Les politiques commerciales du Canada au carrefour des nouvelles réalités mondiales

Aperçu des résultats de recherche

Stephen Tapp, Ari Van Assche et Robert Wolfe

Sébastien Miroudot is senior trade policy analyst in the Trade in Services Division of the OECD Trade and Agriculture Directorate. His research interests include trade in services, trade and investment, and trade flows within global value chains. He is currently working at the OECD on the measurement of trade in value-added terms and the construction of a services trade restrictiveness index. He holds a PhD in international economics from Sciences Po, Paris.

Redesigning Canadian Trade Policies for New Global Realities, edited by Stephen Tapp, Ari Van Assche and Robert Wolfe, is the sixth volume of The Art of the State. Thirty leading academics, government researchers, practitioners and stakeholders from Canada and abroad analyze how changes in global commerce, technology, and economic and geopolitical power are affecting Canada and its policy.

Services have long been regarded as essentially nontradable across international borders, while goods are thought of as the things we trade. But this outdated view of trade is changing due to ongoing technological progress — particularly, the information and communications technology revolution — and a better understanding of the important role services play in manufacturing activities and the overall economy. Changing production practices, featuring the growth of global value chains (GVCs), further underscore the significance of the services that link firms’ geographically dispersed activities, including transportation, communications, logistics and finance (Jones and Kierzkowski 2001). Indeed, these services links are so crucial that, without them, GVCs would not exist.

Services also matter because they now account for the vast majority of employment and output in advanced economies. The efficiency of the services sector is thus a crucial determinant of an economy’s overall competitiveness. Moreover, as recent research suggests, a country’s export competitiveness increasingly depends on its ability to import services easily (Nordås and Rouzet 2015). If this is the case, there are potentially large gains from better aligning services regulations to the realities of today’s global business environment. The next stage of the industrial revolution will likely be a services revolution as the distinction between goods and services dissolves, as anticipated by the “Internet of things” or the “industrial Internet” (see Evans and Annunziata 2012). In this new paradigm, industrial production is widely expected to rely increasingly on intelligent devices, networked sensors, big data analytics and machine learning. As a consequence, digitally enabled products, processes and services increasingly will be combined. Countries that adopt policies to facilitate the seamless provision of services across international borders stand to benefit most from these developments and new business models.

In 2015, Canada exported approximately $99 billion and imported $123 billion worth of services, representing 5.0 and 6.2 percent of its gross domestic product (GDP), respectively.1 The country’s largest services trading partner by far is the United States (with 56 percent of Canada’s total services trade in 2014); in second place is the United Kingdom (with 5.6 percent).2

