Ottawa doit intervenir plus vigoureusement pour assurer qu'un maximum de Canadiens tirent profit de la richesse de nos ressources naturelles

Robin Boadway, Serge Coulombe and Jean-François Tremblay

Acquis au lendemain de la Seconde Guerre mondiale, le titre incontesté de superpuissance économique, financière et militaire des États-Unis semblait inattaquable il y a encore 10 ans, fondé qu’il était sur la force agissante des valeurs typiquement américaines d’individualisme, de libre entreprise et d’ouverture aux plus brillants esprits du monde. Mais depuis quelques années déferle sur ce pays une vague d’angoisse dont témoignent le nombre grandissant d’Américains pour qui la gloire de leur nation est chose du passé et la méfiance sans précédent que leur inspire le gouvernement fédéral.

Les sources de cette inquiétude face à l’avenir des États-Unis sont à la fois internationales et nationales. L’ascension météorique de la Chine et autres pays d’Asie menace tout d’abord leur domination économique en provoquant la délocalisation de la production manufacturière et en érodant la compétitivité des entreprises. Puis au pays même, les contrecoups de la crise financière et d’une grave récession se prolongent bien au-delà de ce qu’on avait vu lors des précédents ralentissements, tandis que la paralysie du système politique bloque toute réponse à l’urgent besoin de freiner l’accroissement vertigineux de la dette publique et, surtout, de réduire une inégalité croissante des revenus qui menace d’effondrement les deux piliers du rêve américain que sont l’égalité des chances et l’accès au mode de vie de la classe moyenne.

Dans l’essai Horizons politiques 2011 de l’IRPP, le réputé chercheur canadien Thomas J. Courchene retrace les facteurs expliquant la montée puis l’éventuel déclin du rêve américain et de la prédominance du pays sur l’échiquier mondial. Et il observe que les éléments du credo américain qui avaient favorisé la réussite économique du pays dans les décennies suivant la Seconde Guerre mondiale contenaient peut-être en germe les conditions d’une régression potentiellement amorcée dans les années 1980. Le « modèle américain » de capitalisme individualiste (partagé à différents degrés par d’autres nations anglophones) est en effet l’héritier naturel du régime de common law britannique, qui privilégie la limitation des pouvoirs de l’État et la défense des droits individuels, contrairement au « modèle européen » de capitalisme communautarien (aussi adopté par le Japon) qui puise ses racines au régime de droit civil français, selon lequel l’État doit s’employer plutôt à rassembler la nation autour de vastes objectifs sociétaux.

Le capitalisme individualiste a très bien servi les États-Unis des années 1950 au début des années 1980, soit pendant une ère « fordienne » de production de masse qui a entraîné une chute des prix, et permis un accroissement des revenus et un essor jamais vu de la consommation. Car à l’inverse d’une Europe et d’un Japon en ruines, note M. Courchene, l’économie des États-Unis s’était tirée indemne de la Seconde Guerre mondiale, si bien que les travailleurs américains ont pu accéder à un abondant capital physique et financier tout simplement inexistant dans d’autres pays et se sont par conséquent révélés plus productifs. Ce qui a permis à d’innombrables travailleurs, même sans qualifications, de jouir du mode de vie de la classe moyenne. À la même époque, des universités de renommée internationale et une immigration qualifiée assuraient au pays sa réputation de chef de file en matière d’innovation.

Puis, sous l’impulsion des technologies de l’information et d’Internet, l’économie mondiale a entamé au début des années 1980 une transformation radicale qui a inauguré l’ère de l’informatique et des réseaux, ceux-ci remplaçant bientôt la production de masse en tant que forme prédominante d’organisation socioéconomique. Une organisation qui, par opposition au capital physique, privilégie les compétences et le savoir, devenus la pierre angulaire de toute prospérité, avec d’évidentes répercussions sur les travailleurs non qualifiés.

Cette transformation économique dictée par les technologies s’est accompagnée d’une mondialisation capitaliste sans entraves, facilitée par les politiques de Ronald Reagan et de Margaret Thatcher en matière de déréglementation, de privatisation, de réductions d’impôt massives et d’affaiblissement des programmes sociaux.

Or les conséquences économiques de ce changement de cap n’ont pas toutes été favorables aux États-Unis. Menée sans contraintes, la mondialisation capitaliste a provoqué une délocalisation considérable de la production intérieure, restreignant d’autant plus la possibilité des travailleurs peu qualifiés d’accéder au rêve américain.

Ces répercussions ont particulièrement aggravé le problème de l’inégalité des revenus, celle-ci s’étant accrue de façon spectaculaire depuis 30 ans. Bien que la dimension individualiste du credo américain mette l’accent sur l’égalité des chances et fasse de l’inégalité des revenus une résultante naturelle des différences d’aptitudes et d’effort de travail, l’ère de l’informatique a porté l’écart qui s’ensuit à des sommets invraisemblables : le salaire d’un PDG par rapport à celui d’un travailleur ordinaire a été multiplié par six depuis le début des années 1980 et est aujourd’hui au moins 20 fois plus élevé que dans les autres pays industrialisés.

On doit prendre très au sérieux cette forte inégalité des revenus, estime M. Courchene, car il en découle de nombreux problèmes de santé et de société. Les études montrent en effet que les pays de capitalisme individualiste sont aux prises avec de plus graves inégalités et de pires problèmes sociaux (toxicomanie, criminalité, grossesses précoces, etc.) que les pays de capitalisme communautarien. Chez les premiers, les minces possibilités d’ascension sociale sont sans doute la donnée la plus frappante, qui font en sorte que les enfants de foyers à faible revenu ont tendance à devenir des adultes à faible revenu. De fait, la mobilité sociale a sensiblement reculé aux États-Unis depuis 1980, un recul qui devrait être perçu comme un signal d’alarme : le rêve américain serait-il en train de tourner au mirage ?

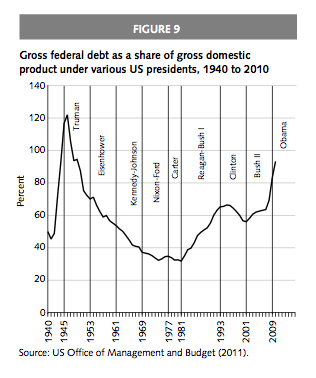

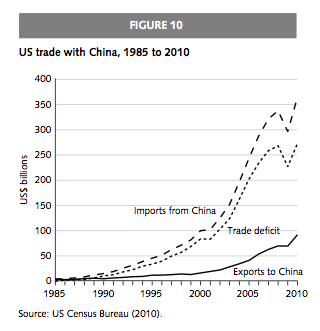

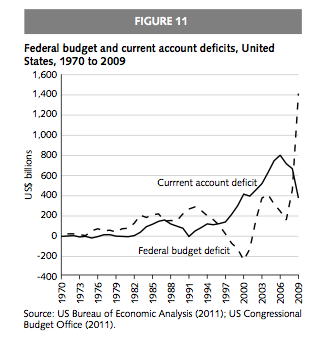

À ces craintes s’ajoute une série de calamités économiques et financières dont la moindre n’est pas la gigantesque dette publique, qui avoisine aujourd’hui 100 p. 100 du PIB du pays. Comme l’explique M. Courchene, les États-Unis ont ce privilège de pouvoir emprunter à l’étranger dans leur propre devise, ce qui leur donne une capacité d’emprunt à peu près illimitée. Or l’ampleur de leur dette publique extérieure, détenue surtout par la Chine, a provoqué un « choc de titans ». C’est ainsi que l’appétit américain pour les exportations chinoises a considérablement renforcé le pouvoir économique de la Chine. Parallèlement, celle-ci est devenue, avec 2,85 billions de dollars en bons du Trésor, un emprunteur de dernier recours pour financer la dette américaine. Et dans cette relation bilatérale déjà difficile, les États-Unis perdent leur ascendant à mesure que la Chine devient moins dépendante du marché américain, alors même qu’ils continuent de compter sur elle pour financer leur dette grandissante.

Que doivent alors faire les Américains ? Sur la scène internationale, toute croissance durable des États-Unis nécessite des règles du jeu équitables. Ils doivent donc s’assurer que la Chine et les autres membres de l’OMC se conforment aux règlements au lieu de céder le pas lorsque ces pays les enfreignent ouvertement (en exigeant par exemple que le partage de la propriété intellectuelle soit une condition d’accès au marché, une demande trop souvent « dictée » par la Chine). Ils doivent aussi reconnaître que les biens chinois importés sont souvent produits selon des normes du travail et environnementales qu’eux-mêmes ne toléreraient pas, d’autant plus que cela entraîne de nouvelles délocalisations et compromet des décennies de gains durement acquis par les travailleurs américains.

