fund had an excess of liabilities over assets of $4.424 billion. The excess of liabilities over assets has to be amortized over a period of no more than 15 years, and the Chief Actuary has calculated that payments of $397 million per year over that period will eliminate the actuarial deficit.

The negative balance of the Fund is attributable in part to the fact that the smoothing of asset values used in the going-concern valuation means that investment losses that arose during 2008 and 2009 still have a negative impact on the actuarial value of the Fund’s assets. Investment earnings were $2.8 billion less than expected over the period since the previous valuation (March 31, 2008). In addition, revisions to actuarial assumptions (e.g., life expectancy) had a negative impact of $1.5 billion on the balance sheet. Of particular importance is a revision of the discount rate for the Fund from 4.3 percent real return (i.e., return net of inflation) to 4.1 percent.

As of the 2011 valuation date, the liabilities associated with the Fund were roughly half the size of the liabilities associated with the Account. This relationship will change in the future as an increasing portion of total liabilities will reflect service after April 1, 2000. Currently, the Fund is analogous to a young pension plan. But, as Hamilton (2007) points out, DB pension plans tend to get more difficult to manage as they mature. Net contributions (contributions minus benefit payments) tend to diminish in their importance as a source of a plan’s revenues; and invest- ment income, which is generally less stable and predictable, tends to become more important. In addition, liabilities tend to grow in relation to pensionable payroll, and as a consequence, the amortization of every percentage point of actuarial deficit represents a growing portion of payroll.

The fact that the PSSP is not subject to a solvency funding requirement is an obvious difference between its financial management and that of workplace pension plans in the private sector. It is a difference that has been important in recent years. But the difficulties that DB plans have had in satisfying solvency requirements have also resulted in changes to solvency requirements.

In the wake of the tech bubble bursting and falling interest rates in the early 2000s, sponsors of DB pension plans successfully lobbied for some relief from solvency funding requirements. The same scenario was played out in the wake of the financial crisis of 2008-09, and further ad hoc solvency relief has been offered in the past year.26

In 2006 and 2007, a number of jurisdictions launched reviews of their DB funding requirements as part of wider reviews of workplace pension plans. The review undertaken by the Ontario Ex- pert Commission on Pensions (OECP 2008) was somewhat more precise than others in speaking to the question of how, why and when solvency funding should be required. Its report argued that pure DB pension plans should be required to satisfy both solvency and going-concern funding tests, whether they are in the private or the public sector. However, the OECP also rec- ommended that plans that satisfy three criteria should be exempt from funding to a solvency standard, even though they should still be required to prepare solvency balance sheets for in- formation purposes.27 The three criteria were the following:

In other words, the OECP took the view that the greater risk to benefits that might arise from dropping a solvency funding requirement is acceptable if there is no pretense that the promised benefits are guaranteed in all circumstances and if plan members can assess the risks they face and decide how to respond to the risks through their participation in plan governance.

By the OECP’s criteria, the PSSP in its current form should be subject to a solvency funding require- ment. But if it were to be reformed in the same way that a number of the workplace pensions in the provincial public and broader public sectors have been, the funding requirements would be based entirely on a going-concern test, and solvency valuations would be for information purposes only.

Research by Robson and Laurin (2009, 2010, 2011) has been the source of well-publicized cri- tiques of the financing of the PSSP and its financial reporting. While each of these studies has focused on different dimensions of PSSP financing and financial reporting, the common element is a claim that the projected cash flows of the PSSP should be discounted on the basis of fair market values (also called fair values) — that is, the current market yield on assets that most closely resemble the liabilities of the PSSP. The authors contend that the PSSPs’ cash flows should be discounted based on the yield on Government of Canada real return bonds (RRBs) as of the effective date of an actuarial valuation or the date on which the government’s assets and liabilities are assessed. The RRB is favoured because it is the financial asset that most closely resembles the character of the benefit promises made to members of the PSSP. Like the PSSP’s benefit promises, RRBs are considered “risk-free” and fully indexed to price movements.28

With interest rates low in the past few years, the yield on RRBs has plummeted. When the bonds were first issued in the early 1990s, the yield was in excess of 4 percent, and even a decade ago, in 2002, it exceeded 3.50 percent. Since then the yield has fallen continuously to a level that has hovered around 0.5 percent since late 2011. The yield on RRBs is well below that used by the Chief Actuary in calculating required contributions to the PSSP, and it is lower than that used to determine the pension liability in the public accounts.