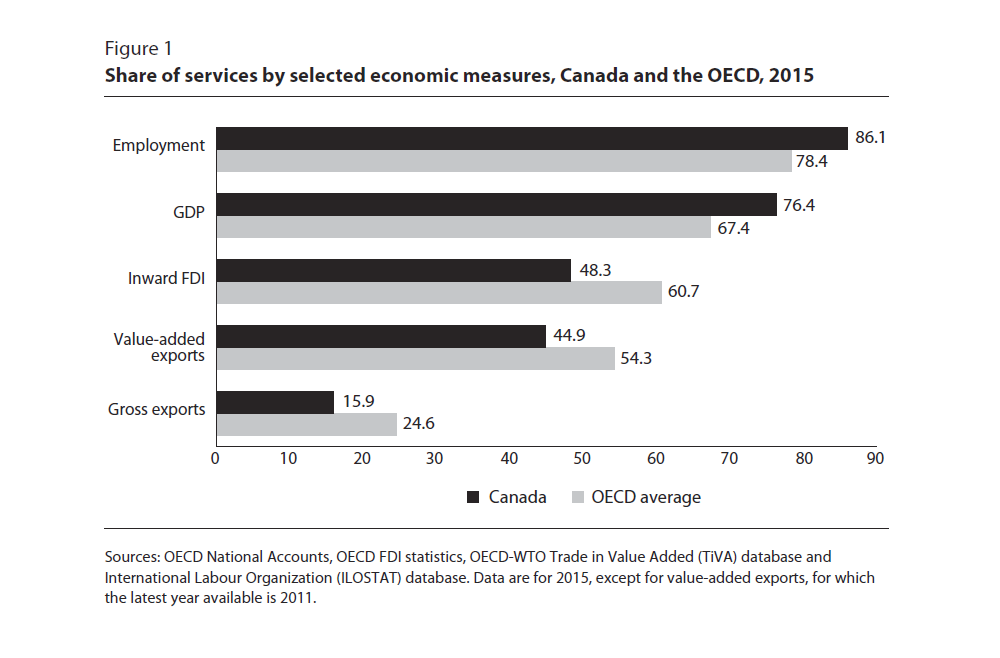

Services still represent only 16 percent of Canada’s gross exports, but 45 percent of the total when measured by value added, as in the Trade in Value Added (TiVA) database compiled by the Organisation for Economic Co-operation and Development (OECD) and the World Trade Organization (WTO) (see figure 1). Put differently, of every $100 worth of products Canada exports, roughly $45, on average, goes to services activities. The value-added share is so much larger than the share measured in gross export terms because many services are embodied in goods that are exported. Services also represent almost half of Canadian foreign direct investment (FDI) inflows, and contribute more than three-quarters of the country’s GDP and more than four-fifths of its total employment. Canada’s economy is, in fact, more services-intensive, in terms of services’ share of both employment and output, than the OECD average, but below the OECD average in services’ share of total exports, partly reflecting the higher share of mining products — which have a relatively low services content — in Canada’s exports (see OECD 2015).

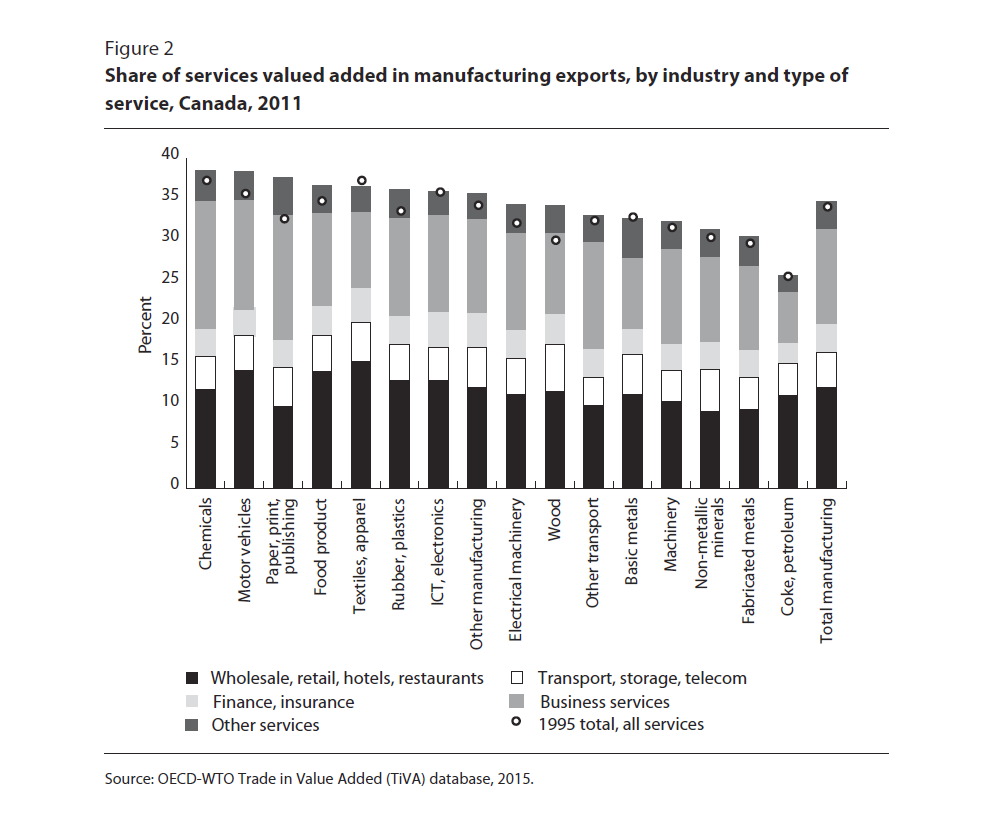

The contribution of services to Canada’s manufacturing exports varies by industry, with distribution services — which include wholesale and retail trade — generating the most value added,3 with business services coming second (figure 2). Transportation, storage and telecommunication, and finance and insurance also account for significant shares of the services value added embodied in Canadian manufacturing exports. Between 1995 and 2011, the services share increased in every manufacturing export industry except textiles and apparel.