De plus, ils doivent mettre à niveau leur économie intérieure en misant sur les compétences et les innovations de l’ère de l’information. Compte tenu des millions de nouveaux diplômés en sciences et en génie d’origine chinoise et indienne, et le fait que pas moins de 50 p. 100 des diplômes américains en génie sont accordés à des étrangers (dont beaucoup rentrent dans leur pays à la fin de leurs études), les États-Unis ne font plus figure de chef de file incontesté de l’innovation. La décision qu’ils ont prise après le 11 septembre de resserrer les règles permettant aux étudiants étrangers de rester aux États-Unis au terme de leurs études est à cet égard contre-productive, tout en dérogeant à la tradition américaine d’accueillir les plus brillants esprits. Mais pour récolter les fruits de l’ère de l’information, il leur est plus urgent encore de renforcer les compétences de leur main-d’oeuvre, notamment des travailleurs hispaniques, un segment de population dont le taux de décrochage au secondaire est trois fois supérieur à celui des Blancs et presque le double de celui des Noirs.

S’attaquer à l’inégalité des revenus et à ses conséquences sociales est d’autant plus nécessaire qu’elles nuisent clairement à cette égalité des chances implicitement inscrite dans le rêve américain. Et le Canada peut offrir à cette fin de précieuses leçons, note ici M. Courchene. Pays de capitalisme individualiste, il mise toutefois sur des programmes ciblés sur le revenu pour atténuer les effets indésirables de l’inégalité des revenus, sans incidence majeure sur le Trésor public. Il cite en exemple la Prestation fiscale canadienne pour enfants, qui partage plusieurs des caractéristiques de l’impôt négatif sur le revenu préconisé par de nombreux économistes conservateurs américains.

Sur le plan financier, M. Courchene estime que l’ampleur de l’écart budgétaire du gouvernement fédéral américain, jumelé aux pressions démographiques à venir sur les dépenses de la sécurité sociale et du programme Medicare, impose aux États-Unis d’intégrer l’accroissement des revenus à toute démarche crédible d’élimination du déficit. Et le moyen le plus efficace d’y parvenir, soutient-il, consiste à mettre en oeuvre une taxe à la valeur ajoutée (TVA) sur la consommation. Une TVA a un effet neutre sur les importations et les exportations et ne diminuerait donc pas l’avantage concurrentiel des exportateurs américains. De plus, contrairement à l’impôt sur le revenu, elle ne décourage pas l’épargne et l’investissement. M. Courchene reconnaît que l’instauration d’une TVA, souvent perçue comme « une machine à faire de l’argent » qui risque de faire gonfler la taille du gouvernement, susciterait une vive opposition politique. Mais il note que le Canada a utilisé une partie des recettes de sa TVA pour réduire l’impôt sur le revenu des sociétés et des particuliers et renforcer du même coup la compétitivité du pays.

Thomas Courchene pose certes un diagnostic sévère, mais son pronostic demeure optimiste quant à la capacité des États-Unis de miser sur les forces qui ont assuré leur prédominance dans la période d’après-guerre afin de réinventer un leadership économique mondial adapté au XXIe siècle. Au lieu de chercher à dominer sur le plan économique, en cette ère des réseaux il leur faudra plutôt utiliser leur atout de « pays le mieux connecté » pour jouer un rôle clé dans un monde de plus en plus interdépendant. Les États-Unis doivent ainsi sortir de leur impasse politique et reconnaître que l’égalité des chances fondée sur les compétences est indispensable à leur réinvention.

Since its creation in 1972, the IRPP’s mission has been to improve public policy decisions by producing analysis and sparking debate on the emerging issues facing Canadians and their governments. On the eve of our 40th anniversary, we are pleased to launch the IRPP Policy Horizons Essay, whose purpose is to look well beyond day-to-day challenges and consider the larger economic, social and cultural shifts on the horizon that will shape Canadian policy and decision-making in the years to come.

For this inaugural essay, we are pleased to have Thomas J. Courchene, JarislowskyDeutsch Professor of Economic and Financial Policy at Queen’s University and Senior Scholar at the IRPP, shed light on the uncertain economic prospects of the United States.

Given that the United States is the destination of more than two-thirds of Canada’s exports and nearly 20 percent of its total economic production, a flagging American economy has obvious and enormous implications for Canada. But, more broadly, a struggling America could jeopardize the stability of the international geopolitical order it helped build after the Second World War, and the economic growth and support for democratic values and individual rights that accompanied it.

The Policy Horizons Essay is intended to bring a multidimensional perspective to complex issues. To this end, future contributors will, like Thomas Courchene, have long and distinguished careers in analyzing Canadian public policy and an exceptional ability to apply rigorous analysis and contribute fresh thinking and new insights to difficult policy challenges, which is at the heart of the IRPP’s mission.

Graham Fox

President

Institute for Research on Public Policy

American exceptionalism seemed unassailable as the world welcomed the third millennium. With its greenback serving as the world’s currency, America was the uncontested global superpower – economically, financially, militarily and, to Americans at least, morally. Among the keys to America’s ability to scale what Yergin and Stanislaw (2002) refer to as the “commanding heights” of the global economy were its individualist ethic, its liberal approach to markets, its openness to the best and the brightest from across the globe and, above all, its inherent dynamism and penchant for innovation.

Yet, from the vantage point of 2011, America’s status as the sole global superpower seems contestable, and in many circles the notion of America declinism is making headway.1 The sources of this concern about America’s future are partly external, stemming less from a decline in the United States than from the spectacular rise of the emerging (and largely Asian) economies – first Japan, then the tigers (Singapore, Hong Kong, Taiwan and South Korea) and now China, India, Indonesia and Brazil. But much is also internal to America, such as the debt and deficit overhang, the unsustainable Social Security entitlements as the boomers become golden agers, the erosion of the middle class and the growing political polarization.

Since 2007 these concerns have become much more acute: the financial collapse, the mortgage debacle, the recession, near-double-digit unemployment and the advent of trilliondollar deficits have given rise to broader societal concern over America’s future. A recent national telephone poll showed that 47 percent of America’s likely voters believed the “nation’s best days are in the past” (Friedman 2010). In the context of a Foreign Affairs article that offers one of the more optimistic visions of America’s future, Joseph Nye nonetheless reminds his readers that there are some storm clouds on the horizon:

Another cause for concern is the decline of public confidence in government institutions. In 2010, a poll by the Pew Research Center found that 61 percent of respondents thought that the United States was in decline. And only 19 percent trusted the government to do what is right most of the time. In 1964, by contrast, three quarters of the American public said they trusted the federal government to do the right thing most of the time. (2010, 8)

This sharp decline of trust in government amid deep-seated angst about the future of the country suggests America’s current predicament is structural in nature and transcends the recent deep recession – indeed a far cry from the commanding heights.

In this essay I will highlight the features and forces that led to the global supremacy of the US in the early post-Second World War period, then assess the constellation of philosophical and policy forces that are now undermining key aspects of American exceptionalism. To conclude I will outline some pathways toward a twenty-first-century version of exceptionalism or, in the words of the title, toward rekindling the American Dream: the enduring belief that individual initiative and hard work will deliver material progress for all.

Why is a Canadian undertaking this exercise? Canada and Canadians obviously have a vested interest in the fate of our southern neighbour. The United States is by far our biggest trading partner and, despite globalization of trade and the increasing thirst of emerging markets for the oil and other natural resources that we are fortunate enough to possess, it will remain a fundamental determinant of Canada’s economic prospects. Moreover, American global leadership gives Canada a privileged position in international affairs, allowing us to “punch above our weight” and to advance issues of mutual interest. Beyond these pragmatic reasons, the US has indeed been a “shining city on the hill.” Under its economic and political leadership, the postwar period has seen unprecedented income growth across the globe, the creation of international governing institutions, a doubling of the number of democratic governments, the reduction of poverty and the successful management of the Cold War, to name just a few accomplishments. And while America presumably acts in its own strategic interests, within this framework the US has revealed itself to be a most generous nation and a defender of rights and freedoms. For these and other reasons, what underlies the often critical assessment of US policies in this essay is an earnest desire for the US to regain its stature.