The lower the discount rate used in the calculations of the required contributions and liabilities, the higher is the required contribution rate and liability. Thus Robson and Laurin (2009) argue that the methods used to arrive at required contributions to the PSSP substantially underesti- mate them. Using the yield on RRBs as a discount rate, they conclude, suggests that required contributions should be in the range of 34 percent of pensionable payroll, as opposed to the 18.5 percent determined by the Chief Actuary.29 They argue that the fair value liability is thus $232 billion, as opposed to the $190 billion stated in the public accounts. These arguments are updated in Robson and Laurin (2010, 2011).

The fair value approach to the discount rate would be perfectly appropriate to a windup valuation of the PSSP (i.e., a valuation that tries to determine whether the assets of the pension plan that are on hand on the valuation date are sufficient to pay all of the benefits that have been earned to that date).30 However, it is far less clear that it is appropriate to valuations or financial analyses that are more forward looking. Even a small change in per- spective, from whether there are sufficient assets on hand on the valuation date to whether there are likely to be sufficient assets until the next valuation, would shift the focus from whether the RRB rate is appropriate given market conditions on the valuation date to the expected rate over the valuation period. Moreover, even in this relatively brief time frame, it might be advisable to shift the emphasis from choosing a single discount rate to apply over the period to working with a plausible range of rates, with a view to assessing the odds of having enough assets.

But there are even longer-term issues that might be addressed, and the use of a current RRB rate to discount future cash flows is less helpful again in this context. For instance, assuming a plan holds a diverse portfolio of marketable assets, one might want to know how much a plan spon- sor should expect to set aside each year over the long term in order to back future pension guar- antees. How this question is answered is highly relevant to longer-term financial planning and compensation. The traditional approach is to choose a discount rate that reflects a reasonable estimate of the expected return on the assets being held, with or without a discount to reflect the risks faced by the plan. This approach is not without its problems, but using a current RRB rate to discount the cash flows does not provide a realistic answer to the question either.

If the question that has to be answered relates to compensation planning, the fair value ap- proach to the discount rate becomes particularly problematic. Both the plan sponsor and the plan members have to make trade-offs between pensions and other types of compensation, such as salaries.

When interest rates are falling, as they have been recently, a market-sensitive discount rate will increase the required contributions to pension plans. Alternatively, benefits could be reduced or some other element in compensation will need to be decreased. There are some clear dangers in ignoring near-term market signals, but how often should the course be changed based on changing market conditions? With today’s computing technology, it is possible to calculate re- quired contributions and liabilities very frequently. But incorporating these consequences into a total compensation framework is very difficult because compensation decisions, such as those embedded in collective bargaining, are triggered less frequently.

Another complication of using current market rates is that they may not provide a clear view of future market conditions and the way that pension promises should be factored into decisions about future compensation. Assessing the relationship between current and future conditions requires keen judgment. If contribution rates and/or benefit levels are changed in response to a downward movement in interest rates, should they be restored when (and if) interest rate trends are reversed?

The approach taken to the discount rate by Robson and Laurin is valuable in a specific con- text.31 But it ignores a problem with traditional analyses that try to take account of longer time horizons. The discount rates used in traditional going-concern valuations are typically high enough that investment returns of the pension fund could achieve the discount rate only if a significant portion of the fund is invested in equities, as is the case with most pension funds. Equity returns vary significantly over time and can disappoint investors for extended periods, as we are witnessing now. This central attribute of equity investments (variability of returns) is obscured when a pension valuation incorporates a discount rate that includes an implicit equity return (risk premium) that is given a fixed value and projected forward year after year in an actuarial valuation. Financial planning for pensions that is built on this type of analysis does not identify the probability of adverse outcomes or the impact of adverse outcomes on required changes to contributions and/or benefits.

Much of the argument supporting the use of a discount rate based on RRB yield rests on the proposition that pension benefit payments are like interest payments on bonds. However, this analogy ignores important dissimilarities. The amounts, start dates and end dates of the cash flows from DB pension plans are highly uncertain. Although the fair value approach to valuing cash flows is sometimes commended for revealing the “true cost” of pension promises, the “true cost” is not known until the last payment is made to the last beneficiary. The cash flows are also subject to ongoing influence from the plan sponsor through the pro- cess of setting salaries and wages,32 and the plans, by definition, have contingent claims on sponsors for financial support if estimates of the plans’ costs prove too optimistic. Indeed, if there were bonds or other financial instruments with characteristics similar to those of a DB pension plan, DB plans would probably not exist.

