La future réforme du financement des soins de longue durée

Frances Woolley

Cette étude examine les récentes propositions de réforme des retraites au Canada, dont celles portant sur une hausse des prestations ou du plafond de cotisations du Régime de pensions du Canada (RPC), les nouveaux régimes recommandés par des groupes d’experts provinciaux ainsi que le régime supplé- mentaire de retraite du Canada mis de l’avant par Keith Ambachtsheer. Ces propositions visent à répondre aux inquiétudes soulevées par le recul de la participation aux régimes de retraite d’em- ployeurs, lequel, n’ayant pas été compensé par une augmentation de l’épargne-retraite individuelle, entraînera une baisse du niveau de vie d’une minorité significative de futurs retraités. L’efficacité restreinte des régimes d’employeurs et des options d’épargne-retraite individuelle est également en jeu.

Les propositions que Bob Baldwin examine dans cette étude ne reposent pas sur l’initiative volontaire d’employeurs ou de particuliers. Car une modification des règles — fiscales et autres — applicables aux régimes de retraite privés ne suffira pas ; il faudra redéfinir la frontière entre programmes obligatoires et facultatifs afin d’améliorer la couverture en matière de pensions.

Toutes les propositions partent du principe que les employeurs individuels, notamment les petites entreprises, ne sont pas les organisations les plus à même d’offrir une pension. Toutes préconisent aussi une capitalisation entière afin d’assurer l’équité intergénérationnelle. Mais l’auteur estime que, au contraire, la capitalisation entière ne garantit pas l’équité entre les générations et risque de freiner inutilement l’instauration de nouvelles prestations.

Les différences entre les propositions mettent en évidence certaines questions qu’il faudra résoudre : l’étendue des gains auxquels s’appliqueraient les nouvelles dispositions, le choix du type de régime (à prestations déterminées, à cotisations déterminées, ou une combinaison des deux), le caractère obligatoire ou non de la participation, et l’incidence de toute modification sur les nombreux régimes d’employeurs actuellement en place et qui fonctionnent bien.

L’auteur note que l’expansion du RPC présenterait des avantages, notamment des frais d’administration peu élevés, une couverture élargie et une relative certitude quant à l’âge de la retraite et au montant des prestations. Mais il faudra tenir compte de certains inconvénients, comme l’obligation qui pourrait être faite aux travailleurs à faible revenu et aux travailleurs autonomes d’épargner au-delà de leurs besoins, ou la déstabilisation des régimes d’employeurs existants. De plus, une expansion entièrement capitalisée du RPC risquerait d’entraîner des taux de cotisation instables, susceptibles de nuire à l’emploi.

Si les autres propositions présentent aussi des inconvénients, l’auteur soutient que ceux-ci pourraient être minimisés en modifiant ces propositions de réforme.

Dans leurs délibérations sur la réforme des retraites, les ministres des Finances du pays doivent résoudre plusieurs dilemmes, notamment en ce qui touche l’importance accordée aux préférences individuelles par rapport aux avantages des instruments de portée générale ; le degré de certitude des prestations par rapport à celui des cotisations ; ou encore l’assurance d’obtenir un revenu de retraite adéquat sans hausse déraisonnable des coûts des régimes.

In June 2010, federal, provincial and territorial ministers of finance met in Morel, Prince Edward Island. It was their third successive semiannual meeting at which pension reform and retirement income adequacy were important items on the agenda.

Before the meeting, the Ontario and federal finance ministers wrote their colleagues to set out their governments’ positions. Both endorsed an unspecified modest increase in Canada Pension Plan (CPP) benefits, and proposed changes to tax and pension rules that would permit the financial services industry to provide multiemployer defined-contribution pension plans to employees and the self-employed outside the context of an employer-employee relationship. The majority of ministers present endorsed this approach, the Alberta minister being the one public dissenter.

The ministers’ proposals were cast at a very high level and leave important questions unanswered — many of which are presented in this paper. Nonetheless, the announcements coming out of the meeting in PEI will make it very difficult not to introduce a package of changes that includes these elements. The meeting of finance ministers in Kananaskis, Alberta, in December 2010 should give us a better sense of the extent to which the ministers will stay on course.

My primary purpose in this study is to present the range of pension reform options that have been discussed in Canada since 2008 and have fed into the finance ministers’ thinking. I focus particular attention on proposals that address concerns about limited and declining participation in workplace pension plans through measures that are not entirely voluntary. Reforms based on purely voluntary measures have been deemed by stakeholders and experts to be necessary but not sufficient. Voluntary programs give only limited coverage in the OECD countries that use them; as well, it is implicit in much of the current debate that single employers — in particular, small ones — may not be the best platform to deliver pension coverage above and beyond the publicly managed parts of the retirement income system. I intend the comparison of the various reform proposals in this study to inform readers and also to help identify issues that need to be addressed in deliberations on pension reform. As implied by the subtitle of this study (which is a reference to Bruce Little’s 2008 book Fixing the Future: How Canada’s Usually Fractious Governments Worked Together to Rescue the Canada Pension Plan), while a revolution may not be necessary, clear choices will once again have to be made.

To set the context, I begin by discussing Canada’s retirement income system and issues related to participation in workplace pension plans1 and retirement income adequacy. I then briefly outline the full range of pension reform options that have been under discussion, and describe in some detail the key proposals that do not rely entirely on the voluntary initiatives of employers and individuals. This part of the study focuses mostly on the proposals’ design parameters. I compare and contrast the latter set of proposals and discuss a number of substantive issues associated with them. Following that, I assess the potential impact of some of the key reform proposals, and I conclude by evaluating the alternative approaches and highlighting some of the high-level philosophical issues in the debate. An appendix describes the continuum of choice along the spectrum from defined-benefit to defined-contribution plans.

For decades, Canada’s retirement income system, like that of most OECD countries, has consisted of three main components, or “pillars.” Most of the reform proposals I discuss in this study relate primarily to the second pillar, currently made up of the Canada and Quebec Pension Plans (CPP/QPP).2

The first pillar is made up of programs financed through general tax revenues, of which Old Age Security (OAS) and the Guaranteed Income Supplement (GIS) are the most important in terms of numbers of beneficiaries and dollars that flow through them. The OAS is paid at age 65 to Canadians who meet residence requirements. Since 1989, a special tax has been imposed on OAS recipients with incomes above a threshold level ($66,733 in 2010). The GIS is an incometested program that pays a maximum benefit to people with no income except OAS. The GIS benefit is reduced by 50 cents for every dollar of income received from sources other than OAS. Benefits are indexed quarterly to changes in the Consumer Price Index (CPI). A federal program called the Allowance and provincial top-ups to the GIS also form minor parts of the first pillar.

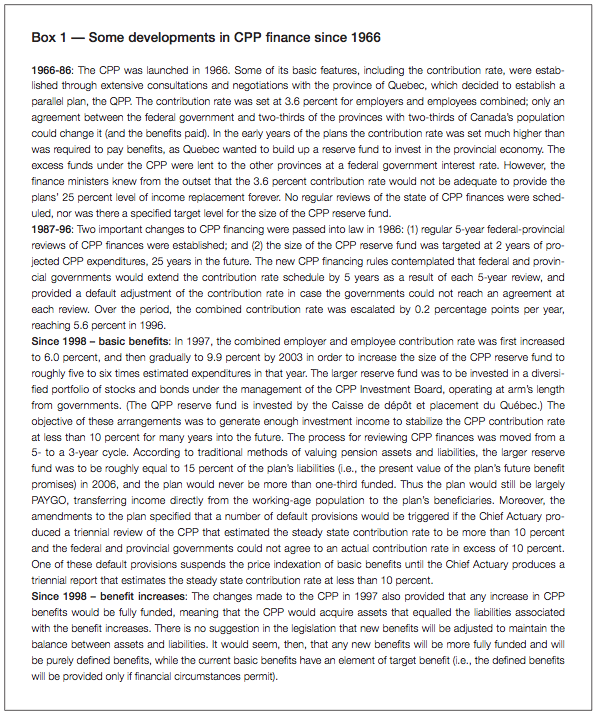

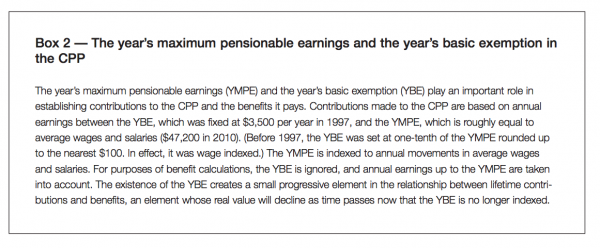

The second pillar is made up of CPP/QPP, compulsory earnings-related programs for the employed and self-employed that provide retirement, survivor and disability benefits as well as benefits for children of deceased and disabled contributors. The plans are designed to provide a retirement benefit of 25 percent of preretirement earnings, but only on annual earnings up to a year’s maximum pensionable earnings (YMPE),3 an amount equal to roughly the average wage and salary ($47,200 in 2010). The 25 percent benefit rate applies at age 65. Lower benefits can be initiated between the ages of 60 and 65, and higher ones between ages 65 and 70. The YMPE is indexed annually to changes in the average wage and salary, and once benefits start being paid to an individual they are indexed annually to changes in the CPI. The QPP applies to Quebec and the CPP to the rest of Canada; the two programs are distinct, but provide benefits that are structured similarly and are fully portable. The contribution rate and certain key features of the CPP/QPP have been adjusted through time; some of the main changes affecting the plans’ finances are described in box 1.