The essay begins by taking a step back to explore some features of the evolution of nations and societies, highlighting key differences between civil-law and common-law regimes, as reflected in continental European communitarian capitalism and Anglo-American individualist capitalism. The analysis then focuses on postwar America’s “Fordism” and the heyday of the American Dream, which held sway for the better part of half a century. What followed during the 1980s was a transition to a new model of capitalism with its liberalized markets, and the emergence of a new technology centred on the Internet and related networks in the informatics era. The conclusion derived from this analysis is that the US has carried individualist capitalism very far in the direction of winner-take-all capitalism, a consequence of which is a drift toward greater societal inequality. While inequality is traditionally not a concern of the American ethos, I argue that it has reached a point where it is threatening equality of opportunity and the middle class, the core pillars of the American Dream.

From the Declaration of Independence: “We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable Rights, that among these are Life, Liberty and the Pursuit of Happiness.” Just as “Liberté, égalité, fraternité” is France’s societal maxim, “Life, liberty and the pursuit of happiness” has always been America’s defining national rhetoric. However, in their cultural and socio-economic implications, the two could not be further apart. In particular, underpinning “Life, liberty and the pursuit of happiness” is the uniquely American interpretation of the individualism of English common law, while “Liberté, égalité, fraternité” flows from the collective nature of continental European civil law (the Napoleonic Code and, before that, Roman law). Indeed, these roots and characteristics distinguish Anglo-American individualist capitalism from continental European communitarian capitalism,2 although the latter is also found in non-European countries such as Japan, and in the province of Quebec.

One critical difference between these regimes has to do with the conception of the state (Fleiner, forthcoming). Under common law, from the Magna Carta forward, the main role of a constitution is to limit the powers of government and, in the US case, to guarantee citizens their “unalienable” rights. Indeed, the function of the branches of government under common law is to moderate among competing powers and interests. In contrast, in the civil-law tradition, the unity of the state is uppermost and is the main legitimizer of a constitution. As such, the civil-law state’s function is to steer society; in the case of France, for example, the role of the constitution is to organize society for the purpose of achieving equality and justice. Note that this civil-law conception of the state as sovereign, central, unitary and indivisible makes it difficult for civil-law societies to embrace federalism. In the German and Austrian federations, for example, the subnational governments are administrative, not legislative, entities, thereby preserving the civil-law vision of the (legislative) unity of the state.

Lester Thurow reflects as follows on the role of labour and capital in the two systems:

In the Anglo-Saxon variant of capitalism…firms must be profit maximizers. For profitmaximizing firms, customer and employee relations are merely a means to the end of higher profits for the shareholders. Wages are to be beaten down where possible and, when not needed, employees are to be laid off…Job switching, voluntary or involuntary, is almost a synonym for efficiency.

The communitarian business firm has a very different set of stakeholders who must be consulted when its strategies are being set. In Japanese business firms employees are seen as the number one stakeholder, customers number two, and the shareholders a distant number three. Since the employee is the prime stakeholder, higher employee wages are a central goal of the firm in Japan. Profits will be sacrificed to maintain either wages or employment. Dividend payouts to shareholders are low.

Communitarian societies expect companies to invest in the skills of their work forces. In the United States and Great Britain, skills are an individual responsibility…Labor is not a member of the team. It is just another factor of production to be rented when it is needed, and laid off when it is not. (1992, 32-3)

Michel Albert in Capitalism vs. Capitalism elaborates that in the “Rhine model” (his term for communitarian capitalism as practised in Germany), “all parties are invited to participate in company decision-making: shareholders, employees, executives and trade unions alike cooperate in a variety of ways to achieve a unique form of joint management [or corporatism] and…a 1976 law makes it compulsory for all firms of 2,000 or more employees to implement this system of shared decision-making at virtually every level” (1993, 110-11).3

The two models of capitalism also differ in their approaches to financial markets and industrial ownership. Although the differences are diminishing over time, in Anglo-American capitalism the dominant source of long-term corporate finance is equity, provided competitively by capital markets, whereas in communitarian capitalism the source of long-term finance tends to be credit, provided by universal banks.4 Arguably, the rising role of equity finance is one of the principal reasons why Frankfurt has not been able to overtake London as the financial capital of the European Union (EU), even though the United Kingdom is not in the eurozone.

Moreover, because corporate America is financed by impersonal capital markets, Americans are less concerned about preserving particular enterprises. As Thurow notes, “Since the group is not important, preserving any firm is not important” (1992, 142). Closely related is the difference in the approaches to industrial ownership. In Anglo-American capitalism, corporate assets are more or less continuously on the auction block. This is simply not the case in Germany, for example, where commercial bank cross-ownership of industry means that to get control of a firm such as Volkswagen, a buyer would have to get several of the German universal banks on side, plus the government. The same challenge would be found in civil-law Japan, where the keiretsu create a complex web of overlapping ownership of the country’s industrial sector. Markets and institutions in such communitarian societies are organic in nature and are an integral part of the societal fabric.

One further area of significant difference between individualist capitalism and communitarian capitalism merits highlighting: immigration. Almost by definition, individualist capitalism will be much more open to immigrants. Labour markets especially are welcoming, since, in principle at least, immigrants are on an equal footing with nationals because it is a worker’s skills rather than other personal characteristics that are rewarded. Hence, one celebrates the American “melting pot” and the “multiculturalism” successes of Canada and Australia – all common-law countries. Moreover, while these three countries have different approaches to immigrant accommodation, what they have in common is that the labour market is the key instrument of societal integration. Indeed, part of the inherent economic dynamism of the US stems from the fact that it has succeeded in attracting “the best and the brightest” to its shores.

In stark contrast, communitarian-capitalist societies appear to have considerable problems with immigration. Some are opposed to immigration (Japan), some tend to invite immigrants to enter primarily as “guest workers” (Switzerland), and some accept them but then are unable or unwilling to integrate them geographically or societally (Germany, France). Not only are these countries denied the rejuvenation from which immigrant-integrating societies benefit, but many of them have further rigidified their labour markets by adopting some version of the “insider-outsider” model of the labour market. Spain is a good example of these rigidities:

One of [every] two euros spent next year by the Spanish government will go on pensions, welfare payments or unemployment benefits. Yet the same government is unwilling to tackle one of the biggest barriers to growth; its unjust, two-tier labour market, in which some workers are nearly unsackable but others (the young, immigrants and others on temporary contracts) take the pain. (The Economist 2009, 61)

Arguably, what makes these insider-outsider models possible is the presence of a generous social safety net to placate the outsiders.5

Canada captured top place in the annual United Nations Human Development Index for much of the 1990s, due to both high material living standards and the superior health and educational outcomes that broad access to good-quality public services allows. It appears that Canada skilfully blended both versions of capitalism by combining the dynamism of the Anglo-American economic model with the inclusiveness of the continental European social model in striving for a society that pursued both efficiency and equity. And, of course, a major reason for this is that our federation likewise embraces both common-law and civil-law traditions.6

Most Canadians are puzzled if not astonished that a country as rich as the US lacks an effective social safety net. To be sure, American individuals and families with ample resources can access excellent health and education services that arguably define the “state of the art” for the rest of the world. However, for a significant and growing number of Americans this is not the case: tens of millions have no health care coverage (though the number will almost certainly decline if President Obama’s health care reform is fully implemented), and the US public school system is recognized as wholly inadequate for a developed country. A major part of this puzzle relates to the manner in which the US approach to individualist capitalism has evolved. In particular, and again incomprehensibly to most citizens of the developed world, the US reality is that while increasing incomes over time is a societal priority, the distribution of this income at any point in time tends not to be. Rather, what has come to be called the American Dream is a temporal dream – the belief of Americans that individual initiative and hard work will eventually deliver material progress for themselves and their children (Cooper 1997, 52). Thus, the American Dream is all about a better tomorrow.

Another characteristic of the US approach to the welfare state is that individualist capitalism, and especially the American “Life, liberty and the pursuit of happiness” variant, places more responsibility on the individual than does communitarian capitalism. As Sawhill notes, “In the US people believe that where you end up depends on your own effort and skills – that is, US citizens believe they live in a meritocracy” (2010, 5). As a result, the American ethic places more emphasis on opportunity than on poverty or inequality (20). But it is also true that the election of President Obama on a “Yes we can” platform signalled in large measure a desire to rejuvenate America’s social safety net. In spite of a confrontational and arguably dysfunctional political system, the passage of the US health care reform bill in 2010 represented “the biggest attack on economic inequality since inequality began rising three decades ago” (Leonhardt 2010, cited in Sawhill 2010).