Services also create value and spur innovation. Increasingly, research and development (R&D) and design activities at the beginning of the value chain are being outsourced (or sent offshore), becoming services inputs in GVCs. For R&D conducted inhouse (or onshore), services such as training and education help to create and maintain essential human capital. Skills improvement, consulting services and other types of business services help increase the productivity of firms at any stage. Product innovation is another important part of the story, as more firms develop value added by bundling goods and services together. Customer services are an integral part of this strategy to add value. Instead of selling products alone, firms increasingly “sell solutions” for their customers’ unique problems. Interactions between producers and customers increase customization, and these tailored solutions enhance productivity and contribute to economic growth.

Given the growing importance of services, it is unfortunate that countries maintain significant barriers to the international trade in services. Particularly in the wake of a painfully slow global economic recovery, reforming services markets could be an important contributor to enhancing growth. To that end, OECD research has focused on identifying services trade barriers and assessing the potential gains from reforms. The OECD’s Services Trade Restrictiveness Index (STRI) is based on a verified and peer-reviewed regulatory database, compiled from laws and regulations currently in place in the 34 OECD member countries, plus Brazil, China, Colombia, India, Indonesia, Latvia, Russia and South Africa. Using this database, the OECD identifies five forms of restrictions on services trade: restrictions on foreign entry; restrictions on the movement of people; barriers to competition; regulatory transparency; and other discriminatory measures. A domestic market completely open to foreign trade and investment would score zero by this system; a market completely closed to foreign services providers would score 1. Importantly, the STRI database is measured on a most-favoured-nation (MFN) basis, and does not take preferential trade agreements into account (for details, see Geloso Grosso et al. 2015).