The third pillar is made up of workplace pension plans and Registered Retirement Savings Plans (RRSPs). This pillar is privately administered but receives support from the tax system; in addition to that, workplace pensions are regulated in the public interest. The third pillar is striking in its diversity. Some workplace pension plans are capable of delivering very good pension benefits, although a majority of the working population at any given moment does not participate in workplace pension plans at all. Many Canadians use RRSPs, but these represent an incomplete substitute for workplace pension plans as a way of maintaining living standards in retirement. Using 2006 Canada Revenue Agency data, Horner (2009) finds that 45.9 percent of all households participate in workplace pensions only or participate in them in addition to RRSPs, whereas 19.8 percent participate only in RRSPs. He estimates that 70 percent of all households saving through RRSPs only will meet a 90 percent consumption standard, compared to 80 percent of those who participate in workplace pension plans only and 82 percent of those who participate in both.

Pillar 1 addresses minimum income or antipoverty objectives. In combination, OAS and GIS benefits come close to exceeding the cutoff line for poverty, by most definitions. All three pillars can help employed people to achieve a different objective: to maintain their standard of living in retirement. But the publicly administered pillars 1 and 2 meet this objective fully only for those earning less than half the average wage and salary. At higher levels of earnings, people need third-pillar income to maintain their standard of living.

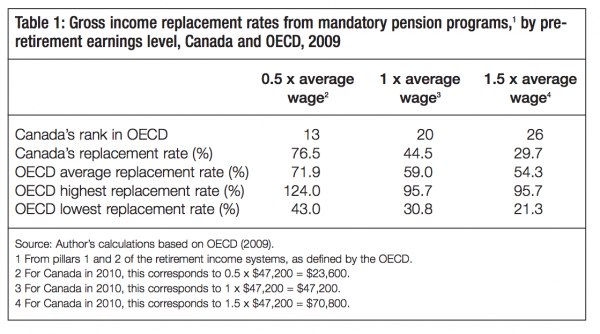

Although most OECD countries’ retirement income systems have all three pillars, the systems combine the pillars in significantly different ways. Canada is among the Anglo-Saxon countries, whose publicly administered programs place more emphasis on the anti-poverty objec-

tive and replace much greater portions of low than high earnings. Table 1 is instructive on this point. It presents the stylized replacement rate of pillars 1 and 2 (only) in Canada, and Canada’s rank order among 30 OECD countries at levels of earnings ranging between half and one and one-half times the average wage and salary. Taking into account the two publicly administered pillars, Canada ranks relatively high at low levels of earnings and much lower at high levels. (That is, the Canadian system replaces the earnings of those with low earnings quite well, but falls comparatively short in replacing the earnings of those with higher levels of earnings.) Consequently, the relatively positive assessment of the Canadian retirement income system in terms of the earnings replacement objective owes much to the contribution of the third pillar. There is a good deal of concern, however, that the third pillar will not contribute as effectively in the future to meeting the earnings replacement objective.

The adequacy of retirement incomes4 is typically judged by two criteria: whether incomes are above a low-income or poverty line, and whether they permit retired people to enjoy the same standard of living after retirement that they enjoyed before retirement.5 Other criteria that play a less prominent role are the relationship between incomes of retirees and incomes of younger age cohorts, and the predictability of retirement incomes.

Baldwin (2009) notes that by virtually any criterion, the latter part of the twentieth century was a period of significant improvement in the incomes of the elderly in Canada. The incomes of older couples increased in real terms (i.e., net of inflation) by 55 percent between 1976 and 2007, while the real incomes of elderly unattached individuals increased by 79 percent over the same period. (Unless otherwise noted, people who are “older” or “elderly” are those aged 65 and over.) The sources of income of the elderly also changed over these years. Income from the CPP/QPP and from the third pillar (workplace pensions and RRSPs) grew, reflecting the maturing of these arrangements.6 Income from employment and investments declined, and income from OAS and the GIS remained stable. There was also a noteworthy equalizing tendency in incomes of the elderly, with the ratio of incomes at the 95th percentile declining in relation to those at the 5th percentile from more than 8:1 in the late 1970s to about 4:1 in the mid-1990s. There has been a slight upward drift since then.7

The poverty rate among the elderly as measured by the after-tax low income measure (LIM) declined from 35 percent in the late 1970s to about 3 percent in the mid-1990s, rising to about 5 percent a decade later.8 This is one of the lowest rates of elderly poverty among the 30 high-income countries that make up the OECD (Veall 2008; Milligan 2008). The income gap between the elderly and non-elderly has also declined. In addition, an analysis of longitudinal data showed that most of the current elderly had sufficiently high incomes in relation to preretirement earnings to be likely to maintain their standard of living. However, a significant minority have incomes that are likely too low to achieve that objective (LaRochelle-Côté, Myles, and Picot, 2008).

Without diminishing the importance of what was achieved during this period, three points of caution need to be kept in mind. The first is that the improvement noted in areas such as poverty reduction among the elderly, the equalizing tendency in their incomes, and the growth in real income from the CPP/QPP was achieved by the mid-1990s; the subsequent period has been one of stability or minor decline. (It is worth noting that there has been a continual increase in real income provided by the third pillar and a small increase in employment income in the 2000s.)

The second point is that there are subsets of the elderly population who experience poverty rates significantly higher than the norm, such as single elderly women, recent immigrants and elderly people with dependants (Veall 2008).

The final point of caution is that the improvement in the incomes of the elderly reflects not only the maturing of key parts of the retirement income system, but also the interaction of various components of the system with a particular set of economic circumstances. The maturing process is largely complete and is unlikely to be the source of new growth in retirement incomes. Moreover, the outcomes generated by the retirement income system were ameliorated by low inflation (after 1990 in particular), high rates of return on financial assets and low wage growth, all of which made it easier to achieve both replacement rate objectives and relative income objectives. The same retirement income system would have produced different outcomes under different economic circumstances (Baldwin 2009).

Despite the strong record of achievement in recent decades, concern about future retirement incomes has become quite broadly based. Underpinning much of this concern has been a widely noted continuous decline in the portion of the employed workforce that participates in workplace pension plans. In 1977, 46 percent of the employed workforce participated in these plans, but by 2008, the percentage was down to 38. The decline has been continuous and gradual. A parallel development over the same period has been a shift in the form of participation from defined-benefit (DB) to defined-contribution (DC) plans. (Of the two, only DB plans are generally considered to offer certainty as to the benefits that will be provided. See the appendix for a more detailed account of these plan types.) In the late 1970s, roughly 95 percent of the members of workplace pension plans belonged to DB plans. By 2005, that number had fallen below 80 percent. These contemporaneous changes have been felt in both the public and private sectors, but have been more pronounced in the latter, where in 2005 roughly 25 percent of employees participated in workplace pension plans (down from 35 percent in the late 1970s), and DB plans accounted for about 60 percent of plan membership (down from 90 percent in the late 1970s) (Baldwin 2009).9

These trends in workplace pension coverage are widely recognized and form the basis for a good deal of the current debate on pension reform. But it is important to note some of the limitations of the data and of the inferences often drawn. The source of the data just cited is Statistics Canada’s Pension Plans in Canada (PPIC) database, built up from filings that workplace pension plans are required to make with federal and provincial regulatory authorities. The database does not include data related to participation in group RRSPs. There is legitimate debate about whether a group RRSP should be considered as the equivalent of a DC pension plan. If they are equivalent, then the overall decline in coverage would be smaller but the shift to DC participation would be greater. Elsewhere, I have estimated that including group RRSP membership as DC membership leads to the conclusion that roughly half of plan membership in the private sector is in DC plans (Baldwin 2008).10

The denominator in the coverage calculations just cited is the employed workforce. Subject to certain caveats identified below, this is an appropriate denominator if the question to be addressed is the portion of the workforce that will be able to replace preretirement earnings with workplace pension income. However, if the question is what portion of the adult population is likely to end up with some workplace pension income, then the coverage calculation must use the adult population as the denominator. If we calculate coverage by workplace pensions in this manner, we find that coverage is quite stable over the period since the late 1970s (Baldwin 2007). The stability results from the fact that the employment-to-population ratio has been increasing, while the portion of employed persons who participate in workplace pension plans has been declining. One trend has been offsetting the other.