The fair value approach suggests that sovereign debt (i.e., government bonds) will provide a good benchmark for a risk-free asset. This may be a reasonable assumption under most cir- cumstances, but not all. In fact, relying on a sovereign debt benchmark will — from time to time — produce some peculiar results. Investor confidence in the creditworthiness of an issuer of bonds is an important element in shaping interest rates. When investors have their greatest confidence in the ability of a government to pay its debts, interest rates will be low (all other things being equal) and government employee pensions will appear to be very expensive. On the other hand, when confidence is low and interest rates are high (as in Greece), government employee pensions will appear to be very cheap and affordable. This is an odd outcome.

When the fair value approach is applied to the PSSP, it is generally taken for granted that the benefit promises of the PSSP are risk free, and on this basis, the yield on Government of Canada RRBs is chosen as the basis for valuing benefits. But the “risk free” premise may not be appro- priate. Robson and Laurin comment that “For federal employees, the [funding] gap represents a risk if future taxpayers refuse to fill the hole left by inadequate contributions” (2010, 3). This raises a question about the riskiness of the benefit promises and whether the benefit promises should be valued based on the yield on a risk-free asset.33 Unlike a private sector employer, the federal government does not face a legal barrier to reducing accrued benefits, so for its members, the PSSP is not a risk-free asset after all. The debate engendered by Robson and Laurin is import- ant, but policy-makers should be wary about using their proposed method as the sole basis for valuation of the PSSP.

The PSSP is one component of a total compensation package that also includes wages and salaries, insurance benefits and paid time off. The question whether the total compen- sation of members of the PSSP is too little, too much or just right is an important question for a citizen and taxpayer. On its own, the size of the component parts of compensation, including the PSSP, is of little concern. An additional concern for a citizen or taxpayer is whether the PSSP reinforces human resources (HR) and other policy objectives of the federal government. In this context, the specific design features of the PSSP and the required contri- butions to it become an issue.

At several points since the end of the Second World War, advisers to the Government of Canada and, on occasion, prime ministers have articulated objectives for the pay of federal employees. A central feature of all these expressions has been the idea that the pay of these employees should be comparable to what is paid to employees in the private sector who do similar work. In 1977, the federal government tabled the Agenda for Cooperation: A Discussion Paper on Decontrol and Post-Control Issues (Finance Canada 1977), a policy paper, that was to guide a wide range of policies following the period of wage and price controls of 1975-78. This paper addressed the issue of compensation for federal government employees and focused for the first time on the need to make total compensation equal between the public and private sectors.

Conceptual, technical and structural difficulties make it hard to achieve comparability in prac- tice. In addition, the objective of comparability often has to compete with other policy object- ives. Thus, debate persists about whether the compensation of federal government employees satisfies the Goldilocks test (i.e., whether it’s just right).

In February 2007, the federal government articulated the Policy Framework for the Manage- ment of Compensation, which remains in effect. It states four principles by which compensa- tion would be guided:

The first principle is clearly designed to provide that when pension benefits are combined with other elements in the compensation package, the total amount of compensation should not exceed what is required to keep federal government employment competitive with private sec- tor employment. At the same time, the Policy Framework notes that in their application, these principles must be reconciled with one another, as well as with economic policy objectives, social policy objectives and public expectations and pressures.

Clearly, the application of total compensation principles does not take precedence over all other policy considerations.

The overall responsibility for HR management and compensation rests with the Treasury Board, and the responsibility for the PSSP is given to the president of the Treasury Board. Central respons- ibility for compensation rests at the political level. Moreover, the creation of the Office of the Chief Human Resources Officer in 2009 has added a focal point for HR matters at the officials’ level.

Authority for compensation on the government side of the employer-employee relationship may be centralized, but the engagement of employees on compensation issues tends to be fragmented. Although the PSSP’s legislative framework, the Public Service Superannuation Act, provides for an advisory committee that includes representatives of the unions whose members belong to it, the PSSP is not subject to collective bargaining. Many employee benefits are sub- ject to ongoing consultations between the government and unions through the National Joint Council. Only basic pay structures are subject to collective bargaining.

An unfortunate side effect of this fragmented approach is that it is not possible to work out direct trade-offs among the different components of the compensation package to the mutual satisfaction of the government and its employees. Because PSSP’s provisions are engraved in legislative stone, members find it difficult to fully appreciate the value of pension benefits as they fluctuate with demographic and market changes. Neither the employer nor the employees can easily place these benefits into a total compensation framework.

The Advisory Committee on Senior Level Retention and Compensation (ACSLRC) produces comparative data each year on total compensation for executives in the federal government and their private sector counterparts. It operates on the premise that the lowest level of federal government executives should have total compensation equal to that of the median level of their private sector counterparts. Total compensation for higher-level executives is based on in- ternal relativities. The practical effect of this approach is that the compensation of higher-level executives is low relative to that of comparable private sector executives. The ACSLRC takes the view that this gap is offset by “the nature of the work and the workplace as important factors in attracting and retaining talent” (ACSLRC 2000).