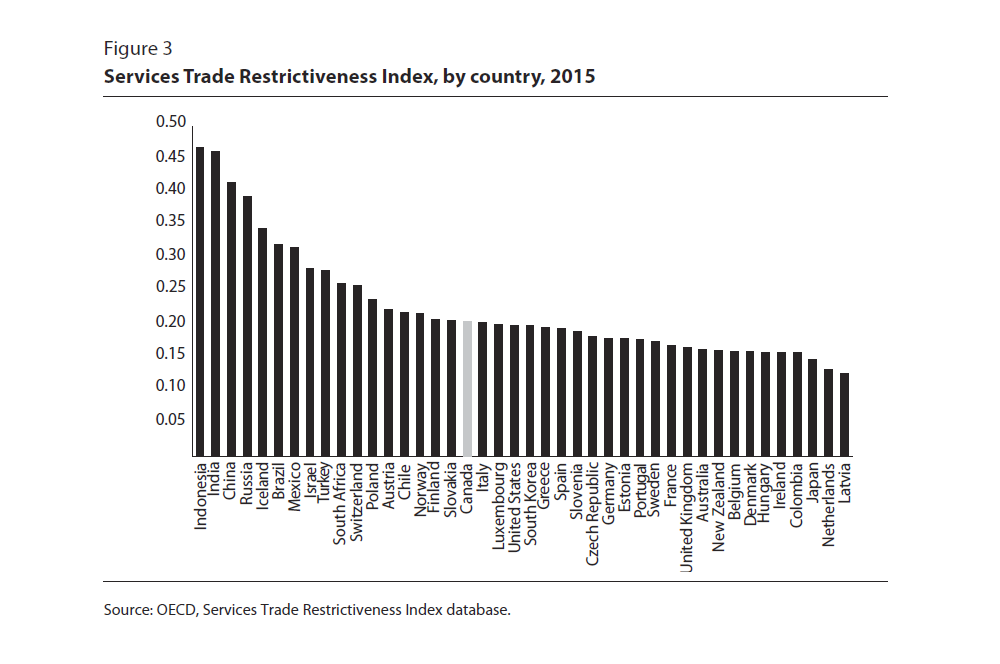

The STRI allows trade negotiators to clarify the restrictions that most impede trade, growth and employment, and businesses to be aware of the requirements they must comply with to enter foreign markets. In all OECD countries and in major emerging economies, services regulations include a variety of measures that restrict trade (OECD 2014). Some explicitly discriminate to protect domestic services providers; others have negative unintended consequences on trade simply because they were not designed for the interconnected world in which we now live. Figure 3 provides an STRI value for each country in 2015, using a simple average over industries that does not account for their relative importance in each country’s economy. The least restrictive economies among the 42 in the STRI with respect to services trade are Latvia, the Netherlands, Japan, Colombia and Ireland, while the most restrictive are the major emerging economies; Canada places near the middle of the pack, ranking 25th, similar to European countries such as Norway, Finland and Italy, and just slightly behind the United States (see figure 3).

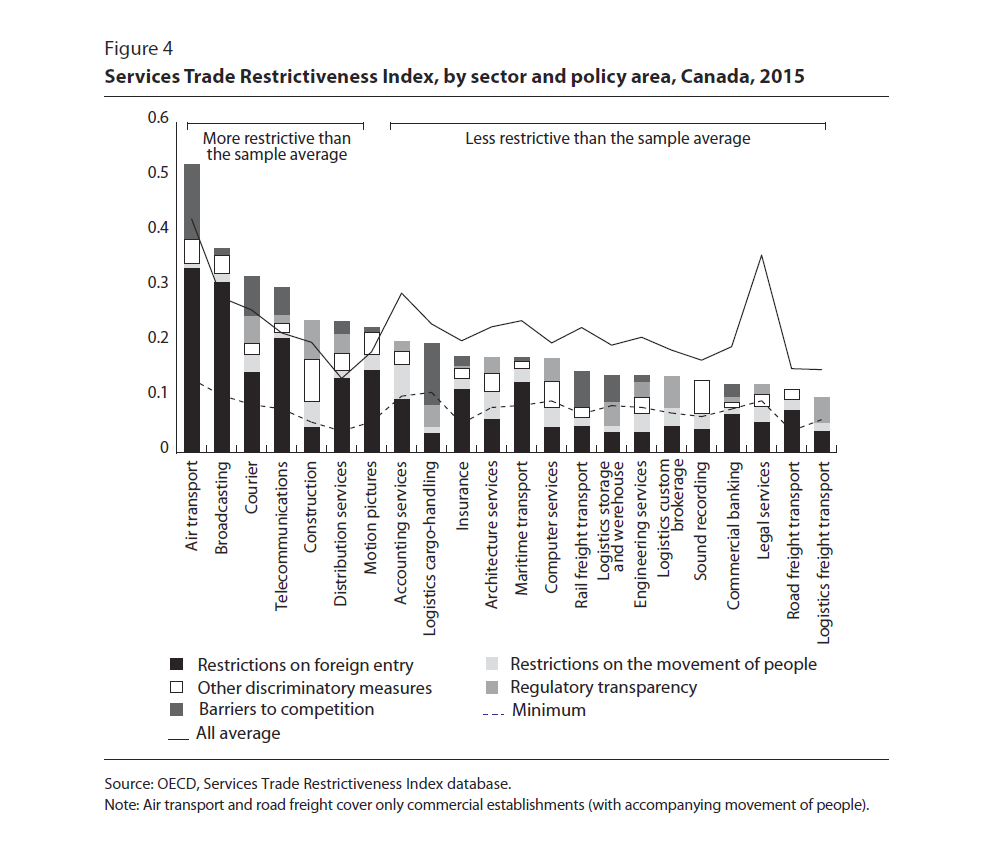

Within countries, the restrictiveness of services trade varies significantly by sector. Canada’s STRI score is lower — that is, less restrictive — than the averages in the 42 countries in the database in 15 out of 22 services sectors (see figure 4). Most of Canada’s reported barriers deal with foreign entry and the treatment of foreign investment. In all sectors of the economy, at least 25 percent of the board members of corporations must be Canadian residents or citizens. In addition, in sectors to which the Investment Canada Act applies, investments are subject to screening — whereby foreign investors acquiring Canadian businesses that are valued above established thresholds must show likely net benefits to Canada. Higher levels of restrictiveness are found in sectors where the investment regime is less trade friendly. For instance, air transport is Canada’s most restricted sector, mostly due to the foreign investment regime, which restricts foreign equity control to less than 25 percent of voting shares for airlines operating in domestic and international airways.