Irrespective of the denominator, the participation of women in workplace pensions has been increasing relative to that of men. According to the PPIC data, the portions of employed men and employed women who participate in workplace pension plans were almost equal in 2008, although only 15 years before, male participation exceeded female participation by 10 percentage points. An important consequence of the increased labour force participation of women and the closing of the coverage gap between genders is that coverage measured at the family level has declined less than coverage measured at the individual level (Morissette and Ostrovsky 2006).

In addition to concerns about trends in coverage and the shift to DC plans, there has been debate about what underlies the decline in the portion of the workforce that participates in workplace pension plans. Two lines of thought predominate in these discussions: one places emphasis on regulatory burden and inadequate incentives to create workplace pension plans; the other emphasizes the role of structural shifts in employment and the decline in the portion of the workforce that is unionized. The latter is more easily quantified. Morissette and Drolet (2000) estimate that most of the decline in the portion of the workforce that participates in workplace pension plans between 1984 and 1998 could be accounted for by shifts in employment from sectors of the economy with high coverage to sectors with low coverage and by declining unionization.

The difference between household or family coverage and individual coverage, and the different perspectives that arise as the coverage denominator changes and participation in group RRSPs is taken into account, point to the need to exercise caution in extrapolating directly from workplace pension coverage measured in terms of PPIC data to future retirement income prospects. The need for caution is accentuated by the fact that people who are not active members of workplace pension plans at a particular moment may be members later (e.g., young workers currently employed in the retail sector). Also, the change in vesting rules11 for workplace pensions in the late 1980s in all Canadian jurisdictions increased the possibility that job changers who are not currently participating in a workplace pension plan may be owed benefits from a former plan. Changes in the rules governing survivor benefits created a new class of beneficiaries made up of people who never belonged to a workplace pension plan.

The decline in workplace pension coverage and its implications for retirement incomes in the future has become a focal point for intergovernmental policy dialogue. A meeting of federal, provincial and territorial ministers of finance in May 2009 established a research program to be organized and overseen by Professor Jack Mintz of the University of Calgary. Mintz commissioned six research studies, four of which addressed workplace pension coverage and income adequacy.12 The province of Ontario commissioned me to prepare a research report addressing the same two issues (Baldwin 2009). When the ministers met again in December 2009, Professor Mintz presented a summary report (2009) on the research prepared under his guidance, and the Ontario delegation presented my conclusions. The mandate given to the researchers was diagnostic; they were not asked to make policy recommendations. All the studies that addressed the question of future income adequacy reached two broadly similar conclusions, summarized in the following statements from Mintz’s report: “The first conclusion from the research is that Canadians are by and large doing relatively well in ensuring that they have adequate savings for retirement…There is, however, evidence that not all working Canadians are saving enough to obtain the same level of consumption in their retirement as in working years” (2009, 26).

Mintz adds: “These estimates suggest that one fifth of Canadians may not have sufficient RPP [registered pension plan] and RRSP assets to replace at least 90 percent of their pre-retirement consumption” (2009, 26).13 This number appears to come from research undertaken by Horner (2009). Horner developed detailed estimates of the percentage of the population at four different levels of earnings whose savings through workplace pension plans and RRSPs seemed insufficient to permit consumption at 90 percent of the preretirement level. The “one-fifth” cited by Mintz is for the population as a whole. Given the redistributive nature of Canada’s first pillar, Horner estimates that only 3 percent of low earners will fall short of the 90 percent consumption target. But the percentages are higher for the higher-earnings groups.14 Horner’s numbers also vary by family type and are higher if a standard of 100 percent of preretirement consumption is used to judge the results: 31 percent of the entire population using the 100 percent standard, versus 22 percent (Mintz’s one-fifth) using the 90 percent standard.15

An important issue in the assessment of retirement income adequacy is the question of how to treat assets that may not have been accumulated specifically to provide for retirement, but which provide consumption and possibly income during retirement. Housing equity is the most broadly based and important example. The importance that one attaches to the decline in workplace pension coverage turns to some degree on the role one attributes to other forms of wealth.

The Mintz summary report (2009), the research prepared for Mintz, and the Ontario study (Baldwin 2009) all recognize some role for nonpension assets in contributing to the well-being of Canadians in old age. None of them explicitly addresses the importance of wealth in the form of workplace pension assets as opposed to other kinds of assets. However, they do make passing comments that demonstrate differences in the perceived importance of the two.

Mintz’s summary may attribute the least importance to workplace pension wealth. He cites a research finding in Ostrovsky and Schellenberg (2009) that earnings replacement rates for men and women aged 70 to 72 who belonged to workplace pension plans in their mid-50s are no higher than those who did not belong to workplace pension plans.16 He uses it to diminish the significance of Horner’s (2009) finding that people who have saved only through RRSPs are less likely to meet retirement income objectives than those who belong to workplace pension plans.

Ostrovsky and Schellenberg’s findings (2009) imply that the greater retirement wealth of people who belong to workplace pension plans shows up more clearly in the age at which they retire than in the income they receive after retirement. Horner’s interpretation is compatible with the findings of Ostrovsky and Schellenberg, who point out in their 2009 study that workplace pension plan members are more likely to retire by age 70 to 72 than are nonmembers. This is consistent with earlier research based on results of the General Social Survey, in which Ostrovsky and Schellenberg concluded that preretirees who were members of workplace pension plans had a clearer view of their retirement date than did nonmembers, and planned to retire earlier (2008). Put another way, for people who are not members of workplace pension plans, the age of retirement is more uncertain than the replacement rate.

Of the papers prepared for Mintz that address income adequacy, the Horner paper (2009) is the clearest in the importance it attaches to participation in workplace pension plans. The Ontario study (Baldwin 2009) notes that, while forms of wealth other than pensions can generate consumption and income in old age, pensions and other forms of wealth tend to complement each other rather than substituting for one another. It urges more research on the issue of wealth substitution, in order to obtain a more complete picture of the adequacy of financial preparedness for retirement among future cohorts of retirees.

By and large, the studies prepared for Mintz and his summary report assume that the current institutional, economic and financial environment will be stable in the future. The Ontario study, however, points out a number of foreseeable trends, including the decline in participation in workplace pension plans, that will tend to increase the difficulty in providing retirement incomes in the future.17

Studies being prepared for the IRPP (in particular, Horner forthcoming, Wolfson forthcoming) add strength to the concern that a significant portion of middle earners are likely to face a decline in their standard of living under existing pension and retirement income arrangements.