Indifference to the actual distribution of income also carries over to the manner in which the US federation operates. Specifically, the US is the only developed federation (probably the only federation, developed or not) that does not have a formal revenue equalization program for subnational governments. It could be argued that, while richer states obviously have higher per capita incomes and therefore have access to higher per capita revenues, these incomes and revenues will get capitalized in the form of higher wages and rents. And since states’ expenditures are correlated with wages and rents, in the final analysis there may be little to equalize. However, the assumption that there is full (100 percent) capitalization is a convenient fiction that allows American individualist capitalism to also ignore point-intime distribution issues as they relate to fiscal relations between the federal government and states, and to fiscal equity between states.7

It should come as no surprise that common-law or individualist-capitalism countries are the last bastions of first-past-the-post (FPTP) electoral systems: the United States; the United Kingdom; Canada; Australia (except for the Upper House); and, until recently, New Zealand. For their part, communitarian-capitalism countries have various forms of proportional representation (PR) systems, which tend to encourage multiple parties and, therefore, coalition or consensus governments, and on occasion even grand coalitions between the two largest parties, as in Angela Merkel’s first mandate in Germany. On the other hand, FPTP systems tend to be adversarial in nature (witness Question Period in the parliamentary democracies of the British Commonwealth), typically involve two main parties and are usually characterized by majority governments. The two parties in FPTP systems often find themselves fighting for the electoral centre, whereas PR systems encourage narrowly focused, even single-issue parties. Here, recent experience in the US is very different. There seems to be no desire to occupy the centre; indeed, there seems little in the way of a policy centre to be occupied.

While the US clearly falls into the FPTP camp, its political culture differs significantly from those of the other FPTP systems. Topping the list of differences is the extraordinary amount of money involved in US election campaigns: over $1 billion in the 2008 presidential campaign and election (with Obama outspending McCain two to one), and $2.6 billion for the 2006 “off year” congressional election.8 In congressional races, a winner of a House of Representatives seat in 2008 spent an average of $1.4 million (compared with $680,000 in 1998), while a Senate victor in 2008 spent an average of $7.5 million (compared with $4.7 million in 1998) (Campaign Finance Institute 2010). In stark contrast, electoral expenditure limits (after the writ is dropped) for aspirants to the Canadian House of Commons in the 2006 election ranged from C$62,000 to C$106,000 (Heard 2011), depending largely on the number of eligible voters in the constituency, with the maximum spending limits for the national political parties set at just over $20 million if they field candidates in all ridings (Elections Canada 2010).

In 2010 the US Supreme Court ruled in Citizens United vs. Federal Election Commission that governments cannot ban political spending by corporations and by third parties more generally. Specifically, the five-to-four decision granted corporations free speech rights under the First Amendment. The consensus was that this ruling would help the Republicans, most immediately in the 2010 midterm elections. Indeed, data released in early December 2010 indicated that spending in those elections would likely end up in the $4-billion-plus range, over 50 percent more than the $2.6 billion spent in the 2006 midterm elections. Not only is the amount spent astoundingly high, but perhaps even more surprising, under this ruling, corporate America’s political donations can remain anonymous. Citizens United will buttress the adage that America has the “best government that money can buy,” and it may well add a new dimension to the meaning of “corporate governance.”

Along somewhat similar lines, US representatives and senators are more likely to be elected as a result of their own strengths, political and financial, than are members of Parliament in the British or Canadian systems, where many gain office on the coattails of their party or leader. Hence, US lawmakers are much freer to break from party positions. Intriguingly, however, the US political parties themselves are arguably more clearly defined than those in Canada or the UK. Specifically, the Democrats tend to be social and moral libertarians and economic protectionists, whereas the Republicans are social and moral conservatives/ protectionists and economic libertarians. At the risk of oversimplification, Democrats favour more expansive public goods and infrastructure on the social side and tend, compared with Republicans, to be pro-choice and to support same-sex unions on the moral side. In contrast, the Republicans embrace the religious right on moral issues, and the ethos of rugged individualism inclines them to be rather indifferent to issues of social equity at home. They also favour an aggressive role for the US abroad as the moral policeman and the defender of liberty and democracy. On economic priorities, Republicans favour lower taxes, smaller government (with the exception of military spending) and liberal trading regimes, whereas the Democrats typically support labour’s penchant toward protectionism and are (implicitly) in favour of higher taxation to fund their preference for a larger social envelope. Given these party preferences, it is not surprising that it is hard to find any common or middle ground.

Unlike Europe and Japan, the US came out of the Second World War with its economy and infrastructure largely intact. In one of their country’s finest hours, Americans embarked on the Marshall Plan, among other initiatives, to rebuild the war-ravaged economies, and they played a lead role in creating a new international institutional order: the World Bank, the International Monetary Fund (IMF) and the General Agreement on Tariffs and Trade (GATT) on the economic and trade side; and the United Nations and the North Atlantic Treaty

Organization on the political and security side. Further on trade and economic matters, the US took the lead in terms of a number of initiatives, including the gold-exchange standard anchored to the greenback (and later the dollar standard itself), as well as the move to restore full currency convertibility and capital mobility across the developed nations. To be sure, these measures were also in America’s self-interest since an expanding global economy was essential for the US to take full advantage of its privileged position as the uncontested economic superpower. Nonetheless, in the process the US paved the way for the Europeans and the Japanese to eventually achieve rough equality with the US in terms of living standards.

The postwar recovery in economic growth and trade led to the era of US mass production, or Fordism, and to significant increases in incomes. The result was a dramatic expansion of the American middle class. One of the key factors underlying this surge in US economic fortunes was the 1944 GI Bill of Rights, which ensured that the roughly 10 million returning soldiers, many of whom had been unemployed before the war, were eligible for training and scholarships. Gabor Steingart writes that this education program “would prove to be an upgrading of the labour force that was unprecedented in the world…[and] led to great jumps in productivity in the post-war era” (2008, 63). In 1946, almost 50 percent of the roughly two million US college or university students and three-quarters of the males were veterans (Bennett 1999).

Indeed, the privileged position of the US in the early postwar period was such that even relatively unskilled Americans could aspire to middle-class status because they were able to work with quantities of physical and financial capital that were simply not available in other countries. Moreover, the American economy was increasingly dynamic and innovative as a result of creating world-class universities and research institutes and of inviting the best and the brightest from the rest of the world to settle in the US. This innovation drove the productivity of all workers, regardless of skill level. For both of these reasons, American factory workers could command higher wages than similarly qualified workers elsewhere. The rising wages and incomes of these factory workers combined with falling prices for consumer goods arising from mass production meant that a majority of Americans were able to live the American Dream: the middle-class lifestyle. The United States had indeed reached the commanding heights.

Inevitably, however, Europe and Japan began to close the income and technological gap with the US, and in the 1990s many observers began to champion aspects of the European socio-economic model, especially its emphasis on training (e.g., apprenticeships) and on the high societal value placed on skilled trades. Part of the argument advanced, consistent with Thurow’s description of labour quoted earlier, was that the individualist-capitalism model’s tendency to view employee benefits and training (and social programs in general) more as a cost of production than as an investment in the education and well-being of workers and citizens was leading to the “commodification” of labour and to the attempt to compete with the bottom end of the labour force (Laux 1991, 289). As I noted in my presidential address to the Canadian Economics Association (Courchene 1992, 770), “While competing with the bottom may make sense as a transition strategy, over the longer term it is a mug’s game since there will always be somebody, somewhere with a lower bottom.” Indeed, I suggested that the resulting inequality of opportunity between skilled and unskilled workers would undermine social cohesion and would likely lead to the kind of societal decoupling consistent with the visions of America articulated by Robert Reich in 1991 and Christopher Lasch in 1994. Not surprisingly, “competing with the bottom” left unskilled labour vulnerable to offshoring.

In contrast, the advocates of communitarian capitalism argued that the better longerterm approach was to compete with the middle and upper parts of the labour market on the one hand and to embrace citizens’ upward mobility through skills enhancement on the other, as in the German apprentice/technologist model. This would lead, the argument went, to an industrial system geared to high-value-added production and thus a high-wage and, if one wished, a high-transfer economy and society. Hence, productivity increases within the European system in this era arose via technological change and by utilization of a labour force with a higher skill mix rather than from the commodification of labour under the individualist-capitalism model (Myles 1991, 363).