For employee groups covered by collective bargaining, the mandate for research on total com- pensation falls to the Public Service Labour Relations Board. This mandate was established in 2006. Information on the Board’s Web site indicates that only two reports have been published, both in 2008. These studies provide a good deal of helpful information on total compensation in specific sectors outside the federal government, but they do not provide information on the compensation of federal government employees. Presumably, this is meant to maintain neutral- ity in the way research is used to inform the collective bargaining process.

A significant effort was made by the federal government to address the comparability of com- pensation of federal government employees with compensation in the private sector in the con- text of the Expenditure Review of the Federal Public Sector (Lahey 2006). This effort concluded that, overall, compensation was about 10 percent higher for federal government employees than for their private sector counterparts and that the PSSP was the largest component of total compensation after wages and salaries. This type of information is not produced by the federal government on an ongoing basis.34

Concern and skepticism about whether the total compensation of federal government employees has been in line with private sector counterparts have prompted a number of studies, in the 1990s and again in the more recent past.35 A consensus emerges from these studies on three main points:

Quite a range of compensation gaps have been identified in the research; in fact, research by the Institut de la Statistique du QueÌbec has found a compensation gap favourable to private sector employees (Lahey 2006). This variation in findings highlights the difficulties in developing a definitive measure of total compensation. Establishing comparable jobs in the public and pri- vate sectors can be challenging because of sampling options, as can deciding what to include in the compensation package (e.g., job security); pricing certain benefits (e.g., pensions and paid time off); and choosing statistical methodology.

It is beyond the scope of this study to resolve all the differences in the debate on total compen- sation. But several key points seem to follow from research in this area:

Recent reports from the Clerk of the Privy Council to the Prime Minister on the state of the public service and the reports to the Clerk from the Prime Minister’s Advisory Council on the Public Service have identified recruitment and retention as major long-term issues (Clerk of the Privy Council 2008-12). Both take as a point of departure the view that employment within the federal government will continue to place emphasis in the years ahead on high- skilled, professional functions, while operational functions will tend to be outsourced. Thus the attraction and retention of university graduates as well as the impending retire- ment of many baby boomers are serious preoccupations. Also of note is the con- cern echoed in these reports about attract- ing mid-career candidates to the public service who can fill managerial positions.

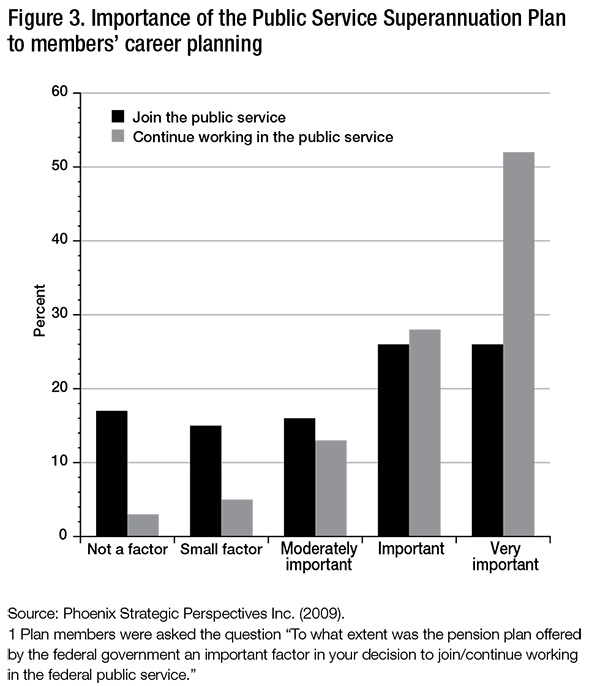

How pension benefits are designed is an im- portant consideration for recruitment and retention of prospective employees. The concerns about retention and when federal civil servants retire will likely become more acute in the years ahead as a result of the labour market changes discussed in the next section. Surveys of active employees of the federal government and of retirees indicate that the PSSP does play a positive role in re- cruitment and a stronger role in retention (Phoenix Strategic Perspectives Inc. 2009). As seen in figure 3, for the vast majority of public servants, the PSSP was a critical factor motivating decisions to join the public service as well as to stay. The role of the PSSP in providing a reason to stay increases with age and years of service. Other benefits tend to be relatively more important at young ages and lower levels of service. Women were more inclined than men to see the PSSP as a reason for staying in the public ser- vice (Phoenix Strategic Perspectives Inc. 2009).