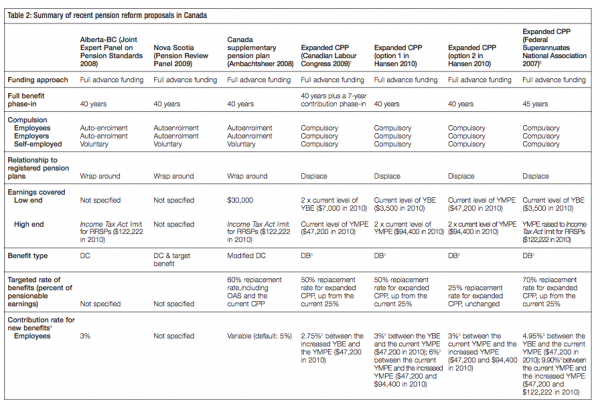

In late 2008 and early 2009, four provinces issued reports arising from formalized study and consultation by arm’s-length panels inquiring into workplace pensions. In November 2008, the government of Ontario released the report of the Ontario Expert Commission on Pensions (the Ontario Commission)(OECP 2008), and a week later, the governments of Alberta and British Columbia released a report prepared by the Joint Expert Panel on Pension Standards (the Alberta-BC panel) (JEP 2008). In January 2009, the government of Nova Scotia released the report of its Pension Review Panel (the Nova Scotia panel) (PRP 2009). The governments of Canada and Quebec addressed similar issues in less formal “in-house” consultations.18

This intense activity focused on workplace pensions reflects a number of problems that had been simmering for some time. They included the following:

The mandates of the provincial inquiries varied somewhat, but they shared a common core — to address problems related to DB financing, including funding rules and the use of surpluses. Although some stakeholders took issue with the inquiries’ recommendations, their adoption would likely make workplace pensions easier to manage by eliminating ambiguity in the regulatory law. The reports understood, however, that regulatory change on its own would not solve the problem of declining coverage. Thus, they addressed this problem as a separate issue.

The Alberta-BC panel and Nova Scotia panel reports recommended the creation of provincial pension plans for employees not already participating in workplace pension plans. In contrast, the report of the Ontario Commission proposed expanding the range of choices for providing pensions within a voluntary framework, which might make it easier for small workplaces to provide pensions at a reasonable cost. It recommended the creation of an Ontario Pension Agency that would serve as a home for deferred vested benefits and might also receive pension contributions from employers and employees. It also recommended that some of the larger pension plans in the province be allowed to provide investment and other services to employers and individuals.19 Finally, the commission suggested that Ontario look into the possibility of increased benefits under the CPP as called for by numerous stakeholders.

The provincial inquiries had a substantial degree of engagement with various stakeholder groups. Not surprisingly, the stakeholder groups and many individuals with a policy interest in pensions have also been articulating reform proposals over the past few years. These fall into three clear groupings.

The first group of proposals is intended to ameliorate the operation of workplace pension plans and/or individual retirement savings without changing the balance between existing voluntary (privately administered) and compulsory (publicly administered) arrangements. The recommendations of the provincial inquiries on matters other than coverage fall into this category.

Some of the proposals in the first group would alter the tax rules governing pensions and retirement savings plans to encourage more retirement saving. Many of these proposals would increase the scope for making tax-deductible contributions to retirement savings vehicles; a minority would change the tax incentive per dollar saved. Some tax-related proposals would drop the requirement that registered pension plans involve an employeremployee relationship between the plan sponsor and plan members, a structural change to the tax rules that the insurance industry has promoted vigorously. The limited incentive that people with low earnings have to save for retirement, including the effect of the GIS tax-back, has received less attention.20

The second group of proposals focuses on first-pillar arrangements — OAS, the GIS, the Allowance and provincial top-ups. The first pillar of the retirement income system has generally not been central to the recent debate on pension reform. The Canadian Labour Congress (CLC 2009) and Monica Townson (2009) have advocated increased GIS benefits for the single elderly as the lesser part of a package of reforms that includes CPP expansion. Tamagno (2007) has proposed changes to OAS to address equity issues, but with no intention of significantly changing the role of OAS in the retirement income system.21 The one proposal that would significantly change the role of OAS was made by Tom Kent (2009), a key policy adviser to former Prime Minister Lester Pearson, who recommends increasing the OAS by 40 percent above changes in the price index. Economist Jonathan Kesselman (2009) has suggested that a reduction in, and gradual elimination of, OAS benefits could be coupled with a significant increase in CPP benefits.

The third category of proposals — the ones that this study examines in detail — would change the balance between mandatory and voluntary arrangements and, in some cases, between privately and publicly administered plans. Some of these proposals would expand the role of the Canada and Quebec Pension Plans as a source of retirement income, while others would develop new institutional mechanisms that are not purely voluntary but may involve some degree of private administration. The primary purpose of these proposals is to increase the proportion of the workforce that participates in pension plans and retirement savings schemes that will allow them to maintain their standard of living in retirement. Their proponents are concerned about the declining portion of the workforce that participates in workplace pension plans, the management and security of these plans, and the effectiveness and cost-efficiency of individual options currently available.

Two things should be noted about the proposals of the third type. First, they tend to emphasize key features of desired reforms without providing much detail on their implementation. This is a reasonable approach for proponents to take at this stage. Second, while several of the proposals I describe would increase CPP benefits, other aspects of the CPP are not fully reflected in reform proposals. These omissions are important enough to warrant a word of explanation. From the time of the CPP’s establishment in 1966, changes to benefits and contributions have required agreement between the government of Canada and two-thirds of the provinces with two-thirds of Canada’s population. The changes made to the financing of the CPP in 1997 established different financing rules for basic benefits in existence at the time and for future new benefits (see box 1). The effects of these changes are rarely taken into account in the proposals; they are discussed below.

Maintaining parallelism between the CPP and QPP has also been an important objective for Canada and Quebec from the inception of the plans. But the different demographic and economic trajectories of the two populations are putting strains on the ability of the two plans to maintain the same contribution rate and very similar benefit structures. Consultations in Quebec have been organized to discuss options for dealing with the future of the QPP (see RRQ 2008). None of the reform proposals I discuss addresses the problem of maintaining parallelism in the future.

Also missing from the reform proposals reviewed here is consideration of the future value of OAS and the GIS. OAS and GIS benefits are indexed quarterly to changes in the CPI. Average real wages have been constant since the early 1980s. As a result, the price indexation of OAS and the GIS has preserved not only the purchasing power of benefits but also the relationship between OAS and GIS benefits and average wages. However, if demographic change induces increases in real wages, as the Chief Actuary anticipates (OCA 2007b), then the value of OAS and GIS benefits relative to the average wage and salary will decline in the absence of OAS increases above those provided through price indexation. As a result, OAS and the GIS will be less able to meet an antipoverty objective,22 and replacement rate targets will have to be met more fully from other sources. The latter issue is explored in Wolfson (forthcoming).

Much of the current interest in pension reform was sparked by the Alberta-BC Joint Expert Panel on Pension Standards (JEP 2008). The Alberta-BC panel proposed the creation of a provincial pension plan that would operate in the two provinces and that other provinces could join. (Saskatchewan has shown some interest in doing so.) Participation in the plan would be on an auto-enrolment basis for employers and employees, meaning that employees would be automatically enrolled in the plan; those who did not wish to participate would need to opt out. Employers would also have the right to opt out.23 There is some ambiguity about whether employees could opt out if their employer did not. The self-employed, however, would have to opt in to be enrolled in the plan.

The Alberta-BC panel noted that the auto-enrolment approach has been used in the United States in its equivalent to group RRSPs, and has been introduced in national schemes in the United Kingdom and New Zealand. The panel ruled out the possibility of operating a compulsory plan at the provincial level rather than nationally, on the grounds that the required contributions to the plan would put employers in the participating provinces at a competitive disadvantage.24

The Alberta-BC panel was generally more conscious of laying out key plan parameters than are most proponents of change. The panel noted that auto-enrolment should probably apply to employees with earnings above a specified level on the grounds that people with low lifetime earnings are adequately provided for through OAS, the GIS and the CPP/QPP. It left for future study the earnings level above which auto-enrolment would apply, as well as the question of how auto-enrolment would apply to nonpermanent employees.

The plan design envisaged by the Alberta-BC panel is pure DC. The panel rejected both target-benefit plans25 and DB plans as being too complex and entailing possible government financial liability for delivering promised benefits. The choice of investments for the plan’s fund would rest with the governors of the plan rather than individual plan members. The panel mooted a number of other possible plan design features, such as having a basic level of required contributions as well as an optional higher level (e.g., 3 and 6 or 9 percent for each of employer and employee), permitting an employer to pay all contributions, and permitting annuity purchases over a period of years before retirement to spread the interest rate risk at retirement over a number of years.

The proposed plan would operate as a not-for-profit organization at arm’s length from government for the exclusive benefit of the plan beneficiaries. The plan’s governing body should have a majority of members with relevant expertise and a minority of stakeholder representatives who would be required to take appropriate training to fulfill their responsibilities. Governments would limit their financial commitment to defraying start-up costs; otherwise, the plan would be self-financing. The panel hoped that the Canada Revenue Agency could administer the collection of contributions.