While Fordism did in this sense sow the seeds of its eventual demise, there were several key features of the US model that ensured that the American Dream would remain alive and well, at least for a time. Prominent among these was the fact that the US still excelled in innovation, while Europe remained largely engaged in economic and technological catch-up, not yet ready to make the transition to technological leadership. To be sure, this is a difficult transition, since the closer a nation gets to the technology frontier, the more “innovation” rather than “replication” becomes the name of the competitive game.

Beyond technological leadership, a second reason why the US trumped Europe and Japan in innovation during, and even beyond, the Fordism era relates to the inherent flexibility and dynamism of the US individualist-capitalism model. As Thurow notes, “America’s greatest strength is not its ability to open up the new…[but rather its] ability to shut down the old” (1999, 56). In more detail:

In contrast to America, where eight of the twenty-five biggest companies in 1998 did not exist or were very small in 1960, all of Western Europe’s twenty-five biggest corporations in 1998 were already large corporations in 1960…[Again] in contrast to America, which in less than a decade went from having two to having nine of the world’s top ten largest companies, Europe started with one and ended with one – Royal Dutch Shell. Europe has been completely unable to grow new companies into big companies in the last forty years. (93)

Whatever the other benefits of communitarian capitalism may be, the organic nature of its markets and institutions (i.e., its corporatism) is not conducive to the Schumpeterian cycle of creative destruction. Moreover, the inability to shut down the old (or sunset) industries means that labour and capital run the risk of being trapped in lower-productivity activities, whereas creative destruction frees up these factors to engage in newer and higher-productivity ventures. In this context, Canadian economist Sylvia Ostry’s oft-repeated dictum merits airing one more time: Governments may be no better or worse than the private sector in picking winners, but losers are incredibly adept at picking governments.

Given that the US has maintained much of the inherent flexibility and dynamism that allowed it to dominate the Fordism era, it would seem rather obvious that these characteristics would stand America in good stead in the informatics era, when Schumpeterian creative destruction holds even more sway. However, while the elites still reap the rewards of this dynamism, the combination of some key features of the informatics era interacting with America’s variant of individualist capitalism has served to undermine not only the American Dream and the middle class, but the US economy as well.

According to sociologist and information theorist Manuel Castells (1996, 2004), the postFordism or post-1980 global economic and financial environment is the product of two developments: a new and transformative technology that led to the emergence of the network as the preeminent and ubiquitous socio-economic organizational form, and a change in the Anglo-American value system in the direction of “unfettered capitalist globalization.” In tandem, these gave rise to the informatics era.

Underpinning the informatics era is a new general-purpose technology based on the dramatic enhancement of our capacity for, and the democratization of access to, information processing and communication, a technology that is built upon successive revolutions in microelectronics, software, computation, telecommunications and digital communication. And at the heart of this latest revolution is the Internet, which is the technological basis for the network. Because networks are located not in the “space of places” but rather in the “space of flows,” they are by definition unconstrained by national boundaries (Castells 2004). It is this characteristic of networks that underlies the informatics era’s conception of globalization – namely, “the ability for an economy to work as a unit in real time on a planetary scale” (Castells 1996, 92). In particular, networks are the key integrating instruments enabling the rapid emergence of global supply chains; indeed, global supply chains are networks.

A further transformative feature of the shift from an industrialization or Fordism paradigm to the new informatics paradigm is that it privileges knowledge and human capital (i.e., skills and educational attainment) relative to physical and financial capital or, to draw on my own terminology (2001), it privileges “mortarboards” over “boards and mortar.” Moreover, since human capital is distributed across the globe much more equally than is physical or financial capital, and since the full resources of the network society are in principle accessible from anywhere on the globe, these space-of-flows enterprise networks have the obvious potential for dramatically reconfiguring the locus of geographical (space of places) economic power.

Another difference, as Paul Romer notes, is the sharp contrast between the “decreasing returns” nature of the former industrial Fordism economy of resource extraction, commodity production and manufacturing and the “increasing returns” nature of the knowledgeinnovation economy characterizing the new era (1997). While competition in the industrial paradigm normally occurs when new firms produce a similar product but at a lower price, this is not the typical pattern in the informatics era. Here, Romer says, competition occurs when new firms enter by developing new and better products: that is, by innovating. This “leapfrogging” or creative-destruction process of innovation is the essence of the ongoing computer and Internet revolution and, more generally, of the informatics era.

Given all this, it is not hard to anticipate part of the ensuing storyline: relatively unskilled workers (especially those operating with abundant physical and financial capital, as was characteristic of US workers in the earlier era) fared much better under “boards and mortar” Fordism than in the “mortarboards” informatics era.

Accompanying this new technological and knowledge-based era was and is a very significant ideological shift. Castells notes that this shift was essential because the existing industrial model was underperforming. Its organizations, values and policies were unable to achieve the economic potential unleashed by the informatics revolution. In effect, this meant calling into question the Keynesian economic model and more generally the role of government within it. What actually transpired might be referred to as the “Reagan-Thatcher transform.” Castells elaborates:

The decisive shift to a different model of accumulation came from governments, albeit in harmony with corporations. It can be related to the twin victories of Thatcher in the UK in 1979 and Reagan in the USA in 1980…They came to government with a mission: to recapitalize capitalism, thus ushering in the era of economic liberal policies that by successive waves took over the world, in different political-ideological versions, over the next two decades. The crushing of organized labor politically, the cutting of taxes for the rich and the corporations, and widespread deregulation and liberalization of markets…were crucial strategic initiatives that reversed the Keynesian policies that had dominated capitalism in the previous twentyfive years…A new orthodoxy was established throughout the world…unfettered capitalist globalization, spearheaded by the liberalization of financial markets…and enshrined in asymmetrical trade globalization represented by the new managing authority, the World Trade Organization. Under the new conditions, global capitalism recovered its dynamism, and increased profits, investment, and economic growth, at least in its core countries and in the networks that connected areas of prosperity around the world. (2004, 15-16)

The immediate US action in pursuit of unfettered capitalism was massive income tax cuts. Ronald Reagan cut the top US marginal personal income tax rate from 70 percent to 28 percent during his presidency, a tax cut that in varying degrees was replicated across the developed world. These tax cuts were accompanied by large increases in defence expenditures. This policy package, appropriately termed “military Keynesianism,” led to the Reagan boom, described by Martin Anderson: “We don’t know whether historians will call it the Great Expansion of the 1980s or Reagan’s Great Expansion, but we do know from official economic statistics that the seven year period from 1982 to 1989 was the greatest, consistent burst of economic activity ever seen in the U.S. In fact, it was the greatest economic expansion the world has ever seen – in any country, at any time” (1990).

The downside of military Keynesianism, however, is that it also generated domestic and foreign indebtedness not seen since the Second World War. During the Reagan era the US went, in absolute terms, from being the world’s largest net creditor nation to being the world’s largest net debtor nation. Specifically, the net international investment position of the US (including direct and portfolio investment) went from a $360.3-billion surplus in 1980 to a $246.2-billion deficit in 1989, while the US net federal debt ballooned from $700 billion to $2.2 trillion over Reagan’s eight years. Although obviously at odds with the traditional Republican principle of limited government, this run-up in debt and deficits did serve to hamstring any and all efforts to introduce major new spending programs in nondefence areas.

Up until the millennium, and even beyond, unfettered capitalism led, as intended, to a dynamic, innovative and growing America. This ideological shift was certainly fully in line with “Life, liberty and the pursuit of happiness” and the individualist-capitalism model. Moreover, it so infused domestic thinking that the US did its very best to export this philosophy to the rest of the world via the Washington Consensus, a set of principles based on liberalization, deregulation, privatization and free markets used by international institutions such as the International Monetary Fund in their programs for economically troubled nations.

The transition from Fordism to the informatics era also led to a social transformation. The reconciliation of social and economic goals inherent in the Fordism era lay in what John Ruggie has termed the “compromise of embedded liberalism”: “Societies were asked to embrace the changes and dislocation attending liberalization. In turn, liberalization and its effects were cushioned by the newly acquired economic and social policy roles of governments” (1995, 508).

As a result, the modern welfare state grew in tandem with increasing international economic openness because the institutional framework embedded this openness within an activist domestic social democracy and an accommodating international regulatory system, most notably the World Bank, the IMF and the GATT. To be sure, the Fordism era was the heyday of the Keynesian revolution, with its attendant growth in the size and scope of governments everywhere, which served to accommodate domestic priorities and aspirations alongside increasing internationalization of trade. In fact, “it [was] in the most open countries, such as Sweden, Denmark and the Netherlands, that spending on income transfers [had] expanded the most” (Rodrik 1997, 6).