DB plans are generally more conducive to retention and to attracting mid-career employees than DC plans. This reflects the fact that DB pension benefits accrue faster as retirement ap- proaches than is the case with DC plans. The advantage of DB plans comes at the cost of less predictable pension contributions and compensation. During a down market, these factors can accentuate budgetary pressures.

In the Chief Actuary’s latest triennial report (OCA 2012), the current service cost of the PSSP is estimated at 20.07 percent of total pensionable payroll for 2013, 20.21 percent for 2014 and 20.26 percent for 2015.36 Government contributions over the period will be 12.79 percent, 12.70 percent and 12.69 percent, respectively. With costs at this level, concern has to arise as to whether the current arrangement makes sense from a lifetime consumption perspective.

The “lifetime consumption” theory suggests that people should give up enough consumption while working, in the form of pension contributions or retirement savings, to secure a retire- ment income that maintains the same level of consumption as they enjoyed during their work- ing life. If a pension plan requires such a high rate of contributions before retirement that plan members’ pre-retirement standard of living is pushed below the post-retirement level, lifetime well-being is reduced.37

In applying the lifetime consumption theory to DB plans, it is important to remember that DB plans are generally designed to produce gross earnings replacement rates (measured as total retirement income divided by pre-retirement income), which are different from consumption replacement rates. For the PSSP, the maximum gross earnings replacement rate is 70 percent. But Wolfson (2011) estimates that a gross replacement rate of 65 to 70 percent of pre-retirement income corresponds to a level of consumption between 55 and 110 percent of pre-retirement levels. The variation in the replacement of consumption reflects a range of factors, including differences in the size and composition of households before and after retirement, whether a person is a renter or a homeowner, and specifics of tax situations.

As the contribution rates to generous pension plans increase, it is possible that the lifetime well-being of plan members will be enhanced by more consumption in the pre-retirement period and less after retirement. If so, the usefulness of the plan in attracting and retaining employees may diminish. I have previously pointed out (Baldwin 2008) that some of the jointly sponsored plans in the provincial public and broader public sectors, particularly those reformed since 2000, began their search for reform alternatives when total employee and employer contributions reached the level of 15 to 20 percent of earnings. The PSSP is now past that threshold.

The Canadian labour market is undergoing significant demographic changes that will con- tinue for many years. These changes will inevitably alter the context in which the federal government satisfies its human resources needs. As this occurs, the role of the PSSP as a tool to recruit and retain employees and to facilitate orderly exits from the federal government’s labour force may also require adaptation.

Discussions of demographic change typically focus on the aging of the baby boom generation. The baby boom is certainly large: people born between 1946 and 1966 accounted for 40 percent of employed Canadians as of December 2011 (CANSIM 282-0001), and the oldest members of this generation became eligible for old age security payments in 2011. In the federal public service, boomers are by far the largest age group of workers (Treasury Board Secretariat 2011). Moreover, this large cohort has had a significant impact on Canadian society at all stages of its life course.

However, the aging of the population involves more than the boomers growing old.38 Changes in life expectancy and fertility are key factors that make population aging a long-term trend. These are some of the implications of these changes:

The slowdown in labour force growth will likely shift the balance between the demand and supply of labour and give rise to some upward pressure on average compensation throughout the econ- omy. After a long period when average real wages and salaries have not grown, the Chief Actuary assumes long-term average real wage growth above 1.0 percent beginning in 2016, rising to an average annual pace of 1.3 percent between 2019 and 2050 (OCA 2011). As real wages rise, it is equally likely that an older workforce will place a greater premium on pensions and elements of compensation that trade off current income for longer-term security (see Towers Watson 2012).

On the demand side of the labour market, the retention of skilled employees is likely to become a more pressing issue for employers, as it will be relatively harder to replace retirees and early leavers with young replacements. Generally speaking, older workers are less likely to change jobs voluntarily than are younger workers.

The age of retirement has been increasing since the mid-1990s, and this trend is likely to con- tinue (Denton, Finnie and Spencer 2009; Carrière and Galarneau 2011; DataAngel 2011; Hicks 2012).40 The general tightening of labour markets is likely to lead to stronger inducements for older workers to remain at work. This general tendency will be reinforced by later entry into the workforce and by the increasing portion of the labour force who are immigrants. Both of these developments will be associated with a delay in accumulating the pension credits and assets necessary for a comfortable retirement. Higher levels of educational attainment should also reinforce the tendency to later retirement, as will general improvements in population health and the continuing shift toward a knowledge-based economy.41 DataAngel (2011) argues that between now and 2030, an increase in the average age of retirement of at least five years should be expected.42

Many of the changes taking place in the wider labour market are also observable in the federal public service. But there are three points of distinction between the public service and the wider labour market that help inform how we analyze future workforce renewal.