The Nova Scotia Pension Review Panel recommended creating a provincial pension plan for Nova Scotia that broadly resembles the plan proposed for Alberta and British Columbia (PRP 2009). Yet although the Nova Scotia panel’s proposal is referred to as a “plan,” it can also be thought of as an organizational structure that supports a variety of plans.

In the Nova Scotia panel proposal, participation would not be mandatory, but employers with 50 or more employees who do not operate their own pension plan would be automatically signed up and would have to opt out. Employers and employees in smaller firms and selfemployed persons could opt in to the new plan. The panel does not mention the possibility of employees in these firms having a right to opt out if their employer opts in. The plan would also act as an institution to which employees who leave their employer before retirement, or whose employer terminates its own plan, could transfer lump-sum settlements.

Although the plan would be a DC plan, individual employers could instead participate on a target-benefit basis (i.e., a DB element would be present). Custom arrangements for funding and benefits could also be provided to groups of employers such as municipalities, and to participants in sector-based organizations such as organizations of retailers or IT firms.

The Nova Scotia panel also proposed that if the Superintendent of Pensions identifies a plan that is being badly managed, the Superintendent “should have the power to transfer the assets and management of it to one of the plans offered under the province wide plan.” While the general intent of this proposal is clear, its precise financial implications are not.

As was the case with the Alberta-BC panel proposal, the plan proposed by the Nova Scotia panel would operate at arm’s length from the provincial government and would be subject to the provisions of the provincial Pension Benefits Act. The province would take financial responsibility for creating the required organizational structure for the provincial plan but would “not be responsible for the funding risks, nor for any costs of administration or investment management.”

Keith Ambachtsheer (2008) has proposed creating a Canada supplementary pension plan (CSPP). The CSPP would automatically enrol employees with earnings of $30,000 per year and above who do not belong to a workplace pension plan. The plan would be designed to generate a 60 percent earnings replacement rate when combined with OAS and the CPP. A default contribution rate (10 percent of earnings is suggested) would be divided equally between employers and their employees. The proposal envisages both opt-out and opt-in rights for employers and employees. The CSPP would operate subject to tax and regulatory laws governing pensions, including the maximum RRSP contribution limits under the Income Tax Act (18 percent of earnings on earnings up to $122,222 in 2010, or a maximum contribution of $22,000).

Contributions to the CSPP would be held in individual accounts to which Canadians would have the right to transfer their other retirement savings. The accounts would be invested in a “risk optimizing portfolio,” but participants would have the right to select instead a more conservative “hedging portfolio.” At age 45, the default option would be to begin purchasing deferred annuities, so that by age 65, half their accumulated wealth would be in the form of annuities. Participants would also be free to alter their level of annuity purchases and to manage the rate at which they withdraw their assets.

Ambachtsheer sees the CSPP as being managed at arm’s length from government but launched through a government initiative. He raises the possibility that assets could be managed by the CPP Investment Board (CPPIB).

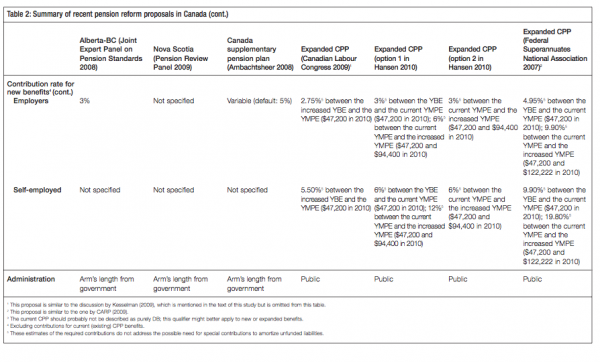

In January 2010, the British Columbia Minister of Finance, Colin Hansen, acting in his capacity as chair of the Steering Committee of Provincial/Territorial Ministers on Pension Coverage and Retirement Income Adequacy, issued a discussion paper, Options for Increasing Pension Coverage among Private Sector Workers in Canada (Hansen 2010). The paper discussed the CSPP proposal, comparing and contrasting it with three options for reforming the CPP. One of the options would increase the level of pensionable earnings from the current level of roughly the average wage and salary ($47,200 in 2010) to one and one-half times the average wage and salary ($70,800 in 2010); the second would increase the level to twice the average ($94,400 in 2010). The third option would see the level of pensionable earnings and the benefit rate doubled. In other words, the CPP would ultimately provide a retirement benefit equal to 50 percent of preretirement earnings on earnings up to twice the average wage and salary ($94,400 in 2010). (See box 2 for an explanation of CPP contribution levels.)

In presenting these options for reform, Hansen noted that no jurisdiction had endorsed any of the options. However, he cited important stakeholder groups that have been proponents of CPP expansion: the Canadian Labour Congress (CLC 2009), the Canadian Association of Retired People (CARP 2009) and the Federal Superannuates National Association (FSNA 2007).26

Hansen’s options for CPP expansion capture important elements from the proposals made by the stakeholder groups but leave aside some noteworthy possibilities. For example, the CLC (2009) proposes doubling to 50 percent the CPP benefit rate on the existing pensionable earnings base ($47,200 in 2010), and British Columbia economist Jonathan Kesselman (2009) discusses a 60 percent benefit rate on the existing pensionable earnings base. The FSNA (2007) has proposed a 70 percent benefit rate on all earnings on which tax-deductible RRSP contributions can be made (in 2010, 18 percent of earnings on earnings up to $122,222).

Neither Hansen’s options nor the proposals coming from stakeholders envisage significant changes in CPP design except for increases in the benefit rate and level of pensionable earnings. The one exception to this generalization is the CLC proposal to double the size of the YBE from $3,500 to $7,000. Proponents of reform see the CPP continuing as a compulsory earnings-related program for the employed and self-employed. They regularly describe the CPP as a DB plan, despite the element of target benefit in the basic CPP benefits.

The reform proposals generally do not discuss the existing governance and management structure of the CPP at any length. This would seem to be an area where silence can quite safely be taken as approval of the status quo.

This section reviews similarities and differences in the reform proposals I have chosen to highlight. These are summarized in table 2.

The proposals for reform I discuss in this study have several things in common. I chose them because they focus on the same retirement income objective — allowing people to maintain their standard of living in retirement. They do not focus on the objective of providing a minimum level of income. The CLC (2009) proposes to increase the GIS for the single elderly in order to bring their incomes above the poverty line, but the central proposal of the CLC is a doubling of the CPP benefit rate. The other proposals reviewed here do not address minimum income. For the provincial inquiries, this issue was outside their terms of reference. The proposals also reflect a common perspective that the voluntary adoption of workplace pension plans and/or the use of individual retirement savings accounts will not achieve this standardof-living objective for an adequate portion of the workforce. Generally, the proponents of reform reach this conclusion on the basis of evidence that the low and declining coverage of workplace pension plans is not being offset by increased use of RRSPs. These two points are central to Canada’s current debate on pension reform.

The reform proposals do not stem exclusively from concerns about the numbers of persons participating in workplace pension plans and using individual retirement savings plans. For many years, Ambachtsheer has expressed concern about the governance and management of workplace pension plans, specifically the plans’ lack of scale, the managers’ insufficient expertise, and the misalignment of interests between plan beneficiaries and the plan governors and managers. All the reports prepared for provincial governments reflect these concerns to varying degrees. The CLC (2009) has also raised concerns about the security of promised defined benefits and the adequacy of workplace pension benefits.

The reform proposals are also striking in that they focus primarily on solving retirement income problems in the future.27 The CLC proposals include a GIS increase which, presumably, would be phased in to help the current low-income elderly. But the centrepiece in the CLC’s proposals is a doubling of the CPP benefit rate. The new higher level of benefits would only be based on years of participation in the plan after the new benefits are adopted. Thus, it would require a full working career to achieve the ultimate 50 percent benefit rate; in CPP terms, that is at least 40 years in the future. None of the other proposals differ on this point. This approach is certainly very different from that of the late 1970s and 1980s in which the relatively low income situation of the current elderly animated much of the discussion.

Bearing in mind the concerns that proponents of reform have regarding workplace pension plans, it is not surprising that they all propose pension delivery platforms other than single employers. Proponents of reform spend little time discussing the future role of workplace pensions, even though most of the reform proposals would still require people with moderate to high earnings to supplement postreform incomes, with either workplace pension income or individual savings, in order to maintain their standard of living in retirement. Because most individual employers are not suitable platforms for the delivery of pension benefits, it would have been helpful if proponents of reform had paid more attention to the role and structure of workplace pensions in a postreform environment.