But in the informatics era it is much less likely that unfettered globalization will be accompanied by a deepening of the social envelope. Rather, the opposite is likely to be true:

Far-sighted companies will tend to their own communities as they globalize. But an employer that has an “exit” option is one that is less likely to exercise the “voice” option. It is so much easier to outsource than to enter a debate about how to revitalize the local economy. This means that the owners of internationally mobile factors become disengaged from their local communities and disinterested in their development and prosperity. (Rodrik 1997, 70)

The question, as Rodrik sees it, is how to ensure that international economic integration does not lead to domestic social disintegration.

Unfortunately, but perhaps unsurprisingly, US policy has effectively ensured that international economic integration will indeed lead to domestic social disintegration. Four signs of this development are examined next: first, the outsourcing and offshoring phenomenon; second, the evolution toward “winner take all” capitalism; third, the current mortgage and financial debacle; and fourth, the eroding middle class.

Human capital is to the informatics era what physical and financial capital were to Fordism. In this increasingly knowledge-based era, the market incomes of those with skills and human capital are rising relative to the market incomes of the unskilled. Furthermore, the greater an individual’s human capital, the more mobile internationally he or she is likely to be. This means that in addition to garnering higher wages, high-level human capital, or “talent,” is now more difficult to tax. This follows from the general proposition that mobile firms and workers can simply move in response to onerous taxation or regulation. No doubt this is part of the reason why Reagan’s dramatic personal income tax reductions triggered analogous reductions across the countries of the Organisation for Economic Cooperation and Development (OECD) and beyond. The evidence suggests that it is the immobile factors (land and unskilled labour) that, relatively and even absolutely, are bearing much of the adjustment cost arising from the informatics era (Rodrik 1997). One of the consequences is that the increase in the returns to human capital will inevitably reconstitute the US middle class along the skills and education spectrum and, equally inevitably, will undermine much of Fordism’s middle class. Indeed, this is the theme that underlies much of what follows.

In a context of unfettered capitalism and global supply chains, firms can now search the globe for the most cost-effective location from which to source inputs into the production process. The first and foremost implication for unskilled labour arises from the fact that while work becomes mobile, low-wage workers do not. Thus, the earlier model, which gave rise to an American middle class based on unskilled labour working with a relative surfeit of physical and financial capital, has become less and less competitively viable. The new reality is that workers at the relatively unskilled end of the labour force no longer have access to the American Dream through simple hard work: there will always be a lower, economically accessible bottom elsewhere where this work can be outsourced.

Intriguingly, society’s long-standing focus on the minimum wage is being turned on its head by the increasing importance of what might be called the “maximum wage.” If the domestic wage related to a given activity is above a certain threshold (i.e., the maximum global wage for this activity), then the activity becomes a candidate for offshoring.

Under unfettered capitalist globalization, there are no longer any “national” firms in the sense of enterprises embracing national goals and policies, unless these are consistent with global economic efficiency or are essential to national security.10 What is possible, however, is for nations to enact policies, or otherwise encourage activities, that generate “positive non-traded externalities” (Storper 1995). By definition, the only way to access these externalities – often found in clusters – is to locate in their midst. Examples would include the depth and breadth of the informatics-literate labour force in Silicon Valley or the expertise associated with golf-club technology and manufacturing in Carlsbad, California. Such untraded externalities also exist at more aggregate levels (America’s flexible and dynamic entrepreneurial environment would qualify, as would Canada’s publicly funded health care).

Encapsulating the dilemma of unskilled workers in the informatics era, as well as pointing the way toward one obvious solution, Lester Thurow writes: “If unskilled first world workers don’t want to be in competition with equally unskilled but lower wage third world workers, they will need much better skills. With globalization and a skill-intensive technological shift, much better skills must be delivered to the bottom two-thirds of the labor force in the developed world if their wages are not to fall” (1999, 132-3). Thurow also offers the following informatics-era truism about the implications of unfettered capitalist globalization: “If capital is borrowable, raw materials are buyable and technology is copyable, what are you left with if you want to run a high wage economy? Only skills, there isn’t anything else” (1993). Because this is a key message for all policy-makers in all economies, it may be that success on this front requires not only an absolute, but also a relative upgrading of skills.

So far in this discussion of offshoring we have been ignoring the elephant in the room – namely, that much of what passes for offshoring represents, as Steingart (2008) suggests, an abandoning of Western values and an embracing of the values of the emerging nations as they relate to labour practices and environmental policies.

With an unfathomable 1.5 billion new workers appearing in the world economy over the recent time frame, the global labour market is experiencing a decline in wages that has caught the West by surprise. Brazil, Russia, India and China now have 45 percent of the world’s labour supply compared with 19 percent for OECD members (Steingart 2008, 150). In the presence of global supply chains, transnational firms will obviously move to take advantage of the resulting wage differential. And a most substantial advantage it is, as Steingart elaborates:

Labor costs make up 23 percent of the retail price of a television set made in the West; the cost of labor that goes into the primarily Asian-made parts is low, but the assembling costs in the West are much higher. If the television set is completely made in China, labor costs make up only 4 percent of its retail price. It is precisely this wage gap – all other production costs being nearly equal – that will ultimately shut out ordinary American workers. (150)

In addition, we can choose a domestic GM vehicle with its associated nonwage labour costs (such as health insurance premiums and pension contributions) of $1,600, or we can choose a car from another country that will not include this markup. Likewise, US-made Whirlpool washing machines cannot compete economically with those from China and elsewhere where workers have deplorable working conditions and there are no environmental standards. Phrased differently, “there is no built-in welfare state in a Chinese made household appliance” (Steingart 2008, 152-3).

The ultimate irony here is that while the West has welcomed China into the World Trade Organization (WTO) in order to ensure that the international playing field becomes more level, it is the West that has embraced (via offshoring of production and reimporting the resulting goods) the social and environmental policies of China and other emerging nations, with the result that the playing field has never been so unlevel from an American (and Western) vantage point. This is a collective decision by the West so that individual Western capitalists have no choice except to take advantage of moving production abroad.

Now some have claimed that, in aggregate, the benefits to all consumers from lower prices as a result of offshoring and then reimporting exceed the dollar costs associated with workers whose jobs have been outsourced. First of all, this is probably not the case: the true dollar costs of this outsourcing must include the ratcheting upward of America’s twin deficits – the fiscal deficit because of the increased draw on social programs and the current account deficit because of the huge trade imbalance with China – and the resulting increase in US foreign indebtedness. Second, this is a comparison that could be made only in a society where consumerism as a value is put on par with access to employment. Arguably, this consumerism ethic is one of the features that sets the US apart from the typical communitarian society.

Outsourcing is an element of what might be referred to as “winner-take-all capitalism.” Writing during the period when the American Dream was secure, economist Kenneth Boulding stressed “the inefficiency of attempting to wrestle $1 away from one’s fellow man when for the same effort one can wrestle $10 from nature” (1973, 95). However, in recent years, when nature seems less bountiful, the temptation to wrestle a dollar from one’s neighbour becomes correspondingly stronger. Indeed, a case can be made that US individualist capitalism has veered in this very direction in recent years, as a more competitive external environment encourages rent-seeking rather than value-adding activities.

As early as the 1990s, Robert Reich in The Work of Nations (1991) argued that the wellbeing of Americans depended on the value that they add to the global economy through their skills and insights. Obviously, not all Americans are equal in this regard. Reich distinguishes among three types of workers or jobs: routine production workers, in-person services and symbolic analysts. He associates symbolic analysts with problem solving, problem identifying and strategic brokering services. In this era of increasing ease and speed of global communication, the economic star of these symbolic analysts is rising dramatically, while it is falling for the other two groups, particularly for the routine workers as they are replaced by cheaper labour elsewhere. Reich notes that these symbolic analysts tend to congregate geographically (e.g., Silicon Valley and Route 128 near Boston), resulting in not only a widening income gap but also a geographic polarization of rich and poor areas. The symbolic analysts are, in effect, “seceding from America” and linking themselves to the global economy: their social and political bonds to America tend to unravel as their economic bonds unravel.

In “The Revolt of the Elites: Have They Cancelled Their Allegiance to America?” Christopher Lasch expands on this phenomenon: “The elites possess most of the wealth. They are becoming increasingly independent from crumbling industrial cities and crumbling public services because they have their own private schools, private health care, private security etc. Their market is international and their loyalties are international rather than…national or local” (1994, 47).