First, the federal government’s labour force is more highly educated and skilled and better paid than the labour force at large. In 2011, average earnings of PSSP members were $71,276, com- pared with Canada Pension Plan (CPP) maximum pensionable earnings for the year of $48,300. Because CPP maximum pensionable earnings are set at 106 percent of average wages and salaries payable on a full-year basis, workers who make above this threshold are dependent on workplace pensions, personal savings or a combination of the two to replace these additional earnings in retirement. For most of its members, the PSSP is obviously an important retirement planning tool.

The move to a more highly educated and skilled labour force has been accentuated in recent years as growth has been strongest in fields of employment requiring higher education and skills. Lahey notes that between 1995-96 and 2006-07, the job classifications in the federal public service grew fastest in a number of knowledge-intensive jobs and occupations, including computer systems, information services, economists and social scientists, biologists, law, physical scientists, admin- istrative services, executives, commerce officers and financial services. These classifications grew from 19 percent to 31 percent of the public service. Over the same period, declines were recorded primarily in nonprofessional classifications, such as secretaries, data processing, electronics, gen- eral labour, general services, ships’ crew, and clerical and regulatory workers. These job classifica- tions shrank from 34 percent to 21 percent of the public service (Lahey 2011).

Further evidence of this trend can be seen in levels of educational attainment among public servants, which are significantly higher than among workers as a whole. In 2010, 45.5 percent of federal government employees had university degrees, compared with 25.6 percent for the employed labour force as a whole. By comparison, in 1991 these figures were 26.1 percent and 15.1 percent, respectively.43 The share of university graduates in the public service is expected to continue to rise as demographic and labour market changes take effect. In a recent analysis of the federal workforce, the Public Service Commission (2008) found that just over two-thirds of all new recruits from outside the public service to permanent positions, including more than three-quarters of new recruits aged 25 to 34, had university degrees.

A second factor to consider is that employment levels and, to some degree, the age structure of federal government employment are prone to more rapid changes than is true of the labour force at large. While it is to be expected that employment levels of any individual employer can vary more than employment in the economy as a whole, Lahey (2011) notes this is particularly true for the federal workforce, which has gone through periods of both significant contraction and significant expansion over the past two decades. Following a drop in total employment of roughly one-fifth during program review in the mid-1990s, strong growth in hiring between 2004-05 and 2010-11 has pushed total employment in the public service to levels now exceed- ing those before program review.

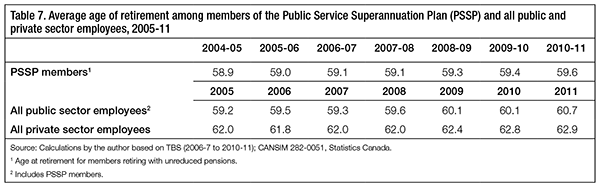

Third, as seen in table 7, the trend in the broader labour market toward later retirement has oc- curred more slowly within the PSSP. In general, PSSP members retire approximately three years earlier than workers in the private sector, and under one year earlier than other public sector employees. Increases in the average retirement age have also been smaller on an absolute basis compared with both the private and the public sectors as a whole.

As is true in the wider society and economy, baby boomers in the federal public service are now reaching retirement age, thus increasing both the age profile and the retirement rate in the public service quite significantly (Fox 2008). By 2007, retirements from the public service were three times the level they were at the start of the 2000s. The average age of active male PSSP members increased from 41.5 years to 45.1 years between 1980 and 2011. The comparable numbers for female active PSSP members are 36.6 years and 44.0 years. These changes have occurred at the same time as the portion of the PSSP membership under 30 has been shrinking (OCA 1985, 2012).

The age at which people become members of the PSSP is also of interest, because it will indicate the portion of PSSP members who may be eligible to retire with unreduced retirement benefits at age 55 with 30 years of service. In 1981, 55 percent of the new female members of the PSSP (i.e., those with less than five years of service) and 50 percent of the new male entrants were under age 30 and potentially able to have 30 years of service at age 55. By 2011, only 33 percent of new female entrants and 29 percent of new male entrants were under 30. Clearly, the portion of new entrants who might become eligible for unreduced benefits at age 55 declined over these three decades (OCA 1985, 2012).44

At the same time as active participants in the PSSP are getting older, the retired population is living longer. In his most recent triennial report on the PSSP (OCA 2012), the Chief Actuary assumes a reduction in annual mortality rates of more than 2 percentage points for males aged 60 to 80 between 2012 and 2031. After 2031, a further reduction of 0.80 percentage points is assumed. Mortality improvements would also be lower for women but would still amount to more than 1.35 percentage points per year up to age 80. In this respect, the PSSP membership is very similar to the population as a whole. With lower mortality rates, life expectancy at 65 will increase by 1 to 1.5 years by 2025 (OCA 2009).