A final and important common element in the proposals is that they all assume that new benefits will be fully prefunded. This important aspect of the proposals receives little discussion and seems largely to be taken for granted. Prefunding may seem obvious for new initiatives with a strong DC element.

In the case of CPP expansion, it may be that the provision adopted in the late 1990s that requires prefunding of benefit improvements was simply accepted by proponents of expansion and needed no discussion. There are good reasons to prefund benefits: lower contributions than on a PAYGO basis, improved intergenerational equity, and so on. Full prefunding, however, may unnecessarily constrain the phasing-in of an expansion. If the expansion, like the CPP’s original introduction (when individuals already in the workforce received full benefits without contributing for a full career), were to provide improved benefits for periods of employment both before and after the new benefits are introduced, then full prefunding would require additional contributions for a time from workers already in the labour force to cover the cost of those improved benefits for earlier periods of employment. More importantly, for reasons discussed below in connection with benefit design, prefunding is likely to introduce some degree of contribution rate volatility. A volatile CPP contribution rate could have perverse employment effects.28

In addition, new fund governance and management issues will arise with an expanded CPP fund. The full liability for existing CPP benefits promised as of the end of 2006 was estimated by the Chief Actuary to be in excess of $700 billion, of which approximately 15 percent, or $105 billion, was funded and under the management of the CPPIB. Adding another $700 billion to the current assets under management of the CPPIB, as a fully mature doubling of all CPP benefits for existing participants in the plan would require, would create new challenges. For example, it might be difficult to maintain the existing portion of CPPIB assets in Canadian securities, and it might take time to find appropriate investment opportunities to permit the scalingup of the private investment activities of the CPPIB.

Even though proponents of reform spent little time explaining their support for full funding, it was often associated with intergenerational fairness: each generation pays its own way. Regardless of the structure of the population, PAYGO schemes in which benefits are phased in quickly are often cited as something to be avoided, as they eventually result in increases in the contribution rate with no corresponding increase in benefits, as larger portions of the population become eligible for benefits. PAYGO contributions also get pushed up if the elderly portion of the population is increasing, as is now the case in Canada and most countries. The early beneficiaries under these schemes receive significant net transfers from younger and future generations. Elsewhere I have questioned the importance that should be attached to this feature of PAYGO schemes (Baldwin 1998). But issues of intergenerational fairness are not limited to PAYGO pension plans. Prefunded plans can give rise to issues of intergenerational fairness even if new benefits are fully funded and phased in over long periods.29

The incomes generated by both DC and prefunded DB plans are sensitive to the gap between investment returns and wage growth. All other things being equal, investment returns that are significantly higher than wage growth will lower the required DB contributions and increase DC incomes. But the relationship between investment returns and wage growth is not stable through time.30 As a result, some generations will be more fully rewarded for their pension contributions (savings) than others.

Then, in the case of DB plans, one of the other key variables affecting required contributions is mortality, which seems to be improving continuously with no tendency to revert to a mean value. People are living longer. As a result, if a constant age of retirement is assumed, every age cohort that passes through a DB plan gets a more valuable benefit than previous cohorts. Given that mortality does not revert to a mean, it is not possible to stabilize both a benefit and a contribution rate, nor can different cohorts insure each other equitably. Stabilizing the relationship between contributions and benefits will require some mix of higher contributions, lower benefit amounts and later retirement.

Prefunding does not resolve all issues of intergenerational equity. There is ample room for discussion of how the concept of intergenerational equity should be put into effect. Policymakers would do well to use this room to enhance the long-term benefits to society of any reforms introduced.

An important difference among the reform proposals is the level of earnings that would be covered by new initiatives, including CPP expansion. Most advocates of CPP expansion have proposed increasing CPP benefits using as a base the first dollar of annual earnings in excess of the current YBE; the CLC would double the YBE. The expansion proposals differ, however, in the upper end of the earnings range to which higher benefits would apply. The CLC proposal would provide increased benefits on earnings up to the current YMPE, roughly equal to the average wage and salary ($47,200 in 2010). The BC discussion paper contemplates the possibility of raising the YMPE to twice the average wage and salary, and the FSNA proposal would raise it to roughly two and one-half the average wage and salary.

The CSPP proposal has a low end of covered earnings for its auto-enrolment of $30,000, which is more than half the average wage and salary. The Alberta-BC panel recommends that there be a lower end to the level of earnings for auto-enrolment in the new provincial plan (i.e., auto-enrolment would not apply to the first X dollars earned), but it does not give a specific figure. The upper limit for auto-enrolment that Ambachtsheer recommends for the CSPP and the Alberta-BC panel recommends for its proposed plan would be the limit set in the Income Tax Act on earnings ($122,222 in 2010) to which the 18 percent RRSP contribution rule can be applied. The Nova Scotia panel was not specific on the earnings its proposed provincial plan would cover.

Proposals that would exempt low levels of earnings from new initiatives generally do so on the grounds that the redistributive nature of the first pillar of Canada’s retirement income system means that people with earnings up to half the average wage and salary are fully replacing their preretirement earnings through OAS, the GIS and current benefits under the CPP/QPP. Thus, their lifetime well-being is likely to be reduced by the contributions required by a mandatory CPP expansion.

For these people, the sacrifice in preretirement living standards is unlikely to be fully rewarded in retirement. The additional benefits that might arise from CPP/QPP expansion or other forms of preretirement savings give rise to lower benefits from the GIS by 50 cents on the dollar. To be sure, people are not worse off in retirement in an absolute sense as a result of the GIS tax-back, but their net gain is diminished. That is to say, they might be better off over their lifetime if they had more disposable income and consumption before rather than after retirement.31

The advocates of exempting a low level of earnings from new initiatives generally also assume that, if minimum incomes provided by OAS and the GIS are deemed to be too low, increased benefits from those programs will address the problem.

Some might argue, however, that reducing the use of the GIS is desirable from both fiscal and social policy points of view. From a fiscal perspective, expenditures are moved off budgetary accounts, and from a social policy perspective, the possible stigma of applying for the GIS is removed. (With respect to concerns about stigma, it is worth noting that the take-up rate for the GIS has grown in recent years to about 86 percent of eligible individuals, according to Luong 2009.) A case for including lower earnings might also be made on the grounds that low earnings in one year may not be indicative of low lifetime earnings levels, and therefore may be only loosely correlated with receiving an adequate retirement income in the future from pillars 1 and 2 as they currently exist.

The reform proposals also differ in terms of the upper end of the range of earnings to which they might apply. The CLC proposal accepts the existing level of the YMPE (approximately equal to the average wage and salary) as the upper limit of earnings covered by the higher CPP benefit rate. The FSNA proposal, the options proposed for consideration by the government of British Columbia, and the CSPP proposal all envisage higher levels of covered earnings. Proposals to increase levels of covered earnings reflect a sense that the earnings range where people are most vulnerable to declining living standards in retirement extends upward beyond the middle range of earnings.

In context, it is also worth noting an important research finding of Statistics Canada analyst Kevin Moore (2009a, 2009b). Using Statistics Canada’s LifePaths model,32 Moore has found that, while a stylized characterization of Canada’s retirement income system suggests that the CPP/QPP will generate approximately 25 percent of preretirement earnings for someone with average lifetime wages and salaries, in fact, the modal replacement rate is only 15 to 20 percent. One reason for this is that wages and salaries do not follow a steady path over the years in relation to the average wage and salary. Years when an individual’s wages and salaries rise above the YMPE give rise to noncontributory earnings, and the CPP/QPP offers no scope for making extra contributions to compensate for this when earnings fall below the YMPE. The periods of earnings higher than the YMPE represent an opportunity to contribute to the CPP that is permanently lost.

The stylized CPP/QPP replacement rate of 25 percent of preretirement earnings for people with average lifetime earnings is the exception rather than the rule. This problem is accentuated if the maximum level of pensionable earnings for a plan like the CPP/QPP is at a relatively low level, where a fairly high degree of variation in annual earnings around the threshold can be expected (as the YMPE is raised to higher multiples of the average wage and salary, the probability of a given individual having annual earnings that exceed the YMPE decreases). According to the OECD (2005), the YMPE of the CPP/QPP is the lowest of similar measures in programs among OECD countries.33 Wolfson (forthcoming) notes that later entry into continuous paid employment also lowers the CPP replacement rate for younger cohorts below the stylized 25 percent.