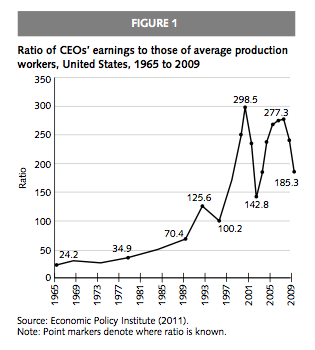

Direct evidence on the extent to which the American elites have in fact “seceded from America” would obviously be hard to come by. However, recent data based on two different approaches to assessing the relative and absolute incomes of the wealthiest Americans reveal that they certainly have the means to do so. The first set of data measures the ratio of US chief executive officers’ earnings to those of the average production worker from 1965 to 2009 (figure 1). In 1965, CEOs earned an average of 24 times more than the average production worker earned. By 1978 the ratio had increased to 35 times. But the big increases came in the informatics era, culminating with an interim high of 298 in 2000. The temporary fall to 143 in 2002 reflects the impact of the high-tech bust. By 2005 the ratio had rebounded to 277, before falling in the wake of the recent recession.

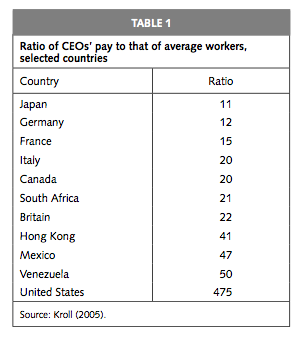

Is America unique here? Or do other capitalist countries, particularly individualist-capitalism countries, have similar patterns? Table 1 comes at this question using different data than in figure 1 – namely, the ratio in 2005 of CEOs’ total pay (rather than salaries and bonuses) to average workers’ pay (rather than production workers’ earnings). The civil-law nations in the table have ratios ranging from 11:1 in Japan to 20:1 in Italy, with Germany and France in between. In individualist-capitalism countries, Canada and Britain have ratios of 20:1 and 22:1, respectively, with common-law Hong Kong coming in with a ratio of 41:1. While these rankings are largely consistent with the two forms of capitalism, the real story is how the US compares with all other countries. With a ratio of 475, it appears that the US has taken the individualist-capitalism model to rather unimaginable heights,11 the latest indication that the US is becoming a winner-take-all (or in the case of bailed-out CEOs, loser-take-all) society.

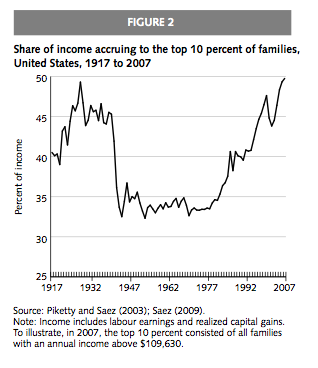

Figure 2 contains further evidence along similar lines: the share of overall nominal market income (including capital income) accruing to the top decile of income earners over the period 1917-2007, based on data compiled by Piketty and Saez (2003) and Saez (2009). For 1917 to 1945 they trace the rapid rise in the top-decile income share from 1917 through to the market crash in 1929 and then the dramatic fall from the crash through to the Second World War.12

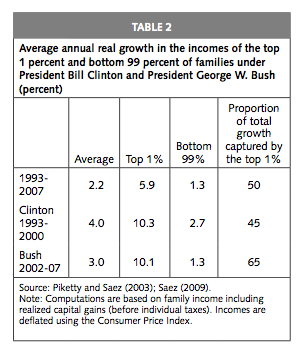

The period from the 1950s to about 1980, which was the heyday of the American Dream, is characterized by a top-decile share averaging just under 35 percent. From 1980 onward, the share rises dramatically, touching 50 percent in 2007. More startling evidence of the widening income gap appears in table 2, which presents the growth of real annual incomes for the top 1 percent of Americans and for the remaining 99 percent, for both the Clinton and the Bush expansions. From 2002 to 2007 (during the George W. Bush era), the top 1 percent captured 65 percent of the total income growth, compared with 45 percent under the Clinton expansion. That the remaining 99 percent of Americans garnered only 35 percent of total income growth over the Bush years is further confirmation of winner-take-all capitalism. While the Clinton period was more benign, the 55 percent share of income growth accruing to 99 percent of Americans from 1993 to 2000 obviously also qualifies for the winner-take-all label. Not only do the data show a dramatically eroding middle class, but the income disparities raise concerns about social stability and democracy. Suffice it to say that as eminent a free-market proponent as Federal Reserve Chairman Alan Greenspan, appearing before a Senate committee in June 2005, commented as follows on the diverging fortunes of different groups in the labour market: “As I’ve often said, this is not the type of thing which a democratic society – a capitalist democratic society – can really accept without addressing” (Grier 2005).

The evidence of the impact of offshoring on low-skilled workers and of the income performance of the richest Americans leads to the conclusion that America is fast becoming the most unequal society in the OECD. For the middle class, prospects are worsening and the promise of the American Dream is fading. Enter the subprime mortgage debacle.

Since China seems omnipresent in any analysis of recent events and future prospects for the US, it should not come as a surprise that China also played an oft-overlooked triggering role in the still-ongoing mortgage collapse in the US. Specifically, the combination of China’s role as the world’s workshop, its surplus labour supply (which has kept its domestic wages relatively low) and the currency peg between the yuan and the greenback effectively meant that US goods and services inflation was also low and stable before the collapse. Even though the US Federal Reserve has not formally embraced inflation targeting, it nonetheless tends to calibrate interest rates with reference to what is happening on the inflation front, so interest rates remained low in the mid-2000s in spite of the fact that the economy and expectations were spiralling upward. In the event, monetary policy was far too easy. (If the inflation rate chosen for assessing the appropriate monetary stance had included asset prices in addition to goods and services prices, interest rates would have increased much earlier than they actually did, thus providing some early dampening to what Greenspan had earlier labelled “irrational exuberance.”)

It was in this environment that “financial engineering” by the largely unregulated investment banking industry found a foothold. The search was on for some relatively high-yielding financial instrument that could be successfully and successively leveraged via collateralized debt instruments and could, therefore, satisfy the excess demand for credit. The fateful choice was mortgages, and specifically subprime mortgages. (Note that “subprime” actually refers to mortgagors, not the instruments: it is the borrowers who did not qualify as “prime.”) In the euphoria of rising home prices in the mid-2000s, the mortgage interest rate for an initial period was set appealingly low, with the renewal rate a couple of years later typically set several percentage points higher. The selling pitch presumably included the likelihood of a substantial appreciation of the value of the property, so that the future interest rate increases could be downplayed. This is one way in which financial engineering morphed into financial subterfuge. Another was that the collateralized debt based on mortgages of subprime borrowers was sliced into tranches, the upper echelons of which were, astoundingly, endowed with triple-A status by the rating agencies.

That regulators could allow the collateralization of these mortgages to balloon into an enormous inverted pyramid and in the process risk the viability of the entire financial sector seems unfathomable, even under the most extreme winner-take-all version of individualist capitalism. And as if the subprime mortgages and the collateralized debt weren’t bad enough, the infamous credit default swaps (which Warren Buffett called “financial instruments of mass destruction”) rounded out the risk-laden picture. These were market instruments that allowed third (unrelated) parties to speculate on the success or failure of specific financial instruments and institutions.

The jump in oil prices to nearly $150 per barrel in mid-2008 put a real damper on expectations of future growth. As the shock of the oil spike spread through the economy, discretionary income fell sharply. Then the built-in interest increases in subprime mortgages kicked in, and a steep increase in foreclosures began: they rose from under 2 percent of mortgages in the second quarter of 2006 to nearly 7 percent in the second quarter of 2008 (Liebowitz 2009). And as these foreclosures spread to the overall financial system, the massive inverted financial pyramid collapsed and triggered the most severe recession since the Great Depression. Not surprisingly, this turned out to be devastating for many lowand middle-income Americans. The unemployment rate approached 10 percent, and the proportion of US homeowners who were “under water” (i.e., who owed more on their mortgages than their properties were worth) soared to about 25 percent (Simon and Hagerty 2009, 24) and remains near that level as of early 2011. This translates to over 11 million households with negative home equity. This is certain to be a further blow to those individuals who had earlier viewed themselves as middle-class, home-owning Americans but had been enticed into remortgaging their homes.