The period between 1980 and 2010 saw a dramatic change in the gender composition of the active PSSP membership, much as happened in the wider labour force. Female active members of the PSSP45 went from 35 percent of total active members in 1980 to 55 percent in 2010 (OCA 1985, 1995, 1998, 2012). An important contributor to this increase is the fact that women were a growing portion of new entrants to the PSSP. The portion of federal employees who are female is likely to continue to rise unless it is offset by more women leaving the PSSP.

Trends in the labour market and in public service employment suggest that the PSSP should become a more important element in the compensation of federal government employees in the future. The public service is likely to become a more educated, better-paid and more diverse workforce (older and with greater representation from women and immigrants in particular). But at the same time, PSSP members are living longer, entering the workforce later and leaving for retirement earlier than the rest of the labour market (though retirement ages are increasing gradually) — all factors that will make the PSSP more expensive in the future.

Keeping DB features within the PSSP will be even more useful in the future. Retaining some leverage over the age of retirement will be helpful to the government as labour markets tighten and keeping employees becomes a more important consideration. On the other hand, retaining DB elements means the inevitable uncertainty of required contributions associated with the financing of DB bene- fits. Finding the right balance between these pressures is critical for the PSSP going forward.

It is clear that a broad range of challenges faces the PSSP, requiring an ambitious set of policy changes in order to provide an effective, efficient and equitable mechanism that balances the retirement income needs of members, the talent management needs of the employer and the fiscal limits of the taxpayer. All parties have a common interest in reforming and renewing the pension plan to meet four overarching objectives:

In this section I discuss some proposals for reform and set out questions that need further examination.

Required contributions to the PSSP have reached a high level, threatening to detract from life- time well-being, as many PSSP members could experience a lower standard of living while working than they will have in retirement. Moreover, demographic developments such as con- tinuing improvements in life expectancy and the later entry into the PSSP of new workers will increase the ratio of years in retirement relative to years of contributions to the PSSP and push contributions up further. These developments will be only partially offset by retirement at later ages. The increasing age of active PSSP members, combined with the greater representation of women, will increase the upward pressure on the contribution rate.

In addition, compared with the 1980s and 1990s, the difference between rates of return on financial assets and wage growth is likely to shrink, adding further to increased contribution rates. Beyond some point that may have been reached already, the PSSP may fail to meet the test of the lifetime consumption principle and may lose its usefulness as a tool for recruitment and retention. This is a problem for the government as employer and for PSSP members.

Looking beyond the level of contributions, there is the issue of rate variability. The most recent triennial valuation report on the PSSP (OCA 2012) shows an actuarial deficit of roughly $4.4 billion in the Fund that will require annual amortization payments of nearly $400 million per year. The impact of actuarial deficits is likely to increase, as the Fund will represent an increas- ing share of the PSSP’s total liabilities in the future. Imposing a solvency funding requirement would further increase the variability of contributions.

In its current form, the PSSP assumes that the Government of Canada, as the PSSP’s sponsor, has an unlimited willingness and ability to accept the variability of contributions. Whether this is true needs to be clarified. Experience in the jointly sponsored plans at the provincial level suggests that in practice, there is an upper limit to acceptable contributions at about 15 to 20 percent of pen- sionable payroll. Adopting the position that there is an upper limit to what the government will agree to take on as special contributions has important implications for benefit design. A limit on contributions cannot be reconciled with a complete guarantee of benefits, as in a pure DB plan.

The PSSP is like most single-employer DB plans in that it assigns formal and legal responsibility for amortizing actuarial deficits to the employer who sponsors the plan. In reality, it is often unclear who bears the ultimate economic burden to make up deficits in a DB plan.46 Despite this lack of clarity, there are likely to be circumstances under which the party that bears these responsibilities in law will also bear the economic burden. Keeping this in mind, it is important to note that there are options for changing how the formal responsibility is shared in the PSSP.

At present, the legal responsibility for deficits falls entirely on the government as employer and PSSP sponsor and ultimately on the citizen as taxpayer. But it could be shared equally, as is now the case in a number of provincial government plans. Quebec has another variation, the employee-sponsored plans that were created at the initiative of the trade union movement, called Quebec Member-Funded Pension Plans. In these plans, employees bear the formal and legal responsibility for underfunding, which results in increased contributions (from employ- ees) when pension plans encounter actuarial shortfalls. These alternatives do not eliminate the need to decide whether there is a limit to the acceptable variability of contributions, but they change the cast of players who have to make these decisions. For the PSSP, such a change would likely result in a different set of considerations, which may in turn lead to different decisions.