Among the proposals for reform that I have discussed, the Alberta-BC panel and CSPP proposals are decidedly DC in their orientation, while a virtue cited for the various proposals for CPP expansion is that they are DB plans. These general characterizations of the proposals deserve further elaboration.

The Alberta-BC and CSPP proposals try to limit some of the key risks in DC plans. Both plans limit the scope for investment choice by plan members in an effort to reduce the difficulties that many people have in making appropriate investment choices, for too much choice may be immobilizing. Both contemplate the use of life-cycle funds34 as default options in an attempt to scale back investment risk as retirement age approaches. This type of fund is an antidote to the tendency to adopt an asset allocation early on in life and to make no change to it. They also anticipate making annuity purchases over a period of years before retirement, with a view to reducing the interest rate risk at the moment of retirement (annuity prices are highly sensitive to interest rates and purchasing annuities over a period of years spreads the risk over time).35

These modifications to the traditional DC model attenuate some of the risks associated with these plans. Nonetheless, the proposals still fix the rate of contribution while leaving the benefits to be provided and/or the retirement ages uncertain. However, this uncertainty applies only to a tranche of the retirement income system. Moderate earners will still be getting a significant portion of their retirement incomes from OAS and CPP, which are largely DB. Moreover, while it is understandable that in the wake of the financial market meltdown of 2008 and 2009, people are preoccupied with the downside of investment risk, such risk does have its advantages. Thus, even if a DC and DB plan are designed to produce comparable benefits over time, there will be periods when each outperforms the other.

The proponents of CPP expansion generally cite the CPP’s defined benefits as one of its attractive features. But the 1997 changes to the plan gave its basic benefits (i.e., the benefits in place in 1997) an element of target-benefit design. If the Chief Actuary establishes a steady state contribution rate36 of 10 percent or higher in a triennial review of the plan, a set of default provisions are triggered, unless the federal and provincial finance ministers agree to accept the higher contribution rate. One default provision is the suspension of pension indexing until the steady state contribution rate drops below 10 percent. The target-benefit nature of the CPP is also reflected in the nontrivial reduction in CPP benefits made as part of the 1997 changes; indeed, the entire reform exercise was triggered in large part by the refusal of some provinces to endorse a CPP contribution rate in excess of 10 percent.

The 1997 rule changes also require any increase in CPP benefits to be fully funded and financially accounted for separately from the basic benefits in place at the time. New benefits are to be valued every three years, and any underfunding of new benefits will give rise to amortization payments.

The Chief Actuary has estimated the current service costs of the CPP benefits now in place as 5.9 percent (OCA 2007a). (The current service cost is the cost of newly accruing benefits on a fully funded basis. The additional 4 percent currently being contributed by workers and employers covers “legacy costs” — the cost of benefits that have been accrued in the past but were not fully funded at the time.) Proponents of CPP expansion have relied on this estimate of current service costs in discussing the contribution rates their proposals require.37 In arriving at this estimate, the Chief Actuary has assumed that funds invested in support of CPP benefits will have an annual rate of return net of inflation of 4.2 percent. This assumption is reasonable, but this rate can be achieved only if the invested funds have a significant equity component, and this implies significant volatility in returns and, from time to time, actuarial deficits and temporary contribution rate increases.38 Thus, the actual contribution rate required by doubling the CPP benefit rate is likely to rise above and fall below 5.9 percent over time.

The fact that basic CPP benefits and new benefits are financed on different bases has an interesting consequence for CPP contributions. Basic benefits are likely to have a more stable contribution rate than new benefits. This stems from the target nature and the largely PAYGO financing of the basic benefits. In relation to the total liability of the basic benefits, the equity holdings of the CPPIB are minor — about 9 percent, rising to about 20 percent in the years ahead, assuming that the CPPIB continues to hold about 60 percent of its portfolio in equities.39 However, in a fully funded CPP valued in the manner that is common for workplace pension plans, the only way to achieve a comparable low level of volatility in the contribution rate would be to minimize equity holdings in the CPPIB, which would increase the current service cost substantially. But one might argue that, because the CPP has virtually no solvency risk, it should be valued in a different manner that takes account of future benefit accruals on the liability side of the balance sheet and the present value of future contributions on the asset side. If a balance sheet prepared in this manner is used to determine the funded status of the plan, it is likely that contribution rate volatility would be minimized by the natural hedging of the plan’s liabilities (assuming that future benefit accruals and contributions are valued in a consistent manner). A balance sheet prepared in this manner would be consistent with the method used to establish the steady state contribution rate (see OCA 2010).

The main proposals for pension reform I discuss here are modified versions of pure DC and pure DB plans. This fact hints at an important reality: the proposals for pension reform now in the public domain barely scratch the surface of the full range of available choice. Generally speaking, we can think of prefunded pension schemes holding assets imperfectly matched to their pattern of future liabilities as lying along a spectrum (see the appendix). Pure DB plans offering complete certainty of benefits and uncertainty of contributions40 are at one end, and pure DC plans offering certainty of contributions and uncertain benefits (or uncertain retirement age) occupy the other end. Along this spectrum are any number of plan designs that mix the certainty and uncertainty of benefits and contributions — sometimes in unplanned ways.

The choice of benefit design could be constrained by the way in which the participation issue is resolved. In practice, DB designs rely more heavily on compulsory participation than do DC designs. In 2008, 90 percent of the members of workplace DB plans in Canada belonged to plans with compulsory membership, while 60 percent of DC plan members were in compulsory plans.41

The reform options I discuss in this study were chosen specifically because they are not purely voluntary in their method of addressing the declining coverage of workplace pension plans and related problems. Nevertheless, they vary in the degree of compulsion they involve and how they would interact with existing workplace pension plans.

The proposals for CPP expansion do not specifically address the question of compulsion. But, by not proposing any alternative to the CPP’s current mandatory coverage of employed and selfemployed workers, proponents implicitly accept this feature of the CPP. In cases where workplace pension plans now provide benefits that the CPP would provide under the reform proposals, presumably these plans’ benefits would be wound down over time. CPP benefits would displace the workplace benefits. This is an intended consequence of the CLC proposal, reflecting the CLC’s concerns over the adequacy and security of workplace pension benefits.42

The proposals of the Alberta-BC panel and the Nova Scotia panel and Ambachtsheer’s CSPP differ from the proposals to expand the CPP in their degree of compulsion, as they contemplate automatic enrolment with the right to opt out by employees, by employers, or by both employees and employers. They generally limit automatic enrolment to employees and exclude the self-employed from this provision. Moreover, the Alberta-BC panel and Nova Scotia panel proposals are viewed as wrapping around existing arrangements rather than displacing them. The same might be said of the CSPP proposal, except that it envisages substantial change in the way workplace pensions are delivered and would, as a consequence, replace many existing plans with new plans and new pension-delivery mechanisms. The differences among the proposals in degree of compulsion and relationship to existing workplace pension plans do not stem from the fundamental mechanisms underlying each proposal. For instance, there is enough flexibility in the CPP mechanism that a second tier of the CPP could function in the same manner as the provincial and CSPP proposals with respect to compulsion and the relationship with existing workplace pensions. On the other side of the coin, plans with the design features of the Alberta-BC panel and Nova Scotia panel plans and of the CSPP could be made compulsory for all employees and for the self-employed.

There is a strong case to be made for a compulsory plan as the most certain solution to the coverage problem. Such a plan may also protect against future claims on the federal budget in the form of GIS payments. Compulsory enrolment will also help with adverse selection problems.43

However, compulsory measures should be held to a higher standard than auto-enrolment and voluntary measures. Plan designers should ensure that new compulsory measures address real, accurately quantified needs, and that their effect is relatively homogeneous on everyone who is required to participate. (That is, the compulsory measures must effectively address well-identified problems.) An element that makes the design of reform initiatives difficult at this point in Canadian history is that current workplace pension arrangements are so heterogeneous in terms of their effectiveness. While many Canadians are participating in very effective workplace pension arrangements, many are not. Finding a reform path that is reasonable for both is a greater challenge than if no pension plans existed or if the plans in place were all dysfunctional.44

The organization of any reform options and the cost of implementing them will depend on how a number of the foregoing questions are resolved. Although none of the proposals make detailed comments on their implementation, there is still much to note on this matter, especially in that low administrative cost is one of the requirements that any reform proposal should fulfill.