The STRI database also records restrictions on the movement of people. Canada maintains labour market tests for contractual services providers and independent services suppliers. Compared with other countries, however, Canada has a rather open trade regime for foreign professionals — particularly in legal and engineering services, where there are no nationality or residency requirements and where a transparent and competency-based system is in place to recognize equivalent education degrees. Canada also scores as comparatively less restrictive in accounting.

Canada generally does not impose discriminatory taxes and subsidies, so there are fewer measures reported in the “other discriminatory measures” category. Examples are found in audio-visual sector, where discriminatory subsidies and tax breaks apply that are subject to cultural tests.4 Canada’s services regulations generally allow for competition, so the country also has low scores in the “barriers to competition” category, with exceptions in sectors with at least one major state-owned enterprise, such as air and rail transport, broadcasting, and postal and courier services. Finally, since its regulations are generally transparent and grant due process to foreign providers — through, for example, appeal procedures — Canada also scores well in the policy area of regulatory transparency.

The prevalence of barriers to trade in services related to investment is a concern, considering the key role investment plays in Canada’s job creation and economic growth and the fact that almost half of its inward FDI is in services, with the potential for positive spillovers from such trade flows (Havranek and Irsova 2011).

While Canada performs relatively well in regulated industries and has few barriers to competition compared to other countries, it is important to continue adjusting services regulations to reflect the evolving business environment. Telecoms and distribution services, in particular, are at the forefront of new technological advancements and these sectors are where Canada performs less well.

Compared with its largest trading partner, the United States, Canada scores as slightly more restrictive overall in services trade. This is particularly true in motion pictures and broadcasting, telecoms and wholesale and retail trade. Alternatively, Canada is less restrictive than the United States in sectors such as engineering, insurance, maritime transportation and the logistics subsectors. Within the European Union, restrictiveness varies considerably, with some members, such as the Netherlands and Ireland, among the least trade restrictive and others, such as Poland and Austria, among the most restrictive. On average, Canada is more restrictive than EU countries in sectors such as broadcasting, telecoms, courier services, and wholesale and retail trade. Canada is, however, significantly less restrictive than the average EU economy in professional services — particularly, as noted, legal and engineering services. The values for Canada and the EU as a whole are close for financial and transport services — but again the average for the EU hides the heterogeneity of EU services markets when it comes to the treatment of non-EU companies.