Workplace pension plans can add value to a compensation program by increasing the ability of an employer to recruit new employees, keep existing employees and provide for an orderly exit of employees.47 Labour market conditions in the future will likely make it more difficult to replace retiring employees and make the retention of existing employees a more important considera- tion. It will be desirable for the federal government to have some leverage over the age of retire- ment so as not to lose employees to retirement at an unplanned and too rapid rate.

The most basic choice about pension plan design is where to locate on the DB-to-DC spec- trum.48 Pure DC has a clear advantage in making required pension contributions certain, but it has risks as well. Modelling by MacDonald and Cairns (2007) suggests that the pure DC option entails the risk that large numbers of federal government employees across a range of age and service conditions will retire when conditions in financial markets make retirement optimal. The pure DC option means that the government as employer gives up all of its leverage over when its employees retire; the retention power of the pension plan is reduced; and the attract- iveness of the PSSP to mid-career employees is diminished.

Establishing the point along the DB-to-DC spectrum where the PSSP should be located depends upon the willingness of the employer and employees to absorb the contribution-rate uncertainty of DB designs. Given the advantages of DB designs to employees and the employer, the PSSP should offer as much certainty of benefits as is consistent with the willingness of those bearing the DB risk to accept the uncertainty of contributions. Many design options allow a mix of DB and DC elements.

The DB elements in the design of a workplace pension have the advantage for an employer of offering some leverage over the retirement decisions of PSSP members. Presently the age and service conditions under which pension wealth is maximized in the PSSP occur at ages that are too young. From the employer perspective, the current incentives run the risk of losing too many high-skilled workers at too young an age. From the perspective of the PSSP members, a declining portion will qualify for benefits at age 55 with 30 years of service, because they are staying in school longer and beginning work later.

The spike in pension wealth should be reached at a later age than at present, and the sharpness of the spike should be dulled. Conceptually, it is not hard to figure out how to increase the age at which pension wealth spikes. The age requirements, the service requirement or both can be increased. But an important question in this respect is whether pension wealth should peak at the same age for all class- es of employees. The current conditions under which the spike occurs may be appropriate for young entrants to the federal workforce who do physically demanding work but not for late entrants who work in the knowledge-intensive jobs, now the majority of occupations in the federal public service.

At present the PSSP provides strong incentives for employees to leave the federal public service at age 55 with 30 years of service. Looking ahead to a period of tighter labour markets, the government should slow down the rush to the exit when these conditions are met. With the changes announced in the 2012 budget, the normal retirement age for new entrants will rise to age 65. A number of other measures could also be used to weaken the incentive at 55 plus 30 when pension wealth is maximized:

Increasing the number of years over which earnings are averaged would do more than reduce the sharpness of the pension wealth spike. It would also remove a potential source of inequity. A relatively short averaging period — now five years — creates the possibility that PSSP members whose earnings increase rapidly just before retirement age get a much higher return on their pension contributions than do people whose earnings do not increase quickly just before retire- ment. All parties to the PSSP should assess whether this is a material concern.

The incentive to remain in employment after 55 plus 30 might be further enhanced by a mix of HR policy and PSSP changes to facilitate progressive retirement. On the HR side, these could include increased openness to reduced and more flexible work schedules. The PSSP could also allow employees to receive a partial pension while still employed, accruing new prorated benefits. Measures that dull the pension wealth spike would reinforce the strength of these initiatives.

The government’s general approach to HR includes the central goal of hiring university gradu- ates and retaining the new hires in the public service for their careers. A secondary need is to recruit people in mid-career. In general, the PSSP is well suited to encourage mid-career transfers to the public service, given its basic DB structure and the network of transfer agreements that are in place. Expanding the network of transfer agreements to the private sector could help, as could an open-ended commitment to accept lump sum transfers into the PSSP from all pension plans.

As the pension expert Keith Ambachtsheer has noted on many occasions, large size is an import- ant virtue in a pension plan (Ambachtsheer 2007). Economies of scale and scope are available to large plans, and the PSSP certainly qualifies as a large plan. Indeed, it is significantly larger than the minimum efficient size mentioned by Ambachtsheer of 50,000 members and $10 billion in assets. Bearing in mind that the PSSP exceeds the size needed to achieve significant efficiencies, it is worth asking the following two questions about the Plan: Are the retirement income needs of all classes of employees sufficiently homogeneous that a single plan for all makes sense? Do career paths and intra-governmental mobility justify a single plan?