A final indignity visited upon the victims of the mortgage debacle can be described only as a display of unrestrained greed: namely, the multimillion-dollar bonuses paid out to executives of financial institutions, some of whom were among the key players in creating this dangerously leveraged financial situation. Indeed, some of these bonus recipients were from firms that exist today only thanks to last-resort bailout efforts by the US Treasury and the Federal Reserve. The defence offered by these institutions is that these bonuses (and more generally the sky-high pay packages) are necessary to retain valued talent and prevent them from moving to competing firms. However, from table 1 and figure 1, it is clear that this market for top-end talent is largely an American-driven market, not a global market. Where else could these people go? Alternatively, given what they have wrought, why are they still so valued today?

It is important to note that the blame for the subprime fiasco should not fall only on the financial market players. For example, as noted earlier, had the Federal Reserve been targeting asset prices in addition to goods and services prices, it would have raised interest rates much sooner and alleviated some of the excess demand for credit. In the event, the financial institutions engaged in increasingly risky loans and mortgages in order to meet this demand. Influencing them in this direction was the earlier government pressure on banks to make home loans in lowand moderate-income neighbourhoods. Moreover, the regulatory bodies were surely aware of the typical modus operandi of the financial lenders in carrying out this mandate of increasing home ownership: offering a combination of no down payment, no verification of income, interest-only payment plans, weak credit history searches and adjustable-rate mortgages. The unfortunate irony here is that this pressure was presumably premised on the notion that home ownership is an integral part of the American Dream. Given that roughly a quarter of existing mortgages are still under water, the devastation of the subprime mortgage debacle may not yet have run its course. This is regulatory failure on a grand scale. An appropriate concluding comment on this shocking episode is from Michael Lewis’ The Big Short: “The leveraging of middle-class America was a corrupt and corrupting event, and the subprime mortgage market in particular was an engine of exploitation and, ultimately, destruction” (2010, 107). Well phrased.

The implications of America’s version of unfettered capitalist globalism for the middle class and for the American Dream can be seen in Middle Class in America (US Department of Commerce 2010), a document prepared for the Office of the Vice President of the United States. For two-parent, two-child families in the 50th income percentile, real income was $67,600 in 1990; in 2008, a 50th-percentile family’s income was $80,000, 20 percent higher.13 However, the inflation-adjusted prices for some major-expenditure items associated with a middle-class lifestyle had increased by much more than 20 percent since 1990 – housing (56 percent), health care (155 percent), public college (60 percent) and private college (43 percent). This, too, is a key feature of the erosion of the American Dream.

While it seems clear that middle-income Americans are worse off today than in past years because they are less able to afford the basket of goods and services that define a middle-class lifestyle, something more worrying has emerged – namely, the polarization of incomes and the resulting increase in inequality in the US.

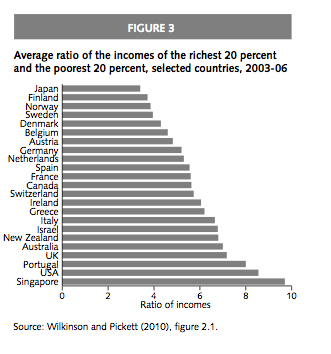

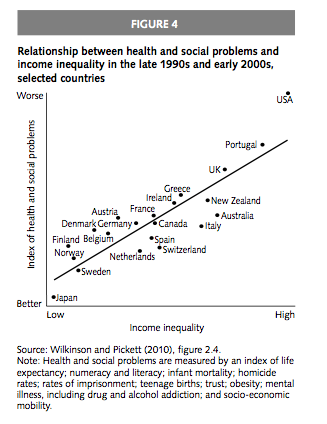

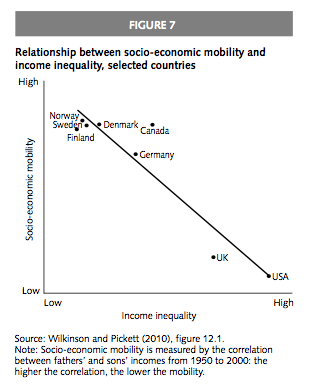

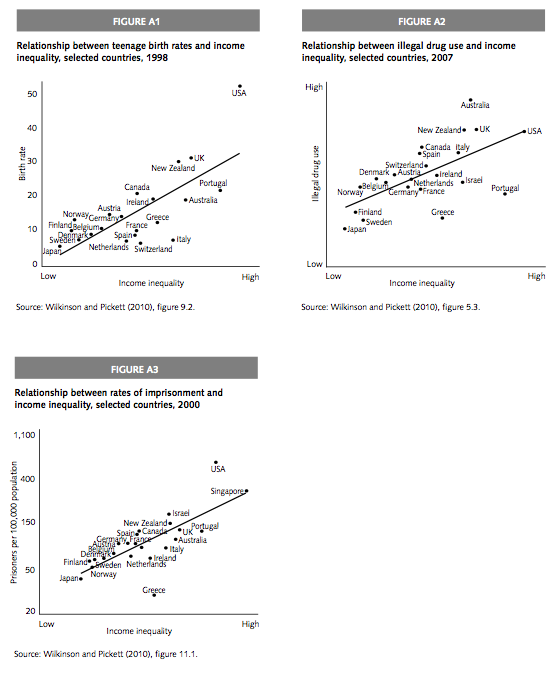

In The Spirit Level: Why Equality Is Better for Everyone (2010), Richard Wilkinson and Kate Pickett bring what they refer to as “evidence-based politics” to the role that income inequality, as distinct from income level itself, plays in the incidence and severity of health and social problems. The measure of inequality that they use to examine a sample of rich countries is UN data on the ratio of income received by the top 20 percent of the population relative to the income of the bottom 20 percent of the population; income is measured as household income after taxes and benefits, adjusted for the number of people in each household. A second data set comprises the 50 US states, with the familiar Gini coefficient used as the inequality measure.

Among 23 rich countries (figure 3), Japan and the Nordic countries have the least inequality and the US is the most unequal, except for Singapore. In the US, the top 20 percent have an income level about 8.5 times that of the bottom 20 percent. Excluding Portugal (because its income per capita is several thousand dollars less than the next-richest country’s, and lower-income countries tend to have more unequal income distribution), something quite surprising is apparent in figure 3: the 6 most unequal countries are all common-law or individualist-capitalism countries, whereas the 11 most equal countries are communitarian-capitalism countries. Canada ranks higher in the equality hierarchy than any common-law country, presumably because it is a hybrid of the two models.

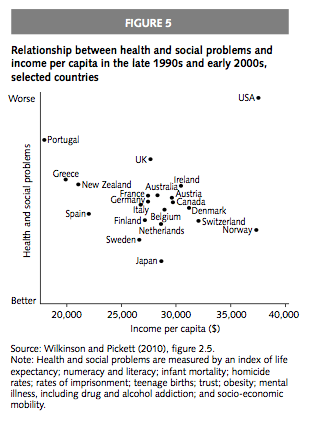

Wilkinson and Pickett find that the greater the degree of income inequality, the worse are the health and social problems; the US is a clear outlier, with the greatest inequality and the worst outcomes. Of the 21 countries in figure 4, the communitarian-capitalism countries tend to do much better than the individualist-capitalism countries. Figure 5 establishes that there is no obvious correlation between the level of per capita income in these countries and the index of health and social problems, so inequality has an impact on social pathologies that is independent of income itself.

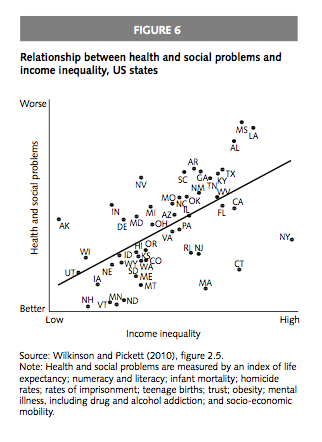

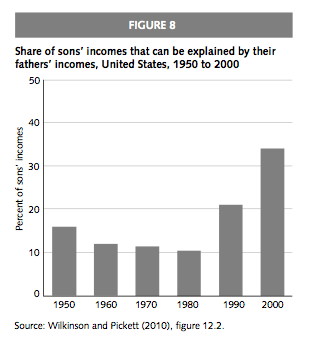

When this exercise is repeated for the individual American states, the results show that, like countries, states with greater inequality (i.e., higher Gini coefficients) have worse health and social problems (figure 6). The authors also show that there is no general relationship between US states’ social pathologies and the level of their per capita incomes, so again inequality appears to have an impact independent of income levels (not shown here).