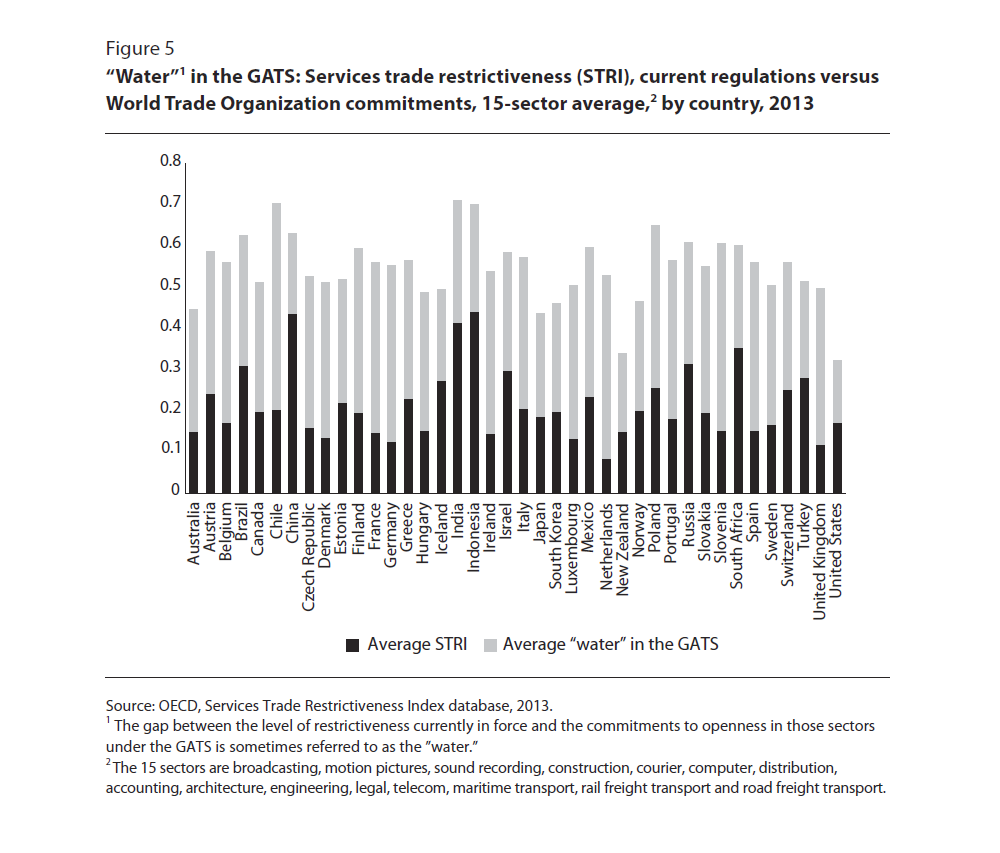

A comprehensive knowledge of the regulations that affect trade in services can help to better understand trade negotiations that are underway and the opportunities for further liberalization. Most trade agreements, starting with the WTO General Agreement on Trade in Services (GATS), include guarantees that there will be no change in the trade regime for foreign services suppliers. Indeed, countries typically now have significantly less restrictive services trade policies than are required by their GATS commitments. (This is expected since over two decades have passed since 1995, when these commitments came into force for many countries in the database.)

Figure 5 shows the difference between the level of restrictiveness according to laws and regulations currently in force (as estimated by the STRI) in 15 sectors and commitments to openness in those sectors under the GATS. This gap is sometimes referred to as the “water” in the GATS. For each bar in figure 5, the lower part shows the average STRIs (for 15 sectors in each country based on the indices released in 2013), while the top part accounts for the “water” in the GATS (the difference with the full bar that measures the average restrictiveness of the same 15 sectors when the STRIs are calculated according to the GATS schedules). The figure shows that simply committing to the openness already in place in services trade, without any further reforms, would considerably increase certainty in the business environment for services on the part of both suppliers and customers.

Figure 5 does not show, however, the extent to which the “water” in the GATS has already been reduced through regional trade agreements not covered in the STRI. Canada, in particular, has a high share of its bilateral trade within the North American Free Trade Agreement, which includes extensive services commitments (Miroudot, Sauvage and Sudreau 2010). The recently signed Comprehensive Economic Trade Agreement between Canada and the European Union also includes such commitments, particularly in financial services, telecommunications and maritime transport. Such agreements, however, generally do not modify the applied services trade regime, as compiled by the STRI. The Trans-Pacific Partnership includes very limited actual liberalization in services trade (Ciuirak, Dadkhah and Xiao 2016): Canada has pledged to create a less restrictive trade regime for commercial banking and insurance services; in return, it gets more open markets for insurance services in Australia and the United States and for commercial banking in New Zealand, but the agreement only binds the existing regime when it comes to Japan.

At the same time, research suggests that trade costs for services providers do not differ significantly in or outside a regional trade agreement (Miroudot and Shepherd 2014). Except for mechanisms such as the mutual recognition of qualifications, it is generally difficult to discriminate among partners when dealing with behind-the-border trade barriers. As a consequence, regional trade agreements generally have not until recently been preferential in the services sectors. So, although such agreements can bring benefits by locking in policy reforms, they are seldom the cause of reforms. This again suggests that services liberalization starts at home. There is no need to wait for progress in multilateral or regional trade negotiations to improve the efficiency of the services sectors. It would be better for Canada to reduce its services trade barriers itself and, in the process, promote growth by spurring trade in services and goods sectors and GVCs more broadly.

Of course, services trade barriers also reduce imports in the restricted sector, which shields some local services providers from competition, but these same restrictions, in turn, also significantly reduce local firms’ competitiveness in international markets. Research based on the STRI suggests that the effect of removing barriers to trade in services is twice as large for imports as for exports (Nordås and Rouzet 2015). One reason is that services trade barriers reduce competition in local markets, which weakens incentives for domestic firms to innovate and explore new foreign markets. In addition, barriers to imports create extra costs for exporters who rely on imported services inputs.