Most of these proposals, as they are currently being discussed, have a bias in favour of a national organizational structure. The provincial focus in the Alberta-BC panel and Nova Scotia panel recommendations may reflect their mandate as much as their authors’ preference. The more recent paper released by the government of British Columbia tends to look at the provincial plan as a second-best solution that comes into play only if there is no national initiative. The preference for a national initiative stems in part from the greater scope it offers for achieving economies of scale and lower administrative costs. It also stems from a desire to facilitate labour-market mobility across the country. The Alberta-BC panel also worried that a compulsory provincial program would cause problems for the competitiveness of provincial industries. This concern assumes that employer pension contributions would cause a net increase in labour costs. (The validity of this concern is addressed in endnote 28.)

Lowering administrative costs in the provision of retirement income has been an important theme in the writing of Ambachtsheer for many years (see Ambachtsheer 2007, and also Jog 2009). It is also an important consideration in the Alberta-BC panel report. Proposals from these sources make it clear that existing organizational structures should be drawn on as fully as possible in implementing their recommendations. Thus, the Alberta-BC panel notes the desirability of getting the cooperation of the Canada Revenue Agency in collecting contributions for its provincial plan. Ambachtsheer sees a role for the CPPIB in investing CSPP contributions.

While all the proposals aspire to low administrative costs, especially compared to what is currently available to individuals saving in the retail market, the proposals that would build on the existing benefit structure of the CPP are likely to achieve the greatest success in this area. Proponents of reforms with a strong DC element generally understand that both start-up and ongoing costs would likely be greater than the costs of a larger CPP as currently designed. As noted previously, an expanded CPP could depart from its current design by, for example, using a different definition of covered earnings and having a stronger DC component. If there is an expansion of the CPP, its designers will need to understand how stretching CPP designs in different directions will affect administrative costs.

Proponents of CPP expansion have not commented on the governance and organization of the CPP or the CPPIB. They seem to accept these features, including the arm’s-length relationship between the CPPIB and the government. One concern that has been raised is whether CPPIB management of individual accounts might dilute the CPPIB’s purpose of investing in support of existing CPP benefits. Another concern may be that investing through the CPPIB implies a closer relationship with government than would be the case if the government’s role were limited to collecting contributions and remitting them to private for-profit or not-for-profit investment companies (e.g., large pension fund managers like the Ontario Teachers’ Pension Plan and the BC Investment Management Corporation).

There is a great deal of scope for mixing and matching public and private functions in the implementation of pension reform options. An important objective of the reforms discussed in this study is to provide pensions at a low administrative cost. This objective should be one of the criteria by which reforms are judged.

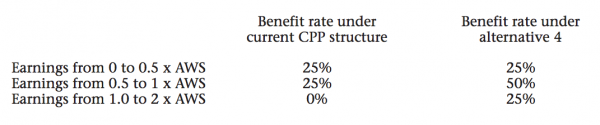

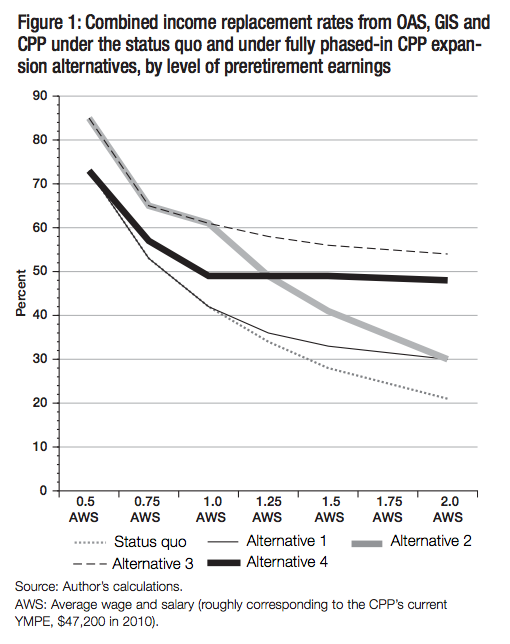

This section presents a brief, stylized assessment of the impact of CPP reform proposals. I have designed the assessment to provide insight into how a variety of changes made to the CPP might affect the earnings replacement rate from the first pillar (OAS and GIS) and second pillar (CPP/QPP). The CPP changes that I consider are the following:45

The consequences of these CPP reforms are compared to the status quo at different levels of earnings, ranging from half the AWS to twice the AWS. Some reform proposals would extend the YMPE beyond twice the AWS. The impact of these proposals can be thought of in terms of a continual linear increase in the benefits in alternatives 1, 3 and 4 beyond twice the AWS (see figure 1).

The dollar values used in this assessment are 2008 values.

Outcomes are presented in terms of gross (pretax) replacement rates for single individuals who begin to receive their CPP retirement benefits at age 65. The use of the gross rates rather than after-tax rates understates the improvement in replacement rates, as no account is taken of the impact of reform on preretirement disposable income. Reforms of the sort assessed here are expected to require additional CPP contributions of roughly 6 percent of earnings (on average over the long term), divided between employers and employees, in order to produce an additional replacement rate of 25 percent.46 The self-employed will bear both shares. The employer contributions will show up as a lower level of wages and salaries than otherwise would be achieved, and the employee share as a deduction from wages and salaries.47 Ignoring income taxes means that marginal effects at higher levels of earnings are overstated relative to the impacts at lower levels of earnings. The interaction between the GIS and changes to the CPP is captured in this assessment. (Horner 2009 estimates that a gross replacement rate of 60 percent equals a consumption replacement rate between 90 and 100 percent.)

Assessments of the sort presented here are quite common in pension discourse, but some of the limitations of the stylized approach should be noted. First, the earnings levels are dealt with as if people’s preretirement earnings maintain a constant relationship with the average wage and salary. As was noted above, this is not the case, although this problem diminishes as the YMPE is increased. Then, in these calculations, the earnings that form the denominator for the replacement rate calculation are those immediately prior to retirement. However, because of the formula used to adjust career earnings in the CPP, the actual CPP replacement rate will be less than 25 percent.48 Using the 2008 values in the calculations yields an “unreduced” replacement rate, at age 65, of 23.6 percent. This replacement rate was used in all calculations here.

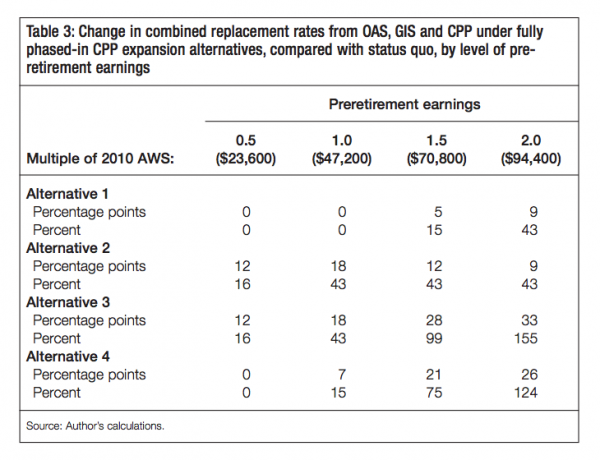

Figure 1 illustrates the replacement rates generated by the first and second pillars at various levels of earnings, assuming the status quo with respect to the benefits provided by the two pillars and then assuming various alternatives for the CPP. Table 3 illustrates the marginal impact in terms of both percentage point changes in the replacement rate (i.e., the replacement rate after reform minus the replacement rate before reform) and the percent change in the replacement rate (i.e., the change in the replacement rate divided by the replacement rate prior to reform). The CPP benefit changes are assumed to be fully phased in.

The pattern of change in retirement incomes that would result from fully phased-in increases in CPP benefits is not surprising. Alternative 1, which lifts the YMPE without changing the benefit rate, delivers all of its impact above the current YMPE without changing benefits paid up to the YMPE. By contrast, alternative 2, which doubles the benefit rate to 50 percent with no change in the YMPE, delivers significant benefit increases on earnings up to the current YMPE. However, the marginal benefit is attenuated at low earnings by the offsetting reduction in GIS benefits. Thus, the maximum percentage point increase in firstand second-pillar benefits comes at the AWS, and the maximum percent increase comes at and above the AWS. Alternatives 1 and 2 are equivalent at twice the AWS.