The emergence of global value chains, the increasing role of services as drivers of productivity and new evidence on services trade embodied in goods all put new emphasis on services policy reforms. Like all OECD countries, Canada maintains services sector restrictions that inhibit international trade, ranking around the middle of the pack. Overall, it tends to have a relatively lower level of restrictions in most sectors, particularly in legal, accounting and engineering services. Canada continues, however, to maintain significant barriers in air transportation, broadcasting, courier, telecom, construction, wholesale and retail trade and motion pictures. Canada could further enhance the efficiency of its economy by prioritizing reforms that increase competition in these services sectors, particularly those that are essential inputs for other industries.

Case studies highlight just how broad a range of service activities is needed to be globally competitive, with companies operating across borders needing access to between 40 and 50 different types of service inputs (Sweden 2012, 2013). Well-targeted reforms for essential inputs — including R&D, transport, logistics, finance, and information and communications technology support — would therefore have positive spillovers felt throughout the economy. Finally, Canada — and other countries — should commit itself in international agreements to the services trade openess already in practice, which is more liberal than are the GATS commitments. In this way, the legal regime for services trade would better reflect the actual trading regime.

Ciuriak, D., A. Dadkhah, and J. Xiao. 2016. “Taking the Measure of the TPP as Negotiated.” Working paper. Ottawa: Ciuriak Consulting.

Evans, P., and M. Annunziata. 2012. Industrial Internet: Pushing the Boundaries of Minds and Machines. General Electric. Accessed June 26, 2016. https://www.ge.com/docs/chapters/Industrial_Internet.pdf

Geloso Grosso, M., F. Gonzales, S. Miroudot, H. Nordås, D. Rouzet, and A. Ueno. 2015. “Services Trade Restrictiveness Index (STRI): Scoring and Weighting Methodology.” OECD Trade Policy Paper 177. Paris: OECD Publishing. Accessed June 26, 2016. https://dx.doi.org/10.1787/5js7n8wbtk9r-en

Havranek, T., and Z. Irsova. 2011. “Estimating Vertical Spillovers from FDI: Why Results Vary and What the True Effect Is.” Journal of International Economics 85 (2): 234-44.

Jones, R., and H. Kierzkowski. 2001. “A Framework for Fragmentation.” In Fragmentation: New Production Patterns in the World Economy, edited by S. Arndt and H. Kierzkowski. New York: Oxford University Press.

Miroudot, S., J. Sauvage, and M. Sudreau. 2010. “Multilateralising Regionalism: How Preferential Are Services Commitments in Regional Trade Agreements?” OECD Trade Policy Paper 106. Paris: OECD Publishing.

Miroudot, S., and B. Shepherd. 2014. “The Paradox of ‘Preferences’: Regional Trade Agreements and Trade Costs in Services.” World Economy 37 (12): 1751-72.

Nordås, H., and D. Rouzet. 2015. “The Impact of Services Trade Restrictiveness on Trade Flows: First Estimates.” OECD Trade Policy Paper 178. Paris: OECD Publishing. Accessed June 26, 2016. https://dx.doi.org/10.1787/5js6ds9b6kjb-en.

OECD (see Organisation for Economic Co-operation and Development)

———. 2014. Services Trade Restrictiveness Index: Policy Brief. Paris: OECD Publishing. Accessed June 26, 2016. https://www.oecd.org/tad/services-trade/STRI%20Policy%20Brief_ENG.pdf

———. 2015. Trade in Value Added: Canada. Paris: OECD Publishing. Accessed June 26, 2016. https://www.oecd.org/sti/ind/tiva/CN_2015_Canada.pdf

Sweden. 2012. National Board of Trade. Everybody Is in Services: The Impact of Servicification in Manufacturing on Trade and Trade Policy. Accessed June 26, 2016. https://www.kommers.se/Documents/In_English/Publications/PDF/Everybody-is-in-services.pdf

———. 2013. Just Add Services: A Case Study on Servicification and the Agri-Food Sector. Accessed June 26, 2016. https://www.kommers.se/Documents/In_English/Publications/PDF/Just-Add-Services.pdf